CHAPTER 5

Price Management

If the approach a firm takes to attract customers in the face of competition is considered its business strategy; and the manner in which prices are positioned, structured, and managed to accomplish the business strategy is considered a pricing strategy issue, then we still have to move from these lofty direction-setting goals to actual execution. Price management converts the firm’s business and pricing strategy into action.

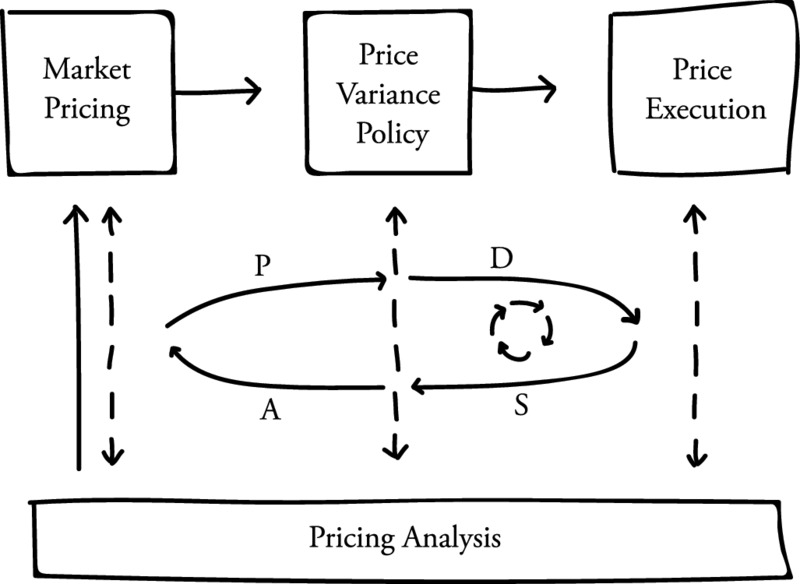

Price management can be disaggregated into three types of challenges supported by a fourth challenge. These three types of challenges are market pricing, price variance policy, and price execution. To inform the price management challenges with facts, as well as to inform pricing strategy and perhaps even business strategy, there are pricing analytics. Pricing analysis underlies all the aspects of pricing, as shown in the Value-Based Pricing Framework.

Market pricing refers to the setting of the list price or margin, or at least the target price or margin, of an offering within a specific market. This is far more detailed and specific work than pricing strategy itself. In contrast, while pricing strategy may define where the offering is to be positioned relative to the competing alternative, market pricing converts that decision into a specific number. And whereas price segmentation may define an overall price structure, market pricing puts numbers to the price structure’s parameters.

Price variance policy refers to the determination of the specific types of price promotions to be offered, price discounts to extend, and the conditions or timing in which these price variances will be allowed. If the pricing strategy allows for price variances, these variances must be managed. And, if the competitive pricing strategy mandates the conditions for reacting to competitive pricing actions, price variance policy can be used to fine tune prices in response to situational changes in the competitive pricing landscape.

Price execution refers to the extending and collecting of specific prices from individual customer purchase decisions at the transactional level. Price execution takes the market-level pricing and the price variance policy from the drawing board to implementation at the customer interaction level. In business markets, it encompasses proposal development, negotiated deal prices, billing and invoicing, accounts receivable and payments collection, and so forth. In consumer markets, it encompasses coupon redemptions, receipting, cash and credit management, rebating, and so forth.

The purpose of the pricing analysis function is to inform pricing decisions across the firm. Through pricing analytics, firms aim to ensure that the right prices are extracted at the right time from the right customer. Pricing analytics informs price variance policy regarding the impact of the discounting and promotions, the variation in prices extracted from the market, and the impact of price variances on customer behavior and purchase decisions. Pricing analysis informs market-level pricing through market research regarding the competitive situation, the offering’s differential value, and variations in a customer’s price and benefits sensitivity by market segment. And, pricing analysis supports strategic decision-making by guiding pricing strategy, clarifying customer demands, and monitoring competitive actions within the industry (see Figure 5.1).

Figure 5.1 Price Management Functions

SaaS Company’s Pricing Challenge

To demonstrate how leading firms are coordinating the price management function, let us consider a business-to-business Software as a Service firm we will call SaaS Co. to protect its identity.

SaaS Co. had grown rapidly to over $100 million in revenue and held the dominant market share in a highly concentrated market with only one significant competitor. Its offering was targeted to a very specific set of clients seeking to address a very specific need. Prior to SaaS Co.’s offering, the target market would address this need in a physical bricks and mortar approach. With SaaS Co.’s offering, the same market need could be addressed digitally from any place in the world and at a significantly lower cost.

Through its rapid growth phase, SaaS Co. had used a price structure and price point that addressed the needs and behaviors of the early target market demand. The market growth through the introduction phase into the early maturity phase was driven largely by the cost savings achievable through SaaS Co.’s approach. And, as the market was reaching early maturity, new market demands were being identified that could be profitably addressed through SaaS Co.’s core offering.

Unfortunately, SaaS Co.’s historic price structure and price points were misaligned with the needs and willingness to pay of many of the newer market segments. In some cases, the predetermined price was too low, which meant SaaS Co. was leaving money on the table in these transactions. In other cases, the price was too high, which resulted in either lost deals or highly unpredictable discounting.

To manage this misalignment between the stated market pricing and the real market demand, the sales department had been authorized to adjust prices based on its understanding of customers’ willingness to pay for individual transactions. This approach kept revenues growing, enabled SaaS Co. to be nimble and flexible in meeting customer needs, and kept SaaS Co. in a dominant market share position.

Yet, as the industry was maturing, this approach to pricing was no longer tenable. Prices at the transaction level began to bear little resemblance to prices expected at the market level.

Finance needed more regularity and predictability with respect to pricing, contract management, customer billing, and revenue. Sales management found itself constantly managing requests for price variances when it really wanted to spend its time developing new markets. New salespeople found it difficult to understand what price they should charge specific customer transactions and when they should request a price variance. Product management had difficulty predicting how important new product features were. And new product uses and geographical markets brought new pricing challenges of their own.

Senior executives were aware of the growing tangible and opportunity costs of these operational challenges and sought more predictability in revenue forecasting. They didn’t want to lose market share to their major competitor nor did they want to discount so much that they were leaving money on the table with each transaction. To address their operational and forecasting challenges while continuing their revenue growth in the face of competition, senior executives at SaaS Co. resolved to improve their price management function and reconsider their pricing structure. Executives from operations, sales, marketing, and finance were engaged with them to identify and drive the necessary improvements.

Market Pricing

Market pricing sets prices for every offering of the firm. This includes reviewing prices of existing offerings, updating prices on enhanced offerings, and setting the go-to-market price of new offerings.

Market pricing determines the specifics of the business and pricing strategy. These issues include the specific price for a specific offering in a specific market. Whether the business strategy requires optimizing profits today or investing to create higher profits tomorrow, market pricing sets prices to achieve the desired business goal.

Market prices are usually set on the timescale of once-per-year as part of the annual planning cycle but may be made more or less frequently depending on the industry dynamics and the firm’s capabilities. Between market pricing cycles, most variations in customer demands and competitive actions are addressed through price variance policy. In the extreme cases where dramatic shifts have occurred in the market, more frequent updates to the market-level pricing may be necessary. Updates to market prices may be triggered by the firm adjusting prices to reflect inflation or changes in input costs, reacting to competitive moves, attempting to drive industry practices toward healthier outcomes, identifying new customer demands or changes in willingness to pay, or reacting to an economic shock that disproportionately favors some competitors over others.

A particularly twitchy form of market pricing is dynamic competitive pricing. In dynamic competitive pricing, prices are updated daily, if not hourly, to reflect the prices of the competition. The goal of dynamic competitive pricing is to consistently be the lowest priced source in the market or to hold a consistent price differential. Dynamic competitive pricing is generally ill-suited for most firms as it generally results in lower prices, both for the firm and the industry, and lowers profits. Yet, firms pursuing market share as a business strategy find this approach to market pricing attractive. Even the airline and hospitality industries, which use revenue (yield) management, a form of dynamic pricing, don’t update prices themselves as often as firms using dynamic competitive pricing (though they do update fare class availability up to multiple times a day).

For most industries, market pricing results in list prices. In certain industries, such as manufacturing and distribution, market-level pricing might imply list margins rather than actual prices as input costs vary widely over the year. Some firms use target prices and margins rather than list prices, allowing price variances at the transaction level to be both above and below the determined target price. The target pricing approach, rather than the list pricing approach, is defended by the need to have the flexibility to react to individual customer situations. Unfortunately, the target pricing approach, rather than the list pricing approach, is also associated with increased organizational complexity, a higher risk of pricing errors, and the inability to signal to customers through the price itself broadly accepted price expectations.

For price structures that extend beyond basic per-unit pricing, market pricing defines the scalar parameters used in the price structure to determine customer-level pricing. For instance, in a strategic price bundling strategy, market pricing might both adjust the prices of the individual products upwards while identifying the price of the bundle to be less than the sum of the individual offerings within the bundle but higher than any single offering within the bundle. Or, if a software offering for retail is adjusted based upon the square footage of retail space, market pricing would determine the price to charge is per square foot of retail space.

Market research and analysis are the primary tools used to set market prices. For pricing, the three primary research methodologies used are (1) modeling the exchange value to customers, (2) surveying customers through conjoint analysis, and (3) statistical analysis of transactional data to uncover opportunities to adjust prices. The specific methodology a firm should use is dependent upon its industry, customer base, and offering. All three approaches aim for the same goal of identifying the prices that would optimize profitability or otherwise achieve the pricing strategy of the firm.

The value of market research is in clarifying uncertainties, validating or invalidating assumptions, and otherwise enabling market prices to be set with greater accuracy. It can reveal how the average customer within a market values the firm’s offering, as well as variations in willingness to pay between different customers or customer segments. Market research can identify what drives or undermines value for customers. It can also detect the price sensitivity of customers to different benefits and brands as well as the price sensitivity of the market overall.

To efficiently and effectively drive the necessary market research, determine the pricing parameters, engage the concerns and interests across the organization, reach the goal of setting prices aligned with the business strategy, and then repeat the effort periodically, market pricing needs to be a process. Moreover, because market pricing impacts the entire performance of the organization from sales to operations, product management, and finance, much of the organization may need to be at least informed of, if not engaged in, the market pricing effort.

Historically, market pricing has been considered the responsibility of product management or market research. Recent research has demonstrated that firm-level profits improve when market pricing decisions include the input from the broader executive leadership, such as sales, finance, and others, despite the added effort such engagement entails. As such, engaging the larger organization in the market pricing effort is advised, even in fast changing industries.

Who specifically needs to be engaged in the decision? What research or customer facts will be gathered to inform the decision? How will market facts be shared across the decision-making team? What members of the organization need to provide input into the decision? Which managers need to be informed of the decision? And who will actually make the decision? These are all part of the managerial challenges in defining the market-level pricing process.

SaaS Company’s Market Pricing

At SaaS Co., executives were open to reviewing their pricing structure and committed to improving their list price definition. Sales, product marketing, and finance wanted to come to agreement on these issues, but each held different viewpoints on what was necessary and each held different domains of knowledge. Three forms of analysis were undertaken to reveal the facts, clarify reality, and drive an aligned decision that managers from sales, marketing, finance, and operations could recommend to the senior executive committee.

First, historical transaction data was mined to uncover patterns related to transaction pricing and customer demand. This analysis helped to identify the price levels accepted within the market and the variation in prices within the market. Importantly, some of these price variations could be correlated with customer usage data to support the development of a new price structure. It also helped to clarify the challenge with the current price structure and, using market simulation techniques, identify parameters within a new price structure that would have minimal impact on prices overall. This is important, for if executives wanted to raise or lower prices, they needed to know exactly how the new price structure should be adjusted to reflect their decision.

Second, discussions with executives from sales, marketing, finance, and operations were held to reveal their beliefs, concerns, and goals for SaaS Co.’s offering. In combination with the facts gathered from data mining, these cross-functional discussions quickly revealed management’s beliefs, enabling them to see the challenge and opportunity from a different perspective, and identify a path toward a better market pricing.

Third, to validate assumptions and clarify uncertainties using the customer’s viewpoint, direct customer interviews were held. These confirmed or corrected many of the managerial suspicions regarding the challenges created through the past price structure, clarified how the proposed price structure would address transactional level challenges, and created a picture of the customer viewpoint on SaaS Co.’s offering in comparison to its competitors’.

With the decisions informed and validated through customer research, the pricing team made recommendations to the senior executives, which included representation from legal and information technology along with sales, finance, marketing, operations, and the CEO. Once approved, SaaS Co. had a new price list to which product management, sales, finance, and operations were aligned and one that senior executives were confident would improve revenue predictability, reduce the challenges of managing price variances, and potentially even improve sales volumes and transaction prices.

This market pricing governance policy was documented to enable SaaS Co. to implement elements of it in future market pricing cycles.

Price Variance Policy

Price variance policy determines the rules for discounts and promotions. The moment market prices are set, someone is going to ask for a discount. At the strategic level, firms will decide if price variances are allowed or not. Price variances need not always be shunned, but if they are allowed, they must be managed. If price variances are allowed, the price variance policies determine the type of price variances allowed, their depth, and the situations in which they might be granted.

Not all firms allow discounts and price promotions. Apple famously held a no discounting policy for several decades on its product lines. In contrast, Samsung manages price variances across its industries and product lines. And other firms may allow price variances on some products, such as HP printers, while maintaining consistent prices on others, such as HP ink. (In the smartphone market where Apple and Samsung compete, it should be noted that Samsung has sold more units than Apple, but Apple has made more profits, as of the time of this writing.)

The goal of price variance policy is to fine-tune the alignment of prices to customers’ willingness to pay at the transactional level after using the blunt tool of market pricing. As noted, different customers will perceive the same offering as delivering different benefits, and therefore they will have different willingness to pay. If prices were held constant at the market level, some customers would be willing to pay more and the firm would find it is leaving money on the table. Meanwhile, other customers would find the offering too expensive and the firm would lose those sales. A well-designed price variance policy both increases the number of customers served and the value extracted from the market by providing guides to micro-segmenting the market.

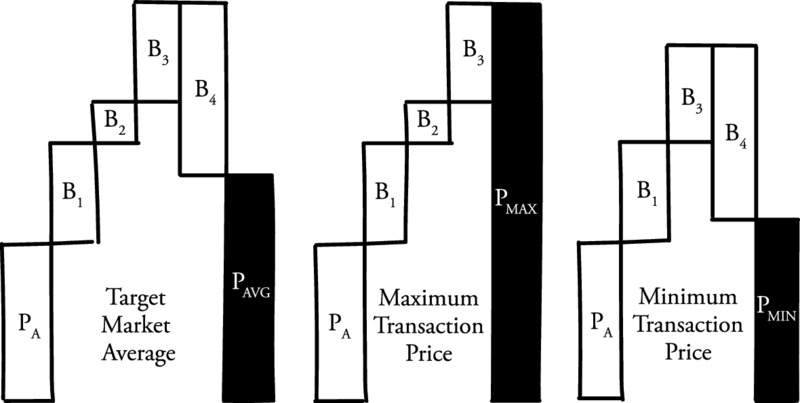

To demonstrate, consider a thought experiment of an offering facing competition shown in Figure 5.2. The competing alternative is priced at PA. The firm offers additional benefits B1, B2, and B3, but is missing benefit B4. It therefore calculates the go-to-market price for the average customer as the price of the competing alternative, plus the value of the additional benefits less the value of the missing benefit: PAVG = PA + (B1 + B2 + B3 – B4), as shown on the extreme left.

Figure 5.2 Variation in Exchange Value to Customer

Once in the market, there may be customers who never cared about the missing benefit B4, and therefore would be willing to pay a higher price than the average calculated. For these customers, the maximum possible transaction price is much higher than the average market price, at PMAX = PA + (B1 + B2 + B3), as shown in the middle diagram. Pricing the product at the average market price, PAVG, leaves money on the table with customers like this one, and the firm has an incentive to use the maximum potential price, PMAX, in this case.

Alternatively, there may be customers who didn’t value benefit B2, which the firm provides, and therefore would not be willing to pay the average market price but would be willing to pay a lower price, which the firm still finds profitable. For these customers, their willingness to pay is still profitable and therefore could be used to define a lower, minimum transaction price (if that price aligns with the strategy for that offering), at PMIN = PA + (B1 + B3 – B4), as shown on the extreme right. Pricing the product at the average market price, PAVG, pushes potential customers like this one out of the market and lowers sales volumes, and the firm has an incentive to use the minimally acceptable price, PMIN, in this case.

Using one price for the entire market leads to market inefficiencies. As we demonstrated, customers who could have profitably purchased the offering are priced out of the market, and customers that would have paid more aren’t asked to. To address the market inefficiencies created by using a single price, many leading firms allow price variances.

Continuing with our thought experiment but in the case of a firm allowing price variances, the firm may wisely choose to price the offering at the maximum transaction price at the market level (center diagram). This list market price will be far above the expected average valuation of the product in the market (left diagram), yet some customers would be willing to pay this price. For those that aren’t willing to pay this price, the firm allows price variances up to, but not below, its minimum acceptable transaction price (right diagram).

If these price variances can be granted and withheld judiciously, the firm’s profits will increase, the number of customers served will increase, and this pricing will more efficiently clear the market of all potentially profitable transactions.

That is the goal of price variance policy: to improve transaction flow and profitability through better price segmentation. But the challenge of price variance policy is contained within the preceding “if” statement: How can executives detect when granting a price variance is both necessary and profit enhancing, and how can they detect when withholding a price variance is both possible and profitable? Not every customer needs a discount or promotion, but some may and these price variances may improve profitability.

Small improvements in price variance policy can drive large improvements in profitability, whereas small errors in price variance policy can, in aggregate, cost firms millions. Getting price variance policy right proves daunting for every firm.

While price variance policy was once considered the domain of sales management, leading firms are increasing their scrutiny of price variance management. Research has demonstrated that cross-functional engagement improves decision-making. Increasingly, firms are engaging not only sales, but also marketing, finance, pricing analytics, and other functions—if not the CEO—to improve decision outcomes.

Firms pursuing both directions, either reducing or increasing price promotions, find price variance policy difficult to get right. Consider the tumultuous 2011 to 2013 tenure of CEO Ron Johnson at JCPenney, during which he removed all price promotions only to find sales implode, and you will see the challenges a firm faces in reducing price promotions. Or, consider the methodical restraint practiced by CEO Michael Jeffries of Abercrombie & Fitch from 2009 to 2011 as he introduced price promotions and led his organization to learn how to manage price promotions properly, resulting in Abercrombie & Fitch’s sustained strong profit margins relative to most of its industry competitors.

While price variances are a daily challenge for most firms, price variance policy should not need to be adjusted that frequently. Most firms find reviewing and adjusting price variance policy on roughly a quarterly basis sufficient.

Price variance policy determines which types of promotions and discounts are allowed, the conditions under which they can be extended, and the allowable depth of those promotions and discounts. If a discount or promotion is requested that does not meet the price variance policy, then price variance policies also determine the decision escalation rules under which an extraordinary promotion or discount may be allowed.

Pricing analytics has proven to greatly improve price variance policy. Through data mining, finely tuned market segments can be identified and priced accordingly. And through controlled price variance policy experimentation, improvements to decision-making can be made. Enterprise and desktop software both have greatly reduced the cost of these efforts making them worthwhile for most businesses.

In the absence of a known price variance policy, the default policy is one that allows for any price at any time, as long as the salesperson and customer can get away with it. This usually results in erratic pricing where the largest discounts go to the customers that negotiate the loudest or is used heavily by salespeople with sufficient organizational power to be granted a variance, rather than for those transactions in which a discount would materially impact the customer’s purchasing decision. In these cases, one of the easiest approaches executives take to improve pricing and price capture is to define the pricing variance policy.

Price variance policy for most firms starts at the level of decision escalation rules. As customers request deeper discounts, approvals are granted at higher levels of the organization, eventually reaching the CEO.

Price variance decision escalation processes can cause many challenges, however. Consider how it can bias sales departments into thinking that every customer is highly price sensitive, since the most salient, recent, and available data they collect from the market tells them consistently that the firm’s prices are too high. Or consider that it requires a lot of time, both delaying transactions and chewing up the time of expensive managerial resources to execute. Finally, consider that it can lead to spending more time and rewarding low-paying customers when they make the biggest fuss about prices while effectively punishing a firm’s best customers, who accept the prices offered and, therefore, contribute to higher margins.

One alternative is to identify rules to guide when and to whom price variances can be granted. Firms typically find that rule-based price variance policy is much easier to manage, accelerates transactional decision-making, and improves price variance outcomes. In defining these rules to price variances, executives are asking: Which segments deserve a price variance? Can a price variance be related to cost reductions in order processing, shipping, or elsewhere? What kinds of price variances drive the largest change in customer buying patterns? Which kinds do not? How can price variances drive loyalty? When do they end up encouraging customer churn as customers switch from brand to brand with no long-term profit improvement but high, short-term profit losses?

Crafting these rules may require some level of trial and error, which is why price variance policy should be monitored and adjusted far more frequently than market-level pricing. Firms consistently find experimentation with price variance policy far more profitable than one-and-done decision-making approaches.

A second alternative is to change the incentive structure of the sales force itself. Incentive plans for salespeople are shifting from a volume or revenue basis toward a profit base in many, but not all, leading firms. The shift has been undertaken to align the salespeople’s price variance decisions with the profit goals of the firm. The decision to use profit-based sales incentives is a strategic one. It may not align with the firm’s strategy if the firm is seeking market share over profits. And, it may not be useful if salespeople do not have any price variance decision-making authority or the variable costs are negligible compared to the unit price. Other research has demonstrated that the act of engaging sales in the market-level pricing decision itself decreases the need for incentive alignment.

Firms can use all three of these price variance policy approaches simultaneously.

SaaS Company’s Price Variance Policy

SaaS Co. was aware it had challenges in managing price variances. Historically, price variances were managed by sales and sales operations through an escalation process. Changes to the price structure and price points were designed to reduce discounts and surcharges related to high- and low-volume purchases, yet it was suspected that further discounting rules would be needed in the future. To guide the future development of further discounting rules, a pricing analysis effort was undertaken in the months shortly after implementing the new price structure and points to demonstrate the depth, frequency, and market segments related to discounting. This analysis was circulated among sales, product management, and operations, and helped the company identify opportunities to improve decision-making in price variance policy.

Price Execution

Price execution applies the right price to the right transaction at the right time. It touches every customer purchase. It is the point where all the prior decisions turn into action. Corporate strategy, pricing strategy, market pricing, and price variance policy are all converted from ideas into action in price execution. At this point of execution, these decisions are put to the test: Will the target customers purchase at the target price?

The goal in price execution is to quickly apply the correct prices according to the strategic and managerial decision rules and then collect those prices from the customer in a timely manner—all with zero errors. While this goal may sound simple at first, it isn’t.

In retail environments, price execution isn’t just tallying up the total and adding relevant sales taxes, it is also an issue of coupon processing, discount application, rebate management, and much more. Entire industries have been created just to address these issues appropriately and efficiently, not to mention the numerous point-of-sale hardware and software systems to support retailers.

In business environments, including manufacturing, distribution, and services, price execution is further complicated due to the presence of individually negotiated contracts with many, if not each, customer and by the presence of highly complicated ordering with multiple line items. Not only must each offer, invoice, and account receivable be managed for individual customers, but the market pricing and price variance policy must be applied appropriately in the execution of these tasks.

For instance, consider a simple order for furnishing an office by a business. While the specific desks, chairs, tables, whiteboards, and other elements may be selected by an interior design firm and approved by the business customer, the billing at the manufacturer level for that order may include thousands of line items in multiple quantities such as desk leg style, desk leg color, chair style, upholstery color, structural colors, armrest options, desk surface style, desk surface color, desk surface finishing, and so on. The list of item options related to the simple task of furnishing an office is a book unto itself. When this order is placed, price execution must not only ensure that the configuration of parts in the order work together, but also that any contractual terms it holds with the interior design firm, channel partner, or the end customer are also applied. And, if further negotiation is required to close the order, price execution must manage the negotiation approval process and implement those results as well. Even when it comes to accounts receivable, that one contract may have started with a net 15 term but ended up at a net 60 due to the purchasing power of the end customer, and even that process must be managed.

Price execution is a high-frequency activity. Every day firms will manage quotes, orders, and billings, and for large firms, these activities can occur millions of times per day. Individually, specific order, invoice, and bill collection events may have limited impact, but collectively, they determine the entire revenue of the firm. Given this nature of price execution, some firms have successfully applied continuous improvement techniques to improve process outcomes.

At the customer level, price execution can squander all the firm’s profits by misapplying price variance rules, or it can irritate critical customer relationships when proper relationship management etiquette is poorly applied.

Price execution is often managed at the interface of sales and finance, wherein sales detects and defines the customer need and willingness to pay, and finance approves the quote according to the market pricing and price variance policy, then manages the invoicing, billing, and accounts receivable. Firms have named the price execution function alternatively as customer care, sales operations, deal desk, proposal management, billing, accounts receivable, and many others.

While price execution sometimes falls under the pricing function, it does not always and need not always be. The other pricing functions strongly depend upon fact collection, analytical thinking, and strategic creativity. Price execution depends more upon process management, executional excellence, and quick reaction times. In other words, price execution requires a different skill set and mentality than the other functions in pricing.

In price execution, the firm is focused on applying the best price between the maximum and minimum level defined as acceptable through the market level and price variance policy. For profit-seeking firms, this implies trying to detect and apply the highest possible price with each customer. For growth or share-seeking firms, price execution might instead focus on capturing the strategically defined price for that market segment. In both cases, price execution requires knowing the specific price the firm is willing to walk away from in a deal. That is, the price that is “out of target.”

Much of the improvement possible in price execution focuses on identifying and rectifying mistakes or improving cycle time. These challenges can be found in quoting, ordering, billing, and accounts receivable. Indicators of challenges could be numerous high-bill complaints, excess exceptional or special order discounting, or delays in price execution process time that affect transaction flow.

Often the challenges identified at the price execution level are actually caused by failures in price variance policy, market pricing, or pricing strategy. As such, many executives start with improving other aspects of pricing, and once improved, wait to measure their effect on price execution challenges.

SaaS Company’s Price Execution

At Saas Co., price execution was jointly managed by sales, sales operations, and billing. Challenges at the price execution level were being felt acutely by the sales operations and billing functions. Yet the company believed that the causes of the price execution efforts were primarily driven by challenges in the price structure and pricing points themselves.

Once the new price structure and price points were released, price execution focused on implementing the new rules. This required a sizable change in management effort—not so much in the form of process changes, but in the form of attitude changes. Salespeople had to learn the new price structure, its rationale, and how it should affect their transaction pricing in order to effectively sell with the new price structure.

Pricing Analysis

At leading firms, every pricing decision is informed by some form of analysis. Whether the pricing decision revolves around customer strategy, competitive strategy, pricing strategy, market pricing, price variance policy, or price execution, pricing analysis is charged with collecting facts, converting these facts into information, identifying possible decision options, and analyzing the relative merits of these decision alternatives.

For business strategy, pricing analytics address: What is the market? What are the competing alternatives? Does the firm have pricing power? Does it have a competitive advantage? Does willingness to pay vary between customers? Which market segments most value the firm’s offering or are otherwise most valuable?

For pricing strategy, pricing analysis addresses: Would there be a significantly larger customer base at lower price points to warrant penetration pricing? Is there a strategic reason to use skim pricing? Should the firm use a price-neutral strategy? How do the benefits of the firm’s offering compare to the competing alternatives? Which specific benefits correlate with willingness to pay? What price structure best matches the value delivered to customers while remaining market-acceptable and improving profits? How should the firm react to competitive price pressures? What organizational abilities are needed to achieve the given pricing strategy?

For market pricing, pricing analysis addresses: What is the specific value customers place on specific differential benefits? How does the monetary value of these benefits vary across customer segments? If demand is below expectations, is it really a pricing problem or an offering design problem? Which customer segments would naturally be attracted to the offering? Which customer segments can be served on an opportunistic basis at best? Which products are allowed to experience price variances? Which are not?

For price variance policy, pricing analysis addresses: What is the range of prices actually captured in the market? What forms of discounts and promotions does the firm offer? What is the cost of price variances? Which specific price variances drive customer purchases or reduce costs to acquire and serve customers? Should price variances be related to market segment variables, such as volume, geography, industry, customer size, or customer behavior? Which ad-hoc price variances currently managed through an escalation process should be converted into targeted price variance rules based on objective criteria?

And, for price execution level, pricing analysis addresses: What is the error rate in price execution? How much effort or time is required to price an offer or manage price variances? How often are exceptional price variances required? What is the frequency of customer ordering and billing complaints or inquiries?

In the past, many forms of pricing analysis have been assumed to be too expensive to execute. Due to the advances in software, both at the desktop and enterprise level, the costs and time required to execute many of these analytical techniques has dropped dramatically. Today, even small firms can reasonably benefit from pricing analysis and large firms are generating highly significant profit increases by improving their pricing decision-making through proper analytics.

Yet, even with advances in computing, pricing analysis is not a software problem alone. Pricing analytics rely on a wide variety of specialized techniques. Unique skills are required to collect the needed raw data, convert it into facts, and then apply the proper analytical technique to develop useful and unbiased information for decision-making. And, as can be told from a close reading of the text to this point, pricing analysis is required on an ongoing, quarterly, annual, and business cycle basis. In short, pricing analysis requires firms to create a new organizational capability.

Pricing analysis functions are generally welcomed across the organization. Sales professionals have a desire to perform and value useful metrics that clarify their potential to capture higher prices. Marketing professionals desire to see their products perform and seek knowledge regarding how to improve the profitability of their products. And finance professionals enjoy the clarity and predictability that good pricing analysis provides.

SaaS Company’s Analytics

SaaS Co. conducted an analysis of price variances after the new price structure was implemented. Measurements of the price captured indicated that the new price structure did have a significant positive effect on future revenues. Measurements of price variances also showed the depth and range of discounting, variation in deals won versus lost by discounting, variation in discounts by salesperson, and variations in discounts by product. These measurements clarified that the new price structure was both improving profits and enabling customer capture, but several salespeople were continuing with their past pricing practices or utilizing the maximum discount allowable within their discretion. Because the win/loss study by price offered demonstrated that the new prices had no material impact on deal-close rates, management determined to use this information to encourage sales force behavioral change and to demonstrate that adopting the new price structure would be revenue positive, and therefore more profitable for the individual salespeople.

To conduct future analysis, SaaS Co. created a pricing function. This pricing function was charged not only with managing transactional- level pricing analytics, but also informing pricing decisions for new products and otherwise providing pricing insight for senior executives.