5. Environmental Finance: Innovating to Save the Planet

The now-famous “inconvenient truth” of the twenty-first century is that our collective failure to value our natural resources has placed the planet in real peril. Pollution, deforestation, and climate change are taking a fearsome toll on biodiversity, nature’s astounding variety of plant and animal species.

Back in 1997, a group of economists and biologists estimated that humans derive trillions of dollars each year in benefits from ecosystem services that they don’t pay for—benefits that total between 55% and 185% of global GDP.1 In purely economic terms, this equation is unsustainable.

Under the weight of our consumption, the world’s stocks of natural capital—that is, ecosystems and the benefits and resources they provide—have dramatically shrunk in the past century. Vast swaths of coral reefs lie bleached and lifeless in the Caribbean and around Australia, while tropical rainforests have been leveled in the Amazon and Indonesia. The International Union for the Conservation of Nature (IUCN) released a report in 2008 warning that 25% of all wild mammal species are in danger of disappearing.2 Scientists have estimated that there are anywhere from 5 million to 30 million species on Earth, but we have identified only some 1.5 million to date. Less than half a million have been analyzed to determine their potential economic uses.3

The burning of fossil fuels and massive deforestation are also hastening global warming, which brings with it more volatile and extreme weather, along with the potential for rising seas, the spread of infectious disease, and fertile soil turning to desert. Together these trends portend massive destruction of real assets.

The stark reality of the situation presents a crystal-clear call to action: We must speed the convergence of environmental and capital markets and seize the opportunity to build a more sustainable economy. We have the ability to create new markets that value air, water, and natural resources. We can fund new clean technologies and find more equitable and sustainable ways to generate jobs, income, and wealth in the future.

To achieve this paradigm shift, we will need to apply financial technologies to the valuation and pricing of environmental externalities (such as air and water pollution) and common-property resources (such as biodiversity). The first step is building an adequate pricing mechanism, mobilizing proven innovations for developing environmental markets. The price discovery made possible through innovative environmental finance signals the real market value of natural resources, and thereby stimulates inventive conservation practices and new clean technologies that will facilitate growth. This process requires a new approach to financial decision making that monetizes formerly hidden assets.

From experience with curtailing acid rain via the sulfur dioxide–allowance market to the implementation of the Clean Water Act, market-based solutions have proven consistently more effective in protecting the environment than government regulation alone. Project financing, public–private partnerships, and tradable permits have come to supplement or replace conventional command-and-control regulation and purely tax-based instruments. This approach can minimize the aggregate costs of achieving environmental targets while providing dynamic incentives for the adoption and diffusion of greener technologies.

Market-based financial and public policy instruments emerged in the 1980s and have steadily gained momentum. Tradable permit systems have been deployed to phase down use of leaded gasoline, end the use of ozone-depleting chlorofluorocarbons, and even reduce air pollution in the smoggy skies above Los Angeles.4 New attempts are being made to attach an economic value to public goods such as biodiversity. In fact, the United Nations Environment Programme has launched a Finance Initiative as a formal mechanism for mobilizing the financial sector to take a more active role in protecting the environment.

This chapter demonstrates that it is possible, and urgently necessary, to apply principles of finance and economics—efficient use of scarce capital, price transparency, and lowered transaction costs—to environmental issues. Aligning the interests of consumers, producers, and the general public can have a powerful effect. A crucial point to underline is that economic growth appears to be a necessary condition for environmental protection. Growth is not the enemy of conservation.

Market Failures and the Environment

Economists call them “externalities.” When someone engages in wasteful production or consumption, they may cause negative impacts on others who had absolutely nothing to do with the original activity. These costs are never accounted for by the parties actually engaged in and most directly affected by that activity. Negative externalities are a type of market failure, leading to the misallocation of resources, and environmental degradation is perhaps the prime example of this concept.

It is possible, of course, to ban or tax environmentally destructive behavior, but doing so can weigh down economies and cause other market distortions. The most efficient way to resolve externalities is to internalize them—to embed them into the economic decision making and transactions of market actors by adequately pricing them. Achieving this shift requires clearly defined property rights and some kind of market mechanism.

One way to understand externalities is to revisit the famous “tragedy of the commons,” a theory explored by biology professor Garrett Hardin in 1968.5 In a later article, Hardin noted that satellite photos taken over Africa in 1974 captured this concept unfolding. They revealed a dark patch covering 390 square miles. It turned out to be nothing more than a fence enclosing fertile grasslands; but outside the fence, the soil was barren and lifeless.

The explanation was simple: The fenced area was private property, subdivided into five portions. Each year the owners moved their animals to a new section. Fallow periods of four years gave the pastures time to recover from the grazing. The owners did this because they had an incentive to take care of their land. But no one owned the land outside the ranch. It was open to nomads and their herds .... Their needs were uncontrolled and grew with the increase in the number of animals. But supply was governed by nature and decreased drastically during the drought of the early 1970s. The herds exceeded the natural “carrying capacity” of their environment, soil was compacted and eroded, and “weedy” plants, unfit for cattle consumption, replaced good plants. Many cattle died, and so did humans.6

Air, fishing grounds, and drinking water ... these resources belong to everyone but are owned by no one, so they are used heedlessly. But eventually, the principle of diminishing marginal returns kicks in: As more and more people exploit a natural resource, the benefits they derive from that resource increase at a declining rate. Even though it is in everyone’s interest to preserve shared resources, larger societal goals do not typically motivate individual market actors as they pursue their narrow self-interest. Resources may be destroyed by the combined actions of multiple parties intent on maximizing their own consumption rather than conserving for the future. Without direct ownership, people have little incentive to preserve a resource.7

It is not so much that the market fails; rather, it does not exist. The public and social costs of private production can be priced and paid for through a market exchange; creating that platform is critical to conservation. The problem inherent in doing so is that buyers and sellers lack information about available supply and demand of environmental goods and services without any guarantee of uniformity. But this issue can be overcome—just as market mechanisms were established for corn, rice, wheat, railroads, or manufacturing debt and equity in the past. The crucial ingredient is a system of well-defined, enforceable, and transferable property rights.

Property Rights and Professor Coase

The absence of property rights can hinder the very essence of a market economy—and perhaps, in this case, threaten human survival. Environmental problems often stem from the absence or incompleteness of property rights. When rights to resources are defined and easily defended, all market actors have an incentive to avoid pollution problems. The externality of air pollution, for instance, can be solved by establishing property rights over clean air so that residents are entitled to a fee if nearby smokestacks belch soot into their “property.”

The first to suggest that a system of well-defined property rights could overcome the problem of externalities was Ronald Coase, in a ground-breaking 1960 article that won him the 1991 Nobel Prize for economics.8 If property rights can be established for clean air and water, Coase maintained, individuals and firms will be forced to pay for any negative impacts they impose on others. This would provide incentives for more eco-friendly behavior and investments in improved technology, while also creating efficient economic returns. The “Coase theorem” stresses the importance of clearly defining property rights and using their transferability to allocate resources. By creating a property right in water or air, or embedding the costs of environmental impacts in business decisions, the public and social costs of private production can be priced and traded.

New Directions in Environmental Finance

While innovators in labs and factories are racing to harness renewable sources of energy and make our daily lives more energy efficient, financial innovators have been also been pushing the envelope in the environmental field, searching for new ways to apply economic concepts to protecting public goods.

Water withdrawals from sources such as groundwater have tripled over the last 50 years, and with continued population growth, demand is rising exponentially.9 Product and process technologies affecting water desalination, recycling, filtration and treatment, metering, and infrastructure stand ready to be taken to scale. The pressure of ever-growing demand is simultaneously driving the creation of new markets and public payment mechanisms in watershed ecosystem services.

Another nascent market is being formed to value biodiversity. These measures have often taken the form of government regulations, fines, and tax breaks, but now there is a movement to apply the principles of cap-and-trade (in which the government sets a cap on pollution or usage and then allocates permits to businesses and other entities, allowing them to trade permits among themselves) to diverse fields ranging from fisheries management to wetlands protection. The United States has led the way in this field, but market-based approaches are also taking hold in Australia and New Zealand and across Europe (the Netherlands, in particular, stands out for its willingness to try a wide range of different market mechanisms).10 One ground-breaking idea actually set up a market for “woodpecker credits” to help attach a value to endangered red-cockaded woodpeckers; if developers harm their habitats in one area, they must purchase credits to offset that harm. This has given rise to a market among those who own similar land. Now that a value is attached, they have an economic incentive to protect it.11

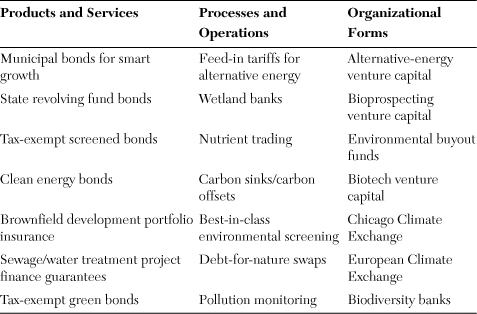

Table 5.1 offers some examples of the wide-ranging innovations already being deployed in environmental finance, from strategies that help protect ecosystems as providers of public goods to tools that help launch green businesses (including access to credit and loans, venture capital, and investment guarantees; resource extraction rents and/or severance fees related to natural resource development; entry fees and concessions; and securitization of revenues generated by marketable goods and services such as ecotourism, climate regulation, erosion control, pollination, water services, carbon offsets, and the like).12

Table 5.1. Types of Innovations in Environmental Finance

Financing Conservation Projects

State Revolving Funds: From Seed Money to Self-Sustaining Project Financing

For many years, the United States financed environmental improvements, such as sewage treatment plants, with substantial one-time grants made by the federal government to localities. But as the demand for funding grew, policymakers and capital market experts began to think creatively about how to leverage finances: to generate, for example, $2 million of pooled capital from a one-time $500,000 grant.

In 1987, Congress passed the Federal Clean Water Act and replaced its aging grants program with state revolving funds (SRFs).13 Under this model, each state applies for a federal capital grant, which requires a 20% local match; this pool of funding is then supplemented with capital market investment and possibly “seed money” from philanthropies. The states then make low-interest loans to local municipalities and organizations, which repay the loans from project revenue and local taxes. States may provide loans to communities, individuals, nonprofit organizations, and commercial enterprises.14 Their repayments recapitalize the state fund, creating a sustainable resource for funding.

This model maximizes the impact and longevity of government grants. SRFs have successfully ensured a steady flow of capital into water quality and management projects in rural areas, small towns, and major cities. The Environmental Protection Agency (EPA) estimates that they have provided more than $68.8 billion in cumulative assistance, serving more than 115 million people; the agency also states that, between 1987 and 2005, the funds created more than 600,000 construction jobs and 116,000 additional jobs.15

The local river and stream projects receiving funding generate sustainable income (through local taxes, tourism revenue, or usage fees, for example) that repays the original loan and recapitalizes the fund. Because the loans are offered at well below market interest rates, local communities save substantially on the cost of capital. Local river authorities can also leverage their resources with capital market investment through the sale of municipal bonds that can finance multiple projects.

SRFs provide federal assistance while maintaining state and local control over spending priorities. States are granted flexibility in setting up the structure of their programs. In addition to offering low-interest loans, they may allow the funds to be used for refinancing, purchasing, or guaranteeing local debt, or purchasing bond insurance. States set their own loan terms, including interest rates and repayment periods, and can customize these terms to assist small and disadvantaged communities.16

A state’s fund is rated on the entirety of its program, not on individual loans made to specific projects. This pooling of projects to reduce risk through diversity has been a key to success. In 2008 alone, the SRF program funded $2.7 billion for treatment facilities, $2.9 billion for sewer construction, and more than $220 million for controlling nonpoint source pollution (pollution that stems from many diffuse sources and is carried by rainwater runoff). These nonpoint source projects included sanitary landfill and brownfield rehabilitation (the cleanup of abandoned industrial sites), urban storm water–runoff management, and the improvement of agricultural water-management practices.17

State revolving funds have enabled new product development within the municipal bond market. By moving financing away from general obligation risks and toward revenue-bond project financing based on the business models of individual projects, it became possible to raise more funding in the capital markets. Moreover, these innovations made it possible to leverage limited government funds and to use the power of aggregating to pool risk over a large number of diverse projects. New organizational forms also arose that engage private investors in these projects. By moving away from reliance on conventional municipal bonds, the market itself was transformed by new capital structures and financial products that have results in cleaner rivers and better water management.

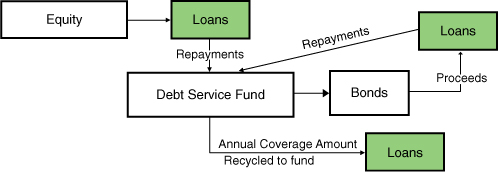

There are two basic SRF models. The “cash flow model” uses the fund’s original equity (the federal and state contributions) to originate direct loans to the communities. Repayments are pledged to bond issuance, with more loan repayments coming in than are actually needed to pay the bond debt. The proceeds from the sale of the bonds go to fund additional loans, creating a collateralized cash flow (see Figure 5.1). The coverage from the direct loans provides added security, as well as the subsidy on the loans.

Figure 5.1. The cash flow model

Source: Susan Weil, Lamont Financial

The “reserve model” uses the original equity to create a pool that cushions the fund from any potential defaults. The size of the reserve can vary anywhere from 30% to 70% of overall transactions. Bonds are then issued, and the proceeds from these bonds provide loans to local communities for river projects (see Figure 5.2). The interest earned by the reserve subsidizes the loans.

Figure 5.2. The reserve fund model

Source: Susan Weil, Lamont Financial

Missouri offers a good case study of a successful reserve model. The volume of loans issued through its SRF program ranks twelfth in the nation.18 Despite a slow start, the state had completed 150 loans to its communities, resulting in over $1.7 billion in construction, as of late 2008. The state’s residents must vote to approve project financing, and thus take an active interest in the success and subsequent repayment of any loan.

Missouri’s SRF is a leveraged loan program with dedicated pool financing across municipalities and towns. The fund maintains a reserve at 70% of its total transactions; this is the highest reserve level in the nation, ensuring excellent bond ratings.

The recipient of one of Missouri’s early SRF loans was the town of Branson, one of America’s country-music capitals, with a population of just 3,700 but an influx of 5 million tourists per year. When it became clear that Branson’s water infrastructure was inadequate for the needs of the community and such concentrated tourism, the city council approved a $56 million wastewater system capable of meeting stringent discharge limits and growing demand. Because the project’s budget could not possibly be paid by the town’s small population, the city enacted a 2% tourism tax on the cost of hotel rooms and entertainment, and a 0.5% tax on restaurant tabs. Moving debt responsibility to the tourism industry has enabled Branson to repay its SRF debt for the past 14 years.

Both the cash flow and reserve models of SRFs have worked successfully. Some states have also attempted to create a hybrid of these structures, using a set portion of the original equity for a reserve and the remainder to fund direct loans. Whatever blend is chosen, it is clear that the revolving fund has proven to be an effective financing model that eventually leads to self-sufficiency. It is important to note that loans give the recipient a stake in the financial package, creating an incentive to reduce wasteful expenditures.

Once the revolving fund idea proved its effectiveness, it served as a model for a number of other programs, with its scope being gradually broadened over time. In 1996, Congress established the Drinking Water State Revolving Fund (DWSRF) program, which mirrors the Clean Water Fund program in assistance options, state and federal responsibilities, and other structural aspects. In the DWSRF program’s first decade, states were able to loan $12.6 billion for 5,555 projects around the country. Special assistance has gone to small drinking water systems and disadvantaged communities, enabling them to meet public health standards.19 Revolving funds are also being used by the EPA to finance the cleanup of brownfields.

Using SRFs for Land Acquisition

In certain cases, the best way to improve water quality is to set aside strategically chosen parcels of land where water flows or originates, preventing pollution from development and industrial uses. By saving wetlands, we can also maintain important wildlife habitats.

New York State has deployed its SRF as a low-cost way to fund land-acquisition projects that protect water quality. In 2000, the city of Rye used a $3.1 million short-term, zero-interest loan from the Clean Water State Revolving Fund (CWSRF) to acquire and protect crucial land in the Long Island Sound Estuary.20 This fragile ecosystem is a huge and complex watershed, where the Connecticut, Housatonic, and Thames rivers meet and mingle with ocean waters. It is also a vitally important breeding and migratory habitat for a rich variety of bird species.

Some 20 million people live within 50 miles of Long Island Sound, enjoying its scenic beaches and consuming fish and shellfish from these waters.21 But industry, shoreline development, and heavy recreational use placed this vital watershed under stress, degrading wildlife habitats and causing frequent beach closures. Sewage plant discharge and storm water runoff deposit nitrogen into the water, creating “dead zones” where marine life cannot thrive. Extensive cleanup efforts have been underway for decades, but much more remains to be done.22

Long Island Sound’s Comprehensive Conservation and Management Plan recommended key land acquisitions as part of the ongoing strategy for saving this vital watershed. Rye’s acquisitions are an important piece of the puzzle; they will preserve and improve the waterfront, tributaries, and wetlands that lie within the city. In fact, New York State expanded its SRF to provide not-for-profit organizations with a mechanism for funding similar land-acquisition projects that protect water quality.

In California’s Central Valley, local land trusts and conservancies have partnered with federal and state agencies to leverage millions of dollars (including $9.5 million in CWSRF loans) for conservation purposes. The partnership has successfully protected tens of thousands of acres of land surrounding the Valley’s vernal pool wetlands, unique ecosystems that support rare plant and animal species. The Nature Conservancy (TNC) has played a crucial role in this effort: In 1999, the group pooled an $8 million loan from the state with $6 million from private and public sources in order to preserve the sprawling Howard Ranch as part of the Cosumnes River Preserve in South Sacramento County. The ranch is now off limits to new housing developments and conversion to vineyards or orchards, protecting its wetlands and delta streams. The local Sacramento Valley Conservancy later obtained a $1 million SRF loan to help set aside the Sacramento Vernal Pool Prairie Preserve.23

Debt-for-Nature Swaps

At first glance, a country’s external debt and its ability to protect biodiversity might appear to be completely unrelated. But linking these issues creatively through debt-for-nature swaps has made progress possible on both fronts. By relieving the foreign debt burden carried by developing nations, it is possible to secure their commitment to invest in local conservation projects and save imperiled ecosystems.

Most debt-for-nature swap deals executed up to now have been designed to protect endangered tropical forests. Not only are rain forests essential to the well-being of local communities, but they have global significance due to their ability to act as “carbon sinks,” absorbing the CO2 that causes climate change.24 Science has barely scratched the surface of the discoveries that lie hidden in these wilderness areas, which are teeming with rare and exotic plants and animals.

Yet around the globe, rain forests are under assault from a variety of factors: mining, logging, displaced farmers, cattle grazing, poverty-stricken locals gathering firewood, and new hydroelectric dams. Preserving the amazing biodiversity sheltered within these rain forests is a concern that transcends national borders.

Debt-for-nature swaps are the brainchild of Thomas Lovejoy of the World Wildlife Fund, who seized on the idea back in 1984 as a way to deal with the entwined problems of environmental degradation and the crushing sovereign debt burdens shouldered by many developing nations. When the Latin American debt crisis hamstrung the ability of many highly indebted nations across the region to focus on conservation, Lovejoy called for building an explicit link between debt relief and environmental protection.25

Many debt-for-nature swaps begin with a nongovernmental organization (NGO) or a “conservation investor” undertaking the purchase of a developing country’s hard-currency debt titles. A commercial bank might even be willing to sell to the NGOs at a discount, since the ability of the debtor nation to repay is already considered shaky. The NGO then forgives the debt in exchange for the debtor country’s commitment to fund a conservation project or set aside a crucial parcel of land. The debtor government might also be asked to use this newly freed-up financial stream to issue bonds, appointing local environmental groups to make grants from the proceeds. Conservation International conducted its first debt swap transaction in 1987, when it purchased a portion of Bolivia’s foreign debt from a commercial creditor, then cancelled that debt so the Bolivian government would set aside 3.7 million acres in and around the Beni Biosphere Reserve.26

Bilateral debt-for-nature swaps are a slightly different animal. In this case, the debt forgiveness deal is a direct transaction between two governments. In 1991, President George H.W. Bush unveiled the Enterprise for the Americas Initiative to pursue this strategy.27 The Environmental Foundation of Jamaica was the first fund established under this program; in exchange for forgiveness of $311 million of the island nation’s bilateral debt, the foundation received funding to administer child development programs, along with projects such as water quality monitoring, waste management, reforestation, and biodiversity protection.28

The U.S. Tropical Forest Conservation Act (TFCA) was enacted in 1998 to further institutionalize the idea of debt-for-nature swaps. Under this program, developing countries can reduce high levels of debt owed to the U.S. government, generating funds in local currency for programs that will protect local rain forests. Hundreds of millions of dollars that once went to debt payments have now been redirected to conservation activities in more than a dozen countries, from Botswana and Bangladesh to Paraguay and the Philippines.29

NGOs often help broker TFCA agreements and contribute additional funding. The Nature Conservancy and Conservation International each contributed $1.26 million to facilitate a 2007 debt-for-nature swap under the TFCA, in which the United States forgave $26 million of Costa Rica’s debt.30 The debt relief will finance forest conservation in Costa Rica over the next 16 years, helping rural and indigenous communities pursue sustainable livelihoods while protecting one of the world’s great natural treasures for future generations. (A portion of this funding will go to protect the La Amistad region, a tract of virgin rain forest that shelters some 90% of Costa Rica’s known plant species, more than 350 species of birds, and a host of exotic animals, including giant anteaters and ocelots.)31

Conservation International and The Nature Conservancy also played a key role in a 2006 deal that cancelled $24 million of Guatemala’s debt to the United States. The money will instead be channeled into a local fund for conservation grants to be distributed over the next 15 years. The grants will be used to protect Guatemala’s cloud forests, rain forests, and coastal mangrove swamps, home to many rare and endangered species.32

In June 2009, the U.S. government announced the largest debt-for-nature swap secured to date under the TFCA. Conservation International helped to broker and underwrite the deal, in which the United States will forgive nearly $30 million of debt payments owed by Indonesia in exchange for commitments to protect the Sumatran rain forest, which has experienced rampant destruction.33 The debt reduction will help to provide livelihoods for the people of the island while hopefully ensuring the survival of some critically endangered species, including tigers, elephants, orangutans, and rhinos. Over eight years, the government of Indonesia will pay the nearly $30 million to a trust, which will issue grants for forest conservation and restoration work in Sumatra. It will lead to increased protection of 13 vital areas of Sumatran rain forest that are home to hundreds of species of threatened plants and animals.34

Pollution Markets

The most practical solution for building a greener economy is to correct faulty pricing by making consumers and firms pay for the environmental damage they cause. Once these negative externalities are internalized, they will be incorporated in the prices of goods and services, creating real incentives for the creation and adoption of clean technologies.

One of the most compelling examples of using these principles to fix broken markets is that of cap-and-trade pollution markets. In such markets, the cap (or maximum amount of total pollution allowed) is usually set by government. Businesses, factory plants, and other entities are given or sold permits to emit some portion of the region’s total amount. If an organization emits less than its allotment, it can sell or trade its unused permits to other businesses that have exceeded their limits. Entities can trade permits directly with each other, through brokers, or in organized markets. This approach leaves individual companies free to choose if and how they will reduce their emissions and by how much.

Markets can achieve abatement targets at the lowest possible cost. Firms will choose the most affordable way to comply with the pollution cap, creating competitive incentives to develop new clean technologies. This dynamic speeds innovation, creates new opportunities for innovators, and quickly lowers compliance costs. In other words, Schumpeter’s theory of creative destruction (referenced in Chapter 3, “Innovations in Business Finance”) clearly applies to environmental markets. Invention, innovation, and replication on a large scale are required for the development and application of physical and financial technologies alike.

The U.S. Acid Rain Program and the Sulfur Dioxide (SO2) Market

The overriding concern for today’s green movement is global warming, but back in the 1970s and 1980s, acid rain was public enemy number one. This phenomenon occurred when power plants and industrial smokestacks spewed sulfur dioxide and nitrogen oxides into the atmosphere, where they mixed with water vapor. Alarms went off when scientists observed that fish, algae, and frogs were dying off in lakes and rivers. Acid rain not only took a toll on forests, crops, and buildings—it actually ate through the paint on cars and damaged ancient archeological landmarks. The problem seemed too diffuse and complex to be tamed by a simple command-and-control solution. After all, sulfur dioxide was emanating from thousands of unique sources, falling under multiple regulators.35

Two economists working for the precursor organization to the U.S. EPA, Ellison Burton and William Sanjour, decided to tackle the problem from a unique angle, building on the work of Coase and others. In their quest to find a low-cost, decentralized solution for abatement, they hit upon the idea of creating an actual marketplace to control emissions. The key was to devise penalties for polluting and incentives for emitters to invest in changing their practices.36

The breakthrough came in 1990, when the United States passed new amendments to the Clean Air Act. With these changes, the EPA placed a national cap on emissions of sulfur and nitrogen oxides and set up a system for polluters to trade permits among themselves. Title IV of the 1990 Clean Air Act established the allowance market system known today as the Acid Rain Program, which eventually became the prototype for emissions trading in all other major pollutants. The ultimate goal was to reduce annual SO2 emissions to about half of their 1980 levels. The cap was gradually lowered, with implementation coming in two stages of tightening operating restrictions on power plants.37 The market for emissions allowances simply would not function and create accurate pricing without an effective regulatory cap on the total number of allowances available.

When Congress placed an overall restriction on power plant emissions nationwide in 1990, plants had a choice: They could invest in cleaner fuels or abatement technologies, or they could purchase extra emissions rights from plants that had managed to achieve their own reductions and had surplus permits to sell. The ability to buy excess rights enables older, less efficient plants to comply with the new rules. Emissions targets are met at the lowest possible cost.38

In the initial phase of the program, from 1995 to 1999, the allowance market encompassed only about one-fifth of the nation’s plants, but it focused on the biggest polluters. Phase 2 kicked in after 2000, bringing virtually all power plants above a certain size into the market. One of the key features of this program is that “banking” is allowed; power plants can save their allowances for future use, though they cannot borrow permits from future years to pollute today. This provides additional flexibility and a much more meaningful price signal.39

The world sat up and took notice of the significant environmental progress achieved by this nationwide experiment in capping and trading pollutants. The initial goal was to cut annual sulfur dioxide emissions in half by 2010, but the cap-and-trade program achieved its targets three years ahead of schedule and at a fraction of the initial cost estimates.

In 1992, estimates of emissions rights ranged from $981 to $1,500 a ton. By 1998, the Chicago Board of Trade auctioned off a large number of allowances at $115 a ton40 (though it is important to note that improved technologies for burning low-sulfur coal and lower fuel costs simultaneously contributed to lowering these costs41). Prices spiked from 2004 to 2006, reaching over $1,400 a ton, but soon fell just as sharply. In 2008, the SO2 allowances saw a 65% price decline; that trend continued in 2009, with prices hitting $71 a ton by May.42

The program is now fully phased in, with the final 2010 SO2 cap set at 8.95 million tons, approximately one-half of the emissions from the power sector in 1980. Actual emissions in 2008 were well below that level, at 7.6 million tons.43 One widely cited study has estimated the cost savings of allowance trading at $784 million annually during the second phase of the program, which began in 2000. That is approximately 43% of the estimated cost of compliance under an enlightened command-and-control model of achieving reductions.44 The EPA also states that the program has achieved billions of dollars in health care savings each year, since the emissions removed from the air have been linked to heart and lung ailments.45 All in all, the U.S. experiment in curbing acid rain can be considered the first successful large-scale model of an environmental market.

Carbon Dioxide (CO2) Emissions Trading

Since carbon emissions increase the threat of significant climate change, setting up a trading system for emissions permits is the equivalent of taking out low-cost global risk insurance against infinitely larger societal, economic, and health consequences. Multiple economists (including Richard Sandor and Sir Nicholas Stern, author of Britain’s landmark study on global warming) have demonstrated the economic imperatives of acting to cut greenhouse gas emissions now rather than paying a crippling toll for inaction in the years to come. The benefits of decisive, early action on climate change far outweigh the costs of the irreversible impacts that may lie ahead, including volatile weather, coastal destruction, droughts, famines, species extinction, and migration.46

The industrialized world can make dramatic strides in bringing down CO2 emissions by utilizing financial innovations that drive down compliance costs, penalize environmentally harmful activities, and create incentives to change that behavior. Achieving these goals will not be easy, since the fossil fuels that produce greenhouse gas (GHG) emissions underlie almost every facet of the global economy; emissions are embedded in most of our daily activities. One study estimated that setting an aggressive cap that reduces emissions to 50% below their 1990 levels by 2050 would cause a hit to GDP of 1% per year—a significant cost, but one that can be absorbed. It also estimates that the price of allowances would rise from $41 per ton of carbon in 2015 to $161 per ton in 2050, causing conventional coal-fired power generation to fall out of favor by 2040. The proposed system could also generate hundreds of billions of dollars per year in government revenue if allowances are auctioned.47

But the remarkable aspect of the market-based solution is that reducing our carbon footprint is not only feasible, but consistent with growth. Implementing a cap-and-trade program for GHG emissions allowances will ensure that environmental policy has only a relatively contained impact on the U.S. economy. In fact, the benefits of developing a “green economy” include the possibility of spawning entirely new industries to provide environmental services. Tackling the emissions problem by imposing taxes or regulation runs the risk of slowing down overall growth. But a cap-and-trade system simply transfers capital from one part of the economy to another, slowing “dirty” sectors while jump-starting growth in green industries.48

The market for carbon trades is already a reality, whether it is voluntary (such as the Chicago Climate Exchange, a financial institution that currently operates North America’s only cap-and-trade system for all six greenhouse gases) or mandatory (such as the European Union Emissions Trading System, or EU ETS). Members of the Chicago Climate Exchange, which include a number of Fortune 500 companies and major utilities, make a voluntary but legally binding commitment to reduce their GHG emissions. Their reasons for joining range from bolstering their green credentials to gaining a leg up on compliance and trading competencies before such a system becomes mandatory.49 Ten Northeastern states are establishing a cap-and-trade program for their power sectors, called the Regional Greenhouse Gas Initiative (RGGI), and California may employ a similar approach as it seeks to implement 2006 legislation (AB 32) that mandates emissions reduction. As of this writing, Congress is preparing to debate landmark legislation that would establish a mandatory national cap-and-trade system across the United States. In the meantime, the Commodity Futures Trading Commission (CFTC) has already moved to begin regulating the Chicago Climate Exchange—a clear signal that the market has reached a new level of maturity.50

Launched in 2005, the EU ETS became the world’s first cap-and-trade system for CO2 emissions, and it remains the largest such market to date. Its inaugural three-year trial period reveals a number of instructive lessons, as outlined in an evaluation by the Pew Center for Global Climate Change. Allowances to emitters were initially overallocated, causing price volatility. But allowance banking and borrowing, along with better information flow and a switch to allocating allowances for longer trading periods, should address this issue. Overall, however, the market has developed with remarkable speed and smoothness, especially considering the number of sovereign governments involved. It generated an accepted price for tradable allowances, and an infrastructure of institutions, registries, and monitoring processes quickly took shape. Trading volumes have grown steadily. Businesses have already begun to incorporate the price of allowances into their decisions, thus internalizing what was once an externality.51

The successful functioning of a cap-and-trade program starts with standardizing the commodity (the offsets). The act of trading enables price discovery and builds the infrastructure and institutions that lower transaction costs. A system of hedging and options will evolve, as it has in other markets, and global harmonization and integration will quickly follow. If China and the United States, the world’s two largest sources of GHG emissions, were to form a global market, the impact would be sweeping and transformative.52

Flexibility encourages cost efficiency in approaching the problem of climate change.53 A cap-and-trade system allows individual emitters to decide which clean technologies to adopt. Instead of governments choosing which innovations to back, the marketplace decides—and that competition encourages breakthroughs and cost reductions.

Apart from cap-and-trade systems, there are complementary approaches to reducing global emissions. The Kyoto Protocol included provisions dubbed “flexible mechanisms.” These provisions allow industrialized economies to meet their reduction targets under the agreement by buying GHG emission credits through exchanges, by funding projects that reduce emissions in developing economies, or by buying credits from other developed countries with excess allowances.

Even if a developing nation has no GHG emissions restrictions, it now has a financial incentive to create abatement projects: the opportunity to earn “carbon credits,” or offsets, which can be sold to buyers from wealthier nations. The clean development mechanism (CDM) allows both emerging and industrialized economies to benefit from mitigation projects in the developing world. Projects must first be approved by a developing nation’s “designated national authority” and then submitted for accreditation by the Clean Development Mechanism Executive Board, which was established under the United Nations Framework Convention on Climate Change (UNFCC).54 Standardization of the CDM trading system is critical for reducing transaction costs, as it has been for the development of every financial market employing these tools.

Markets for Public Goods

The principles and prototypes used in emissions trading have applications in other environmental challenges, creating a chorus of possibility in financial innovation.

Saving Oceans and Fisheries: Individual Transferable Fishing Quotas

For millennia, fisheries have been considered a common property resource. Most people believed that the ocean’s supply of fish was limitless. But population growth and the industrialization of fishing have depleted that stock of capital at an alarming rate. Restoring the health of fisheries is a matter of urgent global concern, since just under 3 billion people depend on fish for 15% or more of their animal protein (in some emerging nations, it accounts for around half of animal protein intake).55 As fishermen race to exploit the last of a dwindling resource rather than restocking for the future, the tragedy of the commons comes into full play.

In 2006, marine ecologist Boris Worm issued a chilling report about the state of the world’s fisheries, predicting that continued bad practices would cause a global collapse of all fish species by 2048.56 In 2009, however, he issued an updated study with a brighter outlook, pointing to clear progress in restoring five out of ten major fisheries (including those in the United States) that have employed strong conservation-management measures. Despite these positive signs, he warns that a great deal of work still lies ahead: Many species remain threatened, and 63% of fish stocks need to be rebuilt.57

When it first became clear that intensive fishing could endanger renewal of the existing stock, command-and-control approaches were tried, such as imposing time limits on fishing or restricting the number of boats in a given area. But these regulations failed to accomplish much other than creating a frantic “rush to fish.” Fishermen incurred higher costs, but the stock of fishing capital was never rebuilt.

Today financial innovations are being applied to the problem, with the goal of restoring stocks, improving catch standards and revenue, and bringing economic sustainability to local fishing communities. There’s an old saying that fishing is like a bank account: You have to live off the interest and leave the principal intact (the fish you leave in the water being the principal here). Catch-share programs, or “limited access privilege programs” (LAPPs), allocate a dedicated percentage share of a fishery’s total catch to individual fisherman, communities, or associations. Originating in Australia, New Zealand, and Iceland in the 1970s, the catch-share management model is now employed at a number of federal fisheries in the United States.

Under a traditional system, fishery managers set a maximum total catch, and individual boats rush to haul in the largest catch possible before the entire fishery reaches its limit. But the catch-share program operates like a cap-and-trade program for emissions. Scientists determine the optimal annual numbers of fish that can be safely harvested in a given area, setting the total allowable catch (TAC). Permits for shares of that total catch are then distributed to commercial fishing operations, based on their historical catch or an auction. Fishermen then have the right to buy, sell, or lease these shares through individual fishing quotas (IFQs) and individual transferable quotas (ITQs). These are limited-access permits to harvest definite quantities of fish, essentially a property right conveyed by the government to a private party.

There are currently around a dozen fisheries operating under catch-share programs in the United States. The Obama administration recently proposed increased funding to greatly expand the program to additional fisheries, with the goal of restoring depleted stock and halting ocean damage from overfishing.58

Catch-share programs have increased the abundance of fish and cut in half the collapse rate for fisheries. According to Christopher Costello’s study of 121 fisheries that have implemented ITQs, catch-shares have halted, and even reversed, the global trend toward widespread fishery collapse.59 Another 14-month study by the Environmental Defense Fund found that catch-shares reduced “bycatch” (the netting of creatures other than the intended species) by more than 40%, and that catch-share fisheries deploy 20% less gear to catch the same amount of fish, leading to reduced ocean habitat destruction. The model also had a positive impact on the economic viability of fishing, raising revenue per boat by 80% in what were recently struggling fishing communities.60

Wetlands Mitigation and Biodiversity Banking

Human activity has had a devastating impact on the diversity of life on Earth—and that impact is growing, whether it is caused by land development, redirecting the flow of rivers, pollution, trawling the ocean floor, burning fossil fuels, or simple overexploitation. Great profits have been made along the way, but at a terrible cost to natural ecosystems—and to poor rural populations in the developing world, who tend to suffer most acutely when “free” services such as clean water, viable fishing grounds, and forest resources disappear.

The U.N.’s Millennium Ecosystem Assessment warned that the changes in biodiversity that have been taking place over the past 50 years are unprecedented in human history. It reported that natural habitats and species are declining by 0.5% to 1.5% per year, and that more land has been converted to crops in the past 60 years than in the eighteenth and nineteenth centuries combined. One-quarter of the world’s coral reefs have been destroyed or degraded in the last several decades, while more than one-third of mangrove forest was lost in the same time period, reducing coastal defenses against storms.62

Quantifying the very real economic benefit of ecosystem services is the first step toward internalizing these impacts in business decisions. A variety of approaches are being tried, from payments for watershed services (funded by a user tax and paid to encourage landowners to keep rivers and streams free of pollution and invasive plants) to “bioprospecting,” which involves charging companies (such as pharmaceutical firms) for the right to access and inventory areas rich in biodiversity, eventually receiving a share of the profits if the compounds and genetic materials they discover lead to new commercial products.

Some of the initial groundwork was laid in the United States by the Clean Water Act. The law states that any developer who wants to dredge or fill a sensitive wetland needs a permit from the U.S. Army Corps of Engineers or the EPA. Those agencies will try to avoid or minimize any damage to the land in question, but if they deem it cannot be avoided, the law directs developers to compensate by “creating, enhancing, or restoring” a wetland of similar function and value in the same watershed. The government thus forces developers to see wetland damage as a liability. The developer can turn to a third party to help them amass the credits they need to win approval—and thus wetland mitigation banking was born. Enforcement has to be a key component of this program, as government agencies must verify that wetland credits are truly comparable and the land is being maintained as intended in perpetuity. Although it is hard to get an accurate read on this market, it was recently estimated that there are 400 wetland banks operating in the United States in a market worth $3 billion a year. Entrepreneurial wetlands bankers constitute a major slice of this market.63

Once the wetland mitigation bank idea took hold, the same concept was stretched further and applied to endangered species. Instead of simply regulating landowners harboring rare species, the Endangered Species Act set up a mechanism to reward them. If a threatened woodpecker or an endangered species of fly, for example, lives on a developer’s property, the developer can get a permit to harm their habitat—if they compensate for it by creating or preserving habitat for that species somewhere else. The necessity of getting this permit and paying this price makes developers think twice before plowing through fragile land. But if they are bent on following through, they have to pay—and other owners holding similar habitat suddenly find themselves with a valuable commodity on their hands. “Conservation banking” or “species banking” is a relatively new idea, but one that is gaining traction. The Australian states of New South Wales and Victoria have launched similar programs to protect biodiversity and native vegetation.64

This burgeoning field is not without its controversies and growing pains. But the effort to place a value on biodiversity has caught the attention of national and world leaders. In December 2008, the U.S. Department of Agriculture announced the formation of the new Office of Ecosystem Services and Markets. And at their 2007 meeting in Potsdam, the G8 environment ministers (along with their counterparts from newly industrializing nations) agreed to launch a major study bent on assessing the global price of biodiversity. Their statement underlined the important role financial innovations can play in saving the planet:

We will approach the financial sector to effectively integrate biodiversity into its decision making ... and we will enhance financing from existing financing instruments and explore the need and the options of additional innovative mechanisms to finance the protection and sustainable use of biological diversity, together with the fight against poverty. In this context, we will examine the concept and the viability of payments for ecosystem services.65

Conclusions

Creating a sustainable economy will require massive investment to establish new means and methods of production, alternative energy, clean technologies, and new green industries. This kind of immense demand for capital is exactly the sort of trigger that sets financial innovation in motion.

The point of departure is the identification of specific market failures that result in environmental degradation. By developing techniques to account for environmental goods and services, innovators can devise market mechanisms and capital market solutions to environmental problems, opening the door to real progress in the quest to conserve air, water, fisheries, wildlife, and biodiversity.

The tools already exist to identify and internalize environmental costs, discover prices for environmental goods and services, and finance projects that address environmental needs. New markets have been built, and they are rapidly maturing. The ability to create new capital structures and build mutually beneficial relationships with equity and debt investors has increased the available funding for all types of green projects.

This field is currently operating with the winds of momentum in its sails, as visionary thinkers respond to the most urgent challenge of our era and devise creative new strategies for minimizing our footprint on the planet.

Endnotes

1 Robert Costanza, et al., “The Value of the World’s Ecosystem Services and Natural Capital,” Nature 387 (1997): 253–260. See also Gretchen Daily and Katherine Ellison, The New Economy of Nature: The Quest to Make Conservation Profitable (Washington, DC: Island Press, 2002).

2 Juliet Eilperin, “25% of Wild Mammal Species Face Extinction,” Washington Post (7 October 2008).

3 Anil Markandya, et al., “The Economics of Ecosystems and Biodiversity: Phase 1 (Scoping) Economic Analysis and Synthesis,” final report for the European Commission, Venice, Italy (July 2008).

4 Robert Stavins, “The Making of a Conventional Wisdom,” Belfer Center for Science and International Affairs, John F. Kennedy School of Government, Harvard University (13 April 2009). Available at http://belfercenter.ksg.harvard.edu/analysis/stavins/?tag=leaded-gasoline-phasedown.

5 Garrett Hardin, “The Tragedy of the Commons,” Science 162, no. 3859 (1968): 1,243–1,248.

6 Garrett Hardin, in The Concise Encyclopedia of Economics, 2nd ed. (Indianapolis: Liberty Fund, 2008).

7 Nathaniel Keohane and Sheila Olmstead, Markets and the Environment (Washington, DC: Island Press, 2007).

8 Ronald Coase, “The Problem of Social Cost,” Journal of Law and Economics 3 (1960): 1–44.

9 “Facts and Figures” summary from “Water in a Changing World,” United Nations World Water Development Report 3 (UNESCO, 2009): 8.

10 Anil Markandya, et al., “The Economics of Ecosystems and Biodiversity: Phase 1 (Scoping) Economic Analysis and Synthesis,” final report for the European Commission, Venice, Italy (July 2008).

11 Ricardo Bayon, “A Bull Market in Woodpeckers?” The Milken Institute Review (first quarter 2002): 30–39.

12 Ricardo Bayon, “Innovating Environmental Finance,” Milken Institute policy brief no. 25 (March 2001).

13 Environmental Protection Agency (EPA), “SRF: Initial Guidance for State Revolving Funds” (1988): 104.

14 EPA, “Guidebook of Financial Tools: Paying for Sustainable Environmental Systems” (2008). Available at www.epa.gov/efinpage.

15 EPA, “Clean Water State Revolving Fund Programs,” 2008 Annual Report: Cleaning Our Waters, Renewing Our Communities, Creating Jobs (2008): 2. Available at www.epa.gov/OWM/cwfinance/cwsrf/.

16 EPA, “Financing America’s Clean Water Since 1987: A Report of Progress and Innovation” (1987): 7–8. Available at www.epa.gov/OWM/cwfinance/cwsrf/.

17 EPA, “Clean Water State Revolving Fund Programs, 2008 Annual Report: Cleaning Our Waters, Renewing Our Communities, Creating Jobs (2008): 18.

18 Presentation by Steve Townley, Finance Officer of the Missouri Environmental Improvement and Energy Resources Authority, at a Milken Institute Financial Innovations Lab held 5 November 2008 in Israel.

19 EPA, “Drinking Water State Revolving Fund 2007 Annual Report: Investing in a Sustainable Future” (March 2008): 3. Available at www.epa.gov/safewater/dwsrf/index.html#reports.

20 EPA fact sheet, “Using the Clean Water State Revolving Fund” (2002). Available at www.epa.gov/owow/wetlands/facts/contents.html.

21 EPA, “Long Island Facts, Figures, & Maps.” Available at www.epa.gov/NE/eco/lis/facts.html.

22 Audubon Society, Long Island Sound Campaign, “Lifeline to an Estuary in Distress” (DATE).

23 EPA fact sheet, “Using the Clean Water State Revolving Fund” (2002). Available at www.epa.gov/owow/wetlands/facts/contents.html.

24 Jeffrey Q. Chambers, Niro Higuchi, Edgard S. Tribuzy, and Susan E. Trumbore, “Carbon Sink for a Century,” Nature 410, no. 6827 (March 2001): 429.

25 Thomas A. Sancton, Barry Hillenbrand, and Richard Hornik, “Hands Across the Sea,” Time (2 January 1989). Available at www.time.com/time/magazine/article/0,9171,956635-2,00.html.

26 Conservation International, www.conservation.org/sites/gcf/Documents/GCF_debtfornature_overview.pdf.

27 USAID, www.usaid.gov/our_work/environment/forestry/intro_eai.html.

28 Environmental Foundation of Jamaica, www.efj.org.jm/Current_Projects/current_projects.htm.

29 USAID, www.usaid.gov/our_work/environment/forestry/tfca.html.

30 Marc Lacey, “Costa Rica: U.S. Swaps Debt for Forest Aid,” New York Times (17 October 2007).

31 The Nature Conservancy, www.nature.org/wherewework/centralamerica/costarica/misc/art22576.html.

32 “Biggest U.S. Debt Swap for Nature Will Conserve Guatemala’s Forests,” USAID press release (2 October 2006).

33 “Largest TFCA Debt-for-Nature Agreement Signed to Conserve Indonesia’s Tropical Forests,” U.S. State Department press release (30 June 2009).

34 “U.S. to Forgive $30 Million Debt to Protect Sumatra’s Forests,” Conservation International press release (30 June 2009).

35 Joel Kurtzman, “The Low-Carbon Diet: How the Market Can Curb Climate Change,” Foreign Affairs (September–October 2009): 114–122.

36 Ibid.

37 EPA, Overview: The Clean Air Act Amendments of 1990, Title IV: Acid Deposition Control. Available at www.epa.gov/air/caa/caaa_overview.html#titleIV.

38 Richard L. Sandor and Jerry Skees, “Creating a Market for Carbon Emissions: Opportunities for U.S. Farmers,” Choices, Magazine of the American Agricultural Economics Association (first quarter 1999): 13.

39 Keohane and Olmstead, Markets and the Environment, Markets and the Environment (Washington, DC: Island Press, 2007).

40 Richard L. Sandor and Michael J. Walsh, “Some Observations on the Evolution of the International Greenhouse Gas Emissions Trading Market,” in Emissions Trading: Environmental Policy’s New Approach, Richard Kosobud, ed. (New York: John Wiley & Sons, 2000).

41 Curtis Carlson, Dallas Burtraw, Maureen Cropper, and Karen Palmer, “Sulfur Dioxide Control by Electric Utilities: What Are the Gains from Trade?” (discussion paper no. 98-44-REV, Resources for the Future, 2000): 4.

42 EPA, Clean Air Markets, Emissions, Compliance, and Market Data, www.epa.gov/airmarkets/progress/ARP_1.html.

43 Ibid.

44 Carlson, et al., “Sulfur Dioxide Control by Electric Utilities: What Are the Gains from Trade?” (discussion paper no. 98-44-REV, Resources for the Future, 2000): 4.

45 EPA, www.epa.gov/acidrain/effects/health.html.

46 Nicholas Stern, The Economics of Climate Change: The Stern Review (Cambridge, UK, and New York: Cambridge University Press, 2007).

47 Robert N. Stavins, “A U.S. Cap-and-Trade System to Address Global Climate Change,” (discussion paper no. 2007-13, The Brookings Institution, October 2007).

48 Kurtzman, “The Low-Carbon Diet: How the Market Can Curb Climate Change,” Foreign Affairs (September–October 2009).

49 Chicago Climate Exchange, Overview, www.chicagoclimatex.com/content.jsf?id=821.

50 Simon Lomax, “CFTC Plans to Regulate Chicago Climate Exchange, Gensler Says,” Bloomberg (27 August 2009).

51 A. Denny Ellerman and Paul L. Joskow, The European Union’s Emissions Trading System in Perspective, Pew Center for Global Climate Change (May 2008).

52 Ibid.

53 Michael J. Walsh, “Maximizing Financial Support for Biodiversity in the Emerging Kyoto Protocol Markets,” The Science of the Total Environment 240, nos. 1–3 (1999): 145–156.

54 Available at http://cdm.unfccc.int/index.html.

55 “The State of the World’s Fisheries and Aquaculture 2008,” United Nations Food and Agriculture Organization.

56 Boris Worm, et al., “Impacts of Biodiversity Loss on Ocean Ecosystem Services,” Science 314, no. 5800 (2006): 787–790.

57 Boris Worm, et al., “Rebuilding Global Fisheries,” Science 325, no. 5940 (2009): 578–585.

58 Alison Winter, “Obama Administration Proposes Major Spending for Fishery Cap-and-Trade Plan,” New York Times, 11 May 2009.

59 Christopher Costello, Steven D. Gaines, and John Lynham, “Can Catch Shares Prevent Fisheries Collapse?,” Science 321, no. 5896 (2008): 1678–1681.

60 “Sustaining America’s Fisheries and Fishing Communities: An Evaluation of Incentive-Based Management,” Environmental Defense Fund (2007): 4, 18.

61 James Sanchirico and Richard Newell, “Catching Market Efficiencies: Quota-Based Fisheries Management,” Resources for the Future (Spring 2003); Boris Worm, et al., “Rebuilding Global Fisheries,” Science 325, no. 5940 (2009): 578–585; and Richard Newell, James Sanchirico, and Suzi Kerr, “Fishing Quota Markets,” Resources for the Future (discussion paper 02-20, August 2002).

62 United Nations Millennium Ecosystem Assessment, Findings (2005). Available at www.millenniumassessment.org/en/SlidePresentations.aspx.

63 Ricardo Bayon, “Using Markets to Conserve Biodiversity,” State of the World 2008, Worldwatch Institute.

64 Ibid. See also Bayon, “A Bull Market in Woodpeckers?” The Milken Institute Review (First quarter 2002).30–39.

65 “Biodiversity and Ecosystem Services: Bloom or Bust?” United Nations Environment Program Finance Initiative (March 2008): 7.