Understanding the European Financial System

Europe is comprised of a rich diversity of countries; however, one often becomes so familiar with national structures to the point of sometimes wrongly assuming that the reality is similar in the rest of Europe. The characteristics of mortgages and the use of bank accounts can be mentioned as two illustrative examples of the stark differences observed across countries.

In Spain and Ireland, virtually all mortgages are agreed with a rate that is adjusted to market conditions on an annual basis—using the Euribor or official rates as a reference. In countries like Belgium and Germany, however, the majority of mortgages are agreed with the interest rate fixed for as long as 10 years or even for the entire duration of the mortgage. The structure of mortgages and whether the rates are adjusted regularly or remain fixed for the entire life of the loan has an important impact on how risks are managed by banks across EU countries and on how movements in interest rates affect both the profitability of financial institutions and the capacity of households to consume and save.3

Similarly, one may have gotten so used to credit cards so as not to realize that, in a few European countries, up to 30 to 50 percent of the population did not have a bank account in 2011.4 The access to a bank account and the lack thereof have important implications on how payments are organized, on how savings can be channeled to investments or on the possibility of using the Internet for online purchases.

These two examples illustrate how the European financial sector can be very different and much more complex than what we apprehend from our own experience in a single country. A broad understanding of the functioning of the European financial sector is the starting point to grasp the circumstances leading to the crisis, how the crisis unfolded and the constraints faced by public authorities to confront it. Moreover, a general idea of the structure of the financial sector, in terms of the relative size of the various market segments and how they interact with each other, is crucial for understanding the reaction to the crisis.

Therefore, this chapter sets the context for understanding the rest of the book and is organized as follows: it first discusses how funds circulate across the economy (Section 1.1) and the size of the different sectors in terms of financial assets and liabilities (Section 1.2). Thereafter, the various instruments or financial products are presented (Section 1.3) as well as the different channels: financial intermediation (Section 1.4), direct financing through capital markets (Section 1.5) and direct financing through alternative channels (Section 1.6). The complexity of the interconnections among the different sectors and the implications are discussed in Section 1.7. Finally, Section 1.8 concludes. The chapter is complemented by four boxes presenting the institutional framework of the European Union (Box 1.1), discussing the role of the public sector (Box 1.2), presenting the various financial instruments and their main features (Box 1.3) and discussing financial and economic bubbles (Box 1.4). To complement the perspective provided in the main text, an annex presents a summary of the circulation of funds from the perspective of fund flows.5

Box 1.1 The European Framework

This book is about the response provided to the financial crisis from a European perspective. It is therefore important to clarify some particularities about how the European Union is structured and organized.

The Conferral of Powers to the EU

A sovereign State can regulate and intervene in any domain. However, the EU is bound by the explicit conferral of powers enshrined in the EU Treaties. The European authorities can only act in the areas for which the Member States have explicitly transferred competences—for instance, monetary policy in the euro area has explicitly been transferred to the European Central Bank. In most cases, competences are only partially transferred to the EU and they are, therefore, shared between the Member States and the EU.

When the competences are shared, the exact functions of the EU and the Member States are guided by the principles of subsidiarity and proportionality. Subsidiarity indicates that decisions should be taken as close as possible to citizens—for instance, by local or national governments. In other words, EU initiatives have to demonstrate the need to act in common or that the objectives set out in the Treaty6 cannot be achieved by only national actions. Proportionality means that no more than what is necessary to attain the objectives should be done at the supranational level.

A European directive sets out the principles and goals but allows Member States to define the means through the transposition of the directive into national legislation. A European regulation is directly applicable in all Member States and, therefore, it does not allow for a flexible adaptation to national specificities. Following the principle of proportionality, proposals for European regulations need to justify why a directive—or a recommendation—was considered insufficient to achieve the intended goals.

The foundations of the European project rely on a voluntary renunciation to sovereignty by the States, which is transferred, in specific areas, to the EU level. But this can only be done to achieve a benefit that needs to be accurately explained. Therefore, the principles of subsidiarity and proportionality are critical for the legitimacy of the European construction and they rely heavily on the trust on the other partners. The relevance of these principles has become clear during the recent refugees crisis when many countries restored border controls and even built new fences and walls.

On top of the subsidiarity and proportionality tests, any European proposal must pass through the legislative procedure. Draft legislative initiatives are presented by the European Commission (which represents the overall interest of the European Union), which are eventually adopted by the Council of the EU (which represents the Member States) and the European Parliament (which represents the citizens). The Council and the Parliament, acting as colegislators, can modify the Commission proposals by including amendments.

While in most areas the European Parliament is on equal footing with the Council, in a few other areas, decisions are taken on a more intergovernmental fashion with a prominent role of the Council and a much limited involvement of the Parliament.

Economic Decisions in the European Commission: Main Departments

Among the three main institutions of the EU (the Commission, the Council, and the Parliament), the European Commission is, by far, the largest. It is therefore important to understand how the Commission is organized internally in the area of economic and financial affairs.

The reaction to crisis stemmed mainly from three departments: the Directorate-General of Economic and Financial Affairs (DG ECFIN), which is in charge of monitoring macroeconomic developments across European countries; the Directorate-General for Internal Markets and Services (DG MARKT, later restructured into the Directorate-General for Financial Stability, Financial Services and Capital Markets Union or DG FISMA), which is in charge of the regulatory framework of financial services; and the Directorate-General for Competition (DG COMP), which is in charge of ensuring compliance with competition rules. The role of DG COMP consisted in striking the right balance between avoiding the distortions of the government support provided to financial institutions and allowing for certain flexibility in the interpretation of State aid rules to accommodate the extraordinary circumstances stemming from the financial turmoil.

The Circulation of Funds in an Economy

An economy can be schematically represented through five institutional sectors with specific roles. Corporations produce the goods and services that households consume. At the same time, households provide corporations with a workforce and capital in exchange for the payment of an income, either in the form of a salary or a dividend. Some market failures prevent corporations from providing certain goods and services that are then provided by the public sector. Examples of such services include defense or the establishment and enforcement of the general legal framework.7

Moreover, a financial sector is needed not only for managing the payment system but also to channel funds from savers to investment opportunities. This is done through financial intermediation and maturity transformation. Finally, an economy interacts with other countries. While those other countries can also be divided into the same four institutional sectors (households, corporations, public sector, and financial sector), the external sector is usually taken altogether in a miscellaneous “rest of the world ” category.

As can be deduced from the description of these sectors, they are all highly interdependent. As all economic sectors depend on each other, contagion through vicious and virtuous circles can multiply initial effects. Deep problems in one sector can be transmitted to other sectors and ultimately impact the whole economy. For instance, high unemployment rates can constrain the consumption capacity of households and therefore reduce corporations’ income. Given their decreasing income, households and corporations may encounter difficulties to repay their credits to the financial sector. Subsequently, public finance can be eroded by declining taxes due to the reduction in economic activity and increasing expenditure in the social safety net. Problems can also originate, however, in other parts of the economy, such as in an unstable political system unable to steer the economy or in a weak financial sector struggling to provide credit.

On the other hand, a specific strong sector can be an anchor for a virtuous circle and lead the recovery of the whole economy to pull it out of a recession. For instance, a strong external sector can boost exports and employment, and a strong public sector can temporarily substitute the lack of investment by corporations and of demand by households.

The interdependence among institutional sectors stems from bilateral interactions between individual agents (Figure 1.1). In modern economies, any real operation—like the provision of labor, provision of capital, sale of a product or service—is generally matched with a monetary payment in the form of salaries, dividends, or cash. It is very rare, however, that there is a perfect match between the moment the real operation occurs and the moment of payment. In most cases, there is a certain time lag, which means that the real operations are translated into temporary financial positions between creditors and debtors. These positions represent the commitment to make or receive a payment in the future. Similarly, the institutional sectors can save in the present—by generating financial claims—to increase their resources available for future payments. In other words, financial positions represent an intertemporal transfer of resources between economic agents. They are recorded in the balance sheet of the sector providing the funding as a financial asset, and in the balance sheet of the sector receiving the funding as a financial liability. When, in the future, the borrower pays back its debt to the creditor, the respective positions in the corresponding balance sheets cancel each other.

Figure 1.1 Economic sectors and interdependence

Any economy can be divided into four institutional sectors interconnected with each other and with the rest of the world.

Source: Own elaboration.

Note: NFCs: Nonfinancial corporations.

Barter economies, and even economies based exclusively on cash transactions, have significant limitations. The flexibility in payments stemming from the existence of financial positions allows modern economies to achieve high levels of development. However, the existence of financial positions requires high levels of trust; in other words, one economic agent will be willing to accept a postponement in the payment if she can trust her counterpart will honor the debt in the future. Trust, therefore, is the cornerstone of modern economies. A clear example of this high level of trust is our reliance on banknotes and even electronic money as our regular means of payment.

Trust is somehow formalized or ensured by contracts, the rule of law and the legal system. However, trust is much broader and engraved in the values and culture of societies. Trust can evaporate even without formal changes in contracts or laws; this was for instance the case during the financial turmoil of September 2008 when confidence in financial markets fell. Excessive indebtedness or excessive inflation may also erode trust; yet, it is extremely difficult to discern the boundaries beyond which borrowing or increasing prices could become problematic.

In short, financial positions—that is, temporarily lending and borrowing—contribute to the well-functioning of an economy by enabling an enhanced mobilization and allocation of resources. At the same time, financial positions may also pose some risks as they rely on trust, which can suddenly drop. Knowing the dynamics of financing positions in an economy contributes to better understanding the functioning of that economy, but also to identifying where potential risk may be building up.

The financing positions of the different sectors in an economy, as well as the channels throughout which financing flows, are summarized in Figure 1.2. In broad terms, agents with an excess of financial resources (savers or investors) will provide funds to other agents with a financing need (borrowers). Two economic agents may directly agree with each other about the terms and conditions of a financial transaction, like an intercompany loan. Such operations are, however, embedded with several constraints such as negotiation costs and limited liquidity.

Capital markets may solve some of these problems by providing flexibility both to investors and borrowers. For instance, investors do not need to stick to the overall maturity of the initial contract as they can sell their investment in shares or bonds in the secondary market in case they need liquidity. On the other hand, capital markets enable borrowers to access a wide pool of investors.

Figure 1.2 Circulation of funds in the economy: financing channels

Each institutional sector in the economy can provide and receive financing from other sectors. This can be done by the direct contact between two agents—sometimes using an organized market to meet—or through the intermediation of a financial institution.

Source: Own elaboration.

Notes: The height of each box is proportional to the actual size of the sector.

Nevertheless, not all financing needs and excess funds can be channeled and matched through direct interactions between agents or through financial markets. A household seeking to buy a house does not have the financial and technical capacity to issue securities in the markets. Moreover, most households and businesses do not have the capacity to assess the creditworthiness of a potential borrower. In this context, financial intermediaries provide additional flexibility in channeling funds from savers to borrowers by exerting two critical functions: maturity transformation and the assessment of the creditworthiness of potential borrowers. For instance, financial intermediation allows for a deposit placed by a household in a bank to be transformed into a mortgage to another household without a direct connection between the depositor and the mortgage borrower. In this context, financial intermediaries facilitate the mobilization of additional resources to be allocated to productive projects, which otherwise would remain idle.

Until now, we have seen that the existence of financial positions involves a provider of funds, a recipient, a channel, and an amount. Moreover, financial positions can take the form of different instruments, such as loans or bonds, with defined features in terms of maturity, repayment schedule and collateral, amongst others. The combination of these six main dimensions of financial positions—from whom, to whom, what, where, how, and how much (Table 1.1)—imply a dense network of bilateral relations. This chapter tries to disentangle the complexities of this network of interactions by quantifying and discussing the basic features of these various dimensions.

Box 1.2 The Role of the Public Sector

The main role of the public sector in an economy is to improve the allocation of resources and economic and social welfare. In general, an efficient allocation of resources can be achieved through market forces—that is, individuals acting in the pursuit of self-interest and meeting on a marketplace. However, a series of market failures prevent this to happen in many circumstances.

In certain cases, not all the costs or benefits are incurred or enjoyed by the parties providing or receiving a service. These are the so-called externalities, which can be positive—for instance, public safety—or negative—for instance, pollution. Internalities or asymmetric information—for instance, moral hazard and adverse selection—the existence of public goods, coordination failures and market power or distortions of competition—for instance, natural monopoles, abuse of dominant position, cartels, reduced competition—are additional market failures which lead to an inefficient allocation of resources and loss of welfare.

A public authority can intervene in different ways to address these market failures. It can pass and enforce legislation which set the rules of the game seeking to keep the system honest—competition enforcement—it can also directly provide certain goods and services—for instance, education, health, or social protection—or it can use taxes and subsidies to internalize the externalities.

The public sector may also redistribute income to improve social welfare. Finally, it can implement macroeconomic interventions to overcome prolonged recessions and reduce unemployment. Indeed, the public sector plays a crucial role in smoothing the economic cycle by embarking in countercyclical policies, including automatic stabilizers. This is why it constitutes a cornerstone for an economy to address and overcome a crisis.

Economies evolve through recurring expansionary—contractionary cycles. Public finances help smooth these cycles by taxing profits during economic expansions and by providing social protection and not taxing losses during economic downturns (Figure B.1). These effects are usually referred to as automatic stabilisers.

In order not to run into problems during contractions, the public sector needs to save during the expansionary phase of the cycle. In other words, periods of economic expansions have to be used by the public sector to reduce its debt and get ready to confront the next crisis with sound public accounts. However, maintaining fiscal discipline is challenging. A public sector running surpluses usually receives pressure to transfer these extra resources back to the economy either by reducing taxes or by investing or spending those surpluses. Therefore, it is not always easy for a government to find the right balance between preparing for a future crisis—by reducing public debt—and supporting the economy during the expansionary phase of the cycle.

Figure B.1 The public sector and the economic cycle

The economy evolves in cycles. The intervention of a public sector contributes to smoothing the magnitude of the cycle.

Source: Own elaboration.

Table 1.1 Financial relations in an economy: dimensions

Who? Institutional sector |

What? Instrument or product |

Where? Geography |

How much? Measurement |

Households Nonfinancial corporations (NFCs) Governments Monetary and Financial Institutions (MFIs) Central banks Credit institutions Money Market Funds (MMFs) Insurance Corporations and Pension Funds (ICPFs) Insurance corporations (ICs) Pension Funds (PFs) Other Financial Institutions (OFIs) Investment funds (IFs) Financial Vehicle Corporations (FVCs) Miscellaneous financial intermediaries Nonresidents (RoW) |

Loans Bonds Quoted shares Unquoted shares Deposits Ins. technical Reserves Other assets/liabilities |

European Union Euro area Member States (28) |

Absolute terms (Euro) Relative terms Percentage of GDP Percentage of balance sheet Growth rates |

How? Circulation of funds |

When? Time |

How much? Variable |

|

Direct financing Through markets Outside markets Financial intermediation |

Historical perspective Annual series Monthly series |

Stocks (outstanding volumes) Flows Gross issuances Redemptions Net issuances |

Data on financial relations are defined through a number of dimensions including the institutional sector, the type of product and the location, among others.

Source: Own elaboration.

The Size of the Institutional Sectors

Total Positions: Assets and Liabilities

In 2015, the euro area economy had a total size, in terms of aggregated (financial) balance sheet of all institutional sectors, of more than €130,000 billion and more than 13 times annual GDP.8 Between 2000 and 2015, the total financial position of euro area sectors more than doubled. This implies a much faster growth than nominal GDP, which only grew by 50 percent. As a consequence, the relative size of the financial positions with respect to the production—that is, the leverage—increased, particularly after 2005 (Figure 1.3).

Figure 1.3 Balance sheet of the institutional sectors, outstanding amounts, euro area, € billion

The institutional sectors have different sizes in terms of financial assets and liabilities. Overall, the total financing position (balance sheet) of euro area institutional sectors has expanded, particularly since 2004.

Source: ECB, Eurostat, and own calculations.

Notes: RoW: Rest of the world. Nonfinancial assets (such as buildings and machinery, land) are not reported.

Financial corporations represent about half of the financial assets and liabilities of the economy. Concerns have been raised about the potential excessive size of the banking system in Europe.9 Although the relative size of the financial sector increased between 2000 and 2010, a slight decline can be observed thereafter. This is mainly explained by the process of deleveraging undertaken by banks in Europe.

Households and nonfinancial corporations (NFCs) represent about 15 percent of total financial assets each. Their joint relative size has significantly declined from representing almost 40 percent of the euro area economy in the early 2000s to about 30 percent in the last few years. The financial balance sheet of the public sector is much smaller. Finally, non-euro area residents contribute to the euro area economy by providing about 15 percent of financial assets and liabilities. These are mainly financial corporations from world financial centers such as the UK or the US; their relative importance has continuously expanded from representing about 10 percent in 2000 to more than 16 percent in 2015.

Following the outbreak of the crisis, a debate emerged about whether indebtedness or leverage had become excessive so as to negatively affect confidence. Several voices argued about the need to reduce the indebtedness of the different agents or “deleverage.” Throughout the crisis, however, there were no signs to indicate such a trend. For instance, the 16th Geneva Report on the World Economy10 argues that, despite the length and depth of the crisis, the world has not yet begun to deleverage; global debt-to-GDP is still growing, breaking new heights (page 1). The Geneva report also indicates that deleveraging interacts in a vicious loop with slow nominal growth, as the latter makes the deleveraging process harder and the former exacerbates the economic slowdown (page 2).11 Eventually, according to the latest data, some signs of declining leverage seem to be emerging.

Net Financial Positions

The difference between financial assets and financial liabilities, or net financial worth, indicates the cumulative net contribution to the financing of the economy provided by each financial sector. When a sector has a positive net financial worth, it provides financing to other sectors. When net financing worth is negative, the sector is absorbing financing, in other words, it has a financing need to be covered by borrowing from other sectors.

Households are the main provider of funding to the economy. Households’ net savings represented more than 140 percent of GDP in 2015 and originated most of the financing created in the euro area economy throughout the crisis. Indeed, households’ net financial worth increased from €10,500 billion in 2008 to almost €15,000 billion in 2015 (Figure 1.4). Financing ultimately coming from households also had to be used for compensating the withdrawal of funding resources by foreign investors, whose net positions significantly declined throughout the same period.

Figure 1.4 Net financial worth of the institutional sectors, outstanding amounts, euro area

The net financial worth of the institutional sectors is significantly smaller than gross financial positions. Households provide net funding to NFCs and governments. Despite its large size in terms of financial assets and liabilities, the net contribution of the financial sector to the financing of the economy is negligible. Net financial worth has expanded in absolute terms, but it has remained rather stable as a percentage of GDP.

Source: ECB, Eurostat, and own calculations.

Notes: RoW: Rest of the World. Net financial worth is computed as financial assets minus financial liabilities.

Nonetheless, two important factors have been eroding the capacity of households to continuously provide financing to the rest of the economy. In the short run, unacceptably high levels of unemployment entail a net absorption of financial resources. In the long run, demographic developments, including longer lives and reduced fertility rates, imply a shrinking share of working population with respect to number of people already in retirement.12

The main net users of financial resources are NFCs and governments. NFCs can obtain credit because they have large amounts of equity and significant amounts of tangible assets such as buildings, machinery, and others that are not accounted for in the financial accounts. Governments borrow against their future collection of taxes, their main source of revenues. The net financial worth of NFCs remained rather stable throughout the crisis.

The financial and economic crisis triggered important financing needs in the public sector. Government net financial negative worth (net public debt) increased from €4,000 billion in 2008 to over €7,000 billion in 2015. This is explained by its function as an automatic stabilizer—providing social benefits, for example13—but also for the need of the public sector to step in to support financial institutions under stress.

We have seen that the balance sheet of the financial sector represents about half of the aggregated balance sheet of the economy. However, given their intermediation function, the net contribution of financial corporations to the financing of the economy is only incidental.

The financing of the economy is completed by resources provided by the external sector. The crisis triggered a retrenchment of the financial sector to their main activities, including the reduction of cross border positions. Accordingly, the net lending obtained by the euro area from the rest of the world declined from a peak of more than 30 percent of GDP in 2009 to less than 10 per cent in 2015.14

Box 1.3 The Financial Instruments Available in an Economy: An Overview

The provision of funding can be formalized through different instruments or products with specific features in terms of liquidity, maturity, or legal implications. Among the wide range of sources that are available for firms to finance their activities, a major divide appears between equity instruments and debt instruments. Obtaining funding through equity instruments implies the transfer of property to equity providers and their involvement in decision making. Consequently, the remuneration of equity depends on the results of the company. In other words, equity instruments are the first layer for the absorption of losses, but, in compensation for that, equity holders benefit from potential extraordinary profits.

In principle, equity instruments are permanent or perpetual, so holders need to find a buyer in case they want to untie their positions. In this context, quoted shares can be more easily liquidated than other equity instruments because they are quoted in organized markets. Note that equity includes both fresh injections of capital—either at the inception of a company or at a later stage—and the earnings retained throughout the life of the firm. This applies both to quoted shares and to other equity instruments. The case of insurance technical reserves represents a special case of equity.

Debt instruments do not transfer property and usually require a fixed interest payment15 and the reimbursement of the principal within a specific time frame. Bonds are standardized debt instruments that are traded in organized markets. Loans are bilateral contracts, which cannot be traded unless they are converted into bonds through securitization. Besides borrowing from banks, firms can obtain loans from other economic agents. There are four types of such loans: first, loans agreed between two companies belonging to a group of companies, also called intragroup lending; second, loans agreed between two companies not belonging to the same group, usually stemming from a suppliercustomer relationship but that cannot be classified as trade credit; third, loans provided by households to entrepreneurs and small firms—often from family and friends; finally, loans provided by the State and public authorities, whether subsidized or not—for instance, stemming from a government initiative to promote entrepreneurs and start-ups.

The economic transactions between a company and its suppliers, clients, employees and other stakeholders imply intrinsic financing resources that cannot be provided by capital markets nor by the financial sector. These sources of funding are usually generated by the difference between a continuous accrual of economic value and a point-in-time nature of payments and settlements. Therefore, they are not formalized in the form of a loan contract. These sources of funding can be grouped in the category of trade credit and advances (receivable or payable), where trade credit refers to the financing positions within the supplier-customer chain and advances refers to the relations with other stakeholders.16

There are many examples of trade credit and advances. When we purchase plane tickets months before our actual journey through a webpage, we are providing an advance to the air carrier. In business-to-business relations it is very common to make the payment up to ninety days after the delivery of goods. Another example is a monthly salary: employees of a company generate value on a daily basis, but they only receive their wages on a monthly basis. Similarly, utility companies—like electricity, water, or Internet suppliers—provide their services on a continuous basis but they are only paid at the end of the period—once a month, for instance.

Taxes due and tax claims have similar features to advances. Companies intermediate in the collection of VAT taxes, which are only settled once a quarter. Income taxes, which are settled once a quarter or once a year, have somehow an analogous nature. When, following a tax declaration, one is entitled to a tax reimbursement, the household or the firm have been financing the State; similarly, when one is required to pay additional taxes, one has been financed by the State.

The label derivatives includes a wide range of instruments with the only commonality of being somehow linked to the evolution of an underlying asset. Deposits and currency are the most liquid instruments; they are usually kept for transactional purposes, although their holders may also receive a small remuneration.

In general, in order to guarantee the financial stability of an economic agent, long-term assets—such as buildings or machinery—should be financed by long-term sources of funding—such as equity, long-term loans or long-term bonds—and current assets—such as inventories or advances to customers—should be financed by a shortterm source of funding.17

In any financial transaction, there are two counterparties involved: one providing the funds and the other one providing the needs. As a consequence, any instrument is recorded twice: as an asset by one counterpart and as a liability by the other. However, given the intermediation function of the financial sector, the correspondence between assets and liabilities can be complex.

Sources of Financing Used by the Economy: Instruments

The composition of assets within the nonfinancial sectors (households, NFCs and governments) provides an indication of how the economy is organized and the role of financial intermediation and the financial sector. If households keep their savings in the form of deposits, banks can intermediate and provide credit through loans. However, if households prefer to directly invest in bonds or equity, there is little room for bank intermediation—and maybe even no need.

In general, the product mix depends on the “preferences” of economic agents. These preferences are in fact a combination of factors such as the need for liquidity for transactional purposes, the remuneration level of the different instruments, risk aversion or entrepreneurial culture, amongst others. Transaction costs, informational barriers or bankruptcy regimes may also play a role. In other words, they are strongly driven by legal and institutional frameworks.18

The funding mix differs widely from one sector to the other19 (Figure 1.5). NFCs finance more than half of their activities with own resources (51 percent); the majority of which takes the form of equity other than quoted shares (35 percent total liabilities) and, the rest, the form of quoted shares (16 percent). Given that less than 0.05 percent of EU companies have listed shares,20 a 16 percent use of quoted shares seems to signal well-developed equity markets (see Section 1.5).

NFCs use also a variety of debt instruments including bank loans (14 percent of total financing sources), other loans (18 percent), and trade credit and similar advances (11 percent of liabilities). The use of bonds (4 percent) and other financing sources (1.5 percent) is much more limited. Overall, NFCs obtain one third of their financing from the traditional financial sector—bank borrowing, bonds, and quoted shares—while the other two thirds come from alternative sources.

Households use bank loans as their main source of financing (77 percent of their financial liabilities), while the use of other sources is more limited.

The bulk of governments’ financial liabilities are bonds (over 70 percent of their financial liabilities). Bank loans, other loans and “other sources”—such as trade credit, pending bills, pending transfers, and advanced taxes—represent about 10 percent each.

Figure 1.5 Sources of funding (financial liabilities), euro area, 2015, € billion

The funding mix differs across institutional sectors. Households use mainly bank loans and governments mainly bonds. On the other hand, NFCs, MFIs and OFIs use a variety of funding sources.

Source: Eurostat and ECB: euro area accounts.

Note: “Bank loans” for MFIs correspond to interbank deposits received. “Other loans” for MFIs correspond to deposit received (other than interbank): € 14,700 billion. “Other equity” for OFIs: €16,300 billion. “Other financing” for ICPFs corresponds to insurance technical reserves. Investment fund shares and mutual fund shares are included in other equity.

The financial sector stands out due to the low level of equity issued in the market—only 2 percent of its financial liabilities are quoted shares compared to 16 percent for NFCs. Capitalization—including both quoted shares and other equity—is particularly low for banks—less than 10 percent of total liabilities compared to over 50 percent in the case of NFCs.21 Even when the financial sector is taken as a whole, capitalization is rather limited—less than 30 percent. Moreover, the interlinkages within the financial sectors—for instance, the equity of OFIs corresponds mainly to shares of investment funds and mutual funds22—should not be neglected. This implies a lower loss absorption capacity than that which the headline figure of equity may seem to suggest.23 In the wake of the financial crisis and following both market pressure and regulatory reforms, the financial sector, and banks in particular, has been raising new capital to reinforce their loss absorption capacity; however, the financial sector still functions with much lower capital levels than NFCs.

The use of bonds as a source of funding is significant for banks (14 percent of financial liabilities) and OFIs (13 percent) and much less so for ICPFs (1 percent). The most prominent source of funding for banks are deposits and loans provided by other sectors (45 percent) and interbank lending (23 percent). These two categories are also somehow relevant for OFIs (a combined value of 18 percent). The main source of financing for ICPFs is insurance technical reserves—included in “Others.”

Turning to the evolution of the funding mix,24 the crisis particularly eroded the value of the equity of NFCs (both quoted shares and other equity) in 2008–2009, and to a slightly lesser extent the second dip of 2011 (Figure 1.6). This corresponds with the loss absorption function of equity. Equity other than quoted shares, however, recovered precrisis values already from mid-2010. The recovery in the value of quoted shares seems to have lagged behind. In 2015, the expansion in quoted shares and other equity seems to have ground to a halt, which already hints at the turmoil of early 2016.

Figure 1.6 Sources of funding (financial liabilities), breakdown by instrument, euro area, € billion

A differentiated impact of the crisis is observed across sectors and sources of funding.

Source: ECB, Eurostat, and own calculations.

Notes: The financial sector includes MFIs, OFIs, and ICPFs. RoW: Rest of the World. Deposits received by banks are included under the category “Banks loans” (interbank deposits) or “Other loans” (deposits other than interbank). Investment fund shares and mutual fund shares are included in other equity.

A stagnating or even declining volume of bank loans to the nonfinancial part of the economy can be observed since the outbreak of the crisis. It has been argued that the capacity of the banks to provide loans has been jeopardized by the financial crisis; however, demand factors may also be playing a role.25 A similar evolution is observed for other liabilities, consisting mainly of trade credit. This may be explained by the context of reduced economic activity (i.e., demand factors) and also, to a certain extent, by a certain decline in confidence observed since the outbreak of the crisis.

This negative evolution in loans and other liabilities is more than compensated by the expansion of bonds—mainly issued by governments but also by large NFCs—which almost doubled between 2008 and 2015 and of loans other than bank loans (intercompany loans, loans from households, and government loans), which increased by more than 40 percent during the same period.

Overall, and despite the crisis, the total size of funding resources used by the NFCs of the economy expanded between late 2007 and 2015 (from €40,000 billion to almost €50,000 billion). Although an important part of this expansion is explained by the increase in government debt (from €7,200 billion to €12,500 billion), NFCs also increased their use of funding to a certain extent (from €12,500 billion to €14,300 billion), but at a slower pace than in mid-2000.

Turning to the financial sector, the financial crisis negatively impacted all sources of financing, which in general stagnated or even started to decline from 2013. A notable exception is the significant expansion in “other equity,” which is mainly explained by the expansion of OFIs—particularly investment funds. Since the outbreak of the crisis, the overall size of funding resources used by the financial sector has evolved in “waves” with periods of roughly two years of stagnation followed by about two years of expansion. This may be linked to the excessive size reached by the financial sector—with a total size of almost €90,000 billion26 compared with about €10,200 billion of the euro area GDP—and recurring pressures to deleverage (cf. discussion in Section 1.2). Having said that, the different subsectors within the financial sector show divergent evolutions (see next section for further details).

Financial Intermediation

Once the different instruments that can be used to finance economic activities have been reviewed, we will look at the providers of those funding resources or financial channels. Therefore, this section focuses on the intermediation through financial institutions and the next two sections focus on the direct financing either through organized markets, or by the direct interaction between ultimate providers and end users of funds.

The Role of Financial Institutions

Financial institutions perform a number of functions such as creating and managing payment systems, providing market infrastructure—such as trading platforms or management of initial public offerings—providing savings facilities for households—for instance, investment funds, insurance or pension funds—participating actively in markets—for instance, through “proprietary trading” of bonds and quoted shares—providing liquidity—for instance, through factoring—and helping economic actors to manage and insure against risks—for instance, insurance companies and pension funds.

The intermediation function of the financial sector implies channeling savings and excess liquidity from one part of the economy toward other areas in need of funding. In general, however, financial institutions do not create net additional financial resources (see Section 1.3). Banks usually assess the risk of their clients and should only finance projects that they consider viable. The intermediation and risk assessment function of banks is usually combined with maturity transformation. This means that a bank will typically be financed through short-term savings—typically overnight deposits—and will provide long-term loans—for instance, for buying a house or for a factory to invest in equipment.

While the maturity transformation function of banks plays a crucial role in the financing cycle of the economy, it also puts banks in an inherently weak position. In light of the fact that they use short-term funding to finance long-term projects, they can be confronted with liquidity problems if a large share of depositors were to claim their funds at a given moment. To mitigate this risk, financial institutions must comply with some prudential requirements in terms of liquidity and capital. In addition to that, the central bank provides a lender of last resort safety net in the event of liquidity constraints.

If a bank were to act recklessly, public authorities could be confronted with a dilemma between the risk that basic financial services, such as ensuring the functioning of the payment system, could collapse, and bailing out banks with a reckless behavior. An exploitation of this dilemma by banks is known as moral hazard.

A moral hazard situation appears when the potential benefits and risks are not well balanced or do not fall on the same actors. This is for instance the case of an insurance contract, which leads a person to be less careful in her behavior because she knows that the potential damages will be covered by the insurance company.

While it is not possible to completely eliminate moral hazard, prudential requirements and supervision of financial institutions tries to strike a balance between private initiative and maintaining financial stability. The crisis has shown that the previous framework was not properly calibrated. A series of measures has been implemented to better constrain the occurrence of moral hazard situations (see Part D).

Subsectors of Financial Intermediation: Size and Evolution

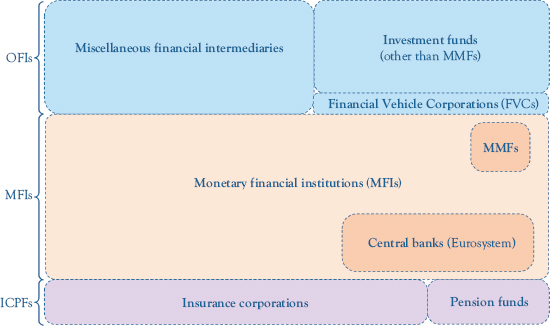

Financial institutions can be classified in three subsectors: monetary financial institutions (MFIs), insurance corporations and pension funds (ICPFs), and other financial institutions (OFIs). In 2015, MFIs’ total assets accounted for about half of all euro area financial institutions, ICPFs for about 15 percent and OFIs for about 40 percent. MFIs can further be split into credit institutions, money market funds and the central bank; OFIs, can be split into investment funds, financial vehicle corporations and miscellaneous financial intermediaries; ICPFs can be split into insurance corporations and pension funds (Figure 1.7).

Figure 1.7 Financial intermediaries and subsectors

Source: Own elaboration.

Notes: The surface of each box is proportional to the size of the sector in the euro area in 2015. OFIs: Other financial institutions. MFIs: Monetary financial institutions (credit institutions, MMFs and central banks). MMFs: Money market funds. ICPFs: Insurance corporations and pension funds.

In 2015, the total balance sheet of euro area financial institutions was almost €70,000 billion, over six times the annual GDP of the euro area. Between the early 2000s and 2012, euro area financial institutions doubled in size (in terms of total assets). This was driven by growth in all the three main subsectors. Since the onset of the crisis, however, the banking sector grew much slower than the other sectors, and even declined in size after 2012. On the other hand, both ICPFs and OFIs kept expanding, particularly the latter (Figure 1.8). While a part of this growth may be autonomous, it has also been driven, to a large extent, by a transfer of assets from banks to OFIs. Indeed, it has been argued that the increasing regulatory requirements imposed on banks and the pressure to deleverage have led to a transfer of assets to other less regulated parts of the financial system, the so-called shadow banking sector.27 If that would be the case, while the banking sector may seem smaller, the overall size of the financial system as a whole, and therefore the risk embedded in it, does not seem to have declined, rather the contrary.

Figure 1.8 Total assets of financial intermediaries, outstanding amounts, euro area, € billion

The size of the financial sector has more than doubled since 2003. MFIs represent about half of the financing sector, but they have lost relative importance mainly due to a significant expansion of OFIs.

Source: ECB, Eurostat, and own calculations.

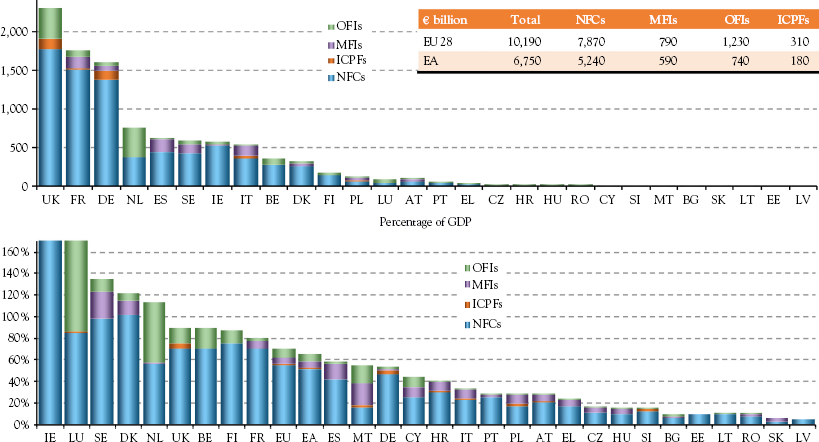

The size of the financial sector varies widely across countries, both in absolute and in relative terms. In absolute terms, the UK has the largest financial sector (26 percent of the total); in Germany and France, the financial sector is about half the size of that of the UK. Despite its small size of Luxembourg in terms of GDP, its financial sector is the fourth largest in the EU because of the country’s role as a financial center. It is remarkable to note that the Dutch financial sector is larger than that of Italy or Spain, even though the country is between two to three times smaller. This is explained, to a certain extent, by the significant development of pension funds (Figure 1.9).

In relative terms, the countries with the largest financial systems are Luxembourg, Malta, and Ireland (with a size representing more than 20 times their respective GDP), followed by Cyprus, the Netherlands, the UK, and Denmark. On the other hand, in most eastern European countries, the financial sector represents no more than three times GDP. As discussed previously, the financial sector contributes to the efficient allocation of resources in the economy; however, excessive debt can also entail risks. Although there is no magic number indicating the optimal level of the financial sector as it depends on multiple factors, it needs to be monitored to avoid becoming excessive.28

In terms of composition, in most countries, MFIs account for more than half of the financial sector. The exceptions are Luxembourg, the Netherlands, Cyprus, and Malta, where OFIs are the largest sector. In the UK, Germany, Belgium, and Hungary, OFIs are also significant. ICPFs tend to be smaller across the board.

Direct Financing Through Debt and Equity Capital Markets

Besides financial intermediation, funds can also be directly channeled from savers/investors to borrowers. This may require the intervention of a financial institution to provide the infrastructure—for instance, the stock exchange—or some services—such as brokering. There are various such direct financing channels: organized markets for shares or bonds, trade credit and advances, company loans, loans from family and friends, amongst others (Figure 1.10).

Financial markets enable the pooling of resources from numerous investors. As bonds and (quoted) shares are standardized products, secondary markets can grow, enabling investors to convert their securities into liquidity at any time.

Figure 1.9 Size and composition of the financial sector, total assets, 2015 € billion

The size of the financial sector varies widely across countries. In absolute terms, the United Kingdom, Germany, and France concentrate the largest share of financial institutions; in relative terms, Luxembourg, Malta, Ireland, and Cyprus are important financial centers. OFIs tend to concentrate in the largest countries or in the financial centers.

Source: ECB, Office for National Statistics (UK), Eurostat, and own calculations.

Notes: Luxembourg: OFIs = 19,000 percent of GDP. Data for Bulgaria are not available.

Figure 1.10 Direct financing of the economy

A variety of options are available for the real economy to obtain direct financing without the intervention of an intermediary.

Source: Own elaboration.

Notes: PP: Private placement. CF: Crowdfunding. PE: Private equity. ABF: Asset-based finance. Advces & other: Advances and other financing (includes items such as trade credit, advances by different stakeholders, tax claims and similar items). The surface of each box is proportional to the size of the sector in the euro area in 2015 (except for PP and CF, which have a very small size).

A market authority ensures the issuers seeking finance comply with a series of requirements, such as regularly disclosing information about their financial situation. The European supervisory authority in charge of ensuring the integrity, transparency, efficiency, and orderly functioning of securities markets, as well as investor protection is the European Securities Market Authority (ESMA). It works very closely with the national competent authorities, which are members of the Board of Supervisors, its highest decision-making body.29

In addition to a market authority, this type of direct financing requires a market infrastructure and financial institutions to provide services such as investment advice, market-making, and brokering. This can sometimes be offered by credit institutions or by independent institutions, classified under “miscellaneous financial institutions” (Figure 1.7).

While capital markets have existed for centuries, they grew rapidly in the 18th and 19th centuries during the industrial revolutions, when large amounts of money were needed to finance infrastructure—mainly railroads and canals—and the construction of large factories. In the last 30 years, markets have been boosted by three factors: (1) electronic trading, (2) technological developments, and (3) deregulation and harmonization of rules across Europe. The combination of these developments fostered a quick expansion of capital markets: between 1990 and 2008, both bond and equity markets multiplied sevenfold (Figures 1.11 and 1.14).

Figure 1.11 Bond markets, euro area, € billion

The volume of bonds significantly expanded until the early 2000s, when it stagnated. Bonds are mainly issued by government and MFIs. Gross flows (primary issuances and redemptions) are significantly larger than net flows, particularly for MFIs. However, they have dropped since 2009.

Source: ECB and own calculations.

Notes: Bonds issued by ICPFs are negligible (less than €60 billion of outstanding volumes) and are therefore not included.

Bond Markets: Overview

A bond is a debt instrument, that is, the issuer has to reimburse the principal and pay interest. The need to reimburse the principal at nominal value makes bonds very different from shares in two respects. Firstly, fluctuations in bond prices are much more limited than those of shares. However, this can change when a company—or a State—is under stress and investors fear or expect a default. Secondly, bonds need to be rolled over regularly, making them somehow more liquid than shares. As a consequence, the outstanding volumes of bonds may be similar in size to annual flows—gross issuance and redemptions.

Bond markets in Europe are sizeable. They expanded steadily at an average of 9 percent a year over the period 1990–2011. Growth accelerated in the first stages of the crisis, but total volume of bonds has stagnated since early 2012 (Figure 1.11, top-left panel) at about €16,500 billion—or 160 percent of 2015 euro area GDP.

Bond markets are more or less evenly split between bonds issued by financial corporations (MFIs and OFIs, €7,400 billion) and government bonds (€7,800 billion). The volume of bonds issued by NFCs is much smaller (€1,100 billion).

Throughout the 2000s, the outstanding volume of bonds was similar in size to annual gross issuances and redemptions. This indicates that bonds had an average maturity of about one year, however, there maturities were different across sectors (Figure 1.12). The average maturity of government bonds remained between three and four years while the average maturity of bank bonds was about half a year. This is consistent with the maturity transformation function of banks and their business model based on the exploitation of the yield curve. Since the early 2000s, gross issuances were clearly dominated by MFIs—they issued over 70 percent of all euro area bonds during the peak of 2008–2010—while the outstanding volume of bonds issued by MFIs was less than 40 percent of the total. This indicates that the maturities of MFIs’ bonds were much shorter than the maturities of bonds issued by other sectors.

As a response to the crisis, the ECB reduced its policy interest rates to virtually zero (Figure 4.8). This led to a significant decline not only of short-term interest rates but also of long-term interest rates; in other words, the yield curve declined and flattened. As a consequence, the issuance of bonds with longer maturities became more advantageous. This explains the evolution of gross issuance observed since 2010, particularly for bonds issued by MFIs (Figure 1.11, bottom-right panel). Since mid-2015, the gross issuance of bonds by MFIs has dropped to reach levels similar to the gross issuances by governments. This phenomenon is explained by a significant extension of the maturities of the bonds issued by MFIs leading to less frequent roll over needs and, therefore, less gross issuances and redemptions30 (Figure 1.12). By mid-2015, the average implicit maturity of bonds had increased to two and a half years.

Figure 1.12 Implied maturity of bonds by issuer sector, bonds outstanding, euro area, years

The implicit maturity of bonds is different across sectors. An expansion in the maturity is observed since 2008 driven by declining (long-term) interest rates.

Source: ECB and own calculations.

Notes: The implied maturity indicates how many years are needed to redeem the total volume of bonds outstanding assuming that redemptions continue at the same rate as in the year-to-date.

Concerns about a reduction in market liquidity in bonds markets were raised throughout 2015.31 Although measuring liquidity involves a number of dimensions, the extension of maturities and the consequent reduction in roll over needs may explain, to a large extent, the perceived decline in market liquidity.

Bond Markets: Details by Sector

Throughout the crisis, euro area governments continuously and significantly increased the volume and flows of bonds issued: outstanding volumes expanded by more than 50 percent between 2008 and 2016 (from bout €5,000 billion to €7,800 billion) through a significant expansion in net flows. Gross issuance increased significantly in the first stages of the crisis (2008–2010) and have since remained at very high levels compared with historical series; redemptions have followed with a certain lag. After peaking in 2009, net annual issuance of bonds by governments has declined to historical averages (Figure 1.13).

This evolution in government bonds stems from the reactions to the crisis. As discussed in Chapter 2, in the early stages of the crisis, governments had to step in to support financial institutions in difficulty; such bank bailouts were financed by issuing debt. At the same time, economic contraction (or subdued growth) eroded public finances both on the income side (lower amounts of tax collected) and the expenditure side—higher social benefits spending linked, for instance, to unemployment—this is the so-called automatic stabilizing function of the government budget.32 These factors have driven the expansion of the volume of government bonds.

Figure 1.13 Bond issuance by sector, euro area, € billion

Beside size differences, divergent evolution is observed across sectors. The volume of bonds issued by governments and NFCs has continuously expanded while the stock of bonds issued by OFIs and MFIs have stagnated or declined since the outbreak of the crisis. Gross flows (primary issuance and redemptions) have stagnated or declined given the environment of declining interest rates.

Source: ECB and own calculations.

Notes: Bonds issued by ICPFs are negligible (less than € 60 billion of outstanding volumes) and are therefore not included.

At the same time, three other drivers constrained such an expansion and explained the relative reduction in net flows and the slowdown in the growth of outstanding amounts observed from 2010 onwards. First, governments carried out a number of structural reforms to improve their finances. Second, the countries with the most acute financial problems (Greece, Ireland, Portugal and, later on, Cyprus) asked their European partners for support and discontinued or significantly reduced their issuances of new debt in the market (see Chapter 5). Finally, EU governments agreed to implement additional constraints in their public accounts by revamping economic governance rules (see Chapter 8).

To put it differently, the growth in the volume of government bonds declined from a peak of over 12 percent a year in 2009 to about 2.5 percent a year in 2015. While this implies a significant drop in growth rates, public debt continues to expand, not only in absolute terms but probably also relative to GDP (given that GDP growth is quite limited at about 2.5 percent). This reiterates the fact that leverage has not really started to decline as discussed in Section 1.2.

Bonds issued by MFIs show a totally different pattern. Their expansion, in terms of outstanding volumes, came to a halt with the outbreak of the crisis and a significant contraction occurred from late 2012, which reflects their process of deleveraging. Banks faced a number of pressures to reduce their balance sheets and leverage levels. Reducing the total size of the balance sheet implies reducing banks’ assets, but also liabilities. One way of doing this is by not rolling over a (significant) share of the bonds that reach maturity.

On the other hand, a dramatic expansion in annual flows is observed between the mid-2000s and the outbreak of the crisis and a significant drop thereafter. As explained earlier, this has been driven by the rotation of the yield curve. The flat but high yield curves observed in the mid-2000s forced banks to issue bonds with very short maturities to obtain a sufficient margin from maturity transformation. With declining yields, banks may use relatively longer-term financing sources and still obtain a margin.

Bonds issued by OFIs, although initially of an order of magnitude lower than the bonds issued by governments and MFIs, significantly expanded in the run-up to the crisis. This mainly reflects the boom in securitization. The financial crisis put a halt in securitization activity (see Chapter 3). However, outstanding volumes of bonds issued by OFIs have not declined but simply stagnated since late 2009. Therefore, the contraction in securitization seems to have been offset by an equivalent expansion in the issuances of bonds by other institutions in the OFIs sector. Data on flows seem to support that interpretation: although net annual flows have fluctuated around zero, primary issuances and annual redemptions have remained at historical heights since 2010.

Finally, NFC bonds also followed a specific pattern. Although at much lower levels than any other sector, they expanded significantly both before and during the crisis. This partially reflects a certain switch from bank financing to bond financing by NFCs. Given that banks were particularly impacted by the crisis; the declining central bank rates (Figure 4.8) were translated into (declining) retail loan rates to a limited extent only and heterogeneously across countries (Figure 3.9). In this context, large corporations with investment-grade ratings could profit more from the decreasing interest rates by issuing bonds than by turning to bank credit. That being said, the slowdown in economic activity reduced the financing needs of NFCs because of its effect on demand.

Bond Markets: Specificities Across Countries

Four countries—the UK, France, Germany, and Italy—account for over 60 percent of bond issuances in the EU; this share goes up to over 75 percent when the Netherlands and Spain are included. This supposed concentration of markets stems mainly from the size of those six countries—their combined GDP also represents over 75 percent of EU GDP.

In most countries, as well as in the euro area as a whole, the government sector and the financial sector account for most bond issues (Figure 1.14). Issuance by financial institutions other than banks is particularly significant in Luxembourg, Ireland, the UK, and the Netherlands both in absolute terms and relative to their respective GDP. Luxembourg and Ireland are known to be attractive to international financial institutions as a point of entry to EU markets. By contrast, bond issuance by banks (MFIs) is particularly significant in Denmark, Sweden, and Luxembourg.

Figure 1.14 Issuance of bonds by country and sector, bonds outstanding, 2015

The issuance of bonds concentrates on the largest countries (the United Kingdom, France, Germany, and Italy) although, in relative terms, they are also significant in Luxem-bourg, Ireland, the Netherlands, and Denmark, mainly driven by OFIs and MFIs (in the case of Denmark only).

Source: ECB and own calculations.

Notes: Luxembourg: OFIs: 1,350 percent of GDP; Ireland: OFIs: 290 percent of GDP.

With a few exceptions, bonds issued by NFCs account for about 10 percent or less of total issuance in each country and 10 percent or less of its respective GDP.

Stock Markets: Overview

Stocks have very different features from bonds. Equity instruments are, in principle, permanent, so they do not need to be rolled over. Consequently, annual issuance of equity is much smaller than the outstanding volumes and the annual issuance of bonds. Similarly, redemptions tend to be small.

Euro area equity markets (quoted shares) have a size which is less than half the size of bond markets: market capitalization hovered about €7,000 billion in 2015, or 68 percent of euro area GDP, compared with over €16,000 billion of outstanding volume of bonds. The bulk of quoted shares are issued by NFCs, while the market capitalization of banks and OFIs is much smaller (Figure 1.15, bottom-left panel). It appears that NFCs and financial corporations (MFIs and OFIs) have opposite preferences in their mix of quoted shares (equity) and bonds as a source of funding. NFCs make extensive use of equity markets as a source of funding and much more limited used of bond markets; while financial corporations use bond markets extensively and issue equity to a much lesser extent.

Figure 1.15 Equity markets, euro area, € billion

The volume of equity securities evolves with much more volatility than in the case of bonds. Given the permanent nature of equity, issuance is significantly smaller than capitalization. The bulk of stocks has been issued by nonfinancial corporations.

Source: ECB: securities statistics and own calculations.

Market capitalization is significantly affected by price fluctuations, which reflect actual revenues or losses but also other factors such as the outlook of the firm, investor confidence and other psychological factors. Stock markets tend to have a more volatile evolution than bond markets and can sometimes be affected by the dynamics of bubbles (Box 1.4).

Box 1.4 Financial and Economic Bubbles

Many episodes of financial bubbles have occurred throughout history. As early as in the 17th century, the tulip mania in the Netherlands is known as one of the first bubbles. Maritime transport in the 18th century and railway construction in the 19th century also generated financial bubbles—for instance, the South Sea Company, the Mississippi Company, or the Railway Mania. In the 20th century, bubbles were mainly rooted in stock exchanges or in housing: the roaring twenties leading to the crash of 1929, the Asian financial crisis of 1997 or the dotcom bubble of 1996–2001.

The data on flows of quoted shares clearly depict the blowing up and the burst of the dotcom bubble (Figure 1.15). Net issuance of shares by NFCs—mainly firms dealing with new technologies—skyrocketed from €20 billion a year to over €140 billion a year. This went hand in hand with a widespread hype and increasing demand, which multiplied the prices of these stocks. This explains, to a large extent, the rise in capitalization from €1,500 billion to over €4,500 billion. However, at a certain point, investors realized that this was not sustainable and stopped buying new shares—the “Minsky moment.”33 The artificially high stock prices were corrected and capitalization went down to almost €2,000 billion.

The recent financial crisis that started in 2007 seems to be the outcome of a similar pattern—capitalization increased from €2,000 billion to over €5,000 billion and subsequently collapsed back to almost €2,000 billion. However, the evolution of net issuance had nothing to do with the ones observed in the late 90s. This is explained by the fact that the 2007–2008 bubble did not arise in the stock exchange but in credit and housing prices.34 Net flows of bank loans to households and firms increased significantly throughout the early 2000s (Annex 1.1); a significant expansion in net interbank and interfinancial loans is also observed during that period. The turmoil in Chinese markets that started in summer 2015 or the Volkswagen scandal related to the gas emissions uncovered in September 2015 seemed to have had a contained impact in euro area stock markets. However, with the turn of 2016 a bear mood seems to have settled in the markets. Although past performance cannot be used to make exact predictions of future evolution of stocks, it is quite likely that the capitalization of euro area stocks will continue to correct until bottoming out at about €4,000 billion.

An important difference between the dotcom bubble and the financial bubble of 2007–2008 is the availability of capital buffers to accommodate the burst. More than half of the financing of NFCs comes from equity (Figure 1.5); therefore, they have a large buffer to absorb shocks, and losses are borne by the investors responsible of the decisions of the companies in difficulties. This allowed a quick cleanup of problematic balance sheets in the dotcom bubble without major contagion to other economic agents. The buffers available in bank balance sheets—and those of financial institutions in general— are much smaller.35 Given this lack of buffers, the excesses cannot be corrected through prices and losses but by issuing new equity, but this can take a long period of time. Indeed, since the outbreak of the crisis, the issuance of quoted shares, particularly by banks, has remained at very high levels for historical standards (Figure 1.15). Having said that, public authorities and analysts should cautiously assess if such levels of net issuance of equity are indeed used to address the weaknesses of the banks surfaced on the wake of the 2007–2008 crisis or if rather a new bubble is in the making.

The latest technological developments have led to a radical change in how markets operate and to an acceleration and amplification of economic bubbles. Indeed, electronic trading has substituted outcry auctions; retail investors do not need to interact with their bank through a physical or telephonic contact but they can just trade through Internet from home and, more recently, from anywhere with a portable device; professional investors have developed algorithms to trade at the nanosecond. All these factors have played an important role in the dotcom bubble of the early 2000s, in the one of 2007–2008, and in the more recent events in China. Moreover, advances in IT have made the financial and the real economy much more interconnected at global level.36

Stock Markets: Specificities Across Countries

Three countries, the UK, Germany, and France concentrate almost 60 percent of the shares issued across the EU in absolute terms (Figure 1.16, top panel). However, the largest markets relative to GDP are those of Ireland, Luxembourg, Sweden, Denmark, and the Netherlands (Figure 1.16, bottom panel). In the majority of countries, the bulk of quoted shares are issued by NFCs. However, in a few countries—Malta, Luxembourg, the Netherlands, and Bulgaria—OFIs issued more than 30 percent of all shares in terms of capitalization and, in a few others—Slovakia, Poland, Malta, Hungary, Czech Republic, and Greece—shares issued by MFIs are also relatively significant—representing about 30 percent or more of all quoted shares.

Figure 1.16 Issuance of quoted shares by country and sector, capitalization outstanding, 2015

The bulk of EU stock markets concentrate in the United Kingdom, France, and Germany, although stock markets are also significant in Ireland, Luxembourg, Sweden, Denmark, and the Netherlands, relative to their respective GDP. NFCs represent the lion share of equity securities, with the exception of Luxembourg and the Netherlands, where the stocks issued by OFIs have a similar size to NFCs stocks.

Source: ECB and own calculations.

Notes: Luxembourg: OFIs = 90 percent of GDP. Shares issued in Luxembourg by MFIs are nil; this indicates that (listed) banks with subsidiaries in Luxembourg issue their shares in their country of origin. Ireland: NFCs: 240 percent of GDP; MFIs = 15 percent of GDP; OFIs = 10 percent of GDP; ICPFs = 0 percent.

Direct Financing Beyond Capital Markets

Besides investors and financial intermediaries, a number of other stakeholders are critical to the day-to-day life of businesses and to economic production in general: employees, customers, suppliers, public authorities, services providers, educational systems, and so on. Economic transactions between suppliers and clients, and between companies and employees, imply intrinsic financing resources that can be provided neither by capital markets nor by the financial sector. These sources of funding arise from the difference between the continuous accrual of economic value and the point-in-time nature of payments and settlement. While they are mostly short-term, they are still critical for a well-functioning economy. Wages, trade credit, utilities and tax claims are common examples. Although they entail direct financing between two economic agents, the financial sector can still play a role by providing some services linked to these bilateral positions—such as asset-based lending, factoring, and leasing.

Nonetheless, these “alternative” sources of funding may also have a long-term nature. This can be the case for intercompany loans, government subsidies, internal funding, or equity provided by family and friends. While there is much less data and information about all these sources of information, they represent the bulk of the financing of the real economy. For instance, about one third of the financing of NFCs takes the form of equity other than quoted shares (see Figure 1.5), which corresponds to the initial contributions needed to start a family business and the subsequent profits ploughed back into the firm.

Beyond the Static Structure of Funding

Up until this point, we have mainly described the funding structure of the economy for the different agents individually. However, individuals and firms are not isolated; the interactions between different actors determine, to a large extent, how individual positions evolve over time. Therefore, this section discusses more in detail the interconnectedness among all market participants and what this implies in moments of financial stress such as during the recent financial crisis.

Interconnectedness and Contagion

Banks play a central role in the financial system: insurance corporations form groups with banks through “bank/insurance” holding companies; insurance corporations, pension funds and investment funds provide financing to MFIs by buying their securities; financial vehicle corporations channel the securitization activities of various financial intermediaries (mainly banks), which nevertheless may retain a significant chunk of an issuance; and many of the companies classified as “miscellaneous financial institutions” are in fact subsidiaries of credit institutions. Moreover, banks are connected with each other through interbank lending markets (Figure 1.17).

Banks and financial institutions are not only interconnected with each other but they are also closely interlinked with the real economy. Through their intermediation function, financial institutions obtain financial resources from some households and NFCs and provide credit to other households and NFCs, as well as to governments. Moreover, firms are closely interconnected with a large number of stakeholders, including suppliers, customers, employees, and civil society.

Figure 1.17 Interconnections within the financial sector: positions

The various components of the financial sector interact with each other creating a highly connected network.

Source: Own elaboration.

Notes: The surface of each box is proportional to the size of the sector in the euro area in 2015.

As shown in Section 1.1, the interconnection among the various parts of the economy can lead to feedback loops where the weaknesses or the strengths of a sector impacts other sectors with potentially amplified effects. For instance, a government in financial difficulties may pay suppliers late; some of these suppliers may be confronted with cash constraints and therefore pay salaries late; employees paid late will probably need to postpone some of their spending and therefore consumption will weaken; consequently, retailers will reduce their orders and factories will reduce their production with both potentially reducing their labor force; this will further exacerbate the difficulties for paying suppliers and employees and further decrease consumption.

While the economy is formed of a complex network of financial interconnections, not all of these interconnections have the same features.37 In particular, the bond between two economic agents can be very closely tied or very loose. This is crucial to understanding how the crisis unfolded (Part B) and the political response vis-à-vis the financial sector (Parts C and D) and the real economy (Part E). Depending on the distance in the relationship between two economic agents, their fate may be more or less dependent on each other.

In this context, a first distinction appears between equity instruments and debt instruments. Equity investors can scrutinize all the activities of the firm as they participate and are responsible for the day-to-day management of the company. Consequently, they take great interest in the performance of the company as their rewards, in the form of returns, are closely linked to the income generated by the business of the firm.

Employees and firms are usually bonded by very close ties, a longterm relationship and mutual trust. For instance, in many countries, large firms are legally required to involve employees (through representatives) in the important decisions of the firm. Staff interest may be closely aligned with the interest of shareholders and the firm. Furthermore, in companies that take the form of cooperatives, the employees are in fact the shareholders. Given this framework, whenever a firm is in difficulty, employees may accept some sacrifices—such as a delay in the payment of wages for a couple of months or a reduction in the salary—in the hope of contributing to the survival of the firm and, therefore, to that of their own jobs.

The relationship between a firm and its long-term suppliers and customers has similar features. Most suppliers search for long-term commercial relationships rather than a specific order, therefore a supplier may accept to be paid later than initially agreed if a customer is facing temporary difficulties.