CHAPTER 13

Low-Income Housing, New Markets, Rehabilitation, and Other Tax Credit Programs

§ 13.2 NONPROFIT-SPONSORED LIHTC PROJECT

p. 944. Insert the following before the first full paragraph of this section:

Some nonprofits that have engaged in LIHTC transactions have asserted somewhat aggressive positions that attempt to, in effect, compel renegotiation of their financial upside in transactions that have closed years before. One scenario occurs where a nonprofit that agreed to a certain financial split with its for-profit partner(s) when entering into a transaction years later asserted that honoring it would provide an undue benefit (“impermissible private benefit”) for the for-profit developer.

Ironically, the nonprofit would be taking the contrary position that it would take if the IRS raised the private benefit issue on audit and by litigating the issue, the nonprofit lays out the IRS's argument in publicly available documents.

Another situation involves LIHTC deals coming to the end of the compliance periods, where nonprofits assert Code § 42(i)(7) rights as to first refusal to purchase below fair market value.4.1 One case in Massachusetts has been litigated. See Homeowner's Rehab, Inc. v. Related Corp. V. SLP. L.P., 99 N.E., 3d 744 (Mass. 2018).

§ 13.3 LOW-INCOME HOUSING TAX CREDIT (REVISED)

(b) Introduction to the Low-Income Housing Tax Credit

p. 949. Insert the following at the end of this subsection:

The fiscal year (FY) 2018 omnibus spending bill provided increases for affordable housing, both on the tax and the appropriations front.

- A 12.5 percent increase in low-income housing tax credit allocation for four years (2018–2021), and

- A new permanent provision on income averaging, which would allow housing credit units to be affordable at up to 80 percent of area median income (AMI), offset by deeper targeting in other units to maintain average affordability in the project at 60 percent AMI.

The IRS has released Notice 2020-53, which allows certain time-sensitive actions, such as the 10 percent test for carryover allocations, the 24-month minimum rehabilitation expenditure period, and the reasonable period of casualty loss restoration or replacement, that were due from April 1, 2020, through December 30, 2020, to have a new deadline of December 31, 2020.

(c) Utilization of the LIHTC by Tax-Exempt Organizations

p. 949. Insert the following at the end of footnote 17:

A low-income housing project whose activities would be attributed to private foundation met Rev. Proc. 96-32, 1996-1 CB 717 safe harbor requirements and would continue to do so after the EO's acquisition of all LLC membership interests, where activities furthered the organization's § 501(c)(3) charitable purpose of providing affordable housing for those of low and moderate income. PLR 201603032, January 15, 2016.

(g) Applicable Credit Percentage

p. 974. Insert the following at the end of the first paragraph on this page:

The minimum applicable percentage of 9 percent was extended to before January 1, 2014, under the American Taxpayer Relief Act of 2012 (§ 302), and to before January 1, 2015, under the Tax Increase Prevention Act of 2014 (§ 112). Finally, the Protecting Americans from Tax Hikes Act of 2015 (§ 131) permanently extended that minimum applicable percentage of 9 percent as of January 1, 2015.

In addition, a permanent minimum rate for the 4 percent LIHTC was implemented at the end of December 2020 with passage of the Consolidated Appropriations Act of 2021 (Division EE—Taxpayer Certainty and Disaster Tax Relief Act of 2020, § 201, p. 2451) on December 27, 2020 (“2020 Act”). This legislation fixed the applicable percentage for the 30 percent present-value LIHTC (4 percent credit) at 4 percent (“4% Floor”) regardless of prevailing interest rates. To qualify for the 4% Floor, new or existing buildings, for which IRC section 42(b)(2) does not apply, must (i) be placed in service after December 31, 2020, (ii) receive a LIHTC allocation after December 31, 2020 and (ii) be financed by a tax-exempt bond issued after December 31, 2021 that is subject to the applicable volume cap.107.1

(m) Disposition of the Partnership's or Investor's Interest Following the Compliance Period

p. 989. Insert new footnote 164.1 at the end of the first sentence of this subsection:

164.1 Various interpretations of § 42(i)(7) continue to result in uncertainty among nonprofit entities, project investors, and for-profit partners as to the applicability of the right of first refusal. See Homeowner's Rehab, Inc. v. Related Corp. V SLP, L.P., 479 Mass. 741, 99 N.E.3D 744 (2018) (rejecting the project investor's claim that a right of first refusal under § 42(i)(7) was not triggered by a bona fide offer). Industry professionals continue to request guidance from the Internal Revenue Service as to (1) whether a bona fide offer is necessary to trigger the right of first refusal, (2) whether the right of first refusal applies only to the sale of the project or also to the sale of the limited partner's interest in the owner of the project, and (3) what assets are covered by the right of first refusal. These issues are being litigated/settled across the country and have been in the forefront of industry discussions. Also, the Homeowner's Rehab case has been widely reviewed in the industry and includes a lengthy discussion of the legislative history of § 42(i)(7). (The materials referenced in this footnote were contributed by Carolyn Scogin, an attorney at Blanco Tackabery, who specializes in LIHTC transactions.)

(n) LIHTC 15-Year Issues

p. 991. Insert the following at the end of the second full paragraph on this page:

Some allocating agencies require a waiver by the project owner of the right to request a Qualified Contract (“QC”) as part of the LIHTC application process. The Qualified Allocation Plan (“QAP”) for an allocating agency may also disqualify from participation any principal involved in a project for which a Qualified Contract has been requested. Preliminary consideration and review should be given to both of the foregoing prior to commencing the Qualified Contract process with an allocating agency.

§ 13.4 HISTORIC INVESTMENT TAX CREDIT

(f) Profit Motive Requirement

p. 1006. Add (i) to the beginning paragraph of this subsection.

p. 1009. Add the following new subsection (ii) before paragraph (g):

(ii) Historic Boardwalk Guidance In January 2014, Treasury and the IRS issued Revenue Procedure 2014-12, 2014-3 I.R.B. 414, which established a safe harbor for federal historic tax credit investments made within a single tier or through a master lease pass-through structure. This guidance was issued in response to the Third Circuit decision in Historic Boardwalk discussed earlier. Although the Revenue Procedure does not establish substantive tax law, it does create a safe harbor for structuring HTC-advantage transactions.201.1

According to the revenue procedure, either an investor may hold a direct partnership interest in the lessor entity that holds fee ownership of the project or, where an election is made by a lessor to pass through the HTCs to the lessee of the project, an investor may hold an indirect partnership interest in the lessor through the lessee, provided, however, that the investor does not also hold any other interest in the lessor.

The guidance makes clear that there is no minimum amount of cash that is required to be distributed to the investor in order to be respected as a partner, so projects that do not generate substantial cash returns can satisfy the upside return requirement of the guidance even if the aggregate cash generated by the investment will not exceed the investor's capital contribution. The investor, however, must receive a reasonably anticipated value, exclusive of tax benefits, commensurate with the investor member's percentage interest in the partnership.

- At least 20 percent of an investor's total expected capital contribution must be contributed to the partnership prior to placement in service of the project and maintained for the duration of the investor's ownership of an interest in the partnership. Moreover, at least 75 percent of the investor's expected capital contribution must be fixed before placement in service. The contribution of the “fixed” portion of the investor's investment may be subject to contingencies such as placement in service, stabilization, or receipt of a Part 3 approval from the NPS. This requirement is intended to establish “downside” risk.

- Funded guaranties are prohibited, and there is a defined range of “impermissible” guaranties. Impermissible guaranties include any guaranty of partnership distributions or other economic return and any guaranty for which the guarantor agrees to maintain a minimum net worth. It is also impermissible for any guaranty of tax structural risk or other disallowance or recapture events that are not due to an act or omission of the managing member or its affiliate. Similarly, no person involved in the HTC-advantaged transaction may pay the investor's costs or indemnify the investor for expenses incurred with respect to an IRS challenge of the HTCs.

- Unfunded guaranties may cover 100 percent of the amount of the HTCs or the capital contributed to the partnership with respect to the HTCs. Unfunded guaranties may also cover all of the loss due to failure to complete the project as well as environmental liabilities. Further, an operating deficit reserve not in excess of 12 months of operating expenses may be established, and an operating deficit guarantee capped at 12 months of operating expenses may be provided to the investor.

- According to the guidance, although a managing member or its affiliates may not hold a “call” option to acquire the investor member's interest in the partnership, the investor may hold an option to “put” its interest to the managing member or its affiliate for an amount that does not exceed fair market value.

The revenue procedure does not address other types of federal or state credits or transactions that combine HTCs with federal low-income housing or federal new markets tax credit transactions.

The guidance provides that the value of the investors' interest may not be diluted by “disproportionate rights to distribute distributions.” Preferred returns and special tax distributions to investors are permitted and, if not paid currently, may accrue. There will need to remain some meaningful amount of variable cash distributions after payment of deferred returns.

The guidance authorizes “flips” in the partnership interest after the end of a five-year HTC recaptured period. At all times, however, the principal's interest must be at least 1 percent of each material item of partnership income, gain, loss, deduction, and credit, and the investor's interest in such must be at least 5 percent of the largest investment percentage of such material items in the tax year for which the investor's percentage interest is the largest.

(g) Recapture Provisions

p. 1010. Add the following at the end of the subsection:

The 2017 Tax Act amended the 20 percent HTC, which now needs to be claimed “ratably” and impacted the application of the recapture provisions. See, in this regard, new subsection 13.4(i).

p. 1010. Renumber the current subsection (h) to (j) and insert the following as new subsections (h) and (i):

(h) The Treatment of 50(d) Income and Qualified Leasehold Improvements

The IRS issued Chief Counsel Advice 201505038, which clarified that, in a lease pass-through transaction, the lessee must include ratably in gross income an amount equal to 100 percent of the HTC claimed (rather than 50 percent).

The IRS plans to issue additional guidance shortly that will clarify various issues, including:

- whether § 50(d) income is an item of partnership income at the lessee level that increases a partner's outside basis in its partnership interest (§ 705(a));

- whether an investor's distributive share of § 50(d) income can be reduced (along with its distributive shares of other partnership tax items) in a partnership “flip” of the kind described in Rev. Proc. 2014-12;

- whether, upon the sale of an investor's interest in the lessee, an investor's share of any unrealized § 50(d) will be accelerated, or whether it would be allocable to the remaining partners in the lessee over the remainder of the applicable recovery period; and

- the consequences of a termination of a lease after the expiration of the HTC recapture period.201.2

Generally, in HTC deals, the recovery period for nonresidential real property is 39 years. There are exceptions, however, including an exception for “qualified leasehold improvement property” (“QLIP”), which has a 15-year recovery period.

QLIP is any improvement to an interior portion of a building that is nonresidential real property, if:

- the improvement is made under or pursuant to a lease, by the lessor, the lessee, or a sublessee of such portion of the building;

- such portion of the building is used exclusively by the lessee (or any sublessee) of such portion; and

- such improvement is placed in service (“PIS”) more than three years after the date the building was first PIS.201.3

(i) The 2017 Tax Legislation and Issuance of the Proposed Regulations201.4

Under the 2017 tax legislation, the 10 percent rehabilitation tax credit was repealed, and the 20 percent HTC discussed in subsection 13.4(b) was modified. The new law amended the 20 percent HTC to require it to be claimed “ratably” over a five-year period. The proposed regulations added sections 1.47-7(a) through (e) to provide rules for calculating the new ratable share and the determination of the HTC. The proposed regulations also coordinate with IRC section 50 (see subsection 13.4(h) with regard to the treatment of section 50(d) income) as well as recapture in the event of a disposition and the income inclusion related to lease property when the lessee is treated as the owner.

The term “ratable share” is the amount equal to 20 percent of HTC determined with respect to the qualified rehabilitated building (“QRB”), as allocated ratably to each taxable year during the five-year credit period. The term “rehabilitation credit determined” is an amount equal to 20 percent of the qualified rehabilitation expenses taken into account for the taxable year the QRB is placed in service. The proposed regulations clarify that the HTC is determined in the taxable year the QRB is placed in service and allocated over a five-year period for each of the next five taxable years, rather than creating five separate rehabilitation credits for a single QRE.

As to the timing, that is, the year the section 50(c) basis adjustment is to apply to investment credit property (in a direct investment structure), the proposed regulations provide examples to clarify the section 50(c) basis adjustment (see subsection 13.4(h)) that is accounted for in the year the QRB is placed in service for the full amount of the HTC determined rather than recorded as the credits are claimed. When the lessee is treated as owner and subject to an income inclusion requirement (in a lease pass-through structure) due to the HTC being claimed over five years, the section 50(d) income, similar to section 50(c) basis adjustment, is also calculated on the full amount of HTC determined in the year the QRB is placed in service and amortized ratably into income over the shortest depreciable recovery life of the QREs that gave rise to the HTC.

As to recapture provisions under section 50(a) (see subsection 13.4(g)), the proposed regulations clarify that there is one five-year tax credit period, which starts from the placed-in-service date of the QREs.201.5 The proposed regulations provide an example to illustrate how to calculate tax credit recapture in the event of a201.6 disposition.

(j) State Tax Credits (as renumbered) p. 1012. Insert the following new paragraphs at the end of this subsection:

The Tax Court maintained this position when it decided SFW Real Estate, LLC v. Commissioner.205.1 The case involved the sale of Virginia state tax credits, and the Court again determined that the sale of the Virginia state tax credits was a disguised sale and the taxpayer was appropriately taxed on the economic benefit of funds received from the sale of the Virginia state tax credits.205.2

In Gateway Hotel Partners, LLC v. Commissioner,205.3 the Tax Court determined that two of the transfers of Missouri Historic Preservation Tax Credits were partnership distributions, but that a portion of the third credit transfer was a taxable sale.205.4 The Tax Court considered whether three transfers made by a partnership resulted in taxable sales under the disguised sale rules, substance over form principles, or otherwise.

In Gateway,205.5 the Tax Court considered whether the transfer of tax credits to an indirect owner of the partnership constitutes income to the partnership. No disguised sale under § 707(a)(2)(B) was found where a partner (Washington Avenue Historic Developer (“WAHD”)) contributed the proceeds of a bridge loan to a partnership (Gateway Hotel Partners, LLC (“Gateway”)) formed to engage in a historic real property development project in exchange for a preferred interest in Gateway and later received a distribution of state tax credits generated by the project. IRS took the position that Gateway was the bridge loan borrower and Gateway repaid the bridge loan by transferring the tax credits. However, the Tax Court found that the borrower was an upper-tier entity that borrowed the funds and then contributed the proceeds to Gateway through several tiers of entities, including WAHD.

The Tax Court then held that the distribution of the tax credits was not a disguised sale because (i) the transfer was made after the two-year period during which transfers are presumed to be a sale under Reg. § 1.707-3(d), so there was a presumption against a disguised sale; and (ii) the facts and circumstances indicated that the transaction was not a sale. In so holding, the Tax Court rejected the IRS's argument that the transfer of the credits was a disguised sale. The Tax Court primarily focused on the fact that the timing and amount of the subsequent transfer of the tax credits was not reasonably certain at the time of the bridge loan contribution and that WAHD/HRI did not have a legally enforceable right to the tax credits: since Gateway could have satisfied WAHD's preferred return with cash, instead of distributing the credits, WAHD had no right to the credits, so its preferred return was subject to the entrepreneurial risks of Gateway's business.

The IRS has listed facts and circumstances, each of which indicates that a transaction is a disguised sale because, at the time of the earlier transfer, the later transfer was not dependent on “entrepreneurial risks” of partnership operations (and, conversely, if the facts and circumstances show that, at the time of the earlier transfer, the later transfer may or may not occur, the transaction will not be treated as a disguised sale):205.6

- The timing and amount of a subsequent transfer are determinable with reasonable certainty at the time of the earlier transfer.205.7

- The transferor has a legally enforceable right to the subsequent transfer.205.8

- The partner's right to receive the transfer of money or other consideration is secured in any manner, taking into account the period during which it is secured.205.9

- Any person has made or is legally obligated to make contributions to the partnership so it can make the transfer of money or other consideration.205.10

- Any person has loaned or agreed to loan the partnership the money or other consideration it needs to make the transfer, taking into account whether any such lending obligation is subject to contingencies related to partnership operations.205.11

- The partnership has incurred or is obligated to incur debt to acquire the money or other consideration needed to make the transfer, taking into account the likelihood that the partnership will be able to incur the debt (including factors such as whether any person has agreed to guarantee or otherwise assume personal liability for the debt).205.12

- The partnership holds money or other liquid assets beyond the reasonable needs of the business that are expected to be available to make the transfer (taking into account the income that will be earned from those assets).205.13

In Gateway, even though WAHD had a disproportionately large allocation of the tax credits and did not have to return the tax credits to the partnership, the transaction was not a disguised sale (i.e., the transaction was not a disguised sale because, at the time of the earlier transfer, the later transfer was dependent on “entrepreneurial risks” of partnership operations).

So long as developers of historic rehabilitation projects recognize the importance of proper documentation and adherence to contractual arrangements, the Gateway decision should provide comfort to developers that their tax reporting of such credits is likely to be respected.205.14 Further note that to avoid recharacterization of such a transfer of tax credits as a disguised sale under the disguised sale rules, real estate partnerships should ensure that partners do not have a right to receive tax credits specifically at a particular point in time.

However, the Tax Court determined that Gateway had sold excess tax credits with respect to a certain portion of the credits transferred. Gateway was not entitled to rescind the transaction since it did not attempt the rescission until the subsequent year. Accordingly, Gateway was required to include as income the proceeds from this transfer. It should be noted that the court imposed a 20 percent negligence penalty with regard to this small portion of the credits determined to have been sold by the taxpayer. The court's determination that the proceeds should have been applied to partnership's income deemed unreported is a warning to taxpayers as to what can happen when the documentation is not complete.

§ 13.6 NEW MARKETS TAX CREDITS (REVISED)

(b) Allocation of New Markets Tax Credits

p. 1023. Delete the second full paragraph on this page and insert the following in its place:

In July 2020, the CDFI Fund awarded more than $3.5 billion in new markets tax credit allocation to 76 CDEs through the calendar year (CY) 2019 round. The CDFI Fund selected the 76 awardees from a pool of 206 applicants requesting an aggregate $14.7 billion in allocation authority. The award recipients are headquartered in 30 states and the District of Columbia. In their applications, awardees estimated that they would make more than $898 million in total investment in rural areas. Through 16 NMTC rounds, the CDFI Fund has made 1,254 allocation awards totaling $61 billion in tax credit authority.

(d) Allocation Process (Revised)

p. 1026. Delete the second full paragraph on this page and insert the following in its place:

The New Markets Tax Credit (NMTC) program was extended through 2025 with a $5 billion annual appropriation as part of the Consolidated Appropriations Act, 2021, signed by President Trump on December 28, 2020. Before the extension, the NMTC was set to expire at the end of 2020. The NMTC appropriation increased from $3.5 billion per year for calendar years 2010 to 2019 to $5 billion per year for calendar years 2020 through 2025. Additionally, the legislation permits any unallocated funds less than the $5 billion appropriation to be carried forward through 2030, instead of 2025 as under prior law.

(g) Qualified Low-Income Community Investments

p. 1032. Insert footnote 299.1 at the end of the last sentence of the last paragraph on this page.

299.1 See Compliance, Monitoring, and Evaluation FAQs 42, 43, and 44, discussed in subsection 13.6(x), infra.

(i) Qualified Active Low-Income Community Business p. 1036. Insert the following at the end of this subsection:

(v) Exiting the NMTC Transaction: The Unwind

(i) Tax Issues: Use of the A and B Notes by For-Profit QALICBs

(2) RELATED-PARTY ACQUISITION

p. 1064. Insert the following at the end of this subsection:

In a case where an affiliate of the QALICB steps into the shoes of the investor at the time when either the put or the call is exercised, COD income may be generated to the members of the QALICB. Accordingly, the QALICB often looks for alternatives to minimize the impact of §§ 6(a)12 and 108(e)(4)(A). In this regard, it may consider making a charitable contribution of all of its rights, title, and interest under the put/call agreement; however, there is an issue as to whether the members of the QALICB will be entitled to a charitable contribution deduction. Moreover, before accepting the donation a charity would need to get board approval and potentially be prepared to fund the put or call.

It is important to note that debt restructuring, which is common among financially troubled debtors, may have income tax consequences to the QALICB. It may result in a deemed taxable exchange of the old debt instrument for the new debt instrument triggering recognition of COD income. In this regard, § 1.1001-3 of the Treasury Regulations provides various tests to analyze whether debt modification is significant and will often be triggered by changes in yield, changes in payment, and timing, among others. In this regard, a change in yield is most important because it will occur if the yield varies from the annual yield on the unmodified debt (determined as of the modification date by more than the greater of (1) one-quarter of 1 percent (25 basis points) or (2) 5 percent of the annual yield of the unmodified debt (0.05 × annual yield)). See Reg. § 1.1001.

Assuming that the purchaser under the put or call assigns all of its interest to a § 501(c)(3) organization, it may propose to modify the terms, especially in the case where the B Note has more than 20 years before principal is due following the end of the compliance period.

In summary, as to the members of the QALICB, any significant reduction that is a moratorium on annual interest or a deferral of interest payments for a number of years is likely to be treated as a significant debt modification (because it would be greater than 25 basis points or 5 percent of the annual yield). The effect of this may be to trigger COD income to the debtor unless it can be shown that the adjusted payments on the modified debt would not result in a reduced yield over the remaining life of the B Note.

To conclude, there are five alternatives in the event that the QALICB members are unwilling to recognize COD income in the year following the end of the compliance period:

- See the qualified real property business indebtedness exception under § 108(a)(1)(D), discussed in § 13.6(e)(iii)(B); however, the exclusion requires that the value of the property has declined below the mortgage debt; it would also have an impact on depreciation deduction of future years.

- The purchaser may be able to negotiate with the charity a reduction in the annual interest for, say the first five years, with an increase in the rates at the back end of the term, so that the overall yield on the debt remains the same.

- The members may be able to negotiate a deferral as to the exercise date in the put/call agreement with the equity investor—in effect, be able to “kick the bucket.”

- The affiliate could consider contributing its rights to a trust for the benefit of the QALICB members' children, but not only would there be a gift tax issue, but also the trust would be treated as a related party with all COD implications.

- The affiliate could assign the put/call agreement to an unrelated party (at least 50 percent owned by an unrelated party such as a brother-in-law or sister-in-law, with the members' children owning 49 percent or less); however, this would have gift tax implications both at the initial assignment and subsequently if the majority owner attempts to reassign ownership of the B Note to the members at a later date.

(w) Nonprofits' Use of NMTC (Revised)

(ii) Multiple Roles

(B) AS QALICB

page 1071. Insert the following after the last Example:

Nonprofit QALICBs, in contrast to for-profit QALICBs, are more likely to produce human capital amenities including employment training centers, childcare centers, school facilities, and, most frequently, healthcare facilities. Park, open space, and recreation and community centers are the most common quality-of-life amenities, followed by art museums, cultural institutions, and public libraries, all of which are more likely to be provided by nonprofit QALICBs. Project improvements to public infrastructure most often include parking lots and garages sponsored by for-profit QALICBs.374.1

(iii) Board Approval p. 1074. Add the following after the Caveat under this subsection:

Traps for the Unwary. Finally, the board of the charity needs to be educated by counsel with regard to five possible traps for the unwary involving UBIT, an advance agreement to forgive the leveraged loan, the CDE fee structure, the allocation of COD income, and the use of a “straw party” as a party to the unwind.

- There is a potential UBIT concern on exit by the nonprofit charity, after the seven-year compliance period expires, if the project is not “substantially related” to the exempt function of the organization, such as relief of the poor or underprivileged or relieving the burdens of the government. The location in a QCT isn't enough.381.1

- It is critical that there is no agreement in advance that the leveraged loan will be forgiven at the end of the compliance period; otherwise, the basic structure of the NMTC may be defective.

- In most cases, there may be a need for multiple CDEs in order to direct their allocations to the project; it is important that the board of the nonprofit examine the proposed CDE fees because the fees fluctuate and in certain cases may be above market.

- If the QALICB is structured as an LLC with multiple parties or members, including a nonprofit, and is taxed as a partnership, the operating agreement should contain specific language covering the allocation among the partners of the COD income, if any. It is important to define narrowly the section on “Refinancing Proceeds” relative to exercise of a put.

- A straw party should not be used by a QALICB to acquire the equity interest pursuant to the exercise of the put or call. The approach may backfire on the QALICB under the related-party rules (i.e., direct or indirect acquisition of debt, which could generate COD income for the taxpayer).381.2

p. 1075. Delete the last two sentences of the first full paragraph on this page and add the following new subsections after subsection (iv):

(v) Questions a Nonprofit Board Should Consider in the Context of New Market Tax Financing.382.1

- What capital investments is the organization planning over the next 12 to 18 months?

- Real estate development/construction

- Asset purchases

- New lines of business/service

- Capital investments in the ordinary course of business

- Does the organization plan on increasing headcount or services over the next 12 to 24 months?

- Does the organization plan any potential reduction in community services issues over the next 12 months due to lack of funding?

- Does the organization have projects/services that have been postponed or canceled due to capital costs and lack of funding through traditional capital campaign activities?

- The board needs to examine the following issues before approving the structure:

- What is the minimum deal size that is practicable, considering overall costs and recognizing that leveraged funds are difficult to obtain?

- How does the organization go about attracting allocation?

- Deals can take six months or longer, so it may be beneficial to begin as long as a year in advance of an allocation to “market” with prospective CDEs and equity investors.

- Will there be continuity in management during the project development period and compliance period (seven years)?

- Donors to a 501(c)(3) QALICB may want to have certain controls over the project and site selection.

- There is often a perception that pledges are to be used to pay interest rather than providing a new service consistent with the exempt function of the charity.

(vi) Using a Title-Holding Corporation as a QALICB.382.1 A QALICB charter school may use a title-holding corporation both as an asset protection vehicle and as a means of obtaining financing from a CDE in connection with an NMTC transaction.

To finance improvements on the property, the title-holding corporation may borrow funds from a third-party lender. If the title-holding corporation otherwise qualifies as a QALICB, it may borrow the required funds from a CDE as part of an NMTC transaction. The title-holding corporation may use a portion of the rent it receives from Charity A to repay the loan from the CDE. Despite the limitations imposed by § 501(c)(2) of the Code, the activities undertaken by the title-holding corporation in this example—holding a leasehold interest in improved real property in a low-income area, using loan proceeds to improve that property, leasing that property to another party, and paying all remaining income over to Charity A—are consistent with its qualifications both as a tax-exempt organization described in § 501(c)(2) of the Code and as a QALICB described in § 45D(2) of the Code.

p. 1075. Add the following new subsections (x) and (y), after subsection (w):

(x) CDFI Fund Frequently Asked Questions (FAQs) The CDFI Fund has issued a series of New Markets Tax Credit Compliance and Monitoring Frequently Asked Questions (FAQs) since September 2011, by adding, revising, or updating select questions, some of which are highlighted here:382.3

- When a CDE has received principal repayments on a QLICI and reinvests those proceeds in a new QLICI, the new QLICI is subject to the same requirements found in § 3.2 of the allocation agreement (i.e., types of QLICIs, service area, etc.).

To the extent a CDE reinvests repayments of principal as new QLICIs, the CDFI Fund is required to check compliance for all reported QLICIs against the requirements specified in the allocation agreement.

- The six-month cure period is available to correct a CDE's or subsidiary CDE's failure to invest substantially all of its QEI proceeds.

The six-month cure period382.4 is available to correct a CDE's or subsidiary CDE's failure to invest substantially all of its QEI proceeds in QLICIs within the 12-month period.382.5

However, the six-month cure period is not automatically added to the 12-month period. The rules state that the six-month cure period begins on the date the CDE becomes aware (or reasonably should have become aware) of the failure to invest substantially all of the QEI proceeds in a QLICI within the 12-month period. (See FAQ 17.)

- Supporting documentation that an allocatee needs to retain in order to demonstrate compliance with investing in areas of higher distress as reflected in § 3.2(h).

In addition to CIMS, which provides non-metropolitan status, poverty rate, median family income (MFI) percentages, and unemployment rates, the CDFI Fund has provided several links on its website to assist allocations. (See the “Compliance Monitoring and Evaluation” link for details.)

Allocatees are advised to retain all relevant information in support of its decision to invest in such areas. Supporting documentation for the areas of higher distress requirement may include statistical indices of economic distress such as poverty rates, median family income, or unemployment rates at the census tract level based on the 2006–2010 ACS; materials from other government programs (e.g., HUD Renewal Communities or EPA Brownfields) demonstrating the area qualified for assistance under those programs; and others.

The “Compliance Monitoring and Evaluation” section on the CDFI Fund's website has links to the following sites:382.6

- Federally Designated Empowerment Zones, Enterprise Communities, or Renewal Communities

- Brownfield Sites

- SBA-Designated HUB Zones

- Medically Underserved Areas (Department of Health and Human Services)

- Food Desert

- Promise Zone

- All allocatees are required to invest substantially all (generally 85 percent) of their QEIs as QLICIs. Section 3.2(j) of the allocation agreement may require an allocatee to invest an even higher percentage of QEIs (e.g., 95 percent or 100 percent) as QLICIs, based on representations made by the allocatee in its allocation application.

- All allocatees must be able to demonstrate that they initially made QLICIs in the amount specified in their allocation agreements.

- If an allocatee subsequently receives repayments of principal from the QLICIs (e.g., amortizing loan payments), but consistent with applicable IRS regulations does not reinvest these proceeds into other QLICIs, then the allocatee will be treated as fulfilling the requirements of § 3.2(j)—notwithstanding the fact that the allocatee is no longer “fully invested” at the initial percentage.

- If an allocatee subsequently receives repayments of principal from the QLICIs that are sufficient enough to trigger reinvestment requirements under the IRS regulations, the allocatee is required to reinvest those proceeds in the same percentage as is required in the allocation agreement.

- Section 6.9 of the allocation agreement requires CDEs to report Material Events to the CDFI Fund within 20 days of the occurrence.

An updated Material Events Form can be found on the CDFI Fund's website. An allocatee should use this form to identify the nature of the event so that the CDFI Fund can determine whether it is material and affects the CDE's ability to retain certification as a CDE or remain compliant with its Allocation Agreement.382.8

The CDFI Fund defines a “Material Event” as an occurrence that affects an organization's strategic direction, mission, or business operation and, thereby, its status as a certified Community Development Financial Institution (CDFI) or Community Development Entity (CDE), and/or its compliance with the terms and conditions of the Allocation Agreement. The following list provides examples of Material Events that should be reported to the CDFI Fund on the Certification of Material Event Form.

- An Event of Default as that term is defined in Section 8.1 of the allocation agreement, or any event that upon notice or lapse of time, or both, would constitute an Event of Default.

- A merger, acquisition, or consolidation with another entity.

- A change in the Controlling Entity identified in any allocation agreement or where the Controlling Entity will no longer have any ownership or management interest in the Allocatee and/or will no longer have control over the day-to-day management and operations (including investment decisions) of the Allocatee.

- A change in the organization legal status (e.g., dissolution or liquidation of the organization, bankruptcy proceedings, receivership, etc.).

- An event that materially changes the strategic direction, mission, or business of the organization such that the organization no longer meets one or more CDFI or CDE certification requirements such as no longer providing loans or equity investments.

- Changes in business strategy that might have influenced the merits of awarding the application to the extent that such changes result in the allocation use being generally inconsistent with the strategies (including, but not limited to, the proposed product offerings and markets served) set forth in the Allocation Application.

- An event that materially changes the organization's tax and/or corporate structure (e.g., changing from for-profit to nonprofit status).

- An event that results in a change in control of the organization (e.g., control by, controlling relationships, loss of control—as such term is defined in the allocation agreement—by any entity that is a party thereto).

- A change in the composition of the organization's Board of Directors (or other governing body) such that the percentage of the governing or advisory board members representing the organization's Service Area is diminished or altered.

- Relocation of the organization's primary office to another state, which alters the organization's ability to serve or be accountable to its Service Area (based on its most recent certification prior to the relocation).

- A proceeding or enforcement action instituted against the allocatee in, by, or before any court or governmental or administrative body or agency, which proceeding or its outcome could have a material adverse effect on the financial condition or business operations of the allocatee.

- A proceeding instituted against a regulated Affiliate of an allocatee by or before any court or governmental or administrative body or agency, which proceeding or its outcome could have a material adverse effect on the financial condition or business operations of the allocatee.

- A material adverse change in the condition, financial or otherwise, or operations of the allocatee that would impair the allocatee's ability to carry out the authorized uses of the allocation.

- The debarment, suspension, exclusion, or disqualification by the Department of Treasury, or any other federal department or agency, of any individual or entity (or principal thereof) that received any portion of the allocation in a procurement or nonprocurement transaction, as defined in 31 C.F.R. § 19.970.

- The replacement of any key management official(s) (e.g., the Executive Director, the Chief Financial Officer, the Board Chairperson, or their equivalents) who had been named in the Allocation Application.

- The receipt of an Adverse Opinion, Qualified Opinion, or Disclaimer of Opinion in audited financial statements of the allocatee.

- An allocatee may request an amendment to its allocation agreement.

An allocatee may request an amendment to its allocation agreement by submitting a written request on the CDE's letterhead to the CDFI Fund. The request, at a minimum, must:382.9

- identify the name and control number of the allocatee;

- identify the portion(s) of the allocation agreement that needs to be modified;

- state the reasons why the allocatee is making the request; and

- explain the extent to which the proposed modifications are consistent with what the allocatee had proposed in its initial application to the CDFI Fund, and will help to further the goals of the New Markets Tax Credit Program.

The request can be submitted by email to [email protected] with subject line: NMTC: Allocation Agreement Amendment Request. The request can also be submitted by mail to:

- Attention: Compliance

- U.S. Department of the Treasury

- Community Development Financial Institutions Fund

- 1500 Pennsylvania Avenue, NW

Washington, DC 20220

Justification for approving an amendment to an allocation agreement includes, but is not limited to, a determination that the amendment request is:

- consistent with the intent of the NMTC Program statute and regulations and furthers the goals of the NMTC Program;

- consistent with (or not a substantive departure from) the business strategy proposed in the initial application for an allocation; and

- sufficiently narrow in scope that it does not disadvantage other allocatees or other applicants from the same allocation round.

Although an amendment request can be submitted at any time, it must be submitted no later than 90 calendar days before the allocatee needs the determination.

- There are new QALICB use restrictions that relate to QLICI proceeds being used to repay or refinance any debt or equity provider (or an affiliate of any debt or equity provider). Beginning with the CY 2015–2016 round, any debt or equity provider, or affiliate of any debt or equity provider, whose capital was used, directly or indirectly, to fund a QEI may receive QLICI proceeds to repay or refinance reasonable expenditures that are incurred by the debt or equity provider (or affiliate) and that are directly attributable to the qualified business of the QALICB if the expenditures (i) were incurred no more than 24 months prior to the date on which the QLICI transaction closes or (ii) represent no more than 5 percent of the total QLICI proceeds from the QEI.382.10

In summary, of the $1.7 million in documented, reasonable expenditures directly attributable to the qualified business of the QALICB incurred by A, the QALICB may elect to either reimburse the full amount of reasonable expenditures incurred within 24 months of the QLICI closing date ($1 million) or reimburse reasonable expenditures that represent up to 5 percent of the QLICI proceeds incurred at any time prior to the QLICI closing date ($500,000). It may not do both.

The CDFI Fund will need to monitor the restriction on the use of QLICI proceeds to directly or indirectly repay or refinance any debt or equity provider, or affiliate to any debt or equity provider, whose capital was used, directly or indirectly, to fund the QEI required under the CY 2015–2016 NMTC application.382.11

A QALICB may use QLICI proceeds to repay or refinance any debt or equity provider, or affiliate of any debt or equity provider, and to monetize an asset owned by, contributed, sold, or otherwise transferred to the QALICB (or an affiliate of a QALICB) but not including the accreted value of an asset.

Under the CY 2015–2016 round, a QALICB is permitted to use QLICI proceeds only to repay or refinance a debt or equity provider (or affiliate of a debt or equity provider) whose capital was used directly or indirectly to fund the QEI, subject to the provisions referenced in this section. The QALICB may use QLICI proceeds to repay or refinance expenditures incurred by the debt or equity provider (or their affiliate) for the acquisition of any asset contributed, sold, or otherwise transferred to the QALICB to the extent such asset represents a reasonable expenditure directly attributable to the qualified business for the QALICB. However, the amount that can be repaid or refinanced for such an asset is limited to the asset's original cost and not to any accreted value obtained by appraisal or other valuation methods. Such transactions remain subject to the aforesaid 24-month rule or 5 percent rule.

(y) Future of the NMTC Program

§ 13.10 THE ENERGY TAX CREDITS

(a) Overview

p. 1093. Add the following footnote at the end of the second sentence:

402.1 Community solar projects enable low-income residents in the District of Columbia and elsewhere to have access to the benefits of solar energy with the goal of reducing by at least 50 percent the electric bill of low-income households with high energy burdens. The program is part of the Renewable Portfolio Standard Expansion Amendment Act of 2016, funded by the Renewable Energy Development Fund (REDF). Community solar programs allow multiple energy customers to subscribe to the shared solar projects. After solar panels are installed, they convert the sun's energy into direct current (DC) electricity, which is sent to a converter that then converts the DC electricity into an alternating current (AC) so that it can be used in homes and businesses. A meter measures the amount of electricity produced by the solar panels before the electricity is fed into the utility grid. The utility company keeps track of how much electricity (kilowatt hours) is fed into the grid by the solar panels. The value of this electricity provides a cash credit to specified low-income residents' monthly electric bills. Although there are significant challenges in order to implement community solar projects, the innovative program has been developed by Herb Stevens of Nixon Peabody. The author retains a copy of a PowerPoint presentation titled “Innovative Thinking and Lawyering for Community Solar Projects” (March 2017) written by Herb Stevens and Carolyn Lowery, which was presented to a Georgetown Law School graduate tax class, Advanced Topics in Exempt Organization.

p. 1097. Add the following new subsection following subsection (f):

(g) 2015 PATH Act

In December 2015, Congress passed the Protecting Americans from Tax Hikes (PATH) Act, which contained a long-awaited multiyear extension of solar and wind tax credits together with one-year extensions for a range of other renewable energy technologies. Prior to this extension, Congress would only renew the credits in one- and two-year extensions. This discouraged technology development and building of facilities.

The PATH Act amended §§ 48(a) and 48(a)(5)(C) of the Code to provide that the investment tax credit is extended for wind energy facilities beginning construction in 2015 and 2016, subject to a phaseout as follows:

- Credit is reduced by 20 percent for projects that begin construction in 2017;

- Credit is reduced by 40 percent for projects that begin construction in 2018; and

- Credit is reduced by 60 percent for projects that begin construction in 2019.

The Act also amended § 48(a)(2)(A)(i) of the Code to extend the investment tax credit for solar energy projects beginning construction prior to 2022, subject to a phaseout as follows:

- Credit is reduced to 26 percent for projects that begin construction in 2020; and

- Credit is reduced to 22 percent for projects that begin construction in 2021.

In the case of projects that begin construction prior to 2022 and are not placed in service before 2024, the credit is reduced to 10 percent.

p. 1097. Insert the following new section at the end of Section 13.10:

§ 13.11 THE OPPORTUNITY ZONE FUNDS: NEW SECTION 1400Z-1 AND SECTION 1400Z-2431 (REVISED)

Similar431 to the enactment of the New Market Tax Credit, the 2017 Tax Act (Pub. L. No. 115-97) (the “Tax Act”) provided a new provision to encourage economic growth and investment in distressed communities. It provides two main tax incentives to encourage investment in qualified opportunity zones. First, it allows for the temporary deferral of inclusion in gross income for capital gains that are invested in a qualified opportunity fund. The second main tax incentive in the bill excludes from gross income the post-acquisition capital gains on investments in opportunity zone funds that are held for at least 10 years (Act § 13823(a); see also new IRC §§ 1400Z-1, 1400Z-2).

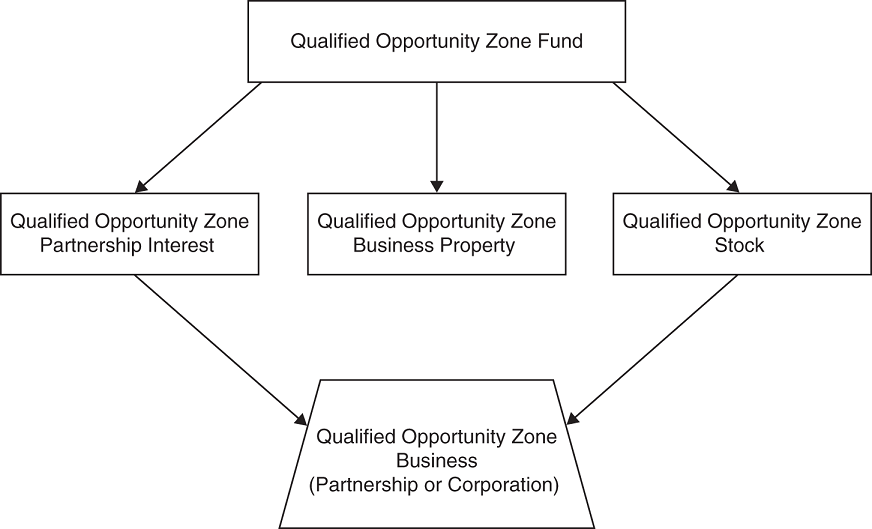

Opportunity funds must be certified by the U.S. Department of Treasury and are required to hold at least 90 percent of their assets in qualified opportunity zone businesses and/or business property.

The definition of low-income community is similar to that used in the new market tax credit structure. Governors are responsible for identifying areas in their states to be designated as opportunity zones. The Tax Act generally allows for 25 percent of the states' low-income community population census tracks to be so designated.

Although opportunity zones are similar to new market tax credits in that they still bring investments to low-income areas, there is a benefit in that total amount of investments that qualify for the subsidy are not limited by annual allocation amounts.

The rules are very technical, and Treasury needs to develop rules on how the Opportunity Funds are certified and meet the criteria. Once that occurs, new capital should begin to flow into the area, similar in effect to the new market tax credit, to incentivize the low-income community.

(a) Introduction

The 2017 Tax Act allows individuals and corporate investors to defer capital gains on the sale of stock business assets or other property (wherever located) by investing in a qualified opportunity zone (which must invest at least 90 percent of its assets, directly or indirectly, in businesses located in designated opportunity zones, i.e., low-income communities). But the deferral does not apply to gains generated on the sale to the fund itself.

The proceeds must be invested within 180 days beginning from the initial sale or exchange in the amount equal to the gain to be deferred. Moreover, there is partial forgiveness of the deferred capital gain if held for five or seven years; and furthermore, any future gain on the investment in an opportunity fund may be excluded if the investment is held for ten years.432

The deferred portion of the gain is taxable when the investment in the opportunity fund is sold or, if sooner, on December 31, 2026, unless the date is subsequently extended. So if the opportunity fund investment is held for 10 years, beyond 2026, the tax basis of the new investment is deemed to be its fair market value on sale. In effect, further appreciation on the investment, but not the deferred gain, is eliminated permanently. As a result, leveraged investments generating depreciation during the hold may not be recaptured. It is important to note that the original property sold need not be located in or connected in any way with a qualified census tract.

This is a remarkable opportunity for high-net-worth individuals to defer gain and subsequently exclude further gain based upon the appreciation of their investment in an opportunity zone. Moreover, and most important, it allows and incentivizes investments in qualified census tracts.

(b) Operations of QOZ Business

An opportunity fund may be sponsored by CDFIs as well as banks that are presently involved in the new market tax credit program as well as other individuals, corporations, or nonprofits. The opportunity fund needs to invest in qualified opportunity zone property (“OZP”), which would include qualified stock, partnership interests, and business property. In all cases, to qualify as an opportunity zone business, substantially all of the tangible assets of the business must be used in an opportunity zone. A qualified opportunity fund must hold at least 90 percent of its assets in qualified opportunity zone properties (which does not include another opportunity fund). The 90 percent requirement is determined by the average percentage of two OZP held by the Fund measured on the last day of the first six-month period of the taxable year of the Opportunity Fund and the last day of the taxable year (for calendar year taxpayer would be June 30 and December 31, but there could be a short-year issue). If the Fund fails the 90 percent test in any year, it is not disqualified but is required to pay a penalty for each month it fails to meet the requirement in an amount equal to the excess of the 90 percent of its aggregate assets over the amount of qualified opportunity zone property held by the Fund multiplied by the underpayment rate under § 6621(a)(2) of the Code. If the opportunity fund is a partnership or a pass-through entity, each partner must pay his proportionate share of the penalty. There is an exception if the opportunity fund can demonstrate that its failure to meet the 90 percent test is due to reasonable cause.

The qualified opportunity zone stock or partnership interest must be acquired from the corporation or partnership by the fund after December 31, 2017, solely in exchange for cash. (It is an equity investment structure.) During substantially all of the holding period of the qualified opportunity stock or partnership interest, the corporation or partnership must continue to qualify as an opportunity zone business.

Similar limitations with regard to the qualified opportunity zone business are based upon the new market tax credit rules relative to active businesses such as the 50 percent of gross income and the limitation on intangibles and nonqualified financial property and “sin” uses. See subsection 13.6(i).

Investments in qualified opportunity zone business property must be tangible property used in a trade or business acquired by purchase (see § 179(d)(2)) in which the related party rules apply, but substitute a 20 percent test instead of 50 percent). Second, and most important, the original use in the qualified opportunity zone must commence with the zone business or the business must substantially improve the property, which means during any 30-month period beginning after the acquisition of the property, additions to basis of the property must exceed an amount equal to the adjusted basis of the property at the beginning of the period. In effect, the improvements must exceed the adjusted basis of the purchase of the property.

(i) Combining with Other Tax Incentives.433

(c) Pairing Opportunity Zone Incentives with NMTCs

Through the NMTC structure, the investor can take advantage of the leveraging structure and generate tax credits over a seven-year period. So not only can the capital gains be deferred for a seven-year period, including an increase in basis with partial forgiveness after five- and seven-year holding periods, but the taxpayer can receive incremental benefit through the tax credit regime. However, the investor is likely to be a C corporation in view of the AMT, which was retained in the 2017 Tax Act as to individuals. Nevertheless, sufficient basis is needed to absorb the required NMTC basis adjustment. Accordingly, the OZ deferral election will generally be limited to the QEI less the sub-CDE fees and the NMTCs that are generated.

(d) Use by Tax-Exempt Organizations: Win-Win

Opportunity funds may be purchased and sold similar to mutual funds. A fund could invest in all aspects of mixed-use development in designated qualified census tracts beneficial to low-income exempt organizations. It incentivizes urban renewal as well as rural development, allowing developers to create and expand communities with new multifamily housing and retail venues.

It may also attract “angel” investors and incubators, along with venture capitalists, thereby attracting companies to locate in opportunity zones, where, after a 10-year hold, a liquidation may generate millions of dollars in capital gains with permanent exclusion from taxation.

There are many reasons why a nonprofit should form joint ventures or a for-profit subsidiary to directly partner with the OZF to operate in the designated low-income high-unemployment zones, consistent with its exempt function. Because the law favors new businesses, new construction, startups, and incubators may be motivated by the incentives. Thus, an opportunity fund could operate or fund a new technology or healthcare business in the zone. A successful tech startup could experience significant growth over a decade, allowing the investor a large permanent exclusion from taxation. Community healthcare and food deserts are also sorely needed in many low-income communities, and walk-in clinics and urgent care facilities, already growing in popularity, may also be attractive projects for opportunity funds.434

(e) Preliminary Steps in Formation of Opportunity Fund

- Formation of Opportunity Zone Fund (OZF) as a corporation or a partnership for purposes of investing in Qualified Opportunity Zone Property (“QOZF”): use of an LP/Query: will an LLC qualify as an OZF?

- General Partner of the LP: formation of the limited liability company; operations of OZF. (See 90 percent test, discussed in subsection 13.11(b).)

- Management Company: formation of the limited liability company that will act as a management company.

- Terms of the Investment Management Agreement.

- Overall fee structure, which needs to be competitive in the marketplace, with return of capital and preferred annual distributions; minimum ten year hold, claw back, etc.

- Confirmation of designation as QCT by Governors, approved by Treasury.

- Self-certification of OZF based upon IRS Frequently Asked Questions. To self-certify, a taxpayer merely completes a form (to be released in summer 2018), which is attached to taxpayer's federal income tax return.

- Preparation of OZF Business Plan (to be reviewed by counsel), including land and building acquisition, timing. Need to “tie-up” properties within designated zones.

- Draft of private placement memorandum.

- Draft of the subscription agreement.

- Review of exemptions under the Securities Act, state blue sky laws, and the Investment Advisers Act.

- Proposed liquidation of fund, cash-out of investors, redemption, etc., after ten years.

(f) Treasury Publishes Opportunity Zone Proposed Regulations

The First Important Step in the Structuring of OZ Funds. As part of the 2017 Tax Act, a new tax incentive program was created to spur economic growth and investment in designated distressed communities (each an “opportunity zone” or “OZ”). Not only does the OZ incentive program allow for the deferral of certain capital gains to the extent that such gain is invested in a qualified opportunity fund (“QOF”), but it also allows for income exclusion for gains on investments in QOFs that are held for at least ten years. While the OZ incentive program was well-received, both practitioners and potential investors had many questions about the program that seemed to be unanswered by the initial provisions provided for in the Tax Act.

As such, on October 19, 2018, the Treasury Department issued additional guidance for the OZ incentive program. Specifically, the Treasury Department issued a set of proposed regulations and a revenue ruling, both of which can be relied on by taxpayers. In addition to the proposed regulations and the revenue ruling, the Treasury Department provided a draft Form 8996, the self-certification form for QOFs, and corresponding instructions for the form. Although the additional guidance answers many questions that investors and practitioners have about the OZ incentive program, there were still a number of unanswered questions, some of which were addressed in the second tranche of guidance issued from the Treasury Department in April 2019.435

A highlight of the guidance from the proposed regulations is as follows:

- Eligible Taxpayers. Taxpayers who are eligible to defer gain under the OZ incentive program are those that recognize “capital gain” for federal income tax purposes. As such, individuals, C corporations (including REITs and RICs), partnerships, common trust funds, qualified settlement funds, disputed ownership funds, and certain other types of entities should qualify.

- Gain Issues. The OZ incentive program provides gain deferral for capital gains only; however, unrecaptured 1250 gain (depreciation recapture) should be eligible for deferral. More IRS guidance is needed to clarify this issue. The gain to be deferred must be gain that would have been recognized (assuming that deferrals under the OZ incentive program were not permitted) no later than December 31, 2026. In the case of a taxpayer who made an election to defer with respect to some but not all eligible gains, the term “eligible gain” includes the portion of the eligible gain for which no election has been made.

The gain to be deferred must not arise from a sale or exchange with certain related persons. Generally, the OZ incentive program adopts the related-party rules found in § 267(b) and § 707(b)(1) of the Internal Revenue Code (the “Code”), except that it substitutes “20 percent” in place of “50 percent” each place it occurs in § 267(b) or § 707(b)(1). For example, a partnership and a person owning, directly or indirectly, more than 20 percent of the capital interest, or the profits interest of such partnership, are considered to be related parties.

Except as otherwise provided for in provisions of the OZ incentive program, the first day of the 180-day period during which an investment of capital gains must be made into a QOF is the date on which the gain would be recognized for federal income tax purposes.

- Gains of Partnerships and Other Pass-Through Entities. A partnership may elect to defer all or part of a capital gain to the extent that it makes an eligible investment in a QOF. If so, no part of the deferred gain is required to be included in the distributive shares of the partners. If the partnership does not elect to defer capital gain, a partner may elect to defer gain with respect to its distributive share under the OZ incentive regime (provided that all other requirements have been met). A partner's 180-day period generally begins on the last day of the partnership's taxable year. A partner may also choose to begin its own 180-day period on the same date as the start of the partnership's 180-day period (in situations in which the partner knows both the date of the partnership's gain and the partnership's decision not to elect deferral).

- Inclusion in Income When Deferral Ends. All of the deferred gain's tax attributes are preserved through the deferral period and are taken into account when the gain is included. If a taxpayer disposes of less than all of its fungible interests in a QOF, the interests that are disposed of are identified using a first-in, first-out method.

- QOF Qualification. A QOF must be classified as a corporation or partnership for federal income tax purposes. Thus, it seems that limited liability companies also should qualify, since Reg. § 1.1400Z-2(d)-1(a) states that it is “qualified as a corporation or partnership for federal tax purposes.” A QAOF must be created or organized in one of the 50 states, the District of Columbia, or a U.S. possession. If organized in a U.S. possession, then an entity must be organized for the purpose of investing in qualified opportunity zone property that relates to a trade or business operated in the possession in which the entity is organized. There is no prohibition to using a “preexisting” entity as a QOF, provided that all other requirements of the OZ incentive program are satisfied, including that QOZ property is acquired after December 31, 2017.

- Investment in QOF. To qualify for the OZ incentive program, an investment in a QOF must be an equity interest in the QOF, including preferred stock or a partnership interest with special allocations (i.e., such investment cannot be a debt instrument within the meaning of § 1275(a) and Reg. § 1.1275-1(d)). Thus, convertible debt should not qualify for the OZ incentive program, but query whether certain types of debt instruments may also qualify, as some of these instruments may be classified as equity for federal tax purposes. Provided that the eligible taxpayer is the owner of the equity interest, status as such is not impaired by the taxpayer's use of the interest as collateral for a loan. Deemed contributions of money under § 752(a) of the Code do not qualify as an investment in a QOF, which is a beneficial result.

- Designating When a QOF Begins. It is expected that Form 8996, the self-certification form, will be attached to a QOF's federal income tax return for the relevant tax years. On Form 8996, it appears that the penalty for nonqualification is calculated monthly, but such penalty does not apply to any months before the first month in which an eligible entity is a QOF. On Form 8996, a QOF is allowed to identify both (1) the taxable year and (2) the first month in that year in which the entity becomes a QOF. If an eligible entity fails to specify the first month it is a QOF, then the first month of its initial tax year as a QOF is designated as the first month that the eligible entity is a QOF. The “first six-month period of the taxable year of the fund” under the 90 percent test means the first six-month period composed entirely of months that are within the taxable year and during which the entity is a QOF. For example, if a calendar-year entity was created in February and chooses April as its first month as a QOF, then the 90 percent test dates are the end of September (which is six months from April 1) and the end of December. This means that if a calendar-year QOF chooses a month after June as its first month as a QOF, then the only testing date for that first taxable year is the last day of the QFO's taxable year. But see the second tranche under subsection (g).

- Valuation Method for Applying the 90 Percent Asset Test. For purposes of the 90 percent asset test of a QOF, the QOF is required to use the asset values that are reported on the QOF's applicable financial statement for the taxable year (namely, a financial statement within the meaning of Reg. § 1.475(a)-4(h), which, generally, includes a financial statement filed with the SEC or one that has significant business use). (But see modification in the second tranche of proposed regulations under subsection (g).) This may present a problem for certain QOFs if GAAP financial statements are used, since GAAP accounting takes into account impairment, depreciation, and so forth, which could strain the 90 percent asset test. If there is no applicable financial statement, then the QOF should use “cost of the asset.” Presumably, this means the original cost basis, without regard for depreciation.

- Working Capital Safe Harbor. A new working capital safe harbor is established for QOF investments in QOZ businesses that acquire, construct, or rehabilitate tangible business property, which includes both real property and other tangible property used in a business operating in an OZ. The safe harbor allows QOZ businesses to hold a reasonable amount of working capital (generally, cash, cash equivalents, or debt instruments with a term of 18 months or less) for 31 months if (1) there is a written plan that identifies the financial property as property held for the acquisition, construction, or substantial improvement of tangible property in the OZ, (2) there is a written schedule consistent with the ordinary business operations of the business that the property will be used within 31 months, and (3) the QOZ business complies with such schedule. Solely for purposes of applying the 50 percent “active” conduct test in § 1397C(b)(2), as required by the definition of a QOZ business, if any gross income is derived from a reasonable amount of working capital, then such gross income is counted toward satisfaction of such 50 percent test.

- Basis Step-Up Election. Taxpayers may make the election for a step-up in their QOF investments after the QOZ designation expires. Specifically, such election is preserved until December 31, 2047 (essentially allowing all QOF investments to qualify for the step-up).

- QOZ Business Qualification. Generally, to qualify as a QOZ business, “substantially all” of a corporation or partnership's tangible property owned or leased must be QOZ business property. In this context, “substantially all” means at least 70 percent. Note that this means that if $100 were invested in a QOF, and the QOF decided to invest through a partnership or corporation, the proposed regulations dictate that a minimum of $63 must be QOZ business property (90 percent × 70 percent × $100). If the QOF operates a trade or business directly and does not invest equity in any QOZ business, then the 90 percent asset test would apply (i.e., $90 must be QOZ property). Thus, there is an incentive for QOFs to invest in a QOZ business rather than holding QOZ business property directly.

- QOZ Stock. Certain redemption transactions will cause stock acquired by a QOF to not be treated as QOZ stock. For example, stock issued by a corporation is not treated as QOZ stock if, at any time during the two-year period beginning on the date one year before the issuance of such stock, the corporation made one or more purchases of its stock with an aggregate value exceeding 5 percent of the aggregate value of all of its stock as of the beginning of the two-year period.

- Revenue Ruling: Exclude Basis of Land. New Revenue Ruling 2018-29 primarily addresses the concept of “original use” as follows:

If a QOF purchases an existing building located on land that is wholly within a QOZ, the original use of the building in the QOZ is not considered to have commenced with the QOF, and the requirement that the original use of the tangible property in the QOZ commence with a QOF is not applicable to the land on which the building is located. If a QOF purchases a building wholly within a QOZ, a substantial improvement to the building is measured by the QOF's additions solely to the adjusted basis of the building. Measuring a substantial improvement to the building by additions to the QOF's adjusted basis of the building does not require the QOF to separately improve the land upon which the building is located.

By excluding the basis of land, the rules facilitate repurposing vacant buildings in QOZs. But see the second tranche of proposed regulations under subsection (g).

- Key Issues Not Addressed. Key issues not addressed in the initial October 2018 guidance include many critical subjects that are described below. There has been further clarification, however, in the second tranche referenced in subsection (g):

- The term “substantially all” is used in various places of the OZ incentive program. For example, for property to qualify as QOZ business property, during substantially all of the QOF's holding period for such property, substantially all of the use of such property must be in a QOZ. Further, for definitions of “qualified opportunity zone stock” and “qualified opportunity zone partnership interest” during substantially all of the QOF's holding period for such interest, such interest is qualified as a QOZ business. What does this term “substantially all” mean as it is used in these other references? See subsection (g), infra.

- How long is the “reasonable period” for a QOF to reinvest proceeds from the sale of qualifying assets without paying a penalty? The OZ incentive program provides that a QOF has “a reasonable period of time to reinvest the return of capital from investments in qualified opportunity zone stock and qualified opportunity zone partnership interests, and to reinvest proceeds received from the sale or disposition of qualified opportunity zone business property.” For example, if a QOF sells QOZ property shortly before a testing date, such QOF should have a reasonable amount of time in which to bring itself into compliance with the 90 percent asset test. See subsection (g), infra.

- In calculating the value of a QOF's assets, Form 8996's instructions allow the use of a certified audited financial statement that is prepared in accordance with GAAP. However, the proposed regulations' requirements are a bit more complex. Additional guidance was necessary to reconcile this conflicting guidance. See subsection (g), infra.

- Will there be any relief for a taxpayer who fails to reinvest eligible gain into a QOF within 180 days of the transaction that produced such gain? Currently, there is no such relief.

- Do section 1231 gains need to be aggregated with section 1231 losses in order to be an “eligible gain”? Section 1231 gains are only capital gains to the extent that they exceed section 1231 losses. See subsection (g), infra.

- There does not appear to be guidance on whether a new building built on unimproved land satisfies the “original use” and “substantial improvement” requirements for QOZ business property. See subsection (g), infra.

- The additional guidance does not appear to address leased property. How such property is accounted for may put pressure on the 90 percent asset test. This subject is discussed in subsection (g), infra.

- How are interim gains—that is, gains recognized at the QOF level—treated? For example, will such gains be eligible for deferral to the extent that they are invested? This subject is answered favorably in the second tranche. See subsection (g), infra.

- Is carried interest a qualifying investment in a QOF? Currently, there is no distinction for interest received for cash versus services. See subsection (g), infra.

- What other information reporting requirements are necessary under the OZ incentive program? For example, what are the forms and instructions by which an eligible taxpayer may elect to defer eligible gains?

- What are some examples that will lead to an entity's decertification as a QOF?

(g) Treasury Publishes the Second Tranche of Proposed Opportunity Zone Regulations

On April 17, 2019, the Treasury Department issued a second tranche of proposed regulations, which again can be relied on by taxpayers. This additional guidance provides answers to open issues related to the definition of “substantially all,” the use of qualified OZ business property, the treatment of leased tangible property, the sourcing of gross income in a QOZ, a reasonable period for a QOF to reinvest proceeds from the sale of a qualifying asset without paying a penalty, and various other topics. However, as was the case with the first set of regulations, there are still a number of unanswered questions (some of which the Treasury Department solicited additional comments on).

A highlight of the guidance from the second tranche of proposed regulations is as follows:

- Qualified Opportunity Zone Business Property. Definition of “Substantially All” for Purposes of Code Sections 1400Z-2(d)(2) and (d)(3). After the first tranche of proposed regulations, the term “substantially all” remained undefined in a number of places in the OZ incentive program. “Substantially all” is clarified to mean (i) 70 percent as it relates to usage of tangible property in an OZ and (ii) 90 percent as it relates to the holding period of tangible property used in an OZ, an interest in stock, or a partnership interest (which qualifies as qualified OZ stock or qualified OZ partnership, respectively).