Chapter Thirty-Six

Shared Services and Cost Pooling Arrangements in the United States and Singapore

Governments Are increasing the requirements they impose on multinational taxpayers as to the allocation of services, whether these services take place inside or outside the specific governmental jurisdiction. As a result, a multinational taxpayer, on a practical basis, may need to address the treatment of a myriad number of its service costs to fulfill the compliance objectives that tax collectors impose. The taxpayer might face an uncertain future when it comes to the allocation of services costs and its need to develop complex calculations to fulfill government objectives.

Without more, such a multinational taxpayer faces the need to apply various service cost methodologies, making that determination in a plethora of circumstances. Both the Internal Revenue Service (IRS) in the United States and the Inland Revenue Authority of Singapore (IRAS) in Singapore have begun to address these transfer pricing services issues. The IRS, in recognizing these transfer pricing services concerns, permits taxpayers to set up and utilize shared services arrangements. However, as we shall see, the IRS then curtails the shared services arrangement (SSA) process, limiting the salutary benefits the SSA provides. In contrast, the Singapore provisions do not impose these cost pooling limitations.

This analysis addresses the SSA process in the United States and the cost pooling process in Singapore in regard to transfer pricing services provisions.1

HISTORICAL BACKGROUND

The transfer pricing services regulations have evolved over a more than 40-year period in the United States. The Treasury Department and the IRS:

- Initially issued transfer pricing services regulations on August 16, 1968.2

- Then issued proposed transfer pricing services regulations on September 10, 2003.3

- Later issued temporary transfer pricing services regulations on August 4, 2006.4

- Issued final transfer pricing services regulations on July 31, 2009.5

The shared services and cost pooling provisions in Singapore have their own history:

- The initial transfer pricing services regulations did not contain SSA provisions.

- The 2006 temporary transfer pricing services provisions provided for shared services arrangements.

- On February 23, 2009, the Government of Singapore adopted and modified the SSA provisions specified in the U.S. 2006 temporary transfer pricing provisions.

- The Treasury Department and the IRS adopted the SSA in issuing final transfer pricing services regulations on July 31, 2009.

- The Treasury Department and the IRS, in adopting the shared services arrangement, apparently did not take the Singapore provisions into account as reference.

EXPLANATION OF THE SHARED SERVICES ARRANGEMENT PROVISIONS

The final SSA provisions address three issues raised in the temporary SSA provisions:

Tie-in to the Services Cost Method

The Explanation of the Provisions for T.D. 9456 categorize the SSAs as being a subset of the SCM,6 thus making the application of the other transfer pricing services methods problematic in the SSA context. It is our view as transfer pricing practitioners that the Treasury Department and the IRS necessarily narrowed the focus of the SSA provisions by this connection to the SCM. For example, the Singapore SSA has no parallel limitation that would tie transfer pricing services to methodologies selected.

As a general matter, commentators to what became the final transfer pricing services regulations supported the SSA provisions in the temporary regulations. The commentators viewed the SSA provisions as being a useful mechanism for allocation of costs from shared services or centralized services. However, commentators did call into question the SSA restriction to “covered services” priced under the SCM.

The limitation arises as to the requirement that service not be “eligible” for the shared service arrangement. In response to that commentary concerning shared services arrangements, the IRS issued Notice 2007-5, which provides that a taxpayer can use a services cost arrangement outside the SCM context. Notice 2007-5 specifically provides that the taxpayer “may also make allocations of arm’s length charges for services ineligible for the SCM that yield a benefit to multiple members of a controlled group.” In such a situation in which the SCM is not eligible, the Treasury Department and the IRS provide that the flexible SCM rules for establishing the joint benefits and selecting the allocation key are inapplicable.

The Treasury Department and the IRS would employ a “more robust” analysis under the transfer pricing rules “for determining the appropriate arm’s length charges, benefits, allocation keys, etc.” The Treasury Department and the IRS considered providing additional SSA rules to services priced under methods other than the SCM, but the Treasury Department and the IRS concluded that such rules would be unnecessary. In any event, as stated in Notice 2007-5, the Treasury Department and the IRS are intent on denying flexibility that they afforded in the SCM context in establishing the joint benefits, and selecting the allocation key that is inapplicable in the non-SCM context.

As transfer pricing practitioners, we suggest the Treasury Department and the IRS applied a more flexible standard in determining the applicability of shared services arrangements, recognizing that the taxpayer and the IRS might not be able to ascertain whether the SCM is the best transfer pricing method until after the taxpayer compiles the necessary data and allocation key. We further suggest that the SSA process should be a separate issue from the transfer pricing services selection process. In addition, we suggest the transfer pricing services provisions recognize that SCM ineligibility is an amorphous issue, and the taxpayer might not be able to make that determination as to eligibility at the time the taxpayer formally undertakes the section 1.482-9(b)(7)(ii)(C) SSA process.

Pursuit of Different Cost Objectives

Other commentators to what became the final transfer pricing services regulations requested that the IRS respect the SSA even if a party that reasonably anticipates its benefits makes a payment to its share under the SSA to the service provider pursuant to a different arrangement. T.D. 9456 provides an example under which a controlled service provider performs services to ten taxpayers that are members of the controlled group. Nine of the service recipients agree in a written contract to allocate the arm’s length charge based on a reasonable allocation basis. The tenth services recipient does not agree to these terms but instead pays for its share of the services pursuant to a separate agreement. The Treasury Department and the IRS refused to accept the validity of the SSA in such circumstances, concluding that it wants to reserve for itself the power to determine whether an agreement is an SSA based on a case-by-case determination based on facts and circumstances.

Applicable Shared Service Arrangement Standards

Other commentators to what became the final transfer pricing services regulations observed that the SSA provisions require the allocation of costs on the basis that “most reliably reflects” the participants’ respective shares of “reasonably anticipated” benefits. Some of the SSA examples use the phrase “precisely known.” Thus, there appears to be a disparity between the “reasonably anticipated” benefits and amounts that are “precisely known.” This disparity has caused some commentators to question whether the SSA rule creates an unattainable standard or whether the SSA rule imposes a higher standard than the reasonable standard for allocation of costs in Treasury Regulation section 1.482-9(k). These commentators suggested changes to these examples.

The Treasury Department and the IRS rejected the commentators’ approach to change these services cost standards. The Treasury Department and the IRS concluded that these examples do not create a standard based on “precisely known shares” of reasonably anticipated benefits. Rather, according to the Treasury Department and the IRS, the examples use hypothetical, precisely known reasonably anticipated benefits as a measuring stick to provide an easily understood comparative analysis of potential allocation keys for illustrative purposes.

SHARED SERVICES ARRANGEMENTS

Section 1.482-9(b)(7) addresses covered services that might be the subject of an SSA. In the event that covered services are subject to an SSA, sec.1.482-9(b)(7)(i) generally provides that the arm’s length charge to each participant for such services will be the portion of the total costs of the services otherwise determined under the SCM of this sec. 1.482-9(b)(7) that is properly allocated to such participant pursuant to the arrangement.

Section 1.482-9(b)(7)(ii) contains the requirements for an SSA. An SSA must meet three requirements described in sec. 1.482-9(b)(7):

Section 1.482-9(b)(7)(iii) provides for definitions and special rules as to shared services arrangements.

Eligibility Requirements

Section 1.482-9(b)(7)(ii)(A) provides, as to the eligibility requirements for an SSA, that the arrangement, to be eligible for treatment under this sec. 1.482-9(b)(7), must meet these eligibility requirements:

- The arrangement must include two or more participants, as specified by sec. 1.482-9(b)(7)(ii)(A)(1).

- The arrangement must include, as participants, all controlled taxpayers that “reasonably anticipate a benefit.” Section 1.482-9(l)(3)(i) defines “benefit” as from one or more covered services specified in the shared services arrangement, as specified by sec. 1.482-9(b)(7)(ii)(A)(2), that directly results in a “reasonably identifiable increment of economic or commercial value that enhances the recipient’s commercial position or that may reasonably be anticipated to do so.”

- The arrangement must be structured such that each covered service, or each reasonable aggregation of services within the meaning of sec. 1.482-9(b)(7)(iii)(B), confers a benefit on at least one participant in the SSA, as specified by sec. 1.482-9(b)(7)(ii)(A)(3).

The “reasonably anticipated benefits” rule applies in ascertaining shared services. Section 1.482-9(b)(7)(ii)(B) provides, as to the allocation requirement specified in sec. 1.482-9(b)(7)(iii)(B), that the participants must allocate costs for covered services among the participants based on their respective shares of the reasonably anticipated benefits from those services. The participants are to make this determination as to benefits without regard to whether the anticipated benefits are in fact realized. “Reasonably anticipated benefits” are “benefits” as defined in sec. 1.482-9T(l)(3)(i).

Allocation of Costs

Participants must allocate the costs that are applicable to the benefits they receive. The allocation of costs that the participants select must provide the most reliable measure of the participants’ respective shares of the reasonably anticipated benefits under the principles of the best method rule. See sec. 1.482-1(c) as to the definition of best method. The participant must apply the shares of the reasonably anticipated benefits allocation on a consistent basis for all participants and for all services.

The allocation to each participant in each taxable year must reasonably reflect that participant’s respective share of reasonably anticipated benefits for such taxable year. The Commissioner may not adjust such allocation basis if the taxpayer reasonably concluded that the SSA, including any aggregation pursuant to sec. 1.482-9(b)(7)(iii)(B), allocated costs for covered services on a basis that most reliably reflects the participants’ respective shares of the reasonably anticipated benefits attributable to such services, as provided for in sec. 1.482-9(b)(7). For allocation purposes, taxpayers need not prove to the IRS that its allocation is necessarily the best transfer pricing method, only that the taxpayer’s method is reasonable and the allocation method reliably reflects respective shares of the reasonably anticipated benefits attributable to such services.

Documentation

Section 1.482-9(b)(7)(ii)(C) provides, as to the documentation requirement within the shared services provisions, that the taxpayer must maintain sufficient documentation to establish that the taxpayer satisfies the requirements of sec. 1.482-9(b)(7). The taxpayer is to include six facets to demonstrate its documentation:

Section 1.482-9(b)(7)(iii) provides three definitions and special rules for SSAs:

- The aggregation takes place in a reasonable manner.

- The aggregation takes into account all the facts and circumstances.

- The facts and circumstances that take into account whether the relative magnitude of reasonably anticipated benefits of the participants that share the costs of such aggregated services are reasonably reflected by the allocation basis employed pursuant to sec. 1.482-9(b)(7)(ii)(B).

- The aggregation of services under an SSA may differ from the aggregation used to evaluate the median comparable markup for any low-margin covered services described in sec. 1.482-9(b)(3)(ii).

- However, a taxpayer seeking to aggregate services can do so provided that the taxpayer can implement such alternative aggregation on a reasonable basis, including appropriately identifying and isolating relevant costs, as necessary.

- A taxpayer can make an allocation to a participant in an SSA that is also a participant in a cost sharing arrangement subject to sec. 1.482-7T.

- The taxpayer can make this cost sharing arrangement allocation to the extent that such amount with respect to covered services is first allocated pursuant to the SSA under sec. 1.482-9(b)(7).

- Costs that a taxpayer allocates pursuant to an SSA may (if applicable) be further allocated between the intangible development activity under sec. 1.482-7T and other activities of the participant.

SERVICES COST METHOD EXAMPLES

The sec. 1.482-9(b)(8) regulations provide 24 examples that illustrate the SCM. The drafters do not intend an inference as to whether the presence or absence of one or more facts is determinative of the conclusion in any example. Note these factual parameters as to Examples 16 through 24: The fact patterns assume that Company P and its subsidiaries, Company X, Company Y, and Company Z, are corporations and members of the same group of controlled entities (PXYZ Group). The fact pattern assumes that Company P and its subsidiaries satisfy all of the requirements for an SSA as specified in sec. 1.482-9(b)(7)(ii) and sec. 1.482-9(b)(7)(iii).

Example 16. Shared Services Arrangement and Reliable Measure of Reasonably Anticipated Benefit (Allocation Key)

- Company P operates a centralized data processing facility that performs automated invoice processing activities and performs order generation for all of its subsidiaries.

- Company P’s subsidiaries are Companies X, Y, and Z.

- Company P undertakes an SSA with Companies X, Y, and Z.

- Company P is to evaluate the shares of reasonably anticipated benefits from the centralized data processing services as part of the SSA.

- The total value of the merchandise on the invoices and orders may not provide the most reliable measure of reasonably anticipated benefits shares in determining the reasonably anticipated benefits.

- The total value of the merchandise on the invoices and orders may not provide the most reliable measure of reasonably anticipated benefits shares because value of merchandise sold does not bear a relationship to the anticipated benefits from the underlying covered services.

- The total volume of orders and invoices processed may provide a more reliable basis for evaluating the shares of reasonably anticipated benefits from the data processing services.

- Alternatively, depending on the facts and circumstances, total central processing unit time attributable to the transactions of each subsidiary may provide a more reliable basis on which to evaluate the shares of reasonably anticipated benefits.

Example 17. Shared Services Arrangement and Reliable Measure of Reasonably Anticipated Benefit (Allocation Key)

- Company P operates a centralized center that performs human resources (HR) functions.

- Such HR functions include the administration of pension, retirement, and health insurance plans that are made available to employees of its subsidiaries, Companies X, Y, and Z.

- Companies P, X, Y, and Z allocate the cost of these HR functions pursuant to a shared services arrangement.

- In evaluating the shares of reasonably anticipated benefits from these centralized services, the total revenues of each subsidiary may not provide the most reliable measure of reasonably anticipated benefit shares.

- The total revenues of each subsidiary may not provide the most reliable measure of reasonably anticipated benefit shares because total revenues do not bear a relationship to the shares of reasonably anticipated benefits from the underlying services.

- Employee headcount or total compensation paid to employees may provide a more reliable basis for evaluating the shares of reasonably anticipated benefits from the covered services.

Example 18. Shared Services Arrangement and Reliable Measure of Reasonably Anticipated Benefit (Allocation Key)

- Company P performs HR services (service A) on behalf of the PXYZ Group.

- The PXYZ Group services qualify for the SCM.

- Under the SCM, Company P determines the amount charged for these HR services pursuant to a shared services arrangement.

- Company P applies the sec. 1.482-9(b)(7) SSA.

- Service A constitutes a specified covered service described in an unspecified revenue procedure pursuant to sec. 1.482-9(b)(3)(i).

- The total services costs for service A, as otherwise determined under the SCM, is 300.

- Companies X, Y, and Z reasonably anticipate benefits from service A.

- Company P does not reasonably anticipate benefits from service A.

- Assume that if relative reasonably anticipated benefits were precisely known, the appropriate allocation of charges pursuant to sec. 1.482-9T(k) to Company X, Y, and Z for service A is:

Service A Total cost 300, delineated as:

X 150 Y 75 Z 75 The total number of employees (employee headcount) in each company is:Company X 600 employees Company Y 250 employees Company Z 250 employees Company X, Y, Z total: 1,100 employees.Company P allocates the 300 total services costs of service A based on employee headcount, doing so as shown:Service A Total Cost Company (headcount) Allocation Key Amount X 600 164 Y 250 68 Z 250 68 Total 1,100 300 - Based on the preceding facts, Company P may reasonably conclude that the employee headcount allocation basis most reliably reflects the participants’ respective shares of the reasonably anticipated benefits attributable to service A.

Example 19. Shared Services Arrangement and Reliable Measure of Reasonably Anticipated Benefit (Allocation Key)

- Company P performs accounts payable services (service B) on behalf of the PXYZ Group.

- Company P determines the amount charged for the services under such method pursuant to an SSA based on an application of sec. 1.482-9(b)(7).

- Service B is a specified covered service described in a revenue procedure pursuant to sec. 1.482-9(b)(3)(i).

- The total services costs for service B otherwise determined under the SCM is 500.

- Companies X, Y, and Z reasonably anticipate benefits from service B.

- Company P does not reasonably anticipate benefits from service B.

- Assume that if relative reasonably anticipated benefits were precisely known, the appropriate allocation of charges pursuant to sec. 1.482-9(k) to Companies X, Y, and Z for service B is:

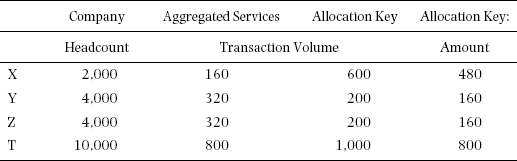

Service B Company Cost

X 125 Y 205 Z 170 Total 500 The total number of employees (employee headcount) in each company is:Company X 600 Company Y 200 Company Z 200 Total employees 1,000 The total number of transactions (transaction volume) with uncontrolled customers by each company is:Company X 12,000 Company Y 4,000 Company Z 3,500 Total volume of transactions (transactions volume) 19,500 If Company P allocated the 500 total services costs of service B based on employee headcount, the resulting allocation would be:Service B Total Cost Headcount Allocation Amount X 600 300 Y 200 100 Z 200 100 Total 1,000 500 In contrast, if Company P used volume of transactions with uncontrolled customers as the allocation basis under the SSA, the allocation would be:Transaction Volume Amount X 2,000 105 Y 4,000 211 Z 3,500 184 Total 9,500 500 Based on these facts, Company P may reasonably conclude that the transaction volume, but not the employee headcount, allocation basis most reliably reflects the participants’ respective shares of the reasonably anticipated benefits attributable to service B.

Example 20. Shared Services Arrangement and Aggregation

- Company P performs two services on behalf of PXYZ Group.

- Company P performs HR services (service A).

- Company P performs accounts payable services (service B).

- Company P applies the SCM to service A and to service B.

- Company P applies an SSA based on an application of sec. 1.482-9(b)(7), which determines the amount charged for these services.

- The example provides that service A and service B are specified covered services described in a revenue procedure.

- Rev. Proc. 2007-13 could determine the covered services pursuant to sec. 1.482-9(b)(3)(i).

- The PXYZ Group determines the total services costs under the SCM for service A is 300.

- The PXYZ Group determines the total services costs under the SCM for service B is 500.

- The PXYZ Group determines the total services costs under the SCM for service A and service B is 800.

- Company P determines that aggregation of services A and B for purposes of the arrangement is appropriate.

- Companies X, Y, and Z reasonably anticipate benefits from services A and B.

- Company P does not reasonably anticipate benefits from services A and B.

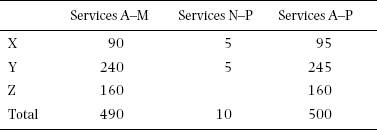

- Assume that if P precisely knew the relative reasonably anticipated benefits, the appropriate allocation of total charges pursuant to sec. 1.482-9(k) to Companies X, Y, and Z for services A and B is:

Services A and B X 350 Y 100 Z 350 Total Cost 800 The total volume of transactions with uncontrolled customers in each company is:Company X 2,000 Company Y 4,000 Company Z 4,000 Total employees 10,000 The total number of employees in each company is:Company X 600 Company Y 200 Company Z 200 Total employees 1,000 If Company P allocated the 800 total services costs of services A and B based on transaction volume or on employee headcount, the resulting allocation would be: In contrast, if P allocated the aggregated services AB by reference to the total U.S. dollar value of sales to uncontrolled parties (trade sales) by each company, these results would obtain:

In contrast, if P allocated the aggregated services AB by reference to the total U.S. dollar value of sales to uncontrolled parties (trade sales) by each company, these results would obtain:Aggregated Services AB Amount Allocation Key: Trade Sales X $400 million 314 Y $120 million 94 Z $500 million 392 Total $1,020 million 800 Based on these facts, Company P may reasonably conclude that the trade sales allocation basis, but not the transaction volume or the employee headcount, most reliably reflects the participants’ respective shares of the reasonably anticipated benefits attributable to services AB.

Example 21. Shared Services Arrangement and Aggregation

- Company P performs services A through P on behalf of the PXYZ Group that qualify for the SCM.

- Company P determines the amount charged for these services under such method pursuant to an SSA based on an application of sec. 1.482-9(b)(7).

- All of these services A through Z constitute either specified covered services or low-margin covered services described in sec. 1.482-9(b)(3).

- The total services costs for services A through Z otherwise determined under the SCM is 500.

- Company P determines that aggregation of services A through Z for purposes of the arrangement is appropriate.

- Companies X and Y reasonably anticipate benefits from services A through Z, and Company Z reasonably anticipates benefits from services A through X but not from services Y or Z.

- Company Z performs services similar to services Y and Z on its own behalf.

- Company P does not reasonably anticipate benefits from services A through Z.

- Assume that if relative reasonably anticipated benefits were precisely known, the appropriate allocation of total charges pursuant to sec. 1.482-9(k) to Company X, Y, and Z for services A through Z is:

The total volume of transactions with uncontrolled customers in each company is:

The total volume of transactions with uncontrolled customers in each company is:Company X 2,000 Company Y 4,500 Company Z 3,500 Total 10,000 Company P allocates the 500 total services costs of services A through Z based on transaction volume in this way:Aggregated Services A–Z Total Costs 500 Allocation Key: Transaction Volume X 2,000 100 Y 4,500 225 Z 3,500 175 Total 10,000 500 Based on these facts, Company P may reasonably conclude that the transaction volume allocation basis most reliably reflects the participants’ respective shares of the reasonably anticipated benefits attributable to services A through Z.

Example 22. Renderer Reasonably Anticipates Benefits

- Company P renders services on behalf of the PXYZ Group that qualify for the SCM.

- Company P determines the amount charged for these services under such method.

- Company P’s share of reasonably anticipated benefits from services A, B, C, and D is 20% of the total reasonably anticipated benefits of all participants.

- Company P’s total services cost for services A, B, C, and D charged within the group is 100.

- Based on an application of sec. 1.482-9(b)(7), Company P charges 80. P allocates this amount among Companies X, Y, and Z.

- No charge is made to Company P under the SSA for activities that it performs on its own behalf.

Example 23. Coordination with Cost Sharing Arrangement

- Company P performs HR services (service A) on behalf of the PXYZ Group.

- Such HR services qualify for the SCM.

- Company P determines the amount charged for these services under such method pursuant to an SSA based on an application of sec. 1.482-9(b)(7).

- Service A constitutes a specified covered service described in a revenue procedure pursuant to sec. 1.482-9(b)(3)(i).

- The total services costs for service A otherwise determined under the SCM is 300.

- Companies X, Y, Z, and P reasonably anticipate benefits from service A.

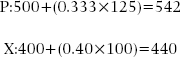

- Using a basis of allocation that is consistent with the controlled participants’ respective shares of the reasonably anticipated benefits from the shared services, the parties allocate the total charge of 300 as shown:

X 100 Y 50 Z 25 P 125 Total 300 - In addition to performing services, P undertakes 500 of research and development (R&D) and incurs manufacturing and other costs of 1,000.

- Companies P and X enter into a cost sharing arrangement in accordance with sec. 1.482-7.

- Company P will undertake all intangible development activities under the arrangement.

- Company P devotes all its R&D activity to the intangible development activity under the cost sharing arrangement.

- Company P will manufacture, market, and otherwise exploit the product in its defined territory.

- Companies P and X will share intangible development costs in accordance with their reasonably anticipated benefits from the intangibles.

- Company X will make payments to Company P as required under sec. 1.482-7T.

- Company X will manufacture, market, and otherwise exploit the product in the rest of the world.

- A portion of the charge under the SSA is in turn allocable to the intangible development activity undertaken by Company P.

- The most reliable estimate of the proportion allocable to the intangible development activity is determined to be 500 (Company P’s R&D expenses) divided by 1,500 (Company P’s total noncovered services costs), or one third.

- Accordingly, one third of Company P’s charge of 125, or 42, is allocated to the intangible development activity.

- Companies P and X must share the intangible development costs of the cost-shared intangibles (including the charge of 42 that is allocated under the SSA) in proportion to their respective shares of reasonably anticipated benefits under the cost sharing arrangement.

- That is, the reasonably anticipated benefit shares under the cost sharing arrangement are determined separately from reasonably anticipated benefit shares under the SSA.

Example 24. Coordination with Cost Sharing Arrangement

- The facts and analysis in Example 26 are the same as in Example 24, except that Company X also performs intangible development activities related to the cost sharing arrangement.

- Using a basis of allocation that is consistent with the controlled participants’ respective shares of the reasonably anticipated benefits from the shared services, the parties allocate 300 of service costs as shown:

X 100 Y 50 Z 25 P 125 Total 300 - In addition to performing services, Company P undertakes 500 of R&D.

- Company P incurs manufacturing and other costs of 1,000.

- Company X undertakes 400 of R&D and incurs manufacturing and other costs of 600.

- Companies P and X enter into a cost sharing arrangement in accordance with sec. 1.482-7T.

- Both Companies P and X will undertake intangible development activities under the cost sharing arrangement.

- Companies P and X devote all of the R&D activity to the intangible development activity under the cost sharing arrangement.

- Both Companies P and X will manufacture, market, and otherwise exploit the product in their respective territories.

- Both Companies P and X will share intangible development costs in accordance with their reasonably anticipated benefits from the intangibles.

- Both Companies P and X will make payments as required under sec. 1.482-7T.

- A portion of the charge under the SSA is in turn allocable to the intangible development activities undertaken by Companies P and X.

- The most reliable estimate of the portion allocable to Company P’s intangible development activity is determined to be 500 (Company P’s R&D expenses) divided by 1,500 (P’s total noncovered services costs), or one third.

- Accordingly, one third of Company P’s allocated SCM charge of 125, or 42, is allocated to its intangible development activity.

- In addition, it is necessary for the taxpayer to determine the portion of the charge under the SSA to Company X that should be further allocated to Company X’s intangible development activities under the cost sharing arrangement.

- The most reliable estimate of the portion allocable to Company X’s intangible development activity is 400 (Company X’s R&D expenses) divided by 1,000 (Company X’s costs), or 40%.

- Accordingly, 40% of the 100 that was allocated to Company X, or 40, is allocated in turn to Company X’s intangible development activities.

- Company X makes a payment to Company P of 100 under the shared services arrangement.

- Company X includes 40 of SCM charges in the pool of intangible development costs.

The parties’ respective contributions to intangible development costs under the cost sharing arrangement are:

SINGAPORE SHARED SERVICES ARRANGEMENTS

The IRAS issued Transfer Pricing Guidelines for Related Party Loans and Related Party Services on February 23, 2009. The IRAS employs the SSA process, referring to this process as “cost pooling.”7 Singapore taxpayers can apply this cost pooling technique to certain routine services expenditures that occur among related parties with the corporate group. Cost pooling arrangements differ in numerous respects from cost contribution arrangements (or cost sharing arrangements) that taxpayers enter into primarily to develop intangible assets. Regrettably, the Singapore services guidelines fail to distinguish between cost pooling arrangements and cost sharing arrangements.

Singapore taxpayers might find it mutually beneficial to enter into a cost pooling contract among members of the corporate group.8 The cost pooling contract enables members of the corporate group to share in the costs of routine support services for the common use of the group to meet a common need of the members. The cost pooling arrangement allows the members of the corporate group to pool resources together in order to acquire services that meet these parameters:

- A party to the cost pooling contract must have a reasonable expectation of benefiting from or actually benefit from the services for which costs are being shared.

- Contributions by related parties to the costs of providing the services must be made in proportion to the nature and extent of the expected benefits that each party receives.

- Each party’s share of the costs in the cost pooling arrangement must be borne in the form of cash or by other monetary contributions.

The proposed Singapore services guidelines provided that the arrangement must be necessary for the corporate group to function effectively. The final Singapore services guidelines eliminated this requirement.

Additional pooling requirements in Singapore are:9

- The arrangement is to acquire services that are not the principal activities of the corporate group.

- The arrangement is not intended to be a profitable exploit of the corporate group.

- The arrangement must address mutual benefit among members of the group.

- The party to the arrangement must reasonably expect to benefit from the shared services or actually benefit from the shared services.

- The party to the arrangement must determine the contribution as to the costs of providing the service in proportion to the expected benefits that each party receives.

- Each party must bear the share of its costs in the form of cash or other contributions, and nothing else.

- To satisfy the arm’s length principle, each participant’s share of the costs must be consistent with the costs to which an independent party would have agreed under comparable circumstances, given the benefit the participant would have expected to derive from the services being provided.

The Singapore services guidelines provide specific parameters for the allowance of the cost pooling arrangement:10

- The arrangement must be termed as a proportionate share of the cost of the services.

- The arrangement can be determined on a prospective basis.

- The arrangement is to be determined with no element of markup.

- The service provider that offers its services to its related parties does not offer these same services to unrelated parties.

- The service provided to the related parties does not reflect the principal activity that the service provider is to undertake. The term “principal activity” is based on facts and circumstances, based on a 15% threshold.

- These provisions apply to Annex A specified services in Singapore.

- The taxpayer provides sufficient documentation to show that the parties intended to pool their resources to share costs, doing so before the service provider performs the services.

The Singapore services guidelines require the taxpayer to maintain adequate documentation to support the cost allocation as being arm’s length. The services guidelines require the taxpayer to maintain adequate documentation to demonstrate the sharing of expected benefits arising from providing these services. The proposed services guidelines were concerned about the taxpayer’s risk of double taxation and suggested that the taxpayer retain the following documentation:11

- Description of the type of services provided

- Rationale for selecting a specific cost method

- Nature of the related parties’ contributions

- Anticipated benefits

- Calculation details

NOTES

1. R. Feinschreiber and M. Kent, “Singapore Issues Transfer Pricing Guidelines for Related-Party Loans and Services,” Corporate Business Taxation Monthly (June 2009): 41.

2. 33 FR 5849; see R. Feinschreiber, Paying for Intercompany Services, Prentice-Hall U.S. Taxation of International Operations Service, January 14, 1981.

3. 68 FR 53448.

4. 71 FR 44466.

5. T.D. 9456.

6. A.1.g.

7. IRAS, Transfer Pricing Guidelines for Related Party Loans and Related Party Services, 3.3.14.

8. IRAS, Transfer Pricing Guidelines for Related Party Loans and Related Party Services, 3.3.15.

9. IRAS Transfer Pricing Guidelines for Related Party Loans and Related Party Services, 3.3.16.

10. IRAS Transfer Pricing Guidelines for Related Party Loans and Related Party Services, 3.3.16.

11. IRAS Transfer Pricing Guidelines for Related Party Loans and Related Party Services, 3.3.16.