OVERVIEW

Complex financial instruments are used by companies to manage risk, raise capital, and minimize the cost of capital and taxes. Complex financial instruments include derivatives (such as options and warrants, forwards, and futures) and hybrid/compound instruments (such as convertible debt, debt with detachable warrants, and perpetual debt). The value of a derivative is derived from the value of its underlying primary financial instrument, index, or non-financial item. Hybrid/compound instruments have both debt and equity characteristics, and may have a debt component as well as an equity component. Stock options are often included in employee share-based compensation plans, which are also discussed in this chapter.

STUDY STEPS

Understanding the Underlying Business Arrangements Related to Complex Financial Instruments and Share-Based Compensation Plans

Derivatives

Primary financial instruments include most basic financial assets and financial liabilities such as accounts receivable, accounts payable, and long-term debt. The value of these instruments is based on their contractual right to receive or obligation to pay cash in the future. In contrast, derivative financial instruments “derive” their value from an underlying primary financial instrument, index, or non-financial item. Derivatives are defined as financial instruments that create rights and obligations that have the effect of transferring, between parties to the instrument, one or more of the financial risks that are inherent in an underlying primary financial instrument. They transfer risks that are inherent in the underlying primary instrument without either party having to hold any investment in the underlying (per CICA Handbook, Part II S. 3856.05 and IAS 39.9). Derivatives have three characteristics:

- Their value changes in response to the underlying instrument.

- They require little or no initial investment.

- They are settled at a future date.

Derivatives include options and warrants, forwards, and futures.

Businesses face many financial risks, including credit risk, liquidity risk, and market risk, which are defined in IFRS as follows:

- “Credit risk is the risk that one party to a financial instrument will cause a financial loss for the other party by failing to discharge (respect) an obligation.”

- “Liquidity risk is the risk that an entity will have difficulty meeting obligations that are associated with financial liabilities …”

- “Market risk is the risk that the fair value or future cash flows of a financial instrument will fluctuate because of changes in market prices.” There are three types of market risk: currency risk, interest rate risk, and other price risk.

Derivatives help companies in many different industries manage risk. For example, a company that has market risk related to its inventory faces the risk that the value of its inventory may change while the company is holding the inventory. To help manage this market risk, the company may enter into a forward contract to sell and deliver a quantity of inventory units on an agreed-upon date at an agreed-upon price, as specified in the forward contract.

Options may be purchased options (purchased by the company which becomes the option holder) or written options (sold by the company to an option holder). An option gives the option holder the right to buy (call) or sell (put) an underlying instrument (called “the underlying”) at a certain price (exercise price) over a certain period (exercise period), regardless of changes in market value of the underlying over the exercise period. An option or right to do something in future is valuable; as a result, an option holder usually pays an upfront fee or premium to purchase an option. For example, an investor may pay a $1 fee for a call option to buy a share of a company (the underlying) for $10 (exercise price) at some time in the exercise period. If the share's market price increases to above $10 (exercise price) at some time in the exercise period, the option is considered “in-the-money” at that time. For example, if the market price of the share goes up to $20, the investor need only pay $10 (exercise price) to acquire the share, and the total cost to the investor would be $11 ($10 exercise price plus $1 option fee) for a share with a market value of $20. If the share's market price decreases to below $10 (exercise price), the option is considered worthless and “out-of-the-money.” However, the investor is not obligated to exercise his or her option to purchase the share for $10 (exercise price) and would only lose $1 (the option fee). Therefore, options allow the option holder to benefit from changes in market value of the underlying instruments, while limiting exposure to loss.

Warrants are similar to options, but are often attached to debt, and may be detachable (sold separately). A company may attach warrants to debt to increase the investor's potential yield on the instrument and “sweeten” the deal, thus allowing the company to pay lower interest on the debt portion of the instrument and manage its liquidity risk.

Forwards are contracts under which both parties commit to perform or do something in the future. Parties in a forward contract may not opt out of their commitment. For example, if one party agrees to buy U.S. $100 in 30 days for $120 cash, and the other party agrees to sell U.S. $100 under those terms, the price and time period are locked in under the forward contract and both parties must honour their commitment regardless of changes in the exchange rate. In this example, both parties are managing currency risk. Forward contracts are usually unique to the parties involved, and are therefore not actively traded.

Futures are standardized forward contracts that are actively traded. Futures contracts also require a deposit of collateral (usually a percentage of the contract's value) to a margin account (similar to a bank account) with the exchange or broker.

Recall that the value of a derivative is derived from the value of its underlying primary instrument, index, or non-financial item. Referring to the examples above, the call option derives its value from the underlying company shares, and the forward contract derives its value from the market price of a U.S. dollar (versus the contract price). Because the value of a derivative is derived from the value of its underlying, a derivative can be used to offset, or hedge, risks associated with an underlying. For example, if a company purchases an investment and would like to offset the risk that the fair value of the investment (the underlying) will decrease, the company may enter into a fair value hedge by, for example, purchasing a put option to sell the investment at a certain price. If the fair value of the investment does in fact decrease, the fair value of the put option would increase. A derivative can also be used to offset risks associated with an underlying series of payments. For example, if a company agrees to make a series of payments to a debt holder at a variable interest rate, and would like to offset the risk that the interest rate will increase, the company may enter into a cash flow hedge by, for example, swapping payments in an interest rate swap. In an interest rate swap, the company would pay a fixed interest rate to a counterparty and receive the variable interest rate from the counterparty, which would be used to pay the variable interest rate payments to its debt holder.

Hybrid/compound instruments

Hybrid/compound instruments have both debt and equity characteristics, and may have a debt component as well as an equity component. The contractual terms and economic substance of hybrid/compound instruments and the conceptual framework definitions of liability and equity must be analyzed to determine proper classification of these instruments as debt, equity, or part debt/part equity. Examples of hybrid/compound instruments include perpetual debt, convertible debt, and debt with detachable warrants.

Perpetual debt is debt with no maturity date but with a steady stream of interest payments. Because perpetual debt represents an obligation to pay interest (a debt-like feature) but has no maturity date (an equity-like feature), it is considered to have both debt and equity characteristics. However, perpetual debt is classified as debt (a liability) because it represents a contractual obligation to pay cash (interest), and is measured at the present value of interest to be paid (in perpetuity).

Convertible debt is debt that carries with it an option for the holder to convert the debt to common shares of the company. Convertible debt allows the holder to limit his or her risk and still participate in the rewards of common share ownership, by receiving stable interest payments that rank in payout priority (over dividends on preferred shares) and having the option to convert to common shares if the value of common shares increases significantly. Convertible debt holders have added security if the convertible debt they hold is secured by company assets. Because convertible debt offers holders greater choice, it is generally more valuable, and allows the issuing company to obtain the related convertible debt financing at a lower interest rate. Because convertible debt has a debt component as well as an equity component (conversion option), it is classified as part debt/part equity.

Share-based compensation

The intent of employee share-based compensation plans is generally to motivate senior employees to improve the company's performance in the long term. Share-based compensation plans also help companies conserve cash because they do not require any cash payment. In fact, if options in a share-based compensation plan are exercised, employees will pay cash into the company upon exercise.

It is important to note that not all employee stock option plans are compensatory (in payment for employee services provided). For example, employee stock option or purchase plans (ESOPs) are usually made available to a wide variety of employees to give them an opportunity to invest in the company. Employees in ESOPs usually pay for their options, either fully or partially, and the company records these options as increases in assets (cash) and shareholders' equity (contributed surplus). In contrast, compensatory stock option plans (CSOPs) are usually made available to senior executives or restricted groups of employees, and are considered part of their remuneration package. Therefore, the fair value of options in CSOPs are recorded as compensation expense, allocated to the periods when the company expects to benefit from the related (employees') services. Determining whether an employee stock option plan is compensatory or not may require professional judgement, and analysis of various factors including option terms (compensatory options tend to have more flexible terms), amount of discount from market price (compensatory options tend to have a larger discount from market price), and eligibility (compensatory options are usually offered only to certain restricted groups of employees).

Share appreciation rights (SARs) plans, sometimes called “phantom” stock plans, reward employees for increases in share price by giving them the right to receive compensation equal to the share appreciation (excess of market price per share at exercise date over a pre-established price) multiplied by a notional number of shares or SARs held. Therefore, SARs plans are always compensatory. Share appreciation may be paid in cash, shares, or a combination of both. SARs plans allow employees to benefit from share appreciation without having to pay cash on the exercise date, and without requiring the company to issue the related shares to the employee. It is expected that if the executive (employee) is more productive and effective, the company will perform better and its share price will increase, causing the value of the executive's SARs to increase. SARs plans are often in effect for a limited time, and employees under SARs plans may exercise their SARs at any time during the pre-established SARs period. The notional number of shares or SARs held may reflect the executive's status in the company. For example, a more senior executive would generally have more notional shares or SARs.

Understanding the Presentation and Measurement Issues Related to Complex Financial Instruments and Share-Based Compensation Plans

Derivatives

In general, derivatives are recognized in financial statements at cost when the company becomes party to the contract, and are subsequently remeasured to fair value with gains and losses through net income. (At subsequent remeasurements, the fair value of the derivative is affected by fair value changes in the underlying.) However, there are some significant exceptions to this general rule, including purchase commitments, derivatives involving the entity's own shares, and hedges accounted for under special optional hedge accounting. See Illustration 16-1 for further discussion.

Hybrid/compound instruments

Consistent with the conceptual framework definition of a liability, a hybrid/compound instrument is classified as debt or part debt/part equity if the instrument represents or includes a contractual obligation to pay cash that the company is required to satisfy. Under IFRS, if the instrument includes a contingent settlement provision where the contingency is outside the control of the issuer, the instrument is classified as a liability. Under ASPE, the instrument would be classified as a liability only if the contingency is highly likely to result in a liability.

Under IFRS, the value of a hybrid/compound instrument that is part debt/part equity is allocated to each component based on the residual value method, with the debt component being valued first (at fair value or present value of future cash flows discounted at the market rate for similar straight debt), and the residual being allocated to the equity component. Under ASPE, the equity component of a hybrid/compound instrument that is part debt/part equity may be measured at $0; or the component that is more easily measurable may be measured first, with the residual being allocated to the other component.

Share-based compensation plans

Because share-based compensation plans are compensatory (in payment for employee services provided), they result in the recording of compensation expense or salaries and wages expense, which must be recognized and measured in the periods in which the employee performs the related services.

Compensatory stock option plans (CSOPs) are recorded at the fair value of the options that are expected to vest (that employees are expected to earn the right to). Fair value is measured at the date the options are granted to employees (grant date), using market prices or an options pricing model. The grant date is therefore the measurement date. No adjustments are made after the grant date in response to increases or decreases in share price. The options pricing model incorporates several input measures as follows:

- The exercise price

- The expected life of the option

- The current market price of the underlying shares

- The volatility of the underlying shares

- The expected dividend during the option life

- The risk-free rate of interest during the option life

The fair value of the options that are expected to vest is allocated over the periods in which the employee performs the related services (service period), which is usually also the vesting period. The vesting period is the time between grant date and vesting date.

Share appreciation rights (SARs) plans give rise to different measurement issues. Under a stock option plan, the employee receives a fixed number of shares upon option exercise. However, under a SARs plan, the employee receives an amount of cash, shares, or a combination of both cash and shares, based on the excess of the market share price at the exercise date over a pre-established price. As a result, total compensation cost is not known until the exercise date. However, for faithfully representative financial reporting, total compensation expense must still be estimated and allocated over the service period. Under IFRS, total compensation expense is estimated using an options pricing model. Under ASPE, total compensation expense is usually estimated as the rights' intrinsic value—the difference between the share's current fair value and the pre-established exercise price, multiplied by the number of SARs outstanding. Estimated total compensation expense is recalculated, based on current information, at the end of each reporting period that the SARs are outstanding. Compensation expense for each interim period is recorded based on the percentage of the total service period that has elapsed, multiplied by updated estimated total compensation expense, minus compensation expense that has already been recognized in previous periods.

TIPS ON CHAPTER TOPICS

- Financial liability is defined as any liability that is a contractual obligation (a) to deliver cash or other financial assets to another entity, or (b) to exchange financial assets or financial liabilities with another entity under conditions that are potentially unfavourable to the entity.

- An equity instrument is a contract that represents a residual interest in the assets of an entity after deducting all of its liabilities.

- A primary financial instrument is an instrument whose value is not derived from the value of another instrument, index, or non-financial item. Most basic financial instruments are primary financial instruments, including accounts receivable, accounts payable, and long-term debt.

- A derivative financial instrument is an instrument whose value is derived from the value of an underlying primary instrument, index, or non-financial item (for example, underlying company shares, market price of the U.S. dollar, market interest rates, or gold). Derivative financial instruments include options and warrants, forwards, and futures.

- Derivative financial instruments are used mainly to help companies hedge against and manage various financial risks, including credit risk, liquidity risk, and market risk (which includes currency risk, interest rate risk, and other price risk). Examples of derivative financial instruments include forward contracts and interest rate swap contracts.

- In general, derivatives are recognized in financial statements at cost when the company becomes party to the contract, and are subsequently remeasured to fair value with gains and losses through net income. However, some significant exceptions to this general rule include purchase commitments, derivatives involving the entity's own shares, and hedges accounted for under special optional hedge accounting. All derivatives are subject to extensive disclosure requirements.

- Purchase commitments are generally considered executory contracts (where neither party has performed or fulfilled its part of the contract). A company with a purchase commitment agrees to take delivery of inventory at an agreed-upon price on an agreed-upon date, as specified in the purchase commitment contract. Purchase commitments technically meet the definition of derivatives. (For example, the value of a purchase commitment changes with the value of the underlying inventory.) However, under ASPE, purchase commitments are not accounted for as derivatives because they are not exchange traded and are therefore difficult to measure. Under IFRS, in general, if the company intends to take delivery of the underlying inventory according to the purchase commitment contract, the purchase commitment is not accounted for as a derivative. A purchase commitment that is not accounted for as a derivative does not affect the company's statement of financial position until the company takes delivery of the underlying inventory.

- An example of a derivative involving the entity's own shares is a purchased call option, which gives the entity the right to buy an amount of the entity's own shares at the exercise price. IFRS states that the cost of the option in this example should be recorded as contra-equity, and not as an investment. If the derivative involving the entity's own shares is a written call option, the entity agrees to issue a fixed number of shares for a fixed amount of cash consideration; these contracts are also generally presented as equity. However, there are some exceptions to this “fixed for fixed” rule. See Illustration 16-1 for further discussion.

- Under IFRS, special optional hedge accounting is discussed in two basic categories: fair value hedges and cash flow hedges. Under ASPE, special optional hedge accounting may only be applied to certain specific types of hedging transactions that also qualify as effective and properly documented hedges. In all, the objective of hedge accounting is to achieve symmetry in, or match, the recording of gains and losses due to changes in fair value of the derivative (the hedging instrument), with the recording of gains and losses due to changes in fair value of the hedged instrument or future transactions. For example, in a fair value hedge, hedge accounting results in the recognition of gains and losses (resulting from remeasurement to fair value) of both the hedge and its hedged instrument through net income, even if the hedged instrument is normally accounted for as fair value through other comprehensive income.

- Hybrid/compound instruments have both debt and equity characteristics, and may have a debt component as well as an equity component. The most common example of a hybrid/compound instrument is convertible debt. Convertible debt is considered part debt/part equity and must be bifurcated (split into its component debt and equity parts).

- Bonds with detachable share warrants are another common example of hybrid/compound financial instruments. The detachable share warrants are separate financial instruments and are treated as written call options. The bonds carry a contractual obligation to pay interest and principal, and represent the liability component.

Accounting for Derivatives

In general, derivatives (including options and warrants, forwards, and futures) are recognized in financial statements at cost when the company becomes party to the contract, and are subsequently remeasured to fair value with gains and losses through net income. (After acquisition, the fair value of the derivative is affected by fair value changes in the underlying.) However, there are some significant exceptions to this general rule:

- Purchase commitments. Purchase commitments are executory contracts (contracts to do something in the future, with no cash or goods exchanged upfront). Most purchase commitments are not accounted for as derivatives, and therefore most purchase commitments do not affect the statement of financial position until the related goods are received. However, under IFRS, if the purchase commitment can be settled on a net cash basis or by transferring other assets (instead of taking delivery of the underlying goods) and if the goods are not expected use (the company does not expect to take delivery of the underlying goods), then the purchase commitment is accounted for as a derivative.

- Derivatives involving the entity's own shares. If the derivative's underlying is the company's own shares, the derivative may not be recorded as either a financial asset or a financial liability, as a normal derivative would be. Under IFRS, if the derivative will be settled by issuing a fixed amount of cash for a fixed number of shares (fixed for fixed), then the derivative should be recorded as either contra-equity or equity. However, IFRS identifies some exceptions to this general “fixed for fixed” rule: (1) if the derivative represents an obligation to pay cash or other assets, it should be recorded as a financial liability, and (2) if the derivative can be settled on a net cash basis or by exchanging shares, unless all possible settlement options result in the instrument being equity, the derivative should be recorded as either a financial asset or a financial liability. ASPE does not give explicit guidelines regarding derivatives involving the entity's own shares; however, if the derivative meets the definition of an asset or liability, it should be recorded as such.

- Hedges accounted for under special optional hedge accounting. Under IFRS, if the derivative is a fair value hedge or a cash flow hedge, it may be accounted for under special optional hedge accounting. Under hedge accounting for fair value hedges, the underlying or hedged item is recognized and measured at fair value with gains and losses through net income, in order to match or offset its fair value hedge (the derivative), which is also recorded at fair value with gains and losses through net income. Under hedge accounting for cash flow hedges, the cash flow hedge (the derivative) is recorded at fair value with gains and losses through other comprehensive income, because changes in value (and resulting gains and losses) related to the cash flow hedge's underlying future variable cash flows are not captured in financial statements. The gains and losses on the derivative that are booked through other comprehensive income may be recycled to net income when the hedged item is booked to net income. Under ASPE, special optional hedge accounting may only be applied to certain specific types of hedging transactions that also qualify as effective and properly documented hedges. In all, the objective of hedge accounting is to achieve symmetry in, or match, the recording of gains and losses due to changes in fair value of the derivative, with the recording of gains and losses due to changes in fair value of the derivative's underlying instrument or future transactions.

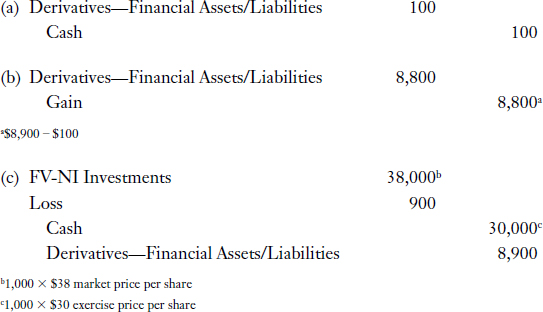

PURPOSE: This exercise will illustrate how to account for purchased call options.

On July 1, 2014, Dalia Corporation paid $100 for a call option to buy 1,000 shares of Base Corporation at an exercise price of $30 per share any time during the next six months. The market price of Base's shares was $25 per share on July 1, 2014. On November 30, 2014, the market price of Base's shares was $38 per share, and the fair value of the option was $8,900.

Instructions

(a) Prepare the journal entry to record the purchase of the call option on July 1, 2014.

(b) Prepare the journal entry(ies) to recognize the change in the call option's fair value as at November 30, 2014.

(c) Prepare the journal entry that would be required if Dalia exercised the call option and took delivery of the shares as soon as the market opened on December 1, 2014.

Solution to Exercise 16-1

EXPLANATION: A call option gives the holder the contractual right to purchase an underlying instrument at a fixed price (the exercise price) within a defined term (the exercise period). In this exercise, Dalia purchased a call option and has the contractual right to purchase 1,000 shares of Base at $30 per share within the exercise period, which ends on December 31, 2014. In general, derivatives (including options and warrants, forwards, and futures) are recognized in financial statements at cost when the company becomes party to the contract, and are subsequently remeasured to fair value with gains and losses through net income.

- The fair value of a call option is based on intrinsic value and time value. Intrinsic value is the difference between the market price of the underlying and the exercise price at any point in time. Time value refers to the option's value over and above its intrinsic value.

- In this exercise, the option is a six-month option and it was exercised at the five-month point. At November 30, 2014, with one month remaining in the exercise period, Dalia may exercise the call option on any date in December 2014. The $8,900 fair value of the option on November 30, 2014, includes its $8,000 intrinsic value [1,000 × ($38 − $30)] and $900 time value, where the $900 time value reflects the possibility that the price of Base shares will continue to increase during the remaining month of the exercise period. Therefore, the loss recorded on December 1, 2014, is a result of the lost time value for the one month that is remaining in the exercise period. Note that the loss recorded on December 1, 2014, may be considered net against the gain recognized the day before, and that the $7,900 net gain on the transaction ($8,800 − $900) is equal to the increase in intrinsic value from the date of purchase of the call option to the exercise date, less the cost of the call option itself [1,000 × ($38 − $30) − $100 = $7,900].

PURPOSE: This exercise will illustrate how to record the issuance of convertible debt and subsequent conversion to common shares.

Wagagoostui Corporation has 300,000 common shares outstanding on January 1, 2014, when it issues convertible bonds. The debt issue is composed of 1,000 bonds at $1,000 face value with a 20-year term and a 10% coupon rate. Each bond is sold at 101 and is convertible into 20 common shares. An underwriter advises Wagagoostui that the bonds would likely have sold for 99 without the conversion feature. The straight-line method is used to amortize any premium or discount, as well as bond issue costs. Wagagoostui prepares financial statements in accordance with ASPE.

Instructions

(a) Record the issuance of the convertible bonds on January 1, 2014.

(b) Record the conversion of 50% of the bonds on January 1, 2016, assuming the book value method is used.

Solution to Exercise 16-2

- Under ASPE, to record the issuance of an instrument with a debt component as well as an equity component, the residual value method may be used, with the more easily measurable component being measured first. In this exercise, similar straight bonds would have sold for 99, which is an estimate of the fair value of the bonds without the conversion feature. Therefore, the debt component (bond payable) is measured first, and the equity component is assigned the residual value.

- Under ASPE, to record the issuance of an instrument with a debt component as well as an equity component, the equity component may instead be measured at $0, in which case, the entire net proceeds of the bond issue would be allocated to debt (in this case, bonds payable).

- A bond discount of $10,000 is included in the above calculation of the initial carrying amount of bonds payable, equal to the $1,000,000 (1,000 × $1,000) maturity value less the $990,000 (1,000 × $1,000 × 99%) fair value of the bonds.

EXPLANATION: The net book value of bonds payable is removed from the accounts and recorded in appropriate shareholders' equity accounts. A proportionate share of contributed surplus is reclassified to common shares. No gain or loss is recorded.

- This method of recording bond conversion is referred to as the book value method and simply removes the net book value of the bonds and the contributed surplus recognized at issuance, and transfers the amounts to appropriate shareholders' equity amounts. No gain or loss is recorded when the book value method is used.

- Recall that book value is synonymous with carrying value and carrying amount.

- Interest, dividends, gains, and losses related to a hybrid/compound instrument are accounted for consistently. For example, if a preferred share is classified as debt because it represents an obligation to pay cash, the preferred share's dividends are recorded as interest or dividend expense (and not directly debited against retained earnings).

PURPOSE: This exercise will illustrate how to account for convertible preferred shares.

Royal Corporation has 1,000 shares of $50 no par value, 6% convertible preferred shares outstanding at December 31, 2014. Each share was issued in a prior year at $54. The preferred shares are convertible into common shares.

Instructions

(a) Record the conversion of 100 preferred shares if one preferred share is convertible into four common shares.

(b) Record the conversion of 100 preferred shares if the conversion ratio is 6:1.

Solution to Exercise 16-3

![]()

If the preferred shares had been $50 par value and a contributed surplus account was used to record the difference between the par value and the $54 issue price, a proportionate amount of the contributed surplus account would also be closed to common shares.

![]()

Note that the journal entry would be the same in both situations. However, financial statements would be updated and would show different numbers of convertible preferred shares and common shares issued under each situation.

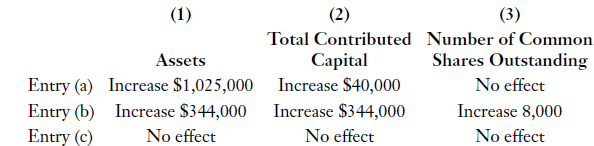

PURPOSE: This exercise will review the accounting procedures for issuance of debt with detachable warrants.

A new issue of 1,000 bonds was sold at 102.5 on January 1, 2014. Each bond had a face amount of $1,000 and one detachable warrant attached. One warrant allows the holder to purchase 10 common shares at $43 per share. Market price per common share was $46 on January 1, 2014. Shortly after issuance of the bonds and warrants, quotes were 98.5 for a bond ex-warrant and $48 for a common share warrant. A few months later, 800 warrants were exercised. Two years later, the remaining 200 warrants expired. The company prepares its financial statements in accordance with IFRS.

Instructions

(a) Record the issuance of the 1,000 bonds with detachable warrants.

(b) Record the exercise of 800 warrants.

(c) Record the expiration of 200 warrants.

(d) Indicate the effect of each of the entries [in parts (a), (b), and (c)] above on (1) assets, (2) contributed capital (paid-in capital), and (3) number of common shares outstanding. State the direction and amount of each effect.

(e) Explain how the journal entry for part (a) would differ if the market value of a bond ex-warrant were unknown.

Solution to Exercise 16-4

EXPLANATION: Under IFRS, for bifurcation of a hybrid/compound instrument that has a debt component as well as an equity component, the residual value method (incremental method) must be used. The debt component is measured first (at fair value or present value of future cash flows discounted at the market rate for similar straight debt), with the remainder of the proceeds allocated to the equity component. In this exercise, the market price for a bond ex-warrant was 98.5, which is an estimate of the fair value of the bonds without the conversion feature, and is used to measure the initial carrying amount of bonds payable. The residual (the difference between total proceeds and initial carrying amount of bonds payable) is allocated to equity.

- A bond discount of $15,000 is included in the initial carrying amount of bonds payable, equal to the $1,000,000 (1,000 × $1,000) maturity value less the $985,000 (1,000 × $1,000 × 98.5%) fair value of the bonds.

- Recall from your study of bonds payable that a bond's price is quoted in terms of a percentage of its par value. Carefully calculate the bond's price; in this exercise, a very common error would be to use $98.50 for the price of one bond rather than the correct price of $985.00 (98.5% of $1,000 face value).

The number of shares obtainable upon exercise of one warrant does not affect the calculations in part (a) (at time of issuance of bonds plus warrants) but it does affect the calculations in part (b) (at time of exercise of the warrants).

(e) If the market value of a bond ex-warrant was unknown, the bond payable would be measured at the present value of interest payments (if any) plus the present value of the bond itself ($1 million) discounted using an effective interest rate applicable to similar straight bonds. The remainder of the proceeds would then be allocated to the warrants.

Accounting for Stock Option Plans Issued to Employees

Before accounting for stock options issued to employees, it is necessary to determine whether the stock options are compensatory (used to compensate employees for their services provided) or non-compensatory (used to give employees an opportunity to invest in the company or to raise capital). Employee stock option plans (ESOPs) are usually fully or partially paid for by employees and considered non-compensatory. Therefore, stock options under ESOPs increase assets (cash) and increase shareholders' equity (contributed surplus and, if options are exercised, common shares). In contrast, compensatory stock option plans (CSOPs) are considered compensatory and in payment for the employee's services provided. Therefore, the fair value of options granted under CSOPs is recognized as an expense (compensation expense) which is allocated to the periods when the company benefits from the employee's services.

Some factors to consider in determining whether or not a stock option plan is compensatory are as follows:

- Option terms—Non-standard terms giving employees a longer time to enrol and the ability to cancel the option would imply that the options are compensatory.

- Discount from market price—A larger discount would imply that the options are compensatory. Note that non-compensatory plans might also offer options at less than fair value, but the discount would be small and represent savings on issue costs.

- Eligibility—Availability only to certain restricted groups of employees (such as executives) would imply that the options are compensatory.

In accounting for stock option plans that are compensatory, the issues usually revolve around recognition and measurement of compensation expense.

The steps in determining compensation expense are as follows:

- Total compensation expense is measured by the fair value method. Using the fair value method, total compensation expense is measured at the fair value of the options that are expected to vest (that employees are expected to earn the right to), at the date the options are granted to employees (or grant date), using market prices or an options pricing model.

- Allocate total compensation expense to one or more periods in which the employees are required to provide services to the company in exchange for the options (often called the service period). The grant or award may specify the service periods, or the service periods may be inferred from the grant terms or from patterns of past grants or awards. Unless otherwise specified, the service period is the vesting period (the time between grant date and vesting date). The vesting date is the date when the employees' right to receive or retain shares or cash under the grant is no longer contingent upon remaining employed by the company.

- The consideration that a corporation receives for shares issued through a CSOP consists of cash or other assets, if any, received from the employees, plus the employees' services provided during the service period.

- Although the measurement date for a stock option plan may be the grant date, it is sometimes later. For example, assume a stock option plan provides for the company's president to obtain 1,000 common shares between January 1, 2014, and January 1, 2016, at a price equal to 20% of the market price at the date of exercise. The measurement date for this plan is the exercise date; the option price is unknown until the exercise date. If the measurement date is later than the grant date, the company should record compensation expense in each period from the grant date to the measurement date based on an estimate of the final number of shares and the option price. This estimate may need to be adjusted in a later period.

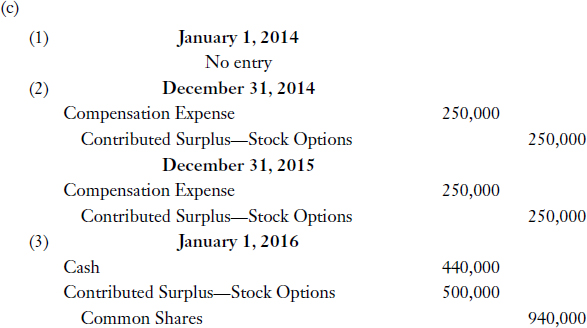

PURPOSE: This exercise will illustrate the application of the fair value method in accounting for a compensatory stock option plan.

Worldwise Corporation granted options for 10,000 common shares to certain executives on January 1, 2014, when the market price was $52 per share. The option price is $44 per share and the options must be exercised between January 1, 2016, and December 31, 2018, after which time they expire. The options state that the related service period is January 1, 2014, to December 31, 2015. An options pricing model determined that, at the date of grant, the estimated fair value of these options was $500,000.

Instructions

(a) Calculate total compensation expense.

(b) Explain when compensation expense should be recognized.

(c) Prepare the journal entries for the following (items 3 and 4 are independent assumptions):

- To record the issuance of the options (grant of options) on January 1, 2014.

- To record the compensation expense, if any. Date the entry(ies). Assume all employees remain employed by Worldwise.

- To record the exercise of the options, assuming all of the options were exercised on the earliest possible date, January 1, 2016.

- To record the expiration of the options, assuming all of the options were not exercised because the market price fell below the exercise price before January 1, 2016, and stayed below the exercise price for the balance of the option period.

Solution to Exercise 16-5

(a) Using the fair value method, total compensation expense is $500,000 (fair value of the options measured at the grant date).

The option price is often called the exercise price.

(b) Compensation expense should be recognized in the periods when the executives perform services for which the options are granted. The service period is either stated or inferred. In this case, the stated service period is from January 1, 2014 (grant date), to December 31, 2015. Thus, compensation expense should be recognized evenly over the two-year service period, equal to $250,000 per year.

When answering exam questions on this subject, use the stated service period if it is clearly indicated. If it is not stated, indicate the period you assume to be the service period. (Choose from grant date to vesting date, from grant date to date the options first become exercisable, or from grant date to date the options expire.) If the question is multiple-choice and you cannot state your assumption, use the amount of time from grant date to date the options first become exercisable as the service period. If your resulting solution does not match one of the answer selections, redo your calculations using the amount of time from grant date to date the options expire as the service period. Your new solution should now match one of the answer selections given.

The entry to record the exercise of these options is not affected by the exercise date. Thus, this same entry would record the exercise if it took place on December 31, 2016. If there is a situation in which the options are exercised prior to the end of the service period (prior to the date that total compensation expense is charged to expense), an unearned compensation cost account is charged. The balance of this Unearned Compensation Cost account is classified as contra shareholders' equity.

The fact that a stock option is not exercised does not mean that compensation expense attributable to the stock option plan should not have been recorded. Therefore, compensation expense is not adjusted upon the expiration of options. However, if a stock option is forfeited because an employee fails to satisfy a service requirement (by leaving the company, for example), compensation expense recorded in the current period should be adjusted (as a change in estimate). This change in estimate would be recorded by debiting Contributed Surplus—Stock Options and crediting Compensation Expense, thereby decreasing compensation expense in the period of forfeiture.

ANALYSIS OF MULTIPLE-CHOICE QUESTIONS

Question

1. Market risk is the risk that the fair value or future cash flows of a financial instrument will fluctuate due to:

EXPLANATION: Market risk is the risk that the fair value or future cash flows of a financial instrument will fluctuate due to a change in foreign exchange rates (currency risk), market interest rates (interest rate risk), and/or other market factors (other price risk). Credit risk is the risk that one of the parties to the contract will fail to fulfill its obligation. Liquidity risk is the risk that the company itself will not be able to fulfill its obligation under the contract. (Solution = c.)

Question

2. An example of a derivative financial instrument is:

- a bond payable.

- a forward contract to buy U.S. currency at a fixed rate in the future.

- an account receivable.

- redeemable/retractable preference shares.

EXPLANATION: Bonds payable, accounts receivable, and redeemable/retractable preference shares are examples of primary financial instruments because their value is not derived from an underlying instrument, index, or non-financial item. A forward contract is a derivative financial instrument because its value is derived from an underlying primary instrument, index, or non-financial item—in this case, the market price of the U.S. dollar (versus the contract price). (Solution = b.)

Question

3. Albert Company has forward contracts to buy U.S. $100,000 at a rate of $1.20 in 180 days. The U.S. exchange rate is currently $1.25 (at the statement of financial position date). Albert Company would show the following on its statement of financial position:

- an asset of U.S. $5,000 (in equivalent Canadian dollars).

- a liability of U.S. $5,000 (in equivalent Canadian dollars).

- a liability of $120,000 (Canadian).

- an asset equal to the fair value of the contract at the statement of financial position date, with an offsetting credit to income.

EXPLANATION: In general, derivatives are recognized in financial statements when the entity becomes party to the contract, and are measured at fair value with gains and losses booked through net income. In this case, as at the statement of financial position date, the forward contract may potentially be settled with favourable terms. Therefore, the forward contract is a financial asset as at the statement of financial position date, and should be measured at fair value, resulting in recognition of a gain on the income statement. (Solution = d.)

There are some significant exceptions to the above-stated general principles in accounting for certain derivatives, including purchase commitments, derivatives involving the entity's own shares, and hedges accounted for under special optional hedge accounting. See Illustration 16-1 for further discussion.

Question

4. On December 1, 2014, Puree Company enters into a purchase commitment to buy apples in two months at an agreed-upon price. Puree intends to take delivery and to use the apples in the production of Delicious Apple Puree, its best-selling product. No cash or product was exchanged when Puree became party to the purchase commitment. However, the terms of the commitment contract state that the contract can be settled on a net basis by paying cash instead of taking delivery of the apples. Puree prepares financial statements in accordance with IFRS. The purchase commitment should be presented on the December 31, 2014 financial statements as:

- a derivative measured at fair value with gains and losses booked through net income.

- a derivative measured at fair value with gains and losses booked through other comprehensive income.

- an executory contract, and therefore not recognized until the apples are delivered.

- a liability measured at fair value.

EXPLANATION: Under IFRS, a purchase commitment contract that has net settlement features (and can be settled on a net basis by paying cash or other assets instead of taking delivery of the underlying product) is not accounted for as a derivative as long as the purchase commitment is expected use (and the company intends to take delivery of the underlying product). In this example, Puree intends to take delivery of and use the apples in its production process; therefore, the purchase commitment should be accounted for as an executory contract and Puree's statement of financial position should not be affected until the apples are delivered (even though the contract has net settlement features). Note that because this purchase commitment contract has net settlement features, if the purchase commitment was not “expected use,” it would generally be accounted for as a derivative and measured at fair value with gains and losses booked through net income. (Solution = c.)

Under ASPE, purchase commitments are generally accounted for as executory contracts (not recognized until the underlying non-financial item is delivered) because they are not exchange traded, and are therefore difficult to measure.

Question

5. Barrie Company has issued written call options, which entitle option holders to buy a fixed number of Barrie shares for a fixed amount of cash. Barrie has no contractual obligation to pay cash or other assets as a result of these call options. Barrie prepares financial statements in accordance with IFRS. The written call options should be presented in Barrie's financial statements as:

- an increase in shareholders' equity.

- a reduction in shareholders' equity.

- a financial asset.

- a financial liability.

EXPLANATION: Under IFRS, a written call option that is settleable using the entity's own shares is presented as an increase in shareholders' equity if the holder has the right to buy a fixed number of the company's shares for a fixed amount of consideration (called the fixed for fixed principle), and there is no contractual obligation to pay cash or other assets. The terms of Barrie's written call options are consistent with the conditions for application of the fixed for fixed principle; therefore, the written call options should be presented in Barrie's financial statements as an increase in shareholders' equity. (Solution = a.)

- In general, if a derivative that is settleable using the entity's own shares also gives rise to a contractual obligation to pay cash or other assets (even if fixed for fixed conditions exist), the fixed for fixed principle is overridden, and the derivative is generally accounted for as a financial liability.

- Under IFRS, a purchased call or put option that is settleable using the entity's own shares is presented as a reduction in shareholders' equity (contra-equity) if the company has the right to buy or sell a fixed number of its own shares for a fixed amount of cash, and there is no contractual obligation to pay cash or other assets.

- Under ASPE, rules surrounding derivatives that are settleable using the entity's own shares are not as specific. In classifying such derivatives, professional judgement is required in applying conceptual framework definitions of “financial asset,” “financial liability,” and “equity.”

Question

6. Which of the following are not considered to be dilutive securities?

- debt that is convertible into preferred shares

- convertible preferred shares

- stock options

- stock warrants

EXPLANATION: A dilutive security is a security that would reduce the book value per common share or earnings per share if it was converted to common shares or exercised to purchase common shares. As such, warrants, options, and convertible preferred shares are dilutive since, if they are issued or converted, there would be more common shares outstanding, and therefore a smaller amount of earnings for each of the remaining groups of common shareholders. (Solution = a.)

Question

7. A corporation issues bonds with detachable warrants. Under IFRS, the amount to be recorded as Contributed Surplus—Stock Warrants is:

- zero.

- calculated as excess of total proceeds over present value of future cash flows or fair value of the bonds.

- equal to the market value of the warrants.

- based on the relative market values of the bonds and detachable warrants.

EXPLANATION: Under IFRS, instruments that have both debt and equity components are required to be bifurcated (split into their debt and equity parts and presented separately in the financial statements) using the residual method with the debt component being measured first (at fair value or present value of future cash flows discounted at the market rate for similar straight debt). Under ASPE, the residual method may be used (with the more easily measurable component being measured first); or the equity component may be measured at $0. (Solution = b.)

Question

8. Goode Corporation issued 1,000 8% convertible bonds with a face value of $1,000 each at a price of 102. An underwriter advised the corporation that without the conversion feature, the bonds could not have been issued at a price above 99. Goode prepares its financial statements in accordance with IFRS. At the date of issuance, the amount to be recorded as contributed surplus attributable to the conversion feature is:

- $0.

- $10,000.

- $20,000.

- $30,000.

EXPLANATION: Recall that under IFRS, instruments that have both debt and equity components are required to be bifurcated (split into their debt and equity parts and presented separately in the financial statements) using the residual method with the debt component being measured first, at fair value or present value of future cash flows discounted at the market rate for similar straight debt. Since the above bonds would have been issued at a discount (99) without the conversion feature, 99 is an estimate of the fair value of the bonds without the conversion feature, and the conversion feature is the reason the bonds were issued at a premium. The journal entry to record issuance would be as follows:

Question

9. To induce conversion, a corporation offers its convertible bondholders a $15,000 cash premium to convert to common shares. Upon conversion, the $15,000 cash premium should be reported as:

- an expense of the current period.

- an unusual loss.

- a direct reduction of shareholders' equity.

- a split between expense (debt retirement cost) and issue cost.

EXPLANATION: When an issuer offers some form of additional consideration (called a “sweetener”) to induce conversion of convertible debt, the consideration is allocated between debt and equity components using the method originally used at the time of issuance (to bifurcate the convertible debt). In most cases, this will be the residual (book value) method, which would require a portion of the consideration to be expensed as a debt retirement cost, with the remainder treated as a capital transaction similar to a redemption cost. (Solution = d.)

Question

10. A corporation issued convertible bonds with a face value of $800,000 at a discount. At a date when the unamortized discount was $70,000, and the Contributed Surplus—Conversion Rights balance was $20,000 (related to these bonds), the bonds were converted to common shares having a market value of $870,000. Using the book value method, the amount of gain or loss to record on conversion is:

- $0.

- $70,000.

- $120,000.

- $670,000.

EXPLANATION: Reconstruct the journal entry to record conversion. The book value of the bonds is removed from the accounts and recorded in the appropriate shareholders' equity accounts. There is never a gain or loss recognized when the book value method is used to record the conversion of bonds to shares. The journal entry is as follows:

Question

11. Which of the following is not a factor in determining whether an employee stock option plan is compensatory or non-compensatory?

- discount from market price of the shares

- time frame for exercising the warrant

- eligibility

- option terms

EXPLANATION: Referring to the factors listed in Illustration 16-2, it is evident that the size of the discount from market price of the shares is a factor (the higher the discount, the more likely it is that the plan is compensatory); eligibility is a factor (if the plan is restricted to a group of employees, such as executives, it is likely compensatory); and finally, the option terms are a factor (non-standard terms indicate that the plan is likely compensatory). (Solution = b.)

Question

12. The cost of a compensatory employee stock option plan (CSOP) is accounted for as follows:

- a capital transaction that is measured at grant date.

- an expense that is measured at grant date.

- an expense that is measured at exercise date.

- none of the above.

EXPLANATION: The cost of a CSOP is measured at the grant date at fair value (which is estimated using market prices or a valuation technique such as an options pricing model), and expensed over the service period. The cost should be expensed over the service period since it is the period when the employee is motivated to work harder as a result of the plan. The service period is normally the period between the grant date and vesting date. Any fluctuations in value of the options during the service period are not accounted for by the company; the employee is considered to be the bearer of this risk. (Solution = b.)

Question

13. Stock options allowing selected executives to acquire 10,000 common shares are granted on January 1, 2014. Market price per share on January 1, 2014, is $22, and the option price is $10. The options are for services to be performed over four years starting from the grant date. The options become exercisable on January 1, 2016, and expire on December 31, 2018. Fair value of the options is determined to be $120,000 at the grant date. The amount of compensation expense related to these options for 2014 is:

- $24,000.

- $30,000.

- $60,000.

- $120,000.

EXPLANATION: (1) Calculate total compensation expense. Total compensation expense is $120,000, or fair value of the options determined at the grant date. (2) Determine the service period, or the span of time over which employees are required to provide services to the company in exchange for the options. In this example, the service period is clearly identified as four years starting from grant date: 2014, 2015, 2016, and 2017. (3) Divide total compensation expense ($120,000) by number of years in the service period (four years) to arrive at $30,000 per year. (Solution = b.)

Question

14. On January 1, 2014, Chandler, Inc. granted stock options to officers and key employees for the purchase of 1,000 common shares at $20 per share as additional compensation for their services to be provided over the next two years. The options are exercisable during a four-year period beginning January 1, 2016, by grantees still employed by Chandler. The fair value of the options determined at the grant date is $6,000. Market price per common share was $26 at the grant date. The journal entry to record compensation expense related to these options for 2014 would include a credit to Contributed Surplus—Stock Options for:

- $20,000.

- $6,000.

- $3,000.

- $1,000.

EXPLANATION: Reconstruct the journal entry to record compensation expense for 2014:

![]()

Total compensation expense is the fair value of the options determined at the grant date, $6,000 in this case. Total compensation expense is allocated to the periods included in the two-year service period ($6,000 ÷ 2 = $3,000 per year). (Solution = c.)

Question

15. A share appreciation rights plan may best be described as:

- an employee compensation plan whereby the employee is entitled to the increase in value of the company's shares without having to actually hold the shares.

- an employee compensation plan whereby the employee is entitled to the increase in value of the company's shares and must also hold the shares.

- an employee compensation plan whereby the employer sets aside shares for employees who are allowed to buy the shares at a fixed price within a pre-specified time period.

- an employee compensation plan whereby the employer sets aside shares in a separate trust for later issue to employees upon exercise of options.

EXPLANATION: The main feature of a share appreciation rights (SARs) plan (or phantom stock option plan) is that the employee is entitled to participate in the increases in value of the company's shares without actually having to buy the shares. (Solution = a.)

Question

16. Thériault-Morin Corporation has $500,000 in long-term debt in Canadian funds at a fixed rate of 7%, with no other long-term debt outstanding. It believes that market interest rates will drop in the next few years. The best way to “manage” or “hedge” this exposure is to:

- lend money at a floating rate.

- pay off the debt immediately.

- enter into a forward contract to buy sufficient U.S. dollars at the maturity date to pay off the debt and perhaps gain on the exchange.

- enter into an interest rate swap contract with a party that has floating rate debt and believes that interest rates will go up.

EXPLANATION: While it is usually best to pay off debt, it is presumed that the company is unable to do this. This presumption would also exclude the possibility of lending money at a floating interest rate. The most common method of managing interest rate risk is to enter into an interest rate swap contract. Recall that any company that has long-term debt will be exposed to interest rate risk. Those with fixed rate debt face the risk that market interest rates will go down, and those with floating rate debt face the risk that market interest rates will go up. (Solution = d.)

Question

17. Using the facts above, assume that Thériault-Morin enters into an interest rate swap contract to pay the equivalent floating (market) rate to another party based on a notional principal of $100,000 for the next three years. Assume that the market interest rate averaged 8% in the first year. The total interest expense that Thériault-Morin will record in the first year is:

- zero (all interest will be recorded when the contract is up and the rates are definite).

- $40,000.

- $35,000.

- $36,000.

EXPLANATION: In an interest rate swap contract, no principal amount is exchanged between the parties. Rather, each party pays the other party's interest rate based on the agreed notional principal. Therefore, Thériault-Morin Corporation pays the market interest rate (instead of its own fixed rate) on $100,000 of its long-term debt, and pays its own fixed rate (7%) on the remainder of its long-term debt. Interest expense totals $36,000: $400,000 × 7% plus $100,000 × 8%. (Solution = d.)

The interest rate swap contract is a derivative because it derives its value from the market interest rate (versus its fixed rate of 7%). Therefore, the contract should be disclosed in financial statements and measured at fair value (which, at the end of the first year, would be approximated by the present value of paying 1% more than it otherwise would have paid, multiplied by the notional principal, over two years).

Question

18. Continuing with the above example, how would the contract be presented on the statement of financial position at the end of the first year?

- The contract would not be presented on the statement of financial position since market interest rates will change frequently over the contract.

- An asset would be presented at fair value.

- A liability would be presented at fair value.

- None of the above.

EXPLANATION: The interest rate swap contract is a derivative and would be recorded on the statement of financial position (in this case, as a liability) at fair value. (Solution = c.)