Chapter 7

Project Cost Management

The PMBOK® Guide—Third Edition defines Project Cost Management as “the processes involved in planning, estimating, budgeting, and controlling so that the project can be completed within the approved budget.” Chapter 7 of the PMBOK® Guide—Third Edition describes three processes:

7.1 Cost Estimating

See Section 7.1 of the PMBOK® Guide—Third Edition.

7.2 Cost Budgeting

As stated in the PMBOK® Guide—Third Edition, “Cost budgeting involves aggregating the estimated costs of individual schedule activities or work packages to establish a total cost baseline for measuring project performance.”

7.2.1 Cost Budgeting: Inputs

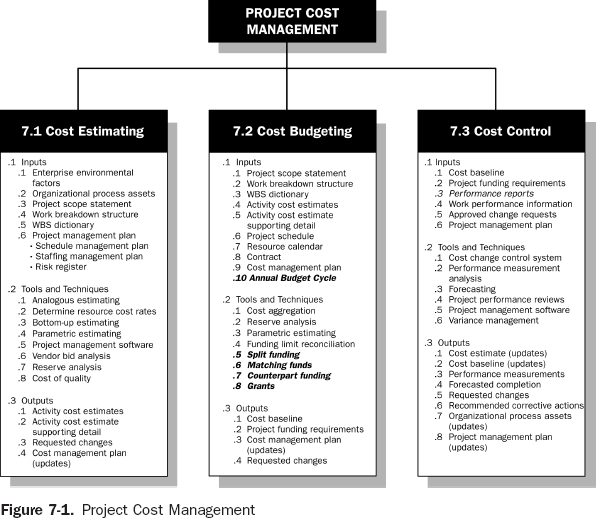

Section 7.2.1 of the PMBOK® Guide—Third Edition discusses nine inputs to Cost Budgeting (See 7.2.1.1 through 7.2.1.9), all of which are used on government projects. There is an additional input used when managing government projects, the “annual budget cycle.”

- .10 Annual Budget Cycle

The annual budget cycle is the unique, and often most difficult, time constraint for government projects. To prevent abuse, the governing body budgets funds for only a limited time. Budgets are typically for one fiscal year at a time. This means that projects and programs may be divided into one-year slices. “Use it or lose it” provisions require funds to be spent by the end of the fiscal year. Project delays can cause the loss of funding if work moves from one fiscal year into the next. Fortunately, funds are generally appropriated to programs rather than individual projects. Effective program managers can often move funds between projects to minimize the overall loss of funding.

7.2.2 Cost Budgeting: Tools and Techniques

The PMBOK® Guide—Third Edition describes four tools and techniques (see 7.2.2.1 through 7.2.2.4). There are five additional tools used in government projects:

- .5 Split Funding

If a single project receives financial contributions from more than one program or fiscal year, it is split-funded. Common methods of split funding include defined elements of work, defined contribution, and percentage split.

Split funding by program. Programs are discussed in Section 1.6 of this standard. Government bodies in large governments generally assign funds to programs rather than to individual projects. They set rules for how the funds are to be divided among individual projects. If the government body budgets by program, each project must be funded from one or more of these programs. It is possible that a single project can contribute to the goals of more than one program. This is particularly common in transportation infrastructure projects. For example, a road-widening project could be combined with pavement rehabilitation, bridge rehabilitation, seismic retrofit, or new signals. These are generally budgeted as separate programs. Similar situations are common whenever new facilities are budgeted separately from rehabilitation. It generally makes sense to have a single contractor perform both the new work and the rehabilitation at a particular location. This minimizes the overhead cost of developing and managing multiple contracts, and it minimizes the disruption to the occupants of the facility.

To the legislative body, defined elements of work is often the preferred method, because each program pays only for the elements that it wants. However, this method requires a detailed manual accounting system, because an automated system can seldom discern which elements are being worked on. Such a manual process is prone to inaccuracy, and requires a large commitment of time for reporting and auditing. The increased cost generally outweighs the slight increase in the accuracy of charges. The defined elements of work method also requires a far more detailed work breakdown structure (WBS) than the other two methods. To capture each program’s portion accurately, the WBS must be defined to a level where each program’s portion maps uniquely to a set of WBS elements. This level of detail is generally far greater than what is needed to manage the project. The defined contribution does not require an amendment to the WBS. Typically, contributions are established as a percentage split. When the limit is reached for the fixed programs, the split is changed to a 100 percent payment by the risk-bearing program. If the project is completed within budget, the change never occurs. Percentage split is the simplest approach and is often the most efficient method. The contribution of each program is estimated at the start of the project. Based on that estimate, each program bears its percentage of the project cost. Since programs fund many projects, variances on one project will probably be counterbalanced by opposite variances on other projects.

Split funding by fiscal year. Split funding by fiscal year is funding allocated over more than one annual budget cycle. (The annual budget cycle is discussed in Section 7.2.1.) If a project begins in one fiscal year and ends in another, it will need funding from the budget of each fiscal year in which there is project work. This split funding by fiscal year can be decreased through obligations, if the government body allows them (see Section 6.4.2.). Funding by fiscal year requires that project managers plan their work by fiscal year with great care. This is particularly true in large governments with many levels of review. In the United States government, for instance, the President submits a budget to Congress in January for the fiscal year that begins in October. Before this, the executive staff must assemble all the supporting data for the budget. Staff must also agree on priorities for the allocation of limited funds. To be included in the January budget, the project manager must have project plans completed by 30 June of the previous year. This is more than fifteen months before the start of the fiscal year. Once a budget request is submitted, changes are difficult to effect. Fortunately, funds are generally appropriated to programs rather than individual projects (see Section 1.6). Program managers can use funds from projects that underrun their fiscal year budgets to fund the overruns in other projects. These are fiscal year variances, not variances in the total cost of the project. Private sector firms could not survive with the government budget process. They must respond quickly to market challenges from their competitors. Without a quick response, they will lose business and may descend into bankruptcy. Large private firms, therefore, delegate the detailed budget decisions to smaller cost centers. The manager of each cost center has clear performance measures: make a profit, satisfy customers so that the firm gets return business, and obey the law. In government, there is no profit motive and customers seldom have the option not to return. Paradoxically, fiscal year funding can have an effect that is opposite to what is intended. Annual budgets are intended to establish limits on the executive. In operational work, annual budgets achieve this goal; in projects, they often fail. For a discussion of operations and projects, see Section 1.2.2 of the PMBOK® Guide—Third Edition.

The executive must request budgets for each project in fiscal year slices. This focus on fiscal years can draw attention away from the overall multiyear cost of the project. The government body may not see this overall cost. Projects can incur large overall cost overruns without the government body becoming aware of this fact. Therefore, government bodies need to be aware of this problem and require multiyear reports. Project managers should provide multiyear reports to their project sponsors. Government accounting standards often fail to recognize the peculiar needs of multiyear projects. Project managers should keep records on the entire project that are reconciled with the government’s official accounts. Some governments have begun to adopt performance-based budgeting as an alternative to the rigid annual budget process. This is discussed in Section 8.1.2.

- .6 Matching Funds

Matching funds are a form of split funding by program (see Section 7.2.2.5). When governments “devolve” project selection to lower government bodies, they often require those lower bodies to pay a portion of the project costs. This ensures that the lower government is committed to the project. Matching funds may be apportioned on a percentage basis or as a defined contribution.

- .7 Obligations

Obligations are tools to minimize the impact of split funding by fiscal year. They can be used only where there is a contractual commitment to fund the project. For more discussion on obligations, see Section 6.5.2.11 of this document.

- .8 Counterpart Funding

This is also called “counterfunding.” This tool involves funding from the private sector, and is an option in “developing” countries, which will not have enough funds for many years to meet all the basic infrastructure needs of their population.

- .9 Grants

Grants are tools used to acquire additional funding for projects. Grant cycles and amounts vary. Grants have required application specifications and deadlines that must be met.

7.2.3 Cost Budgeting: Outputs

See Section 7.2.3 of the PMBOK® Guide—Third Edition.

7.3 Cost Control

See Section 7.3 of the PMBOK® Guide—Third Edition.

7.3.1 Cost Control: Inputs

Section 7.3.1.3 of the PMBOK® Guide—Third Edition identifies performance reports as an input to cost control. Performance reports are also cost control inputs for government projects. These reports are not only internal to the organization, but they provide project performance information to external funding sources. Upon acceptance of the project performance reports, the external funding sources release funds to the project. These reports are distributed to the external stakeholders by the government body.

7.3.2 Cost Control: Tools and Techniques

See Section 7.3.2 of the PMBOK® Guide—Third Edition.

7.3.3 Cost Control: Outputs

See Section 7.3.3 of the PMBOK® Guide—Third Edition.