Appendix C

![]()

Health Savings Account

Overview: A health savings account (HSA) requires a trust to be set up for paying qualified medical expenses. The contributions are deductible, and the payments for these qualified medical expenses are tax-free.

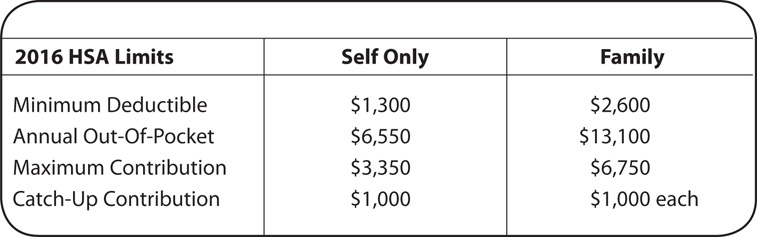

Qualifying: You must use the HSA proceeds for qualified medical expenses. In addition, you must have a high deductible medical policy.1 A high deductible plan is one whose annual deductible and out-of-pocket expenses are as follows:2

Caution: You can’t have another medical plan that covers your deductibles. Thus, if you have a plan, such as Aflac, that pays for sickness and injuries, this may disqualify your HSA. However, you can have a plan that pays for specific types of diseases such as cancer, and you can have a plan that pays for daily stays in hospitals. In addition, you can have a self-insured medical plan, flexible spending account, or cafeteria plan in addition to the HSA if these plans have at least the same deductibles as the HSA.

Observation: In my opinion, the self-insured medical plan is still the better option since you don’t need a high deductible policy, don’t need to set up a trust with yearly fees paid to financial institutions, and don’t have any dollar limitations on contributions other than the fact that the payments must be reasonable for the hours and work performed. An HSA, however, might be advisable if you are single and don’t have a C corporation or you don’t want to hire your spouse in your business in order to utilize the benefits of the self-insured medical plan for yourself. Frankly, I have an HSA setup for my family that works very well.

Notes

1. Section 223(b)(3)(A) of the IRC.

2. Section 223(c)(1)(A) of the IRC and Rev. Proc. 2008-66, 2008-45 IRB.

3. Section 223(g) of the IRC and Rev. Proc. 2011-52.