CHAPTER 10

Paying Your Taxes

As a self-employed person, what are the taxes you have to pay? It goes beyond income taxes. You are required to pay self-employment tax if you have a profit in order to earn Social Security and Medicare credits. If your earnings are high enough, you'll pay an additional Medicare tax. And if you are effectively only an investor in your business, with others doing the heavy lifting, you may owe another additional Medicare tax.

Because you are not a W-2 employee, there's no withholding on your earnings so you have to be proactive in paying all of your taxes. You do this by making four estimated tax payments over the course of the year.

Self-Employment Tax

In a nutshell, this tax is like FICA tax, which is paid by employers and employees to cover Social Security and Medicare taxes, but instead of applying it to taxable wages it is levied on your profits. Self-employment tax includes both the employer and employee share of FICA, even though you are neither an employer nor an employee. However, you do get to deduct the so-called employer share (as explained in Chapter 7).

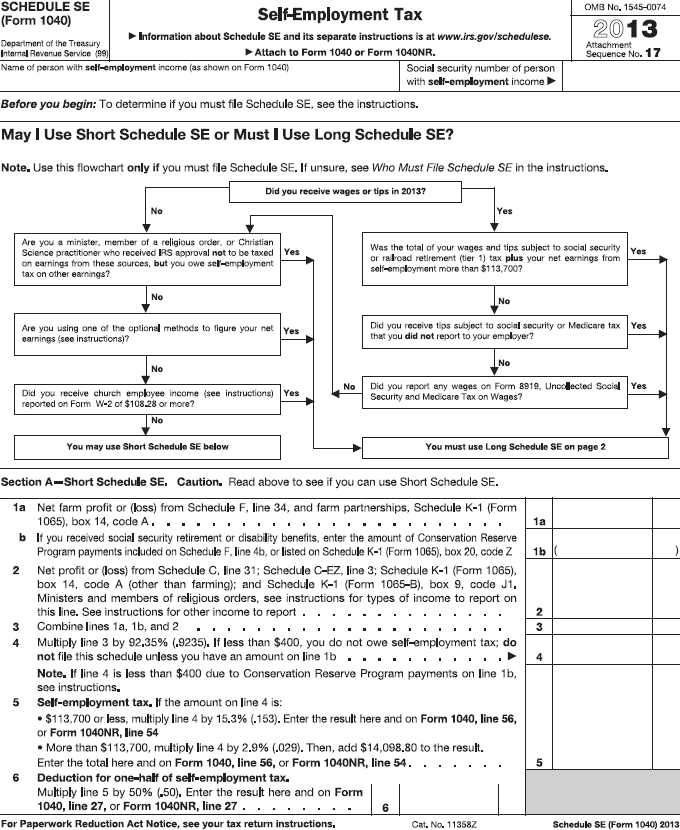

For 2013, self-employment tax is essentially 15.3% on net earnings (profits) up to $113,700, plus 2.9% on net earnings over this amount. However, the computation is a little more complex. Fortunately, tax preparation software and cloud solutions only require you to input your earnings and the computer does the rest. However, if you're interested in seeing how the tax is figured, review the following example.

Example

Your Schedule C shows a profit in 2013 of $125,000. Congratulations on your success. Regardless of how much or how little your income tax bill is on this profit (which depends on your tax bracket), you'll pay self-employment tax of $17,724. This is figured by multiplying your net earnings of $125,000 by 2.9% and then multiplying the lesser of $113,700 (the 2013 wage base) or 92.35% of $125,000 by 12.4%.

You must complete Schedule SE, Self-Employment Tax, if your net earnings for the year are $400 or more. However, when using tax preparation software or a tax professional, this computation is done for you automatically. (See Figure 10.1.)

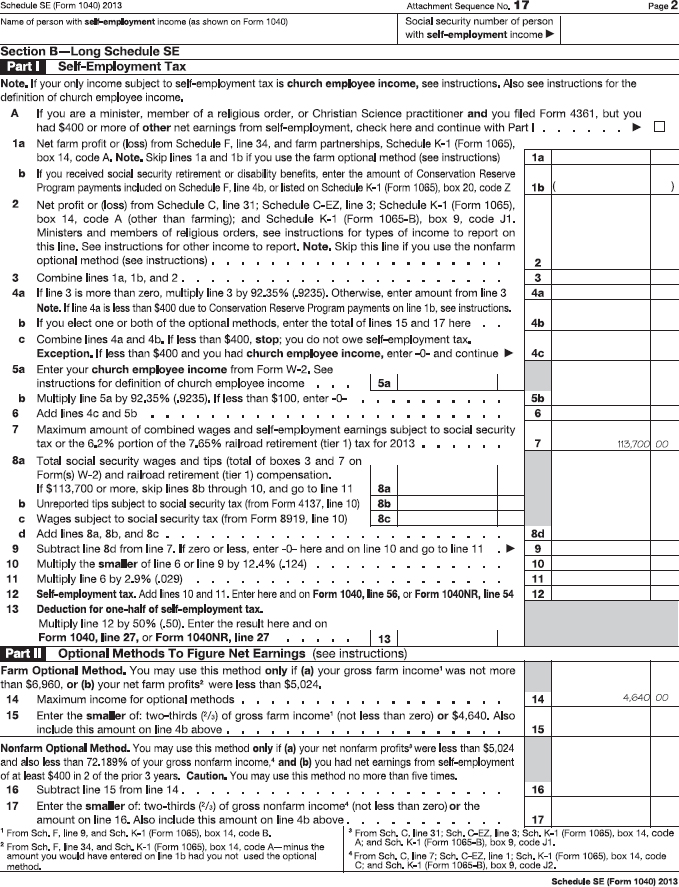

If you have more than one business, you only need a single Schedule SE because you combine your net earnings on the form to figure your self-employment tax.

If you have a job as well as your self-employment business, you pay FICA on your wages. The wages taken into account for FICA reduce or eliminate the Social Security portion of self-employment tax. However, regardless of FICA on wages, you'll pay the Medicare portion on net earnings from self-employment.

Example

You have a job that pays $75,000. You also have a sole proprietorship that you run part time; your profits for the year are $50,000. You pay the Social Security portion of self-employment tax on $38,700 of your profit (the amount of your net earnings from self-employment that, when added to your wages, bring to you the $113,700 cap for 2013). You pay Medicare taxes on $50,000.

Earning Social Security Credits When You're Not Profitable

Anyone can have a bad year. It happens to the best of entrepreneurs when they just start out or when unexpected catastrophes occur. You aren't required to pay self-employment tax if the net results of your business activities are below $400, zero, or a loss. However, you can choose to pay a small amount of self-employment tax in order to earn Social Security credits. This ensures your eligibility for Social Security benefits when you reach retirement age or become disabled. Choosing to pay self-employment tax is called the optional method (a term you'll notice on Schedule SE).

For 2013, for example, it takes four credits (not tax credits but earning a specified amount during a calendar quarter) of up to a maximum of $1,160 each to earn Social Security credits required for coverage. Thus, if your self-employment income is at least $4,640 ($1,160 × 4), you receive four credits (the maximum credits you can earn each year).

ELIGIBILITY FOR THE OPTIONAL METHOD

It applies if your profits (line 31 of Schedule C) are less than $4,894 and are also less than 72.189% of your gross income (other than from farming). Also, you must be regularly self-employed. You meet this requirement if your actual net earnings from self-employment were $400 or more in two of the three prior years (that is, you paid self-employment tax in two of the three prior years).

You can use this optional method for five years; the years do not have to be consecutive.

Additional Medicare Tax on Earned Income

In addition to the Medicare tax you pay through self-employment tax, there is another Medicare tax of 0.9% on your earned income. This additional Medicare tax applies if your profit on Schedule C exceeds a threshold amount that depends on your filing status. The tax starts in 2013 and is a permanent feature in the tax law. It is a tax only on your profit; there is no doubling of this tax as there is in the case of regular the Medicare tax, which is part of self-employment tax (discussed earlier in this chapter).

Earned income includes profit from your sole proprietorship, plus any wages and other business income you receive, over a threshold amount that depends on the filing status you use on your personal return.

The threshold amount is:

- $250,000 for married persons filing jointly

- $200,000 for singles, heads of households, and qualifying widow(er)s

- $125,000 for married persons filing separately

These amounts will not be adjusted for inflation in the future.

Example

In 2013, you are very successful and net $230,000 from your consulting business. If you are single, you'll pay an additional Medicare tax of $270 (0.95 × [$230,000 − $200,000 threshold]).

Again, this additional Medicare tax is not part of Schedule SE. Instead, you figure the tax on Form 8959, Additional Medicare Tax, if you prepare your return by hand. Otherwise, the computer will automatically figure the additional Medicare tax based on the earned income you've entered.

Additional Medicare Tax on Net Investment Income

As the infomercials say, “But wait—there's more.” Also starting in 2013, there is an additional Medicare tax of 3.8% on the lesser of net investment income or adjusted gross income over a threshold amount related to your filing status. This is called the net investment income (NII) tax.

The same threshold amounts that are used for the additional Medicare tax on earned income are used as the threshold amounts for the NII tax. Again, the threshold amount is:

- $250,000 for married persons filing jointly

- $200,000 for singles, heads of households, and qualifying widow(er)s

- $125,000 for married persons filing separately

These amounts will not be adjusted for inflation in the future.

You may be thinking, “What does this NII tax have to do with my self-employment business?” Investment income for this purpose includes income from businesses in which you do not materially participate. Thus, if you own a store as a sole proprietor but don't run it yourself, you may be merely a passive investor for purposes of this additional Medicare tax. So it's not likely that your sole proprietorship will trigger or increase the NII tax, but it could happen.

The NII tax is figured on Form 8960, Net Investment Income Tax–Individuals, Estates, and Trusts.

Estimated Taxes

You can't simply wait until you file your return to pay your taxes because there's an underpayment penalty. Instead you must pay what you expect to owe in four installments during the year. These payments are referred to as quarterly payments, but as you'll see later they don't fall equally throughout the year. Estimated taxes are required if you expect the taxes listed in the next section to be $1,000 or more for the year.

What's Included in Estimated Taxes?

Estimated taxes are not a separate tax. Rather, they are a way of prepaying all of the following taxes together:

- Income taxes, including those on your share of business income

- Self-employment tax

- Additional Medicare tax of 0.9% on earned income, if this tax applies to you

- Additional Medicare tax of 3.8% on the lesser of net investment income, if this tax applies to you

Estimated tax also includes any alternative minimum tax (AMT) that you may have, as well as employment taxes you may owe for a domestic worker (not a business employee).

You make a single estimated tax payment covering the taxes related to your business income as well as your personal affairs. For example, if you had significant profitable stock sales in your personal portfolio, taxes on these gains are factored into your estimated tax payments related to your business income.

When You Pay Estimated Taxes

The quarterly estimated tax payments do not fall equally throughout the year. Instead, the four annual payments occur on specific dates. Estimated taxes are due on April 15, June 15, September 15, and January 15 of the following year. If any of these dates falls on a Saturday, Sunday, or legal holiday, the due date is pushed ahead to the next business day. For example, for 2013, estimated payments are due April 15, June 17, September 16, of this year; the final payment is due January 15, 2014.

Payment Methods

There are several ways to pay your estimated taxes:

- Write a check. Send a check made payable to the U.S. Treasury (not to the IRS) and send it along with Form 1040-ES. This form is essentially a payment coupon to make sure the money is credited to your tax account. On the check, write your Social Security number (and your spouse's if you file jointly), along with the notation of the installment to which it relates (e.g., 2014 Form 1040-ES, first quarter). As long as you send the check by the due date, it's considered to be timely even if the government receives it after the due date.

- Use a major credit or debit card. The IRS doesn't have a fee for this, but the card processor charges a convenience fee. Find a list of IRS-approved card processors, and the fees they charge, at www.irs.gov/uac/Pay-Taxes-by-Credit-or-Debit-Card.

- Pay electronically. The government's EFTPS (electronic federal tax payment system) is free to use and easy to arrange at www.eftps.gov. You can schedule payments in advance. Thus, you won't have to worry if you're on the road when a payment is due by scheduling a payment before you leave. When you apply for an EIN (see Chapter 2), you are automatically enrolled in EFTPS.gov.

Strategies for Estimated Taxes

One of the most common problems that self-employed people face is having the cash on hand to pay estimated taxes when the payment deadline rolls around. Unfortunately, some people can't make the payments and fall farther and farther behind in their taxes, leading to non-filing of returns. This situation produces not only growing tax penalties and interest, but also sleepless nights and headaches. Fortunately, there are a number of business and tax strategies you can use to minimize your tax payments without penalty and ensure adequate cash available to pay your taxes when they come due.

RELY ON ESTIMATED TAX SAFE HARBORS

You can pay the balance due with your tax return and won't incur estimated tax penalties if you peg your estimated tax payments according to either of the following safe harbors:

- 90% of your tax bill for the current year

Example

Your taxes for 2013 total $10,000. You won't owe a penalty if you pay $9,000 in total for the year ($2,250 each installment).

- 100% of the prior year's tax bill (or 110% if your adjusted gross income in the prior year exceeds $150,000, or $75,000 if married filing separately)

Example

Your taxes in 2012 were $10,000 (and your adjusted gross income wasn't over $150,000). You won't be penalized for underpaying estimated taxes if you pay at least $10,000 in total for the year ($2,500 each quarter).

Looking ahead to estimated taxes for the coming year, check on what your tax bill is for this year (or what you expect it to finally turn out to be). When looking ahead, take into account what's likely be different:

- Changes in your family (a marriage; divorce; birth of a child; spouse starting to work)

- Changes in the tax law (expirations of breaks you typically rely on; new laws you can use)

After you've made your projections, then decide whether to use a safe harbor and which one to use.

ADJUST PAYMENTS AS BUSINESS FLUCTUATES

Unlike W-2 employees who have income that's relatively constant, other than bonuses and raises, self-employed individuals don't enjoy this certainty. Your business income may not be constant from year to year. And what you expect to earn for the year may turn out to be too high, or too low. If you rely on a safe harbor but find that business isn't as good as you expected, you can always reduce future estimated payments to reflect your actual situation.

For example, say you use the prior-year safe harbor to figure your first two installments of estimated taxes, but midyear your business hits a wall and profits are way down. You may be able to reduce or even eliminate the final two installments. This conserves cash and avoids the need to wait until you file your return to obtain a refund. Remember, you aren't paid interest by the government for advancing taxes that are later refunded to you (assuming the government doesn't delay the refund).

CHANGE WAGE WITHHOLDING

If you have a job in addition to your self-employment, or if you have a spouse who has a job, you can reduce or avoid the need to make estimated tax payments by increasing withholding from wages. File Form W-4, Wage Withholding Allowances, with your or your spouse's employer to reduce withholding allowances so that more taxes will be withheld from wages.

Alternatively, near year-end, if you anticipate that you haven't had sufficient withholding to cover your estimated tax needs, file Form W-4 to request a specific amount be withheld. This action may be warranted if you or your spouse receives a year-end bonus, even if nothing changes from your projections of your self-employment income.

SAVE FOR TAX PAYMENTS

How can you make sure that you have the funds available when you have to make an estimated tax payment? It's wise to set up a separate bank account to accumulate the necessary cash.

How much you squirrel away in this separate account depends on what you project your needs to be. What was your tax bracket last year? Was it 15%, 28%, or more? You can use your tax bracket, or what you think it will be, as a guideline for savings.

As a service provider you might want to set aside as a minimum 10% or 20% of each payment received for services performed. Remember that the income you earn is reduced by your business expenses, so only the net amount is taxable. By setting aside a portion of each payment you receive, you will ensure that the money isn't spent on other things and is there when estimated tax payments are due.

DON'T OVERPAY

While you want to be sure that estimated taxes are sufficient to cover your tax obligations, you don't want to overpay. Doing this effectively means you've made an interest-free loan to the government. You can't recoup your overpayment until you file your return and receive a tax refund.

It's better to err on the side of underpaying rather than overpaying even if you will owe a penalty. In today's low-interest environment, the underpayment penalty is modest and you have the use of your money until you pay what's owed. Of course, don't underpay so much that you needlessly incur penalties and may have difficulty coming up with the cash to cover your taxes and penalties.

If, despite your best efforts, you do overpay estimated taxes, consider:

- Filing your tax return as quickly as possible to receive a refund.

- Applying the overpayment to next year's estimated taxes. You do this simply by indicating the portion of your return that you want to apply for this purpose. It can be some or all of your overpayment. Depending on the amount of your overpayment and what you expect to owe in taxes for the coming year, applying the overpayment to next year's estimated taxes may allow you to skip one or more estimated tax payments for next year.

Sales Taxes

Every state except Alaska, Delaware, Hawaii, Montana, New Hampshire, and Oregon has sales tax. When local sales taxes are taken into account, there are now more than 10,000 sales tax jurisdictions in North America. What is your sales tax responsibility? Keep these points in mind:

- The tax is levied on your customer, so the tax doesn't come out of your pocket.

- You are the tax collector who must remit the sales tax to the state.

- Each state has its own rules on what is subject to sales tax and what's exempt. Services may be subject to sales tax, depending on where you are located.

- You must file sales tax returns with your state (and any other state in which you do business and collect sales taxes).

Stay alert to possible changes in sales tax rules for businesses that sell across state lines. The Marketplace Fairness Act of 2013, which passed the Senate in the spring of 2013, would require online sellers to collect sales tax from buyers in remote states unless the sellers qualified for a small business exception. If enacted, the new law may or may not impact you; it may affect what you have to pay for goods you order from sellers outside your state.

Find information about your sales tax responsibilities from your state tax department, which you can link to from http://www.taxadmin.org/fta/link/default.php. Sales tax is complicated, so if you don't understand what you have to do, seek professional help.

What's Ahead

Taxes aren't a once-a-year activity. True, you only file your income tax return once a year. But you need to stay on top of changes in the tax law and changes in your business to maximize your tax savings. This is a daily endeavor and that's the focus of the next chapter.

Chapter Takeaways

- You must pay self-employment tax to cover your Social Security and Medicare tax responsibilities.

- You may be subject to additional Medicare taxes if your income is high enough.

- All of your taxes are paid through estimated tax payments four times a year, unless you can cover the liability through wage withholding from a job or spouse's job.

- Plan ahead to have the money ready for tax payments.

- Understand your sales tax responsibilities.