9

ATTRACTING AND USING INVESTOR MONEY TO INCREASE YOUR PROFITS

There are many passive investors who have their cash in a low-yielding bank account or who are unhappy with their returns in the stock market. Others may now own investment real estate but want to retire from active management.

They are looking for an alternate and safe investment with a reasonable return. They have no interest in doing the work it takes to buy and manage a property but could be interested in investing with someone who would do all of the work.

If you have the knowledge and ability to buy and manage a house that will produce a profit but are short on cash to buy property, then investing with others can benefit you both. You can buy property that you could not buy without an investor. The investor can participate in the profits that the property produces and earn a better return.

IDENTIFYING POTENTIAL INVESTORS

Suppose that you find a great buy and need money for a down payment. Make a list of people who you know who like real estate and believe that it is a good investment. They do not invest in real estate because they don’t want to deal with the tenants, nor do they want to negotiate the purchase and sale of a house. They don’t know how to make a good buy or manage tenants, and they won’t take the time to learn—but they are great prospects as passive investors.

There are four traits important in any potential investor:

• Honesty

• Intelligence

• A long-term outlook

• Enough money or credit to acquire a house

Never get involved with someone who has to borrow the money to invest.

Consider whom you now know who has these traits and who may want to invest with you. They may be any of the following:

• Business associates—employer, employees, landlord

• People to whom you now owe money

• Family members who need a better return on their money

• Other investors who buy in your town

You may also want to consider those who know your business and may be able to refer others, such as …

• Your accountant

• Your attorney

• Your insurance agent

• A title company that you do business with

• A Realtor you do business with

• Contractors who do work for you

DON’T JUST ASK THEM IF THEY WOULD LIKE TO INVEST

Instead, you should find a house that you would like to buy and make an offer on it “subject to” arranging financing that is acceptable to you. After this is decided, you should talk to potential investors, show them your contract and the house. If they are interested, ask them if they would like to invest with you in this house if you agreed to take care of the management. Show them the estimated loan payments, gross rents, and expected expenses so that they understand how you will repay any money borrowed and how much cash flow the house will potentially produce.

If this is not a deal that they want today, ask if they know anyone who might be interested. Your time has not been wasted if they say no. They may be a potential investor for another deal in the future, and they may tell their friends about you.

Do not ask others to invest with you until you can buy at good prices and know how to manage. You build credibility with potential investors when you can talk about other property that you own and manage now.

ADVANTAGES TO USING AN INVESTOR’S CASH FOR THE DOWN PAYMENT

1. It does not have to be repaid until you sell the property.

2. You make no payments on it and pay no interest until you sell the property.

3. By using an investor’s cash to make a larger down payment and close quickly, you can negotiate a bigger discount on the price.

4. Using the investor’s cash for a larger down payment will reduce the debt on the property and increase the cash flow, making the house a safer investment.

As you start to invest, a source of money for down payments can allow you to buy property with less debt that will have more cash flow. If you buy a house with a low down payment and finance most of the purchase price, most if not all of your cash flow will go toward repaying the debt. If you borrow too much or borrow on bad terms, you may have to make an additional investment each month to pay the loan.

When an investor makes a larger down payment on the house, then the debt will be less, and the payments should be lower. This allows you to buy and have immediate cash flow.

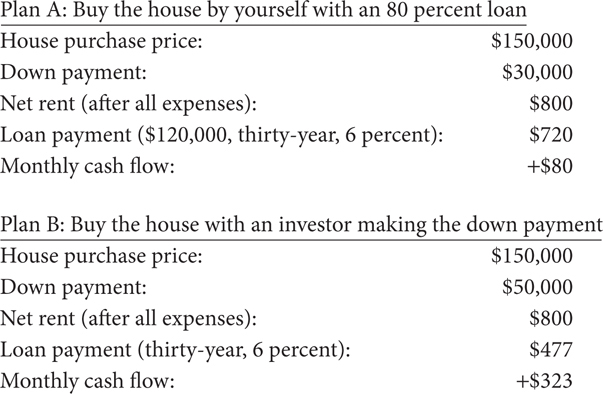

The example below shows a comparison between buying a house with high leverage by yourself and using an investor’s money for the down payment. This house had a fair market value of between $170,000 and $180,000.

Notice a couple of things. The larger down payments allow the borrower to get a better interest rate. If you could qualify for the lower rate yourself and you had the $30,000 down payment, I would advise you to buy this house by yourself.

Splitting Profits Fairly

With any joint venture, it is important to agree up front on how you will split profits. Many joint ventures pay the organizer and the manager of the investment both a commission and a share of the profits before the investor gets his money back or any share of the profit.

This seems unfair to the investor, who is taking most of the risk. A fairer approach is to split profits 50/50 with an investor, each participating in the cash flow, both positive and negative, and then returning the investor’s initial investment before splitting the profits on the sale 50/50.

This gives the buyer/manager the incentive to buy a property with profit potential and then manage it well, since he only gets paid as the property produces a profit.

If the investor participates in 50 percent of the cash flow and appreciation, each would receive half of the $323 a month and half of the eventual profit on the sale. You, as the manager, would have monthly cash flow and own half of a house with equity that will grow over time.

Although the cash flow is low in the first few years, it will increase with time and, in addition, the loan is being paid down each month and the property may appreciate with time. Never make a guarantee of profits. Show the actual numbers today, and then plan on holding a property until it doubles in value.

BOTH YOU AND THE INVESTOR SHARE TAX BENEFITS

Profit produced by buying the property below the market will be taxed at the lower capital gains rate. You and the investor also may be able to shelter some of your current income from taxes with the depreciation the house produces.

You will agree to find and buy the property, manage the property, and then—years from now—handle the sale. The investor’s part is to put up the down payment and, if necessary, qualify for and sign the loan. When you borrow using an investor, limit your loan to a maximum of 75 percent of the value of the house, and borrow for the longest term possible so that your rents will cover the payments. It will be a low-risk loan and should be an easy loan for any investor with good credit to obtain.

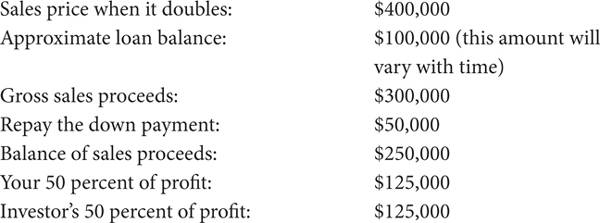

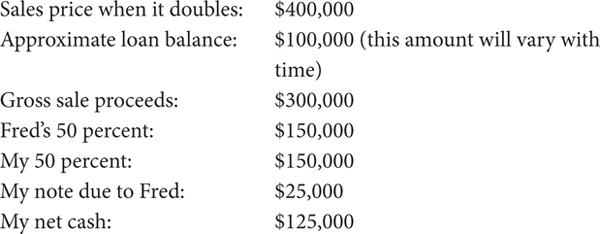

Your plan is to hold the house until it doubles in value, and then sell and split the profits with the investor 50/50, after repaying the down payment he made.

You hold the house until it doubles in value.

You made $125,000 plus half of the cash flow with no money invested, but you used your time and skill to find a good deal, buy it, and manage the property and the tenants. The investor made $125,000 plus half of the cash flow in profit on his $50,000 investment, without ever talking to a seller, tenant, or a buyer.

Finding a bargain, negotiating a below-market price and maybe great terms, managing the property well until it doubles in value, and then selling it for a retail price is worth a lot. Sharing half the profits when one party puts up the money and the other provides the brains is not fair. It’s a great deal for the investor. Do a good job finding and managing deals and you will have many people wanting to invest with you.

How much would an investor earn on $50,000 in a year where it is invested now, say, in a mutual fund or savings account? How much would they have in ten years? Compare that number with the return they would make owning half a house with you.

PROTECTING YOURSELF AND THE INVESTOR

There are several ways to hold title to a house with an investor. You want to protect both parties’ interests and use easy-to-understand documents and agreements.

A simple way to protect your interest is to be named on the title to the property. Document your agreement to manage the property with a short and clear management agreement. Because you are also an owner of the property, you would not need a real estate license to manage the property (a nonowner may need a license to manage investment real estate in some states).

HOLDING TITLE AS TENANTS IN COMMON

A simple way for you and investors to own a house together is to have the investor buy the house, finance it, and then deed to you an undivided one-half interest with the loan in place. All these papers can be signed at one meeting at the closing of the property and be recorded in the proper order in the public records. You then would be an undivided one-half owner on the public records, holding title as tenants in common.

This is not a partnership, and you should not call it a partnership, nor file a partnership tax return. Each owner actually owns an undivided half of the house. Each owns half the roof, half the lot, and so on.

Because you actually own one-half of a house, you could sell your half interest to another person, but few buyers are interested in buying half a house. The plan is to hold the whole house until you sell both halves to a new owner.

If something unexpected happens to your investor—he dies, loses a lawsuit, or files bankruptcy—then his half may be transferred to a new owner, but you would still own your half. An advantage of holding title as tenants in common is that claims against the investor’s half will not attach to the other half that you own.

All that is required to hold title as tenants in common is the proper language in the deed. You can go into title and borrow the money together to acquire the house. Or, as suggested earlier, the investor can go into title, borrow the money, and then deed one-half interest to you. If you buy and borrow together, then you will have to furnish financial statements and pay for credit reports and other expenses.

HOLDING TITLE IN A TRUST, CORPORATION, OR LLC

Another way to hold title that has the advantage of keeping the names of the owners off the public records is to form a trust, corporation, or limited-liability company (LLC) or limited-liability partnership (LLP) to own the property. These entities either can pass through the income and expenses to the owners or pay the taxes before making distributions. An advantage of using an entity that can be taxed as a partnership is that you can make disproportionate distributions of income and allocations of expenses.

These entities require documentation and you may be required to file an annual tax return. To be used wisely, they require a good understanding of how they work.

One disadvantage is that lenders often will not lend money on properties that are owned by trusts or other entities. The bankers may require you to hold the title personally to finance or refinance. Some states require you to use an attorney to evict tenants owned by corporations or LLCs. Insuring properties held in different entities may be a challenge. If using these entities to hold title sounds more complicated and expensive, it is.

When you are dealing with other people’s money, you want to be cautious, and you want to be sure that documents are prepared, executed, and recorded or filed properly. If you want to form a separate entity to hold title, find a competent attorney with lots of experience in forming these entities. There are advantages and disadvantages to taking title in a separate entity. Obtain both legal and tax advice before spending thousands of dollars to form and maintain an entity that you may not need.

MY FIRST INVESTOR AND THE DEALS THAT WE MADE

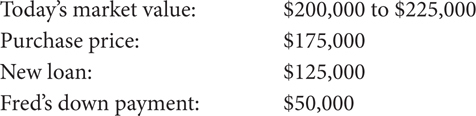

My first investor was Fred, a retired attorney with a good income and great credit. He understood real estate but had no interest in being an active investor with any management responsibilities.

I would find houses that he could buy at a bargain price, and then Fred would make the necessary down payment to get a low-interest-rate, long-term loan. Fred would close on the house in his name alone and acquire the new loan.

He then would deed me one-half interest in the house and we would own the house as tenants in common. I gave him my personal note (I.O.U.) for an amount equal to one-half of his down payment.

When we sold a property, we would split the proceeds and I would repay my note to him, which had no interest and required no payments, to repay my half of the down payment.

We hold the house until it doubles in value.

Fred has traded the interest he could collect on the $25,000 he loaned me to buy my half interest in the house for the profit he earned. We shared the cash flow the house produced while we owned it.

His return was greater than he could achieve with other investments and had less downside risk. Fred’s cash flow and long-term profit totaled more than 10 percent a year.

My profit of $125,000 was a great return, since I borrowed my share of the down payment from Fred. The proof that it was good for both of us is that we did it over and over again.

BORROWING FROM OTHER INVESTORS

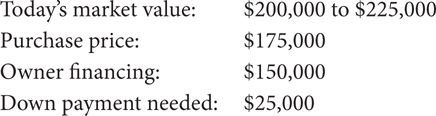

If you find an investor like Fred and make him money, he may be a source of financing to you for properties that you do not own together. Suppose that you found a house that you could buy from an owner who would finance most of the purchase price for you.

For example:

Your “Fred” would have confidence in your abilities and trust you after you have owned property together for a few years. He should be willing to lend you the $25,000 that you need to buy this house and take a note secured by the house at a reasonable interest rate.

BORROWING ON INTEREST-ONLY TERMS

When you borrow from an investor like Fred, the investor prefers to keep her capital invested. She doesn’t want you to amortize a loan, that is, pay back a little of the principal each month. She would prefer that you pay interest on the entire amount as long as you need her money.

When an investor sees that she can collect significantly more interest than the bank will pay her with an acceptable amount of risk, she will want to invest more with you.

Many people have money in self-directed retirement accounts or other accounts that they will need in the short run and are not willing to invest in property. They may be willing to invest in a relatively short-term (five to ten years) loan that would pay them more interest than they could earn in their bank account.

Bankers have high overhead and pay depositors a small fraction of what they charge their borrowers. If you cut out the middleman, the bank, you can borrow directly from depositors and pay them far more than the bank will. Investors can still be an affordable source of funds for you.

An additional advantage of borrowing from a private source is that you sometimes can negotiate a loan with no payments due until you sell the property. If your lender is a pension plan that is not going to distribute the income to the beneficiaries for ten more years, the fund doesn’t need the money back soon. The fund can make you a three-year loan with no payments for three years with interest to accrue that you could use to buy a property and repay it with interest when you sell.

The biggest concern of private lenders is getting their money back. They are not as concerned about earning a high rate of interest as they are in getting their money back. Oversecure any money that you borrow from a private lender. Give private lenders more than one property if you need to so that they will feel secure. A secure lender is a happy lender, who sleeps well, and such a lender will lend to you at a reasonable rate of interest.

Avoid lenders who charge high interest. Only a speculator who is buying and selling a property in a short time can afford these rates. The speculator is giving the lender a share of the profit and has to pay the high rate, because he is often borrowing near 100 percent of the purchase price. Buying and selling is much higher risk than buying and renting.

RULES FOR INVESTING WITH OTHERS

• Don’t buy properties that you don’t know how to manage.

• Do buy at a price and on terms that will produce cash flow.

• Don’t make projections.

• Never invest with someone who has to borrow the money to invest.

• Don’t overpromise.

• Do write down your agreement in such a way that it cannot be misunderstood in years to come.

• Protect your interest by taking title to half interest in the property to secure your interest.

• Protect the investor’s interest by having him on title for half interest, plus give the investor a note secured by your interest in the property to secure his cash invested.

• Account for and distribute income annually, and keep a cash reserve for unforeseen expenses.

Who You Invest with Is Important

• If the property needs financing, the investor should have great credit in order to get a low-interest-rate loan.

• Choose carefully: whom you do business with is more important than the deal.

• When a deal is too one-sided, it will go bad.

• Look for investors who can do more than one deal—who have what you need, lots of credit or lots of money

• Make every deal good for your investor and she will want to do another with you and she will tell her friends.