6

![]()

Home Office: The Misunderstood Key to Saving $15,000 Every Five Years

Tax reform is taking the taxes off things that have been taxed in the past and putting taxes on things that haven’t been taxed before.

—Art Buchwald

Is a home office really worth it? Be honest. Do you believe or have you heard from your accountant that taking a home office deduction isn’t worth the risk or hassle? I’ll bet your answer to this question is yes!

Without question, the home office area has more myths than any other topic. People have told me that they’d heard that they can’t claim a home office because their home is not zoned commercially. The truth is that the Internal Revenue Service (IRS) couldn’t care less about your local zoning. I also have heard with more frequency than I would have believed that “you can’t claim a home office deduction unless you have a back entrance.” I’m not sure what business these people are in!

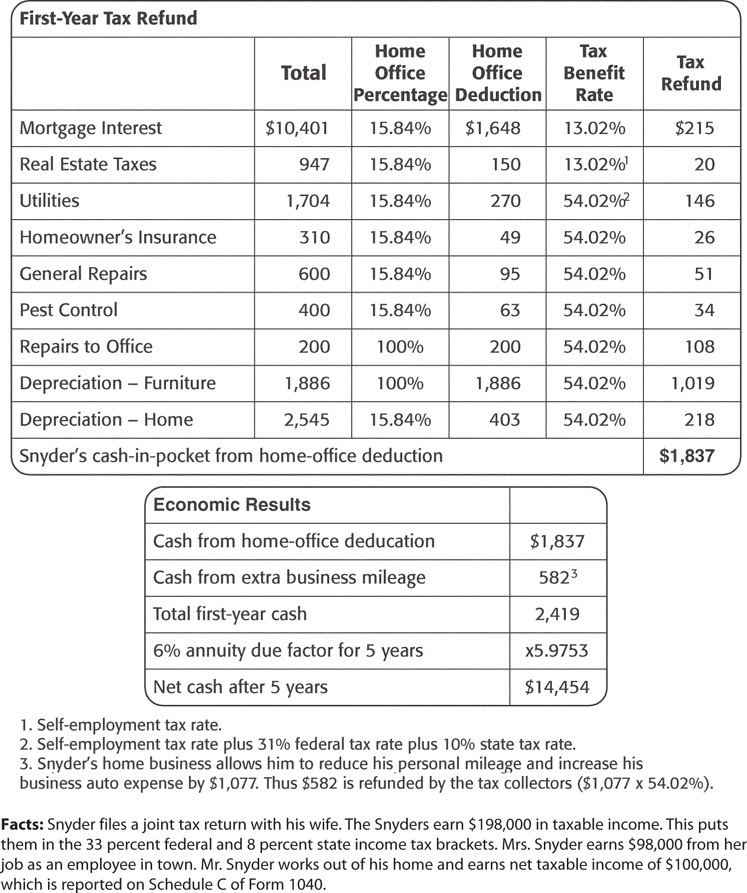

A home office deduction is like having a bunch of pregnant dollar bills—they give birth to many more dollars. If you look at the example for the individual named Snyder, you will see that, based on a $200,000 home, a home office can generate over $15,000 in cash every five years (see Figure 6-1).

Figure 6-1. How Snyder benefits from the home office deduction.

This is based on the fact that you get some new deductions. You can deduct some of your property taxes and mortgage interest as a business expense. You also can increase your business mileage because travel from a qualified home office to a business stop is all business.1 Finally, you get additional deductions that you aren’t normally eligible to get, such as depreciation, some repairs on the home, utilities, and some house cleaning.2 I also have factored in something that most people never think of: interest. I assumed that you could earn a conservative long-term interest rate of 6 percent on your tax savings. My question now is simple: “Assuming that you would qualify for the home office deduction, would an extra $15,000 or more every five years be worth the slight increase in documentation?”

Home Office Rules

![]()

The general rule is that you can’t deduct your home or dwelling unit insofar as it is used as a residence.3 However, if you meet the home office rules, you can deduct some expenses related to your residence. The law states that a home office deduction is available only to the extent that a portion of the dwelling unit (your home) is used exclusively on a regular basis as one of the following:4

• Your principal place of business

• A place of business that you use to meet and deal with patients, clients, or customers in the normal course of your trade or business

• A separate structure that is not attached to the dwelling unit (residence)

• Part of a day-care business

In addition, in the case of an employee, the home office deduction is allowed only if the exclusive use is for the convenience of the employer.5 Although this is a factual issue, if you are an employee, the courts generally feel that this test is met if “you are required by the employer to have a home office or to work out of your home.” Let’s examine these tests.

Qualify by Making Your Home Your Principal Place of Business

![]()

What constitutes a principal place of business has been the subject of a great deal of litigation and controversy. The good news is that this issue went all the way up to the Supreme Court to decide.6 The bad news is that the Supreme Court should never take a tax case because the justices rarely understand what they’re doing in this area.

The court provided two tests for determining whether your home is a principal office.

The first and most important test is, “Where are the most important functions conducted for your business?” For most businesses, it’s where you would see customers or patients or where you render your services.

Example: Doctor Soliman was an anesthesiologist. He rendered his services in the hospital but billed his patients and kept his books from home. The hospital is where he performs his important services.

The second test is a time test. If you work over 50 percent of your total working hours out of your home, then your home will qualify as a principal place of business.

This is important to you because the IRS requires all businesses first to examine where they do their most important functions for their business. If there’s a clear answer, this is the test that is used, and you never resort to the time test.7 Some examples of major factors that the IRS uses would be where you meet your customers, where you render your services, where contracts are signed, etc. Some examples will illustrate the application of the Soliman decision very clearly.

Example: A sales representative spends 30 hours per week taking orders from clients in various stores and spends 12 hours per week working at home on administration for his business. Visiting with clients and taking orders will be deemed the most important functions for his business, and he would not be eligible for the home office deduction under Soliman. Yuck!

Example: Same facts as above, but the orders are placed over the phone, and the sales representative spends 30 hours a week working from his home and 12 hours seeing customers. He would be allowed a home office deduction because the most important business functions occurred at home (selling products and taking orders), and if there was any confusion, he met the 50 percent time test.8

Those adversely affected by Soliman will be people who really perform most administrative duties out of their home and/or put in over 50 percent of their working hours outside the home. Realtors, insurance professionals, financial planners, and many consultants probably will have their home office deductions disallowed because of where they see clients and where they usually perform most of their working activities. The same would be true for most plumbers, carpenters, electricians, etc.

Thus who can take a home office deduction under the Soliman case? Anyone who truly works out of his or her home and performs his or her most important functions at home. This would include network marketers, freelance writers, musicians who do most of their practicing out of their homes, and consultants who do most of their important work out of their homes.

Because the Soliman case eliminated the deduction for many people, Congress passed a great exception to the Soliman case. If you meet this exception, you don’t need to worry about the Soliman requirements. If you don’t meet this exception, you’re back to trying to fit within the Soliman factors.

Exception to Soliman

![]()

Starting in 1999, Congress passed a new exception to Soliman that will help many small-business and home-based business owners. Your home office qualifies as a principal place of business if9

• The office is used to conduct administrative or management activities of your trade or business, and

• There is no other office where you conduct substantial administrative activities.

Thus, if you do your logs, contact patients or customers, listen to educational tapes, read business materials, and prepare bills for customers, you’re rendering administrative activities.

Example: John, a self-employed plumber, spends most of his time in homes repairing and installing plumbing. He has an office at home that he uses exclusively and regularly for his administrative and management activities, such as billing customers, making appointments, and ordering supplies. His home qualifies as a principal office for the home office deduction.10

Example: Eddie, an independent contractor of clothing, meets with clothing store owners in their stores. He shows his new lines and takes the initial orders, which he completes in his home. His home is where he conducts his administrative activities for billing customers, keeping his books and records, ordering supplies, and forwarding orders and reports to his company. Assuming that Eddie uses a room exclusively and regularly for his business, his home office is deemed to be his principal place of business for the home office deduction.

The real congressional “gotcha” is found in the second part of the exception. You can’t have another office where you render any significant administrative or management activities.11 This means that you can have another office, but you just can’t do any substantial administrative services there.12 In fact, even if an office is provided you, you still may claim a home office deduction if you opt to work out of your home and perform all your administrative and management activities out of your home. Thus, if you do some minimal paperwork elsewhere, this won’t disqualify you from the home office deduction.13 This is especially true if you render some administrative or management services at a location that isn’t a fixed office or fixed place, such as a hotel while traveling or a car.14

Example: Edith is a traveling saleswoman. She occasionally writes up orders and sets appointments from the hotel room during business travel. She has no fixed location for performing her administrative or management activities other than in a set spot in her home. She does all her other administrative activities in her home, including finishing the sales paperwork, preparing reports to her company, keeping her books and records, and billing customers whenever credit was declined or a check bounced. Her home qualifies as the principal office for purposes of the home office deduction.

Author’s note: This is a very different result from that of the Soliman case, where both Edith and Eddie would have been deemed to perform their most important functions away from the home. Thus this exception has saved their deduction, as it will save the home office deduction for many small-business owners.

I also should note here that the key is that your administrative and management activities must occur out of your home. Other activities can occur from other locations. Thus, if you meet with clients or customers or you render services such as medical, legal, and plumbing away from the home, these services will not disqualify you from the home office exception.15 The key to the Soliman exception is that your administrative or management activities must occur out of a set spot in your home.

One final point that should be noted is that you can have other companies do some administration for you, and this won’t disqualify you from the exception.16 Thus, if you have a billing company bill your customers, this won’t disallow the deduction.

Qualify by Meeting and Greeting Clients or Customers in Your Home

![]()

If you do not use your home office as your principal place of business, another way to qualify for the deduction is to use the home office as a place to meet or deal with clients, patients, and prospects in the normal course of your business.17 However, this exception applies only if the use of the home office by your clientele is substantial and integral to conducting your business.18 Occasional meetings are insufficient to make this exception applicable.19

Example: A lawyer meets with clients in her office three days a week and in her home two days a week. She qualifies for the exception.

This “meet and greet” test requires a physical presence in your home. You can’t just make phone calls, no matter how extensive or frequent the conversations.20

Author’s note: If you want to use the “meet and greet” exception, I recommend at my seminars that you have your clients, customers, or prospects sign a guest log whenever they come to your home. This log should show who the guest was, the date that he or she visited you, and the reason for the visit. More on this will be discussed below in the section on audit-proofing your home office.

Qualify by Using a Separate Structure

![]()

You may qualify for a home office deduction if, in connection with your trade or business, you use a separate structure not attached to your dwelling unit.21 The separate structure must be used exclusively and on a regular basis for your business.22 (These requirements will be discussed further below.) It need not, however, be your principal place of business or a place where you meet customers or prospects.23 Examples of structures that meet the “separate structure” requirement would be an artist’s studio, a florist’s greenhouse, and a carpenter’s workshop.24

Qualify by Storing Inventory or Product Samples

![]()

A deduction is allowed when you use your home on a regular basis to store either inventory or product samples if you are in the business of selling products at retail or wholesale and if your residence is your fixed location for that business.25 This exception is available to you even if you sell your products at no fixed locations, such as craft shows, flea markets, or a customer’s business premises.

On reading this, you might be tempted to place all your product samples along your hallways and in your bathrooms in order to inflate the deduction (as some tax books and even some companies have recommended). However, the IRS has thought of this trick. The storage of your inventory or product samples must be in a separately identifiable area suitable for storage.26 Moreover, only this separately identifiable storage area would qualify for the deduction.

Example: Jane runs her network marketing business out of her home, where she sells vitamin supplements. She stores her inventory and product samples in a set part of her basement. She may claim a deduction for the space used to store product samples and inventory.

The space used doesn’t have to be used exclusively for storing inventory. It just has to be in a set, identifiable area. Thus, even though Jane uses her basement for occasional personal use, her deduction wouldn’t be denied.27

Finally, this exception applies only to inventory or product samples and not to other business assets. Thus it doesn’t apply to old records,28 law or business books,29 or client or business files.30

Qualify by Running a Day-Care Center in Your Home

![]()

Without question, day care is in big demand and is very encouraged by companies and the government as well. In fact, in terms of deducting home office expenses, day-care business gets slightly better treatment than other small businesses.

The general rule is that a day-care business can deduct a portion of a home that is used regularly in the trade or business of day care for children and adults who are age 65 or older or who are mentally or physically incapable of caring for themselves. The key is that the day care must have applied for or have been granted a state license or be exempt from having a license.31

Author’s note: If you want to claim a home office deduction for a day-care facility, you must comply with state law requirements.

The nice fact about day-care facilities is that you don’t need to use a room or part of a room exclusively for the business.32 In fact, you can use a room for day care during the day and use it for your family or for personal reasons at night and still get a home office deduction. However, the IRS has developed a formula for prorating your business use among the available hours.33

The formula uses two fractions. The first fraction is the square footage used by the day-care facility out of the home’s total square footage. The second fraction would be the total hours in the year that the day care uses the home divided by the total hours in the year, which is 8,760 for a normal year and 8,784 for a leap year. Hours used to prepare for the day care or to clean up after the care is over also get treated as day-care hours.34 Thus it would appear as follows:

![]()

This fraction is the portion of home expenses such as interest, taxes, utilities, repairs, and depreciation that can be deducted on the tax return for the day-care business.

Example: Mary runs a day care out of her home for 12 hours a day, 5 days a week, 50 weeks a year. (Thus she runs the day care for 3,000 hours a year.) She uses 1,200 square feet of the home’s 1,600 square feet for the day care.35 Assuming that her total housing expenses for taxes, interest, depreciation, utilities, garbage, etc. totaled $10,000, the following would be her home office deduction:

![]()

Must Use Your Home Office for Business Regularly

![]()

In addition to one of the business uses that I noted earlier, you must use your home regularly for business. Interestingly, the Internal Revenue Code does not define regular use. However, some courts indicate that regular use means using your home three to four days a week for 10 to 12 hours a week.36 Thus, if you use your home for business less than this, such as four hours per week, your use may not be deemed regular, so your deduction may be disallowed.

You Must Use Your Home Office for Business Exclusively

![]()

With the exception of storing inventory or product samples or running a day-care facility in your home, you can qualify for the home office deduction only for the parts of your home used exclusively for business. This is a difficult requirement for many people. The term exclusive use means just that.37 No personal or other nonqualifying work may occur in the home office area.38 A portion of a room can qualify as a home office, but all business items must be located in the same contiguous area, and there should be some physical separation of the business area from the personal area.39 You must get all personal items out of the home office area other than purely de minimis items such as a radio for music while you’re working, etc.

Author’s note: I constantly get asked whether the IRS actually will come over to your home and check out whether you’re using a portion of the home exclusively for business. The answer is yes, an agent may pay a visit. Get any personal items out of the home office area. Get all nonbusiness books out of the bookshelf in the home office, and don’t play games on the computer. An IRS agent that I know was involved in an audit where the taxpayer kept a convertible couch in his home office. When questioned, the taxpayer admitted that his parents sometimes slept there on occasional visits. His entire home office deduction was disallowed.

What Deductions Are Available with a Home Office?

![]()

In claiming deductions for a home office, you need to break them into three categories:

1. Expenses that are directly related to the home office portion.40 Examples of these types of deductions are painting of the home office or repairing a water leak in the home office. These would be deductible in full.

2. Expenses that don’t benefit the home office either directly or indirectly. These expenses are not deductible because they are clearly not related to the home office in any way. Some examples of these expenses are repairs or painting in another room, plumbing repairs in an unrelated bathroom, and according to the IRS, lawn care if you don’t meet and greet people in your home.41 These expenses are not deductible at all.

Author’s note: Many people believe that in order to take the deduction, you must own your home. This is incorrect. You can deduct the portion of the rent that’s attributable to your home office square feet.

3. Indirect expenses related to the home in general. These include depreciation, costs for a home security system and for monitoring, utilities, repairs and painting to the outside of the house, etc. These expenses get allocated using one of three methods noted below.

Methods for Allocating Indirect Expenses

![]()

There are three methods that you can use to calculate the amount of indirect expenses that you can deduct.

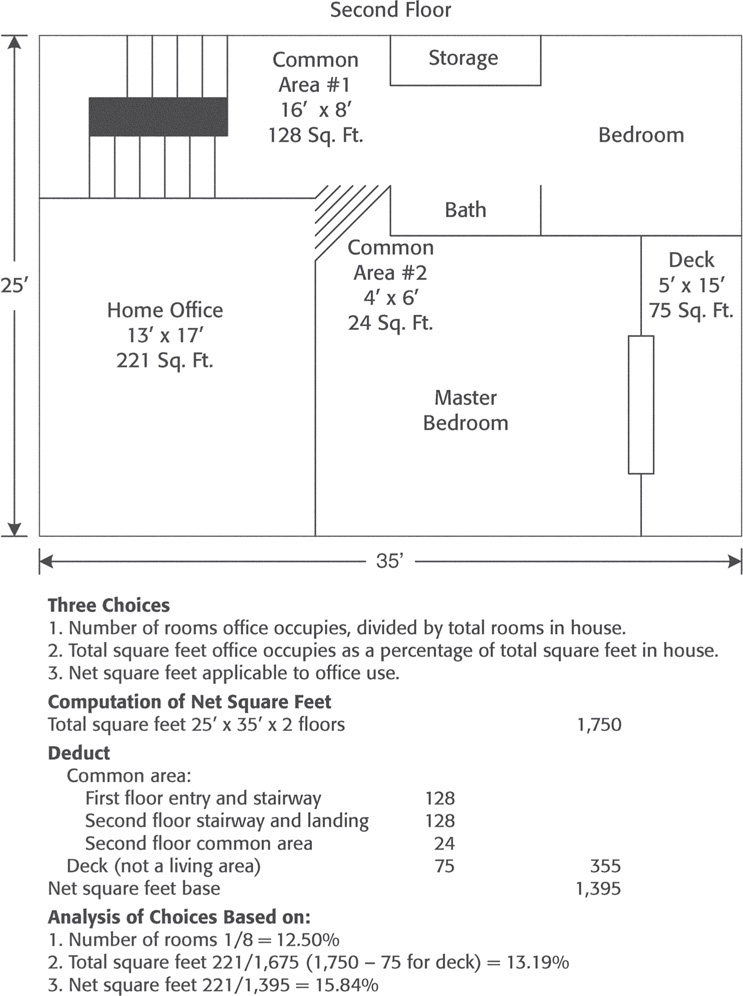

Method one is based on the amount of home office square feet out of the total usable square footage of the house.42 Interestingly, only the usable square feet count, not the total square footage.43 You also can ignore square feet outside the house, such as a deck (see Figure 6-2).

Figure 6-2. Maximizing home office square footage.

Example: You have 1,675 square feet in your home, and your hpome office is 221 square feet. The allocation of your indirect expenses would be 221/1,675 = 13.19 percent.

The second method is known as the number-of-rooms method. You would take the room used for the home office and divide by the number of rooms in the house.44 Thus, if you have eight rooms, and you use one room as an office, you may deduct ![]() , 12.50 percent, of the indirect costs. There’s a catch with this method, however. The IRS allows this method only if your rooms are approximately equal in size and you don’t use a room that’s much smaller than the other rooms.45

, 12.50 percent, of the indirect costs. There’s a catch with this method, however. The IRS allows this method only if your rooms are approximately equal in size and you don’t use a room that’s much smaller than the other rooms.45

The final method, which may be the best method of all, is called the net-square-footage method.46 This is similar to the square footage method, but you subtract from your total square feet of common areas, such as hallways, entranceways, landings, and stairways. In the preceding example, you would have 221 square feet in your home office divided by your net square feet, which would be 1,395. This would result in a deduction of 15.84 percent of your indirect expenses.

Author’s note: I’ve discussed these methods in order to alert you and your accountant to take the approach that results in the biggest deduction. As you can see, in our example, the amount of the deduction will vary from 12.50 percent using the number-of-rooms method to 15.84 percent using the net-square-footage method. This could result in thousands of dollars of extra deductions over your duration of use of a home office.

Starting in 2013,47 IRS has allowed use of a “simplified method” for keeping track of your home office deductions. If you use this method, you would compute the amount of square feet used in a qualifying home office and multiply this figure by $5. This is your total deduction. Thus, if you use a room that has 250 square feet for business, you would get a deduction of $1,250 (250 feet × $5/sq foot).

The problem with this method is that it gives the worst results for taxpayers for several reasons. First, the simplified method is in lieu of any other home deductions including depreciation. You don’t get depreciation. Secondly, the home office rules only allow a home office deduction up to the net income from the business. Any excess can be carried forward to future income. With the simplified method, there is no carryover. Third, you cannot deduct any other home office expenses such as the business use of your interest and taxes in computing your net income from your business. These expenses, however, can still be taken as an itemized deduction. Finally, you must meet all of the home office requirements such as being the principal place of business and use a portion of the home regularly and exclusively. In short, I don’t recommend the simplified IRS method.

Audit-Proofing Your Home Office

Take a Picture

![]()

Take a yearly, dated picture of your home office to establish that it was used exclusively for business. It’s easy to say that you qualified for the home office deduction. However, if you get audited for it, you’ll need some planning to prove that you were eligible in the past. Thus one important bit of documentation that you should have is a yearly photograph of your office to prove that it actually existed and that there were no personal items in the office that would disqualify the deduction. It’s best to use a digital camera because the date of the photo usually is recorded on the picture.

Author’s note: Do not send the photo to the IRS with your tax return. One person did this—and in the photo made some “undesirable” hand and arm gestures! Personally, I thought that it was quite amusing, but the IRS higher management didn’t, and the person got audited.

Keep Records of the Square Footage

![]()

Keep blueprints or other documentation showing the square footage of your home office and the square footage of your home. If blueprints aren’t available, make a drawing of your home office showing the relationship of the home office’s square footage to the total square footage of the home.

Display Your Address and Phone Number

![]()

Use your home office phone number and address on business cards, stationery, and advertising as proof that you actually operated a business from your home. If economically feasible, install a separate business phone in your home. The business phone should be listed in the business’s name in both the White and the Yellow Pages.47 You should have business stationery with your home address on it.48 If you have two business addresses, they should have equal prominence on the stationary.49 You also should use your home address on your business cards.50 If two addresses appear, they should have equal prominence.51 If you have two phone numbers, they should have equal prominence too.52

Author’s note: You would be wise to put in a second business line anyway because tax law allows no deduction for the first telephone line into your personal residence regardless of use.53 Local charges are deductible only if you install a second phone line in your home. Welcome to tax simplification!

I should note that long-distance charges made for business reasons are deductible and should be documented on your bill.

Have Your Business Visitors Sign a Logbook

![]()

If you claim a home office deduction because you use the office in the normal course of business to meet and deal with clients, patients, or prospects, have your business visitors sign a guest book each time they come to your office. The guest book need not be formal, just a record of business contacts who meet with you in your home office. It should contain the name of the guest, the date of the visit, and the purpose. Remember: The burden of proof is on you. If you claim use of your home office to see clients and customers, you must be able to prove that clients, patients, prospects, or colleagues were physically present in your home office.

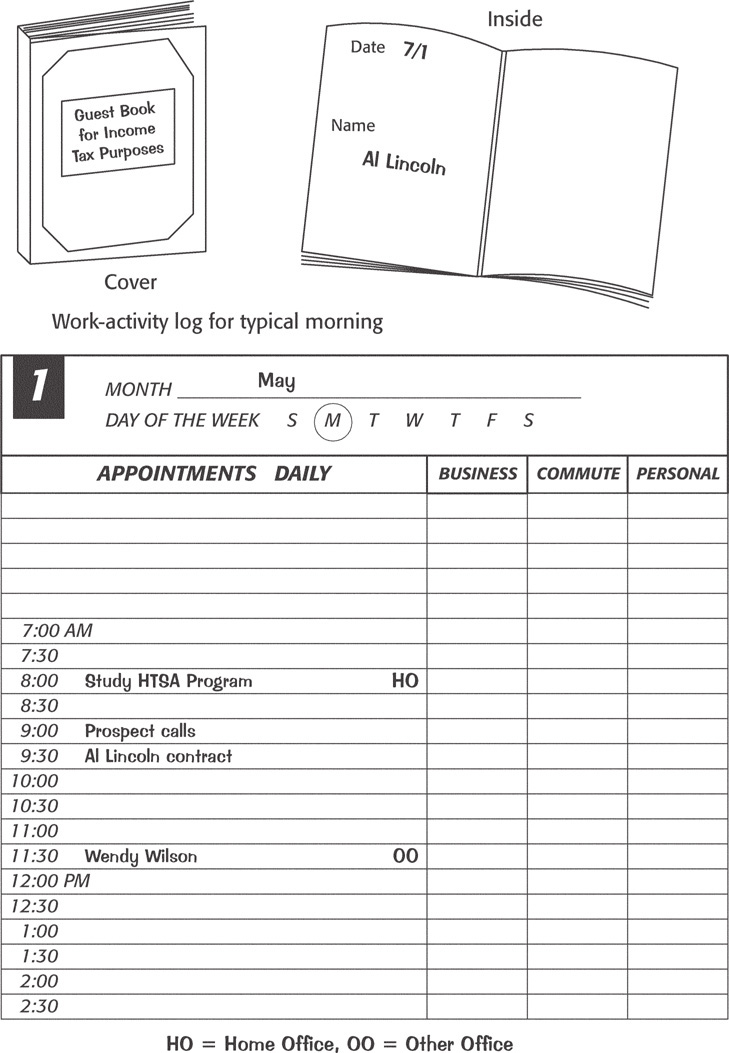

Keep a Work-Activity Log for Time Spent in Your Office

![]()

Showing how much time you spent working in the home office is important because it establishes that you put in your substantial administrative time and worked in the office regularly (at least 10 hours per week). Thus a work-activity log, which could be a meticulously annotated daily diary or tax organizer, constitutes an excellent supporting document to establish where you spent your work time. This does not need to be elaborate. You already have a daily diary. Simply use it as an activity log. If you are working in your home office, you simply could write “home office” (or some abbreviation) and note the time spent there.

Author’s note: I’ve also found that some details that indicate the specific type of work you are doing at home help immensely. See the example in Figure 6-3.

Figure 6-3. Guest book and work-activity log for a typical morning.

Problems with Claiming a Home Office

![]()

As I illustrated at the beginning of this chapter, a home office deduction can be worth thousands to you every year. There are three drawbacks to claiming this deduction. However, most of the drawbacks can be eliminated with some planning or knowledge. Remember my favorite saying, “Where there’s a will, there’s a lawyer.”

1. The Home Office Deduction Has a Gross Income Limitation

![]()

Your home office deduction is the only business deduction that is limited to the net income from the business that is attributable to your home office.54

Example: Alan conducts a home-based business for which he claims a home office deduction. He grosses $6,000 from his business and has $5,000 of business expenses other than for his home office. His home office expenses for his share of the taxes, utilities, interest, depreciation, security monitoring, and garbage collection costs amount to $2,500. He may deduct only $1,000 of these costs because his net income from the home-based business is $1,000 ($6,000 less $5,000 of business expenses). This is the bad news.

The good news is that you don’t lose the excess deductions from the home office because you get to carry them over forever.55 What this means is that you can use the excess deduction against future income from your home business.

Example: In the preceding example, if Alan makes a net profit of $4,000 next year, he may use the unused $1,500 deduction to offset this $4,000 net profit and thus pay tax on only $2,500 in the next year.

2. You Will Have to Pay Tax on Any Depreciation at the 25 Percent Rate

![]()

If you claim a home office deduction, you will be depreciating a portion of your home. This means that you take the home office portion of your residence and deduct the cost over 39 years.56

Example: You paid $200,000 for your home. If you use 10 percent for your home office, then you deduct $20,000 over 39 years at the rate of approximately $513 per year. Thus, if you were in the 35 percent federal tax bracket over all the 39 years, this would save you $7,000.

If you sell your home, you cannot exclude the entire amount of gain on the sale. As a result of the tax simplification law, Congress makes you pick up this depreciation taken after May 6, 1977, as income and taxes you on it at your normal tax rate, but up to a maximum 25 percent rate.57

Example: Karen claims a home office in 1998 and thereafter. If she claims $4,000 in depreciation as a result of the home office, she’ll have to report the first $4,000 of gain on the sale of her home at the 25 percent rate of tax, which means that she would pay back $1,000 on the depreciation taken.58

Author’s note: This may sound bad to you, but it isn’t. If you are in the 31, 36, or 38 percent bracket when you take the depreciation but have to pay it back at only the maximum rate of 25 percent, you’re certainly coming out ahead!

An Employee Can Claim a Home Office Deduction Only if the Office Is for the Convenience of the Employer

![]()

As I mentioned earlier, employees don’t get the same benefits from the tax law that self-employed people get. If you’re an employee, your home office not only must meet all the rules noted earlier but also must be used for the convenience of the employer.59 Thus the home has to be more than just helpful and appropriate for you.60 This means61 that

• Your company must require you to maintain your home office as a condition of your employment, or

• The home office is necessary for the functioning of your employer’s business, or

• The home office is necessary for you to perform your duties.

What all this means is that if your employer provides you with a perfectly good office, you probably can’t claim a home office deduction as an employee. If, however, the office is inadequate for you to perform your functions (if there’s too much noise, if there’s not enough privacy for sensitive work, or if you’re a musician and practice is mandatory), then you can claim a home office.

Author’s note: Frankly, it’s much better for an employee to have a side business and work this business out of the home. However, if you choose not to have a business, at least get a letter from your boss mandating that you work at home and giving the reasons for this directive. Remember: If the IRS feels that the office is for your convenience and not that of the firm, you won’t get the deduction.

Depreciate Furniture and Equipment That You Use for Business

![]()

A major misunderstanding is that the home office deduction applies to all business equipment, too. This is not true. The deduction applies only to the real estate and related deductions, such as interest, taxes, depreciation, utilities, rent, and maintenance.62 Furniture and equipment are depreciable to the extent you use these items for business. You do not need to claim a home office deduction in order to deduct your furniture.63

Example: You work in an office in your home but do not qualify for the home office deduction because the office is not used exclusively for business. Your work adds up to 80 percent of the use. The result is that you may depreciate the furniture and equipment such as the desk, the chair, the computer, the carpeting under the desk, and the lamp lighting up the desk.

Author’s note: This applies even if you’re an employee taking work home. If you use a desk 80 percent for business, you may depreciate that desk.

Now that you are aware that you can depreciate furniture such as desks, chairs, file cabinets, and computers, the question becomes, “What do you depreciate?” The answer is that if you purchased the desk, the chair, the file cabinet, and the computer several years ago, you may start to depreciate those items under what is known as the lower of cost or fair market value rule.65

Example: You have an antique desk that you purchased three years ago. It cost you $500 but has a current fair market value of $600. (Antiques tend to appreciate.) If you use the desk 80 percent for business, you may depreciate 80 percent of the original cost of $500, which is the lower of the cost or fair market value.

Required Record Keeping

![]()

You’ll need to have some reasonable method for determining your business use. With bookcases and file cabinets, it’s easy to determine business use. If you have three file drawers, of which you use two strictly for business files and one for personal files, then you can depreciate two-thirds of the file cabinet. Similarly, if you have a bookcase with four shelves, of which three are for business books and one for fiction, then you can depreciate three-fourths of the bookcase.

With desks, chairs, and computers, it becomes tougher. You want to keep records of use for three consecutive months, as you would do with your automobile, by documenting what you or your family members do when using the furniture.66 The following is an illustration of what I would do for some sample days out of the three months.

On Monday, no one uses the room, so you write down nothing. On Tuesday, you made client calls from 6 to 9 p.m., so you note in your log “made client calls 6 to 9 p.m.” On Wednesday, your son plays the game EverQuest from 3 to 7 p.m., so you log “game or personal use 3 to 7 p.m.”

Keeping this log will show what percentage you can deduct your desk, your chair, your computer, your rug, and your lamps. Thus, if you use this furniture 150 hours for business out of 200 hours during the three-month test, you could depreciate three-fourths of these items.

Expense New Equipment Instead of Depreciating

![]()

There are, in effect, three methods of depreciation. Yes, you read that correctly! You can depreciate computers and monitors over five years and furniture over seven years. The second method, which is known as a Section 179 expense election (named after the code section that allows this), allows you to deduct the cost of the equipment immediately, rather than depreciate, up to $500,000 in 2016 and thereafter and $25,000 for sport utility vehicles (SUVs) used in business.

The equipment must be new to you.67

Example: You buy a new computer, monitor, and printer for $2,500 and a used shredder for $1,000. (Shredders are popular in Washington and Houston.) You may depreciate the computer equipment over five years and the shredder over seven years, or you may elect to write off the entire $3,500 purchase in the year that you buy the equipment.

Author’s note: You may make this election on most items of business equipment but not equipment used for investment purposes. Some examples of equipment used in business include desks, computers, printers, faxes, shredders, lamps, chairs, throw rugs, cell phones and phone systems, etc.

Warning: If you expense an asset but your business use drops to under 50 percent or less during years that it would have taken to depreciate the asset, you must recalculate the original expense amount as if you had claimed the straight-line depreciation and then report the difference as taxable income.68 Thus, for computers, you must keep the business use above 50 percent for five years, and for other office equipment, you must keep the business use above 50 percent for seven years.

What if You Purchase over $500,000 Worth of Equipment?69

Let’s say that you want to purchase more than $500,000 worth of equipment in 2016. You can elect to write-off up to $500,000 and depreciate the difference.

![]()

Author’s note: This may sound like a great benefit, but with tax rates going up, it is questionable whether you want to take the deduction in the year of purchase rather than depreciate over five to seven years. Higher tax rates mean bigger benefits from deductions. One final point that I want to make regarding the expense election is that you actually must elect on your tax return to expense rather than depreciate. You would actually check off a box on your tax return noting that you make an election to deduct up to $500,000 of equipment in 2016. You don’t just take the deduction without the election. Many people make this mistake—to their dismay when the IRS finds out.

Author’s note: If you buy over $2,000,000 of equipment in 2016, the $500,000 election phases out dollar-for-dollar over $2,000,000 in equipment purchases. Thus, if you buy $2,100,000 worth of equipment, you can only elect to write-off $400,000

Summary

• A home office deduction is a tax-deductible gold mine. If you’re eligible, you should clearly take the deduction. Earning over $15,000 every five years should convince you that it’s worth the trouble.

• The best ways to ensure a home office deduction are to use your home as a principal place of business or where you meet and greet customers in the normal course of business, have a separate structure that isn’t attached to your home (such as a greenhouse or an art studio), use your home to store inventory or product samples, or run a day-care center.

• Audit-proof your home office by taking yearly pictures, keeping blueprints of the home that clearly show your home office square footage, and having business cards, stationery, and Yellow Pages listings of your home office address and/or phone number.

• Deduct all expenses for equipment that you use in your home for business, even if you never claim a home office deduction.

Notes

1. See Chapter 5 for this discussion and for the footnotes.

2. See IRS MSSP, Child Care Providers (3/2000).

3. Section 280(A)(a) of the IRC.

4. Section 280(A)(c)(1) of the IRC.

5. Section 280(A)(c) of the IRC.

6. Commissioner v. Soliman, 506 U.S. 168 (1993).

7. Revenue Ruling 94-24, 1994-1 CB 87 and IRS Publication 587 (2001).

8. IRS Publication 587 (1998).

9. Section 280(A)(c)(1) of the IRC.

10. IRS Publication 587 (2001).

11. Section 280(A)(c)(1) of the IRC.

12. Section 280(A)(c)(1) of the IRC and IRS Publication 587 (2001).

13. H. Rept.105-148 (PL 105-34), p. 407.

14. IRS Publication 587 (2001).

15. H. Rept. 105-148 (PL 105-34), p. 407, and IRS Publication 587 (2001).

16. Ibid.

17. Section 280A(c)(1)(B) of the IRC and Section 1.280A-2(c) of the ITR.

18. Section 1.280A-2(c) of the ITR.

19. Section 1.280A-2(c) of the ITR. See also IRS Publication 587 (2001), p. 6.

20. Ibid. See also Green v. Commissioner, 707 F.2d 404 (9th Cir. 1983).

21. Section 280A(c)(1)(c) of the IRC and Section 1.180A-2 (d) of the ITR. See also IRS Publication 587 (2001), p. 6.

22. Ibid.

23. Ibid.

24. IRS Publication 587 (2001).

25. Sections 280A(c)(1)(c) and 280A(c)(2) of the IRC.

26. Section 1.280A-2(e)(2) of the ITR.

27. IRS Publication 911 (2000), p. 5, and IRS Publication 587 (2001).

28. Lloyd Pearson, T.C. Memo 1980-459.

29. James Druker, 77 T.C. 867 (1981).

30. Thomas L. Borom, T.C. Memo 1980-459.

31. Section 280A(c)(4)(B) of the IRC.

32. S. Report No. 95-66 (P.L. 95-30), p. 91.

33. Section 280A(c)(4)(c) of the IRC; IRS Publication 587, p. 10. See also Revenue Ruling 92-3, 1992-1 C.B. 141.

34. IRS MSSP, Child Care Providers (3/2000), p. 12.

35. This example was taken from Revenue Ruling 92-3, 1992-1 C.B. 141.

36. Green v. Commissioner, 78 T.C. 428 (1982) rev’d on another issue, 83-1 USTC Par. 9387 (9th Cir. 1983).

37. Section 280A(c)(1) of the IRC.

38. Hamacher v. Commissioner, 94 T.C. 348 (1990). See also Section 1.280A-2g(1) of the ITR.

39. Gomez v. Commissioner, 41 T.C.M. 585 (1980); Section 1.280A-2(g) of the ITR.

40. Section 1.280A-2(i)(5) of the ITR.

41. IRS Publication 587 (2001).

42. Section 1.280A-2(i) of the ITR and IRS Publication 587 (2001).

43. Ronald Culp, T.C. Memo 1993-270.

44. Section 1.280A-2(i)(3) of the ITR. See also Gene Moretti, T.C. Memo 1982-552.

45. IRS Publication 587 (2001) and Revenue Procedure 2013-13.

46. IRS Publication 587 (2001).

47. Rev. Proc 2013-13

48. Jackson v. Commissioner, 76 TC 696 (1981); Heuer v. Commissioner, 32 TC 947 (1959).

49. Ibid.

50. Ibid.

51. Ibid.

52. Ibid.

53. Ibid.

54. Section 262(b) of the IRC.

55. Section 280A(c)(5) of the IRC.

56. Ibid.

57. Section 168(c). See also IR-2008-117.

58. Section 121(d)(6) of the IRC.

59. Section 121 of the IRC.

60. Section 280A(c)(1) of the IRC and IRS Publication 587 (2001).

61. IRS Publication 587 (2001).

62. Hamacher v. Commissioner, 94 T.C. 348 (1990).

63. IRS Publication 587 (2001), p. 2.

64. Section 280 of the IRC and Mulne v. Commissioner, T.C. Memo 1996-320.

65. Section 1.167(g)-1 of the ITR. See also IRS Publication 551 (1992).

66. Section 1.274-5T(c) of the ITR.

67. Sections 168 and 179 of the IRC. See also Small Business Jobs Act of 2010, 9/27/10.

68. IRC Section 179(d); and IRS Publication 946 (2010), p. 15).

69. Section 280F(d)(1) of the IRC and IRS Publication 587 (2001).

70. American Taxpayer Relief Law.