CHAPTER 2

The Recording Process

FEATURE STORY Accidents Happen

How organized are you financially? Take a short quiz. Answer yes or no to each question:

- Does your wallet contain so many debit card receipts that you've been declared a walking fire hazard?

- Was Yao Ming playing high school basketball the last time you balanced your bank account?

- Do you wait until your debit card is denied before checking the status of your funds?

If you think it is hard to keep track of the many transactions that make up your life, imagine what it is like for a major corporation like Bank of Taiwan (BOT) (TWN). If you had your life savings invested at BOT, you might be just slightly displeased if, when you checked your balance online, a message appeared on the screen indicating that your account information was lost.

To ensure the accuracy of your balance and the security of your funds, BOT, like all other companies large and small, relies on a sophisticated accounting information system. That's not to say that BOT or any other company is error-free. In fact, if you'veever overdrawn your bank account because you failed to track your debit card purchases properly, you may take some comfort from one accountant's mistake at Fidelity Investments (USA), one of the largest mutual fund investment firms in the world. The accountant failed to include a minus sign while doing a calculation, making what was actually a $1.3 billion loss look like a $1.3 billion—yes, billion—gain! Fortunately, like most accounting errors, it was detected before any real harm was done.

No one expects that kind of mistake at a company like Fidelity, which has sophisticated computer systems and top investment managers. In explaining the mistake to shareholders, a spokesperson wrote, “Some people have asked how, in this age of technology, such a mistake could be made. While many of our processes are computerized, accounting systems are complex and dictate that some steps must be handled manually by our managers and accountants, and people can make mistakes.”

PREVIEW OF CHAPTER 2

In Chapter 1, we analyzed business transactions in terms of the accounting equation. We then presented the cumulative effects of these transactions in tabular form. Imagine a company like Bank of Taiwan (BOT) (as in the Feature Story) using the same tabular format as Softbyte SA to keep track of its transactions. In a single day, BOT engages in thousands of business transactions. To record each transaction this way would be impractical, expensive, and unnecessary. Instead, companies use a set of procedures and records to keep track of transaction data more easily. This chapter introduces and illustrates these basic procedures and records.

The content and organization of Chapter 2 are as follows.

The Account

Learning Objective 1

Explain what an account is and how it helps in the recording process.

An account is an individual accounting record of increases and decreases in a specific asset, liability, or equity item. For example, Softbyte SA (the company discussed in Chapter 1) would have separate accounts for Cash, Accounts Receivable, Accounts Payable, Service Revenue, Salaries and Wages Expense, and so on. (Note that whenever we are referring to a specific account, we capitalize the name.)

In its simplest form, an account consists of three parts: (1) a title, (2) a left or debit side, and (3) a right or credit side. Because the format of an account resembles the letter T, we refer to it as a T-account. Illustration 2-1 shows the basic form of an account.

Illustration 2-1 Basic form of account

We use this form often throughout this textbook to explain basic accounting relationships.

Debits and Credits

The term debit indicates the left side of an account, and credit indicates the right side. They are commonly abbreviated as Dr. for debit and Cr. for credit. They do not mean increase or decrease, as is commonly thought. We use the terms debit and credit repeatedly in the recording process to describe where entries are made in accounts. For example, the act of entering an amount on the left side of an account is called debiting the account. Making an entry on the right side is crediting the account.

Learning Objective 2

Define debits and credits and explain their use in recording business transactions.

When comparing the totals of the two sides, an account shows a debit balance if the total of the debit amounts exceeds the credits. An account shows a credit balance if the credit amounts exceed the debits. Note the position of the debit side and credit side in Illustration 2-1 .

The procedure of recording debits and credits in an account is shown in Illustration 2-2 for the transactions affecting the Cash account of Softbyte SA. The data are taken from the Cash column of the tabular summary in Illustration 1-10 (page 21).

Illustration 2-2 Tabular summary and account form for Softbyte's Cash account

Every positive item in the tabular summary represents a receipt of cash; every negative amount represents a payment of cash. Notice that in the account form we record the increases in cash as debits, and the decreases in cash as credits. For example, the €15,000 receipt of cash (in red) is debited to Cash, and the payment of cash (in blue) is credited to Cash.

Having increases on one side and decreases on the other reduces recording errors and helps in determining the totals of each side of the account as well as the account balance. The balance is determined by netting the two sides (subtracting one amount from the other). The account balance, a debit of €8,050, indicates that Softbyte had €8,050 more increases than decreases in cash. That is, since it started with a balance of zero, it has €8,050 in its Cash account.

DEBIT AND CREDIT PROCEDURE

In Chapter 1, you learned the effect of a transaction on the basic accounting equation. Remember that each transaction must affect two or more accounts to keep the basic accounting equation in balance. In other words, for each transaction, debits must equal credits. The equality of debits and credits provides the basis for the double-entry system of recording transactions.

Under the double-entry system, the dual (two-sided) effect of each transaction is recorded in appropriate accounts. This system provides a logical method for recording transactions. As discussed in the Feature Story about Bank of Taiwan (TWN), the double-entry system also helps to ensure the accuracy of the recorded amounts as well as the detection of errors. If every transaction is recorded with equal debits and credits, the sum of all the debits to the accounts must equal the sum of all the credits.

The double-entry system for determining the equality of the accounting equation is much more efficient than the plus/minus procedure used in Chapter 1. On the following pages, we will illustrate debit and credit procedures in the double-entry system.

DR./CR. PROCEDURES FOR ASSETS AND LIABILITIES

In Illustration 2-2 for Softbyte SA increases in Cash—an asset—were entered on the left side, and decreases in Cash were entered on the right side. We know that both sides of the basic equation must be equal. It therefore follows that increases and decreases in liabilities will have to be recorded opposite from increases and decreases in assets. Thus, increases in liabilities must be entered on the right or credit side, and decreases in liabilities must be entered on the left or debit side. The effects that debits and credits have on assets and liabilities are summarized in Illustration 2-3 .

Illustration 2-3 Debit and credit effects—assets and liabilities

Asset accounts normally show debit balances. That is, debits to a specific asset account should exceed credits to that account. Likewise, liability accounts normally show credit balances. That is, credits to a liability account should exceed debits to that account. The normal balance of an account is on the side where an increase in the account is recorded. Illustration 2-4 shows the normal balances for assets and liabilities.

Illustration 2-4 Normal balances—assets and liabilities

Knowing the normal balance in an account may help you trace errors. For example, a credit balance in an asset account such as Land or a debit balance in a liability account such as Salaries and Wages Payable usually indicates an error. Occasionally, though, an abnormal balance may be correct. The Cash account, for example, will have a credit balance when a company has overdrawn its bank balance (i.e., written a check that “bounced”).

EQUITY

As Chapter 1 indicated, there are five subdivisions of equity: share capital—ordinary, retained earnings, dividends, revenues, and expenses. In a double-entry system, companies keep accounts for each of these subdivisions, as explained below.

SHARE CAPITAL—ORDINARY Companies issue share capital—ordinary in exchange for the owners' investment paid in to the company. Credits increase the Share Capital—Ordinary account, and debits decrease it. For example, when an owner invests cash in the business in exchange for ordinary shares, the company debits (increases) Cash and credits (increases) Share Capital—Ordinary.

Illustration 2-5 shows the rules of debit and credit for the Share Capital–Ordinary account.

Illustration 2-5 Debit and credit effects—share capital—ordinary

We can diagram the normal balance in Share Capital—Ordinary as follows.

Illustration 2-6 Normal balance—share capital—ordinary

• HELPFUL HINT The rules for debit and credit and the normal balances of share capital—ordinary and retained earnings are the same as for liabilities.

RETAINED EARNINGS Retained earnings is net income that is kept (retained) in the business. It represents the portion of equity that the company has accumulated through the profitable operation of the business. Credits (net income) increase the Retained Earnings account, and debits (dividends or net losses) decrease it, as Illustration 2-7 shows.

Illustration 2-7 Debit and credit effects and normal balance—retained earnings

DIVIDENDS A dividend is a company's distribution to its shareholders. The most common form of a distribution is a cash dividend. Dividends reduce the shareholders' claims on retained earnings. Debits increase the Dividends account, and credits decrease it. Illustration 2-8 shows that this account normally has a debit balance.

Illustration 2-8 Debit and credit effect and normal balance—dividends

REVENUES AND EXPENSES

• HELPFUL HINT Because revenues increase equity, a revenue account has the same debit/credit rules as the Retained Earnings account. Expenses have the opposite effect.

The purpose of earning revenues is to benefit the shareholders of the business. When a company recognizes revenues, equity increases. Revenues are a subdivision of equity that provides information as to why equity increased. Credits increase revenue accounts and debits decrease them. Therefore, the effect of debits and credits on revenue accounts is the same as their effect on equity.

Expenses have the opposite effect: expenses decrease equity. Since expenses decrease net income, and revenues increase it, it is logical that the increase and decrease sides of expense accounts should be the reverse of revenue accounts. Thus, debits increase expense accounts, and credits decrease them.

Illustration 2-9 shows the effect of debits and credits on revenues and expenses.

Illustration 2-9 Debit and credit effects—revenues and expenses

Credits to revenue accounts should exceed debits. Debits to expense accounts should exceed credits. Thus, revenue accounts normally show credit balances, and expense accounts normally show debit balances. We can diagram the normal balance as follows.

Illustration 2-10 Normal balances—revenues and expenses

Equity Relationships

As Chapter 1 indicated, companies report share capital—ordinary and retained earnings in the equity section of the statement of financial position. They report dividends on the retained earnings statement. And they report revenues and expenses on the income statement. Dividends, revenues, and expenses are eventually transferred to retained earnings at the end of the period. As a result, a change in any one of these three items affects equity. Illustration 2-11 shows the relationships related to equity.

Illustration 2-11 Equity relationships

Summary of Debit/Credit Rules

Illustration 2-12 shows a summary of the debit/credit rules and effects on each type of account. Study this diagram carefully. It will help you understand the fundamentals of the double-entry system.

Illustration 2-12 Summary of debit/credit rules

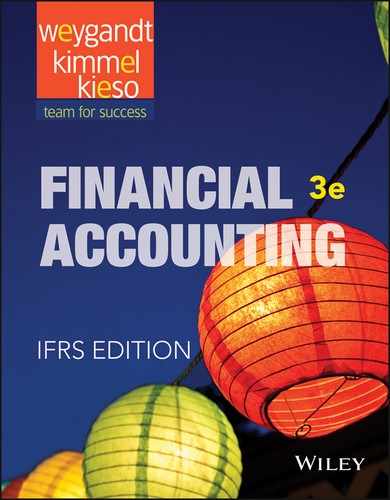

Steps in the Recording Process

Learning Objective 3

Identify the basic steps in the recording process.

Although it is possible to enter transaction information directly into the accounts without using a journal, few businesses do so. Practically every business uses three basic steps in the recording process:

- Analyze each transaction for its effects on the accounts.

- Enter the transaction information in a journal.

- Transfer the journal information to the appropriate accounts in the ledger.1

The recording process begins with the transaction. Business documents, such as a sales receipt, a check, or a bill, provide evidence of the transaction. The company analyzes this evidence to determine the transaction's effects on specific accounts. The company then enters the transaction in the journal. Finally, it transfers the journal entry to the designated accounts in the ledger. Illustration 2-13 shows the recording process.

Illustration 2-13 The recording process

The steps in the recording process occur repeatedly. In Chapter 1, we illustrated the first step, the analysis of transactions, and will give further examples in this and later chapters. The other two steps in the recording process are explained in the next sections.

The Journal

Learning Objective 4

Explain what a journal is and how it helps in the recording process.

Companies initially record transactions in chronological order (the order in which they occur). Thus, the journal is referred to as the book of original entry. For each transaction, the journal shows the debit and credit effects on specific accounts.

Companies may use various kinds of journals, but every company has the most basic form of journal, a general journal. Typically, a general journal has spaces for dates, account titles and explanations, references, and two amount columns. (See the format of the journal in Illustration 2-14 , below.) Whenever we use the term “journal” in this textbook, we mean the general journal, unless we specify otherwise.

The journal makes several significant contributions to the recording process:

- It discloses in one place the complete effects of a transaction.

- It provides a chronological record of transactions.

- It helps to prevent or locate errors because the debit and credit amounts for each entry can be easily compared.

JOURNALIZING

Entering transaction data in the journal is known as journalizing. Companies make separate journal entries for each transaction. A complete entry consists of: (1) the date of the transaction, (2) the accounts and amounts to be debited and credited, and (3) a brief explanation of the transaction.

Illustration 2-14 shows the technique of journalizing, using the first two transactions of Softbyte SA. On September 1, shareholders invested €15,000 cash in the corporation in exchange for ordinary shares, and Softbyte purchased computer equipment for €7,000 cash. The number J1 indicates that the company records these two entries on the first page of the general journal. (The boxed numbers correspond to explanations in the list below the illustration.)

Illustration 2-14 Technique of journalizing

- The date of the transaction is entered in the Date column.

- The debit account title (that is, the account to be debited) is entered first at the extreme left margin of the column headed “Account Titles and Explanation,” and the amount of the debit is recorded in the Debit column.

- The credit account title (that is, the account to be credited) is indented and entered on the next line in the column headed “Account Titles and Explanation,” and the amount of the credit is recorded in the Credit column.

- A brief explanation of the transaction appears on the line below the credit account title. A space is left between journal entries. The blank space separates individual journal entries and makes the entire journal easier to read.

- The column titled Ref. (which stands for Reference) is left blank when the journal entry is made. This column is used later when the journal entries are transferred to the ledger accounts.

It is important to use correct and specific account titles in journalizing. Erroneous account titles lead to incorrect financial statements. However, some flexibility exists initially in selecting account titles. The main criterion is that each title must appropriately describe the content of the account. Once a company chooses the specific title to use, it should record under that account title all later transactions involving the account.2

SIMPLE AND COMPOUND ENTRIES

Some entries involve only two accounts, one debit and one credit. (See, for example, the entries in Illustration 2-14 .) An entry like these is considered a simple entry. Some transactions, however, require more than two accounts in journalizing. An entry that requires three or more accounts is a compound entry. To illustrate, assume that on July 1, Tsai Company purchases a delivery truck costing NT$420,000. It pays NT$240,000 cash now and agrees to pay the remaining NT$180,000 on account (to be paid later). The compound entry is as follows.

Illustration 2-15 Compound journal entry

In a compound entry, the standard format requires that all debits be listed before the credits.

The Ledger

The entire group of accounts maintained by a company is the ledger. The ledger keeps in one place all the information about changes in specific account balances.

Learning Objective 5

Explain what a ledger is and how it helps in the recording process.

Companies may use various kinds of ledgers, but every company has a general ledger. A general ledger contains all the asset, liability, and equity accounts, as shown in Illustration 2-16 . Whenever we use the term “ledger” in this textbook, we mean the general ledger, unless we specify otherwise.

Illustration 2-16 The general ledger

The ledger provides the balance in each of the accounts and keeps track of changes in these balances. For example, the Cash account shows the amount of cash available to meet current obligations. The Accounts Receivable account shows amounts due from customers. The Accounts Payable account shows amounts owed to creditors. Each account is numbered for easier identification.

STANDARD FORM OF ACCOUNT

The simple T-account form used in accounting textbooks is often very useful for illustration purposes. However, in practice, the account forms used in ledgers are much more structured. Illustration 2-17 shows a typical form, using assumed data from a cash account.

This is called the three-column form of account. It has three money columns—debit, credit, and balance. The balance in the account is determined after each transaction. Companies use the explanation space and reference columns to provide special information about the transaction.

Illustration 2-17 Three-column form of account

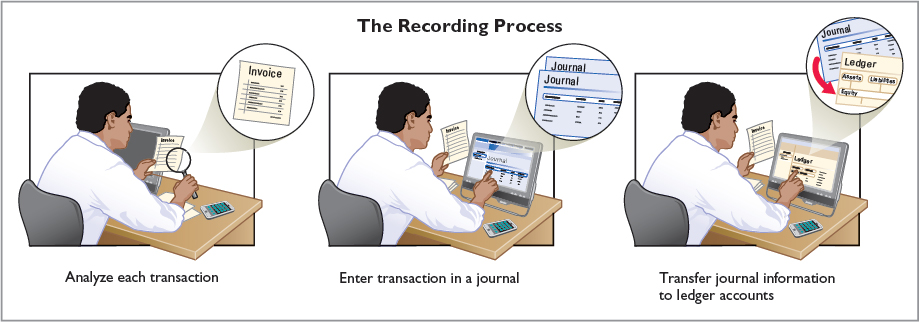

Posting

Learning Objective 6

Explain what posting is and how it helps in the recording process.

Transferring journal entries to the ledger accounts is called posting. This phase of the recording process accumulates the effects of journalized transactions into the individual accounts. Posting involves the following steps.

- In the ledger, enter, in the appropriate columns of the account(s) debited, the date, journal page, and debit amount shown in the journal.

- In the reference column of the journal, write the account number to which the debit amount was posted.

- In the ledger, enter, in the appropriate columns of the account(s) credited, the date, journal page, and credit amount shown in the journal.

- In the reference column of the journal, write the account number to which the credit amount was posted.

Illustration 2-18 shows these four steps using Softbyte SA's first journal entry, the issuance of ordinary shares for €15,000 cash. The boxed numbers indicate the sequence of the steps.

Illustration 2-18 Posting a journal entry

Posting should be performed in chronological order. That is, the company should post all the debits and credits of one journal entry before proceeding to the next journal entry. Postings should be made on a timely basis to ensure that the ledger is up to date.3

The reference column of a ledger account indicates the journal page from which the transaction was posted.4 The explanation space of the ledger account is used infrequently because an explanation already appears in the journal.

CHART OF ACCOUNTS

The number and type of accounts differ for each company. The number of accounts depends on the amount of detail management desires. For example, the management of one company may want a single account for all types of utility expense. Another may keep separate expense accounts for each type of utility, such as gas, electricity, and water. Similarly, a small company like Softbyte SA will have fewer accounts than a corporate giant like Anheuser-Busch InBev (BEL). Softbyte may be able to manage and report its activities in 20 to 30 accounts, while Anheuser-Busch InBev may require thousands of accounts to keep track of its worldwide activities.

• HELPFUL HINT On the textbook's endpapers, you will also find an expanded chart of accounts.

Most companies have a chart of accounts. This chart lists the accounts and the account numbers that identify their location in the ledger. The numbering system that identifies the accounts usually starts with the statement of financial position accounts and follows with the income statement accounts.

In this and the next two chapters, we will be explaining the accounting for Yazici Advertising A.Ş. (a service company). The ranges of the account numbers are as follows.

- Accounts 101–199 indicate asset accounts

- 200–299 indicate liabilities

- 300–399 indicate equity accounts

- 400–499, revenues

- 500–799, expenses

- 800–899, other revenues

- 900–999, other expenses

Illustration 2-19 shows the chart of accounts for Yazici Advertising A.Ş. Accounts shown in red are used in this chapter. Accounts shown in black are explained in later chapters.

Illustration 2-19 Chart of accounts for Yazici Advertising A.Ş.

You will notice that there are gaps in the numbering system of the chart of accounts for Yazici Advertising A.Ş. Gaps are left to permit the insertion of new accounts as needed during the life of the business.

The Recording Process Illustrated

Illustrations 2-20 through 2-29 show the basic steps in the recording process, using the October transactions of Yazici Advertising A.Ş. Yazici's accounting period is a month. A basic analysis and a debit-credit analysis precede the journalizing and posting of each transaction. For simplicity, we use the T-account form in the illustrations instead of the standard account form.

Study these transaction analyses carefully. The purpose of transaction analysis is first to identify the type of account involved, and then to determine whether to make a debit or a credit to the account. You should always perform this type of analysis before preparing a journal entry. Doing so will help you understand the journal entries discussed in this chapter as well as more complex journal entries in later chapters.

Illustration 2-20 Investment of cash by shareholders

• HELPFUL HINT Follow these steps:

- Determine what type of account is involved.

- Determine what items increased or decreased and by how much.

- Translate the increases and decreases into debits and credits.

Illustration 2-21 Purchase of office equipment

Illustration 2-22 Receipt of cash for future service

Illustration 2-23 Payment of monthly rent

Illustration 2-24 Payment for insurance

Illustration 2-25 Purchase of supplies on credit

Illustration 2-26 Hiring of employees

Illustration 2-27 Declaration and payment of dividend

Illustration 2-28 Payment of salaries

Illustration 2-29 Receipt of cash for services provided

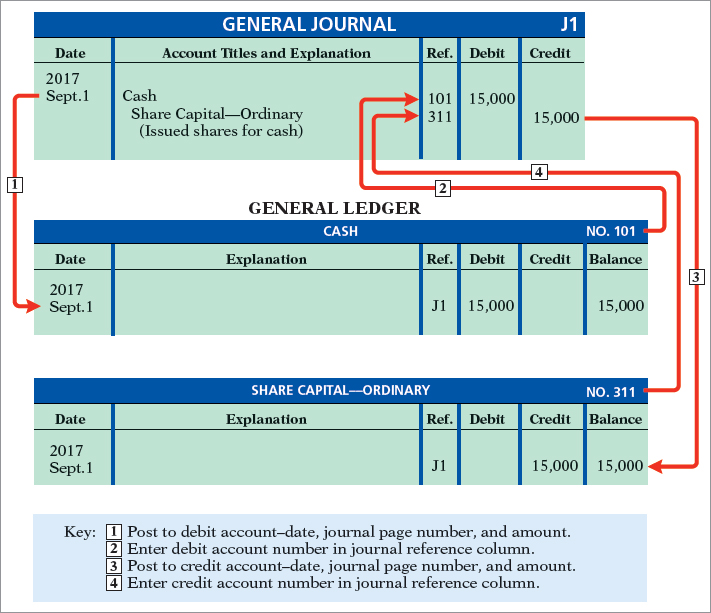

Summary Illustration of Journalizing and Posting

Illustration 2-30 shows the journal for Yazici Advertising A.Ş. for October. Illustration 2-31 (page 72) shows the ledger, with all balances in red.

Illustration 2-30 General journal entries

Illustration 2-31 General ledger

The Trial Balance

Learning Objective 7

Prepare a trial balance and explain its purposes.

A trial balance is a list of accounts and their balances at a given time. Customarily, companies prepare a trial balance at the end of an accounting period. They list accounts in the order in which they appear in the ledger. Debit balances appear in the left column and credit balances in the right column.

The trial balance proves the mathematical equality of debits and credits after posting. Under the double-entry system, this equality occurs when the sum of the debit account balances equals the sum of the credit account balances. A trial balance may also uncover errors in journalizing and posting. For example, a trial balance may well have detected the error at Fidelity Investments discussed in the Feature Story. In addition, a trial balance is useful in the preparation of financial statements, as we will explain in the next two chapters.

The steps for preparing a trial balance are:

- List the account titles and their balances.

- Total the debit and credit columns.

- Prove the equality of the two columns.

Illustration 2-32 shows the trial balance prepared from Yazici Advertising's ledger. Note that the total debits (![]() 28,700) equal the total credits (

28,700) equal the total credits (![]() 28,700).

28,700).

• HELPFUL HINT To sum a column of figures is sometimes referred to as to foot the column. The column is then said to be footed.

Illustration 2-32 A trial balance

A trial balance is a necessary checkpoint for uncovering certain types of errors. For example, if only the debit portion of a journal entry has been posted, the trial balance would bring this error to light.

• HELPFUL HINT A trial balance is so named because it is a test to see if the sum of the debit balances equals the sum of the credit balances.

Limitations of a Trial Balance

A trial balance does not guarantee freedom from recording errors, however. Numerous errors may exist even though the totals of the trial balance columns agree. For example, the trial balance may balance even when (1) a transaction is not journalized, (2) a correct journal entry is not posted, (3) a journal entry is posted twice, (4) incorrect accounts are used in journalizing or posting, or (5) offsetting errors are made in recording the amount of a transaction. As long as equal debits and credits are posted, even to the wrong account or in the wrong amount, the total debits will equal the total credits. The trial balance does not prove that the company has recorded all transactions or that the ledger is correct.

Locating Errors

Errors in a trial balance generally result from mathematical mistakes, incorrect postings, or simply transcribing data incorrectly. What do you do if you are faced with a trial balance that does not balance? First, determine the amount of the difference between the two columns of the trial balance. After this amount is known, the following steps are often helpful:

- If the error is $1, $10, $100, or $1,000, re-add the trial balance columns and recompute the account balances.

- If the error is divisible by 2, scan the trial balance to see whether a balance equal to half the error has been entered in the wrong column.

- If the error is divisible by 9, retrace the account balances on the trial balance to see whether they are incorrectly copied from the ledger. For example, if a balance was $12 and it was listed as $21, a $9 error has been made. Reversing the order of numbers is called a transposition error.

- If the error is not divisible by 2 or 9, scan the ledger to see whether an account balance in the amount of the error has been omitted from the trial balance, and scan the journal to see whether a posting of that amount has been omitted.

Currency Signs and Underlining

Note that currency signs do not appear in journals or ledgers. Currency signs are typically used only in the trial balance and the financial statements. Generally, a currency sign is shown only for the first item in the column and for the total of that column. A single line (a totaling rule) is placed under the column of figures to be added or subtracted. Total amounts are double-underlined to indicate they are final sums. Negative signs or parentheses do not appear in journals or ledgers.

GLOSSARY REVIEW

- Account

- A record of increases and decreases in specifi casset, liability, or equity items. (p. 54).

- Chart of accounts

- A list of accounts and the account numbers that identify their location in the ledger. (p. 64).

- Compound entry

- A journal entry that involves three or more accounts. (p. 61).

- Credit

- The right side of an account. (p. 54).

- Debit

- The left side of an account. (p. 54).

- Dividend

- A distribution by a company to its shareholderson a pro rata (equal) basis. (p. 56).

- Double-entry system

- A system that records in appropriate accounts the dual effect of each transaction. (p. 55).

- General journal

- The most basic form of journal. (p. 60).

- General ledger

- A ledger that contains all asset, liability, and equity accounts. (p. 62).

- Journal

- An accounting record in which transactions are initially recorded in chronological order. (p. 60).

- Journalizing

- The entering of transaction data in the journal. (p. 60).

- Ledger

- The entire group of accounts maintained by a company. (p. 62).

- Normal balance

- An account balance on the side where an increase in the account is recorded. (p. 55).

- Posting

- The procedure of transferring journal entries to the ledger accounts. (p. 63).

- Retained earnings

- Net income that is kept (retained) in the business. (p. 56).

- Simple entry

- A journal entry that involves only two accounts. (p. 61).

- T-account

- The basic form of an account. (p. 54).

- Three-column form of account

- A form with columns for debit, credit, and balance amounts in an account. (p. 62).

- Trial balance

- A list of accounts and their balances at a given time. (p. 72).

PRACTICE MULTIPLE-CHOICE QUESTIONS

-

Which of the following statements about an account is true?

- The right side of an account is the debit or increase side.

- An account is an individual accounting record of increases and decreases in specific asset, liability, and equity items.

- There are separate accounts for specific assets and liabilities but only one account for equity items.

- The left side of an account is the credit or decrease side.

-

Debits:

- increase both assets and liabilities.

- decrease both assets and liabilities.

- increase assets and decrease liabilities.

- decrease assets and increase liabilities.

-

A revenue account:

- is increased by debits.

- is decreased by credits.

- has a normal balance of a debit.

- is increased by credits.

-

Accounts that normally have debit balances are:

- assets, expenses, and revenues.

- assets, expenses, and share capital—ordinary.

- assets, liabilities, and dividends.

- assets, dividends, and expenses.

-

The expanded accounting equation is:

-

Which of the following is not part of the recording process?

- Analyzing transactions.

- Preparing a trial balance.

- Entering transactions in a journal.

- Posting transactions.

-

Which of the following statements about a journal is false?

- It is not a book of original entry.

- It provides a chronological record of transactions.

- It helps to locate errors because the debit and credit amounts for each entry can be readily compared.

- It discloses in one place the complete effect of a transaction.

-

The purchase of supplies on account should result in:

- a debit to Supplies Expense and a credit to Cash.

- a debit to Supplies Expense and a credit to Supplies.

- a debit to Supplies and a credit to Accounts Payable.

- a debit to Supplies and a credit to Accounts Receivable.

-

A ledger:

- contains only asset and liability accounts.

- should show accounts in alphabetical order.

- is a collection of the entire group of accounts maintained by a company.

- is a book of original entry.

-

Posting:

- normally occurs before journalizing.

- transfers ledger transaction data to the journal.

- is an optional step in the recording process.

- transfers journal entries to ledger accounts.

-

Before posting a payment of €5,000, the Accounts Payable of Senator Company had a normal balance of €16,000. The balance after posting this transaction was:

- €21,000.

- €5,000.

- €11,000.

- Cannot be determined.

-

A trial balance:

- is a list of accounts with their balances at a given time.

- proves the mathematical accuracy of journalized transactions.

- will not balance if a correct journal entry is posted twice.

- proves that all transactions have been recorded.

-

A trial balance will not balance if:

- a correct journal entry is posted twice.

- the purchase of supplies on account is debited to Supplies and credited to Cash.

- a £100 cash dividend is debited to Dividends for £1,000 and credited to Cash for £100.

- a £450 payment on account is debited to Accounts Payable for £45 and credited to Cash for £45.

-

The trial balance of Clooney Ltd. had accounts with the following normal balances: Cash £5,000, Service Revenue £85,000, Salaries and Wages Payable £4,000, Salaries and Wages Expense £40,000, Rent Expense £10,000, Share Capital—Ordinary £42,000, Dividends £15,000, and Equipment £61,000. In preparing a trial balance, the total in the debit column is:

- £131,000.

- £216,000.

- £91,000.

- £116,000.

Solutions

PRACTICE EXERCISES

Analyze transactions and determine their effect on accounts.

- Presented below is information related to Conan Real Estate Agency plc.

Oct. 1

Arnold Conan begins business as a real estate agent with a cash investment of £18,000 in exchange for shares. 2Hires an administrative assistant. 3Purchases office equipment for £1,700, on account. 6Sells a house and lot for B. Clinton; bills B. Clinton £4,200 for realty services performed. 27Pays £900 on the balance related to the transaction of October 3. 30Pays the administrative assistant £2,800 in salary for October.

Instructions

Journalize the transactions. (You may omit explanations.)

Solution

Journalize transactions from account data and prepare a trial balance.

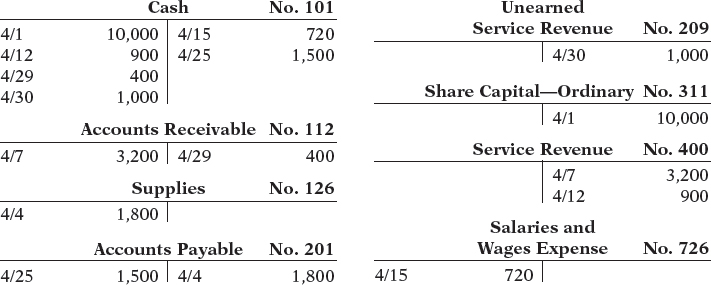

- The T-accounts below summarize the ledger of Garfunkle Landscaping Company at the end of the first month of operations.

Instructions

- Prepare the complete general journal (including explanations) from which the postings to Cash were made.

- Prepare a trial balance at April 30, 2017.

Solution

PRACTICE PROBLEM

Journalize transactions, post, and prepare a trial balance.

A group of student investors in Hong Kong opened Campus Laundromat Ltd. on September 1, 2017. During the first month of operations, the following transactions occurred.

Sept. 1 |

Shareholders invested HK$200,000 cash in the business in exchange for ordinary shares. |

2 |

Paid HK$10,000 cash for store rent for the month of September. |

3 |

Purchased washers and dryers for HK$250,000, paying HK$100,000 in cash and signing a HK$150,000, 6-month, 12% note payable. |

4 |

Paid HK$12,000 for a one-year accident insurance policy. |

10 |

Received a bill from the Daily News for advertising the opening of the laundromat HK$2,000. |

20 |

Declared and paid a cash dividend to shareholders HK$7,000. |

30 |

Determined that cash receipts for laundry fees for the month were HK$62,000. |

The chart of accounts for the company is the same as for Yazici Advertising A.Ş. (Illustration 2-19 on page 64) except for the following: No. 610 Advertising Expense.

Instructions

- Journalize the September transactions. (Use J1 for the journal page number.)

- Open ledger accounts and post the September transactions.

- Prepare a trial balance at September 30, 2017.

Solution

WileyPLUS

Brief Exercises, DO IT! Review, Exercises, and Problems, and many additional resources are available for practice in WileyPLUS.

QUESTIONS

- Describe the parts of a T-account.

- “The terms debit and credit mean increase and decrease, respectively.” Do you agree? Explain.

- Jason Hilbert, a fellow student, contends that the double-entry system means each transaction must be recorded twice. Is Jason correct? Explain.

- Sandra Browne, a beginning accounting student, believes debit balances are favorable and credit balances are unfavorable. Is Sandra correct? Discuss.

- State the rules of debit and credit as applied to (a) asset accounts, (b) liability accounts, and (c) equity accounts (revenue, expenses, dividends, share capital—ordinary, and retained earnings).

- What is the normal balance for each of the following accounts? (a) Accounts Receivable. (b) Cash. (c) Dividends. (d) Accounts Payable. (e) Service Revenue. (f) Salaries and Wages Expense. (g) Share Capital—Ordinary.

- Indicate whether each of the following accounts is an asset, a liability, or an equity account and whether it has a normal debit or credit balance: (a) Accounts Receivable, (b) Accounts Payable, (c) Equipment, (d) Dividends, (e) Supplies.

- For the following transactions, indicate the account debited and the account credited.

- Supplies are purchased on account.

- Cash is received on signing a note payable.

- Employees are paid salaries in cash.

- Indicate whether the following accounts generally will have (a) debit entries only, (b) credit entries only, or (c) both debit and credit entries.

- Cash.

- Accounts Receivable.

- Dividends.

- Accounts Payable.

- Salaries and Wages Expense.

- Service Revenue.

- What are the basic steps in the recording process?

- What are the advantages of using a journal in the recording process?

- When entering a transaction in the journal, should the debit or credit be written first?

- Which should be indented, the debit or credit?

- Describe a compound entry, and provide an example.

- Should business transaction debits and credits be recorded directly in the ledger accounts?

- What are the advantages of first recording transactions in the journal and then posting to the ledger?

- The account number is entered as the last step in posting the amounts from the journal to the ledger. What is the advantage of this step?

- Journalize the following business transactions.

- Alberto Rivera invests R$9,000 cash in the business in exchange for ordinary shares.

- Insurance of R$800 is paid for the year.

- Supplies of R$2,000 are purchased on account.

- Cash of R$7,500 is received for services performed.

- What is a ledger?

- What is a chart of accounts and why is it important?

- What is a trial balance and what are its purposes?

- Joe Kirby is confused about how accounting information flows through the accounting system. He believes the flow of information is as follows.

- Debits and credits posted to the ledger.

- Business transaction occurs.

- Information entered in the journal.

- Financial statements are prepared.

- Trial balance is prepared.

Is Joe correct? If not, indicate to Joe the proper flow of the information. - Two students are discussing the use of a trial balance. They wonder whether the following errors, each considered separately, would prevent the trial balance from balancing. What would you tell them?

- The bookkeeper debited Cash for €600 and credited Salaries and Wages Expense for €600 for payment of wages.

- Cash collected on account was debited to Cash for €900 and Service Revenue was credited for €90.

- What are the normal balances for TSMC's Cash, Accounts Payable, and Interest Expense accounts?

BRIEF EXERCISES

Indicate debit and credit effects and normal balance.

BE2-1 For each of the following accounts, indicate the effects of (a) a debit and (b) a credit on the accounts and (c) the normal balance of the account.

- Accounts Payable.

- Advertising Expense.

- Service Revenue.

- Accounts Receivable.

- Share Capital—Ordinary.

- Dividends.

Identify accounts to be debited and credited.

BE2-2 Transactions for the Kaustav Sen Company ASA, which performs welding services, for the month of June are presented below. Identify the accounts to be debited and credited for each transaction.

June 1 |

Kaustav Sen invests €4,000 cash in exchange for ordinary shares in a small welding business. |

2 |

Purchases equipment on account for €900. |

3 |

€800 cash is paid to landlord for June rent. |

12 |

Sent an invoice to L. Nigh €300 for welding work performed on account. |

Journalize transactions.

BE2-3 Using the data in BE2-2, journalize the transactions. (You may omit explanations.)

Identify and explain steps in recording process.

BE2-3 ![]() Tim Weber, a fellow student, is unclear about the basic steps in the recording process. Identify and briefly explain the steps in the order in which they occur.

Tim Weber, a fellow student, is unclear about the basic steps in the recording process. Identify and briefly explain the steps in the order in which they occur.

Indicate basic and debit-credit analysis.

BE2-3 J.A. Motzek SA has the following transactions during August of the current year. Indicate (a) the effect on the accounting equation and (b) the debit-credit analysis illustrated on pages 65–70.

Aug. 1 |

Opens an office as a financial advisor, investing R$5,000 in cash in exchange for ordinary shares. |

4 |

Pays insurance in advance for 6 months, R$1,800 cash. |

16 |

Receives R$1,100 from clients for services performed. |

27 |

Pays secretary R$1,000 salary. |

Journalize transactions.

BE2-6 Using the data in BE2-5, journalize the transactions. (You may omit explanations.)

Post journal entries to T-accounts.

BE2-6 Selected transactions for the Gilles Ltd. are presented in journal form on the next page. Post the transactions to T-accounts. Make one T-account for each item and determine each account's ending balance.

BE2-8

Post journal entries to standard form of account.

Selected journal entries for the Gilles Ltd. are presented in BE2-7. Post the transactions using the standard form of account.

BE2-9

Prepare a trial balance.

From the ledger balances given below, prepare a trial balance for the Starr SE at June 30, 2017. List the accounts in the order shown on page 73. All account balances are normal.

Accounts Payable €8,600, Cash €6,800, Share Capital—Ordinary €20,000, Dividends €800, Equipment €17,000, Service Revenue €6,000, Accounts Receivable €3,000, Salaries and Wages Expense €6,000, and Rent Expense €1,000.

BE2-10

Prepare a correct trial balance.

An inexperienced bookkeeper prepared the following trial balance. Prepare a correct trial balance, assuming all account balances are normal.

CHENG COMPANY LTD. Trial Balance December 31, 2017 |

||

| Debit | Credit | |

| Cash | £16,800 | |

| Prepaid Insurance | £ 3,500 | |

| Accounts Payable | 3,000 | |

| Unearned Service Revenue | 4,200 | |

| Share Capital—Ordinary | 13,000 | |

| Dividends | 4,500 | |

| Service Revenue | 25,600 | |

| Salaries and Wages Expense | 18,600 | |

| Rent Expense | 2,400 | |

| £39,600 |

£52,000 |

|

EXERCISES

Analyze statements about accounting and the recording process.

E2-1 Larry Burns has prepared the following list of statements about accounts.

- An account is an accounting record of either a specific asset or a specific liability.

- An account shows only increases, not decreases, in the item it relates to.

- Some items, such as cash and accounts receivable, are combined into one account.

- An account has a left, or credit side, and a right, or debit side.

- A simple form of an account, consisting of just the account title, the left side, and the right side, is called a T-account.

Instructions

Identify each statement as true or false. If false, indicate how to correct the statement.

Identify debits, credits, and normal balances.

E2-2 Selected transactions for B. Madar SE, an interior decorating firm, in its first month of business, are shown below.

Jan. 2 |

Invested €15,000 cash in the business in exchange for ordinary shares. |

3 |

Purchased used car for €7,000 cash for use in the business. |

9 |

Purchased supplies on account for €500. |

11 |

€1,800 of services were performed and billed. |

16 |

Paid €200 cash for advertising. |

20 |

Received €700 cash from customers billed on January 11. |

| 23 | Paid creditor €300 cash on balance owed. |

| 28 | Declared and paid a €1,000 cash dividend. |

Instructions

For each transaction indicate the following.

- The basic type of account debited and credited (asset, liability, equity).

- The specific account debited and credited (cash, rent expense, service revenue, etc.).

- Whether the specific account is increased or decreased.

- The normal balance of the specific account.

Use the following format, in which the January 2 transaction is given as an example.

Account Debited |

Account Credited |

||||||||

| Date | (a) Basic Type |

(b) Specific Account |

(c) Effect |

(d) Normal Balance |

(a) Basic Type |

(b) Specific Account |

(c) Effect |

(d) Normal Balance |

|

Jan. 2 |

Asset |

Cash |

Increase |

Debit |

Equity |

Share Capital |

Increase |

Credit |

|

Journalize transactions.

E2-3 Data for B. Madar SE, interior decorating, are presented in E2-2.

Instructions

Journalize the transactions using journal page J1. (You may omit explanations.)

Analyze transactions and determine their effect on accounts.

E2-4 Presented below is information related to Beijing Real Estate Agency Ltd.

| Oct. 1 | Lynn Robbins begins business as a real estate agent with a cash investment of ¥200,000 in exchange for ordinary shares. |

| 2 | Hires an administrative assistant. |

| 3 | Purchases office furniture for ¥19,000, on account. |

| 6 | Sells a house and lot for N. Fennig; bills N. Fennig ¥32,000 for realty services performed. |

| 27 | Pays ¥8,500 on the balance related to the transaction of October 3. |

| 30 | Pays the administrative assistant ¥25,000 in salary for October. |

Instructions

Prepare the debit-credit analysis for each transaction as illustrated on pages 65–70.

Journalize transactions.

E2-5 Transaction data for Beijing Real Estate Agency Ltd. are presented in E2-4.

Instructions

Journalize the transactions. (You may omit explanations.)

Analyze transactions and journalize.

E2-6 Minsk Industries OAO had the following transactions.

- Borrowed py50,000 from the bank by signing a note.

- Paid py25,000 cash for a computer.

- Purchased py4,500 of supplies on account.

Instructions

- Indicate what accounts are increased and decreased by each transaction.

- Journalize each transaction. (Omit explanations.)

Analyze transactions and journalize.

E2-7 Rockford Enterprises Ltd. had the following selected transactions.

- Kris Rockford invested £5,500 cash in the business in exchange for ordinary shares.

- Paid office rent of £1,100.

- Performed consulting services worth £4,700 on account.

- Declared and paid a £400 cash dividend.

Instructions

- Indicate the effect each transaction has on the accounting equation , using plus and minus signs.

- Journalize each transaction. (Omit explanations.)

Analyze statements about the ledger.

E2-8 Rachel Manny has prepared the following list of statements about the general ledger.

- The general ledger contains all the asset and liability accounts, but no equity accounts.

- The general ledger is sometimes referred to as simply the ledger.

- The accounts in the general ledger are arranged in alphabetical order.

- Each account in the general ledger is numbered for easier identification.

- The general ledger is a book of original entry.

Instructions

Identify each statement as true or false. If false, indicate how to correct the statement.

Post journal entries and prepare a trial balance.

E2-9 Selected transactions from the journal of Roberta Mendez SLU, investment broker, are presented below.

Instructions

- Post the transactions to T-accounts.

- Prepare a trial balance at August 31, 2017.

Journalize transactions from account data and prepare a trial balance.

E2-10 The T-accounts below summarize the ledger of Pierre Landscaping Company SA at the end of the first month of operations.

Instructions

- Prepare the complete general journal (including explanations) from which the postings to Cash were made.

- Prepare a trial balance at April 30, 2017.

Journalize transactions from account data and prepare a trial balance.

E2-11 Presented below is the ledger for Sparks Co. Ltd.

Instructions

- Reproduce the journal entries for the transactions that occurred on October 1, 10, and 20, and provide explanations for each.

- Determine the October 31 balance for each of the accounts above, and prepare a trial balance at October 31, 2017.

Prepare journal entries and post using standard account form.

E2-12 Selected transactions for Isabella Rossini Company SpA during its first month in business are presented below.

| Sept. 1 | Invested €10,000 cash in the business in exchange for ordinary shares. |

| 5 | Purchased equipment for €12,000 paying €4,000 in cash and the balance on account. |

| 25 | Paid €2,400 cash on balance owed for equipment. |

| 30 | Declared and paid a €500 cash dividend. |

Rossini's chart of accounts shows No. 101 Cash, No. 157 Equipment, No. 201 Accounts Payable, No. 311 Share Capital—Ordinary, and No. 332 Dividends.

Instructions

- Journalize the transactions on page J1 of the journal. (Omit explanations.)

- Post the transactions using the standard account form.

Analyze errors and their effects on trial balance.

The bookkeeper for Arno Equipment Repair NV made a number of errors in journalizing and posting, as described below.

- A credit posting of €400 to Accounts Receivable was omitted.

- A debit posting of €750 for Prepaid Insurance was debited to Insurance Expense.

- A collection from a customer of €100 in payment of its account owed was journalized and posted as a debit to Cash €100 and a credit to Service Revenue €100.

- A credit posting of €300 to Property Taxes Payable was made twice.

- A cash purchase of supplies for €250 was journalized and posted as a debit to Supplies €230 and a credit to Cash €230.

- A debit of €495 to Advertising Expense was posted as €459.

Instructions

For each error:

- Indicate whether the trial balance will balance.

- If the trial balance will not balance, indicate the amount of the difference.

- Indicate the trial balance column that will have the larger total.

Consider each error separately. Use the following form, in which error (1) is given as an example.

Error |

(a) In Balance |

(b) Difference |

(c) Larger Column |

(1) |

No |

$400 |

debit |

Prepare a trial balance.

E2-14 The accounts in the ledger of Tempus Fugit Delivery Service Ltd. contain the following balances on July 31, 2017.

| Accounts Receivable | £10,642 | Prepaid Insurance | £ 1,968 |

| Accounts Payable | 8,396 | Maintenance and Repairs Expense | 961 |

| Cash | ? | Service Revenue | 10,610 |

| Equipment | 49,360 | Dividends | 700 |

| Gasoline Expense | 758 | Share Capital—Ordinary | 40,000 |

| Utilities Expense | 523 | Salaries and Wages Expense | 4,428 |

| Notes Payable | 26,450 | Salaries and Wages Payable | 815 |

| Retained Earnings | 4,636 |

Instructions

Prepare a trial balance with the accounts arranged as illustrated in the chapter and fill in the missing amount for Cash.

Identify cash flow activities.

E2-15 The statement of cash flows classifies each transaction as an operating activity, an investing activity, or a financing activity. Operating activities are the types of activities the company performs to generate profits. Investing activities include the purchase of long-lived assets such as equipment or the purchase of investment securities. Financing activities are borrowing money, issuing shares, and paying dividends.

Presented below are the following transactions.

- Issued shares for €20,000 cash.

- Issued note payable for €10,000 cash.

- Purchased equipment for €11,000 cash.

- Received €15,000 cash for services performed.

- Paid €1,000 cash for rent.

- Paid €600 cash dividend to shareholders.

- Paid €6,500 cash for salaries.

Instructions

Classify each of these transactions as operating, investing, or financing activities.

PROBLEMS: SET A

Journalize a series of transactions.

P2-1A Prairie Park ASA was started on April 1 by F. L. Wright and associates. The following selected events and transactions occurred during April.

Apr. 1 |

Shareholders invested €50,000 cash in the business in exchange for ordinary shares. |

4 |

Purchased land costing €34,000 for cash. |

8 |

Incurred advertising expense of €1,800 on account. |

11 |

Paid salaries to employees €1,500. |

12 |

Hired park manager at a salary of €4,000 per month, effective May 1. |

13 |

Paid €1,500 cash for a one-year insurance policy. |

17 |

Declared and paid a €1,400 cash dividend. |

20 |

Received €6,400 in cash for admission fees. |

25 |

Sold 100 coupon books for €30 each. Each book contains 10 coupons that entitle the holder to one admission to the park. |

30 |

Received €8,500 in cash admission fees. |

30 |

Paid €900 on balance owed for advertising incurred on April 8. |

Prairie Park uses the following accounts: Cash, Prepaid Insurance, Land, Accounts Payable, Unearned Service Revenue, Share Capital—Ordinary, Dividends, Service Revenue, Advertising Expense, and Salaries and Wages Expense.

Instructions

Journalize the April transactions.

Journalize transactions, post, and prepare a trial balance.

P2-2A Lena Fohn is a licensed accountant. During the first month of operations of her business, Lena Fohn, AG, the following events and transactions occurred.

| May 1 | Shareholders invested €20,000 cash in exchange for ordinary shares. |

| 2 | Hired a secretary-receptionist at a salary of €2,000 per month. |

| 3 | Purchased €1,500 of supplies on account from Hartig Supply Company. |

| 7 | Paid office rent of €900 cash for the month. |

| 11 | Completed a tax assignment and billed client €2,800 for services performed. |

| 12 | Received €3,500 advance on a management consulting engagement. |

| 17 | Received cash of €1,200 for services performed for Lucille Co. |

| 31 | Paid secretary-receptionist €2,000 salary for the month. |

| 31 | Paid 40% of balance due Hartig Supply Company. |

Lena uses the following chart of accounts: No. 101 Cash, No. 112 Accounts Receivable, No. 126 Supplies, No. 201 Accounts Payable, No. 209 Unearned Service Revenue, No. 311 Share Capital—Ordinary, No. 400 Service Revenue, No. 726 Salaries and Wages Expense, and No. 729 Rent Expense.

Instructions

- Journalize the transactions.

- Post to the ledger accounts.

- Prepare a trial balance on May 31, 2017.

Journalize and post transactions and prepare a trial balance.

P2-3A Sean Browne owns and manages a computer repair service, which had the following trial balance on December 31, 2016 (the end of its fiscal year).

BYTE REPAIR SERVICE, LTD. Trial Balance December 31, 2016 |

||

| Cash | £ 8,000 | |

| Accounts Receivable | 16,000 | |

| Supplies | 13,000 | |

| Prepaid Rent | 3,000 | |

| Equipment | 24,000 | |

| Accounts Payable | £19,000 | |

| Share Capital—Ordinary | 33,000 | |

| Retained Earnings | 12,000 | |

| £64,000 |

£64,000 |

|

Summarized transactions for January 2017 were as follows.

- Advertising costs, paid in cash, £1,000.

- Additional supplies acquired on account £4,000.

- Miscellaneous expenses, paid in cash, £1,100.

- Cash collected from customers in payment of accounts receivable £13,000.

- Cash paid to creditors for accounts payable due £15,000.

- Repair services performed during January: for cash £5,000; on account £9,000.

- Wages for January, paid in cash, £3,000.

- Dividends during January were £2,000.

Instructions

- Open T-accounts for each of the accounts listed in the trial balance, and enter the opening balances for 2017.

- Prepare journal entries to record each of the January transactions. (Omit explanations.)

- Post the journal entries to the accounts in the ledger. (Add accounts as needed.)

- Prepare a trial balance as of January 31, 2017.

Prepare a correct trial balance

P2-4A The trial balance of the Jason Company Ltd. shown below does not balance.

JASON COMPANY LTD. Trial Balance May 31, 2017 |

||

Debit |

Credit |

|

| Cash | £ 3,850 | |

| Accounts Receivable | £ 2,750 | |

| Prepaid Insurance | 700 | |

| Equipment | 12,000 | |

| Accounts Payable | 4,500 | |

| Unearned Service Revenue | 560 | |

| Share Capital—Ordinary | 11,700 | |

| Service Revenue | 8,690 | |

| Salaries and Wages Expense | 4,200 | |

| Advertising Expense | 1,100 | |

| Utilities Expense | 800 | |

| £30,800 |

£20,050 |

|

Your review of the ledger reveals that each account has a normal balance. You also discover the following errors.

- The totals of the debit sides of Prepaid Insurance, Accounts Payable, and Utilities Expense were each understated £100.

- Transposition errors were made in Accounts Receivable and Service Revenue. Based on postings made, the correct balances were £2,570 and £8,960, respectively.

- A debit posting to Salaries and Wages Expense of £200 was omitted.

- A £1,000 cash dividend was debited to Share Capital—Ordinary for £1,000 and credited to Cash for £1,000.

- A £520 purchase of supplies on account was debited to Equipment for £520 and credited to Cash for £520.

- A cash payment of £450 for advertising was debited to Advertising Expense for £45 and credited to Cash for £45.

- A collection from a customer for £420 was debited to Cash for £420 and credited to Accounts Payable for £420.

Instructions

Prepare a correct trial balance. Note that the chart of accounts includes the following: Dividends and Supplies. (Hint: It helps to prepare the correct journal entry for the transaction described and compare it to the mistake made.)

Journalize transactions, post, and prepare a trial balance.

P2-5A The Classic Theater Ltd. opened on April 1. All facilities were completed on March 31. At this time, the ledger showed No. 101 Cash €6,000, No. 140 Land €10,000, No. 145 Buildings (concession stand, projection room, ticket booth, and screen) €8,000, No. 157 Equipment €6,000, No. 201 Accounts Payable €2,000, No. 275 Mortgage Payable €8,000, and No. 311 Share Capital—Ordinary €20,000. During April, the following events and transactions occurred.

| Apr. 2 | Paid film rental of €800 on first movie. |

3 |

Ordered two additional films at €1,000 each. |

9 |

Received €1,800 cash from admissions. |

10 |

Made €2,000 payment on mortgage and €1,000 for accounts payable due. |

11 |

Classic Theater contracted with D. Zarle Company to operate the concession stand. Zarle is to pay 18% of gross concession receipts (payable monthly) for the rental of the concession stand. |

12 |

Paid advertising expenses €300. |

20 |

Received one of the films ordered on April 3 and was billed €1,000. The film will be shown in April. |

25 |

Received €5,500 cash from admissions. |

29 |

Paid salaries €1,600. |

30 |

Received statement from D. Zarle showing gross concession receipts of €1,200 and the balance due to The Classic Theater of for April. Zarle paid one-half of the balance due and will remit the remainder on May 5. |

30 |

Prepaid €1,300 rental on special film to be run in May. |

In addition to the accounts identified above, the chart of accounts shows No. 112 Accounts Receivable, No. 136 Prepaid Rent, No. 400 Service Revenue, No. 429 Rent Revenue, No. 610 Advertising Expense, No. 726 Salaries and Wages Expense, and No. 729 Rent Expense.

Instructions

- Enter the beginning balances in the ledger as of April 1. Insert a check mark (✓) in the reference column of the ledger for the beginning balance.

- Journalize the April transactions.

- Post the April journal entries to the ledger. Assume that all entries are posted from page 1 of the journal.

- Prepare a trial balance on April 30, 2017.

PROBLEMS: SET B

Journalize a series of transactions.

P2-1B Surepar Disc Golf Course was opened on March 1 by Bill Arnsdorf. The following selected events and transactions occurred during March:

| Mar. 1 | Invested €60,000 cash in the business in exchange for ordinary shares. |

3 |

Purchased Lee's Golf Land for €38,000 cash. The price consists of land €23,000, shed €9,000, and equipment €6,000. (Make one compound entry.) |

5 |

Advertised the opening of the driving range and miniature golf course, paying advertising expenses of €1,300. |

6 |

Paid cash €3,000 for a one-year insurance policy. |

10 |

Purchased golf discs and other equipment for €1,050 from Parton Company payable in 30 days. |

18 |

Received €440 in cash for golf fees recognized. |

19 |

Sold 100 coupon books for €18 each. Each book contains 4 coupons that enable the holder to play one round of disc golf. |

25 |

Declared and paid an €800 cash dividend. |

30 |

Paid salaries of €250. |

30 |

Paid Parton Company in full. |

31 |

Received €200 cash for fees recognized. |

Surepar uses the following accounts: Cash, Prepaid Insurance, Land, Buildings, Equipment, Accounts Payable, Unearned Service Revenue, Share Capital—Ordinary, Dividends, Service Revenue, Advertising Expense, and Salaries and Wages Expense.

Instructions

Journalize the March transactions.

Journalize transactions, post, and prepare a trial balance.

P2-2B Judi Dench is a licensed dentist. During the first month of the operation of her business, the following events and transactions occurred.

| April 1 | Shareholders invested £40,000 cash in exchange for ordinary shares. |

1 |

Hired a secretary-receptionist at a salary of £600 per week payable monthly. |

2 |

Paid office rent for the month £1,400. |

3 |

Purchased dental supplies on account from Halo Company £5,200. |

10 |

Performed dental services and billed insurance companies £6,600. |

11 |

Received £1,000 cash advance from Rich Welk for an implant. |

20 |

Received £2,100 cash for services performed for Phil Stueben. |

30 |

Paid secretary-receptionist for the month £2,400. |

30 |

Paid £1,900 to Halo Company for accounts payable due. |

Judi uses the following chart of accounts: No. 101 Cash, No. 112 Accounts Receivable, No. 126 Supplies, No. 201 Accounts Payable, No. 209 Unearned Service Revenue, No. 311 Share Capital—Ordinary, No. 400 Service Revenue, No. 726 Salaries and Wages Expense, and No. 729 Rent Expense.

Instructions

- Journalize the transactions.

- Post to the ledger accounts.

- Prepare a trial balance on April 30, 2017.

Journalize transactions, post, and prepare a trial balance.

P2-3B Richardson Services Ltd. was formed on May 1, 2017. The following transactions took place during the first month.

Transactions on May 1:

- Shareholders invested £50,000 cash in exchange for ordinary shares.

- Hired two employees to work in the warehouse. They will each be paid a salary of £2,800 per month.

- Signed a 2-year rental agreement on a warehouse; paid £24,000 cash in advance for the first year.

- Purchased furniture and equipment costing £30,000. A cash payment of £6,000 was made immediately; the remainder will be paid in 6 months.

- Paid £1,800 cash for a one-year insurance policy on the furniture and equipment.

Transactions during the remainder of the month:

- 6. Purchased basic office supplies for £940 cash.

- 7. Purchased more office supplies for £1,300 on account.

- 8. Total revenues recognized were £18,000—£5,000 cash and £13,000 on account.

- 9. Paid £400 to suppliers for accounts payable due.

- 10. Received £3,000 from customers in payment of accounts receivable.

- 11. Received utility bills in the amount of £260, to be paid next month.

- 12. Paid the monthly salaries of the two employees, totalling £5,600.

Instructions

- Prepare journal entries to record each of the events listed. (Omit explanations.)

- Post the journal entries to T-accounts.

- Prepare a trial balance as of May 31, 2017.

Prepare a correct trial balance.

P2-4B The trial balance of Mueller SE shown below does not balance.

MUELLER SE Trial Balance June 30, 2017 |

||

Debit |

Credit |

|

| Cash | € 3,840 |

|

| Accounts Receivable | € 2,898 |

|

| Supplies | 800 |

|

| Equipment | 3,000 |

|

| Accounts Payable | 2,666 |

|

| Unearned Service Revenue | 2,200 |

|

| Share Capital—Ordinary | 9,000 |

|

| Dividends | 800 |

|

| Service Revenue | 2,380 |

|

| Salaries and Wages Expense | 3,400 |

|

| Utilities Expense | 910 |

|

| €14,008 |

€17,886 |

|

Each of the listed accounts has a normal balance per the general ledger. An examination of the ledger and journal reveals the following errors.

- Cash received from a customer in payment of its account was debited for €570, and Accounts Receivable was credited for the same amount. The actual collection was for €750.

- The purchase of a computer on account for €620 was recorded as a debit to Supplies for €620 and a credit to Accounts Payable for €620.

- Services were performed on account for a client for €890. Accounts Receivable was debited for €890, and Service Revenue was credited for €89.

- A debit posting to Salaries and Wages Expense of €700 was omitted.

- A payment of a balance due for €309 was credited to Cash for €309 and credited to Accounts Payable for €390.

- The payment of a €600 cash dividend was debited to Salaries and Wages Expense for €600 and credited to Cash for €600.

Instructions

Prepare a correct trial balance. (Hint: It helps to prepare the correct journal entry for the transaction described and compare it to the mistake made.)

Journalize transactions, post, and prepare a trial balance.

P2-5B The Wilson Theater Ltd., owned by Tegan Wilson, will begin operations in March. The Wilson will be unique in that it will show only triple features of sequential theme movies. As of March 1, the ledger of Wilson showed No. 101 Cash £7,000, No. 140 Land £22,000, No. 145 Buildings (concession stand, projection room, ticket booth, and screen) £10,000, No. 157 Equipment £8,000, No. 201 Accounts Payable £7,000, and No. 311 Share Capital—Ordinary £40,000. During the month of March, the following events and transactions occurred.

| Mar. 2 | Rented the three Indiana Jones movies to be shown for the first 3 weeks of March. The film rental was £3,500; £1,000 was paid in cash and £2,500 will be paid on March 10. |

3 |

Ordered the Lord of the Rings movies to be shown the last 10 days of March. It will cost £240 per night. |

9 |

Received £4,000 cash from admissions. |

10 |

Paid balance due on Indiana Jones movies rental and £1,600 on March 1 accounts payable. |

11 |

Wilson Theater contracted with M. Brewer to operate the concession stand. Brewer is to pay 15% of gross concession receipts (payable monthly) for the right to operate the concession stand. |

12 |

Paid advertising expenses £450. |

20 |

Received £4,400 cash from customers for admissions. |

20 |

Received the Lord of Rings movies and paid the rental fee of £2,400. |

31 |

Paid salaries of £2,500. |

31 |

Received statement from M. Brewer showing gross receipts from concessions of £3,000 and the balance due to Wilson Theater of for March. Brewer paid one-half the balance due and will remit the remainder on April 5. |

31 |

Received £9,000 cash from customers for admissions. |

In addition to the accounts identified above, the chart of accounts includes No. 112 Accounts Receivable, No. 400 Service Revenue, No. 429 Rent Revenue, No. 610 Advertising Expense, No. 729 Rent Expense, and No. 726 Salaries and Wages Expense.

Instructions

- Enter the beginning balances in the ledger. Insert a check mark (✓) in the reference column of the ledger for the beginning balance.

- Journalize the March transactions.

- Post the March journal entries to the ledger. Assume that all entries are posted from page 1 of the journal.

- Prepare a trial balance on March 31, 2017.

MATCHA CREATIONS

(Note: This is a continuation of the Matcha Creations problem from Chapter 1.)

MC2 After researching the different forms of business organization, Mei-ling Lee decides to operate “Matcha Creations” as a corporation. She then starts the process of getting the business running. In November 2017, the following activities take place.

Nov. 8 |

Mei-ling sells her investments for NT$520, which she deposits in her personal bank account. |

8 |

She opens a bank account under the name “Matcha Creations” and transfers NT$500 from her personal account to the new account in exchange for ordinary shares. |

11 |

Mei-ling pays NT$65 to have advertising brochures and posters printed. She plans to distribute these as opportunities arise. (Hint: Use Advertising Expense.) |

13 |

She buys baking supplies, such as flour, sugar, butter, and matcha, for NT$125 cash. |

14 |

Mei-ling starts to gather some baking equipment to take with her when teaching the cookie classes. She has an excellent top-of-the-line food processor and mixer that originally cost her NT$750. Mei-ling decides to start using it only in her new business. She estimates that the equipment is currently worth NT$300. She invests the equipment in the business in exchange for ordinary shares. |

16 |

Mei-ling re alizes that her initial cash investment is not enough. Her grandmother lends her NT$2,000 cash, for which Mei-ling signs a note payable in the name of the business. Mei-ling deposits the money in the business bank account. (Hint: The note does not have to be repaid for 24 months. As a result, the notes payable should be reported in the accounts as the last liability and also on the statement of financial position as the last liability.) |

17 |

She buys more baking equipment for NT$900 cash. |

20 |

She teaches her first class and collects NT$125 cash. |

25 |

Mei-ling books a second class for December 4 for NT$150. She receives NT$30 cash in advance as a down payment. |

30 |

Mei-ling pays NT$1,320 for a one-year insurance policy that will expire on December 1, 2018. |

Instructions

- Prepare journal entries to record the November transactions.

- Post the journal entries to general ledger accounts.

- Prepare a trial balance at November 30.

BROADENING YOUR PERSPECTIVE

Financial Reporting and Analysis

Financial Reporting Problem: TSMC, Ltd. (TWN)

BYP2-1 The financial statements of TSMC are presented in Appendix A. The notes accompanying the statements contain the following selected accounts. The company's complete annual report, including the notes to the financial statements, is available in the Investors section of the company's website, www.tsmc.com.

| Accounts (Trade) Payable | Tax Payable |

| Accounts (Trade) Receivable | Interest Expense (finance cost) |

| Property, Plant, and Equipment | Inventories |

Instructions

- Answer the following questions.

- What is the increase and decrease side for each account?

- What is the normal balance for each account?

- Identify the probable other account in the transaction and the effect on that account when:

- Accounts (Trade) Receivable is decreased.

- Accounts (Trade) Payable is decreased.

- Inventories are increased.

- Identify the other account(s) that ordinarily would be involved when:

- Interest Expense is increased.

- Property, Plant, and Equipment is increased.

Comparative Analysis Problem: Nestlé SA (CHE) vs. Petra Foods Ltd. (SGP)

BYP2-2 Nestlé's financial statements are presented in Appendix B. Financial statements for Petra Foods are presented in Appendix C.

Instructions

- Based on the information contained in the financial statements, determine the normal balance of the listed accounts for each company.

NestléPetra Foods

1. Inventory 1. Accounts (Trade) Receivable 2. Property, Plant, and Equipment 2. Cash and Cash Equivalents 3. Accounts (Trade) Payable 3. Cost of Sales (expense) 4. Interest Expense (finance cost) 4. Sales (revenue) - Identify the other account ordinarily involved when:

- Accounts (Trade) Receivable is increased.

- Salaries and Wages Payable is decreased.

- Property, Plant, and Equipment is increased.

- Interest Expense is increased.

Real-World Focus

BYP2-3 Much information about specific companies is available on the Internet. Such information includes basic descriptions of the company's location, activities, industry, financial health, and financial performance.

Address: finance.yahoo.com, or go to www.wiley.com/college/weygandt

Steps

- Type in a company name, or use index to find company name.

- Choose Profile. Perform instructions (a)–(c) below.

- Click on the company's specific industry to identify competitors. Perform instructions (d)–(g) below.

Instructions

Answer the following questions.

- What is the company's industry?

- What was the company's total sales?

- What was the company's net income?

- What are the names of four of the company's competitors?

- Choose one of these competitors.

- What is this competitor's name? What were its sales? What was its net income?

- Which of these two companies is larger by size of sales? Which one reported higher net income?

Critical Thinking

Decision-Making Across the Organization

![]()

BYP2-4 Amy Torbert operates Hollins Riding Academy. The academy's primary sources of revenue are riding fees and lesson fees, which are paid on a cash basis. Amy also boards horses for owners, who are billed monthly for boarding fees. In a few cases, boarders pay in advance of expected use. For its revenue transactions, the academy maintains the following accounts: No. 1 Cash, No. 5 Boarding Accounts Receivable, No. 27 Unearned Boarding Revenue, No. 51 Riding Revenue, No. 52 Lesson Revenue, and No. 53 Boarding Revenue.

The academy owns 10 horses, a stable, a riding corral, riding equipment, and office equipment. These assets are accounted for in accounts No. 11 Horses, No. 12 Building, No. 13 Riding Corral, No. 14 Riding Equipment, and No. 15 Office Equipment.

For its expenses, the academy maintains the following accounts: No. 6 Hay and Feed Supplies, No. 7 Prepaid Insurance, No. 21 Accounts Payable, No. 60 Salaries Expense, No. 61 Advertising Expense, No. 62 Utilities Expense, No. 63 Veterinary Expense, No. 64 Hay and Feed Expense, and No. 65 Insurance Expense.