Forensic Accounting Profession

Executive Summary

Forensic accounting has advanced as a distinct profession with the accounting and business profession. Several professional organizations have developed certifications in forensic-related services, from fraud examination to valuation investigation and determination. These certifications demonstrate educational credentials, expertise, experience, and ethical considerations of forensic accountants. This chapter presents several professional certifications relevant to forensic accounting practices and services.

Introduction

The existence and persistence of financial scandals, financial crises, and related FSF reinvigorated interest in education and practice of forensic accounting and FSF examination. Forensic accounting is gaining considerable attention as the American Accounting Association (AAA) has added a new educational and research section on “Forensic Accounting” and the SEC has strengthened its FSF divisions and trained its staff in the area of forensic accounting and FSF, all international public accounting firms have established a forensic accounting department, and forensic accounting and fraud examination is becoming one of the fundamental components of business schoolscurriculum in recent years. Several professional organizations have established certifications in forensic accounting practices. These forensic-related certifications demonstrate forensic accountants’ commitments and professionalism. These certifications require practicing forensic accountants to obtain education, work experience, and continuing professional education (CPE) as well as complying with codes of professional ethics. This chapter presents certifications and professional ethics relevant to forensic accounting.

Initiatives to Promote Forensic Accounting

Several global initiatives have been taken in recent decades, to promote forensic accounting and thus to combat fraud. When a company is not effective in generating sustainable performance, management is under more pressure to manage earnings. Opportunities to engage in FSF are higher when the company is not doing well financially and unable to invest in effective corporate governance and internal controls. Emerging corporate governance reforms, securities laws, and best practices are intended to identify and minimize potential conflicts of interest, as well as the incentives, and opportunities to engage in FSF. The American Institute of Certified Public Accountants (AICPA) issued Statement of Auditing Standards No. 82 (SAS No. 82)1 and then SAS NO.99, “Consideration of Fraud in a Financial Statement Audit” in 2002.2 Sarbanes-Oxley Act of 2002 was passed by Congress to combat FSF.

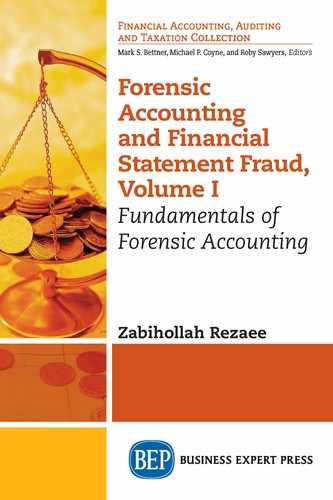

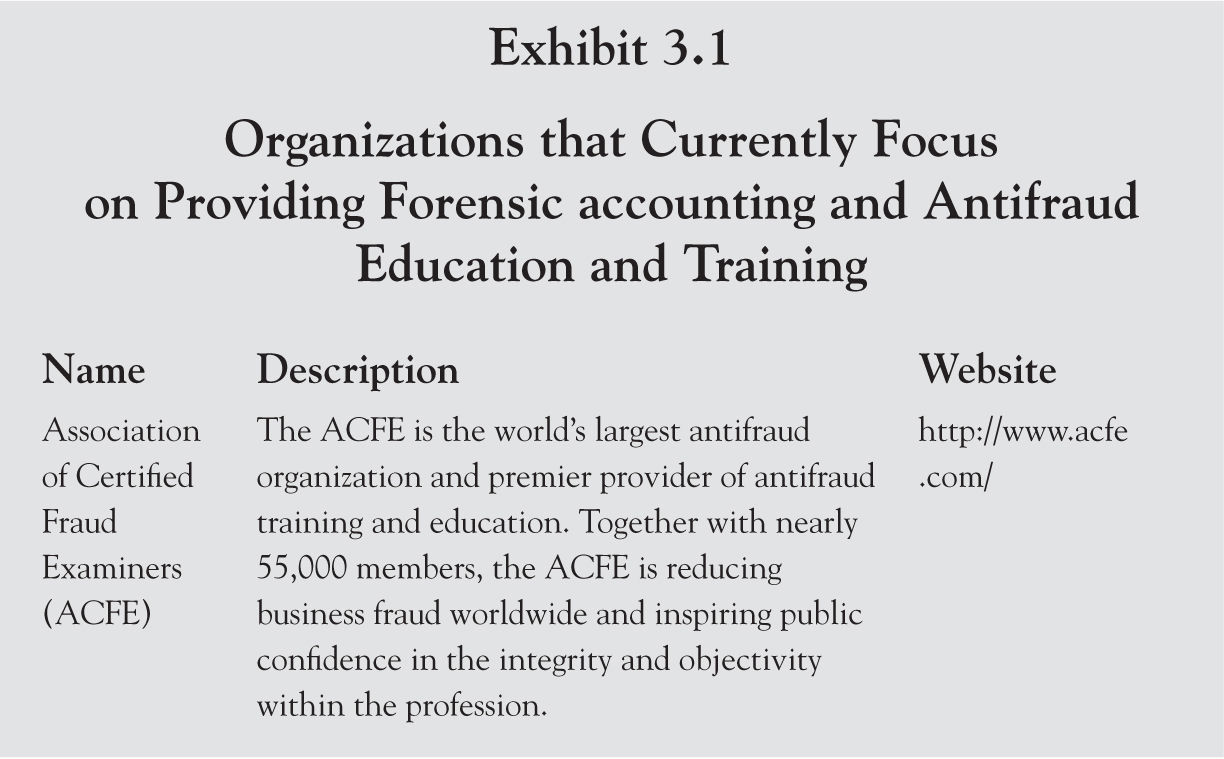

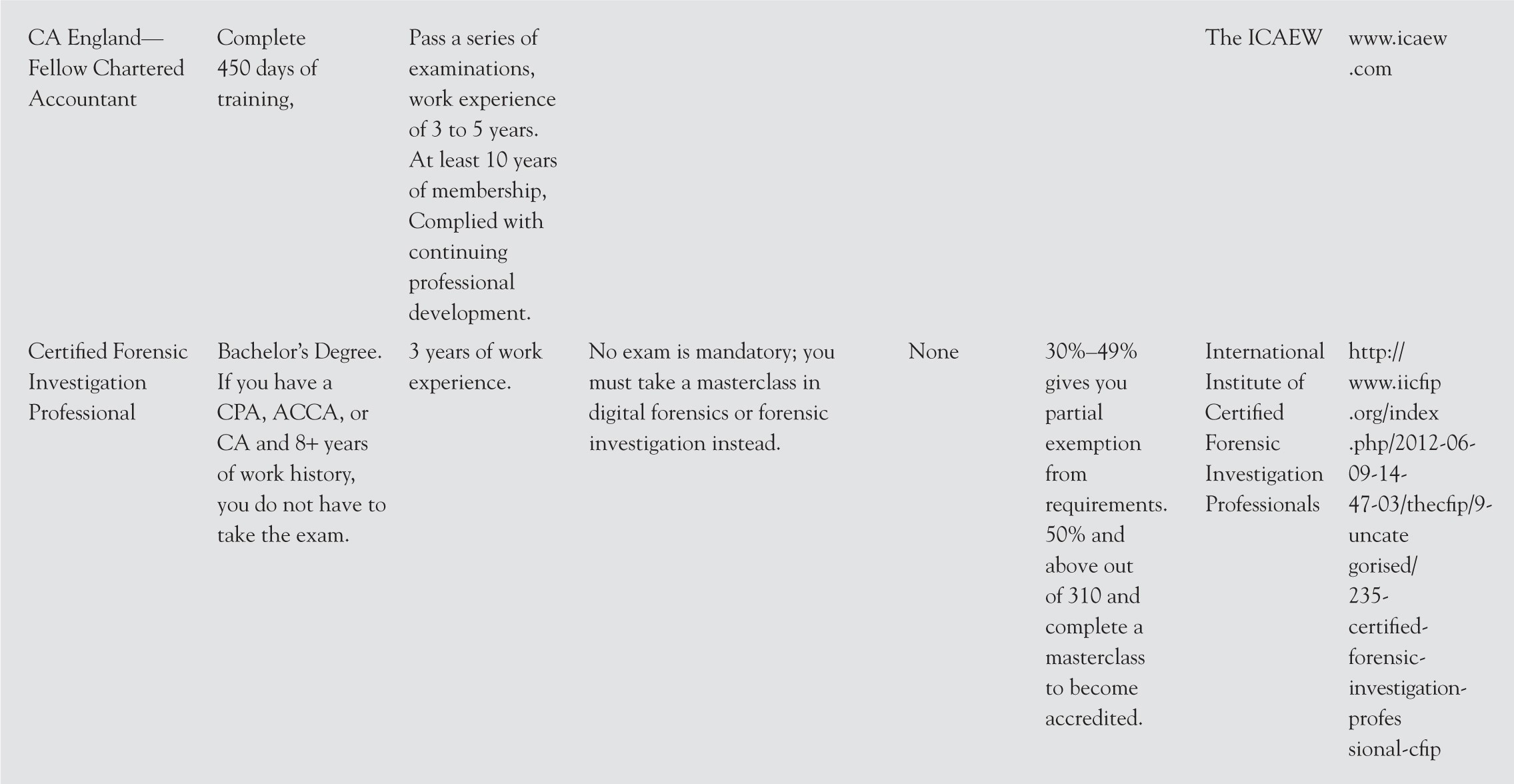

Exhibit 3.1 presents information about organizations that currently focus on providing education and training for forensic accountants, and some of these professional organizations and their role in promoting forensic accounting are described in the following paragraphs. The Forensic Accounting section of the AAA is dedicated to the continual improvement of forensic accounting research and education, through the encouragement, development, and sharing of (1) the promotion and dissemination of forensic and investigative academic and practitioner research; (2) the relevant and innovative curricula with an emphasis on effective and efficient instruction; (3) the exploration of knowledge-organization issues related to forensic accounting programs; and (4) the creation and presentation of CPE courses to members and professionals.

The International Forensic Accounting Association (IFAA) offers membership to individual accountants and accounting firms. The IFAA aids those in need of a forensic accountant with the ability to (1) search for criteria within their location; (2) correspond with those who meet their criteria; (3) participate in the forensic accounting forums to learn about the field and their situation by experts; and (4) find the right accountant to conduct forensic accounting services. National Association of Certified Valuation Analysts’ (NACVA) Financial Forensics Institute (FFI) was established in partnership with some of the nation’s top minds and authorities in forensic accounting, law, economics, valuation theory, expert witnessing, and support fundamentals. It began with the idea of establishing an association for certified public accountants (CPAs) and business professionals that could support their needs in providing intangible asset valuation and financial litigation consulting services. This organization provides training and CPE courses to members and nonmembers.

The National Association of Forensic Accountants (NAFA) provides training and certification to CPAs in various fields of forensic accounting and provides availability and access to the services of those who have achieved NAFA CERTIFIED status. NAFA is the oldest association of CPAs specializing in forensic/investigative accounting organization as well as the fastest growing. The International Institute of Certified Forensic Accountants (formerly the Association of Chartered Certified Forensic Accountants), founded in 2015, is a global organization that administers the forensic accounting exams and grants certification to candidates who pass the exam. The International Institute of Certified Forensic Accountants is a member of the International Federation of Forensic Accountants and Auditors (IFFAA). The American Institute of Certified Public Accountants (AICPA) released its proposed new professional standards for CPAs who perform forensic accounting services. The new proposed Statement on Standards for Forensic Services No. 1 (SSFS 1) was published in December 2018 and is intended to provide more focused and tailored authoritative guidance to CPAs who perform forensic services.3 The proposal would take effect for new engagements accepted on or after May 1, 2019, with early adoption permitted.

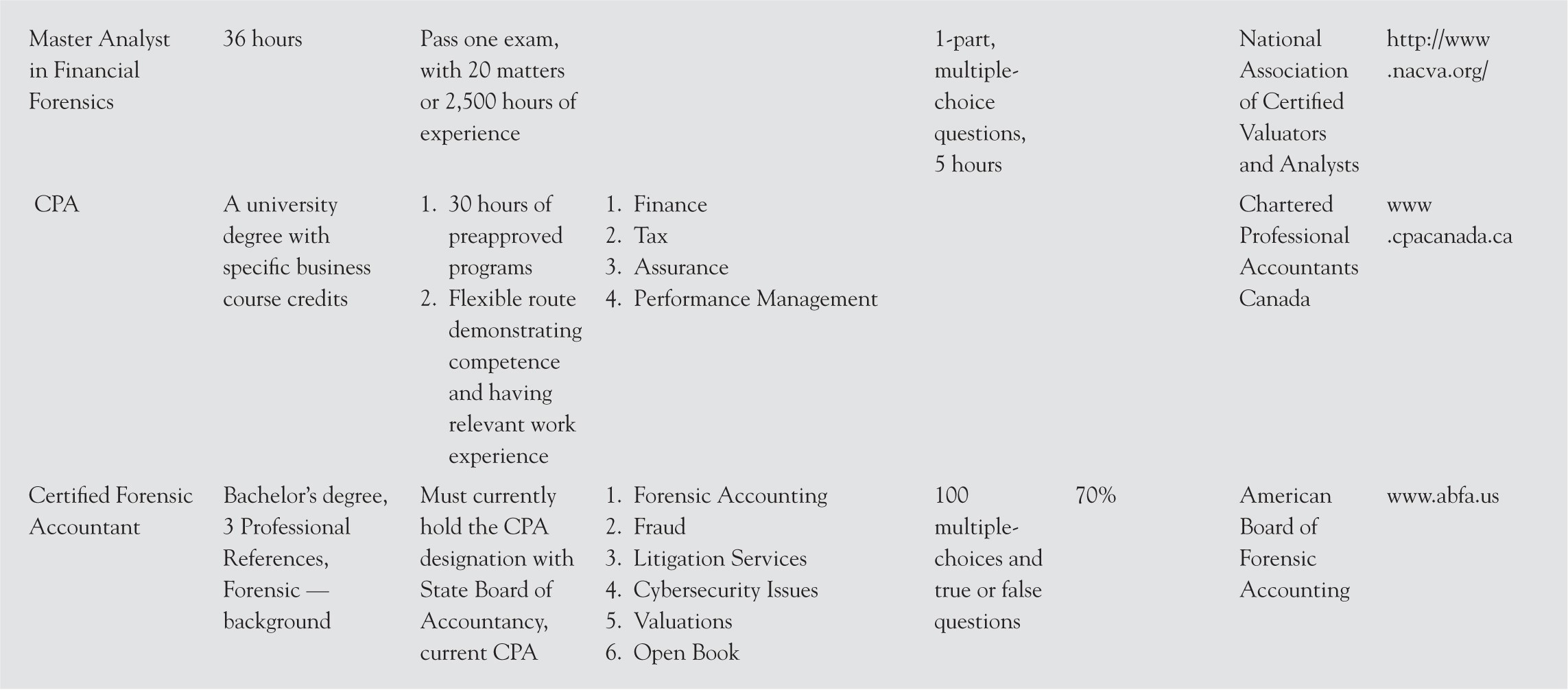

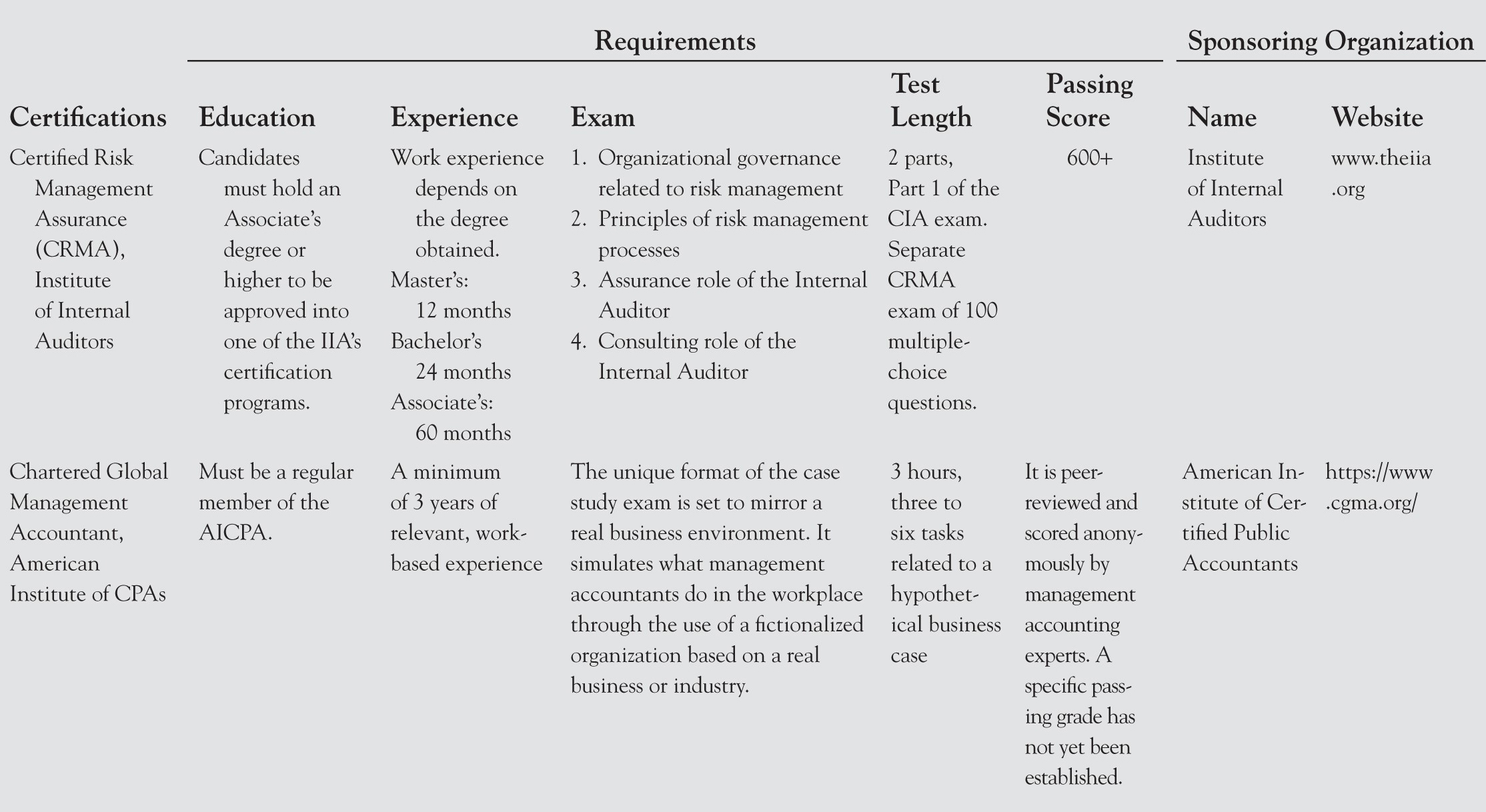

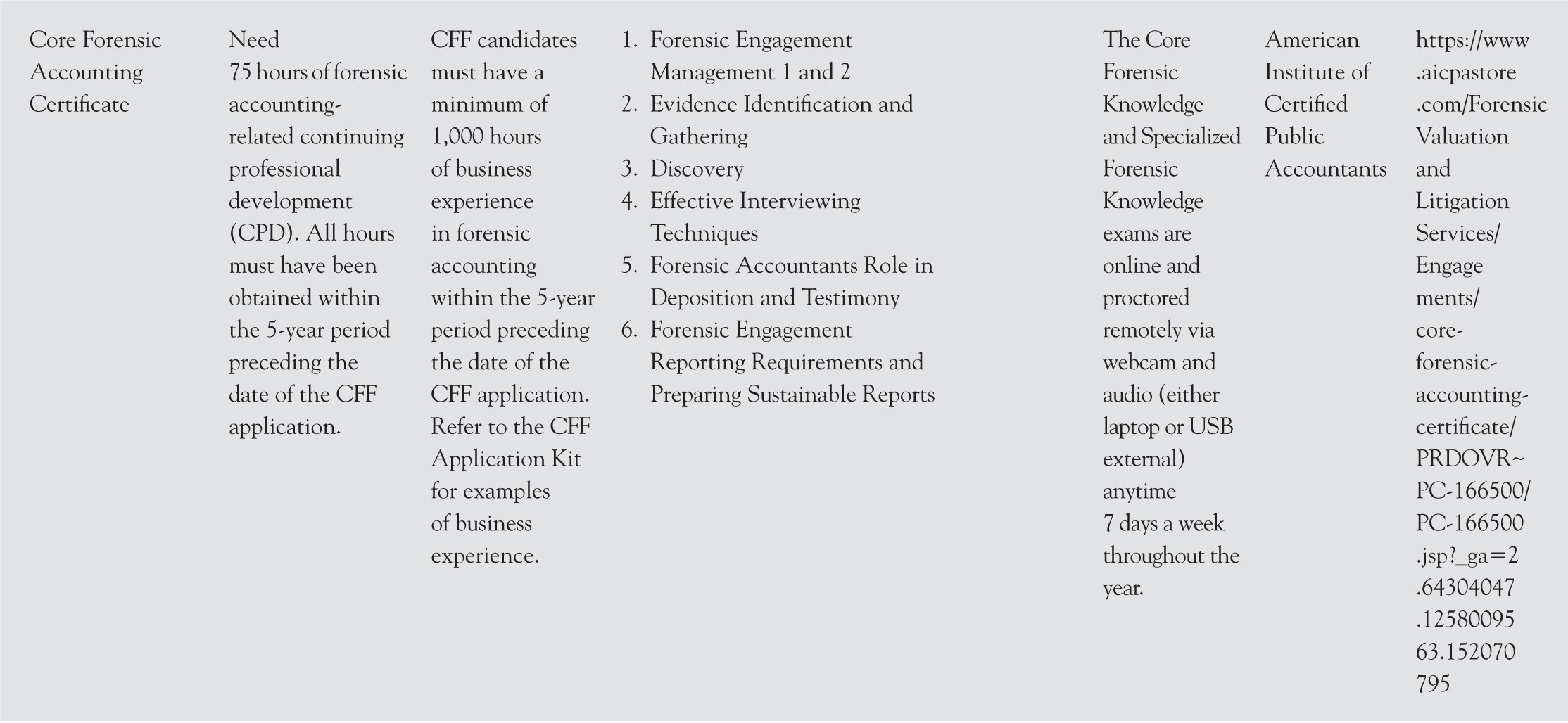

Professional Certifications in Forensic Accounting and Investigative Practices

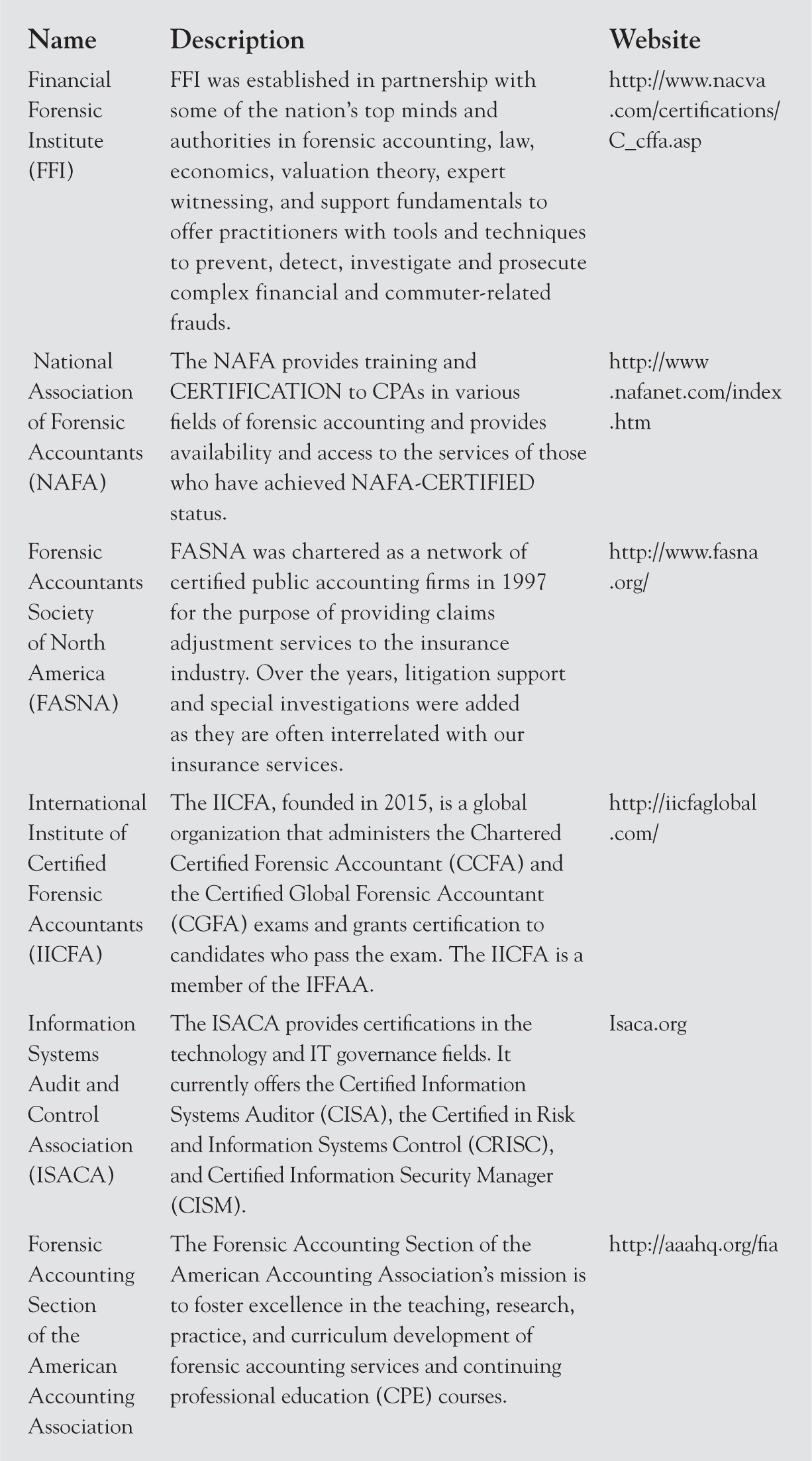

Every profession has its certification of competency, compliance, and ethical conduct. Exhibit 3.2 presents several certifications relevant to practice of forensic accounting and investigative-related services. Exhibit 3.2 contains a list of many of the premier certifications, and while not all-inclusive, it is extensive. Academics, students, and practitioners often ask about the value of professional certifications in general and their importance to them. The accounting profession worldwide has evolved, adapted over time to many factors, and has been shaped by a variety of internal and external influences. One of the most influential factors contributing to the professionalism and refinement of the accounting profession is the certification program.

This list is not all-inclusive; there are other certifications in accounting.

This section provides evidence of the value of professional certifications in general and forensic-related certifications to encourage practicing forensic accountants and candidates to obtain their certification in different fields of accounting and auditing. Being in forensic accounting without being certified does not mean a whole lot. There are several forensic-related certifications in accounting, with the CPA, typically regarded as the mother of all certifications and the highest mark of designation in the global accounting profession. However, many other certifications such as chartered accountants (CA), certified management accountants (CMA), certified internal auditors (CIA), certified fraud examiners (CFE), and Certified Government Financial Managers (CGFM) may be more relevant to the forensic accounting career in different fields of accounting. The discussion of some on the professional accounting certifications and their education, examination, experience, and CPE requirements are discussed in the following paragraphs.

Education

Education requirements are typically a prerequisite for almost all professional exams and vary across certifications. For example, the AICPA requires 150 semester hours of college education for a candidate to be eligible to take the CPA exam. This is typically 30 semester hours beyond the bachelor’s degree in accounting. These additional 30 semester hours are generally taken at the graduate level in the areas of accounting, auditing, international business, information technology, communication, critical thinking, and ethics. All professional certifications in accounting require a bachelor’s degree in accounting or business with concentration in accounting as part of their education requirements. Education requirements are normally classified into (1) technical skills such as financial accounting, auditing, management accounting, taxes, and statistical courses and (2) soft skills such as courses in critical thinking, corporate governance, ethics, organization behavior, and communication. Almost all professional accounting certifications presented in Exhibit 3.2 require CPE to maintain the certification. CPE requirements are explained in the following section.

Examination

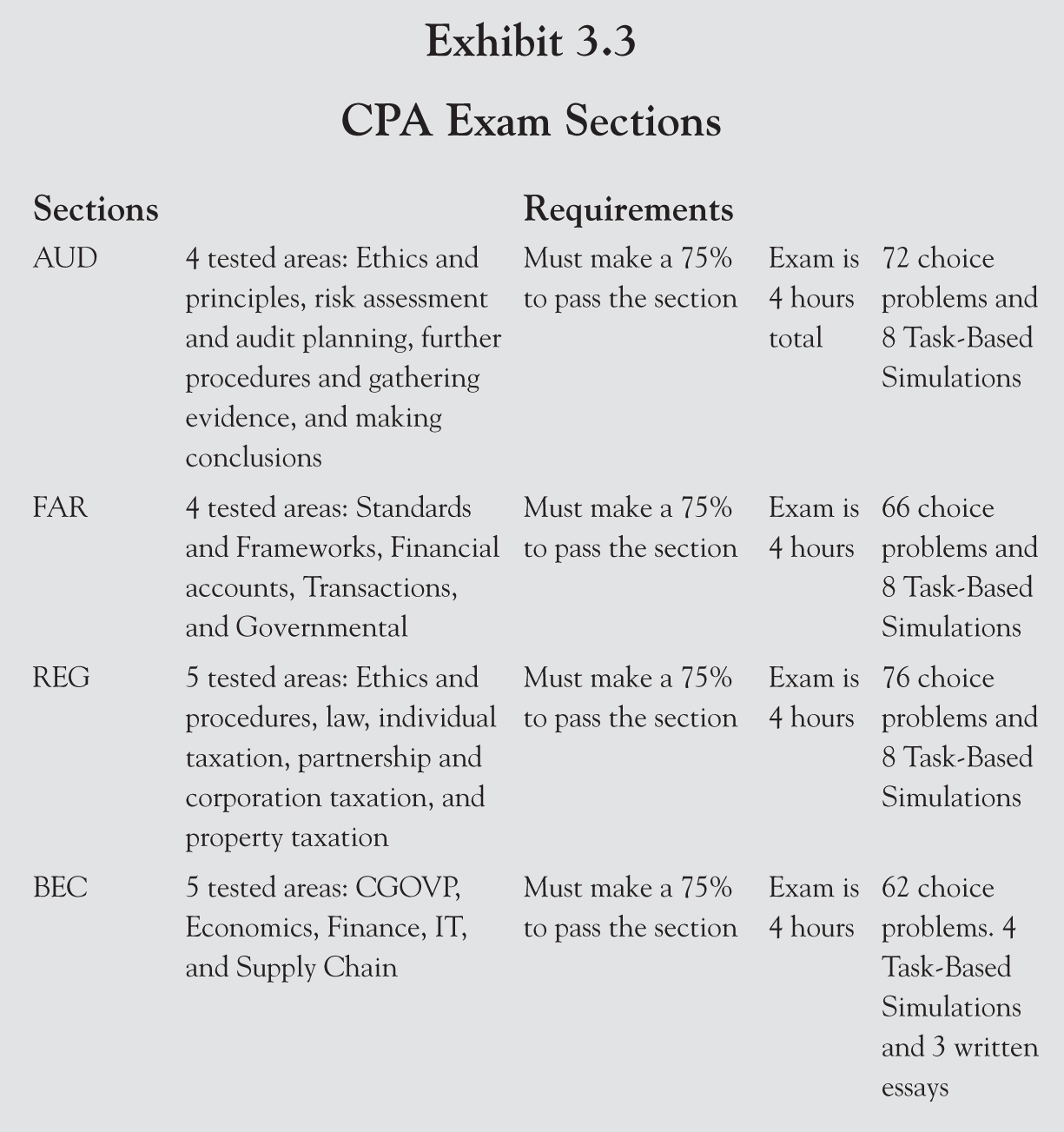

All professional accounting certifications require candidates to take an exam to prove understanding of common body of knowledge in the designated certifications. The content, coverage, and length of the test vary across certifications as indicated in Exhibit 3.3. For example, the AICPA Board of Examiners in administrating the CPA exam currently requires a 14-hour computer-based examination covering auditing, financial reporting, regulation, and business concepts. Certification exams typically consist of: objective questions (multiple-choice), simulation problems, and written questions. The 2018 CPA examination has four parts, FAR (Financial Accounting and Reporting), REG (Regulation), Auditing and Attestation (AUD), and Business Environment and Concepts (BEC). Each section takes 4 hours to complete and a differing number of multiple-choice questions and task-based simulations dependent on the section. Exhibit 3.3 breaks down the sections and explains the requirements for the uniform CPA Examination.

The CPA exam takes a total of 16 hours to complete all four sections in a strictly monitored testing environment. Each section also requires the test taker to make a 75 percent to pass. If this score is not obtained, the individual must retake that section. Once a section is passed, the remaining three sections must be passed within 18 months. After the 18-month period, if all the remaining sections are not passed, the first passed section expires and must be taken again. AUD and FAR have four tested areas and REG and BEC have five tested areas, for total of 18 areas on the examination.4

The Certified Fraud Examiner (CFE) certification requires a bachelor’s degree or its educational equivalent and 2 years of professional experience for certification. The total time of the exam is 10 hours and it comes in four parts across the following subjects:

- Fraudulent transaction

- Legal elements of fraud

- Fraud investigation

- Criminology and ethics

The Certified Internal Auditor (CIA) certification also requires a bachelor’s degree or its educational equivalent. You must have 2 years of internal auditing experience or its equivalent for certification. The total time for the exam is 14 hours. The exam consists of four parts covering the following:

- Internal auditors’ role in corporate governance, risk management, and internal control assessment

- Consulting and advisory activities of internal auditors

- Conducting the internal audit engagement

- Business analysis and information technology

- Business management skills

Experience

Most accounting professional certifications require work experience as either prerequisite for being eligible to take the exam or to become certified. For example, many states that license CPAs to practice accounting require the candidate who has attained the education level and passed the uniform CPA examination to have a certain work experience under supervision of a CPA before obtaining a CPA license to practice accounting. The required work experience is normally between 1 and 2 years. While the AICPA has certain rules, states have varying experience requirements. Texas, for example, requires nonroutine work. This can be considered any work under someone who has a CPA license. Some states, like California, have more strict work experience requirements. It requires candidates to work in audit, tax, or consulting.5 For instance, the Certified Fraud Examiner, Certified Internal Auditor, and Certified Government Financial Manager designations all require 2 years of general professional experience, internal auditing experience, and professional-level experience in government financial management, respectively.

Continuing Professional Education

CPE programs are intended to ensure that practicing accountants keep abreast with developments in their profession. The effectiveness of CPE programs depends on their coverage of emerging issues affecting the accounting profession. The accounting profession has recently been faced with increased scrutiny demanding changes in: business sustainability, corporate governance reforms, possible convergence in both accounting and auditing standards, risk assessment, and electronic accounting and auditing process. To meet these challenges, accountants should keep pace with advances and update their technical and soft skills. One way to obtain, secure, and document the required skills is through the CPE programs.

According to the ACFEs, there are various types of credit across the two classifications of unlimited hours and 10-hour maximum. Participant credit (instruction in an online or formal class), college course credit, in-house training, and self-study credit (one must pass a final exam to receive CPE credit) are of the unlimited variety. This means there is no cap as to how many hours of this variety qualify. Instructor credit (teaching a course), meeting credit, and author credit have 10-hour maximums for each. While still a 10-hour credit, the Fraud Magazine CPE Service is different, in that from any five issues of Fraud Magazine (not older than two years) one may take the quiz listed on the back of each issue. If one passes all five quizzes, one will receive 10 hours of CPE credit.6

The effectiveness of CPE programs depends on their coverage of emerging issues affecting the accounting profession. All accounting professional organizations, including the AICPA, Institute of Management Accountants, and Institute of Internal Auditors, require CPE for their practicing members. The mandatory CPE courses are intended to improve the professional competency and enhance members’ knowledge base, but in many cases, they focus more on compliance than real competency. In summary, prior CPE-related literature suggests that

- management accounting education should address both policy issues regarding ethics and governance, techniques and procedures, and knowledge and skills of management accountants;

- management accounting education should be practical and should include topics that require extensive training in theory including ethics and corporate governance; and

- ethics courses in state CPE programs have grown significantly in recent years.

To maintain their certification and to stay in good standing, practicing accountants should absorb their code of professional conduct and frequently report ethical continuing education and certify compliance with the code of professional conduct. Accountants need to conduct themselves ethically, serve their organizations to the best of their ability, and act in the best interest of their organizations and the public. The AICPA Code of Professional Conduct is applicable and adoptable for all practicing accountants including forensic accountants performing fraud and nonfraud services and provides guidelines and rules in performing their professional responsibilities.7 The purpose of continuing education is to enable accountants to focus on sound education which includes ethics and corporate governance. In addressing accountants’ judgment, one should realize that (1) accountants do not work in isolation, but rather as team players, where their work ethics and behaviors are influenced by the ethics and conduct of coworkers, superiors, and even subordinates within the company; and (2) like other human beings, they can be pressured and motivated when the opportunity is given and thus be tempted to engage in unethical behavior (e.g., manipulation of financial reports). Forensic Accountants should comply with all codes of professional conduct relevant to their practices, including those of the AICPA; the Securities and Exchange Commission (SEC); the Department of Justice (DOJ); the Department of Labor (DOL); the Public Company Accounting Oversight Board (PCAOB); the federal, state, and local taxing authorities; the Associate of Certified Fraud Examiners (ACFE); the Government Accountability Office (GAO); and international, national, and local valuation authorities among others.

Implications for the Accounting Profession and Forensic Accountants

The forensic accounting function can be viewed as a value-added function of producing reliable financial reports that are essential in business decision-making. The auditing profession worldwide has traditionally been regarded as a watchdog of corporate financial reporting and a gatekeeper of the financial reporting process. The sustainability of the accounting profession and forensic accounting depends on the soundness, effectiveness, integrity, and robustness of its credentials and certifications. Best practices of the global accounting profession including certification requirements of education, examination, experience, professional ethics, and CPE, as discussed in this section, are relevant to the accounting profession and forensic accountants and can ensure sustainability of this traditionally respected accounting profession while encouraging the most talented, bright, and ethical college students to join this most rewarding forensic accounting profession. Any inappropriate grandfathering entrance to the forensic accounting profession without meeting and exceeding certification requirements of education, examination, experience, CPE, and ethics will be detrimental to the effectiveness, competency, integrity, and sustainability of the profession.

Conclusion

Several global initiatives have been taken in recent decades to promote forensic accounting. Many professional organizations such as the AICPA, the ACFE among others have developed professional certifications and codes of professional ethics for practicing forensic accountants. These certifications presented in this chapter demonstrate forensic accountants’ commitments and dedications to advance forensic accounting as a distinct profession with demanding and rewarding career. Practicing forensic accountants should obtain certifications relevant to their areas of practice, maintain their CPE, and comply with all applicable rules, regulations, and requirement of certifications as well as related codes of professional ethics presented in this chapter.

Action Items

- Obtain certification relevant to your forensic accounting practice.

- Observe codes of professional ethics relevant to your forensic accounting practice.

- Comply with all applicable laws, rules, and regulations relevant to your forensic accounting practice.

- Maintain CPE to stay in a good standing with requirements of your certifications.

Endnotes

1. American Institute of Certified Public Accountants (AICPA). Statement on Auditing Standards No. 82, Consideration of Fraud in a Financial Statement Audit (New York, NY: AICPA).

2. AICPA. 2002. Consideration of Fraud in a Financial Statement Audit. Statement on Auditing Standards No. 99 (New York, NY: AICP).

3. American Institute of Certified Public Accountants (AICPA). 2018. Exposure Draft: Statement on Standards for Forensic Services No. 1 (SSFS 1). Available at https://www.aicpa.org/interestareas/forensicandvaluation/resources/standards/exposure-draft-statement-on-standards-for-forensic-services.html

4. AICPA. September 30, 2016. Uniform CPA Examination BLUEPRINTS. https://www.aicpa.org/content/dam/aicpa/becomeacpa/cpaexam/examinationcontent/downloadabledocuments/cpa-exam-blueprints-effective-20180101.pdf, (accessed December 1, 2017.).

5. Crush the CPA Exam. 2019. CPA Requirements by State. https://crushthecpaexam.com/cpa-license-requirements/, (accessed September 4, 2018).

6. ACFE. Association of Certified Fraud Examiners—Earning CPE: Types of CPE Credit. https://www.acfe.com/maintaining-cpe-types.aspx, (accessed April 20, 2018).

7. American Institute of Certified Public Accountants (AICPA). 2018. Code of Professional Conduct. https://www.aicpa.org/research/standards/codeofconduct.html