CHAPTER SIX

A MORE SUSTAINABLE AND EQUAL WORLD

At this point it should be clear that embedded finance makes sound business sense. While still early, the numbers speak for themselves in terms of the revenue impact that embedded finance has on businesses both online and off. But does it make sense beyond the boardroom and the balance sheet? What is the larger impact on the world and society as a whole?

This chapter will look more closely at the human element as leaders think about their teams, the talent of the future, and, more broadly, their impact on the world. Specifically, we will discuss how embedded finance fosters financial inclusion among consumers and broader society while supporting key initiatives like sustainability.

DATA AS A FORCE FOR GOOD

One of the promises of fintech, as it emerged from the financial crisis of 2008–2009 that left so many families reeling, was that it would help all people have access to financial services in a way that resonated with them. By improving their financial health, by reducing friction and speeding up access to money, by reducing transaction costs and providing more ways to budget and save, fintech was supposed to make customers’ lives better.

What does financial inclusion really mean at scale and in practice? Financial inclusion means that people and businesses have access to affordable services to help them improve their financial lives. Embedded finance, by dramatically altering and expanding where and how customers touch financial opportunities, will deliver the most dramatic increase of financial inclusion in history. As Sanjib Kalita, founder of Guppy and editor-in-chief of Money20/20 says:

It's a shift from efficiency to resiliency. What we are seeing around the world is that consumers are one paycheck away from financial ruin. What we are getting is consumers that are built up to be efficient but they're very non-resilient. With the new things coming into play, I can see a change in terms of our own consumer financial supply chains and looking at it from a greater sense of resilience rather than just efficiency.

Though fintech has opened some doors, improving customers’ lives has not happened nearly as much as expected and large portions of the global population remain underbanked or still unbanked. There are a myriad of approaches for how to go about solving such a large-scale challenge. One such approach of applying embedded finance is through a much-discussed trend: cryptocurrency. Advocates of cryptocurrency believe decentralization will lead to the democratization of finance and ultimately, financial inclusion. This is what Brian Armstrong, CEO and founder of public company Coinbase, detailed in his 10-year vision for the company. A recent report by Crypto.com found that crypto users in the world grew from 65 million in May 2020 to 221 million in July 2021, close to 4x growth, showing the strong traction cryptocurrencies are enjoying, and embedded finance has played a role in its adoption, as we have already seen in this book.1

The shift toward digital currencies is seen throughout the world, including China. The benefits offered by the Chinese central bank digital currency (Chinese CBDC), which is already strong with 100 million users, are seen when it comes to financial inclusion. As the system and currency are offered by the Chinese state, it will ensure a widespread adoption among retailers, supporting those who cannot use Alipay, WeChat, or even cash. In terms of usage, it will remain similar to what Chinese people are used to with their payment apps and QR codes.

The author and commentator on digital financial services, Dave Birch, notes that the industry is just beginning to understand how embedded finance might work, and how its applications are broader than many realize. “People shouldn't think of embedded finance as just being about payments,” Birch said. “There's a lot more to it. A lot of it is about data and providing the right data to support decision making at the right time.”

Embedded finance's ability to offer greater visibility and insight into personal finances can help improve financial health. Birch said:

People are beginning to talk about the transition from open banking to open finance. You see the emergence of what some people label, I think quite reasonably, the financial health narrative. This is about taking a bigger picture of the consumer, having access to the consumer's finances in order to deliver them a better overall level of financial health. I think that's a very helpful narrative for the next generation of services. Embedded finance is huge. It's going to get better. It's not just about payments, it's about a lot more than that.

Indeed, embedded finance has the opportunity to bring broader financial health and inclusion to the world far beyond fintech or crypto alone because it has revolutionized the delivery system for financial services. While the problem for most underserved people across the globe can be quite complex when you get into the details, at the highest level, it can be simplified to access. For companies large and small, they already have a history with the customer and therefore, should be better able to bring financial services to meet the specific needs of historically underserved groups.

In speaking about how embedded finance impacts financial inclusion, Nigel Verdon, founder and CEO of Railsbank, believes that the impact will be huge. As he says: “Once you deconstruct a product into digital and you've got the mechanism for distribution, then you can find products or micro products when people need them. The byproduct of this is financial inclusion.”

ACCESS TO CREDIT

Economic growth is quite a complex topic and varies by region but across the globe, access to credit is one of the most significant issues for members of developing economies, and one of the best ways for societies to develop healthy middle classes, which are the engines of economic growth. One of the struggles has been that developing economies typically lack the credit reporting infrastructure to properly price and underwrite loans. Outside of the infrastructure, the other primary challenge for growth lies in the thin or nonexistent credit profiles of individuals and small businesses.

Credit is one of the biggest areas where embedded finance can have an impact. We have already seen this play out in markets across the world, and there are many geographies that are in desperate need of moving from unbanked to banked. But markets that are considered more evolved from a financial services perspective, such as the US, still have a great deal of opportunity for growth. According to research done by the Federal Deposit Insurance Corporation, in 2019, there were roughly 7 million people that were “unbanked,” meaning that no one in the household had a checking or savings account at a bank or credit union.2 In the same timeframe they found that roughly 55 million people were underbanked, meaning they have a bank account but also used an alternative financial service product.3

That is not a small number—one in every five adults in the US qualifies as underbanked. This portion of the population is using alternative methods to traditional banks and credit unions. These include methods such as money orders, check-cashing services, or loans from various sources like pawn shops, auto title loans, or payday loans, all of which may have exorbitant fees attached to them. As Zach Pettet, host of the podcast “For Fintech's Sake” and content director for Money20/20 put it: “The embedding of financial products across the lives of humans is actually going to give data that will improve our ability to score, do underwriting, etc. We have seen this play out in other markets, so I hope that the US is that way too.”

So often throughout the last 20 years, we have heard different industry leaders referring to their businesses above all else as data companies. Banking has been no exception, with banks, ranging from megabanks like Citibank to the community banks, being brought into the conversation. The key to the challenge outlined above around credit in many ways is fixed by data, which is why embedded finance becomes such an interesting value proposition. This is true not only for the companies who now have the right information to better offer products and services to their customers with the goal of expanding margins, but also for the end consumer or small business who wouldn't have typically been offered banking services before.

Eduardo Vergara, managing director and global head of Transaction Banking Product and Sales at Goldman Sachs, believes that by enabling fintech and tech platforms to provide financial services to the consumer and SME segments, embedded finance democratizes financial services by making them more accessible, putting pressure on margins due to the commoditization of those services, which ultimately benefits consumers and creates greater financial inclusion. Eduardo mentions that companies launching embedded finance propositions can leverage additional sources of data and therefore offer additional credit opportunities to businesses that they might not have been able to access with their traditional banking provider. This ultimately benefits the business itself, enabling it to borrow to support its growth, but also the economy and the employment rate ultimately.

THE IMPACT ON SMALL BUSINESSES

This data-first strategy doesn't just lie with fintech startups but also large brands such as the likes of Shopify. By using data effectively, Shopify is able to simplify the qualification process, provide funding to merchants a lot faster, while also offering more innovative repayment options. As a result, as of October 2021, Shopify has already offered $2.7 billion in funding through Shopify Capital. This data play is a “win-win-win” strategy as Tui Allen, product director at Shopify, shared with us earlier where everyone wins—from Shopify, their merchants, and the end customers.

Matt Henderson, EMEA business lead at Stripe, explains that its lending product for embedded finance, Stripe Capital, is a product with significant societal impact. In 2021, total loans to small businesses in the US were 40% lower than in 2008. Part of the reason why is that the traditional banks were struggling with being able to serve particular use cases and small businesses efficiently.

Henderson says:

If you were a plumber and you're great at your trade and you're getting a lot of bookings online, as with trading apps and so on, you've got fantastic reviews. And as a way to expand your small one-person business, you're thinking about hiring someone. Now, if you go to a traditional bank, all they can review as part of their decision protocol is your trading history, which is consistent with that of a sole trader. It's hard for banks to make a decision if they're using criteria that are based on a whole small business ecosystem rather than you specifically. Now, if you are a plumber, then the source for the loan application is actually a platform like Housecall Pro, which is a tradesperson platform that uses Stripe. The ratings are native to that platform which means that they can have confidence that the ratings are authentic. They can see from their own data that the ratings correlate with the ability for success in the future. They can then use a different sort of insight about a potential customer and do so in a scalable, automated way to make a loan decision for this plumber that then enables them to hire an extra person. Across the tens of thousands of small business loans that Stripe Capital has offered already, the revenue growth of the small businesses that have taken Stripe Capital loans shows that they on average have grown 114% faster than equivalent small businesses that haven't taken a Stripe Capital loan. It's really an amazing contrast of how such services impact these small businesses and the livelihoods of people.

Matt Henderson shared that we still have a long way to go. He says:

Most businesses, even online ones, are only selling to customers in 20 to 30 countries, some of them even less. It is a real eye-opener for realizing how much opportunity that's holding back. One of the most motivating things to work for companies like Stripe is the degree to which the infrastructure we build is used by large companies and small companies alike. This is lowering the barriers to entry for small businesses.

He continues:

Some of Paystack's users, our African subsidiary, weren't previously able to sell to customers on the other side of the city, let alone to people in other countries. The more you create a platform of capabilities that enables each user to really access the full platform in a way that is near-instant and straightforward, it creates so much economic opportunity. And even though it's simpler to understand it from a payments perspective, it's actually extremely true of the embedded finance capabilities as well, because imagine how small business loans are down in the US and the opportunity that it creates for embedded finance businesses. Imagine what that is like in Nigeria or in Indonesia or many other parts of the world where the loan options to a small business are often the loan shop next door or the local bank that says no to anybody that's smaller than a huge business.

Matt Henderson believes that embedded finance can create the same sorts of opportunities that we are starting to see in some countries now in the rest of the world, both domestically and on a cross-border basis. “I think you will see this dramatic creation of economic opportunity for people around the world, which is just a hugely impactful thing for us to be working on.”

FINANCIAL INCLUSION IN THE GLOBAL SOUTH

The Global South's recent history is marred by exploitation—material, cultural, and financial—by North America and Europe, and many regions never developed sophisticated or universal banking systems. For much of the twentieth century, this meant these nations offered little or no credit to their citizens, which hindered the growth of the middle class and the development of healthy businesses.

This also meant that the transformation brought by mobile phones in the twenty-first century was greater and brought more profound change, especially true in geographies dominated by islands like Indonesia which made access to cellular networks particularly challenging. The mobile phone became the key component in the way to do things. Suddenly a suite of offerings was potentially available and located in the pocket of most adults. In these regions of the world, fintech arrived at the same time as formal banking for the majority of the population, and from bank branches to paper checks and most of the trappings of the twentieth century, these banking norms were leapfrogged where mobile payments and mobile banking became routine.

The mobile phone has created the opportunity for near-universal access, allowing people without bank accounts to send money, as well as more complex examples like the use of the device itself as a means for employment. Over the years, there have been a variety of startups that have focused on just this. One example is from a startup in Indonesia where unemployed women used their mobile prepaid phones to sell and exchange tickets, a big market in the country, and make money off the margin. This income can be $5/day, but that extra continuous income can help lift families out of poverty and it has been shown that it lowers spousal physical abuse rates as women are active contributors to the finances of the family and therefore more empowered. There are dozens of examples like this that are encouraging to look to for the future, and embedded finance has the opportunity to be a key pillar making it happen. The explosion of creativity and innovation that results from this is yet to be fully realized.

And there is more good news. According to the Global Findex database, funded by the Bill and Melinda Gates Foundation, financial inclusion, one of the most effective means of fighting poverty, is on the rise globally.4 More than 1.2 billion adults have obtained a financial services account since 2011, and the percentage of adults living in extreme poverty is now below 10%, down from more than 33% in 1988. This is even more astonishing when we consider that the population of the world is now nearly 8 billion, up from 5 billion in 1988, and most of that increase has been in the developing world.

While we are on the right path, significant challenges remain in the way, including kleptocratic and corrupt governments, ineffective (or overbearing) regulatory structures, and more, but the companies and solutions coming out of this environment will take on problems in new and different ways than those envisioned in the developed world.

This is already happening in key geographies such as with fintech startups like Destacame, originating in Chile. Referred to on their LinkedIn page as the “free online financial management platform with the mission of improving financial inclusion and health in Latin America,” Destacame started with the simple challenge of how to utilize the data of a consumer that already exists but that banks or lenders aren't currently using.5 One of the first pieces of data they used was utility bills as it is commonplace that every home in Chile pays for this. Destacame has since expanded into other data points and other bills and now offers a suite of products that puts the consumer in control, allowing them to manage their financial life. The products include past-due debt repayment, consumer loans, credit cards, savings, and other financial health tools. This methodology of a data-first approach to improve the life of consumers is working and as of Q4 2021, according to their LinkedIn page, Destacame served more than “2.2 million users and collaborates with more than 40 financial institutions,” specifically targeting unbanked segments of the population in Chile, Mexico, and beyond. It is fair to say that this approach is working.

Let's take an example from Vietnam. A farmer is likely not going to have a full life insurance policy for his family. In Southeast Asia the data typically required for underwriting such a policy is scarce, and consequently insurers are cautious about who they give policies to. Through embedded finance, however, this same farmer could have a micro life policy covering specific aspects of what he is doing, such as working with cooperatives around his seed purchases. The seed purchase itself could have some amount of life insurance embedded into it. As described before, the same way that the insurance companies' balance sheet looks like a deposit account, the farmer could buy in and out of his insurance policy. As Nigel Verdon, CEO of Railsbank, puts it: “Embedded finance is democratizing financial services because by nature it can deconstruct financial products into core components that can be distributed at micro levels. Financial services can be brought down to a size that is suitable for inclusion.” The possibilities are endless.

One of the most iconic stories of embedded finance playing out globally comes out of Africa. M-Pesa is a system of value exchange launched in Kenya in 2005 by a telecom provider, Safaricom. The system allowed users to send money from phone to phone, and to cash out through a system of agents, which were brick-and-mortar retail locations. Today M-Pesa allows not just peer-to-peer and consumer-to-business payments, but credit and savings options as well, and operates in multiple countries in Africa and beyond. It is an entire financial system, all located in mobile phones, and not just smartphones. M-Pesa works just as well on inexpensive and widely available feature phones (Figure 6.1).

Figure 6.1 In 10 years, M-Pesa facilitated the creation of more than 30 million deposit accounts.

Source: Njuguna Ndung’u 2017 / Blavatnik School of Government

The M-Pesa service was intentionally launched with financial inclusion in mind, and required the cooperation of the banking sector and the government to operate. But the reason it worked was because the mobile phone service provider already had near-universal access to the customer, because phone penetration was widespread. The banks’ and even the government's opportunities to reach such a broad customer base were much more limited. The success of M-Pesa is now known around the world, and there are many similar use cases emerging from LATAM to Africa to Southeast Asia. Mobile phones are not the only means by which embedded finance will work in the developing world, but in today's world they are certainly the most important, as they are very nearly ubiquitous.

The impact and scale of fintech on the Global South are also felt among underserved customers in the West.

FINANCIAL PRODUCTS FOR THE UNDERSERVED

According to a Federal Reserve survey in 2019, nearly 40% of the US population can't afford a $400 surprise expense, meaning this is affecting large portions of populations around the world today (Figure 6.2). Let's explore what this looks like in more detail, particularly from the lens of the future workforce: the gig economy.

Figure 6.2 Not able to fully pay current month's bills (by layoff in prior 12 months and race/ethnicity).

Source: Federal Reserve 2021 https://www.federalreserve.gov/publications/2021-economic-well-being-of-us-households-in-2020-dealing-with-unexpected-expenses.htm

Imagine that your car breaks down because of engine trouble. Many in the world don't have enough savings to pay for the tow truck and new tire and are forced to take measures such as payday loans to pay for the essential services they need. There is a socioeconomic component to this as Zach Pettet, host of the podcast “For Fintech's Sake” and content director for Money20/20 shares:

I used to live in a really horrible part of town and I drove a really crappy car. If you were to look at me socioeconomically without a lens on the rest of my life, you would think this is a horrible credit risk for all intents and purposes. But if you look at the next year of my life after that, things changed dramatically and I was not living in that specific area anymore. But because my driving behavior was the same, regardless of what zip code I lived in and what car I drove, I would still be able to save a few hundred dollars on car insurance. The worst part is that it was just because I was living in a specific zip code that I even had to pay that initial fee that I was saving money on.

This is primarily why companies like Root have such amazing potential to enhance the lives of their customers. At the most fundamental level, Root offers auto insurance but they use this as a wedge into the larger offerings of financial services. According to their LinkedIn profile6, Root uses “data and technology to bring fairness and ease to car insurance.” At its essence, there is a large data play here building off of driver's actions. Imagine getting insurance based on how you actually drive day in and day out. The app tracks the way that you drive, monitors things like how you turn, how quickly you brake, and so on, and therefore offers you a more favorable rate based on the quality of driver you are. Insurance acts as the wedge into getting close to their customers.

It is fair to assume that the initial target customer for a company like Root are people who are tighter on money, hence why they look to Root to help them save on auto insurance. These are likely the same people who, if on the way to work run into auto trouble, may very well likely need to take out a payday loan to pay for repairs. Because these customers already have a relationship with Root and Root has the data on them, it would make natural sense for Root, through embedded finance, to provide the loan right at the moment the problem occurs or the check engine light comes on. Because of the data that Root has, because all of the background work has already been completed from KYC (know your customer), to compliance, etc., Root is best positioned to offer this to the driver. As Pettet states: “I don't think people really think of companies like a Root as something that is interesting. But if we look ahead 10 years, we're going to say ‘Oh, that's what data means to the world.’ And that's what an underwriting advantage means to the world.”

THE GIG ECONOMY: THE NEW WORKFORCE

We have already heard how rideshare companies like Grab and Uber are providing financial services to their drivers through their apps. Those engaged in the so-called “gig economy” are often financially vulnerable, lacking savings to draw on in emergencies, and require specialized services because they receive nontraditional payments for their labor.

The term “gig economy” has become widespread, but it risks being misunderstood. “Gig” refers to contract work, payment for specific tasks rather than hourly or salaried wages. But the term should not be taken to imply gig workers are only driving for Uber, for example, as a side job. Millions of Americans and workers worldwide depend on nontraditional work such as that in the gig economy for their primary earnings. The idea that independent non-salaried work is casual, secondary, or a side hustle is as harmful and incorrect as the notion that only teenagers or those just entering the workforce perform minimum-wage jobs.

Gig economy work has expanded rapidly in recent years, and was accelerated by the Covid pandemic that saw white-collar office workers remain safe at home while deliveries of essentials were performed by contract workers for comparatively low wages. Some estimates put gig economy participation among American workers as high as 36%.7 The job service Upwork says there are 59 million independent workers in the US, and it expects 86 million by 2027 (see also Figure 6.3).8

The “creator economy” has further accelerated the boom of gig workers where people are paid for specific services and/or unique assets. While there are some in this world that have made large sums of money, many others suffer from feast or famine based on when their items sell. These workers suffer from irregular and often unpredictable pay, and often lack traditional healthcare and rely on nontraditional financial services, such as check-cashing. These workers take many shapes from drivers to on-call workers, those holding multiple jobs, and seasonal or itinerant workers. They don't have time to go to a bank, and banks haven't traditionally wanted their business as their income can be unpredictable.9

Figure 6.3 The future of the gig economy.

Source: https://www.rolandberger.com/en/Insights/Publications/The-future-of-the-gig-economy.html

Embedded finance is in a perfect position to assist this next generation of workers through a concept called earned wage access. The concept is simple: through earned wage access people are paid for the labor they incur that day or the project they complete or the moment their asset is sold. This is a basic but fundamental shift in society and one that has long-term impact.

Let's say, for instance, that your utility bill is due the 28th of each month, your car payment is due the 30th and your paycheck comes bimonthly, typically getting paid out the last day of the month. If you are living paycheck to paycheck, these two bills as described above come days before you receive your paycheck making it less likely you will be able to pay them on time, thus incurring late charges, and it snowballs from there.

Now imagine instead that you have the money the same day you earned it. You would then have the ability to pay on time without incurring late fees. This is not some far-off concept only applicable to the outliers of society and edge cases. Getting paid when you do the work will change people's lives.

Financial services need to be rebuilt from the ground up for nontraditional workers, from their first paycheck to filing taxes. Square recently announced it was offering free tax services to its customers. And as anyone who has been self-employed or done freelance work knows, taxes can be extremely complex, even when relatively small amounts of money are involved, and it takes a fair amount of knowledge and research to correctly identify how much to withhold throughout the year so that when tax time comes, people aren't left owing a tax bill they can't afford to pay.

Fintech has made some inroads into taking business from exploitative industries like check-cashing, which charge exorbitant fees for giving customers access to their money to offer cheaper fees to access money. While these up and comers are gaining traction, they still lack the scale to reach the many millions engaged in gig work. Embedded finance is a crucial component in opening up the true scalability of such products for society.

Uber and Grab

Uber and Grab, two companies that we have referenced a handful of times now, are key examples of embedded finance in action through the implementation of earned wage access, paying drivers salaries on the day they provide the rides as opposed to waiting until the end of week or month. These companies take this a step further by also providing loans, money for gas, etc., to their drivers, enabling them to work more and provide for their families.

Uber is a leader in offering services to its drivers through its relationship with Green Dot Bank, which offers instant access to earnings, small-dollar loans, and credit products, and also includes tax services to its drivers. Because every driver has to have an Uber app, the company can reach every single driver naturally in an experience they are already accustomed to. The company is the key here, but it can't do the work alone. We have mentioned the bank partner, and there are also startups that fit into this ecosystem, helping employers and other companies meet the specialized needs of gig workers. Providing financial services to gig workers is a win-win for employers/platforms (Figure 6.4).

With 6 in 10 people underbanked or unbanked, and 9 in 10 people lacking access to credit cards, the opportunity of driving financial inclusion in Southeast Asia is massive.10 This opportunity became obvious very early on for Grab as they were setting up their transportation services offering. Indeed, most drivers didn't have access to basic banking services and at this time Grab was making partnerships with various banks and financial services providers to enable them to receive the payments from the drives they were completing, spend the money for their day-to-day needs, and insure themselves against accidents. Having identified this gap in the market and being conscious of their unique position, possessing the data and as a driver partner and merchant relationship owner, Grab decided to launch its own line of financial services.

Figure 6.4 What do consumers want bond webinar.

Source: Cornerstone Advisors.

The company launched GrabPay in 2018 and then further services with micro-lending, insurance, and wealth management. They use the data they gather on their users to design products that are relevant to them and price their financial services according to the risk profile of each user, allowing them to make those services more affordable than a standard financial services provider. They also offer insurance products such as driving insurance or critical illness to those people who would not get it offered by traditional companies and adapt the premiums of those services based on the behavior of their driver partner and merchant users.

UPSKILLING TODAY'S WORKFORCE

We can't consider the social impact of embedded finance without considering how it affects current and future employment prospects.

The shifting financial landscape will create new jobs, as brands big and small will start needing experts within financial services to offset their product team. We are already beginning to see this shift take place and we know we are still in early days. According to LinkedIn, as of December 2021, Apple had roughly 30 people on their team with the word fintech in their title, Amazon proper (not including Amazon Web Services or other ancillary businesses) had roughly 45 people, and Microsoft had over 90 people with the word. This doesn't account for the hundreds of engineers, product designers, and marketing teams built around these offerings. At one point in time, the brightest minds were flocking into finance, then the shift went into the large tech companies, and now there is a big movement toward decentralized finance. Through embedded finance as an enabler, financial services in general will become the hot commodity again. Maybe then people will stop asking us what in the world we do for our careers:)

Fintech, with its emphasis on automation, has always had an ambivalent relationship with jobs. Yes, as the banking industry continues to undergo digital transformation, new jobs were created, attracting new types of talent. However, through automation, and the new digital world, certain roles and responsibilities will be replaced, leaving people feeling uneasy. Employment has changed dramatically as the digital economy, with its self-service and automation, has gained market share from the traditional offline economy. Skills of the present are not always skills of the future and the jobs of the future mostly don't exist yet. Some jobs requiring less traditional skill sets have been automated out of existence, while some jobs requiring high levels of specific skill are no longer relevant.11 New skills are needed as is the new training to teach those skills. Some old-school jobs (calling all COBOL programmers) remain in high demand.

It is quite obvious that there will be many opportunities for new talent to enter the space but this movement will also require retraining many employees with outdated skills, a topic that is front and center in leaders' minds as they think about the future of work. Just because we are seeing a new trend driven by technology with financial services as the backbone, there is no reason we can't build upon the expertise of the talent within existing teams to equip them with the knowledge and skills necessary for the future. There is a big opportunity for the subsets of the working population within financial services that are at risk of their jobs being made redundant by technology to embrace the concept of embedded finance and use their background as a strength for companies outside the traditional industry (Figure 6.5).

Without a concerted effort from governments and industry leaders to reorient the workforce to be able to take on the jobs of tomorrow, many workers will be left behind. There is a big opportunity for talent to upskill and potentially change jobs better suited for the new world. In order to aid in this development, both public and private sectors need to have a clear plan for where the industry is going, about which roles will need to be upskilled or repurposed, and a strategy on how best to get there. This has consequences beyond merely the economic effects of unemployment and stagnating wages. The consequences have been shown to be much worse. There is strong evidence that the transforming economy and the workers it has left behind have contributed to the rise of populism and political extremism in both Europe and North America and, as such, it is imperative that we think strategically about equipping the modern-day workforce for the future.

Figure 6.5 Fintech employs more people than many financial centers.

Source: CFTE 2021 https://courses.cfte.education/wp-content/uploads/2021/11/The_Fintech_Job_Report_2021_CFTE.pdf

With embedded finance, the most important jobs in banking will have to do with APIs and configuring connections to outside parties. This is nothing new to banking. After all, the ATM was first introduced 50 years ago and began the long process of reducing branch staff. The process continued with digital banking on the desktop and mobile banking. The pandemic, with its limitations on human interaction, further advanced this trend. The 2020 Financial Services Talent Strategy Report notes that bank teller roles declined more than 30% during the first year of the pandemic. And while the retention rate of bank branch staff has always been relatively low compared to other roles within banking, that doesn't mean we can't use this shift to open up a new career path for people. After all, as anyone from HR will share, it is more expensive to train a new employee than it is to retain an existing one.

The talent strategy one chooses is as varied as the company, but again, through embedded finance, there are huge opportunities as most companies offering embedded finance will need to some extent (more or less depending on how they decide to operate) internal resources skilled in fintech, banking, and regulated environments. There are several ways you can address the opportunity: upskilling internal staff, onboarding half of the staff externally and balancing the other half with internal resources, or looking purely external.

There is certainly a lot of opportunity in the future of embedded finance from a talent perspective. The question then becomes, what skills should companies look for to build out their embedded finance teams?

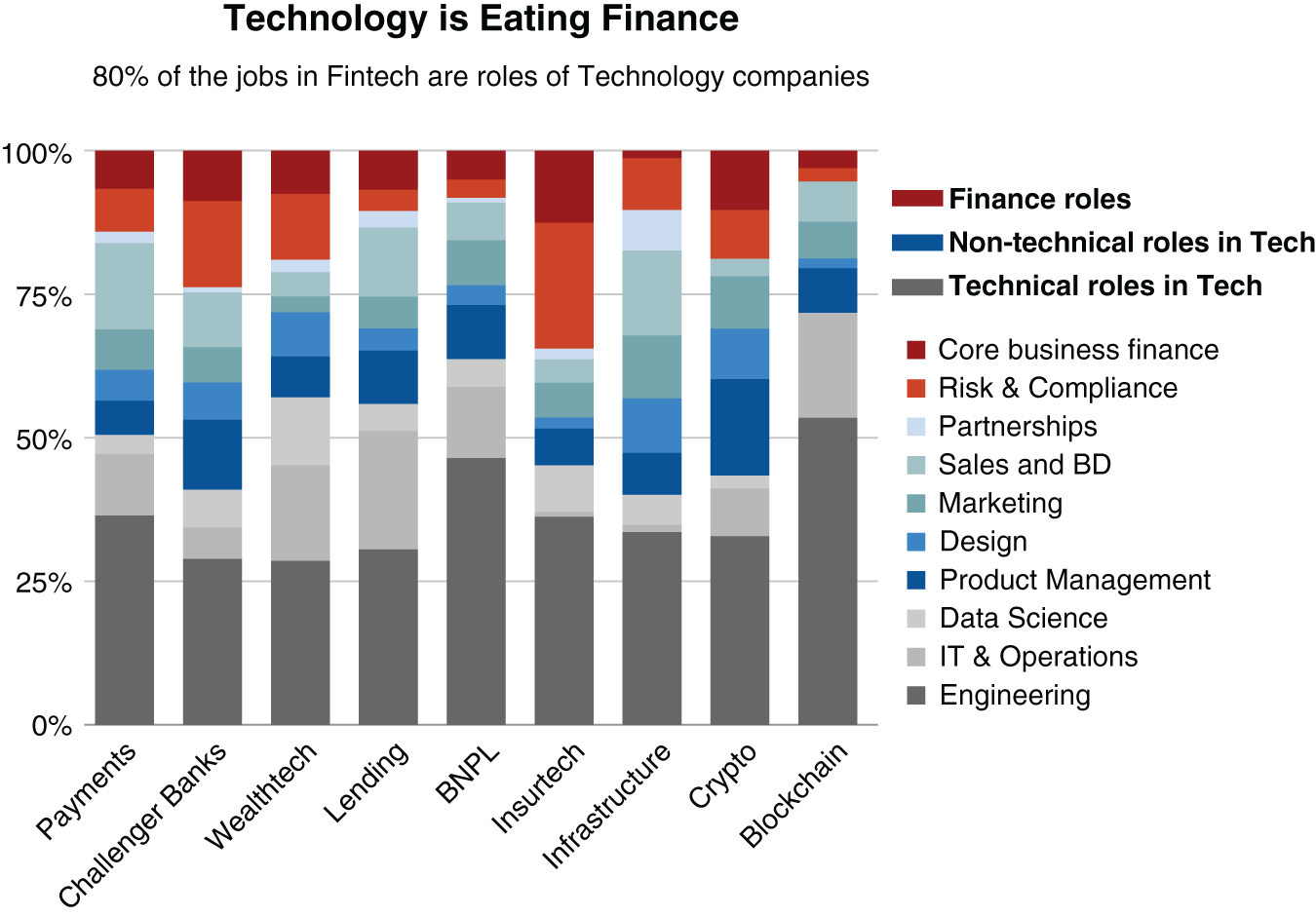

The Centre for Finance, Technology, and Entrepreneurship (CFTE) recently published the fintech job report, including the analysis of the more than 40,000 jobs existing in the 225 largest fintech unicorns across the globe. Tram Anh Nguyen, co-founder of CFTE, explains that even now, technology skills are already more important than finance skills and there is data to back this up. She says: “If you look at Citi, one of the largest banks in the world, it is striking that more than 50% of the current job openings are related to technology.” She outlines that, on top of hard skills, soft skills, and mindset (including an entrepreneurial or, in corporate-speak, intrapreneurial spirit), and the ability to work with diverse teams in a cross-functional context, will play a key role in making those embedded finance teams successful (Figure 6.6). Her wildest guess? In 2030, most big tech companies will have an embedded finance team with very diverse backgrounds and skill sets.

Figure 6.6 Technology is eating finance. Source: CFTE 2021 https://courses.cfte.education/wp-content/uploads/2021/11/The_Fintech_Job_Report_2021_CFTE.pdf

When speaking with Tui Allen, product director from Shopify, she identified two key talent areas that she believed were crucial for success as embedded finance becomes more mainstream. The first area is around a team that are experts in pricing and monetization strategy. “So often, it is easy to get caught up in the excitement of offering financial services, but to really enable the win-win-win mentality, having a concrete pricing strategy is crucial,” says Allen. The second area involves compliance and regulation. With a commerce platform as global as Shopify, it is imperative to have team members who are experts in the areas of compliance and regulation. As Allen puts it:

Financial services is a very complex environment in terms of compliance and regulation. This is true regionally as well as internationally. Just keeping up with different changes in regulation. Whether it be country to country, or region to region is incredibly important. Having the right structure in place to keep a pulse on that and also to make sure that you're doing your due diligence in advance to avoid situations where you have to potentially have a bunch of rework or potentially can't enter a certain region or market.

Allen is absolutely right. This type of talent is crucial for entering the world of embedded finance and is a great opportunity for those already within financial services to branch out of their traditional roles or, on the pricing strategy side as an example, to potentially leverage talent with a data and statistical background who might not have historically leaned toward a big brand like a retailer or other.

We have seen this impact on job creation in China at a massive scale. Yassine Regragui, fintech specialist and expert on China, shares that through embedded finance in the country and the job creation induced by the development of those solutions, an estimated 40 million jobs have been created by Alibaba alone and 3 million jobs have been created by Tencent.

SUSTAINABILITY

BBVA is one of the most important financial institutions taking an active role in sustainability now and for the future. Javier Rodriguez Soler, BBVA's global head of Sustainability, believes that the bank's strategy related to sustainability is one of the two key pillars that differentiates the bank, stating: “Sustainability is a key component for the life of individuals, SMEs and big corporations.” BBVA sees sustainability as much more than just an aspect of their nonprofit endeavors, but rather as core to their overall business. They believe that sustainability carries a large business opportunity, particularly in the world of ESG, also known as Environmental, Social and Corporate Governance, centered around climate change and decarbonization. In his role, Javier duly reports to the chairman for strategy and the CEO for all things business-related. The key business units across the bank in turn co-report to Javier.

BBVA is not the only financial institution taking an active role in sustainability. In 2021, at the latest COP26 conference, also known as the United Nations Climate Change Conference, the banking sector stood out as having one of the strongest levels of commitment across all sectors. According to Javier, it is believed that $7 trillion per year is going to be needed in the next two or three decades to invest in decarbonization across industries. A lot of this money will come from the public sector and off large companies’ balance sheets but a significant portion of this will be channeled through banks, as it has in the past. To have the type of impact they need, BBVA believes they need to mobilize hundreds of billions themselves, and other banks agree.

What does a commitment like this actually look like? BBVA has set out a commitment with portfolio alignment in five sectors in order to reduce the relative emissions of their clients, impacting primarily large, corporate clients across coal, power sector, road transportation, cement, and steel; and BBVA is working on a similar approach for oil and gas, aviation, shipping, real estate, and agriculture. Reducing the relative emissions of CO2 or equivalent relative to the unit of energy. BBVA commits to this reduction with each client. BBVA works with each respective client to understand the plan to decarbonize; if they don't have a plan, BBVA will work with them to create a plan, and for those clients that commit, BBVA is willing to bank them further, provide larger loans, and other advantages. They take this approach on a sector-by-sector basis, and if clients don't commit in the way they are expected to, BBVA will no longer bank them.

As outlined above, for sustainability to succeed, there has to be a business opportunity behind it. Inclusive growth investing needs to be done in a way for profit. This investment benefits not only the environment but people as well. BBVA is actively doing this in geographies across the world, having a direct impact on people's lives by giving credit cards to individuals who haven't had them in the past, opening accounts for portions of the population in Mexico and the rest of LATAM that were completely unbanked, and so on. This is a primary example about how embedded finance is good for society as a whole. As Javier puts it:

Our presence in emerging markets, both for decarbonization where most of the investments are going to be needed, and the social inclusion, gives us a privileged position versus other banks in the world to be leading this sustainability as a business linked with embedded finance. Embedded finance is already including all the sustainability aspects. I believe we will start hearing about embedded sustainable finance quite soon.

Embedded finance is evident in BBVA's banking app, which also includes components around sustainability. Through the app, customers can track habits including monitoring your carbon footprint through your transportation methods and your health. The goal of including such components inside BBVA's mobile app is to encourage their customers to live in a more sustainable way, emitting less CO2.

Another point Eduardo Vergara, managing director and global head of Transaction Banking Product and Sales at Goldman Sachs, makes is that embedded finance propositions can be used to incentivize companies to improve their offerings or achieve specific goals. He mentions: “One of the things that Transaction Banking at Goldman Sachs is doing is offering an ESG deposit account for companies. Those companies are offered higher yield on these accounts when they reach their ESG goal. That's another way where we can see how some of these embedded finance offerings can have a large positive impact on society.”

Yassine Regragui believes that embedded finance has been leveraged to create some environmental impacts on China as well. He states:

Ant Group launched a new feature called Ant Forest, which is a game provided by the app where the more the user uses the app or walks, the higher level of virtual energy they collect to reach certain levels. When those levels are reached, a certain number of real trees are planted in China. Around 200 million trees have been planted so far.

Tracey Davies, president of Money20/20, knows only too well the importance of this topic. She says:

At Money20/20 our goal is to reflect what the industry is thinking about but also to lead the agenda. We have always had a strong theme at the shows around fintech for good, reflecting that the industry contributes more than just profit but that the product innovation that comes from this sector can impact society and business as a force for good. Now, we have a situation that is not just about good but clearly a critical emergency for the world and one that governments, business and all of us have to lean into.

As outlined with banks like BBVA and Goldman Sachs, there have been some strong initiatives emerging, and sustainability has made its way front and center to the UN, who appointed the former Bank of England Governor Mark Carney as the Special Envoy on Climate Action and Finance. In a recent interview on the UN's website, he spoke about how private finance is increasingly aligned behind achieving net-zero greenhouse gas emissions, where emissions produced equal those removed from the atmosphere.12

He emphasized that with any large-scale movement, whether social or environmental, there will be cynicism and that we all want to avoid greenwash and to ensure that we are getting genuine progress and solutions. It is clear that the financial services sector can have an agenda-driving role in this if it chooses to, and choose it, it must.

THE LIMITS OF EMBEDDED FINANCE

While we are advocates for the benefits of embedded finance in the future, it is important to note some of the challenges that embedded finance will create on society and where there are potential limitations. As we have referenced numerous times, the seamless, frictionless nature of embedded finance allows users to make purchases immediately without even thinking about it. While this is a great experience from a UX perspective, the psychological nature of it is much more complex.

Embedded finance also tends to privilege convenience over privacy, as Dave Birch and others have pointed out, and this issue will be explored in more detail later in this book. Issues relating to identity fraud, privacy, and data ownership are massive, and should not be minimized just because they remain largely unknown. We will continue to learn more about each of these problems, and the education will be painful and expensive. Participants in embedded finance must be advocates for responsible use of data and identity, even if regulations and customer sentiment have not yet caught up to the dangers.

Over the holiday season, we spent time shopping for presents with a friend. In every store we entered, the friend paid for her purchases with cash. Over the course of the day, she had spent over $350 on gifts. A bit perplexed, we asked why she chose to pay cash for all the gifts; it seemed cumbersome and even a bit dangerous to carry that amount of money. Her response was simple: “Cash is tangible, I can feel it. I can see it. I know it is there and I can see it leaving my wallet. It holds me accountable.” This was a profound statement. There are a myriad of reasons as to why large portions of the population are financially insecure. As a society, we, and the governing bodies around us, have the responsibility to help people make the best financial decisions for them.

One key trend playing into this over the last few years is the concept we have discussed at length, Buy Now, Pay Later (BNPL). BNPL companies are exploding around the world with many going public in 2021. Not all companies in the space can be considered equal. They serve different target markets with different spending power and purchasing needs. Optimists will point to the ability for people to purchase necessary items like repairs for their cars to get to work when they need them most. Skeptics point to the fact that BNPL offers loans to people for luxury items they don't need at the point when they are the most likely to take it, resulting in people getting into even greater debt. Credit Karma conducted a survey with consumers using BNPL in early 2021 and found that nearly 40% of all respondents who have utilized BNPL have fallen behind on payments at least once and “almost three-quarters of people with a late payment say they have seen their credit scores drop.”13

THE QUESTION OF IDENTITY AND PRIVACY

As Ping An demonstrates, embedded finance has applications beyond offering financial services in another context. One of those is managing our identities. “Identity” is shorthand for authenticating ourselves, or proving that we actually are who we say we are. Banks have considerable expertise in this area, and with good reason. If they handed out money to the wrong person, that was a serious problem. In the old days, you would walk into the bank branch and prove your identity with a driver's license or passport, or even your signature. When accounts were opened, banks would require account holders to sign signature cards, which could be used to verify the signatures on checks and other items. As late as the 1990s and early 2000s in the US, customers were asked to sign paper forms when they wanted to move money between accounts or to another account holder.

Today identity is much more likely to be verified by digital methods, but these authentication methods can be intrusive or annoying. Dave Birch is one of the leading authorities on identity in the world. Speaking of cases where embedded finance might help consumers, Birch said:

I think one of the simplest examples is where you're just trying to prove that you exist, that you're a person, not a bot. For a lot of online services, we can't even do that at the moment. So the services that are being provided through the embedded finance channel don't have to be transferring money and things like that. It can be other things, and I think that's underexploited at the moment.

Birch points out that the use cases don't even need to be related to finances. There may not be any money changing hands. Birch commented:

So if I take a really simple example, if I go and sign up for an internet dating app, how does the internet dating app even know that I'm a real person and not a bot? We're already used to situations where you go to sign up for something and you get bounced through Plaid to your bank account to sign in, not because they want you to pay anything or transfer any money, but because they want access to some other credential that can be provided through financial services.

Banks have had a stake in identity because they have a history of needing to know who you are. They also have the related task of securely storing data as well as money. Birch and a few others in financial technology have long advocated for banks to expand their services in these areas, but today when we think of ways of authenticating ourselves digitally and storing important data, most people think of Google and Apple rather than Wells Fargo or BNP Paribas.

But embedded finance goes beyond the banks to include tech companies, and Birch points out that these companies too struggle with identifying users. “Who is it that knows you're a real person?” Birch asks.

Twitter doesn't know whether I'm a real person or not. Facebook doesn't know whether I'm a real person or not, but the bank does know whether I'm a real person or not. And so those kinds of examples are maybe the more interesting areas. Like in the UK, the government was going to pass a law that you had to be over 18 to access certain kinds of services, adult services, gambling, that kind of thing. But we have no ID card, same as in America, and we have no idea who anybody is or how old they are or anything like that. So who is it that actually knows that I'm a real person, that I'm over 18? It's the bank. So it makes sense for that to become a tokenized credential that the bank can provide. There are fantastic opportunities for growth in embedded finance for financial services, payments and so on. But I also think there are really interesting opportunities for growth in other areas that are related to credentials and reputation and participation in the new economy.

Tokenization is a way to protect valuable or sensitive data, such as your name, social security number, credit card number, and so on. To do this, the sensitive data is replaced with secure data that, if intercepted or discovered by a third party, cannot be used because keys are required to unlock the information. The intercepted information is meaningless without the keys to unlock it, and even powerful computers lack the computing power to unlock tokens. Some experts argue that quantum computers, which are vastly more powerful but, as of this writing, still in their very early stages, will pose a threat to tokenization, but that day is not yet here!

Identification versus Authentication

Birch points out that though “nerdish,” there is an important distinction between authentication and identification, which are often used interchangeably, and the distinction has to do with privacy.

When I buy something with my Apple Pay and I use Face ID, that's authentication. The phone is just checking. Am I on the phone? It doesn't know that I'm Dave Birch or anybody else, the phone's just checking, Is this the right person to do this? And actually, that's a very good way of doing things. It's not particularly because it's a security technology, but because it's a convenience technology. People will do it because it makes things easier and increases the overall security of the system. Biometrics as an identification technology is very tempting, and I can understand exactly why. It's the idea that, when you walk into the store and the system knows it's me, then I just go and buy the stuff I want. And then that's very tempting. But I just wonder if it just makes me uncomfortable, that level of identification. Because you can't turn it on and off. I can choose whether to turn on the loyalty program on my phone and walk in, or I can choose whether to run the supermarket app when I'm walking around the store, but I can't choose to turn my face off. It doesn't really work like that.

Birch may not be among the most enthusiastic shoppers at Amazon Fresh stores, but he points out that, in 2022 at least, most shoppers are wearing masks, which foils the technology anyway!

Chris Skinner, author, commentator, and founder of The Finanser blog, notes the common use of payments enabled by iris, face, and fingerprint recognition, specifically in China, and in the future, can happen by identifying the way you walk, which would be the ultimate act of embedded payments. We could get to the stage where we walk around, and pay for things based on just where we walk and how we walk. While there are so many ways in which technology is improving our lives, it can to some extent also become intrusive on how we live. The more identified or identifiable, the more potentially our lives become tracked and traced. So privacy versus identity is a very important issue that must be resolved.

Because embedded finance depends on identifying or at least authenticating people digitally, it favors payment methods that carry a great deal of data and context. This means that cash, which can be used anonymously and carries the least amount of data for merchants and financial services providers, is poorly suited for embedded finance. Privacy advocates often consider this aspect of cash a plus feature rather than a bug, but it also presents something of a paradox for embedded finance. As we have noted previously in this book, embedded finance is an important tool for financial inclusion and even lifting people out of poverty, and the impoverished and underserved are the most likely to be dependent on cash in their daily lives. There are often good reasons beyond privacy concerns that an individual might be cash-dependent. They may be paid in cash and lack access to an account to convert the cash to digital value. They may reside in a remote or underserved region. They may even be someone in an extreme situation such as being a political refugee, homeless, or fleeing domestic violence.

Cash use is in decline across the planet, even in countries where cash usage is common. But today there are more ways than ever to convert cash into digital value. Startups such as PayNearMe, founded in 2009, and Square's Cash App allow users to convert cash at the point of sale at brick-and-mortar locations into digital value. In Africa, Jumia allows cash payments upon delivery of orders placed digitally, and services like M-Pesa allow cash handed to physical agents to be converted to value that can be stored and spent on an account accessed by mobile phone. Ultimately it is likely that cash use will continue to decline until it remains only for specific use cases, and embedded finance by its nature is unlikely to feature prominently among those cases.

THE NEW WORLD

It is clear that embedded finance has the potential to make a fundamental impact on the world as we know it—from ESG, to financial inclusion, to the next workforce. What will the growth of embedded finance look like over the next decade? Who are the companies poised to take advantage of it? What will our everyday transactions look like when embedded finance is embroidered naturally throughout our financial lives? Let's explore the world of embedded finance in 2030.

NOTES

- 1. https://thefintechtimes.com/crypto-market-size-is-up-to-221-million-users-finds-crypto-com/ Accessed January 3, 2022.

- 2. https://www.fdic.gov/analysis/household-survey/index.html Accessed January 11, 2022.

- 3. https://www.federalreserve.gov/publications/2019-economic-well-being-of-us-households-in-2018-banking-and-credit.htm Accessed January 11, 2022.

- 4. https://www.worldbank.org/en/news/press-release/2018/04/19/financial-inclusion-on-the-rise-but-gaps-remain-global-findex-database-shows Accessed January 15, 2022.

- 5. https://www.linkedin.com/company/destacame/about/ Accessed January 15, 2022.

- 6. https://www.linkedin.com/company/rootinsurance/

- 7. https://www.smallbizgenius.net/by-the-numbers/gig-economy-statistics/#:~:text=About%2036%25%20of%20US%20workers%20are%20part%20of%20the%20gig%20economy.&text=If%20the%20gig%20economy%20keeps,41%25%20of%20postgraduates%20freelance. Accessed January 15, 2022.

- 8. https://investors.upwork.com/news-releases/news-release-details/upwork-study-finds-59-million-americans-freelancing-amid Accessed January 15, 2022.

- 9. https://www.rolandberger.com/en/Insights/Publications/The-future-of-the-gig-economy.html Accessed January 3, 2022.

- 10. https://assets.grab.com/wp-content/uploads/media/ir/investor-presentation.pdf Accessed January 3, 2022.

- 11. https://courses.cfte.education/fintech-job-report/?gclid=Cj0KCQiA8ICOBhDmARIsAEGI6o16HKHYzWnT1_chiiee9OAyJHHHpG28ZHqOF_oV3JxGAlkMNQxmCzkaAr2pEALw_wcB Accessed December 20, 2021.

- 12. https://www.un.org/en/climatechange/mark-carney-investing-net-zero-climate-solutions-creates-value-and-rewards Accessed January 13, 2022.

- 13. https://www.creditkarma.com/insights/i/buy-now-pay-later-missed-payments Accessed December 31, 2022.