7. Financing Cures

Science has entered a thrilling new era. Study of the human genome has brought us tantalizingly close to discoveries that can reduce suffering and save lives. But translating research into real treatments is a tortuous process that requires major long-term investment and no small risk of failure.

At the very moment when profound new breakthroughs seem to be within our grasp, there has been a precipitous decline in financing for early-stage biomedical research. This constraint is first and foremost a tragedy for those individuals who are waiting desperately for cures. It is also a factor that limits productivity gains in the global economy and keeps developing nations mired in poverty.

Large pharmaceutical companies, with their powerful research arms and great depth of resources, have traditionally driven most research and development of new treatments. Today, however, that engine of innovation is stalling. Major pharmaceutical firms have seen their business models stagnate, and most have withdrawn from risky early-stage drug discovery and development, instead directing more resources into late-stage developments, line extensions, and “me too” drugs (slight variations on existing medications).1

Research and development (R&D) productivity—as measured by applications to the FDA, both to initiate clinical trials and to market new drugs—has lost momentum.2 Despite increased overall R&D spending and technological advances, the introduction of new priority drugs (treatments that the FDA defines as constituting “a significant therapeutic or public health advance”) has declined, from more than 13 per year in the 1990s to approximately 10 per year in this decade.3

A 2007 report on the industry’s outlook from The Economist summed up the problem of the dwindling drug pipeline, quoting a study from CMR International, a consulting firm. In a typical year during the 1990s, CMR found that the industry typically spent $35 billion to $40 billion a year on R&D and came out with 35–40 new drugs. By 2004, annual spending exceeded $50 billion, but fewer than 30 new drugs were introduced. In 2006, those numbers deteriorated even further: Spending had swelled past $60 billion, with no increase in the number of new drugs brought to market.4

The old business model, in which vertically integrated pharmaceutical giants banked on developing the next blockbuster drug, was once extremely profitable but is becoming unsustainable. In addition to coping with pricing pressures and the prospect of an unprecedented wave of blockbuster patent expirations in the next decade,5 the industry must find ways to respond to the smaller niche markets that are likely to be created as we enter an era of personalized medicine.6

A fresh approach to innovation is needed. The industry is experimenting with new research models, including the outsourcing of R&D operations. But in the meantime, financial innovators have a role to play in supporting the scientific discovery process by bridging the funding gap, which is most acute from very early-stage drug discovery R&D through Phase II clinical trials. This is the point of scientific risk in which capital is critically needed to see that projects make it to the marketplace.

Table 7.1. Types of Financial Innovations for Accelerating Cures

The Structural Demand for Capital

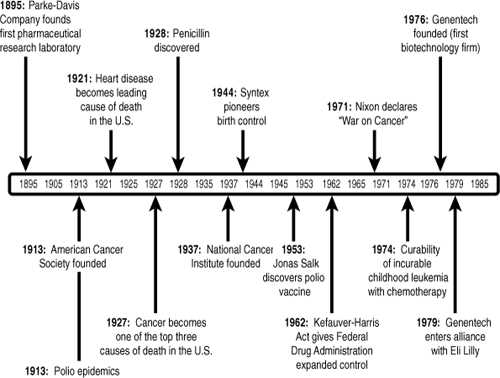

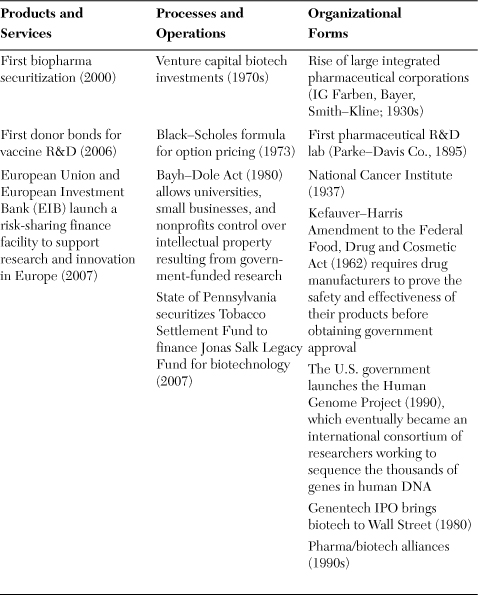

Though the first efforts to finance cures date back to the rise of large integrated pharmaceutical corporations in the 1930s, the business of directing capital to achieve greater results in the life sciences has intensified most rapidly over the past few decades.7 Applying the tools of venture capital, public equity markets, securitization, and public–private partnerships greatly increased the accessibility of capital for drug and medical device development. Valuation methodologies (including Black–Scholes and Monte Carlo estimations) made it possible to monetize intellectual property in new ways, while policy and organizational changes enabled commercialization from government and university labs (via the Bayh–Dole Act of 1980) and other knowledge-sharing organizations (from the National Cancer Institute to the Human Genome Project). A complex ecosystem has formed over the years to support medical innovation, with private-sector R&D complemented by publicly funded health-related research, much of which falls under the auspices of the National Institutes of Health (NIH).

The decline in R&D productivity, which first emerged in the 1990s, is captured by the following contradiction: From 1993 to 2004, the pharmaceutical industry reported that annual R&D spending increased by 147%, but the number of new drug applications submitted annually grew by only 38% (and generally declined over the past several years). In 2004, only 102 applications were submitted to the FDA, representing a 21% drop from 1999 levels. While applications for “new molecular entities”—truly novel drugs—increased from 1993 to 1995, they fell by 40% in the following decade.8

From 1998 to 2003, steady annual increases doubled the NIH budget, increasing federal support for biomedical R&D. But from 2004 through 2008, NIH research funding remained static (and its purchasing power actually decreased due to inflation).9 Hopefully, the infusion of $10 billion into the NIH under the American Reinvestment and Recovery Act of 2009 may start to change these dynamics, but future funding levels will, of course, be subject to the prevailing political and economic winds.

The decline in R&D productivity has painful real-world consequences, as promising discoveries in the fight against cancer and other diseases languish for lack of capital resources and development expertise. But current trends do not point to easy solutions. According to the pharmaceutical industry’s trade group, we have entered the era of the billion-dollar drug; the average cost of bringing a new therapy through development, clinical trials, and market launch has risen sharply, from $138 million in 1975 to $1.318 billion in 2006.10 And market launch is no guarantee of success: Only two out of ten drugs generate enough revenue to recover R&D costs.11

Generic drugs, a major source of competition, currently capture almost two-thirds of U.S. prescription drug volume (but only 16% of total pharmaceutical sales dollars).12 Although generics obviously lower costs for consumers and many health insurers now insist on them, this competition does create another pressure that discourages big companies from deploying their extensive research capacity in risky and expensive drug development.

The major drugs launched in 1965 could expect to thrive in the marketplace for 10–12 years without competition. By 1985, this window had shrunk to 5 years, and the high-profile therapies launched after 1995 have faced immediate competition, sometimes within the same year.13 When one blockbuster drug debuts against another, large pharmaceutical companies cannot recoup their investments.14 Over time, the industry has become more risk averse as a result. The estimated average out-of-pocket cost per new drug has increased at an annual rate of 7.4% above inflation.15

For pharmaceutical and biotech firms, increasingly unfavorable cost–benefit considerations can stifle experimentation, especially for high-risk or niche products. Because of the huge commitment of time and resources it takes to obtain FDA approval for a new drug, many pharmaceutical companies prefer to invest in a safer bet: promoting existing drugs by extending labels, changing doses, or changing drug combinations for existing treatments.16 This diversion of resources to “me too” drugs exacerbates the deficiency in the pipelines. The numbers reveal an extreme picture. In 2006, 123 new drug applications were submitted to the FDA, but only 22 were for truly novel drugs (new molecular entities). The rest were variations on existing therapies.17 Biologically based drugs (new biologic license applications) are even scarcer. Only four such treatments were approved by the FDA in 2006.18

Faced with tough market conditions, pharmaceutical companies often take a shortcut to innovation by purchasing the rights to drugs under development from biotech firms. Yet candidates are scarce on the horizon these days. Emerging biotech companies face a tough slog to commercialize their discoveries and keep going through the arduous process of proving their potential in the early phases of clinical development. Their funding limitations are about to affect the industry at large.19

Biotech firms work on the frontier of medical science, applying the latest technologies in the quest to develop breakthrough therapies. But operating on the cutting edge has its risks, and young biotech firms face many practical business hurdles to fulfilling their scientific promise. The process of developing cures requires a long-term capital commitment that cannot be cut short by premature investor exits.

The old model of venture-based biotech development (often referred to as the “California model”) that dominated in the 1980s and 1990s went like this: You take great research work from the University of California or Stanford, form a company, land venture capital, issue an IPO, and grow up to be Genentech or Amgen. But that model is dead (see Figure 7.1). In today’s environment, few investors are willing to take a chance on premature IPOs with excessive valuations and unproven cash flows. The current recession has seen the market for biotech IPOs grind to a virtual standstill. With the closing of the IPO window, many firms fail to secure the funding they need for development needs.

Figure 7.1. Biotech IPOs over the past three decades

Note: date for 2009 up until 11/3/09.

Sources: SDC (Thomson Reuters), Milken Institute.

A Tough Journey through Two “Death Valleys”

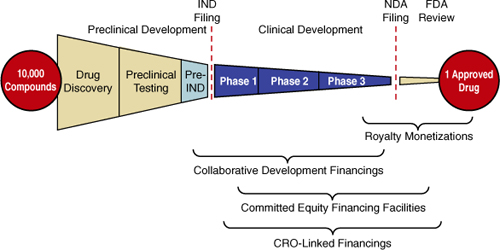

The process of commercializing a new cure in the United States is a long and winding road. This initial phase of scientific discovery, when promising targets are discovered and linked to disease, can take many years of work in both university and industry labs. Going from discovery and validation to assay development can be equally as painstaking, followed by stages that include high-throughput screening and identification of compounds that safely alter the activity of a particular target cell or disease before its efficacy can be tested in clinical trials. Then it’s on to the steps described below20:

• Phase I. This is the first time the drug is tested on humans. Usually 20–80 normal, healthy volunteers take the drug to test it for toxicity (negative side effects) and demonstrate its effect on people of different races.

• Phase II. This is still a pilot stage. But this time the volunteers suffer from the disease the drug aims to help. About 100–300 patients are involved, and the trial can last up to two years. Phase IIA typically focuses on refining dosage requirements, while IIB analyzes efficacy. This phase provides the preliminary data needed to prepare for the larger, Phase III trials.

• Phase III. This is the main clinical trial, usually involving 1,000–3,000 patients. The trial tests for both therapeutic effects and adverse reactions. If there are established drugs for the disease, the new drug is tested against the best on the market. If there is no existing drug, the new drug is tested against a placebo. One group of patients will be given the new drug; another will get either a placebo or an established drug.

• Phase IV. Phase IV is carried out after the drug has been registered with the FDA. The trial is conducted to allow local doctors to become familiar with the drug and to gain their trust.

Many fledgling biotech companies start to undertake this process before their viability has been proven, and they may lack an experienced management team. The financial bottleneck created in the preclinical phase dooms many projects that show high potential for medical success. Due to its harsh nature, this roadblock has been termed the first “death valley.”

A second death valley occurs a few years later, starting at Phase IIB and continuing throughout the approval and marketing phases. In other words, funds are lacking during most clinical trial stages and also after FDA approval. A lucky few biotech firms resolve the funding problem through collaborations with pharmaceutical companies that can provide appropriate marketing resources after FDA approval.

In their long sojourn for FDA approval, drugs face complex regulatory barriers. Even the successful launch of a drug does not guarantee financial success. In some cases, safety issues become apparent only after a drug has been widely used, leading regulators to issue “black box” warnings or even ban certain products that had already made it through the FDA approval process.

From the small start-up in a funding squeeze to the behemoth under pressure from shareholders, generic competition, and regulators, the biopharmaceutical industry is undergoing a painful shakeup that could impede, if not derail, the advancement of next-generation treatments and cures—unless new financial innovations and public policies are applied to help the industry better deal with risk.

Sources for Biomedical Funding

Predominant Methods

The avenues available for emerging biotech firms to finance the development of new therapies include the following:

• Venture capital (VC). Pooling investment dollars from pension funds, universities, and wealthy individuals, venture capitalists have been drawn to the potential of biotech ever since the success of Genentech. But many of the long-shot bets made on early-stage discoveries in the 1990s failed to pan out, causing more risk aversion in this arena. From 2002 through 2007, more than $29 billion in VC funding went to the life sciences, with most of that money concentrated in biotech.21 Biotech also claimed the largest share of VC in the second quarter of 2009, with $888 million going into 85 deals.22 But current levels of VC funding in all industries is a fraction of the levels seen in 2000; and in the aftermath of the financial meltdown, there is a shortage of capital in the sector. Stepping into the void are the large pharmaceutical firms themselves.23 The venture-capital arm of Johnson & Johnson, for example, provided some 30% of the funding to Novocell, a privately owned company focused on producing insulin from human embryonic stem cells for use in diabetes treatment.24 Pfizer, Eli Lilly & Co., Roche, and Merck, among others, have likewise established venture capital operations specifically to invest in promising biotech startups.

• The financial markets. Especially in the 1990s, many biotech companies banked on the prospect of eventually going public. Even after the initial IPO, publicly traded companies can issue secondary offerings of shares, and this strategy has been used frequently by U.S. biotech and pharmaceutical firms. But the demand for shares in public offerings has weakened worldwide, and particularly in the United States, significantly affecting biotech. Yet even when it is applicable, this funding method holds clear disadvantages, as new offerings dilute existing shareholders’ stake in the company. At the same time, the value of the company’s shares does not usually reflect its intrinsic value or the potential value of the company it were to be acquired. Moreover, in recent years, demand from investors has mainly been directed toward companies at advanced phases of development.

• Private investments in public equity (PIPEs). Small to medium-size companies that are already publicly traded but continue to experience funding constraints are increasingly turning to private sources, a.k.a. private investments in public equity (PIPEs), for capital injections. PIPE deals offer much greater speed and efficiency than issuing a secondary offering of shares and fulfilling the related regulatory requirements. In a traditional PIPE, the investor gets to purchase common or preferred stock at a discounted price, while a structured PIPE deal involves purchasing convertible debt. In November 2009, for example, StemCells Inc., a Palo Alto–based biotech company focused on developing treatments for neurological disorders, announced its ninth PIPE offering; the company has raised $133.8 million through these financings. San Diego–based Cardium Therapeutics, which develops novel biologic therapeutics and medical devices for cardiovascular and ischemic disease, has similarly conducted multiple rounds of PIPE financing to raise almost $83 million.25

• Mergers and acquisitions (M&A). The large pharmaceutical companies are increasingly innovating by acquisition, and selling out to one of these giants is considered a profitable endgame for many biotech entrepreneurs. A thriving M&A market has yielded numerous purchases of promising drugs, some at relatively early phases. In one of the most recent deals, European pharmaceutical giant Sanofi-Aventis in 2009 paid $500 million to acquire BiPar Sciences, a small California-based biotech firm that is developing cancer therapies.26

• Sales of promising drug pipelines, still in development, to large pharmaceutical companies. Pharmaceutical firms can also bolster their pipelines by acquiring specific drugs or drug portfolios rather than acquiring an entire biotech firm. In November 2009, Japan’s Takeda Pharmaceutical Co. announced plans to pay up to $1 billion for obesity treatments being developed by Amylin Pharmaceuticals, a San Diego–based biotech. Takeda also agreed to pay 80% of the cost of obtaining FDA approval for the drugs.27

Innovative Business and Financial Models to Bridge the Capital Gap

Opening New Avenues

While most capital is raised through the channels described previously, several new and innovative financing techniques have emerged to see drugs through the difficult journey shown in Figure 7.2:

• Financing by projected royalty streams. Future royalty streams from expected product sales can be sold in exchange for immediate capital by means of debt or investment. One of the earliest examples of this type of deal took place in 2000, when Yale University, in conjunction with Royalty Pharma AG and BancBoston Capital, agreed to pay royalties on an HIV/AIDS drug discovered at Yale to Bristol-Myers Squibb in exchange for $79 million in funding. A few years later came a deal that built in greater diversification: the Royalty Securitization Trust I, which securitized royalties from 23 biopharmaceutical products, medical devices, and diagnostics from 19 companies for $228 million. In that deal, the Paul Royalty Fund had invested in the young companies and then exchanged a portion of its royalty rights for an upfront payment. In 2005, the royalties from eight drugs owned by a subsidiary of Drug Royalty LLC that had been in the market an average of seven years were collateralized for $68.5 million. And in 2007, Northwestern University sold an undisclosed portion of its royalty interests to Royalty Pharma for $700 million. Each transaction required a rating by Standard & Poor’s and/or Moody’s; the ratings ranged from AAA to BB. Two of the deals also had credit insurance.28 This model and its potential variations will be discussed in greater detail in the following section.

Figure 7.2. Funding techniques prominently employed in the U.S.

Source: Mark Kessel and Frederick Frank, Nature Biotechnology, 2007

• Collaborative development financing. In this model, biotech company A grants license and access to its promising drug pipeline to pharmaceutical firm B, which has the resources to bring these projects to their final phases of development and secure FDA approval. In return, company A receives right of first refusal to repurchase the drugs from firm B at a pre-established price. Firm B assumes the risk of development costs in case of failure.

• Contract research organization (CRO)–linked financings. A CRO provides R&D services to biotech companies, supplying required funding and resources (such as skilled manpower or infrastructure for clinical trials, as well as other services required for FDA approval) at a relatively inexpensive price in return for future royalties of drug sales or ownership in the companies it serves. A recent study estimated that demand for CRO services will grow by 16% annually over the next three years.29 In addition to lowering expenses, this strategy may allow biotech firms to write off overhead as a variable cost rather than a fixed cost, rendering the services even cheaper.

• Committed-equity financing facilities (CEFF). This model involves a financing commitment for a limited timeframe, during which publicly traded companies may sell a predefined amount of stock at a price lower than market price, thus securing funds over longer periods of times.

• Designated funds. Funds designated to promote treatment for specific diseases occasionally finance R&D up to Phase II. Often disease-specific philanthropic foundations will become involved in this form of mission-related investment.

• Incubators promoted by large pharmaceutical companies. Large pharmaceutical firms can team up with venture capital funds to finance promising drug development and create incubators to support emerging biotechnology companies. Approximately 40% of funds invested in emerging U.S. biotech companies are raised this way.30

University Partnerships, Private Equity, and Public-Sector/Foundation Investing

More than 30 years ago, researchers from Stanford and the University of California, San Francisco, achieved new breakthroughs in recombinant DNA. This cutting-edge science seemed to present an astounding array of possibilities for commercial applications—and thus the biotech industry was born. This resulted in a flourishing ecosystem of spin-offs, start-ups, and collaborations among biotech firms, investors, and academia. The 1980 Bayh–Dole Act shored up these collaborations by opening up the ivory tower to commerce—allowing universities to own, license, and market the results of their faculty research. The United States led the way in this regard, and nations around the globe quickly followed.

Corporate labs once generated the bulk of research and innovation, but those processes are increasingly shifting back to where they began: the university campus. A number of private/university collaborations have emerged to fund preclinical and Phase I trials. These partnerships were formed to help projects progress out of the university lab and begin early commercialization.

As the global economy increasingly becomes a knowledge economy, universities are natural partners for both business and government. They contribute not only talent and facilities, but an average of approximately $2 million in equity for each venture they fund. But the catch with this business model is that universities need to attract outside investors or partners for the more expensive Phase II funding.31

Private equity has produced additional financing and partnership models. Symphony Capital, a hands-on private equity firm based in New York City, not only funds biotech research, but also, through partnership with RRD International, manages the development process, from preclinical and regulatory phases through manufacturing.

The public sector can also play a role in investing. In 2007, the European Union and the European Investment Bank (EIB) created a risk-sharing finance facility (RSFF). Under the RSFF, the EIB will match up to $1.29 billion from the EU with $1 billion of its own resources to support riskier R&D programs by lending to new entities.32 The EIB will financially sponsor up to 50% of loans, based upon due diligence, thus encouraging other lenders to participate. No external rating is imposed upon the debt, thus enabling companies with low credit ratings but exciting potential to obtain funding.

Another intriguing template mitigates risk and speeds scientific innovation by utilizing disease-specific foundations to establish a “science commons” that designs and defines funding agreements to create a body of shared research and clinical data for a single disease. For example, a foundation may fund projects at a number of universities but find that it must negotiate with each university’s technology transfer office if professors from different universities want to work on the same stem cell lines and reagents. The commons is a mechanism for streamlining contracts, definitions, and funding agreements, allowing funded researchers direct access to the research materials of other researchers also funded by the foundation.33 A further possibility would be to structure a funding and research company that would out-license intellectual property funded by the foundation. The holding company, a specialized special-purpose vehicle (SPV), could then create a royalty stream used to entice university technology transfer offices into the commons. There has been ongoing interest in the scientific community in adopting these ideas, particularly as they relate to sharing of data and resources.34

Overcoming the Limits of Public Equity and Venture Capital Funding

Venture capital and the public equity markets are currently the major sources of funding for medical research, but these two channels alone are proving unable to finance faster cures.

The typical venture capital cycle spans three to six years prior to exit. That timeline, too, presents a fundamental mismatch with the 20-year development cycle that some science requires. The resulting misallocation of capital can prevent medical advances.

Going public does not magically solve the problem for most biotech firms. The difficulties of running a publicly traded company with ten-year or longer investment cycles but short-term earnings pressure is considerable. Most of the typical company’s funding is generated through a single IPO. But due to the volatility of the equity market—particularly for the biotech sector—such offerings may generate less capital than expected or may have to be delayed. The value of a company’s specific technology may be overshadowed by the market’s prevailing sentiment on biotech in general. Potentially life-saving breakthroughs may fall victim to the market’s whim in a given week regarding the sector as a whole.

Since the prevailing channels of financing are problematic, it makes sense to consider a paradigm shift. If there is a way to estimate the value of royalties over time from a portfolio of patents relevant to a particular disease group or medical problem, then the portfolio could be turned into a marketable security that would provide capital for accelerating research. By securitizing or “monetizing” preexisting technology licenses, a company can achieve short-term financing with no negative financial statement or tax consequences and without having to issue additional equity (in other words, with little or no negative impact on the ability to complete an IPO at a later date when market conditions might be more favorable). This structure also has the advantage of enabling investors to bypass the volatility of the equity market and invest more directly in a company’s technology, ultimately sharing in the profitability of that technology.

Potential securitizations for drug development should be considered in the context of intellectual property (IP) protection and commercialization. In general, only about 5% of the innovations in a given intellectual property portfolio has commercialization value.35 Many types of intellectual property (such as copyright royalties, the value of patents, and the value of drug compounds) display a similar distribution of risk and returns (with only a small number of units accounting for large payoff). This pattern of discovery, development, and concentration of financial returns is common to all industries (including entertainment, media, and publishing) in which value overwhelmingly rests upon intangible assets such as ideas. The pooling of multiple patents provides crucial risk diversification, since not all scientific avenues will come to full fruition. The larger the pool of early-stage projects, the greater the odds that one will succeed.

The challenge is to devise a capital structure with credit enhancement, advance sales, and other financial, marketing, or business strategies that align the interests of foundations, investors, patients, governments, and businesses. It should be able to tap liquid capital markets and diversify risks; lower the costs of capital to biotech, pharmaceutical, and medical device companies; and attract scientific and management talent with equity-based compensation. The rules of fundamental analysis and capital structure necessary for financing these vehicles remain constant.

The role of insurance and risk management in meeting this challenge can be crucial. Undertaking this (by providing loan-loss guarantees or credit enhancement through program-related investing at a below-market rate) would require a fundamental shift in the thinking of foundations that focus on disease cures. It would mean using their balance sheets to leverage further private investment in cures rather than following a model of handing out scientific grants.

The most natural analogy with past innovations in the financial markets comes from the corporate bond market. At one time, no one would invest in below-investment-grade debt. But given a transparent valuation model (which clarified the attributes of value and risk to all) and market liquidity, investors were willing to take on the risk and flocked to the new market segment. The odds hadn’t suddenly changed, but transparency made those odds understandable. Similarly, the options markets soared after the introduction of the Black–Scholes option-pricing model. Once investors could identify risks and returns, they could calibrate option prices against other traded securities.

In both of these examples, a market gap was closed by the combination of transparent valuation models and market liquidity. In the pharmaceutical industry, transparent valuation models should be able to play an important role in closing the Phase II funding gap for drug discovery, attracting new sources of funding.

To ensure full transparency, a securitization related to the drug discovery process would have to involve patent attorneys with expertise in the life sciences; medical experts who can assess scientific methods, risks, and implications; pharmaceutical industry experts who can quantify the prospects for commercialization and expected royalties; and foundations with an interest in providing funding and/or credit guarantees.

Strategies for Credit Enhancement in Medical Financing

Credit risk in biomedical securitizations could be reduced by utilizing collateral, insurance, or risk-sharing agreements that would basically subsidize the risk of other investors independent of the balance sheet or performance of the target biomedical companies or projects. Credit enhancement has been used in corporate bonds, securitized debt, derivatives, and other financial instruments. It can be accomplished internally (by providing excess spread over the interest rate received on the underlying collateral, overcollateralization, or a reserve account that could reimburse losses) or externally (through surety bonds, a wrapped security insured or guaranteed by a third party, a letter of credit, a cash collateral account, or another method by an external party in case of default).

Let’s consider two examples of how this could accelerate medical development and commercialization.

Credit Enhancement by Disease-Specific Foundations

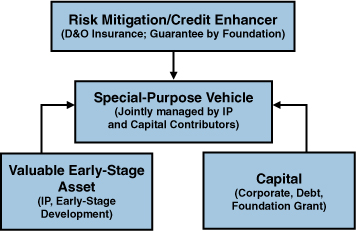

When it comes to credit enhancement, it is insufficient for medical IP holders and capital providers to simply join forces. They need a legal structure to capture the governance, obligations, and payouts of their collaboration. Figure 7.3 illustrates the requisite elements of a transaction.

Figure 7.3. Leveraging foundations to accelerate cures

Source: Technology Option Capital, LLC

The capital provider could be an experienced pharmaceutical industry player with the know-how to reduce development and commercialization risk and create a productive environment for the working scientists. Or it might be a foundation wishing to contribute funding (for a share of the returns) or a guarantee to other capital providers.

The assets could consist of a diversified patent pool (with IP rights obtained from universities or pharmaceutical/biotech firms) and the human capital involved in early-stage development. In this case, a special-purpose vehicle (SPV), a private company, would be comprised of the assets (the intellectual property and talent) provided in exchange for equity, and would be jointly managed by the IP holder and the investors. The goal of the SPV would be to develop the technology or science, increase its value, and reduce the commercial risk to large pharmaceutical firms. (Under this scenario, the IP suppliers would become minority investors with certain protections that ensure them a reasonable return on their equity.)

The SPV could be adapted to the interests of a foundation focused on specific disease research. A foundation focused on Alzheimer’s, for example, might assemble a diversified pool of drugs under development for the disease. While this would reduce the risk of scientific failure, significant commercialization risks would remain, preventing the SPV from issuing investment-grade debt. The foundation could provide the financial guarantee—a credit enhancement that raises the credit quality of the pool—thus opening up the SPV to a larger market of investors. If the guarantee is actually used, it could become a grant, although the diversification of scientific approaches should help to mitigate this risk.

Disease-specific medical foundations, however, require predictable spending on projects, since their budgets typically consist of returns on endowments and can’t support intermittent calls on their capital from a guarantee. To accommodate this process, a disease-specific foundation could provide credit enhancement through the following scenarios:

- After a ratings agency reviews the deal structure to help raise it to investment grade, the foundation could invest 10%–15% of the funding and place a smaller guarantee to raise the credit quality.

- The foundation could work with insurance companies to structure a credit enhancement that better fits its budgetary needs.

- A disease-focused foundation could collaborate with larger foundations, again providing just enough capital and guarantee to bring the transaction structure to investment grade.

The SPV’s equity capital, which could be structured as the purchase price of a call option on control of the SPV, could come from a major pharmaceutical player (much as large pharmaceuticals invest in later-stage biotech firms today). To reduce investor risk, the equity capital could be leveraged 3:1 with debt capital, which, in turn, would be supported by credit enhancements to mitigate risk (such as directors and officers liability insurance, R&D tax credits, or foundation credit enhancements).

Risk mitigation using a market-based analysis allows risk apportionment to different parts of the capital markets and capital providers (including foundations) based on their unique risk appetites. The venture would be successful once the large pharmaceutical firm exercised its call option (and, with that payment, retired the debt). Other scenarios exist for the exercise of the option through a sales/license-back transaction of the IP rights with a private equity investor. Alternatively, the principal on the bonds could be settled with cash raised through the patent investment entity’s exercise of a put option to the insurer.

Using Directors and Officers (D&O) Liability Insurance to Enhance Credit Quality

Directors and officers (D&O) insurance covers the actions of senior corporate management and board members, and includes actions pertaining to intellectual property and product development. For a premium increase, this coverage could be expanded to the scientific and commercial risks of biotech product development.

As a commercial entity, the SPV in Figure 7.3 could carry D&O insurance, which would serve as an additional credit enhancement. The policy would insure against actions the board may take that could harm the value of the firm, including technology management, in general, and drug development failure, in particular. Insurers are already exposed to technology risk, and because the SPV governance structure increases transparency, they should be willing to provide extra coverage for an extra premium.

Financial Innovations to Improve Global Health

In addition to the industry-wide phenomenon of faltering R&D productivity, there is a larger and more pressing problem at work: glaring imbalances in the allocation of health-care investment worldwide. Less than 10% of global investment in pharmaceutical R&D targets diseases such as malaria, AIDS, and tuberculosis that cause untold suffering in developing nations and may affect up to 90% of the world’s population.36

The elimination of widespread ailments such as malaria would have a significant impact on economic growth in emerging nations, reducing inequality around the globe.37 But profit pressures lead pharmaceutical companies to focus on “lifestyle” drugs and treatments for “Western” diseases that are concentrated in more affluent nations, leaving other drug development issues unaddressed. In the current financial environment, good ideas with the potential to cure diseases of poverty are nearly impossible to fulfill. Creative strategies are needed to channel capital to where it is most urgently needed.

The fight against tuberculosis (TB) is a case in point. The World Health Organization (WHO) estimates that one-third of the world’s population is vulnerable to TB, which claims 1.7 million lives each year.38 The nonprofit Global Alliance for TB Drug Development (the TB Alliance) formed a public–private partnership between Bayer Healthcare AG to jumpstart the fight against this deadly disease. It has been estimated that the global market for a tuberculosis drug is $261 million to $418 million.39 The relatively small profit potential in this market (especially when weighed against drug development costs), plus the fact that TB disproportionately affects emerging nations, has made this effort unattractive for any single drug company. As a consequence, doctors treating TB patients are forced to rely on drugs that were developed decades ago; these outdated therapies must be taken for six months at a time.40

The Alliance has taken steps to catalyze medical solutions and save lives. It pursues intellectual property rights in the area of TB research, as well as coordinating drug trials and research efforts. It is funded through country donations (primarily from Europe and the United States), as well as the Bill & Melinda Gates Foundation and the Rockefeller Foundation.41

The Bayer/TB Alliance partnership, announced in 2005, is illustrated in Figure 7.4. Its goal is to coordinate global clinical trials to study the potential of an existing antibiotic, moxifloxacin, in the treatment of TB. In an animal study, moxifloxacin shortened the standard six-month clinical treatment of TB by two months.

Figure 7.4. Transaction structure of Bayer–TB Alliance partnership

Source: Milken Institute

The TB Alliance has been coordinating and helping to cover the cost of the trials, leveraging substantial support from several U.S. and European government agencies. As Figure 7.4 shows, the partnership’s goal is to make an anti-TB drug available at a not-for-profit price. With its costs covered, Bayer could sustain the supply. Furthermore, if the drug development process is successful, Bayer will receive approval from the FDA for an additional prescriptive use for moxifloxacin (under the brand name Avelox); approval may come as soon as 2011.42 As of January 2009, moxifloxacin is in Phase III trials in several locations in Africa.43 After decades with no progress being made on this deadly affliction, this innovative partnership model has revived the drug pipeline for TB.

Another interesting public–private partnership was forged between GlaxoSmithKline Biologicals (GSK) and the International Aids Vaccine Initiative (IAVI). Similar to the TB partnership discussed previously, GSK and IAVI are collaborating to stop the spread of HIV/AIDS. Their goal is to make a sustained supply of an AIDS vaccine available at a not-for-profit price by GSK.44 In the first years of the alliance, new neutralizing antibodies have been discovered that give promise for further drug development for a vaccine drug target.

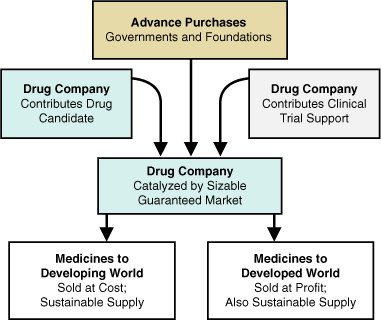

In late 2004, Britain announced major support to shore up the fight against HIV/AIDS. A key element of the British proposal was a major advance purchase agreement (also known as an advance market agreement)—a pledge to purchase millions of doses of an AIDS vaccine, if and when it is developed.45 Under advance market commitments, donors commit money to vaccine makers, guaranteeing the price of vaccines once they have been developed; this gives vaccine makers the incentive to invest the sums required to conduct research, pay staff, and utilize or build manufacturing facilities. Participating companies make binding commitments to supply the vaccines at lower, sustainable prices after donor funds are used up.

Also in 2004, Britain joined with other nations to make a similar commitment to ensure delivery of a breakthrough malaria vaccine developed by GSK. In an interview with the BBC, Gordon Brown, then Britain’s chancellor of the exchequer, summed up why these advance purchases work, stating, “The challenge is in an area where there are insufficient purchasers with funds. We need to ensure that the vaccine does go into commercial production and is available at affordable prices. And therefore I can announce that the British government, working with other governments, is ready to enter into agreements to purchase these vaccines in advance, to ensure a secure market and that these vaccines are available more cheaply.”46

The idea continues to gain traction: In early 2007, a new $1.5 billion multilateral program called the Advance Market Commitment was launched to finance the development of vaccines for children in the world’s poorest countries, using funding donated by international governments. The first phase has focused on producing the pneumococcal vaccine, which prevents deadly pneumonia in children. The plan calls for developed nations to make advance purchases of the vaccine on behalf of poor countries that request them, giving them purchasing power they did not have before. The program “creates market incentives where the private market fails,” noted Tommaso Padoa-Schioppa, the Italian finance minister, at the program’s official launch.47

Advance purchase agreements, illustrated in Figure 7.5, change the economics of the public–private partnership by creating a stable market that will pay fair market price for the therapy. They create a privatization effect, eliminating the need for complex coordination between multiple government agencies, foundations, and the nonprofit catalyst. Where drug makers were once reluctant to enter markets for treating diseases of poverty, this innovation reduces their uncertainty about future returns. By creating a stable market, governments and nongovernmental organizations (NGOs) can redirect the industry’s research capacity to where it is most desperately needed.

Figure 7.5. Transaction structure of advance purchase agreements

Source: Milken Institute

Health economics experts have argued that advance purchases can create a market for treatments in the developing world that is just as robust as that for pharmaceutical products in developed countries. This “pull mechanism,” whereby products are delivered on a demand basis, is likely to be a cost-effective use of public funds.

In a recent study, economists at the National Bureau of Economic Research (NBER) calibrated the potential of advance purchase agreements. Estimates show that biotech and pharmaceutical companies are motivated to pursue drug prospects for markets of $3 billion in revenue or larger. At $15 per dose for the first 200 million vaccines purchased, and $1 per dose thereafter, a $3 billion market could be created by advance purchases. The economists found that the $15-per-dose cost of this financial mechanism is several orders of magnitude more cost effective than current treatments in underfunded countries.48

A critic of the advanced purchase commitment, Andrew Farlow of Oxford University, has argued that the program design will not lead to the most effective cure because it rewards the first pharmaceutical solution to market.49 What if the second vaccine to market is the better cure? Program supporters say that not all funds will be spent at once, so there will be purchasing power left if newer alternatives emerge. Farlow also argues that the program design is rife with potential corruption, as the host government is asked to contribute $1 per vaccine, while the foundations pay $14. An unscrupulous firm could potentially bribe government officials to allocate millions of dollars in revenue.

While these are substantive criticisms, they must be weighed against the apparent preference of foundations and country donors for advance purchase commitments as the best avenue currently available for accelerating treatments to save lives now rather than at some future date.

Using Donor Bonds to Underwrite Medical Research and Drug Delivery

In March 2005, six European governments announced application of a new financial innovation, donor bonds, to accelerate the delivery of medicines to Africa. The bond offerings, expected to total $4 billion over several years, will increase the available funding for immunization in Africa.

Donor bonds, like credit card companies, use future customer repayments as the collateral for borrowing. (In this case, future gifts are the collateral.) Donors guarantee binding commitments that can be advanced under borrowing facility arrangements through bank consortia or capital market securitizations. The future stream of payments is transformed into an immediate lump sum.

Say the pharmaceutical company has already developed a drug and is now marketing it in the developed world at a profit and selling it in the developing world at cost. The donor bonds infuse the developing market with greater demand in the near-term. As the drug is already in production, the mechanics of meeting challenge are now simple ones of production and supply-chain expansion.

The first donor bonds were issued in November 2006, backed by a stream of future donations from the United Kingdom, France, Italy, Norway, Sweden, South Africa, and Spain. (The U.S. government has declined to participate, saying that the federal budget process does not allow for the long-term commitments required by this securitization structure.) The bonds were issued by an SPV known as the International Finance Facility for Immunisation (IFFIm), with the World Bank acting as its financial advisor and treasury manager.50 The programs financed by the bonds will be managed by the Global Alliance for Vaccines and Immunization (GAVI), which has received a pledge of $750 million over ten years from the Bill & Melinda Gates Foundation. GAVI expects that the acceleration of immunizations through donor bonds will save the lives of 5 million children and protect another 5 million as adults. In 2007 alone, some $633 million in IFFIm funding went to efforts such as immunization safety programs, strengthening of health services in developing nations, and efforts to eradicate polio, measles, maternal and neonatal tetanus, and yellow fever.51 Multiple vaccine bonds have been issued, including one launched in June 2009 for $1.5 billion in commitments to guarantee prices to drug makers to produce vaccines for developing countries.

Another organizational model has emerged to address infectious diseases of poverty: the nonprofit pharmaceutical company. Industry veteran Dr. Victoria Hale founded OneWorld Health in 2000 to develop effective and affordable new medicines for neglected diseases that disproportionately affect emerging nations. She has assembled a scientific team that identifies promising drug candidates for diseases that are not profitable for the pharmaceutical giants to pursue.

As a nonprofit, OneWorld Health receives funding from foundations and governments, and provides a tax deduction based on the projected future value of donated intellectual property. It frequently enters into research collaboration with major drug makers and provides a viable path for off-patent drugs that otherwise would not be pursued for new uses. Therapies are being developed for parasitic diseases like kala azar in India, and special focus is given to creating new treatments for common killers like diarrhea and malaria.52

Conclusions

Tangible capital (such as stock, factories, and bank accounts), important as it may be, is not the driver of the twenty-first-century economy. That distinction belongs to human capital. Ideas, research, and new technologies are the new currency—and nowhere are the possibilities more exciting than in the field of medical research.

But it is a sad irony of our time that while immense scientific and technological potential exists to cure disease, customize treatment, and improve global health standards, a funding gap hampers the journey from early-stage research to marketplace. The process of commercializing basic research into new therapies has become fraught with pitfalls.

Although the current state of R&D productivity looks discouraging, we cannot afford to allow stagnation. Today’s challenge is to rethink the financial underpinnings of the research model, finding a way to infuse the system with momentum. If financial innovators apply their best ideas to this arena, we can free scientists to pursue their most promising ideas, hopefully bringing us closer to the long-sought goals of saving lives and reducing suffering in the developing and developed worlds alike.

Whether the solution is diversification and pooling, enhanced D&O insurance, an increased role for foundations and public–private partnerships, advance purchases, donor bonds, or a combination of strategies, one thing remains clear: The capital gaps in the development of drug, medical devices, and health-care technology can be surmounted. Financial technologies, innovative securitization, and structured finance can overcome these barriers, allowing science to fulfill its promise.

Endnotes

1 Jeffrey S. Handen, Industrialization of Drug Discovery (Boca Raton, FL: CDC Press, 2005).

2 Patrick O’Hagan and Charles Farkas, “Bringing Pharma R&D Back to Health,” Bain & Company research report (2009): 1–2.

3 Congressional Budget Office, “Pharmaceutical R&D and the Evolving Market for Prescription Drugs,” Economic and Budget Issue Brief (26 October 2009).

4 “Billion Dollar Pills,” The Economist 27 January 2007.

5 Standard & Poor’s, “Industry Surveys: Healthcare: Pharmaceuticals” (June 2009): 15.

6 Deloitte Consulting LLP, “Reinventing Innovation in Large Pharma” (December 2008); 2. Available at www.deloitte.com/view/en_US/us/Services/consulting/article/fbec1ec6f6001210VgnVCM100000ba42f00aRCRD.

7 This chapter draws on research and presentations from multiple Milken Institute Financial Innovations Labs on accelerating medical solutions. Reports detailing the research, presentations, and findings of these workshops are available for download at www.milkeninstitute.org. We are also indebted to the work of our sister organization, Fastercures (www.fastercures.org).

8 U.S. Government Accountability Office, “New Drug Development: Science, Business, Regulatory, and Intellectual Property Issues Cited as Hampering Drug Development Efforts,” Report to Congress (November 2006).

9 American Association for the Advancement of Science Budget and Policy Programs, www.scienceprogress.org/2009.02/nih-funding-to-states.

10 Pharmaceutical Research and Manufacturers of America (PhRMA), Pharmaceutical Industry Profile 2009. Available at www.phrma.org/publications/.

11 J. Vernon, J. Golec, and J. DiMasi, “Drug Development Costs When Financial Risk Is Measured Using the Fama-French Three Factor Model,” unpublished working paper (January 2008), cited in PhRMA’s Pharmaceutical Industry Profile 2009.

12 Standard & Poor’s, “Industry Surveys: Healthcare: Pharmaceuticals” (June 2009): 21.

13 A. Jena, J. Calfee, D. Goldman, E. Mansley, and T. Philipson, “Me-Too Innovation in Pharmaceutical Markets,” forthcoming, Forums for Health Economics and Policy. See also Tomas Philipson, “The Regulation of Medical Innovation and Pharmaceutical Markets,” Journal of Law and Economics 45, no. S2 (October 2002): 583–586.

14 Joseph A. DiMasi, Ronald W. Hansen, and Henry G. Grabowski, “The Price of Innovation: New Estimates of Drug Development Costs,” Journal of Health Economics 22 (2003): 151–185.

15 Gary P. Pisano, Science Business: The Promise, the Reality, and the Future of Biotech (Cambridge, MA: Harvard Business School Press, 2006).

16 Thomas H. Lee, “Me-Too Products: Friend or Foe?” New England Journal of Medicine 350, no. 3 (2004): 211–212.

17 FDA, Summary of NDA Approvals & Receipts, 1938 to the Present, www.fda.gov/AboutFDA/WhatWeDo/History/ProductRegulation/SummaryofNDAApprovalsReceipts1938tothepresent/default.htm.

18 FDA, NME Drug and Biologic Approvals in 2006, www.fda.gov/Drugs/DevelopmentApprovalProcess/HowDrugsareDevelopedandApproved/DrugandBiologicApprovalReports/NMEDrugandNewBiologicApprovals/ucm081673.htm.

19 IMS Annual U.S. Pharmaceutical Market Performance Review(12 March 2008).

20 Mark C. Fishman and Jeffrey A. Porter, “Pharmaceuticals: A New Grammar for Drug Discovery,” Nature (22 September 2005): 491–493.

21 Patrick Mullen, “Where VC Fears to Tread,” Biotechnology Healthcare (29 October 2007): 29–35.

22 PricewaterhouseCoopers and National Venture Capital Association, MoneyTree Report (Q2 2009 U.S. Results): 2–3.

23 “Big Pharma Invests Where VC Fears to Tread,” Boston Business Journal (14 August 2009).

24 Heidi Ledford, “In Search of a Viable Business Model,” Nature Reports: Stem Cells, published by Nature online (30 October 2008). Available at www.nature.com/stemcells/2008/0810/081030/full/stemcells.2008.138.html.

25 The PIPES Report, DealFlow Media, PipeWire (19 October 2009 and 2 November 2009).

26 Adam Feuerstein, “Sanofi-Aventis to Buy Cancer Drug Firm BiPar,” TheStreet.com (15 April 2009). Available at www.thestreet.com/story/10486199/sanofi-aventis-to-buy-cancer-drug-firm-bipar.html.

27 Elizabeth Lopatto and Kanoko Matsuyama, “Takeda Agrees to Buy Rights to Amylin’s Obesity Drugs,” Bloomberg (2 November 2009).

28 Glenn Yago, Martha Amram, and Teresa Magula, “Financial Innovations Lab Report: Accelerating Medical Solutions,” Milken Institute (October 2006).

29 Tufts Center for the Study of Drug Development, Outlook 2008: 6.

30 G. Steven Burrill, Biotech 2009: Life Sciences. Navigating the Sea Changes (San Francisco: Burrill & Company LLC, 2009).

31 Bioaccelarate Holdings changed its name to Gardant Pharmaceuticals in 2006 and was later acquired by Switch Pharma. Principals from the company participated in a Milken Institute Financial Innovations Lab.

32 “Life Support for Life Science Innovation,” Nature Biotechnology 25, no. 2 (2007): 144.

33 Marty Tenenbaum and John Wilbanks, “Health Commons: Therapy Development in a Networked World,” MIT (May 2008).

34 Paul Schofeld, et al., “Post-Publication Sharing of Data and Tools,” Nature 461 (10 September 2009): 171–73.

35 Glenn Yago, Martha Amram, and Teresa Magula, “Financial Innovations for Accelerating Medical Solutions,” Financial Innovations Lab Report, Milken Institute (October 2006).

36 Frank Lichtenberg, “Pharmaceutical Innovation, Mortality Reduction, and Economic Growth,” in Measuring the Gains from Medical Research: An Economic Approach, Kevin M. Murphy and Robert H. Topel, eds. (Chicago: University of Chicago Press, 2003).

37 J. L. Gallup and J. D. Sachs, “Cause, Consequence, and Correlation: Assessing the Relationship between Malaria and Poverty,” Commission on Macroeconomics and Health, World Health Organization (2001). See also Gary S. Becker, T. J. Philipson, and R. R. Soares, “The Quantity and Quality of Life and the Evolution of World Inequality,” American Economic Review 95, no. 1 (2005): 277–291; David N. Weil, “Accounting for the Effect of Health on Economic Growth,” Quarterly Journal of Economics 122, no. 3 (August 2007): 1,265–1,306; and Daron Acemoglu and Simon Johnson, “Disease and Development: The Effect of Life Expectancy on Economic Growth,” Journal of Political Economy 115, no. 6 (December 2007): 925–985.

38 World Health Organization, Initiative for Vaccine Research, Selection of Diseases in IVR Portfolio. Available at www.who.int/vaccine_research/diseases/ari/en/index4.html.

39 N. R. Schwalbe, et al., “Estimating the Market for Tuberculosis Drugs in Industrialized and Developing Nations,” International Journal of Tuberculosis and Lung Disease 12, no10 (2008): 1173–1181.

40 TB Alliance, Mission & History, www.tballiance.org/about/mission.php.

41 TB Alliance, Donors, www.tballiance.org/about/donors.php.

42 John Lauerman, “Bayer Drug May Cut Tuberculosis Cure Time by Months,” Bloomberg (17 September 2007).

43 Economist Intelligence Unit, “World Pharma: TB Initiatives Bearing Fruit,” Industry Brief (January 2009). Available at www.tballiance.org/newscenter/view-innews.php?id=830.

44 “GSK Biologicals and IAVI Partner to Develop AIDS Vaccine,” IAVI press release (21 June 2005). Available at www.iavi.org/news-center/Pages/PressRelease.aspx?pubID=3044.

45 Ben Russell, “Brown to Earmark £200 M a Year to Fund AIDS Vaccine,” The Independent (1 December 2004).

46 “Britain Backs Anti-Malaria Fight,” BBC Online (24 November 2004). Available at http://news.bbc.co.uk/2/hi/uk_news/politics/4038377.stm.

47 Elizabeth Rosenthal, “Wealthy Nations Announce Plans to Develop and Pay for Vaccines,” New York Times (10 February 2007).

48 Ernst Berndt, Rachel Glennerster, Michael Kremer, Jean Lee, Ruth Levine, Georg Weizsäcker, and Heidi Williams, “Advanced Purchase Commitments for a Malaria Vaccine: Estimating Costs and Effectiveness,” (working paper no. 11288, NBER, May 2005).

49 “Push and Pull: Should the G8 Promise to Buy Vaccines That Have Yet to Be Invented?” The Economist (23 March 2006). More of Professor Farlow’s critiques can be found at www.economics.ox.ac.uk/members/andrew.farlow.

50 IFFIm, Offering Memorandum (9 November 2006).

51 IFFIm, “Results,” www.iff-immunisation.org/immunisation_results.html.

52 One World Health: A New Model for the Pharmaceutical Industry, Case Western Reserve, Weatherhead School of Management (19 January 2006).