OVERVIEW

A lease is a contractual agreement between a lessee and a lessor that gives the lessee the right, for a period of time, to use specific property owned by the lessor, in exchange for periodic cash payments. A lease provides a flexible source of financing for the lessee and a source of finance revenue for the lessor. Operating leases, which do not transfer risks and benefits of ownership of the leased property to the lessee, are accounted for as rentals, and result in recording of rent revenue by the lessor and recording of rent expense by the lessee. In contrast, finance leases (called “capital leases” under ASPE), which do transfer risks and benefits of ownership of the leased asset to the lessee, result in recognition of the leased asset and corresponding obligation under capital lease on the statement of financial position of the lessee. From the lessor's perspective, non-operating leases may be sales-type (called “manufacturer” or “dealer leases” under IFRS, and “sales-type leases” under ASPE) or financing-type (called “finance leases” under IFRS, and “direct financing leases” under ASPE). This chapter discusses classification of leases according to criteria as set out by IFRS and ASPE, accounting procedures under each classification from both the lessee perspective and the lessor perspective, the effect of classification of leases on financial statements, and proposed changes to accounting for leases under IFRS.

STUDY STEPS

Understanding the Nature of Leases

A lease is a contractual agreement between a lessee and a lessor that gives the lessee the right, for a period of time, to use specific property owned by the lessor, in exchange for periodic cash payments. Therefore, the lessor gives up use of the leased property over the lease term in exchange for a stream of revenue (cash payments), and the lessee gives up cash payments in exchange for use of the leased property over the lease term.

While legal title of the leased property does not transfer to the lessee in a lease, the economic substance of the transaction is that benefits from use of the leased property do transfer to the lessee, and further analysis is required to determine appropriate accounting treatment.

Classification Approach to Accounting for Leases

At the time of writing, accounting standards required a classification approach to lease accounting, under which the lessee classifies a lease as either a finance lease (called a “capital lease” under ASPE) or an operating lease, and the lessor classifies a lease as either a finance lease (called a “non-operating lease” under ASPE) or an operating lease.

If the lease does not transfer risks and benefits of ownership of the leased property to the lessee, the lease represents a rental arrangement and is an operating lease. For example, if a tenant (lessee) signs a lease to rent a unit in a commercial building for one year, risks and benefits of ownership of the unit do not transfer to the lessee, the lease is an operating lease, and the tenant records the rent portion of lease payments as prepaid rent or rent expense. However, if the lease does transfer risks and benefits of ownership of the leased property to the lessee, the lease represents an in-substance instalment purchase and is a finance (or capital) lease. For example, if a lessee signs a “lease-to-own” lease agreement for a new computer, the risks and benefits of ownership of the computer do transfer to the lessee; therefore, the lease is a finance lease. In a finance lease, the lessor is effectively selling the asset and the lessee is effectively buying the asset, even though legal title often remains with the lessor under the lease contract (at least initially).

Because leases often contain a variety of terms and conditions, it may not be clear whether risks and benefits of ownership are transferred. As such, both IFRS and ASPE outline criteria for classification of a lease as a finance (or capital) lease. Both standards indicate that if any one or a combination of the criteria is met, there is support for classification of the lease as a finance (or capital) lease. For example, if there is reasonable assurance that the lessee will obtain ownership of the leased property by the end of the lease term, the lease is likely a finance lease. Existence of a bargain purchase option (an option for the lessee to purchase the leased asset at a price significantly less than expected fair value at the time the lessee can exercise the option) usually provides reasonable assurance that the lessee will obtain ownership of the leased asset by the end of the lease term, and therefore, reasonable assurance that the lease is a finance lease. A lease agreement may also include a guaranteed residual value (a maximum amount the lessor can require the lessee to pay at the end of the lease). A guaranteed residual value effectively requires the lessee to assume the risk associated with the residual amount of the leased property at the end of the lease.

From a lessor's perspective, the criteria to assess whether a lease is operating or non-operating are the same as the criteria applied by the lessee, with the exception that, under ASPE, two additional revenue-recognition based criteria must also be met in order to classify the lease as non-operating. In effect, ASPE requires that in order for a lessor to classify a lease as non-operating (and therefore remove the asset from its books and recognize revenue related to the sale of the asset), revenue recognition criteria should also be met. In contrast, in an operating lease, the lessor simply records the rent portion of lease payments received as rent revenue, and the leased asset continues to be depreciated on the lessor's books. Non-operating leases are further classified as either sales-type (called manufacturer or dealer leases under IFRS and sales-type leases under ASPE) or financing-type (called finance leases under IFRS and direct financing leases under ASPE).

Becoming Proficient in Related Calculations and Journal Entries

The following discussion covers finance (or capital) leases from the lessee's perspective, and non-operating leases from the lessor's perspective.

Lessee—Finance (or capital) leases

From the lessee's perspective, if economic substance of the lease is such that risks and benefits of ownership of the leased property transfer (and the lessee is effectively purchasing the property), the lease is a finance (or capital) lease, and is accounted for as follows:

Journal Entries

- Record the asset and obligation under capital lease:

Assets under Lease and Obligations under Lease are debited and credited, respectively, by an amount equivalent to present value of minimum lease payments. Note that the accounts in the above journal entry are similar to the accounts in a journal entry to record purchase and financing of a fixed asset:

- Record lease payments:

Each lease payment consists of an interest component and a reduction of lease obligation (principal) component, as broken down in a lease amortization schedule prepared based on the effective interest method.

- Accrue interest on the lease obligation as of the financial statement date:

If the financial statement date falls between lease payment dates, a journal entry is recorded to accrue interest expense incurred up to the financial statement date.

- Record depreciation on the asset under capital lease as of the financial statement date:

If the lessee will retain the asset at the end of the lease term, the depreciable period is the useful life of the asset to the lessee, and the depreciable amount is equal to capitalized asset cost minus estimated residual value (if any) at the end of the asset's useful life to the lessee. Therefore, if the lessee will retain the asset at the end of the lease term, calculation of depreciation is similar to how depreciation would be calculated had the lessee purchased the asset outright.

If the asset will revert to the lessor at the end of the lease term, the depreciable period is the lease term; however, the depreciable amount depends on whether or not the lessee guarantees a residual value. If the lessee does not guarantee a residual value, the depreciable amount is equal to the capitalized asset cost. If the lessee does guarantee a residual value, the depreciable amount is equal to the capitalized asset cost minus undiscounted guaranteed residual value.

Calculations:

The lessee records the asset under capital lease and the corresponding obligation under capital lease at an amount equivalent to present value of minimum lease payments.

Purchased assets are normally recorded at historical cost, as stated on an invoice or other supporting document. However, the value of a leased asset must be calculated, because the lease contract does not include a purchase or sale price. The amount of the leased asset, and therefore the amount of the corresponding lease obligation, is recorded at present value of minimum lease payments, or present value of the minimum payments the lessee will make, or can be required to make, under the terms of the lease. In other words, the present value of minimum lease payments approximates the cash exchange price of purchasing the asset.

Minimum lease payments (used to calculate present value of minimum lease payments) include minimum rental payments (which exclude executory costs), guaranteed residual value (if any), and bargain purchase option amount (if any, assuming that management would exercise the option to purchase the asset at the end of the lease for a bargain price). Note that whether a purchase option is a bargain or not is sometimes a question of professional judgement. In general, a purchase option would be considered a bargain if the option amount is significantly lower than expected fair value of the asset at the time the lessee can exercise the option.

To calculate present value of minimum lease payments, minimum lease payments are discounted to present value. Under IFRS, present value of minimum lease payments is calculated using the rate implicit in the lease, unless it is not reasonably determinable, in which case, present value of minimum lease payments is calculated using the lessee's incremental borrowing rate. Under ASPE, present value of minimum lease payments is calculated using the lower of the rate implicit in the lease and the lessee's incremental borrowing rate. The rate implicit in the lease is the lessor's internal rate of return at the beginning of the lease that makes the present value of minimum lease payments plus any unguaranteed residual value equal to the fair value of the leased asset. It is the rate of return that the lessor needs to receive in order to justify leasing the asset, and is usually based on factors such as the lessee's credit standing, the length of the lease, and the status of the residual value. The lessee's incremental borrowing rate is the interest rate that the lessee would pay on a similar lease.

The lower of present value of minimum lease payments and fair value of the asset is the capitalized cost of the asset, and is included in the lease amortization schedule as the opening lease obligation amount, from which the first reduction of lease obligation (included in the first lease payment) is deducted. The capitalized cost of the asset is also used to calculate the depreciable amount of the asset under capital lease.

Lessor—Sales-type and financing-type leases

From the lessor's perspective, if the economic substance of the lease is such that risks and benefits of ownership of the leased asset transfer (and the lessee is effectively purchasing the asset), the lease is a finance lease (or a non-operating lease under ASPE). Non-operating leases are further classified as either sales-type (called “manufacturer” or “dealer leases” under IFRS and “sales-type leases” under ASPE) or financing-type (called “finance leases” under IFRS and “direct financing leases” under ASPE), and are accounted for as follows:

Journal Entries

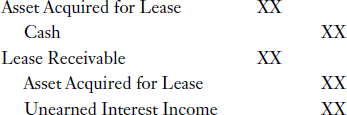

- Record the lease transaction:

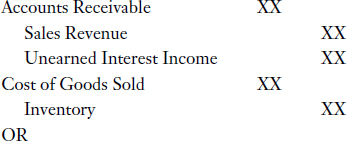

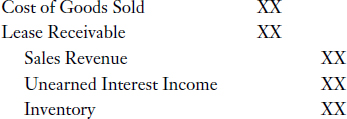

In a sales-type lease, the net investment in the lease and the gross profit on sale of the asset are recorded:

Note that the accounts in the above journal entry are similar to the accounts in the journal entries to record a normal instalment sale of goods:

In a financing-type lease, the asset purchased for lease and net investment in the lease are recorded:

In a financing-type lease, the asset purchased for lease is recorded, and sales revenue and cost of goods sold (and therefore gross profit) are not affected, because the lessor is usually a finance-lease company, or financial intermediary that acquires the specific asset required by the lessee for the purpose of leasing the specific asset to the lessee.

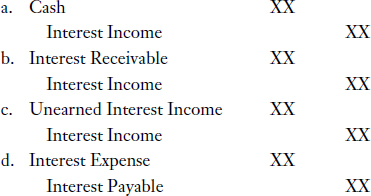

- Record lease payments received:

- Record interest income earned:

Interest income is earned over time based on the net investment in the lease (lease receivable minus unearned interest income) over the life of the lease, and is calculated in a lease amortization schedule prepared based on the effective interest method.

Note that in a non-operating lease (sales-type or financing-type), no depreciation is recorded by the lessor.

Calculations:

In both sales-type and financing-type leases, the lessor records a lease receivable and unearned interest income.

Lease receivable. Lease receivable is calculated as undiscounted rental/lease payments (excluding executory costs) plus any guaranteed or unguaranteed residual value that will accrue to the lessor at the end of the lease or any bargain purchase option. Executory costs are costs related to actual use of the asset (such as insurance, maintenance, and property taxes), and are therefore excluded from the calculation of rental/lease payments. The undiscounted rental/lease payment is the periodic rental/lease payment required to yield the rate implicit in the lease, on the amount to be recovered by the lessor through rental/lease payments. The amount to be recovered by the lessor through rental/lease payments is calculated as:

Investment in asset to be recovered (usually the fair value of the asset plus any initial direct lease costs if the lease is not a sales-type lease)

Minus present value of the amount to be recovered through a bargain purchase option or (guaranteed or unguaranteed) residual value

To calculate the undiscounted rental/lease payment, the amount to be recovered by the lessor through rental/lease payments is divided by an annuity factor reflecting the lease term and the rate implicit in the lease. If the rental/lease payment is made at the beginning of each lease year, an annuity due factor is used. If the rental/lease payment is made at the end of each lease year, an ordinary annuity factor is used.

Unearned finance or interest income. At lease inception, unearned finance or interest income is the difference between lease receivable and fair value of the leased property. Over the life of the lease, unearned interest income is amortized to interest income using the effective interest method, and the rate implicit in the lease.

In sales-type leases, the lessor also records sales revenue and cost of goods sold.

Sales revenue. As a general rule, sales revenue will be the present value of the lease receivable, minus the present value of any unguaranteed residual value.

Cost of goods sold. As a general rule, cost of goods sold will be the laid-down cost of the asset to the lessor, minus the present value of any unguaranteed residual value. Note that inventory is credited for the full amount of laid-down cost to the lessor.

Note that present value of any unguaranteed residual value is excluded from the sales revenue amount and cost of goods sold amount, but included in the lease receivable amount. An unguaranteed residual value cannot be recognized as revenue (or an increase in gross profit) because realization of the amount is not reasonably assured. However, an unguaranteed residual value is included in the lease receivable amount because it is an estimate of the residual value of the asset that will accrue to the lessor at the end of the lease.

Contract-Based Approach to Accounting for Leases

At the time of writing, accounting standards required a classification approach to accounting for leases, under which there are significant differences between accounting for operating and finance (or capital) leases by a lessee, and significant differences between accounting for operating and non-operating leases by a lessor.

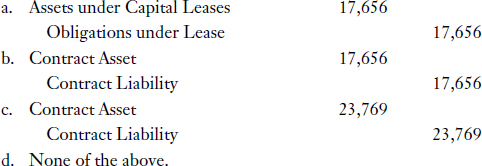

Under IFRS, a contract-based approach to accounting for leases was being proposed, and would apply only to property, plant, and equipment assets. Under this contract-based approach, if control of a leased property or almost all of the risks and benefits of ownership of a leased property transfer to the lessee, the transaction would still be considered an in-substance purchase and sale of the underlying asset (as it would be under current standards). Accounting for the in-substance purchase and sale of the underlying asset would be similar to accounting for a finance (or capital) lease under current standards.

However, under a contract-based approach to accounting for leases, if control of the leased property or almost all of the risks and benefits of ownership of the leased asset do not transfer to the lessee, the lessee is still considered to have the contractual right to use the asset, and therefore, when the contract is signed, the lessee recognizes a contract asset (or contractual lease rights) and a corresponding contract liability (or contractual lease obligation) equal to present value of lease payments. As lease payments are made, the contract liability reduces, and as lease rights are used up (over the term of the lease), the contract asset is amortized. As well, interest expense on the obligation is accrued over the lease term.

The contract-based approach to accounting for leases requires the lessor to take a performance obligation approach to accounting for the lease if control of the leased asset or almost all of the risks and benefits of ownership of the leased asset do not transfer to the lessee. The lessor recognizes a lease receivable and a corresponding performance obligation when the contract is signed, and the asset remains on the lessor's books. As lease payments are received, the lease receivable reduces, and as the performance obligation is satisfied (over the term of the lease), revenue is recognized based on the pattern of the lessee's use of the asset. As well, interest income is accrued over the lease term.

TIPS ON CHAPTER TOPICS

- In accounting for a finance (or capital) lease for a lessee or a non-operating lease for a lessor, consider drawing a timeline and entering all expected cash flows associated with the lease, from the perspective of the party for whom you are preparing journal entries. For a lessee, expected cash flows will be minimum lease payments. For a lessor, expected cash flows will be minimum lease payments plus any unguaranteed residual value that will accrue to the lessor at the end of the lease. A timeline will help to determine the amounts to be discounted for calculation of present value of minimum lease payments.

- Minimum lease payments include the following:

- minimum rental payments (the payments that the lessee will make or can be required to make under the lease agreement, excluding contingent rent and executory costs)

- amounts guaranteed (any amounts guaranteed by the lessee related to the residual value of the leased asset), if any

- bargain purchase option (an option that allows the lessee to acquire the leased asset at the end of the lease term for an amount considerably below the asset's fair value at that time), if any

- penalty for failure to renew, if any

- Under a finance (or capital) lease, the lessee records an asset under capital lease and a corresponding obligation under capital lease at present value of minimum lease payments. However, the amount recorded should not exceed fair value of the asset at lease inception. Under IFRS, present value of minimum lease payments is calculated using the rate implicit in the lease, unless it is not reasonably determinable, in which case, present value of minimum lease payments is calculated using the lessee's incremental borrowing rate is used. Under ASPE, present value of minimum lease payments is calculated using the lower of the rate implicit in the lease, and the lessee's incremental borrowing rate.

- In calculating and recording depreciation of the asset under capital lease, the lessee's determination of depreciable period depends on whether or not the asset will revert to the lessor at the end of the lease term. If the asset will revert to the lessor at the end of the lease term, the depreciable period is the lease term because the lessee will use the asset only for the lease term. If the lessee will retain the asset at the end of the lease term, or if the lease contains a bargain purchase option (and the assumption is that the lessee will exercise the option), the depreciable period is the useful life of the asset to the lessee.

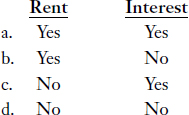

- Under an operating lease, the lessee records rental payments on a straight-line basis over the term of the lease (even if the payments are not payable on a straight-line basis), unless another systematic and rational basis better represents the pattern of the benefits received. Leases involving lease bonuses, scheduled rent increases, or rent-free periods must also conform to this guideline. For example, if a lessee signs a five-year operating lease that includes free rent for the last 10 months of the lease, total rent payments (for 50 months) is divided by 60 months (the entire lease term) to determine monthly rent expense.

- Under an operating lease, the lessor also recognizes rent revenue on a straight-line basis over the term of the lease (regardless of lease provisions), unless another systematic and rational basis better represents the pattern in which the leased asset provides benefits. If cash is not received in a period rent revenue is recognized, a deferral (or an accrual) type adjustment is required.

- The lessor's gross investment in lease is recorded in an account called “Lease Receivable.” Gross investment in lease is defined as undiscounted rental/lease payments (excluding executory costs) plus any guaranteed or unguaranteed residual value that accrues to the lessor at the end of the lease, or any bargain purchase option. Thus, any guaranteed portion of residual value and any remaining unguaranteed portion of residual value that will accrue to the lessor at the end of the lease is included in the lessor's gross investment in lease.

- The lessor records initial direct costs (costs directly associated with negotiating and arranging a specific lease) based on the matching principle. In an operating lease, the lessor defers and allocates initial direct costs over the lease term in proportion to the amount of rent revenue that is recognized. In a financing-type lease, the lessor also defers and allocates initial direct costs over the lease term. In a sales-type lease, initial direct costs are expensed in the year they are incurred (in the year that gross profit is recognized).

- Under a finance (or capital) lease, the lessee's capitalized asset cost and obligation under capital lease is based on the lower of present value of minimum lease payments and fair value of the asset. In contrast, under the proposed contract-based approach to accounting for leases that are not in-substance purchases or sales, the lessee's contract asset (contractual lease rights) and contract liability (contractual lease obligation) are based on a present value, probability-weighted calculation of expected outcomes of rental payments, residual values, and options, and the lease term, which is defined as the longest possible term that is more likely than not to occur.

- Under a financing-type lease, the lessor's lease receivable is based on undiscounted rental/lease payments (excluding executory costs) plus any guaranteed or unguaranteed residual value or any bargain purchase option. In contrast, under the contract-based approach to accounting for leases that are not in-substance purchases or sales, the lessor's lease receivable is based on a present value, probability-weighted calculation of expected outcomes of rental payments, residual values, and options, and the lease term, which is defined as the longest possible term that is more likely than not to occur. The lessor includes in this calculation only amounts that can be reliably measured.

- Under the contract-based approach to accounting for leases, leases that would be considered operating (and accounted for as rental arrangements) under the classification approach to accounting for leases would result in recognition of a contract asset and a corresponding contract liability on the statement of financial position of the lessee, and recognition of a performance obligation on the statement of financial position of the lessor. Therefore, for leases that would otherwise be considered operating under the classification approach, the contract-based approach to accounting for leases would affect the financial statements and ratios of both lessee and lessor significantly.

Classification of Leases

Classification of leases by the lessee

Under the classification approach to accounting for leases, the lessee classifies a lease as either an operating lease or a finance (or capital) lease.

Under IFRS, if the lease meets one or more of the following four criteria, there is support for classification of the lease as a finance lease:

- There is reasonable assurance that the lessee will obtain ownership of the leased property by the end of the lease term. This criterion would be considered satisfied if there is a bargain purchase option in the lease.

- The lease term is for the major part of the economic life of the asset, so that the lessee will receive substantially all of the economic benefits that are expected to be derived from using the leased property over its life.

- The lease allows the lessor to recover substantially all of its investment in the leased property and to earn a return on the investment. This criterion would be considered satisfied if, at lease inception, present value of minimum lease payments (excluding executory costs) is substantially all of the fair value of the leased property.

- The leased property is so specialized that, without major modification, it is of use only to the lessee.

Under ASPE, if the lease meets one or more of the following three criteria, the lessee should account for the lease as a capital lease:

- There is reasonable assurance that the lessee will obtain ownership of the leased property by the end of the lease term. This criterion is considered satisfied if there is a bargain purchase option in the lease.

- The lessee will benefit from most of the property benefits due to the length of the lease term, which is assumed to occur if the lease term is 75% or more of the leased property's economic life.

- The lessor will recover substantially all of its investment in the leased property and earn a return on that investment, which is assumed to occur if, at lease inception, present value of minimum lease payments equals 90% or more of fair value of the leased property.

In summary, under both IFRS and ASPE, if risks and benefits of ownership of the leased property transfer to the lessee, the lease is generally classified as a finance (or capital) lease. IFRS includes one additional identifying characteristic of a finance lease (regarding the specialized nature of the lease property). ASPE criteria include numerical thresholds, which may sometimes take the focus away from applying professional judgement in the classification of leases.

Classification of leases by the lessor

Under the classification approach to accounting for leases, the lessor classifies a lease as either an operating lease or a non-operating (or finance) lease. A non-operating (or finance) lease is further classified as either sales-type (called a “manufacturer” or “dealer lease” under IFRS and a “sales-type lease” under ASPE) or financing-type (called a “finance lease” under IFRS and a “direct financing lease” under ASPE).

Under IFRS, if the lease meets one or more of the four criteria (outlined above) for classification of a lease as a finance lease by the lessee, there is support for classification of the lease as a finance lease by the lessor.

Under ASPE, if the lease meets one or more of the three criteria (outlined above) for classification of a lease as a capital lease by the lessee, and both of the following revenue-recognition based criteria are met, the lessor should account for the lease as a non-operating lease:

- Credit risk associated with collection of lease payments is normal (compared with credit risk associated with collection of similar receivables).

- Amounts of any unreimburseable costs that are likely to be incurred by the lessor under the lease can be reasonably estimated.

If there is a manufacturer's or dealer's profit (or loss) on the transaction, the lease is classified as a sales-type lease. Otherwise, the lease is classified as a financing-type lease. In sales-type leases, the lessor is usually a manufacturer or dealer that entered into the lease agreement as a way of facilitating the sale of the leased property. In contrast, in financing-type leases, the lessor is usually a lease-finance company, or a financial intermediary that acquired the leased property for the specific purpose of earning finance revenue on the lease.

Under ASPE, a lease recorded as a capital lease by the lessee may or may not be recorded as a non-operating lease by the lessor. This is because the lease must meet both additional revenue-recognition based criteria in order for the lessor to record the lease as non-operating. If the lease is recorded as a capital lease by the lessee and recorded as an operating lease by the lessor, both parties would report the leased property on their statements of financial position, and both parties would record depreciation on the leased property.

Steps in Evaluating and Accounting for a Lease Arrangement for a Lessee

| Step 1: | Examine the terms and conditions in the lease agreement. Determine if the lease meets one or more of the criteria for a finance (or capital) lease. (The criteria are listed in Illustration 20-1.) If the lease is a finance (or capital) lease, perform the rest of the steps below. If the lease is not a finance (or capital) lease, account for the lease as an operating lease. |

| Step 2: | Draw the timeline. |

| Step 3: | Calculate present value of minimum lease payments.

|

| Step 4: | Determine cost of the asset under capital lease.

|

| Step 5: | Prepare the lessee's amortization schedule. The beginning obligation under capital lease balance is the amount determined in Step 4. (The interest rate for Step 5 is the rate used in Step 3, unless a new effective interest rate was determined in Step 4.) |

| Step 6: | Prepare journal entries to record the lease on the lessee's books. |

Steps in Evaluating and Accounting for a Lease Arrangement for a Lessor

| Step 1: | Examine the terms and conditions in the lease agreement. Determine if the lease meets one or more of the criteria for a non-operating lease. (The criteria are listed in Illustration 20-1.) If the lease is a non-operating lease, perform the rest of the steps below. If the lease is not a non-operating lease, account for the lease as an operating lease. |

| Step 2: | Determine the undiscounted rental/lease payment required to yield the lessor's desired rate of return on the investment (if the rental/lease payment amount is not given).

To calculate the undiscounted rental/lease payment, the amount to be recovered by the lessor through rental/lease payments is divided by an annuity factor reflecting the lease term and rate implicit in the lease. If the rental/lease payment is made at the beginning of each lease year, an annuity due factor is used. If the rental/lease payment is made at the end of each lease year, an ordinary annuity factor is used. |

| Step 3: | Draw the timeline. |

| Step 4: | Calculate net investment in the lease and unearned finance or interest income.

|

| Step 5: | Prepare the lessor's amortization schedule. Net investment in the lease (calculated in Step 4) is the starting point for this schedule. The lessor's implicit interest rate (the rate implicit in the lease) is used to calculate interest income on net investment in the lease. |

| Step 6: | Prepare journal entries to record the lease on the lessor's books. |

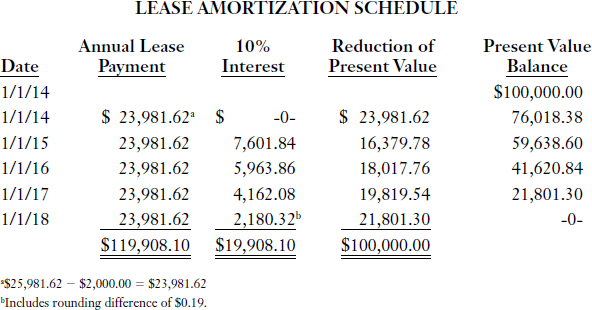

PURPOSE: This exercise illustrates how a lessee and a lessor account for a lease when the lease agreement allows for automatic transfer of title to the leased asset at the end of the lease term.

The following facts pertain to a lease between Sun Bank Leasing (lessor) and JMJ Printers (lessee) for a piece of equipment:

- The lease is for a five-year term, beginning on January 1, 2014. Remaining economic life of the asset is five years.

- The lessor's implicit interest rate is 10%; the lessee's incremental borrowing rate is 10%.

- Fair value of the equipment is $100,000. Cost of the equipment to the lessor is $100,000.

- The annual lease payment is $25,981.62; the first payment is due on January 1, 2014. This amount includes $2,000 for executory costs.

- Title to the equipment automatically transfers to the lessee at the end of the lease term. The asset is expected to have a residual value of $5,000 at the end of its useful life.

- Both the lessee and lessor use the calendar year for their accounting periods and prepare financial statements in accordance with ASPE.

Instructions

(a) Identify the lease type from the standpoint of the (1) lessee and (2) lessor.

(b) Prepare a lease amortization schedule for the lessee and lessor. Explain why they can both use the same schedule in this situation. Also, draw a timeline for the lessor.

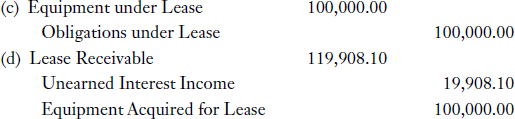

(c) Prepare the journal entry to record the inception of the lease on the lessee's books.

(d) Prepare the journal entry to record the inception of the lease on the lessor's books.

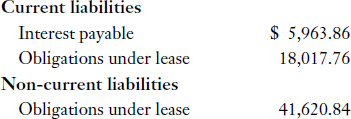

(e) Indicate the amount(s) that will appear on the lessee's December 31, 2015 statement of financial position for this lease. Also indicate the portion that will appear in the current liability section, and the portion that will appear in the non-current liability section. Explain how to determine these amounts.

(f) Indicate the amount(s) that will appear on the lessor's December 31, 2015 statement of financial position for this lease. Also indicate the portion that will appear in the current asset section and the portion that will appear in the non-current asset section. Show the gross investment in lease (lease receivable) and unearned interest components of each net investment amount. Explain how to determine these amounts.

Solution to Exercise 20-1

(a) The lease is a capital lease for the lessee because title to the equipment automatically transfers to the lessee at the end of the lease term. (The lease also meets the two other criteria for a capital lease.) For the lessor, under ASPE, two additional revenue-recognition based criteria must be met in order for the lease to be treated as a non-operating lease. Assuming that credit risk associated with the lease is normal and that the amounts of any unreimbursable costs that are likely to be incurred by the lessor are reasonably estimable, the lessor should record the lease as a non-operating lease. Fair value of the equipment ($100,000) is equivalent to cost of the equipment to the lessor ($100,000); therefore, the lease is a direct financing lease.

(b) Calculations:

$25,981.62 − $2,000.00 executory costs = $23,981.62 annual lease payment (excluding executory costs)

$23,981.62 × present value factor for an annuity due of 1 for n = 5, i = 10% = net investment

$23,981.62 × 4.16986 = $100,000.00 net investment

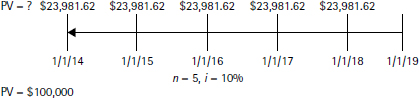

The lessor and the lessee can use the same lease amortization schedule in this situation because they are using the same interest rate to account for the lease (10%), and because there is no unguaranteed residual value that will accrue to the lessor at the end of the lease. For these same reasons, both parties have the same timeline for the lease, which is depicted as follows:

(e) Equipment under Lease will appear in the property, plant, and equipment section of the lessee's statement of financial position (at $100,000). Accumulated depreciation of $38,000 will also appear in that section. To calculate annual depreciation, residual value is deducted from capitalized cost of the equipment under lease to arrive at depreciable amount, and depreciable amount is depreciated over useful life of the asset (because title to the asset will transfer to the lessee at the end of the lease term). Thus, annual depreciation is calculated as ($100,000 − $5,000) ÷ 5 years = $19,000. The amounts that will appear on the lessee's December 31, 2015 statement of financial position under current liabilities and non-current liabilities are as follows:

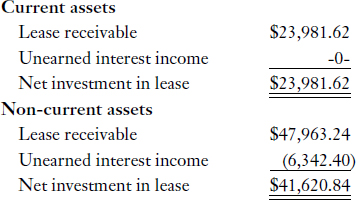

To determine these amounts, refer to the lease amortization schedule. Find the date on the schedule that is relevant to the statement of financial position date (December 31, 2015). If the reporting date is not on the schedule (as is the case here), find the date that most recently precedes the statement of financial position date (January 1, 2015, in this exercise). As of the statement of financial position date, current liabilities include interest payable to date ($5,963.86 due on 1/1/16) and current obligation under lease ($18,017.76 due on 1/1/16), and non-current liabilities include non-current obligation under lease ($19,819.54 + $21,801.30 = $41,620.84).

(f) Net investment in lease at December 31, 2015, is $65,602.46 ($59,638.60 + $5,963.86 = $65,602.46). This will be reflected on the lessor's December 31, 2015 statement of financial position as follows:

To determine these amounts, refer to the lease amortization schedule. Find the date on the schedule that is relevant to the statement of financial position date (December 31, 2015). If the reporting date is not on the schedule (as is the case here), find the date that most recently precedes the statement of financial position date (January 1, 2015, in this exercise). The lease payment on the following line is the amount of gross investment in lease (lease receivable) to be classified as a current asset. The unearned interest portion of that lease payment (as of the statement of financial position date) is deducted to arrive at net investment in lease. In this exercise, no portion of the $5,963.86 interest due on 1/1/16 is unearned as of 12/31/15 because it was all earned during 2015; therefore $0 of unearned interest income is reflected in the current assets section. The total of lease payments (and other receipts) appearing on all subsequent lines of the lease amortization schedule ($23,981.62 + $23,981.62 = $47,963.24) is the amount of gross investment in lease (lease receivable) to be classified as a non-current asset. The unearned interest portion of those lease payments (as of the statement of financial position date) is deducted to arrive at net investment in lease. In this exercise, ($4,162.08 + $2,180.32 = $6,342.40) is deducted from lease receivable to arrive at non-current net investment in lease.

To check the accuracy of the current and non-current portions, the total of current and non-current net investment in lease ($23,981.62 + $41,620.84 = $65,602.46) should equal present value of the lease at the statement of financial position date, which is true in this case. Present value of the lease at the statement of financial position date equals present value balance ($59,638.60) plus any accrued interest earned to the statement of financial position date ($5,963.86).

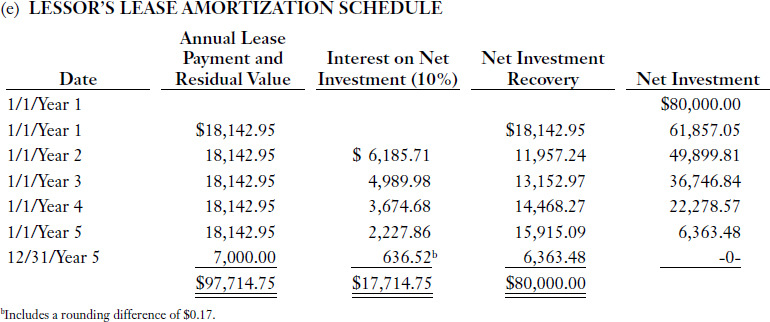

PURPOSE: This exercise is a comprehensive illustration of the accounting procedures for a lease in which the leased asset reverts back to the lessor and still has some value at the end of the lease term. This exercise illustrates (1) how the lessor determines the amount of the periodic lease payment, (2) the lessor's calculations for recording the transactions associated with the lease, (3) the meaning of the terms “gross investment in lease” and “net investment in lease,” (4) the lessee's calculations for recording the transactions associated with the lease, (5) the journal entries on the lessor's books, and (6) the journal entries on the lessee's books.

On January 1, Year 1, Leaseco has a piece of equipment with a cost of $80,000 and a fair value of $80,000. On that date, Leaseco leases the piece of equipment to Rentco for a five-year term at an implicit rate of 10%. The annual lease payment is due at the beginning of each year, and the first payment is due on the lease inception date. The leased equipment will revert back to Leaseco at the end of the lease term; its fair value at that date is estimated to be $7,000. Both Leaseco and Rentco have a calendar-year reporting period, and both companies prepare financial statements in accordance with IFRS. Rentco is aware of Leaseco's implicit rate; Rentco's incremental borrowing rate is 12%.

Instructions

Assuming the lease is a finance lease to the lessee and a finance lease to the lessor:

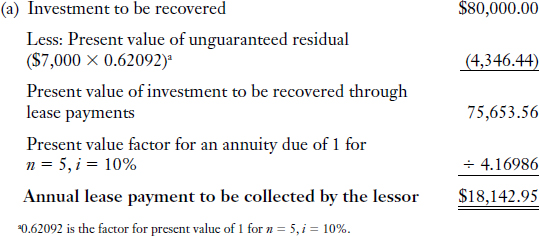

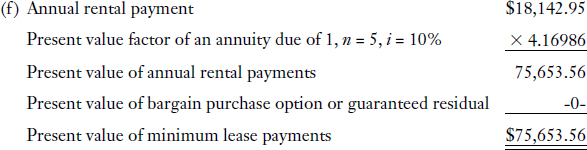

(a) Calculate the amount of the annual lease payment (excluding executory costs) to be collected by the lessor.

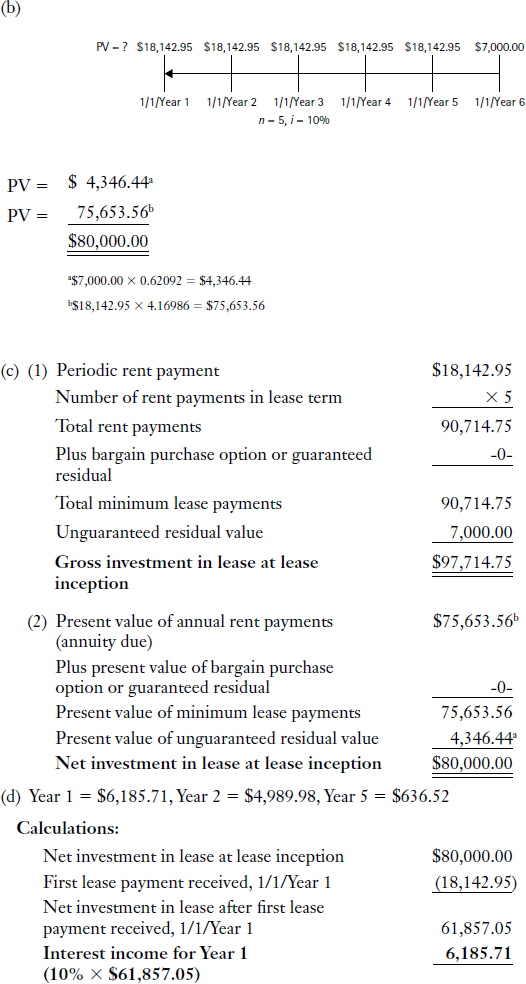

(b) Draw the timeline for the lessor.

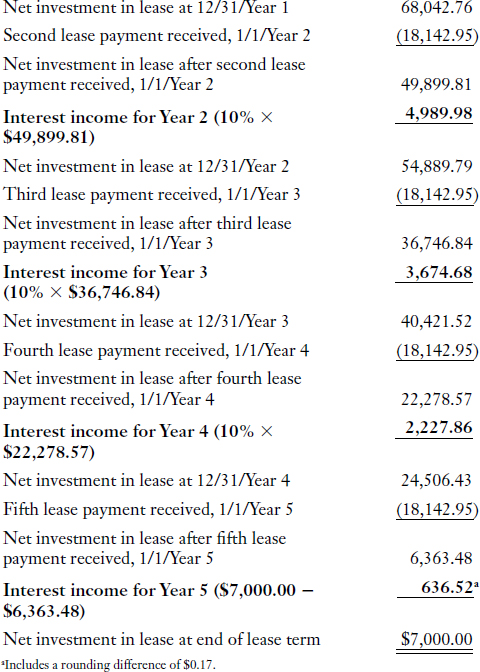

(c) For the lessor, calculate (1) gross investment in lease at lease inception, and (2) net investment in lease at lease inception.

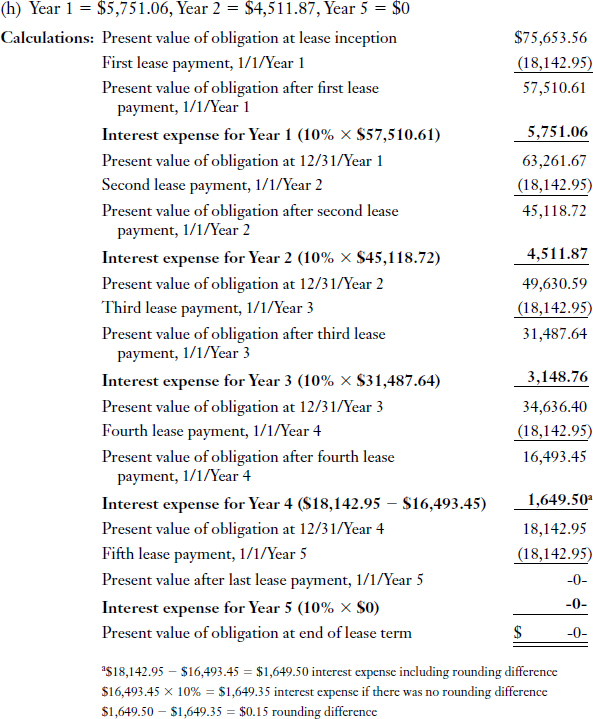

(d) Calculate the amount of interest income to be reported by the lessor for: (1) Year 1, (2) Year 2, and (3) Year 5.

(e) Prepare the lease amortization schedule for the lessor.

(f) Calculate the cost of the lessee's equipment under finance (or capital) lease.

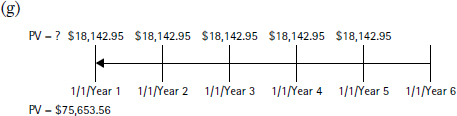

(g) Draw the timeline for the lessee.

(h) Calculate the amount of interest expense to be reported by the lessee for (1) Year 1, (2) Year 2, and (3) Year 5.

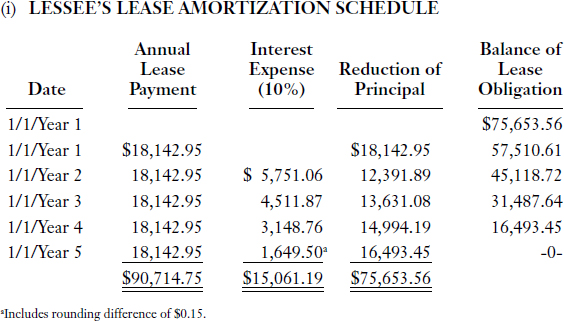

(i) Prepare the lease amortization schedule for the lessee.

(j) Explain why the lessee's lease amortization schedule is different from the lessor's lease amortization schedule. Under what circumstances would the two parties be able to use the same lease amortization schedule?

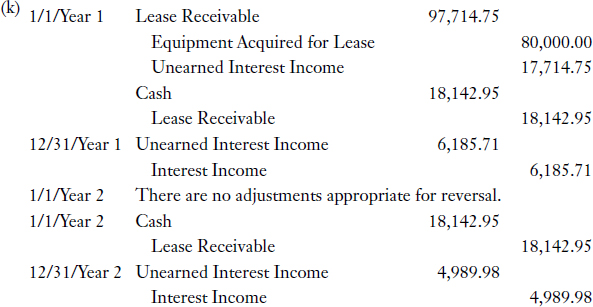

(k) Prepare all of the journal entries for the lessor's books for Years 1 and 2, assuming reversing entries are used.

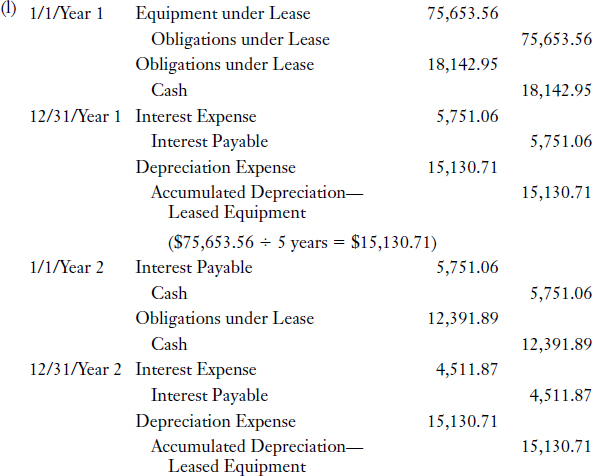

(l) Prepare all of the journal entries for the lessee's books for Years 1 and 2, assuming reversing entries are used.

(m) Compare and contrast the journal entries for the lessee [part (l)] with the journal entries for the lessor [part (k)].

Solution to Exercise 20-2

In this exercise, the lessor's investment is recovered through annual lease payments by the lessee and the equipment's fair value ($7,000) at the end of the lease. Due to the time value of money, today's cash equivalent of $7,000 due in five years is less than $7,000.

- Notice that the interest amount for the last period ($636.52 for Year 5, in this exercise) is a “plug” figure. The difference between the derived amount ($636.52) and the calculated amount of interest ($6,363.48 × 10% = $636.35) is the rounding difference ($636.52 − $636.35 = $0.17).

- Notice that net investment in lease is a present value (discounted) amount.

- Interest income is a function of (a) present value balance, (b) interest rate, and (c) time. As time passes, interest income accrues (due to the time value of money). Interest income increases the present value balance, whereas lease payments decrease the present value balance.

- Notice that there is interest income in Year 5, even though the last lease payment is received at the beginning of Year 5. This is due to the fact that a single sum (unguaranteed residual value, in this exercise) is expected by the lessor at the end of the lease term.

- Interest income included in a lease payment is interest income for the period that occurs prior to the due date of the lease payment. Thus, interest income shown on the 1/1/Year 3 line on the lease amortization schedule is the interest income earned during the Year 2 calendar year.

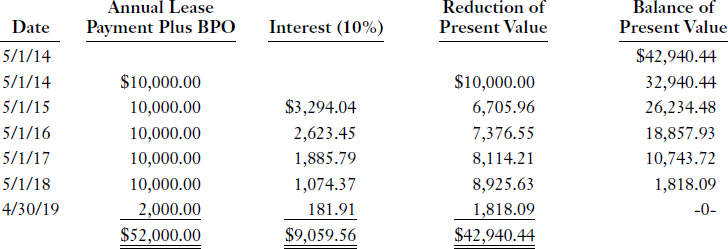

- The amounts on the lessor's lease amortization schedule can be derived by the calculations shown in part (d) above.

- There is no interest income included in the first lease payment received, because the first lease payment is received on the lease inception date and no time has passed during which interest income was earned.

- The rounding difference is always plugged to the interest column on the last line of the lease amortization schedule. If all calculations are performed correctly and are rounded to the nearest cent, the rounding difference will be small—usually less than $10. A larger rounding difference generally indicates that there are errors in the lease amortization schedule. The lease amortization schedule may contain mathematical errors or more serious procedural errors.

- All items that appear on the timeline in part (b) appear in the “Annual Lease Payment and Residual Value” column of the lease amortization schedule.

- On the lease amortization schedule, the total of the “Net Investment Recovery” column is equal to the beginning amount of the “Net Investment” column.

- The total of the “Annual Lease Payment and Residual Value” column is the initial gross investment in lease amount [see solution to part (c)].

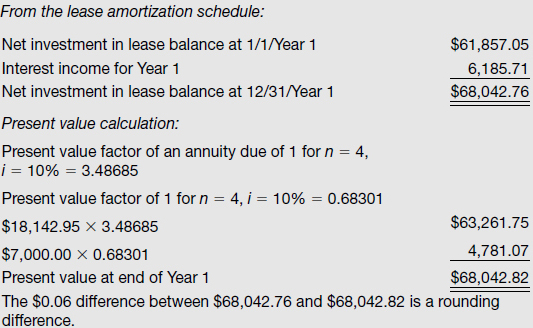

- Notice how the net investment in lease amount at December 31, Year 1, derived from the appropriate numbers on the lease amortization schedule, can be proven by an independent present value calculation as of that date.

- The lessee's cost of the asset under finance (or capital) lease is the lower of the asset's fair value and present value of minimum lease payments. Under IFRS, the interest rate to be used in determining present value of the minimum lease payments is the rate implicit in the lease whenever it can be reasonably determined; otherwise, the lessee's incremental borrowing rate is used. In this exercise, Rentco is aware of the rate implicit in the lease (10%), which is used to calculate present value of minimum lease payments.

- If the leased asset reverts back to the lessor at the end of the lease term and the lessee does not guarantee a residual value, the residual value of the leased asset (if any) does not affect the lessee's calculations. In this exercise, the leased equipment reverts back to Leaseco at the end of the lease term, and Rentco does not guarantee a residual value; therefore, the $7,000 residual value does not affect Rentco's calculations.

In this exercise, the lessee's timeline differs from the lessor's timeline because the lessor expects to have an unguaranteed residual value, which is not relevant to the lessee.

In this situation, there is no interest expense for Year 5 because the obligation is fully paid as of the beginning of the fifth year.

The total of the “Annual Lease Payment” column minus the total of the “Interest Expense” column equals the total of the “Reduction of Principal” column, and the total of the “Reduction of Principal” column equals the obligation's present value at lease inception (the beginning balance of lease obligation).

(j) Even though the lessee and the lessor both use the same interest rate in this exercise, the lessee's lease amortization schedule differs from the lessor's lease amortization schedule because the $7,000 unguaranteed residual value must be included only on the lessor's lease amortization schedule. The lessor and the lessee can use the same lease amortization schedule if they are using the same interest rate and if one of the following conditions exists: (1) an automatic transfer of title at the end of the lease term, or (2) a bargain purchase option, or (3) a residual value guaranteed by the lessee to the lessor, or (4) an unguaranteed residual value for the lessor of zero.

(m) (1) At lease inception, the lessor records the total gross amount to be received in a receivable account (Lease Receivable), whereas the lessee records the total present value amount to be paid in a payable account (Obligations under Lease). Since receivables and payables are generally reported at present value, the lessor sets up a contra receivable account (Unearned Interest Income) to reduce carrying value of the net receivable to present value of all future cash flows associated with the lease.

(2) The lessor accounts for interest as a deferral of income, but the lessee accounts for interest as an accrual of expense. Therefore, the lessor records interest income only at the end of an accounting period, with an adjusting entry. The lessee records interest expense when a lease payment is made and at the end of an accounting period (with an adjusting entry) if the accounting period ends on a date other than a lease payment date. The lessor's adjusting entry to record recognition of interest earned is never reversed; the lessee's adjusting entry to accrue interest expense can be reversed.

(3) The lessor's entry to record a lease payment received is the same each period. (Debit Cash and credit Lease Receivable for the entire lease payment.) The lessee's entry to record a lease payment is different each period because the amount attributed to interest expense and the amount attributed to reduction of lease obligation differ for each lease payment.

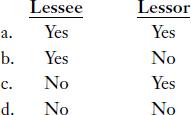

(4) Both the lessor and the lessee record interest, but only the lessee records depreciation in this lease arrangement.

Under IFRS, depreciation for a leased asset is recorded by either the lessee (in a finance lease) or the lessor (in an operating lease). However, under ASPE, if a lease classified as a capital lease by the lessee does not meet both additional revenue-recognition based criteria for recognition as a sales-type lease or a direct financing lease by the lessor, then the lessor classifies the lease as operating, the leased asset is (or remains) capitalized by both the lessee and lessor, and depreciation for the leased asset is recorded by both the lessee and lessor.

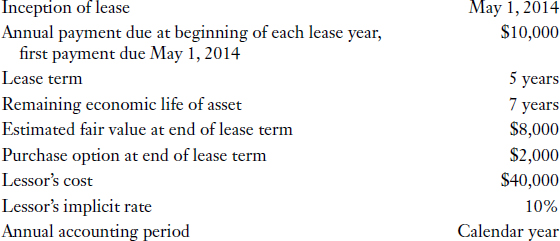

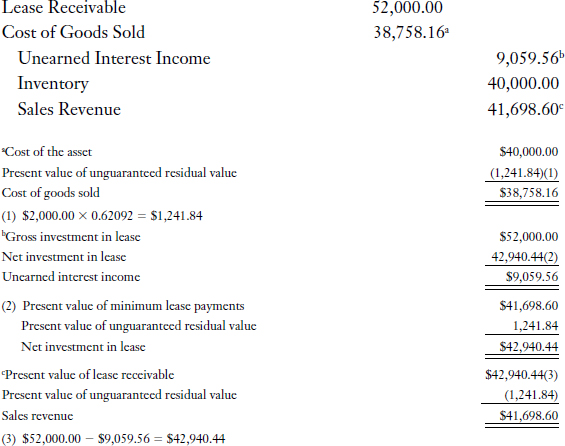

PURPOSE: This exercise provides an example of (1) accounting procedures for a lessor with a sales-type lease, (2) lease periods that do not coincide with accounting periods, and (3) a lease with a purchase option.

The following facts relate to a lease made by the Wormold Company to the Marina Corporation:

Wormold Company prepares financial statements in accordance with IFRS.

Instructions

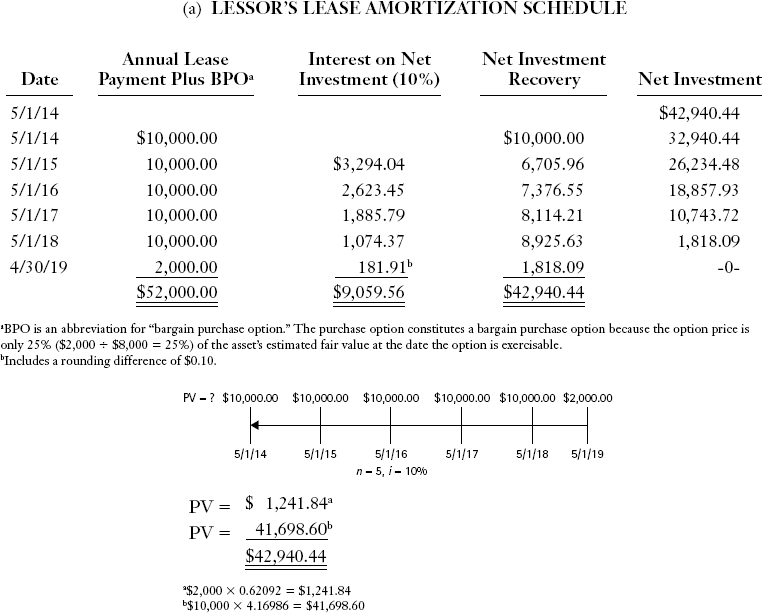

(a) Prepare the lease amortization schedule and draw the timeline for the lessor.

(b) Answer the following questions from the standpoint of the lessor:

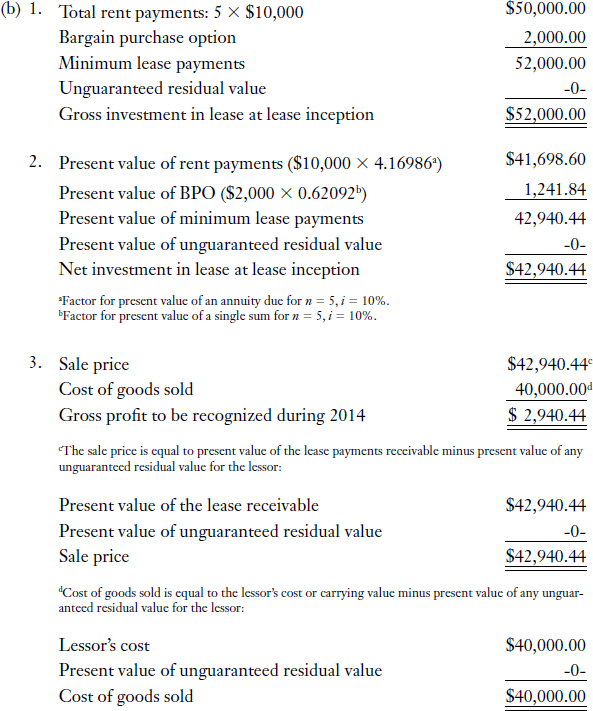

- What is the gross investment in lease at lease inception?

- What is the net investment in lease at lease inception?

- What amount of gross profit should be reported on the income statement for 2014?

- What amount of gross profit should be reported on the income statement for 2015?

- What amount should be reported as interest income on the income statement for 2014?

- What amount should be reported as interest income on the income statement for 2015?

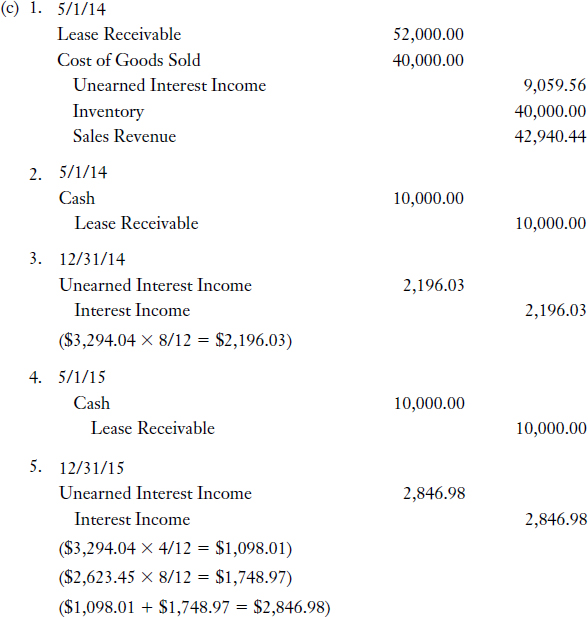

(c) Prepare the following journal entries for the lessor:

- lease inception on May 1, 2014

- lease payment received on May 1, 2014

- adjusting entry at December 31, 2014

- lease payment received on May 1, 2015

- adjusting entry at December 31, 2015

(d) If the lessee has an incremental borrowing rate of 9%, could the lessee use the same lease amortization schedule as the lessor in this situation?

(e) Explain how the entry in part (c) (1) would be different for the lessor if there was no purchase option and if the estimated residual value to the lessor (unguaranteed) at the end of the lease term was $2,000. Also, explain whether or not the lessee could use the same lease amortization schedule as the lessor in this situation.

Solution to Exercise 20-3

4. None. All of the gross profit attributable to a sales-type lease is recognized in the year of lease inception (in this exercise, in the year 2014).

Do not confuse gross profit attributable to a sales-type lease with profit (gain) on sale of an asset attributable to a sale-leaseback transaction, which is generally deferred and amortized. (In a sale-leaseback transaction, the asset is sold and subsequently leased back to the seller by the purchaser.)

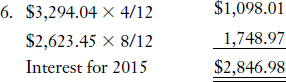

5. $3,294.04 × 8/12 = $2,196.03 interest for 2014

There are eight months between May 1, 2014, and December 31, 2014. Interest income for those eight months is included on the 5/1/15 payment line of the lease amortization schedule. Interest income of $3,294.04 showing on the 5/1/15 payment line is for the 12-month period preceding 5/1/15. Therefore, interest for the last eight months of 2014 is calculated as 8/12 × $3,294.04.

The lease amortization schedule is always prepared using the interest dates (which are dictated by the lease agreement). The interest amount appearing on each payment line is then apportioned to the appropriate accounting period(s). Referring to the lease amortization schedule in part (a), the interest appearing on the 5/1/15 line is the interest for 5/1/14 through 4/30/15. Thus, 8/12 of it belongs on the 2014 income statement and 4/12 of it belongs on the 2015 income statement. Likewise, the $2,623.45 appearing on the 5/1/16 line is the interest for 5/1/15 through 4/30/16. Thus, 8/12 of it is reported on the 2015 income statement.

(d) If the lessee prepares financial statements in accordance with IFRS, the lessee would calculate present value of the lease obligation using the implicit rate because it is reasonably determinable in this exercise. Since the lessee would use the same interest rate as the lessor and there is a bargain purchase option in this lease, the lessee could use the same lease amortization schedule as the lessor. However, if the lessee prepares financial statements in accordance with ASPE, the lessee would use the lower of its incremental borrowing rate and the rate implicit in the lease. If its incremental borrowing rate is 9%, the lessee would calculate present value of the lease obligation and cost of the asset under capital lease using the 9% interest rate, and the lessee would not use the same lease amortization schedule as the lessor.

(e) If there was no bargain purchase option, but there was a $2,000 unguaranteed residual value to the lessor at the end of the lease term, the lessor's journal entry at lease inception would be:

The entry differs from part (c) (1) in that both Sales Revenue and Cost of Goods Sold are reduced by the cash equivalent value of the $2,000 unguaranteed residual value to be received in five years. In effect, a portion of the asset ($2,000) is not considered sold, and the remainder of the asset is considered sold to the lessee.

The lessor's lease amortization schedule would be the same as it appears now in part (a), except that the column heading “Annual Lease Payment Plus BPO” would be changed to “Annual Lease Payment Plus Residual Value.” However, the lessee's lease amortization schedule would differ, even if both parties were using a 10% interest rate. The lessor's lease amortization schedule would include the $2,000 unguaranteed residual value, whereas the lessee's lease amortization schedule would not. The lessee's lease amortization schedule would start with a beginning balance of lease obligation of $41,698.60, rather than $42,940.44.

Residual Value in Non-operating Leases

In accounting for leases, residual value is the estimated value of the leased asset at a future point in time. Residual value may be the estimated value of the asset at the end of the lease term, or at the end of the asset's useful life, depending on which, if either, is relevant to the party for whom you are preparing journal entries.

Residual value of the leased asset at the end of the lease term is included in the lessor's calculation of periodic lease payment if either of the following is true:

- The asset will revert back to the lessor at the end of the lease and the residual value is guaranteed.

- The asset will revert back to the lessor at the end of the lease and the residual value is unguaranteed.

Residual value of the leased asset at the end of the lease term is included in the lessor's calculation of gross investment in lease and net investment in lease if either of the following is true:

- The asset will revert back to the lessor at the end of the lease and the residual value is guaranteed.

- The asset will revert back to the lessor at the end of the lease and the residual value is unguaranteed.

Residual value of the leased asset at the end of the lease term (or any portion thereof) is included in the lessee's calculation of cost of the asset under capital lease and obligation under capital lease, only if the following is true:

- The asset will revert back to the lessor at the end of the lease and the residual value (or any portion thereof) is guaranteed by the lessee.

Guaranteed residual value of the leased asset at the end of the lease term, or residual value at the end of the asset's useful life, is used by the lessee in determining periodic depreciation expense if either of the following is true:

- The asset will revert back to the lessor at the end of the lease and the residual value (or a portion thereof) is guaranteed by the lessee. (Use the guaranteed residual value at the end of the lease term.)

- The asset will transfer to the lessee at the end of the lease term either through an automatic transfer clause or a bargain purchase option. (Use the residual value at the end of the asset's useful life.)

CASE 20-1

PURPOSE: This case reviews the lessee's and lessor's accounting procedures for a lease with a guaranteed residual value.

Instructions

Refer to the facts of Exercise 20-3 above. Assume there is no purchase option at the end of the lease term. Further, assume that the asset reverts back to the lessor at the end of the five-year lease term and that the lessee guarantees the lessor a residual value of $2,000 at that time.

(a) Explain how the lessor's accounting procedures for a lease with a $2,000 guaranteed residual value will differ from the accounting procedures for a lease with a $2,000 bargain purchase option.

(b) Explain how the lessee's accounting procedures for a lease requiring the lessee to guarantee a residual value of $2,000 will differ from the accounting procedures for a lease with a $2,000 bargain purchase option.

Solution to Case 20-1

(a) From the lessor's standpoint, there is no difference in calculations, timeline, or journal entries between a lease with a $2,000 guaranteed residual value and a lease with a $2,000 bargain purchase option. Thus, the Solution to Exercise 20-3, parts (a) through (c), would not change if the lease included a $2,000 guaranteed residual value instead of a $2,000 bargain purchase option (except that “bargain purchase option” or “BPO” would be replaced with “guaranteed residual value” or “GRV”).

(b) From the lessee's standpoint, the timeline, journal entries, and most calculations are the same for a lease with a guaranteed residual value as with a lease with a bargain purchase option. However, there is a major difference in the calculation of depreciation:

- If the lease contains a bargain purchase option, the cost of the asset under capital lease (reduced by any residual value available to the lessee at the end of the asset's useful life) is depreciated over the remaining useful life of the asset because the lessee is assumed to acquire the asset at the end of the lease term.

- If the lease contains a guaranteed residual value, cost of the asset under capital lease reduced by the guaranteed residual value is depreciated over the lease term because the asset will revert to the lessor.

Thus, using the facts from Exercise 20-3, assuming the lessee uses a 10% interest rate to account for the lease and the straight-line depreciation method, annual depreciation expense for the lessee would be as follows:

Assuming a bargain purchase option of $2,000:

Assuming a guaranteed residual value of $2,000:

![]()

If the $2,000 is a guaranteed residual value and the lessee uses the same interest rate as the lessor, the lessee's lease amortization schedule is the same as the lessor's lease amortization schedule.

PURPOSE: This exercise illustrates how to classify receivables and payables related to leases on the statement of financial position.

The following lease amortization schedule is properly being used by both the lessee and lessor. The lease contains a bargain purchase option (BPO). Both the lessee and lessor have a calendar-year reporting period.

Instructions

Fill in the blanks that follow. Show your calculations.

(a) The amount of gross investment in lease to be reported in the current asset section of the lessor's statement of financial position at December 31, 2015, is $_________________.

(b) The amount of net investment in lease to be reported in the current asset section of the lessor's statement of financial position at December 31, 2015, is $_________________.

(c) The amount to be reported in the current liability section of the lessee's statement of financial position at December 31, 2015, by the caption “Interest Payable” is $___________.

(d) The amount to be reported in the current liability section of the lessee's statement of financial position at December 31, 2015, by the caption “Obligations under Capital Leases” is $_____________________.

(e) The amount to be reported in the non-current liability section of the lessee's statement of financial position at December 31, 2015, by the caption “Obligations under Capital Leases” is $_____________________.

Solution to Exercise 20-4

(a) The amount of gross investment in lease to be reported in the current asset section of the lessor's statement of financial position at December 31, 2015, is $10,000.

The most recent payment prior to the statement of financial position date (December 31, 2015) was May 1, 2015. The payment line following that line shows a receipt of $10,000 due on May 1, 2016, which is within one year of the statement of financial position date.

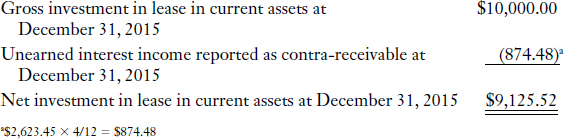

(b) The amount of net investment in lease to be reported in the current asset section of the lessor's statement of financial position at December 31, 2015, is $9,125.52.

The interest portion of the lease payment due to be received on May 1, 2016, is $2,623.45. That amount is for the 12 months that precede May 1, 2016. Thus, at December 31, 2015, four months of the $2,623.45 amount remains unearned.

The net investment reflected in non-current assets (in the non-current investments section) on the lessor's December 31, 2015 statement of financial position would be determined as follows:

(c) The amount to be reported in the current liability section of the lessee's statement of financial position at December 31, 2015, by the caption “Interest Payable” is $1,748.97.

(d) The amount to be reported in the current liability section of the lessee's statement of financial position at December 31, 2015, by the caption “Obligations under Capital Leases” is $7,376.55.

The payment line that follows the statement of financial position date (12/31/15) is 5/1/16. The principal portion of the lease payment due on that date ($7,376.55) represents the current portion of the lessee's obligation under capital lease [excluding any accrued interest calculated in part (c)] at 12/31/15.

- The interest portion of a lease payment is for a period of time, so it is allocated between accounting periods; however, the principal portion of a lease payment falls only in one period and is not allocated between accounting periods. Thus, 8/12 of the $2,623.45 interest on the 5/1/16 payment line is expensed in 2015 and 4/12 of the $2,623.45 interest on the 5/1/16 payment line is expensed in 2016. However, the entire $7,376.55 principal payment appearing on the 5/1/16 lease payment line is due on 5/1/16, and is not allocated between accounting periods.

- In published financial statements, the amount of accrued interest payable [solution to part (c)] is often combined with the current portion of the remaining principal [solution to part (d)] and reported as a single line item in the current liability section.

(e) The amount to be reported in the non-current liability section of the lessee's statement of financial position at December 31, 2015, by the caption “Obligations under Capital Leases” is $18,857.93.

(This figure is the present value balance on the 5/1/16 lease payment line.)

PURPOSE: This exercise reviews the accounting procedures for an operating lease under the classification approach to accounting for leases.

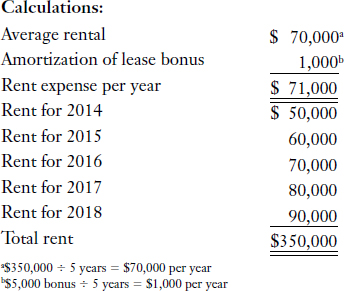

On January 1, 2014, Clarence Corp. leased office space to Montreal Service Corp. The following information applies to the lease:

- The lease is appropriately classified as an operating lease by both the lessee and lessor.

- The lease term is five years.

- The lease payment is $50,000 for 2014 and is scheduled to increase by $10,000 each year.

- Lease payments are due each January 1 and the first one is paid on January 1, 2014.

- The lessee paid a $5,000 bonus payment to the lessor on January 1, 2014, to obtain the lease.

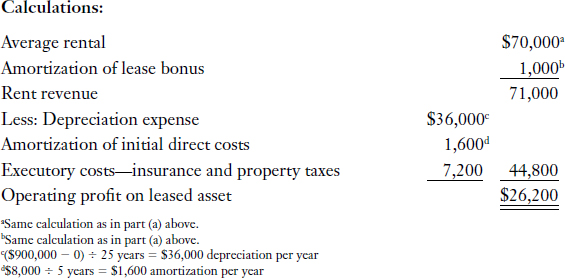

- The lessor's cost of the property is $900,000. The lessor uses straight-line depreciation and estimates that the property has a useful life of 25 years with no residual value.

- The lessor paid an $8,000 finder's fee to a leasing agent for their services.

- Annual insurance and property taxes on the property amount to $7,200 and are paid by the lessor.

Instructions

(a) Calculate rent expense for the lessee for (1) 2014 and (2) 2015.

(b) Calculate the lessor's operating profit (loss) on the leased asset for (1) 2014 and (2) 2015.

Solution to Exercise 20-5

(a) 1. $71,000

2. $71,000

EXPLANATION: Both IFRS and ASPE agree that for an operating lease under the classification approach, minimum lease payments should be expensed by the lessee on a straight-line basis over the lease term, unless another systematic basis better represents the pattern of the benefits received. Thus, the lessee amortizes lease bonus and scheduled rent increases on a straight-line basis over the lease term.

(b) 1. $26,200

2. $26,200

EXPLANATION: Both IFRS and ASPE agree that for an operating lease under the classification approach, an equal (straight-line) amount of rent revenue is recognized in each accounting period regardless of the lease provisions, unless another systematic and rational basis better represents the pattern in which the leased asset provides benefits. Thus, the lessor amortizes the lease bonus and scheduled rent increases on a straight-line basis over the lease term. Initial direct costs paid to independent third parties, such as appraisal fees, finder's fees, commissions, and legal fees, are amortized over the lease term. Executory costs (such as insurance and property taxes) are expensed in the period in which they are incurred.

ANALYSIS OF MULTIPLE-CHOICE QUESTIONS

Question

1. Wells Ltd. leases an airplane from Kitson Corp. under an agreement that meets the criteria for a capital lease for Wells Company. The 10-year lease requires lease payments of $34,000 at the beginning of each year, including $5,000 per year for maintenance, insurance, and taxes. The incremental borrowing rate for the lessee is 15%; the lessor's implicit rate is 12% and is known by the lessee. The present value factor of an annuity due of 1 for 10 years at 15% is 5.77158. The present value factor of an annuity due of 1 for 10 years at 12% is 6.32825. According to ASPE, the lessee should record the leased asset at:

- $29,000 × 5.77158 = $167,376.

- $29,000 × 6.32825 = $183,519.

- $34,000 × 5.77158 = $196,234.

- $34,000 × 6.32825 = $215,161.

EXPLANATION: Think through the steps involved in accounting for a lease for a lessee (see Illustration 20-2). The lessee should record the leased asset at present value of minimum lease payments (excluding executory costs). Under ASPE, present value of minimum lease payments should be calculated using the lower of the lessee's incremental borrowing rate and the rate implicit in the lease. In this example, the annual $5,000 executory cost is deducted from the $34,000 lease payment to arrive at a $29,000 lease payment excluding executory costs. The lessor's implicit rate of 12% is known by the lessee and is lower than the lessee's incremental borrowing rate of 15%; hence, the 12% implicit rate is used to calculate present value of minimum lease payments. Present value of minimum lease payments is calculated by multiplying the lease payment (excluding executory costs) by the factor for present value of an annuity due of 1 for n = 10, i = 12%. There is no indication that the asset's fair value may be lower than the calculated present value of minimum lease payments; therefore, the asset is recorded at this present value. (Solution = b.)

Question

2. The amount to be recorded by a lessee as cost of an asset under finance (or capital) lease is equal to:

- present value of minimum lease payments.

- present value of minimum lease payments or fair value of the asset, whichever is lower.

- present value of minimum lease payments plus present value of any unguaranteed residual value.

- carrying value of the asset on the lessor's books.

EXPLANATION: For a finance (or capital) lease, the lessee records an asset under capital lease and an obligation under capital lease at the lower of (1) present value of minimum lease payments or (2) fair value of the leased asset at lease inception. An unguaranteed residual value is not relevant to the lessee; the lessee does not account for it. The lessor's carrying value is also irrelevant to the lessee. (Solution = b.)

Question

3. The following list of items relates to accounting for leases:

- annual lease payments

- bargain purchase option

- guaranteed residual value

- unguaranteed residual value

From a lessee's perspective, minimum lease payments associated with a finance (or capital) lease would include items:

- I and II only.

- I, II, and III only.

- I, III, and IV only.

- I, II, III, and IV.

EXPLANATION: List the components of minimum lease payments and compare with the above selections. From a lessee's perspective, minimum lease payments include:

- minimum rental payments

- guaranteed residual value (if any)

- bargain purchase option (if any)

Thus, minimum lease payments include only items I, II, and III. (Solution = b.)

An unguaranteed residual value would affect the lessor's accounting for the lease. For example, the lessor's gross investment in lease consists of undiscounted rental/lease payments plus any guaranteed or unguaranteed residual value or any bargain purchase option, and net investment in lease is the present value of gross investment in lease.

Question

4. On December 31, 2013, Ryan Corporation leased a yacht from François Company for an eight-year period expiring December 31, 2021. Equal annual payments of $80,000 are due on December 31 of each year, beginning on December 31, 2013. The lease is properly classified as a finance lease on Ryan's books. At December 31, 2013, present value of the eight lease payments over the lease term discounted at 10% is $469,474. Assuming all payments are made on time, the amount that should be reported by Ryan Corporation as the total obligation under finance lease on its December 31, 2014 statement of financial position is:

- $348,421.

- $400,063.

- $436,421.

- $480,000.

EXPLANATION: Calculate the amounts for the first three journal entries on the lessee's lease amortization schedule. The schedule would appear as follows: (Solution = a.)

Question

5. The following facts pertain to a lease:

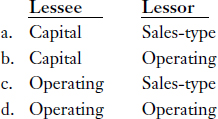

(1) The lease provides that the asset will revert back to the lessor at the end of the seven-year lease term.

(2) Present value of minimum lease payments is equal to $54,000 and fair value of the asset at lease inception is $60,000.

(3) The remaining economic life of the leased asset is estimated to be 10 years.

(4) For the lessor, credit risk associated with the lease is normal.

(5) The lessor guarantees the asset against obsolescence.

(6) Fair value of the asset exceeds its cost on the lessor's books.

(7) Both the lessee and lessor prepare financial statements in accordance with ASPE.

How should the lease be classified on the books of the lessee and lessor, respectively?

EXPLANATION: Review the facts and determine how the lease should be classified on the books of the lessee. Repeat the process and determine how the lease should be classified on the books of the lessor. Refer to Illustration 20-1. Present value of minimum lease payments equals 90% or more of the fair value of the asset, which is one of the ASPE criteria for classification of a lease as a capital lease. Thus, the lease should be classified as a capital lease on the books of the lessee. However, the lessor guarantees the asset against obsolescence, which means that the amounts of any unreimburseable costs that are likely to be incurred by the lessor under the lease cannot be reasonably determined, and the lease should be classified as an operating lease on the books of the lessor. Further analysis of the details of the lease is shown below:

(1) The asset will be returned to the lessor at the end of the lease; therefore, the lease does not meet the first criteria for classification of a lease as a capital lease.

(2) Present value of minimum lease payments ($54,000) is equal to 90% of the fair value of the asset at lease inception ($60,000); thus, the lease meets the third ASPE criteria for classification of a lease as a capital lease.

(3) The lease term is seven years, which is only 70% of the remaining economic life of the asset; hence, the lease does not meet the second ASPE criteria for classification of a lease as a capital lease.

(4) The lessor's credit risk associated with the lease is normal; therefore, the lease meets the first revenue-recognition based ASPE criteria for classification of a lease as a non-operating lease.

(5) The lessor guarantees the asset against obsolescence, which means that the amounts of any unreimburseable costs that are likely to be incurred by the lessor under the lease cannot be reasonably determined. Therefore, under ASPE, the second revenue-recognition based criteria for classification of a lease as a non-operating lease is not met.

(6) If fair value of the asset exceeds its cost on the lessor's books, the lease would be a sales-type lease on the books of the lessor if, under ASPE, the lease meets at least one criteria for classification of a lease as a capital lease on the lessee's books, and both revenue-recognition criteria for classification of a lease as a non-operating lease on the lessor's books. (Solution = b.)

In this example, both the lessee and lessor prepare financial statements in accordance with ASPE, which means that ASPE criteria for classification of leases must be applied. ASPE criteria include numerical thresholds, whereas IFRS criteria do not include numerical thresholds. As well, under IFRS, the degree to which the asset is specialized and of use only to the lessee without major expense to the lessor is an additional criterion considered for classification of a lease as a finance lease.

Question

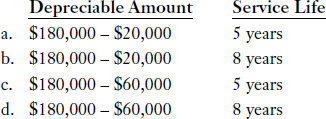

6. Digger Corporation is a lessee with a finance lease. The asset is recorded at a cost of $180,000 and has a useful life of eight years. The lease term is five years. The asset is expected to have a fair value of $60,000 at the end of five years, and a fair value of $20,000 at the end of eight years. The lease agreement provides for automatic transfer of title of the asset to the lessee at the end of the lease term. What depreciable amount and what service life should the lessee use to calculate depreciation for the first year of the lease?

EXPLANATION: Select the option that will provide the best matching of costs with revenues. Because title will automatically be transferred, the lessee is expected to hold and use the asset for eight years. The benefit to be consumed over the eight years is the difference between the asset's recorded cost ($180,000) and its expected value at the end of its useful life to the lessee ($20,000). (Solution = b.)

Question

7. Three different lease situations are described below:

(1) Lessee's incremental borrowing rate is 12%.

Lessor's implicit rate is 12%.

Asset will revert to the lessor at the end of the lease term when the asset is expected to have a fair value of $60,000.

(2) Lessee's incremental borrowing rate is 12%.

Lessor's implicit rate is 12%.

Lease requires the lessee to guarantee a residual value of $30,000 to the lessor.

(3) Lessee's incremental borrowing rate is 12%.

Lessor's implicit rate is 14%.

Lease contains a bargain purchase option of $20,000.

Under IFRS, in which of the above cases can the lessor and lessee use the same lease amortization schedule?

- 1 and 2 only.

- 2 and 3 only.

- 1 and 3 only.

- 1, 2, and 3.