Appendix I

Payroll Accounting

LEARNING OBJECTIVES

After studying this appendix, you should be able to:

- Compute and record the payroll for a pay period.

- Describe and record employer payroll taxes.

- Discuss the objectives of internal control for payroll.

APPENDIX PREVIEW

While the mechanics of payroll accounting are the same around the world, the particular accounts used are country‐specific. Each country has different laws, different health and social programs, and different taxes related to payroll. The examples in this appendix illustrate payroll accounting applied in the United States.

Accounting for Payroll

Learning Objective 1

Compute and record the payroll for a pay period.

Payroll and related fringe benefits often make up a large percentage of current liabilities. Employee compensation is often the most significant expense that a company incurs. For example, Costco (USA) recently reported total employees of 103,000 and labor and fringe benefits costs that approximated 70% of the company’s total cost of operations.

Payroll accounting involves more than paying employees’ wages. Companies are required by law to maintain payroll records for each employee, to file and pay payroll taxes, and to comply with numerous state and federal tax laws related to employee compensation. Accounting for payroll has become much more complex due to these regulations.

The term “payroll” pertains to both salaries and wages. Managerial, administrative, and sales personnel are generally paid salaries. Salaries are often expressed in terms of a specified amount per month or per year rather than an hourly rate. Store clerks, factory employees, and manual laborers are normally paid wages. Wages are based on a rate per hour or on a piecework basis (such as per unit of product). Frequently, people use the terms “salaries” and “wages” interchangeably.

The term “payroll” does not apply to payments made for services of professionals such as certified public accountants, attorneys, and architects. Such professionals are independent contractors rather than salaried employees. Payments to them are called fees. This distinction is important because government regulations relating to the payment and reporting of payroll taxes apply only to employees.

Determining the Payroll

Determining the payroll involves computing three amounts: (1) gross earnings, (2) payroll deductions, and (3) net pay.

GROSS EARNINGS

Gross earnings is the total compensation earned by an employee. It consists of wages or salaries, plus any bonuses and commissions.

Companies determine total wages for an employee by multiplying the hours worked by the hourly rate of pay. In addition to the hourly pay rate, most companies are required by law to pay hourly workers a minimum of 1½ times the regular hourly rate for overtime work in excess of eight hours per day or 40 hours per week. In addition, many employers pay overtime rates for work done at night, on weekends, and on holidays.

For example, assume that Michael Watson, an employee of Academy Company, worked 44 hours for the weekly pay period ending January 14. His regular wage is $12 per hour. For any hours in excess of 40, the company pays at one‐and‐a‐half times the regular rate. Academy computes Watson’s gross earnings (total wages) as follows.

Illustration I-1 Computation of total wages

This computation assumes that Watson receives 1½ times his regular hourly rate ($12 × 1.5) for his overtime hours. Union contracts often require that overtime rates be as much as twice the regular rates.

An employee’s salary is generally based on a monthly or yearly rate. The company then prorates these rates to its payroll periods (e.g., biweekly or monthly). Most executive and administrative positions are salaried. Federal law does not require overtime pay for employees in such positions.

Many companies have bonus agreements for employees. One survey found that over 94% of the largest U.S. manufacturing companies offer annual bonuses to key executives. Bonus arrangements may be based on such factors as increased sales or net income. Companies may pay bonuses in cash and/or by granting employees the opportunity to acquire company shares at favorable prices (called stock option plans in the United States).

PAYROLL DEDUCTIONS

As anyone who has received a paycheck knows, gross earnings are usually very different from the amount actually received. The difference is due to payroll deductions.

Payroll deductions may be mandatory or voluntary. Mandatory deductions are required by law and consist of FICA taxes and income taxes. Voluntary deductions are at the option of the employee. Illustration I-2 (page I‐3) summarizes common types of payroll deductions. Such deductions do not result in payroll tax expense to the employer. The employer is merely a collection agent and subsequently transfers the deducted amounts to the government and designated recipients.

FICA TAXES In 1937, Congress enacted the Federal Insurance Contribution Act (FICA). FICA taxes are designed to provide workers with supplemental retirement, employment disability, and medical benefits. In 1965, Congress extended benefits to include Medicare for individuals over 65 years of age. The benefits are financed by a tax levied on employees’ earnings.

FICA taxes consist of a Social Security tax and a Medicare tax. They are paid by both employee and employer. The FICA tax rate is 7.65% (6.2% Social Security tax up to $117,0001 plus 1.45% Medicare tax) of salary and wages for each employee. In addition, the Medicare tax of 1.45% continues for an employee’s salary and wages in excess of $117,000. These tax rate and tax base requirements are shown in Illustration I-3.

1The $117,000 limit is based on 2014 guidelines set by the Social Security Administration.

Illustration I-2 Payroll deductions

Illustration I-3 FICA tax rate and tax base

To illustrate the computation of FICA taxes, assume that Mario Ruez has total wages for the year of $100,000. In this case, Mario pays FICA taxes of $7,650 ($100,000 × 7.65%). If Mario has total wages of $124,000, Mario pays FICA taxes of $9,052, as shown in Illustration I-4.

Illustration I-4 FICA tax computation

Mario’s employer is also required to pay $9,052 of FICA taxes.

INCOME TAXES Under the U.S. pay‐as‐you‐go system of federal income taxes, employers are required to withhold income taxes from employees each pay period. Four variables determine the amount to be withheld: (1) the employee’s gross earnings, (2) marital status, (3) the number of allowances claimed by the employee, and (4) the length of the pay period. The number of allowances claimed typically includes the employee, his or her spouse, and other dependents.

Withholding tables furnished by the Internal Revenue Service indicate the amount of income tax to be withheld. Withholding amounts are based on gross wages and the number of allowances claimed. Separate tables are provided for weekly, biweekly, semimonthly, and monthly pay periods. Illustration I-5 shows the withholding tax table for Michael Watson (assuming he earns $552 per week, is married, and claims two allowances). For a weekly salary of $552 with two allowances, the income tax to be withheld is $24 (highlighted in red).

Illustration I-5 FICA tax computation

In addition, most states (and some cities) require employers to withhold income taxes from employees’ earnings. As a rule, the amounts withheld are a percentage (specified in the state revenue code) of the amount withheld for the federal income tax. Or, they may be a specified percentage of the employee’s earnings. For the sake of simplicity, we have assumed that Watson’s wages are subject to state income taxes of 2%, or $11.04 (2% × $552) per week.

There is no limit on the amount of gross earnings subject to income tax withholdings. In fact, under our progressive system of taxation, the higher the earnings, the higher the percentage of income withheld for taxes.

OTHER DEDUCTIONS Employees may voluntarily authorize withholdings for charitable, retirement, and other purposes. All voluntary deductions from gross earnings should be authorized in writing by the employee. The authorization(s) may be made individually or as part of a group plan. Deductions for charitable organizations, such as the United Fund, or for financial arrangements, such as U.S. savings bonds and repayment of loans from company credit unions, are made individually. Deductions for union dues, health and life insurance, and pension plans are often made on a group basis. We will assume that Watson has weekly voluntary deductions of $10 for the United Fund and $5 for union dues.

NET PAY

•Alternative Terminology Net pay is also called take‐home pay.

Academy Company determines net pay by subtracting payroll deductions from gross earnings. Illustration I-6 (page I‐5) shows the computation of Watson’s net pay for the pay period.

Illustration I-6 Computation of net pay

Assuming that Michael Watson’s wages for each week during the year are $552, total wages for the year are $28,704 (52 × $552). Thus, all of Watson’s wages are subject to FICA tax during the year. In comparison, let’s assume that Watson’s department head earns $3,000 per week, or $156,000 for the year. In this case, the department head’s FICA taxes are $9,516 ([$117,000 × 6.20%] + [$156,000 × 1.45%].

Recording the Payroll

Recording the payroll involves maintaining payroll department records, recognizing payroll expenses and liabilities, and recording payment of the payroll.

MAINTAINING PAYROLL DEPARTMENT RECORDS

To comply with state and federal laws, an employer must keep a cumulative record of each employee’s gross earnings, deductions, and net pay during the year. The record that provides this information is the employee earnings record. Illustration I-7 shows Michael Watson’s employee earnings record.

Illustration I-7 Employee earnings record

Companies keep a separate earnings record for each employee, and update these records after each pay period. The employer uses the cumulative payroll data on the earnings record to (1) determine when an employee has earned the maximum earnings subject to FICA taxes, (2) file state and federal payroll tax returns (as explained later), and (3) provide each employee with a statement of gross earnings and tax withholdings for the year. Illustration I-11 on page I‐10 shows this statement.)

In addition to employee earnings records, many companies find it useful to prepare a payroll register. This record accumulates the gross earnings, deductions, and net pay by employee for each pay period. It provides the documentation for preparing a paycheck for each employee.Illustration I-8 presents Academy Company’s payroll register. It shows the data for Michael Watson in the wages section. In this example, Academy Company’s total weekly payroll is $17,210, as shown in the Salaries and Wages Expense column.

Illustration I-8 Payroll register

Note that this record is a listing of each employee’s payroll data for the pay period. In some companies, a payroll register is a journal or book of original entry; postings are made from the payroll register directly to ledger accounts. In other companies, the payroll register is a memorandum record that provides the data for a general journal entry and subsequent posting to the ledger accounts. At Academy Company, the latter procedure is followed.

RECOGNIZING PAYROLL EXPENSES AND LIABILITIES

From the payroll register in Illustration I-8 Academy Company makes a journal entry to record the payroll. For the week ending January 14, the entry is:

The company credits specific liability accounts for the mandatory and voluntary deductions made during the pay period. In the example, Academy debits Salaries and Wages Expense for the gross earnings of its employees. The amount credited to Salaries and Wages Payable is the sum of the individual checks the employees will receive.

RECORDING PAYMENT OF THE PAYROLL

A company makes payments by check (or electronic funds transfer) either from its regular bank account or a payroll bank account. Each paycheck is usually accompanied by a detachable statement of earnings document. This shows the employee’s gross earnings, payroll deductions, and net pay, both for the period and for the year‐to‐date. Academy Company uses its regular bank account for payroll checks. Illustration I-9 shows the paycheck and statement of earnings for Michael Watson.

Illustration I-9 Paycheck and statement of earnings

• HELPFUL HINT None of the income tax liabilities result in payroll tax expense for the employer because the employer is acting only as a collection agent for the government.

Following payment of the payroll, the company enters the check numbers in the payroll register. Academy Company records payment of the payroll as follows.

When a company uses currency in payment, it prepares one check for the payroll’s total amount of net pay. The company cashes this check and inserts the coins and currency in individual pay envelopes for disbursement to individual employees.

Employer Payroll Taxes

Learning Objective 2

Describe and record employer payroll taxes.

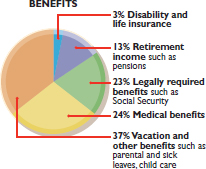

Payroll tax expense for businesses results from three taxes that governmental agencies levy on employers. These taxes are (1) FICA, (2) federal unemployment tax, and (3) state unemployment tax. These taxes, plus such items as paid vacations and pensions, are collectively referred to as fringe benefits. As indicated earlier, the cost of fringe benefits in many companies is substantial. The pie chart in the margin shows the pieces of the benefits “pie.”

FICA Taxes

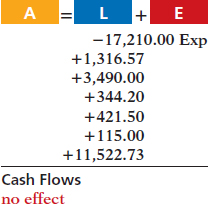

Each employee must pay FICA taxes. In addition, employers must match each employee’s FICA contribution. The matching contribution results in payroll tax expense to the employer. The employer’s tax is subject to the same rate and maximum earnings as the employee’s. The company uses the same account, FICA Taxes Payable, to record both the employee’s and the employer’s FICA contributions. For the January 14 payroll, Academy Company’s FICA tax contribution is $1,316.57 ($17,210.00 × 7.65%).

Federal Unemployment Taxes

The Federal Unemployment Tax Act (FUTA) is another feature of the federal Social Security program. Federal unemployment taxes provide benefits for a limited period of time to employees who lose their jobs through no fault of their own. The FUTA tax rate is 6.2% of taxable wages. The taxable wage base is the first $7,000 of wages paid to each employee in a calendar year. Employers who pay the state unemployment tax on a timely basis will receive an offset credit of up to 5.4%. Therefore, the net federal tax rate is generally 0.8% (6.2% − 5.4%).This rate would equate to a maximum of $56 of federal tax per employee per year (.008 × $7,000). State tax rates are based on state law.

• HELPFUL HINT Both the employer and employee pay FICA taxes. Federal unemployment taxes and (in most states) the state unemployment taxes are borne entirely by the employer.

The employer bears the entire federal unemployment tax. There is no deduction or withholding from employees. Companies use the account Federal Unemployment Taxes Payable to recognize this liability. The federal unemployment tax for Academy Company for the January 14 payroll is $137.68 ($17,210.00 × 0.8%).

State Unemployment Taxes

All states have unemployment compensation programs under state unemployment tax acts (SUTA). Like federal unemployment taxes, state unemployment taxes provide benefits to employees who lose their jobs. These taxes are levied on employers.2 The basic rate is usually 5.4% on the first $7,000 of wages paid to an employee during the year. The state adjusts the basic rate according to the employer’s experience rating. Companies with a history of stable employment may pay less than 5.4%. Companies with a history of unstable employment may pay more than the basic rate. Regardless of the rate paid, the company’s credit on the federal unemployment tax is still 5.4%.

Companies use the account State Unemployment Taxes Payable for this liability. The state unemployment tax for Academy Company for the January 14 payroll is $929.34 ($17,210.00 × 5.4%). Illustration I-10 (page I‐9) summarizes the types of employer payroll taxes.

2 In a few states, the employee is also required to make a contribution. In this textbook, including the homework, we will assume that the tax is only on the employer.

Illustration I-10 Employer payroll taxes

Recording Employer Payroll Taxes

Companies usually record employer payroll taxes at the same time they record the payroll. The entire amount of gross pay ($17,210.00) shown in the payroll register in Illustration I-8 (page I‐6) is subject to each of the three taxes mentioned above. Accordingly, Academy records the payroll tax expense associated with the January 14 payroll with the entry shown below.

Note that Academy uses separate liability accounts instead of a single credit to Payroll Taxes Payable. Why? Because these liabilities are payable to different taxing authorities at different dates. Companies classify the liability accounts in the statement of financial position as current liabilities since they will be paid within the next year. They classify Payroll Tax Expense on the income statement as an operating expense.

Filing and Remitting Payroll Taxes

Preparation of payroll tax returns is the responsibility of the payroll department. The treasurer’s department makes the tax payment. Much of the information for the returns is obtained from employee earnings records.

For purposes of reporting and remitting to the IRS, the company combines the FICA taxes and federal income taxes that it withheld. Companies must report the taxes quarterly, no later than one month following the close of each quarter. The remitting requirements depend on the amount of taxes withheld and the length of the pay period. Companies remit funds through deposits in either a Federal Reserve bank or an authorized commercial bank.

• HELPFUL HINT Employers generally transmit their W‐2s to the government electronically. The taxing agencies store the information in their computer systems for subsequent comparison against earnings and taxes withheld reported on employees’ income tax returns.

Companies generally file and remit federal unemployment taxes annually on or before January 31 of the subsequent year. Earlier payments are required when the tax exceeds a specified amount. Companies usually must file and pay state unemployment taxes by the end of the month following each quarter. When payroll taxes are paid, companies debit payroll liability accounts, and credit Cash.

Employers also must provide each employee with a Wage and Tax Statement (Form W-2) by January 31 following the end of a calendar year. This statement shows gross earnings, FICA taxes withheld, and income taxes withheld for the year. The required W-2 form for Michael Watson, using assumed annual data, is shown in Illustration I-11. The employer must send a copy of each employee’s Wage and Tax Statement (Form W-2) to the Social Security Administration. This agency subsequently furnishes the Internal Revenue Service with the income data required.

Illustration I-11 W-2 form

Internal Control for Payroll

Learning Objective 3

Discuss the objectives of internal control for payroll.

Chapter 7 introduced internal control. As applied to payrolls, the objectives of internal control are (1) to safeguard company assets against unauthorized payments of payrolls, and (2) to ensure the accuracy and reliability of the accounting records pertaining to payrolls.

Irregularities often result if internal control is lax. Frauds involving payroll include overstating hours, using unauthorized pay rates, adding fictitious employees to the payroll, continuing terminated employees on the payroll, and distributing duplicate payroll checks. Moreover, inaccurate records will result in incorrect paychecks, financial statements, and payroll tax returns.

Payroll activities involve four functions: hiring employees, timekeeping, preparing the payroll, and paying the payroll. For effective internal control, companies should assign these four functions to different departments or individuals. Illustration I-12 (page I-11) highlights these functions and illustrates their internal control features.

Illustration I-12 Internal control for payroll

REVIEW

LEARNING OBJECTIVES REVIEW

- Compute and record the payroll for a pay period. The computation of the payroll involves gross earnings, payroll deductions, and net pay. In recording the payroll, Salaries and Wages Expense is debited for gross earnings, individual tax and other liability accounts are credited for payroll deductions, and Salaries and Wages Payable is credited for net pay. When the payroll is paid, Salaries and Wages Payable is debited, and Cash is credited.

- Describe and record employer payroll taxes. Employer payroll taxes consist of FICA, federal unemployment taxes, and state unemployment taxes. The taxes are usually accrued at the time the payroll is recorded by debiting Payroll Tax Expense and crediting separate liability accounts for each type of tax.

- Discuss the objectives of internal control for payroll. The objectives of internal control for payroll are (1) to safeguard company assets against unauthorized payments of payrolls, and (2) to ensure the accuracy and reliability of the accounting records pertaining to payrolls.

GLOSSARY REVIEW

- Bonus

- Compensation to management personnel and other employees, based on factors such as increased sales or the amount of net income. (p. I-2).

- Employee earnings record

- A cumulative record of each employee’s gross earnings, deductions, and net pay during the year. (p. I-5).

- Federal unemployment taxes

- Taxes imposed on the employer that provide benefi ts for a limited time period to employees who lose their jobs through no fault of their own. (p. I-8).

- Fees

- Payments made for the services of professionals. (p. I-1).

- FICA taxes

- Taxes designed to provide workers with supplemental retirement, employment disability, and medical benefi ts. (p. I-2).

- Gross earnings

- Total compensation earned by an employee. (p. I-1).

- Net pay

- Gross earnings less payroll deductions. (p. I-4).

- Payroll deductions

- Deductions from gross earnings to determine the amount of a paycheck. (p. I-2).

- Payroll register

- A payroll record that accumulates the gross earnings, deductions, and net pay by employee for each pay period. (p. I-6).

- Salaries

- Specifi ed amount per month or per year paid to managerial, administrative, and sales personnel. (p. I-1).

- Statement of earnings

- A document attached to a paycheck that indicates the employee’s gross earnings, payroll deductions, and net pay. (p. I-7).

- State unemployment taxes

- Taxes imposed on the employer that provide benefi ts to employees who lose their jobs. (p. I-8).

- Wage and Tax Statement (Form W-2)

- A form showing gross earnings, FICA taxes withheld, and income taxes withheld which is prepared annually by an employer for each employee. (p. I-10).

- Wages

- Amounts paid to employees based on a rate per hour or on a piece-work basis. (p. I-1).

WileyPLUS

Many more resources are available for practice in WileyPLUS.

QUESTIONS

What is the difference between gross pay and net pay? Which amount should a company record as wages or salaries expense?

Which payroll tax is levied on both employers and employees?

Are the federal and state income taxes withheld from employee paychecks a payroll tax expense for the employer? Explain your answer.

What do the following acronyms stand for: FICA, FUTA, and SUTA?

What information is shown on a W-2 statement?

Distinguish between the two types of payroll deductions and give examples of each.

What are the primary uses of the employee earnings record?

(a) Identify the three types of employer payroll taxes. (b) How are tax liability accounts and Payroll Tax Expense classified in the financial statements?

You are a newly hired accountant with Spindle Company. On your first day, the controller asks you to identify the main internal control objectives related to payroll accounting. How would you respond?

What are the four functions associated with payroll activities?

BRIEF EXERCISES

Compute gross earnings and net pay.

BE10-1 Wade Yeo’s regular hourly wage rate is $16, and he receives an hourly rate of $24 for work in excess of 40 hours. During a January pay period, Wade works 47 hours. Wade’s federal income tax withholding is $95, he has no voluntary deductions, and the FICA tax rate is 7.65%. Compute Wade Yeo’s gross earnings and net pay for the pay period.

Record a payroll and the payment of wages.

BE10-2 Data for Wade Yeo are presented in BEI-1. Prepare the journal entries to record (a) Wade’s pay for the period and (b) the payment of Wade’s wages. Use January 15 for the end of the pay period and the payment date.

Record employer payroll taxes.

BE10-3 In January, gross earnings in Padgett Company totaled $79,000. All earnings are subject to 7.65% FICA taxes, 5.4% state unemployment taxes, and 0.8% federal unemployment taxes. Prepare the entry to record January payroll tax expense.

Identify payroll functions.

BE10-4 Rahman Company has the following payroll procedures.

- Supervisor approves overtime work.

- The human resources department prepares hiring authorization forms for new hires.

- A second payroll department employee verifies payroll calculations.

- The treasurer’s department pays employees.

Identify the payroll function to which each procedure pertains.

EXERCISES

Compute net pay and record pay for one employee.

E1-1 Gabrielle Osmon’s regular hourly wage rate is $14, and she receives a wage of 1½ times the regular hourly rate for work in excess of 40 hours. During a March weekly pay period, Gabrielle worked 46 hours. Her gross earnings prior to the current week were $6,000. Gabrielle is married and claims three withholding allowances. Her only voluntary deduction is for group hospitalization insurance at $30 per week.

Instructions

- Compute the following amounts for Gabrielle’s wages for the current week.

- Gross earnings.

- FICA taxes. (Assume a 7.65% rate on maximum of $117,000.)

- Federal income taxes withheld. (Use the withholding table in Illustration I-5, page I-4.)

- State income taxes withheld. (Assume a 2.0% rate.)

- Net pay.

- Record Gabrielle’s pay.

Compute maximum FICA deductions.

EI-2 Employee earnings records for Slaymaker Company reveal the following gross earnings for four employees through the pay period of December 15.

| J. Seligman | $93,500 | L. Marshall | $115,100 |

| R. Eby | $113,600 | T. Olson | $120,000 |

For the pay period ending December 31, each employee’s gross earnings is $4,500. The FICA tax rate is 7.65% on gross earnings of $117,000.

Instructions

Compute the FICA withholdings that should be made for each employee for the December 31 pay period. (Show computations.)

Prepare payroll register and record payroll and payroll tax expense.

EI-3 Welstead Company has the following data for the weekly payroll ending January 31.

Employees are paid 1½ times the regular hourly rate for all hours worked in excess of 40 hours per week. FICA taxes are 7.65% on the first $117,000 of gross earnings and 1.45% in excess of $117,000. Welstead Company is subject to 5.4% state unemployment taxes on the first $9,800 and 0.8% federal unemployment taxes on the first $7,000 of gross earnings.

Instructions

- Prepare the payroll register for the weekly payroll.

- Prepare the journal entries to record the payroll and Welstead’s payroll tax expense.

Compute missing payroll amounts and record payroll.

EI-4 Selected data from a February payroll register for Halverson Company are presented below. Some amounts are intentionally omitted.

FICA taxes are 7.65%. State income taxes are 4% of gross earnings.

Instructions

- Fill in the missing amounts.

- Journalize the February payroll and the payment of the payroll.

Determine employer’s payroll taxes; record payroll tax expense.

EI-5 According to a payroll register summary of Brand Company, the amount of employees’ gross pay in December was $850,000, of which $61,000 was not subject to Social Security taxes of 6.2% and $780,000 was not subject to state and federal unemployment taxes.

Instructions

- Determine the employer’s payroll tax expense for the month, using the following rates: Social Security tax rate 6.2%, Medicare tax rate 1.45%, state unemployment 5.4%, and federal unemployment 0.8%.

- Prepare the journal entry to record December payroll tax expense.

PROBLEMS: SET A

Prepare payroll register and payroll entries.

PI-1A Ethridge Drug Store has four employees who are paid on an hourly basis plus time-and-a-half for all hours worked in excess of 40 a week. Payroll data for the week ended February 15, 2017, are presented below.

| Employees | Hours Worked | Hourly Rate | Federal Income Tax Withholdings | United Fund |

|---|---|---|---|---|

| A. Joseph | 38 | $14.00 | $? | $–0– |

| J. Wilgus | 42 | $13.00 | ? | 5.00 |

| P. Kirk | 44 | $12.00 | 57.00 | 7.50 |

| L. Zhang | 48 | $12.00 | 52.00 | 5.00 |

Joseph and Wilgus are married. They claim 2 and 4 withholding allowances, respectively. The following tax rates are applicable: FICA 7.65% on all wages, state income taxes 3%, state unemployment taxes 5.4%, and federal unemployment 0.8%.

Instructions

- Prepare a payroll register for the weekly payroll. (Use the wage-bracket withholding table in Illustration I-5 on page I-4 for federal income tax withholdings.)

- Journalize the payroll on February 15, 2017, and the accrual of employer payroll taxes.

- Journalize the payment of the payroll on February 16, 2017.

- Journalize the deposit in a Federal Reserve bank on February 28, 2017, of the FICA and federal income taxes payable to the government.

Journalize payroll transactions and adjusting entries.

PI-2A The following payroll liability accounts are included in the ledger of Stockbridge Company on January 1, 2017.

| FICA Taxes Payable | $662.20 |

| Federal Income Taxes Payable | 1,254.60 |

| State Income Taxes Payable | 102.15 |

| Federal Unemployment Taxes Payable | 312.00 |

| State Unemployment Taxes Payable | 1,954.40 |

| Union Dues Payable | 250.00 |

| U.S. Savings Bonds Payable | 350.00 |

In January, the following transactions occurred.

| Jan. | 10 | Sent check for $250.00 to union treasurer for union dues. |

| 12 | Deposited check for $1,916.80 in Federal Reserve bank for FICA taxes and federal income taxes withheld. | |

| 15 | Purchased U.S. Savings Bonds for employees by writing check for $350.00. | |

| 17 | Paid state income taxes withheld from employees. | |

| 20 | Paid federal and state unemployment taxes. | |

| 31 | Completed monthly payroll register, which shows salaries and wages $46,200, FICA taxes withheld $3,534.30, federal income taxes payable $1,770, state income taxes payable $360, union dues payable $400, United Fund contributions payable $1,800, and net pay $38,335.70. | |

| 31 | Prepared payroll checks for the net pay and distributed checks to employees. |

At January 31, the company also makes the following accrual for employer payroll taxes: FICA taxes 7.65%, state unemployment taxes 5.4%, and federal unemployment taxes 0.8%.

Instructions

- Journalize the January transactions.

- Journalize the adjustments pertaining to employee compensation at January 31.

Prepare entries for payroll and payroll taxes; prepare W-2 data.

PI-3A For the year ended December 31, 2017, D. Pienkos Company reports the following summary payroll data.

D. Pienkos Company’s payroll taxes are Social Security tax 6.2%, Medicare tax 1.45%, state unemployment 2.5% (due to a stable employment record), and 0.8% federal unemployment. Gross earnings subject to Social Security taxes of 6.2% total $450,000 and gross earnings subject to unemployment taxes total $110,000.

Instructions

- Prepare a summary journal entry at December 31 for the full year’s payroll.

- Journalize the adjusting entry at December 31 to record the employer’s payroll taxes.

- The W-2 Wage and Tax Statement requires the following dollar data.

Complete the required data for the following employees.

Identify internal control weaknesses and make recommendations for improvement.

PI-4A The payroll procedures used by three different companies are described below.

- In Watson Company, each employee is required to mark on a clock card the hours worked. At the end of each pay period, the employee must have this clock card approved by the department manager. The approved card is then given to the payroll department by the employee. Subsequently, the treasurer’s department pays the employee by check.

- In Blasin Computer Company, clock cards and time clocks are used. At the end of each pay period, the department manager initials the cards, indicates the rates of pay, and sends them to payroll. A payroll register is prepared from the cards by the payroll department. Cash equal to the total net pay in each department is given to the department manager, who pays the employees in cash.

- In Forseth Company, employees are required to record hours worked by “punching” clock cards in a time clock. At the end of each pay period, the clock cards are collected by the department manager. The manager prepares a payroll register in duplicate and forwards the original to payroll. In payroll, the summaries are checked for mathematical accuracy, and a payroll supervisor pays each employee by check.

Instructions

Indicate the weakness(es) in internal control in each company.

Indicate the weakness(es) in internal control in each company.- For each weakness, describe the control procedure(s) that will provide effective internal control. Use the following format for your answer:

PROBLEMS: SET B

Prepare payroll register and payroll entries.

PI-1B Ralph’s Hardware has four employees who are paid on an hourly basis plus time-and-a half for all hours worked in excess of 40 a week. Payroll data for the week ended March 15, 2017, are presented below.

| Employee | Hours Worked | Hourly Rate | Federal Income Tax Withholdings | United Fund |

|---|---|---|---|---|

| K. Litwack | 40 | $15 | $? | $5 |

| E. Burgess | 46 | 13 | ? | 5 |

| R. Perez | 44 | 13 | 60 | 8 |

| H. Hosseini | 48 | 13 | 67 | 5 |

Litwack and Burgess are married. They claim 1 and 3 withholding allowances, respectively. The following tax rates are applicable: FICA 7.65% on all wages, state income taxes 4.5%, state unemployment taxes 5.4%, and federal unemployment 0.8%.

Instructions

- Prepare a payroll register for the weekly payroll. (Use the wage-bracket withholding table in Illustration I-5 on page I-4 for federal income tax withholdings.)

- Journalize the payroll on March 15, 2017, and the accrual of employer payroll taxes.

- Journalize the payment of the payroll on March 16, 2017.

- Journalize the deposit in a Federal Reserve bank on March 31, 2017, of the FICA and federal income taxes payable to the government.

Journalize payroll transactions and adjusting entries.

PI-2B The following payroll liability accounts are included in the ledger of Marcus Company on January 1, 2017.

| FICA Taxes Payable | $760.00 |

| Federal Income Taxes Payable | 1,204.60 |

| State Income Taxes Payable | 108.95 |

| Federal Unemployment Taxes Payable | 288.95 |

| State Unemployment Taxes Payable | 1,954.40 |

| Union Dues Payable | 740.00 |

| U.S. Savings Bonds Payable | 360.00 |

In January, the following transactions occurred.

| Jan. | 10 | Sent check for $250.00 to union treasurer for union dues. |

| 12 | Deposited check for $1,916.80 in Federal Reserve bank for FICA taxes and federal income taxes withheld. | |

| 15 | Purchased U.S. Savings Bonds for employees by writing check for $350.00. | |

| 17 | Paid state income taxes withheld from employees. | |

| 20 | Paid federal and state unemployment taxes. | |

| 31 | Completed monthly payroll register, which shows salaries and wages $46,200, FICA taxes withheld $3,534.30, federal income taxes payable $1,770, state income taxes payable $360, union dues payable $400, United Fund contributions payable $1,800, and net pay $38,335.70. | |

| 31 | Prepared payroll checks for the net pay and distributed checks to employees. |

At January 31, the company also makes the following accrued adjustment for employer payroll taxes: FICA taxes 7.65%, federal unemployment taxes 0.8%, and state unemployment taxes 5.4%.

Instructions

- Journalize the January transactions.

- Journalize the adjustments pertaining to employee compensation at January 31.

Prepare entries for payroll and payroll taxes; prepare W-2 data.

PI-3B For the year ended December 31, 2017, Grayson Electrical Repair Company reports the following summary payroll data.

Grayson Company’s payroll taxes are Social Security tax 6.2%, Medicare tax 1.45%, state unemployment 2.5% (due to a stable employment record), and 0.8% federal unemployment. Gross earnings subject to Social Security taxes of 6.2% total $470,000, and gross earnings subject to unemployment taxes total $125,000.

Instructions

- Prepare a summary journal entry at December 31 for the full year’s payroll.

- Journalize the adjusting entry at December 31 to record the employer’s payroll taxes.

- The W-2 Wage and Tax Statement requires the following dollar data.

Complete the required data for the following employees.

Identify internal control weaknesses and make recommendations for improvement.

PI-4B Selected payroll procedures of Schuster Company are described below.

- Department managers interview applicants and on the basis of the interview either hire or reject the applicants. When an applicant is hired, the applicant fills out a W-4 form (Employee’s Withholding Allowance Certificate). One copy of the form is sent to the human resources department, and one copy is sent to the payroll department as notice that the individual has been hired. On the copy of the W-4 sent to payroll, the managers manually indicate the hourly pay rate for the new hire.

- The payroll checks are manually signed by the chief accountant and given to the department managers for distribution to employees in their department. The managers are responsible for seeing that any absent employees receive their checks.

- There are two clerks in the payroll department. The payroll is divided alphabetically; one clerk has employees A to L and the other has employees M to Z. Each clerk computes the gross earnings, deductions, and net pay for employees in the section and posts the data to the employee earnings records.

Instructions

- Indicate the weaknesses in internal control.

- For each weakness, describe the control procedures that will provide effective internal control. Use the following format for your answer: