Conclusion: Think Globally, Act Locally

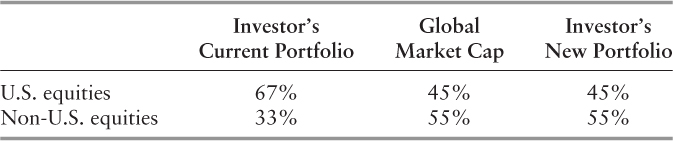

Thinking globally. Beginning the equity allocation process by looking at global equity market capitalization makes all the sense in the world (pun intended). Here is an exercise investors might try. Assume our investor has 35 percent of his entire portfolio in U.S. large-cap stocks, 5 percent in U.S. small-cap stocks, 15 percent in international stocks and 5 percent in emerging markets stocks. Of the 60 percent of the portfolio in equities, then, our investor has 40 percent (67 percent of the equity exposure) allocated to U.S. and 20 percent (33 percent) allocated to non-U.S., compared to a market weighting of (roughly) 45 percent U.S. and 55 percent non-U.S.:

| Investor's Portfolio | Global Market Cap (rounded) | |

| U.S. equities | 67 percent | 45 percent |

| Non-U.S. equities | 33 percent | 55 percent |

Now we might ask ourselves why we are so smart that we can make a huge, 22 percent bet against non-U.S. stocks? What is it we know that gives us confidence to make such a sizable bet? Would we do so elsewhere in our portfolio? If not, we should probably take steps to bring these two allocations closer together.

Acting globally. I have discussed above the challenges associated with using a global manager for our equity portfolio, but of course it's possible to do so, with these being the main choices:

My skepticism of global equity management notwithstanding, I see no reason why adventurous investors shouldn't dip their toes in the global equity market by engaging one of the managers described above. A global manager would therefore be managing money alongside more traditional domestic and foreign managers, and this in itself presents complications in terms of maintaining our asset allocation strategy and in judging relative performance. But it's not impossible, and may be worth the trouble just to gain experience with a global manager.

Most likely, the slowly increasing population of quality global equity managers will be used by sensible investors as satellite managers who provide useful manager diversification, given that they are working with a different opportunity set than pure domestic or pure non-U.S. managers.

Acting “locally.” By acting “locally” I mean implementing the globally designed portfolio in the traditional way: by engaging domestic and international specialist managers. Thus our globally designed, locally implemented portfolio might look something like this:

Long Equity Asset Allocation

Portfolio Implementation (Long Equities)

| Subtotal | Total | |

| (% of Equity Alloc) | (% of Equity Alloc) | |

| U.S. large-cap passive | 35% | |

| U.S. small-cap active value | 4% | |

| U.S. small-cap active growth | 6% | |

| U.S. total | 45% | |

| EAFE active value | 10% | |

| EAFE active growth | 10% | |

| Non-U.S. small-cap | 5% | |

| Emerging markets core | 20% | |

| EM Asia ex-Japan | 10% | |

| Non-U.S. total | 55% |

If you were to inject a global equity manager into the portfolio, you would likely take that manager's allocation out of the U.S. large-cap passive and EAFE active allocations, roughly equally.

Given the very fundamental changes in the economic organization of the world that followed the collapse of the Soviet Union, and how rapidly those changes have evolved over the ensuing two decades, I agree wholeheartedly that a conceptually global approach to equity investing makes sense. I have argued, however, that implementing a global approach using global equity managers remains problematic and it is likely to remain so for many years to come. “Think globally, act locally” is likely to be the preferred strategy for most U.S.-based and non-U.S. based investors.