Preface

Managing employee benefits is growing ever more complex. These programs can be costly and take up more of management’s time than they have in the past. But the employee benefits program is a key part of a human resources strategy. And human resources (or as referred to these days, human capital) is now considered a critical element of the overall business strategy.

Many elements are involved in the management of an employee benefits program, including the following:

• Proper financing and funding of the benefit program

• Accurate actuarial calculations to determine the plan assets and liabilities

• Complying with required laws and regulations

• Proper accounting and recordkeeping, according to the governing accounting standards

• Tax compliance

• Effective administration and communication, including enrollment and eligibility determination, carrier data management, premium billing, employee benefits communication, call-center support, and so on

In addition, various pressures must be dealt with, including rising costs, managing risks, shrinking budgets, improving employee productivity, continual shifts in legislative requirements (the uncertainties surrounding the Patient Protection and Affordable Care Act of 2010 is a prime example), and higher expectations of the workforce. Within this complex structure, the key element in managing employee benefits remains the financial and accounting aspects of these programs.

The employee benefits environment is replete with accounting and finance issues. In addition, there are a plethora of tax, insurance, and legal considerations. Cost and expense considerations dominate the design, planning, and administration of these plans. Accounting and finance, the languages of business, are widely spoken. Therefore, the guardians of these benefit programs, with many working identities, more so than ever, all need to understand and communicate among themselves using those same languages—finance and accounting—proficiently.

In the past 20 years or so, the benefits landscape has shifted. The guardians of these programs are trying to balance the competing demands of rising benefits expenditures—mainly fueled by healthcare costs—against the need to attract, retain, and then maximize the productivity of their human talent base, their employees (or, as mentioned previously, their human capital). This is creating the need for a new mindset: the need to gain more human capital value and, at the same time, manage the financial exposures.

As stated, to traverse the employee benefits landscape effectively, a new common mindset is needed. The purpose of this book is to lay a foundation for this new common mindset by providing an understanding of employee benefits primarily from finance, accounting, and other technical perspectives. To effectively manage and administer employee benefit programs, one needs to use the required finance and accounting languages and terminology. The practitioner needs to understand the principles of finance and accounting as they apply to employee benefits planning.

Also, within the finance and accounting genre, the subgenres of tax, risk mitigation, and actuarial principles heavily affect employee benefit programs. Thus, the employee benefits landscape can get complicated. Clarity of understanding is essential for the practitioner.

With the ever-increasing pressures to improve organizational productivity and efficiency, we have witnessed a relentless drive to manage costs and expenses. However, outside environmental factors have produced counter trends in the costs of these programs. Leading these counter trends has been healthcare benefit costs. Recently, with wages advancing only 1.7%, and with employers shifting more healthcare costs to their workers, a 4% increase in medical premiums has been observed. This increase seems to eclipse the general inflation rate of 2.3%. Insurers had planned push premiums up another 7% in 2013 and beyond.1 To some this might seem onerous, given the current business and economic environment. You can understand, therefore, that the employee benefits practitioner will continue to be challenged to speak and be guided by the finance and accounting languages when designing, planning, and administering employee benefit programs. This book is designed to help in this effort.

1 Morgan, David. “Employer healthcare premiums outpace inflation, wages.” Reuters, September 11, 2012, http://www.reuters.com/article/2012/09/11/us-usa-healthcare-insurance-idUSBRE88A0SQ20120911.

There is also indication that senior management is increasing its focus on employee benefits planning and decision making. It can easily be surmised that the reason for this focus is the control of the escalating expenses. A Prudential Insurance Company study, “Sixth Annual Study of Employee Benefits: Today and Beyond,”2 indicates the following:

2 The research was conducted for Prudential by the Center for Strategy Research, Inc., an independent Boston-based market research firm, in 2011; see www.prudential.com/benefitsbeyond.

• Senior management’s influence has increased in the past 5 years (45%). Human resources is the second most common area to gain in influence (39%). Employee benefits, finance/treasury, employees, and board of directors all increased their influence relatively equally (22%, 22%, 21%, and 21%, respectively).

One reason for the increased influence is the fact that employee benefits program costs are now considered one of the highest line item operational expenses—not only that, it is a line item expense that is on the rise. Hence the need for focus, influence, and control.

• Two-thirds of plan sponsors say four or more areas of their organization are influential in the employee benefits decision-making process, 45% say four to seven areas are involved, 21% say eight or more areas are involved, and only 34% report zero to three areas are involved to some extent.

Therefore, it is important that there be a common understanding of the finance and accounting principles and issues affecting employee benefits program design and planning—the purpose of this book.

Many employers find that the cost of providing their employees adequate and competitive benefits has been one of their largest expenses, typically representing the second or third line item budgeted expense. These soaring costs are reducing capital that employers could better use for other operational expenses and working capital requirements. Significant escalation of the costs of these programs directly reduces free cash flows. A decrease in free cash flows reduces the intrinsic values of the affected entities. Stockholders do not like to see decreases in intrinsic values and hence the stock price.

Managing these escalating costs is possible. However, it requires first that the guardians of the employee benefit programs thoroughly understand the finance, accounting, and other technical principles affecting employee benefit programs. Then there is a need to make more informed, immediate, and aggressive investments in measuring, analyzing, and reporting and using appropriate finance and accounting metrics. In addition, the traditional financial analysis tools (such as analysis using key ratios, rate of returns on investments, and economic value added analysis) should be brought into the employee benefits design, development, and administration framework. The finance and accounting disciplines of analysis, measurement, and control should be rigorously used. The primary purpose of this book is to focus on these concepts.

Legal requirements for plan audits represent another important reason why the finance and accounting principles affecting employee benefits must be understood. Audits are an important part of the financial reporting structure of the Employee Retirement Income Security Act (ERISA). Audits ensure that a plan’s financial statements have been subject to an annual independent examination and that the plan’s processes and financial controls have been examined. The plan audit and reporting requirements help assure participants that there is a high likelihood that the plan’s financial statements accurately set forth the financial condition of the plan and that participant records are appropriately maintained.

Internal benefits professionals need to recognize the importance of the auditor’s evaluation of a plan’s internal controls over financial reporting. Effective internal financial controls can form the foundation of a safe and sound financial administration. A properly designed and consistently enforced system of operational and internal financial control would help a plan’s fiduciaries safeguard the plan’s resources, produce reliable financial reports, and comply with laws and regulations. Therefore, here again, an understanding of financial and accounting principles is vital.

Most senior business executives recognize the current precarious economic climate, and rather than reducing focus on employee benefits, they are finding that putting an accounting- and finance-based business focus on these programs actually creates the opportunity for employee benefits to drive the maximization of human capital.

The main objective of this book is to satisfy the need for a published text that aggregates and synthesizes the finance and accounting (and the related tax, legal and actuarial) principles into an integrated employee benefit framework.

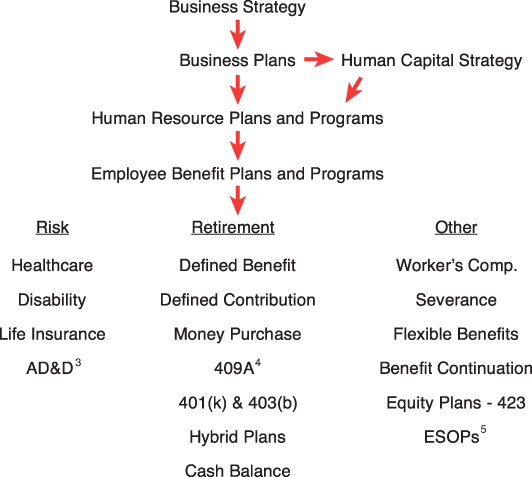

This framework can be further integrated into a total compensation structure that, in turn, flows from a human capital strategy, which was an outcome of the organization’s business strategy and operational plans. Figure P.1 explains this conceptual framework.

3 Accidental Death and Dismemberment

4 The numbers in this diagram refers to IRS Code numbers

5 Employee Stock Ownership Plans

Note, as well, that the practitioners in the employee benefits profession are many. They come from the various disciplines that impact employee benefit plans and programs. You can see the influence of employee benefits lawyers, accountants, benefits consultants, insurance industry personnel (agents and brokers), group insurance specialists, actuaries, regulators, investment specialists, plan administrators, trust officers, and, last but not least, the human resources department personnel (the benefits and compensation staff).

Professionals in this last category are mainly accountable to senior management for the design, development, and administration of these programs. The HR department’s benefits professionals are supported by the other groups mentioned in the preceding paragraph. The HR department staff is not as knowledgeable, usually, in all the technicalities of the disciplines affecting employee benefit plans. That is why they rely on external advisors, consultants, and employee benefits specialists.

If you peruse the job descriptions of internal employee benefits administrators, you will find knowledge requirements such as the following:

• Knowledge of employee benefits principles, concepts, and practices

• Knowledge of governmental regulations and laws related to benefit plans

• Knowledge of Social Security, Medicare, and other retirement plan structures

• Knowledge of statistics and their practical application

• Knowledge of research and data analysis methods and techniques

• Knowledge of customer service standards, principles, and techniques

Furthermore, if you research the skill requirements for internal benefits specialists, you’ll usually find the following:

• Good oral and written communication skills

• Computer skills, especially with word processing and spreadsheets

• Strong analytical skills

Missing from the knowledge and skill requirements is the knowledge of applicable finance and accounting principles. This book is written to fill this knowledge gap.

This book can also serve as a reference source for the HR department’s benefits and compensation professionals on the finance and accounting principles that affect employee benefit programs. This book is intended as a single-source reference book for in-house benefits and compensation professionals.

HR department professionals must now, more than ever, be business savvy. HR departments are being asked to be strategic and knowledgeable about the business side of their organizations. In the past, these folks were content with designing benefit programs that were competitive or regarded as industry best practices. Increasingly, though, HR department staffs are being asked by senior management to justify the programs they recommend from an economic and financial value-added perspective. Employee benefits professionals are increasingly tasked with designing programs that are not only best practices but that also best fit their respective organizations. To justify the economic and financial value-added advantages of the employee benefit programs, HR department professionals need to have a fairly in-depth understanding of the finance and accounting principles that affect these programs and plans. This book is intended to provide that understanding.

Various sources of influence guide the accounting and finance principles affecting employee benefit plans.

The legal influences mainly derive from the following:

• Various labor laws (both federal and state)

• The Employee Retirement Income Security Act (ERISA)

• The Internal Revenue Code (IRS Code)

The accounting influences derive from the following:

• Federal Accounting Standards Board (FASB)

• Securities and Exchange Commission (SEC)

• International Financial Reporting Standards (IFRS)

• Auditing principles and requirements

• Guidance from the American Institute of Certified Public Accountants

The administrative rules, guidelines, and regulations derive from the following:

• From the Department of Labor (DOL)

• Employee Benefits Security Administration (EBSA)

• Employee benefit audit guidance from the American Institute of Certified Public Accountants

• The rules and regulations for employee benefit fiduciaries

The structure of employee benefits that is used in this book centers on risk benefits (health, disability, and life-related risk mitigations), retirement benefits (designed to provide income security in old age), and ancillary benefits (that provide a wide variety of benefits and services that maintain or enhance the employee’s life situations).

You can understand from the earlier discussion that the influences on employee benefits planning are many, and most of them emanate from accounting and finance principles.

Having made the case for a single comprehensive text that covers the whole spectrum of accounting and finance principles affecting employee benefits planning, here is the plan for this book:

• Chapter 1, “Setting the Stage,” discusses in detail the employee benefits landscape for most medium to large organizations, including all the dimensions affecting employee benefits planning: accounting and recordkeeping, finance and investment analysis, tax compliance, actuarial analysis, legal compliance, and auditing.

The rest of the book takes a functional approach to the discussion of employee benefits (which you’ll also be introduced to in Chapter 1). The functional employee benefits covered include healthcare benefits, additional risk benefit programs, equity programs affecting employee benefit plans, retirement programs, tax-deferred employee benefit programs, global employee benefits, worker’s compensation, and other ancillary employee benefits.

The discussion then turns to the impact of various accounting, finance, and tax implications for each of the functional benefits. This is the roadmap for the book:

• Chapter 2, “Healthcare Benefits,” covers healthcare benefits.

• Chapter 3, “Healthcare Benefit Financing,” continues the discussion of healthcare benefits by focusing on the healthcare economics, financing, and cost control.

• Chapter 4, “Other Risk Benefits,” covers other risk benefit programs, such as disability benefits, life insurance benefits, and long-term care plans.

• Chapter 5, “Retirement Plans,” covers the traditional retirement programs (defined contribution and defined benefit retirement plans).

• Chapter 6, “Other Types of Retirement Benefits,” covers many of the other retirement benefit programs.

• Chapter 7, “Equity-Based Employee Benefit Plans,” covers equity-based employee benefit plans, such as discounted stock purchase plans and 409A plans (among others).

• Chapter 8, “International Employee Benefits,” covers global employee plans, especially the cross-border plans such as multinational pooling and umbrella pension plans.

• Chapter 9, “Ancillary Benefits,” covers ancillary employee benefit programs.

• Chapter 10, “Employee Benefits Cost Management,” covers cost containment. As mentioned previously, the primary concern for employee benefit planners and decision makers is the constantly rising expenditures for these programs. Companies around the world are in a constant search to find ways to optimize these costs. So, Chapter 10 focuses primarily on this topic. (Cost-containment strategies and techniques are discussed within each functional benefit, but Chapter 10 aggregates these concepts in one place.)

• The Conclusion wraps up the discussion by summarizing the topics covered in this book.

As mentioned previously, the functional benefit programs discussed in each chapter within the context of the dimensions mentioned earlier are as follows:

• Healthcare benefits

• Other risk benefits

• Retirement plans

• Ancillary employee benefit programs

• Equity compensation within an employee benefits structure

• Tax-deferred employee benefit programs

To reiterate, this book focuses on the following dimensions:

• Accounting and recordkeeping

• Tax compliance

• Auditing and internal control

• Legal compliance

• Actuarial analysis

• Finance and investment analysis

The relevant accounting, finance, tax, and legal concepts are described, discussed, and analyzed for each category of the functional employee benefits covered in the book. The optimum combination of these functional benefits normally forms the strategic portfolio of employee benefits in an organization.

This book covers relevant issues within the context of authoritative guidance provided the rule-making bodies, such as US GAAP (Generally Accepted Accounting Principles) and IFRS (International Financial Reporting Standards), and the guidance provided the American Institute of Certified Public Accountants (AICPA). This book also covers regulatory standards on relevant subjects from the Employee Retirement Income Security Act (ERISA) and the Internal Revenue Service (IRS).

It is known that the two primary accounting standards-framework, US GAAP and IFRS (developed by FASB and IASB—the two accounting standard setting bodies) are on the verge of converging. The convergence process is well on its way. The year 2014 was planned to be the watershed year in the convergence process. Therefore, wherever appropriate, this book compares how the two standard-setting bodies approach specific issues covering employee benefit plans.

Because this book focuses on the accounting, tax, and finance implications of employee benefit plans, the main sources for the material for this book are the relevant authoritative accounting standards from the US GAAP and IFRS. Much material was also sourced from the IRS Codes. Therefore, many of the tables and charts included in this book derive directly from IRS source material available on the Internet. So, most of the research for this book is Internet-based.

The discussions in the book are mostly U.S.-based. However, one chapter is devoted to the technical issues involved in cross-border employee benefit plans.

Let’s begin our journey.