Introduction

Almost every retiree in America is touched by the Social Security system. For some, it is an extra source of income that enables them to touch their individual retirement account (IRA) in unusual circumstances only. For others, Social Security is their primary means of subsistence. It is therefore imperative to understand properly how this system works, who is eligible for benefits, how the benefits are calculated, and if someone should file for early benefits or not.

Learning Goals

•Identify who is and who is not covered by Social Security

•Understand the differences between being fully insured and currently insured for Social Security purposes

•Understand the different coverage programs offered by Social Security

•Identify what coverage is available for a surviving spouse

•Understand how Social Security benefits are calculated

•Identify the implications of taking benefits either early or late

•Explain how to apply for Social Security benefits

•Calculate the portion of Social Security benefits that is subject to income taxes

•Determine when it might be appropriate to file for early Social Security benefits

The Inherent Importance of Social Security

Retirement is intended to be a well-deserved break for those who have spent a lifetime hard at work. Up to this point in this book, you have been learning about all of the various ways that an employer and an employee can save for retirement. This is certainly the ideal scenario, but there is another option that is arguably the most important and most widely used retirement income program in the United States. This, of course, is the Social Security system.

Roughly 90 percent of retired Americans receive some form of benefit from the Social Security Administration (SSA).1 The other 10 percent of workers that are excluded from coverage typically fall into one of four exclusion groups. The first group excluded from Social Security is railroad workers. They are excluded because they have their own special program. Employees of state and local governments are typically excluded from Social Security unless their government body opts into Social Security will a special arrangement directly with the SSA. The third group of excluded workers includes a subset of expatriates. An expatriate is an American citizen who works oversees rather than domestically within the United States. They will be covered by Social Security only if they are working directly for a U.S. company and not for a foreign affiliate. Expatriates will not be covered by Social Security if they are working for the foreign affiliate of a U.S. company unless the U.S. company owns at least 10 percent of the foreign affiliate, and the parent company has a special arrangement with the U.S. Treasury Department. The fourth group of excluded workers is clergy who have opted out of the system. Most clergy earn much lesser salary than their private sector congregants. To help the clergy make ends meet, the government allows them to increase their take-home pay by not withholding any funds for the Federal Insurance Contributions Act (FICA) (Social Security) taxes. This can be a very short-sighted decision for the clergy unless their denomination has some form of retirement income replacement program in place.

In 2014, the SSA will pay almost $863 billion to over 59 million Americans.2 On average, the monthly check from Social Security represents 38 percent of all retirement income for the elderly. The SSA has revealed that 52 percent of married couples and 74 percent of unmarried persons receive at least 50 percent of their retirement income from Social Security. They have also revealed that 22 percent of married couples and 47 percent of unmarried persons receive at least 90 percent of their retirement income from Social Security. The moral of the story…get married! Just kidding…but the data is sobering. Is this healthy? I will let you decide that, but it certainly is a concern if nothing else.

Does the presence of the Social Security safety net create moral hazard for Americans? Moral hazard is an insurance term, which basically means that if someone has insurance to catch them if they fall, then they are more likely to engage in risky behavior. From a retirement planning perspective, I wonder if Americans’ understanding of a Social Security safety net has encouraged and enabled them to spend more money during the years when they should be actively saving for retirement simply because they know that they will at least have Social Security, which itself is questionable in terms of long-term sustainability under its current iteration.

Social Security Funding

Social Security is funded through taxes paid by both the employee and the employer. The taxes will appear on an employee’s wage statement as FICA. The employee’s portion of the tax is 6.2 percent multiplied by the employee’s gross (pretax) income up to a maximum of the taxable wage base, which is $117,000 in 2014. The employer must match the employee’s tax dollar for dollar by paying 6.2 percent as well. Consider an employee who receives a gross salary of $150,000 per year. This employee will have $7,254 (6.2% × $117,000) withheld from their salary and the employer will also pay the same $7,254. The earnings above $117,000 will not be taxes for Social Security purposes. This money must be sent to the federal government periodically to keep funds flowing into the Social Security system.

If the “employee” happens to be self-employed, then the relevant law is SECA, which stands for Self Employed Contributions Act. Because there is no separate employer to make the employer’s contribution, the self-employed person must make both the employee’s 6.2 percent contribution and the employer’s 6.2 percent contribution.

It is important to understand that Social Security tax is withheld from gross wages whenever there is earned income. It does not matter if the worker is retired and receiving Social Security benefits or not. If workers of any age have a positive gross wage, then they will be paying Social Security taxes up to the taxable wage base limit. It is also important to understand that the taxes withheld for Medicare (1.45 percent for the employee and the employer each) do not have a taxable wage base limit. Employees pay Medicare taxes on whatever amount they earn, and self-employed individuals will also pay a double Medicare tax following the same logic as SECA.

To receive Social Security benefits, workers must have accrued a certain number of “credited quarters of coverage.” An employee will receive one credited quarter for each $1,200 of earnings in a year (2014 rule). Credited quarters are subject to a maximum of four per year.

Why do the credits matter? To be considered fully insured, a worker must accrue 40 credited quarters. This is essentially 10 years of at least part-time work. Fully insured is a valuable status because it means that not only will the worker qualify for benefits in retirement, but their survivors will be able to apply for full survivor benefits with the SSA, should the fully insured worker die before the spouse.

What would happen for a young lady who enters the workforce and decides after a few years to put her career on hold to start a family? For someone who has worked less than the required 40 credited quarters, there is another status called currently insured. To qualify as being currently insured, a worker would need to have at least 6 credited quarters out of the most recent 13 quarters available. When workers are at least currently insured, their survivors will receive at least a partial benefit, should the worker pass away.

A third classification is known as disability insured, but it is only available if someone meets the SSA’s requirements to be considered disabled. You will learn about this in the section on Survivor Benefits in this chapter.

Initial Benefit Issues

Full retirement age (also called the normal retirement age) had been age 65 for years. Now the SSA has set the age at 66 for those born between 1943 and 1954 and age 67 for those born after 1960. There will likely be further adjustments over time, but these are the current rules. Benefits are available for early retirement as early as age 62, but they are offered with a requisite reduction, which you will learn about in the Early Retirement section in this chapter.

The normal retirement age was established to be a certain number of years below the average life expectancy. In 1940, the normal retirement age was roughly 12.7 years below the average life expectancy.3 Using actuarial data from 2009, the normal retirement age is now a little over 17.5 years below the average life expectancy.4 This creates a challenge for the long-term solvency of the Social Security system because the duration of benefits payment has declined at the same time that the number of workers per retiree has declined. In 1945, there were 41.9 workers per retiree, and in 2010 there are only 2.9.5 There will likely be a continued trend of gradually raising the normal retirement age to link the retirement age more accurately with average life expectancy.

Any person who is fully insured and at or above the normal retirement age can retire and receive full benefits from the SSA. According to the SSA, 72 percent of all benefits paid are to retired workers.6

Benefits are also available for the spouse of someone who is fully insured and has reached the normal retirement age. The caveat is that the spouse must be at least 62 to qualify for benefits. A strategy that is often employed by financial professionals is to have fully insured workers who have attained the normal retirement age file for their own benefits and then have their spouses test if benefits would be higher taking a spousal benefit or higher waiting until their own normal retirement age with payments based upon their own lifetime earnings.

What about benefits for someone who is divorced? A divorced person is entitled to spousal benefits from Social Security if the marriage lasted at least 10 years and they remained unmarried, they are at least 62 years old, the ex-spouse is fully insured and entitled to benefits, and the divorced spouse’s own benefits would be lower than the calculated spousal benefit.

There are also certain benefits for survivors of a deceased person who was covered by Social Security. According to the SSA’s March 2014 Monthly Statistical Snapshot, survivor benefits comprise 13 percent of all benefits paid. You will learn the details of survivor benefits in the next section in this chapter. One other category of available benefits from the SSA is for disabled persons. You will learn about this category in the next section. According to the SSA’s March 2014 Monthly Statistical Snapshot, 15 percent of all Social Security benefits are paid to the disabled.

Survivor Benefits

There are some specific benefits that are available to the survivor of a deceased fully insured worker. The spouse of a deceased worker who is only currently insured will have reduced benefits available to them.

The first benefit available to the surviving spouse of a fully insured worker is a whopping $255 one-time lump-sum payment. The idea is to help defray burial costs, but this small dollar amount will not offset too much of the expenses from a funeral home. Still, it is a nice idea. The real benefit for the surviving spouse is that they will be eligible for full spousal retirement benefits as if the worker were still living. This benefit is available to the surviving spouse once he or she has reached the normal retirement age. He or she can also receive a reduced benefit as young as age 60 (not 62) or as young as age 50 if he or she is disabled.

Another layer of benefit for the surviving spouse will apply if he or she is also caring for a minor child of the deceased worker. The children must be eligible for dependent children’s benefits and be either younger than age 16 or be disabled themselves. If a surviving spouse is caring for a dependent child of the deceased, then the surviving spouse is eligible to receive spousal benefits at any age as long as the requirements on the child remain met.

Dependent children of the deceased worker are also eligible for benefits provided that they are unmarried and either younger than 18 or younger than 19 if they are still in high school. The age requirement is waived if the dependent child was disabled before he or she turned 22. There are even some special circumstances where stepchildren, grandchildren, and adopted children of a deceased worker can qualify for benefits. These special scenarios are beyond the scope of this textbook, but know that they exist.

There is also a survivor’s benefit for dependent parents of a deceased fully insured worker. The dependent parents must be at least 62 years old to qualify. The other caveat is that the parents must meet the standard Internal Revenue Service (IRS) dependency test, which states that the deceased worker must have been paying at least 50 percent of the dependent parent’s support. Also, a family maximum applies to the total dollar amount that a family can receive if there are two or more individuals receiving survivor’s benefits.

How Is the Actual Benefit Calculated?

Social Security benefits are based on the employee’s average index monthly earnings (AIME). To find a worker’s AIME, the SSA will begin by listing all annual wages earned by an employee and then indexing them with an adjustment factor similar to inflation. It would be unfair to compare wages earned 25 years ago with wages earned last year. The SSA uses the highest grossing 35 years of indexed wage history. They then divide the cumulative wages from the highest grossing 35-year window by 420 (35 × 12 = 420 months in a 35-year window), and voilà…AIME. The SSA provides AIME to all workers on an annual basis. They will mail a statement to each worker’s home address, and the information is also available on their website.

Benefits paid are based on the AIME. The actual monthly Social Security benefits paid are technically known as the primary insurance amount (PIA). The calculation of PIA is very straightforward. For 2014, begin by taking 90 percent of the first $816 of AIME, then take 32 percent of any AIME that falls between $4,917 and $816, then take 15 percent of any AIME above $4,917. Remember that AIME is a monthly compensation figure. Table 20.1 shows how the PIA would be calculated for a worker whose AIME is $7,000 (an average annual salary of $84,000).

Table 20.1 AIME calculation example

|

Threshold percentage |

Amount of AIME |

Benefit |

|

90% |

$816 |

$ 734.40 |

|

32% |

$4,101 ($4,917 − $816) |

$1,312.32 |

|

15% |

$2,083 ($7,000 − $4,917) |

$ 312.45 |

|

|

Cumulative benefit (PIA) |

$2,359.17 |

The worker illustrated in Table 20.1 will have a monthly Social Security benefit of $2,359.17, which means that he or she will replace 33.70 percent ($2,359.17/$7,000) of his or her AIME (proxy for preretirement income) using Social Security benefits!

Early Retirement and Social Security

From the perspective of the SSA, early retirement means applying for benefits any time before a worker reaches the early retirement age. In practice, workers begin to consider this option at age 62.

Most people would love to retire as early as possible, but there is a catch. Receiving Social Security benefits before the normal retirement age will result in a reduced benefit. The absolute earliest that someone could begin to apply for benefits is age 62 (48 months prior to their normal retirement age). If the worker is applying for an early benefit for himself or herself, then the benefit will be reduced by 5/9th of 1 percent for each month before the normal retirement age limited to 36 months. A further reduction is 5/12th of 1 percent for each month before the normal retirement age for the next 24 months. Consider the plight of the worker in the previous example who had a PIA of $2,359.17 at the normal retirement age. What would happen if she chose to retire instead four years (48 months) early? The answer is shown in Table 20.2.

Table 20.2 Early retirement reduction example (Taxpayer)

|

Percentage reduction |

Applicable months |

Total percentage reduction |

Dollar reduction in PIA |

|

5/9th of 1% |

36 |

20% |

$471.83 |

|

5/12th of 1% |

12 |

5% |

$117.96 |

|

|

Cumulative reduction |

25% |

$589.79 |

If the worker shown in Table 20.2 decided to retire four years early, then the reduced monthly benefit (PIA) would be $1,769.38 ($2,359.17 − $589.79), and this reduction in benefit is permanent except under a special scenario, which you will learn about in the second to last section in this chapter. The desire to retire early could materially impact this worker’s ability to enjoy a comfortable retirement. At this point, he is weighing the benefit of retiring early with the loss of monthly income in retirement. That is essentially a very nice car payment!

However, if the spouse of this worker is applying for an early benefit, then the benefit will be reduced by 25/36th of 1 percent for each month before the normal retirement age limited to 36 months, and a further reduction of 5/12th of 1 percent for each month before the normal retirement age for the next 24 months. Consider how things would work for the person we have used so far in examples if we assume that it is a spouse filling for spousal benefits. Assume that the spouse would otherwise have a PIA of $1,912.47 at the normal retirement age. The spousal benefit will be lower than the actual worker’s. What would happen if a spousal filer chose to retire instead four years (48 months) early? The answer is in Table 20.3.

Table 20.3 Early retirement reduction example (Spouse)

|

Percentage reduction |

Applicable months |

Total percentage reduction |

Dollar reduction in PIA |

|

25/36th of 1% |

36 |

25% |

$478.12 |

|

5/12th of 1% |

12 |

5% |

$95.62 |

|

|

Cumulative reduction |

30% |

$573.74 |

The spousal benefit is more negatively impacted (30 percent reduction instead of 25 percent reduction) than the early benefits of the actual worker. The recipient of the spousal benefit would receive $1,338.73 ($1,912.47 − $573.74).

Deferred Retirement and Social Security

Some individuals are very passionate about what they do. They would prefer to work as long as possible. Others delay filing for Social Security simply because they are good at math. Either way, there is added value to delaying retirement beyond the normal retirement age.

For those who choose to delay retirement beyond the normal retirement age, the SSA has arranged a financial incentive. They will increase the delayed filer’s PIA by 8 percent per year for every year that they delay receiving benefits. The SSA will make pro-rata adjustments up to age 70. The incentive to delay is only available for fully insured workers. It is not available for spousal benefit filers.

Obviously, if someone is able to delay retirement, it is best for his or her monthly cash flexibility. As long as the fully insured worker is in good health, this can be an excellent option for them to consider. The benefits of delaying will be realized only if taxpayers either have enough income that they last until age 70 without tapping into their retirement savings or they have a substantial nest egg accumulated.

Another way to think about deferred (or delayed) retirement is using the analogy of a guaranteed inflation-adjusted 8 percent annuity. Where else can a retiree get this kind of guaranteed return? Some would certainly question the guarantee, given the current status of the Social Security trust fund and American politics. The long-term viability will certainly change over time, and there will likely be changes to the payroll tax rates for Social Security, to the normal retirement age, and perhaps even to the level of benefits themselves. But, do not forget that the population of Social Security recipients is a huge voting force in America, and a complete revocation of the system is not likely as long as the American government can still write checks.

The Earnings Test

Can a Social Security recipient have a job during retirement? Absolutely! With so many Americans heavily reliant on Social Security for their retirement income, it may be very wise to also work a part-time job. The complication is that those who work while also receiving early Social Security retirement benefits will be subject to an earnings test, which may result in a reduction of PIA from the SSA. The reduction only applies to those receiving retirement benefits before the normal retirement age (early retirement). The amount that the monthly check is reduced by is not gone forever. In baseball terms, it is benched. The amount that is removed from the PIA due to the earnings test in early retirement is then adjusted back into the PIA after normal retirement age.

Social Security benefits are reduced by one dollar for every two dollars over the income limit established by the SSA. For 2014, this limit is $15,480 for those who attain normal retirement age sometime after 2014 and $41,400 for those who reach normal retirement age during 2014. Consider the previous example of a worker who should receive a reduced early retirement benefit of $1,769.38. If he also worked and earned $20,000 during the year, he would have an earnings test reduction in the monthly benefits equal to $188.33 {[($20,000 − $15,480)/2] then divided again by 12 to get the monthly number}. This individual would receive an adjusted $1,581.05 ($1,769.38 − $188.33) each month until the year in which he would reach normal retirement age. In that year, the earnings test adjustment would be based on an income limit of $41,400, and assuming the additional income remains at $20,000, there will not be any adjustment in the year in which this worker reaches the normal retirement age. Once the taxpayer reaches the normal retirement age, there will no longer be any restrictions on the amount of income that can be earned, and the benefit will be restored to $1,769.38 PLUS an upward adjustment factored by the SSA for each year where the earnings test reduced the benefits.

It is important to understand that the earnings test only applies to earned income. It does not apply to pension benefits or distributions from retirement savings accounts.

Applying for and Taxation of Benefits

A worker who is planning to retire should plan to file for Social Security benefits three months in advance of when he or she will actually need to receive the payments. This is an arm of the federal government and there will be a delay in the processing because there are so many people being covered by the Social Security system. Benefits can be paid retroactively for up to six months. Consider a worker who retires on his 66th birthday and is so focused on his new freedoms that he forgets to file for benefits until two months later. With the three-month potential processing lag, he would potentially miss out on five months of benefit checks that he otherwise would have received, had he been proactive in filing for his benefits. The SSA will provide retroactive payments to cover those five months. Had this new retiree waited six months to file for benefits, then he would be nine months behind (6 months for procrastination and 3 months for the processing lag), and he would only receive six months of retroactive benefits.

An argument can be made to ignore the retroactive payments and to just calculate the payments as a deferred retirement, which would result in an increased monthly benefits check indefinitely. It will be up to the new retiree to figure if the retroactive payments or the higher monthly payment would be more beneficial. If the retiree is in rapidly failing health, the retroactive payment may make the most sense. Otherwise, the increased benefit from deferred retirement should be strongly considered.

Applying to begin benefits is relatively straightforward. One question commonly asked is: How can someone know what benefits they are entitled to in advance of retiring so that they can logically consider their readiness for retirement? The SSA sends an annual mailing (after a taxpayer reaches age 25) to alert taxpayers to their current AIME and PIA status. The SSA also has a section on the website where taxpayers can create an account to monitor their benefits. The website will also provide custom “calculators” to help a worker project retirement scenarios from the perspective of Social Security. It is important to check this information periodically to make sure that the SSA has not missed compensation that should increase the AIME.

Social Security benefits were intended to be a retirement safety net for those who do not have other means of paying for retirement living expenses. However, many individuals, who also have other assets on which they can live, receive benefits. The IRS has structured taxation of Social Security benefits in a way that follows the logic just discussed.

A retiree who is single and receiving retirement benefits from Social Security will apply the tax schedule shown in Table 20.4 to their Social Security benefits.

Table 20.4 When are social security benefits taxable for a single taxpayer?

|

AGI income range |

Percentage of benefits taxed |

|

Under $25,000 |

0% |

|

$25,000–$34,000 |

50% |

|

Over $34,000 |

85% |

Abbreviation: AGI, Adjusted gross income.

From this schedule, you can see that after a retiree’s adjusted gross income (AGI) rises above $25,000, a portion of their Social Security income becomes taxable as ordinary income. Common items that will create AGI for a retiree are interest on bank deposits or certificates of deposits, realized capital gains in taxable investment accounts, distributions from pensions and IRAs (reported on a Form 1099-R), and possibly a part-time job. Sometimes, the amount of money that is withdrawn from an IRA in retirement is enough to put a retiree over either the $25,000 threshold or the $34,000 threshold. This should be monitored by either the taxpayers or their financial professional. The maximum amount of Social Security benefits that could be taxable is 85 percent.

Married retirees have a higher threshold schedule. The taxability schedule in Table 20.5 applies to a married retiree’s Social Security benefits.

Table 20.5 When are Social Security benefits taxable for a married taxpayer?

|

AGI income range |

Percentage of benefits taxed |

|

Under $32,000 |

0% |

|

$32,000–$44,000 |

50% |

|

Over $44,000 |

85% |

Abbreviation: AGI, Adjusted gross income.

Should a Taxpayer Take Early Social Security Benefits?

And now for the $100 million question…should a taxpayer file for early Social Security retirement benefits? Everyone would love to retire as young as possible and begin to enjoy a different pace of life with perhaps more focus on volunteering and family. But, this is not available for everyone. It is imperative to thoroughly evaluate each early retirement scenario on a case-by-case basis. It may be workable for one taxpayer and not for another.

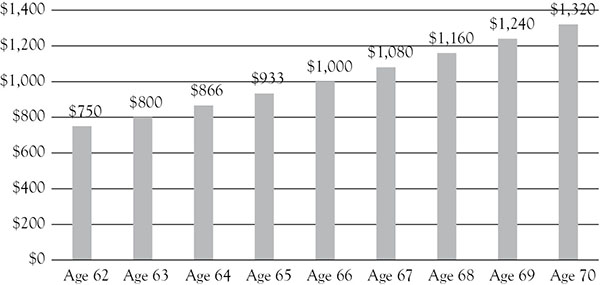

You have already learned that filing for Social Security benefits early will result in a permanently reduced monthly check (PIA). Figure 20.1 shows that early benefits result in a reduction in benefits of roughly 7 percent per year. For every year that workers decide to keep working past age 62, they are essentially earning a 7 percent increase in PIA for each year that they keep working. This thought pattern works up to the normal retirement age at which point the increase in benefits is now 8 percent per year for deferred retirement. This is an interesting way of thinking of this scenario. Hopefully, it makes logical sense to you that by not taking a reduced benefit today, the retiree will receive a higher benefit later. This is an easy way to earn 7 percent more benefits by not taking early benefits and possibly an 8 percent growth strategy if the taxpayer surpasses the normal retirement age and stretches out to age 70!

Figure 20.1 Schedule of Social Security benefits assuming $1,000 PIA at normal retirement age of 66

Source: Social Security Administration

Abbreviation: PIA, Primary insurance amount.

Sometimes an early retirement is the result of an involuntary termination. Business conditions change and layoffs do occur. If a layoff affects someone who is able to qualify for early retirement from Social Security, this might be a tempting option. Some forced retirees in this situation are not planning on remaining in retirement. They are transitional…they are looking for a new job, but they need some money to get them through until the new job is secured. In this instance, the forced retirees have a unique payback option where they could apply for early retirement benefits and then within one year, they could repay all benefits received without interest, and then benefits would be suspended until they reapply for benefits at their planned retirement. Their actual retirement benefits will then be based upon when they reapply for benefits and not on the reduced early retirement amount. This option assumes that the taxpayer has the discretionary cash flow to repay the benefits received.

According to the American Association of Retired Persons (AARP), 41 percent of men and 46 percent of women elect to retire early at age 62. They also reveal that 14.3 percent of men and 9.7 percent of women wait to collect a full benefit at their respective normal retirement age.7 Early retirement, it seems, is chosen by many workers who are eager to retire and change priorities.

Table 20.6 highlights the fact that patience (in terms of filing for Social Security benefits) does have a cost. It is estimated that if someone waits until age 70 to file when they otherwise would have taken benefits at age 66 (their normal retirement age), then they would need to collect the higher benefit level until roughly age 84 before they would be ahead by taking the deferred benefits. If a taxpayer is in very good health, then this might be a worthy gamble. If longevity is in question or at least uncertain, then deferred retirement benefits might not be the best option to select.

Table 20.6 Retirement break-even ages

|

Age to begin benefits |

Relative comparison age |

Break-even age range |

|

66 |

62 |

Between 77 and 78 |

|

70 |

62 |

Between 80 and 81 |

|

70 |

66 |

Between 83 and 84 |

Source: Charles Schwab8

Supplemental Security Income

Supplemental Security Income (SSI) is a secondary layer of retirement income for Americans who meet a specific criterion. They must be below a certain income range, which is determined by each state, and they must be (1) age 65 or older, (2) disabled, or (3) legally blind. While SSI benefits are administered by the SSA, the funds do not come from the Social Security trust fund. Payment for SSI benefits comes directly from the budget of the U.S. Treasury. These payments could be as high as $721 for an individual and $1,082 (2014 limit) for a married couple, and this value is in addition to any Social Security payments being received.9 This category of retirement income is designed to help those who have very little means to care for themselves.

Recipients of SSI benefits must maintain “limited resources.” This means that they cannot own more than $2,000 worth of assets for an individual or $3,000 if they are a married couple. The SSI recipient’s home and one car are not included in this resource limit. This basically means that SSI beneficiaries cannot maintain a bank account larger than these resource thresholds and still receive the additional benefits.

There is one notable exception to the limited resources mandate. The SSI beneficiaries could have a special needs trust (SNT) established for their benefit. An SNT must be established by someone other than the SSI benefit recipient. This could be a parent or some other relative perhaps. Also, an SNT must be irrevocable, and it must stipulate that any sum left in the SNT after the SSI recipient’s death can be remitted to Medicaid to cover any end-of-life expenses paid by the state.10

Discussion Questions

1.Social Security is arguably the most important retirement system in America, yet some workers are not covered under Social Security. Who are these people?

2.Some people say that Social Security creates moral hazard. Why would they say such a thing?

3.Stacey earned compensation totaling $11,000 from a single employer between January 1 and April 1. She then stopped working to care for her mother who was in failing health. How many quarters of coverage does Stacey earn for this taxable year?

4.A certain woman has been out of the workforce for the last 10 years as she has been focusing on raising three children. She has recently decided to reenter the job market. How long will she need to work before her spouse would be eligible for surviving spouse benefits, should that unfortunate circumstance become necessary?

5.What is the earliest age at which a retired worker is eligible to receive Social Security benefits?

6.One of your uncles, who was born in 1948 tells you that he is planning to retire with full Social Security benefits this year at age 65. What advice would you give your uncle?

7.A certain couple divorced five years ago. They were married for eight years and neither has remarried. The ex-wife is now 66 years old and interested in applying for Social Security. What are her options?

8.A tragic car accident claimed the life of a devoted husband and father. The survivors are a 45-year-old wife, a 24-year-old mentally disabled child who has been disabled from birth, a 21-year-old college student, and an 18½-year-old who will be graduating high school in another 10 months. What are the survivor’s benefits available to this family, assuming that the deceased father was fully insured?

9.Below is a series of indexed annual salaries for an individual. He began with a $45,000 indexed salary straight out of college and had annual increases of 3 percent with the exception that every seven years he changed jobs and received a salary increase larger than 3 percent. What is this individual’s AIME?

|

$45,000.00 |

$55,000.00 |

$67,500.00 |

$87,500.00 |

$112,500.00 |

|

$46,350.00 |

$56,650.00 |

$69,525.00 |

$90,125.00 |

$115,875.00 |

|

$47,740.50 |

$58,349.50 |

$71,610.75 |

$92,828.75 |

$119,351.25 |

|

$49,172.72 |

$60,099.99 |

$73,759.07 |

$95,613.61 |

$122,931.79 |

|

$50,647.90 |

$61,902.98 |

$75,971.84 |

$98,482.02 |

$126,619.74 |

|

$52,167.33 |

$63,760.07 |

$78,251.00 |

$101,436.48 |

$130,418.33 |

|

$53,732.35 |

$65,672.88 |

$80,598.53 |

$104,479.58 |

$134,330.88 |

10.Using the AIME you calculated in the previous question, what is this individual’s PIA (using 2014 AIME bend points), assuming that he retires at the normal retirement age?

11.What would happen if the individual whose PIA you just calculated needed to retire at age 63 instead of the normal retirement age of 66?

12.A married client who has been retired for several years has an annual pension from his previous employer equal to $25,000 per year. The combined required IRA distribution for this couple is $12,500. They have taxable capital gains income of $4,500 from their non-IRA account. They have combined Social Security benefits of $35,000. They are considering taking an additional IRA distribution of $10,000 to gift money to their only child. What advice do you have for them relative to their Social Security benefits?

13.A worker born in 1953 is currently planning to file for deferred Social Security benefits at age 68. How much benefit could he expect to receive if his PIA at his normal retirement age would equal $2,473.49?

14.A taxpayer was forced to “retire” (layoff) at age 63. She filed for early Social Security benefits and begins to receive a check for $1,976.43. Six months later, she is able to find a part-time job where she can earn $1,700 per month. This is not enough to cover the living expenses and so she needs to keep receiving Social Security benefits as well. The SSA finds out that she now has a part-time job. What will happen to the monthly Social Security benefits?