CHAPTER 6

Deducting Office-Related Costs

Everyone has to be somewhere, according to a line from an old BBC show. Whether you work in an office building, at a strip mall, at a table in Starbucks, or in your home, you have office-related costs. These costs include expenses related to the physical space, such as rent for an office within a commercial building or a home office deduction if you operate from home. Office costs also include supplies, technology costs for a website and computer backup and maintenance, utilities, and insurance. You may have some or all of these expenses.

Rental Expenses

Whether your office is a retail store, a greenhouse, an artist's studio, a medical office, or an office in a commercial building, it has to work well for you. Check on:

- Location. Does access to foot traffic matter to you? Do you need adequate parking or access to public transportation?

- Size. Is the size of the space suitable for your needs?

- Cost. Rent is usually one of the largest monthly costs for a self-employed person. Can you afford it?

Your monthly rent for commercial space is fully tax deductible. Rent can be a fixed monthly amount or an amount based on a percentage of your gross receipts.

The rent must be reasonable, which is assumed when you and the landlord are not related. However, if the landlord is your brother, your mother, or someone else with a close relationship to you, the IRS may take a close look at whether the amount of the rent is reasonable. If it's too high, you won't be able to deduct the full amount. What's reasonable? Essentially, reasonable means the going market rate. Think about what would be charged to a third person with no relationship with the landlord. Related persons for this purpose include members of your immediate family:

- Spouse

- Children and grandchildren

- Siblings (whole or half)

- Parents and grandparents

Not treated as related persons for this purpose are in-laws, aunts and uncles, and friends.

Other Rent-Related Costs

In addition to the basic monthly rent, there may be other payments that you can or cannot deduct.

SECURITY DEPOSITS

You may be required to pay a security deposit. Usually, the security deposit is viewed as an advance payment because the landlord must keep it on hand and does not have the right to use it now. It very well may be returned to you. Thus, you can't deduct the security deposit until it is kept by the landlord and applied toward the rent or other obligation in the lease.

PREPAYMENTS

You may be given a rent reduction if you agree to pay the rent in advance. The amount you save isn't taxable to you. However, you can't deduct the prepayment if it covers too long a period. There's a 12-month rule that permits you to deduct prepayments if the right or benefit created by the prepayment does not exceed the earlier of

- 12 months after the right or benefit begins

- The end of the year after the year in which the payment is made

Example

On November 1, you prepay rent for the next six months, which covers you through April of the following year. Because the right of occupancy does not run for more than 12 months after the right begins (November 1), you can deduct the full prepayment in the year of payment.

Commercial Leases

A lease is a contract that lets you use space that someone else owns. Don't sign on the dotted line for a commercial lease unless you understand what you're getting into. There may be potential legal traps for you.

- Term of the lease. Many landlords prefer to lease space on a five-year term. However, if you can, it's probably better when starting out to negotiate for a one- or two-year term, with an option to renew. If this can't be done, be sure to have the right under the terms of the lease to sublet your space (in case you no longer need some or all of it). The reason why you want only a limited term is because you personally guarantee the rent. Even though your business name is on the lease and the rent is paid from your business bank account, if you close your business, you're on the hook for rent for the balance of the lease term unless the landlord lets you out of the lease or re-rents your space to a new tenant. (The landlord has a legal duty to try to re-rent, but this may not be possible during poor economic times.)

- Type of lease. Unlike a residential lease, you may be paying for more than just the space you occupy. Your rent may cover the costs of common areas, utilities, insurance, maintenance, and even a share of the landlord's real estate taxes. The lease may be labeled “net lease,” or “gross lease.” A net lease means that in addition to rent, you pay for the building's operating costs (property taxes, insurance, repairs, and utilities). A gross lease is a fixed payment that reflects the landlord's costs, but makes it easier for you to budget your rental expense.

- Improvements. Who's paying for new lighting, carpeting, wiring, and other improvements needed by you for your business? This should be negotiated. If the landlord is having difficulty renting space, the landlord may willingly bear some or all of these costs as an inducement to obtain a new tenant.

- Cancellations and renewals. If the space doesn't work out for you—the location turns out to be poor or the size of the space no longer meets your needs—is there any escape clause to let you out with minimal financial exposure? Some leases allow you to leave if your annual revenues fall short of a specified amount. Or, if you have a non-compete clause in the lease, you can leave without financial cost if the landlord rents space near you to a competitor. On the flipside, if you love where you are and want to stay after the lease is over, what are the renewal terms? How much will the rent escalate? How long is the new lease term?

Just about every term in a commercial lease is negotiable; very little is boilerplate. Thus, it's imperative that you work with a commercial real estate lawyer to help you get the best terms for you and to make sure you fully understand your rights and obligations under the lease.

Did you know …

The attorney's fee for helping you with the lease is not fully deductible in the year you pay it, even though you are on the cash basis. The costs of acquiring a lease are treated under tax rules as a capital expenditure. This means you must capitalize the cost (add it to the lease) and then deduct the fee evenly over the term of the lease. The same tax treatment applies to a broker's fee for finding the space.

Virtual Offices

A solution for a growing number of self-employed individuals who need professional-looking space on an occasional basis is to “rent” by the hour or day in an office suite for this purpose. Maybe you need a conference room to make a presentation; or maybe you want to host prospective customers on Main Street rather than on Elm Street but don't want or can't afford to rent regular office space.

So-called virtual offices are springing up around the country, particularly in urban areas where rents for traditional space are high. Virtual offices have receptionists to answer your phone (whether or not you're at the virtual office), Internet access, photocopying equipment, a kitchen facility, and other amenities you'd find in a traditional office.

Again, the cost of using an office is tax deductible to you.

Home Office Use

If you work from home, you're in good company. The U.S. Small Business Administration says that more than 52% of all small businesses operate from home. What's more, many people take work home after hours, using technology to enhance their productivity.

From a tax and financial perspective, using a home office makes a lot of sense. It turns what would otherwise be nondeductible personal expenses into deductible business expenses. And it avoids the need to pay rent for outside space.

What Is the Home Office Deduction?

The home office deduction is an umbrella term used to describe the single write off you take for a host of expenses related to operating your business from home. The deduction covers:

- Rent if you lease your home; real estate taxes, mortgage insurance, and depreciation if you own it

- Utilities

- Repairs and maintenance

- Insurance

- Alarm system charges

Not every cost related to your home is part of the home office deduction. For example, the cost of landscaping and lawn maintenance is not part of the home office deduction.

Eligibility for the Deduction

To claim a home office deduction, you must meet a two-prong test. First you must show that the purpose of the use is satisfactory for tax law purposes. Then you must show the use of the space in your home is only for business.

PURPOSE OF THE SPACE

The use of the space in your home must be for one of the following:

- Your principal place of business

- A place to meet or deal with clients, customers, or patients in the normal course of your business

- A separate structure, which is not attached to your home, that is used in your business

Check which condition applies to your situation to see if you qualify for the home office deduction.

Your Principal Place of Business

If you only work from home and from no other location, you clearly establish the home office as your principal place of business. Thus, if you are a freelance writer pecking away at your keyboard, your home is the location of your business.

However, many self-employed people really earn their money in the field (e.g., an interior decorator who works with residential clients or an electrician who has commercial customers). In this case, your home office is also treated as the principal place of business if it's where you perform substantial administrative activities and you have no other fixed location for these activities.

Examples of substantial administrative activities include:

- Keeping your books and records

- Ordering supplies

- Scheduling appointments with clients, customers, patients, prospects, and vendors

- Writing proposals and estimates

If you don't use the space for substantial administrative activities, you'll have to see whether, under the facts and circumstances, your home office is your principal place of business, based on the following:

- The relative importance of the activities performed in your home and other business location(s).

- If the relative importance factor doesn't determine your principal place of business, you can consider the time spent in each location.

A Place to Meet or Deal with Clients, Customers, or Patients in the Normal Course of Your Business

A tax return preparer with a downtown office who meets clients in her home office in the suburbs to sign tax returns would meet this condition. However, simply making phone calls from a home office is not considered “meeting” with customers.

A Separate Structure, which Is Not Attached to Your Home, that Is Used in Your Business

A garage converted to a studio, a greenhouse for growing plants you use in your business, or a garage used to store inventory all satisfy this condition.

USE OF THE SPACE

Even if the reason why you use the space in your home is satisfactory, you can't take any deduction unless the use of the space is exclusively and regularly for business.

Exclusive Use

The area you use for business cannot be used at any time for personal purposes.

Example

You are a contractor who uses a den in the evening to prepare estimates for prospective customers. Your children use the den during the afternoon to do their homework. You fail the exclusive use test.

There are two important exceptions to the exclusive use test. You can qualify for a home office deduction if you use part of your home:

- For the storage of inventory or product samples

- As a daycare facility

Exclusive use does not require you to use an entire room for business. You can use a portion of a room and don't even need a physical partition for the office space. Just make sure that the area is, in the words of the IRS, “separately identifiable.”

Regular Use

Regular use of a home office means ongoing and continual. You fail the regular use test if you only use the home office occasionally or incidentally, even if the area is exclusively for business.

Figuring the Deduction

Just like the deduction for business use of your vehicle (Chapter 5), you have two ways in which to figure your home office deduction: the actual expense method and an optional simplified method.

ACTUAL EXPENSE METHOD

The actual expense method allows you to take a fixed percentage of your otherwise personal costs of the home and treat them as a deductible business write off. These are called indirect expenses. You can also add to this the full amount of any expense that directly relates to the home office, such as painting the room used as a home office. These are called direct expenses.

If you own your home, you can take depreciation on the portion of your home used for business. Depreciation is based on the cost of the portion of your home used for business or fair market value, whichever is lower.

Example

In 2010, you bought your home for $280,000 ($30,000 of which represents the cost of the land). You use 10% of the space in your home for business. The value of your home is now $330,000. You can depreciate $25,000, which is 10% of the cost of $250,000 (the cost of the home exclusive of land, which is never depreciated). This is less than 10% of the home's fair market value, or $33,000.

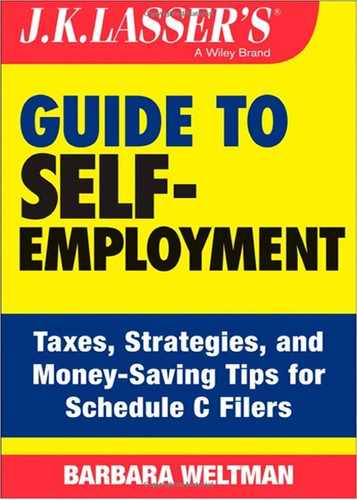

Depreciation is based on the applicable percentage from Table 6.1. Use the percentage for the month you start using your home for business. (The rates in this table are based on your home office being treated as residential realty, with certain special tax rules applied, because your home is being used for business in this case.)

Example

Same facts as in the example where you can depreciate $25,000. You begin to use your home office in May 2013. Your depreciation allowance for 2013 is $401 ($25,000 × 1.605%).

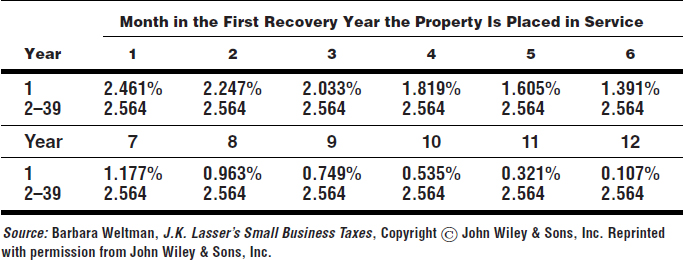

The actual expense method is figured on Form 8829, Business Use of a Home. You'll find a sample form in Figure 6.1.

ALLOCATING SPACE

How much of your home do you use for business? This portion is used to determine how much of your indirect expenses are added to the home office deduction. Usually, this is figured on square-footage basis. Thus, if your home is 2,500 square feet and you use 250 square feet as your home office, then 10% of the home is used for business.

Example

Your indirect expenses total $7,800. You use 15% of the square footage of your home as an office and you qualify for the home office deduction. Your write-off is $1,170 ($7,800 × 15%).

If all of your rooms are of approximately equal space and you use one room for business, then you don't have to use square footage. For example, if you have a five-room apartment and you use one room for an office, you can treat 20% of the space for business, assuming all of the rooms are about the same size.

FIGURE 6.1 Form 8829. Source: www.irs.gov/pub/irs-pdf/f8829.pdf.

A special allocation rule applies to daycare businesses. The rules are based on hours of usage. The fact that the space is not used exclusively for business won't prevent a deduction. Here's how to figure the percentage of business use for a daycare business:

- Compare the number of hours of business use in the year with the number of hours in the year (8,760 for a 365-day year).

- Apply this percentage to the usual business percentage of total space.

Example

You run a daycare business in the basement of your home, which represents 50% of the total space of your home. The business operates 12 hours a day, 5 days a week, 50 weeks a year. Thus, you use your basement for business 3,000 hours a year, or 34.25% of the total hours in the year (3,000 ÷ 8,760). The percentage applied to indirect expenses is 17.13% (34.25% × 50%).

Did you know …

You must have a license, certificate, registration, or other approval from your state to operate a daycare center, or family or group daycare center. You can claim the deduction if you've applied for approval, but not if you've been rejected or had your approval revoked. You don't need licensing if your state says so. For example, you may not need a license to mind three children in your home. Check your state licensing rules, which can be found at http://daycare.com/states.html.

SIMPLIFIED METHOD

The simplified method is a rate set by the IRS and goes into effect for the first time starting in 2013. For 2013, the rate is $5 per square foot up to a maximum of 300 square feet. Thus, the most you can deduct for a home office under the simplified method is $1,500 ($5 × 300). The IRS may increase the $5 limit, but is not required to do so annually or at any other particular time.

Using the simplified method produces all of the following results:

- No depreciation. If you own your home, you can't take any depreciation on the business portion of your home. You are not treated as having taken depreciation, called deemed depreciation, for the home office deduction.

This is a good thing, since you avoid depreciation recapture when you sell your home at a profit.

- No carryover. The gross income limitation (explained later) applies for both the actual expense and the simplified method. However, if you cannot take the deduction now because of the limitation, there's no carryover allowed with the simplified method.

You figure the simplified method on a worksheet for this purpose. You can use the sample worksheet in Figure 6.2.

Strategies for the Home Office Deduction

Which method is better for you to use, the actual expense method or the simplified method? Obviously, if your space is larger than 300 square feet, you may be doing yourself a disservice by using the simplified method.

On the other hand, the time and effort to figure the deduction using the actual expense method may not be worth it. You may have multiple utility bills for items such as electric, oil, water, and other utilities that require really good recordkeeping throughout the year, something you may not choose to do.

If your business isn't profitable, it doesn't pay to use the simplified method because you won't get any tax benefit. There's no current deduction and no carryover in this situation.

Unfortunately, the only way to really know which method is better is to keep records throughout the year and then, at tax time, see which method produces the better result.

DEDUCTION LIMITATION

The deduction, figured under either method, cannot exceed “gross income” from your home office activity. More specifically, if your gross income from the business use of your home equals or exceeds your total business expenses (including depreciation if you own your home), you can deduct all your expenses related to the business use of your home. But if your gross income from the business use is less than your total business expenses, your deduction for certain expenses for the business use of your home is limited.

Your deduction of otherwise nondeductible expenses, such as insurance, utilities, and depreciation (with depreciation taken last), allocable to the business is limited to the gross income from the business use of your home minus the sum of the following:

- The business part of expenses you could deduct even if you did not use your home for business (such as mortgage interest, real estate taxes, and casualty and theft losses)

- Business expenses that relate to the business activity in the home (for example, a business phone line, supplies, and depreciation on equipment), but not to the use of the home itself

If you are subject to a limitation, you may be able to use the deduction in a future year, as explained next.

CARRYOVER OF UNUSED DEDUCTION

If your gross income from the business use is less than your total business expenses, you may be able to carry over the unused amount and deduct it in a future year. Under the actual expense method you can use the deduction next year if you have sufficient gross income from your home office activity next year.

Example

In 2013, you figure your home office deduction to be $2,248. However, 2013 is a loss year for you; you have no gross income from the home office activity. In 2014, you become profitable and have gross income of $52,000. You can use the carryover, as well as a deduction for 2014 home office expenses.

There is no time limit on the carryover, so if your income isn't sufficient next year, you can continue to carry over the unused amount to future years. You lose the carryover once you no longer have a home office business. However, you don't have to have the same home office to use up the carryover. If you move to a new home and maintain a home office in your new home, you can use the carryover as long as you have sufficient gross income for the offset.

Did you know …

No carryover is allowed if you figure your deduction using the simplified method. So using the simplified method reduces your recordkeeping because you don't have to remember that you have a carryover, but a good write-off is wasted.

Strategies to Address Audit Concerns

The home office deduction has been called an IRS audit red flag, meaning that it attracts IRS audits. This isn't necessarily so, given the fact that so many businesses now operate from home. There are no statistics from the IRS on their audit activities with respect to the home office deduction. However, if you still have concerns, you can take certain actions that will help you in the event your home office deduction is questioned by the IRS:

- Make sure you qualify for the deduction. Review the eligibility conditions discussed earlier in this chapter. If you are unsure about your situation, talk with a tax expert.

- Take a photo of your office space. As you've learned, you must use the space in your home for business in order to take a deduction. To help prove that you do, photograph your home office and keep a copy with your tax records. After all, you may move from the space before the IRS questions your deduction and would not otherwise be able to demonstrate your business use of your home.

Ancillary Results of the Home Office Deduction

Once you qualify for a home office deduction, certain other tax breaks fall into place. Your home is your place of business, so travel from and to home on business is not viewed as nondeductible commuting. Instead, the cost of getting from home to see a customer, make a bank deposit, mail a package, take a continuing education course, or buy office supplies becomes tax deductible (see Chapter 5). The return trip is also deductible.

Another benefit is that a computer used in your home office is considered to be used entirely for business. You don't have to keep records of when you use it for business or personal activities. This enables you to deduct the cost of the computer, explained later in this chapter.

However, if you use the actual expense method to figure the home office deduction for a portion of your home used for business and you own your home, there's a downside. While you add an allowance for depreciation into your home office deduction, you then are subject to depreciation recapture when you sell your home at a profit. The depreciation you've claimed becomes taxable at the rate of 25% when you sell your home, even if you're otherwise entitled to claim the home sale exclusion for gain on the sale of your residence.

Materials and Supplies

When it comes to paper, cleaning supplies, materials for the work you do, and items you sell to customers when you provide services, such as a new circuit breaker box when you do electrical work for homeowners, all of these things are tax deductible.

Don't buy more material and supplies than you need. You'll have to store it and items can go bad or become obsolete. For example, if you buy a number of toners for the printer you're using, they become useless to you if you replace the printer with a new one.

It makes good business sense to take advantage of buying discounts. For example, the price per item may go down as you buy in volume. Remember, however, that you're tying up your money in items that won't be used immediately and you have to store what you buy.

From a tax perspective, only buy as much of the items as you expect to use within the coming year so you can deduct your purchases now. You'll see later in this book that stocking up is a good year-end tax strategy (see Chapter 11).

Furniture and Fixtures

When you buy items for your office, you can write off the cost using a number of tax rules listed here and discussed in the following:

- First-year (Section 179) expensing deduction

- Bonus depreciation

- Regular depreciation

Did you know …

You can create good cash flow just by buying items you need for business if you write off the cost with the Section 179 deduction or bonus depreciation. This is because you can take the deduction without regard to whether you've paid for the item in cash or financed the purchase with a loan or paying by credit card.

Example

In December of this year you buy a $2,500 computer and charge it to your credit card. You receive the credit card bill next year and pay it then. You get the deduction this year to save you taxes even though you don't pay for the computer until next year.

These write-off options don't affect what you can ultimately deduct, which is the cost of the items. They merely impact the timing of deductions, whether you claim the write-off up front or spread it over a set number of years fixed by the tax law.

First-Year Expensing

This lets you deduct the cost of the items in the year you place them in service. You have to elect this deduction rule; its application isn't automatic.

“Placed in service” means the year in which they are ready to be used in business and not merely on order, even if you've already paid for them.

Example

In December 2013, you order office furniture and charge the purchase to your credit card. The furniture is delivered six weeks later, on January 25, 2014. Because the furniture is placed in service in January, you cannot deduct the cost in 2013; the deduction will be allowed in 2014.

The deduction for all of the items you purchase this year is limited to a set dollar amount. For 2013, the dollar amount cannot exceed $500,000. It is supposed to decline to $25,000 in 2014, but Congress could change this limit. For most self-employed individuals, even the lower limit is adequate to cover most purchases for the year. You can take the deduction every year in which you buy items for your business; there's no lifetime limit.

Technically, the dollar limit phases out when total purchases of equipment (e.g., furniture) and machinery exceed another dollar limit. Then the deduction amount is reduced dollar for dollar for each excess dollar of purchases until the deduction amount disappears. As a practical matter, it's unlikely that as a self-employed service provider you will exceed the limit, but just so you know, the threshold at which the phase-out of the deduction limit begins is $2 million in 2013; it is scheduled to be $200,000 in 2014.

Here are some other pointers about the Sec. 179 deduction:

- Expensing can be used whether the items you buy are new or used. Thus, if you want to save money by buying pre-owned file cabinets, it makes good business sense. The cost can still be written off using first-year expensing.

- You can only benefit from first-year expensing if you're profitable. Technically, your first-year expense deduction is limited to gross income from business for the year. However, all business is taken into account, including any taxable compensation you, and your spouse if you're married, receive for being an employee. If you elect expensing, you can carry over any amount that is not immediately deductible because of this gross income limit.

Bonus Depreciation

For 2013, you can deduct 50% of the cost of the items in the first year. This 50% write-off is called bonus depreciation because it is in addition to any first-year expensing or regular depreciation you may claim. In effect, bonus depreciation helps you increase upfront deductions; it doesn't give you any greater write-off over the life of the item. Bonus depreciation is set to expire at the end of 2013, but could be extended by Congress to future years.

Bonus depreciation applies only to new items. You cannot use it if you buy pre-owned items.

Bonus depreciation applies automatically. However, you can opt not to use it. For most self-employed individuals, there's really little reason to waive the deduction. If you're not profitable but have purchased eligible equipment, you can still benefit from the deduction because it increases a net operating loss (see Chapter 4).

Regular Depreciation

Depreciation is an allowance that spreads the deduction for the cost of items over a period fixed by tax law. If you use software to figure your taxes or leave it to a tax pro, the deduction for depreciation is figured for you after you provide certain information:

- The cost of the item

- The date it was placed in service

However, so you understand how depreciation works, here are some important details.

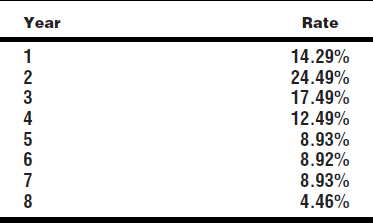

Office furniture, fixtures, office safes, and most other equipment are treated as seven-year property. Annual deductions are figured using a percentage each year that essentially frontloads your write-offs. Because of certain special rules, called conventions, the seven-year recovery period actually works out to eight years. This period may be longer or shorter than your actual use of the items, but this is the period you have to use for regular depreciation.

The percentages for furniture and fixtures in your office usually are the rates found in Table 6.2. These rates are based on a convention called the midyear convention.

Example

This year, you buy furniture for your office that costs $4,000 and you don't write off the cost using first-year expensing or bonus depreciation. Your depreciation deduction this year is $571.60 ($4,000 × 14.29%). Next year, you deduction will be $99.60 ($4,000 × 24.49%), and so on.

If you buy a certain amount of furniture and other equipment and machinery in the last quarter of the year, instead of the percentages listed in Table 6.1, a different convention (called the mid-quarter convention) comes into play. It changes the applicable rates for depreciating all of the purchases during the year.

Instead of using these percentages to frontload your write-offs, at your election, depreciation can be taken in equal amounts (this means using a straight-line method that creates mostly even deductions over the applicable period for the items).

Example

You buy furniture that costs you $4,000 and you don't write off the cost using first-year expensing or bonus depreciation. Divide the cost, $4,000, by the applicable recovery period of seven years. Your deduction in year 1 and year 8 is one-half the usual amount, or $285.71. The deduction in years 2 through 7 is $571.42 annually.

You can find IRS tables listing the depreciation percentages in Publication 946, How to Depreciate Property, at IRS.gov.

Because regular depreciation goes on for a number of years, it's up to you to keep track of this write-off every year. Again, if you use the same computer software for tax preparation, it will remember this information for you. The same is true if you use the same tax return preparer each year; he or she will keep track of your depreciation.

Converting Personal Items to Business Use

When you start a business, you may already have a desk, chair, and other items that you'll be using in your business. From a business standpoint, why buy new when you already have what you need? Conserve your cash for other purposes.

From a tax perspective, putting personally owned items to business use means you can't write off the cost using first-year expensing or bonus depreciation (if it is extended beyond 2013). You can depreciate the items. The basis for depreciation is the lower of its adjusted basis (usually its cost) or its fair market value at the time of conversion to business use. Fair market value is usually what an item is worth to someone else (i.e., what you could get if you sold it now).

Example

Several years ago you bought a desk and chair for $900. You now convert it to business use when its fair market value is $400. You can depreciate $400, which is the furniture's fair market value, because this is lower than its cost.

Computer-Related Costs

Today almost every business runs on or uses computers and mobile devices. All of your computer-related costs usually are deductible.

Purchases

When you buy computers, tablets, printers, and other devices, you can write off your costs using the same methods applicable to furniture, discussed earlier. There are differences to note:

- Computers are eligible for first-year expensing only through 2013, unless Congress extends this rule.

- Computers and peripheral equipment are five-year property. The percentages for five-year property are in Table 6.3.

Remember that even though computers are five-year property, the special convention in the tax law requires the cost to be depreciated over six years.

CONVERTING PERSONAL ITEMS TO BUSINESS USE

When you start a business, you may already have computers or other devices that you begin to use in business. Like personal furniture that you convert to business use, technology items are depreciable. You depreciate the lower of the original cost of the item to you (technically its adjusted basis, which for most purposes will be original cost) or its value on the date you put it to business use (technically called fair market value).

Example

You bought a computer for personal use last year at a cost of $2,500. This year you start a business and begin to use the computer for business applications. The computer is now worth $2,000. You can depreciate $2,000; its fair market value is lower than its adjusted basis.

You can't write off the cost of the items you formerly used for personal purposes using first-year expensing or bonus depreciation. But you can take regular depreciation based on the lower of cost or fair market value at the time of the conversion.

Software and Cloud Solutions

The write-off for the cost of off-the-shelf software depends on the life of the software. If it is useful for only one year, as in the case of tax preparation software, you can deduct it in full in the year you buy it.

If the software has a longer useful life, such as programs you buy for accounting or word processing, it is deductible in the same way as computers. Thus, you can expense the cost.

The cost of cloud solutions that you pay for on a monthly basis is deductible in full. Because you don't own anything, there's no depreciation or other special write-off rules involved. It's simply an ordinary and necessary business expense.

The costs of apps you use on your mobile devices are also deductible.

Data Backup

Your data is too valuable not to protect. The best protection is to back it up regularly. Backup may be done by you to a remote location or handled automatically with a backup service, such as Carbonite. Automating the process is smart so you are sure it gets done.

The cost of backup is deductible as an ordinary and necessary business expense. There's no dollar limit on what you can deduct.

From a business perspective, shop around for good backup. Make sure that you can easily recover anything that is lost because of a computer crash, theft, or other catastrophe. Also comparison shop because costs may vary depending on the amount of data you back up.

IT Maintenance and Repairs

The cost of an IT service that maintains your equipment on a regular basis or the cost of repairs when something goes wrong is deductible in full. However, make sure you know the difference between ordinary repairs and capital improvements. In some cases, the distinction is easy to see; in others, it is not.

Example

Repairing a photocopying machine that continually jams is an expense that is currently deductible. Replacing a hard drive in a computer so that it is good to go for many years to come is a capital improvement, the cost of which is treated the same as if you'd bought a new computer (i.e., the cost is recoverable through depreciation).

Insurance

Insurance is one of those things you don't like to pay for because you never know if you'll ever need it. However, it's good business practice to protect yourself as much as possible. For your office, talk with a knowledge insurance person who can advise you on the coverage you need.

Special Concerns for a Home Office

If you work from home, don't assume that your homeowner's or renter's policy will protect you. The limitations on these policies may exclude protection for business property or provide such dollar caps as to not be helpful. For example, your homeowner's policy may limit recovery for theft or damage to computers and related equipment to $2,000. If your equipment is worth $10,000, your homeowner's coverage is inadequate.

Fortunately, you can easily address the limitations in your existing policies by:

- Tweaking your homeowner's/renter's policy. You may be able to add a rider or endorsement to your business needs at very little annual cost.

- Buying a separate business policy. As discussed in Chapter 1, a business owner's policy (BOP) for your home-based business will provide coverage for both liability and property damage or loss.

Utilities

You may have a variety of utilities related to your office. If you claim a home office deduction, utilities become part of that deduction. If you have a separate office, you separately deduct utilities on Schedule C. Examples of deductible utility costs include:

- Electric and gas charges.

- Internet access.

- Oil.

- Smartphone and other mobile device conductivity fees.

- Telephone landlines. However, if you claim a home office deduction, you cannot deduct the basic service charges of the first line to your home.

- Water and sewage.

Miscellaneous Office-Related Costs

Not everything you buy for your business falls neatly into a category you'll find on Schedule C. You can deduct any ordinary and necessary business expense related to your office. You'll find the terms ordinary and necessary defined in the next chapter.

Here is a list of some of the types of miscellaneous costs you can deduct—currently or through depreciation:

- Aquarium and its maintenance. Many professional offices have beautiful fish tanks in their waiting rooms and you can, too. The cost of the equipment is depreciable; ongoing maintenance is a deductible expense.

- Books. Books on business subjects can be helpful to your activities. The books can explain topics you're not adept at, such as social media, technology, or sales. If the books have a life of one year or less, they are currently deductible. Thus, J.K. Lasser's Small Business Taxes 2014, which is used for 2013 returns, is an annual publication that is currently deductible. Books with an indefinite shelf-life can be expensed or the cost can be recovered through depreciation, as explained earlier in this chapter with respect to the costs of furniture and fixtures.

- Cable TV. The fee for cable service to provide viewing in a waiting room, bar, or other business location is deductible.

- Cleaning and janitorial services. The fees you pay to a cleaning business are deductible. If your office is in your home, allocate the fees to the portion related to your home office; the portion for the rest of your home is not deductible. But beware: If you use someone to clean your home who does not have his or her own business or work for a cleaning service, you may be an household employer liable for employment taxes. Find more details in IRS Publication 926, Household Employer's Tax Guide.

- Decorator fees. If you pay an interior decorator to design your workspace, the fees are deductible. However, some decorators do not charge a separate fee; it is built into the cost of the furniture you buy, which becomes depreciable.

- Flowers and plants. If you dress up your office with flora, you can deduct the cost.

- Postage and shipping. The cost of mailing letters and packages from your office is deductible. If you rent a postage meter, its cost is also deductible. The IRS has said informally that a business can deduct deposited funds for a postage meter as long as they relate to stamps that will be used within

months of the end of the deposit year.

months of the end of the deposit year. - Security system costs. Monthly monitoring fees are deductible. The cost of installing a system can be expensed or recovered through depreciation as explained earlier in this chapter for the cost of furniture and fixtures.

- Uniforms. If you wear a business uniform, including a shirt with your business logo, you probably can deduct it. No deduction is allowed for the cost of clothing that is suitable for street wear, even if it is worn only in business and you would not have purchased the item but for business.

What's Ahead

You've seen the specific deductions you can claim for travel and entertainment costs (Chapter 5) and for office-related expenses (this chapter). But these expenses are only the tip of the iceberg when it comes to running your business. Your business may have myriad costs, from advertising to Xeroxing.

In Chapter 7 you'll see how to handle these other costs.

Chapter Takeaways

- If you rent outside space, you can deduct it.

- Finding the right space at the right price is an important business activity.

- If you work from home, you may qualify for a home office deduction.

- The cost of items used in your office can be written off using a variety of helpful tax rules.

- Write-off restrictions apply when you use items, such as furniture and a laptop, that were formerly used for personal purposes but are now being used in business.

- Insurance for your office is important from a business perspective, and is fully deductible on your tax return.

- Miscellaneous deductions related to your office are deductible as long as they are ordinary and necessary business expenses.