3

All Things Cash Flow

Wealth is the ability to fully experience life.

—Henry David Thoreau, essayist and philosopher

The Day My Cash Flow Stopped

The following took place in 2009, at around the time of the Great Recession. I vividly remember because I was running my homeopathic practice at the time and had several clients desperate to alleviate their fears of the looming economic catastrophe and the detrimental impact it was about to have on their lives. I listened supportively, but made sure not to engage with their fears because I understand the power of how we can sabotage a great business – or anything for that matter – by focusing on negative thoughts.

This time, the circumstances were getting harder to ignore. It seemed as if almost everyone I talked to was focusing on his or her intensified fear of the future and sense of becoming overwhelmed. I didn’t think I was buying into their frenzy, but gradually I noticed that my phone had stopped ringing. No one was calling to make an appointment. This was odd, because I was always booked solid.

The few potential clients who did call asked my fees. After I told them they said, “Oh, I can’t afford that.” My fees had been the same for the past year, so something was clearly amiss.

The first week, I attributed it to the fact that I needed a break. After two more weeks went by, Julie, my assistant, asked, “Allison, what is going on?”

I replied, “I have no idea.”

And then, I started to worry. In fact, I began to feel a great deal of fear rising up in my gut. Then I heard myself talking as I shared my worries with my husband. It was as if I were observing myself play out this fear. While all of this worry energy was bubbling over, it hit me like a sledgehammer: I had been falling – hook, line, and sinker – into my customers’ stories.

No matter how hard I had been trying to distance myself, I was allowing their fears to seep into my thoughts. I was living out this belief that my abundance was coming to a screeching halt.

That day, I drove myself to the beach. I sat in the sand for what felt like hours. My goal was to shift my energy from a state of fear to reconnecting with my vision, passion, and place of abundance. I completed the visualization and once again experienced the joy of working with my clients and helping them heal. I visualized their happiness in my getting well, and how that would impact my clients’ lives. I felt a powerful shift happening inside of me, moving from fear back to a place of abundance and gratitude.

You cannot feel fear and gratitude at the same time, so that helped me anchor my positive thoughts. I could feel the fear dissolve from my body and knew change was in store for my business and me.

The very next day, my phone rang nonstop. Julie called and exclaimed, “You did some visualization, didn’t you!”

■ ■ ■

Cash flow is a crucial part of business and you must have rock-solid strategies in place to support your growth and protect you through the rocky times. However, before anything else, you first must believe it will all come together. There will always be down periods, but they won’t stay that way as long as you remain focused on the vision of where you are going, believe it to your core, even if you are not there yet … and then mix in a ridiculous amount of persistence.

If you truly believe in your mission, if you truly believe you want to make a difference on this planet, the money will be there. By getting into this place of worry and disbelief or non-belief, you’re just pushing it away.

In my mind, cash flow is a living force. If you think of cash in terms of currency, it’s not a big leap to regarding it as business energy – the electrical current that flows back and forth and sustains your company. You must be able to tap into that electrical current of cash flow when you need it most.

When you are flying on the trapeze, you must summon and channel your inner electrical currents to produce needed bursts of energy at the precise moments. Similarly, in your company, you must be able to tap into that electrical current of cash flow when you need it most.

The Truth About Cash Flow

Steel yourself for this: cash flow issues can happen to any company of any size at any time. I don’t care if you’re a $500,000 business or a $500 million business, at some point you will go through a cash flow crunch and need to have a backup plan at the ready. A lot of people think, “Oh, when I hit $50 million, I won’t have a cash flow crunch anymore.”

Expect the crunch: it’s part of business. When it occurs, it doesn’t mean you aren’t good at business. It only means you need to better anticipate and prepare for the “crunchy” months far ahead of time.

CEOs often believe that once their businesses begin to generate seven-figure revenue, their cash flow problems will be over. That couldn’t be further from reality. Consider the fact that every day you read in the news about a major business corporation laying off tens of thousands of employees. Giants such as Hewlett-Packard, General Motors, IBM, and AT&T have laid off 40,000 or more employees during the past few decades. Why? Largely because of cash-flow issues caused by a variety of circumstances.

Business owners must be well aware of the fact that being bigger doesn’t make a company invulnerable. I readily admit to my clients that I have had my share of cash flow issues, even during some pretty large growth years. Why? You need to continually invest in your growth and sometimes it comes after a period of development in your revenue streams, systems, or your team. Or, it may be time for a course correction. Business and the market are changing so quickly these days that you must keep an eye on what is coming down the pike – not to be fearful, but to be smart. Some business owners seem relieved to hear that this is a relatively common occurrence and not necessarily a failing on their part.

Unfortunate, unpredictable things can and do happen when you least expect them. Costs and expenses rise as your company grows. Things break down and need replacement or repair. Your customers sometimes have cash flow issues of their own and can’t (or won’t) pay their bills on time. These are all normal lows of doing business and can deplete cash flow at any time.

As you get to know your business cycle, you will see which times of year are slower and which ones will yield large payments. This is why it is so important to track your cash flow and compare it year to year. Look for consistent cycles. For instance, some businesses are predictably seasonal and based on promotional holidays, such as Valentine’s Day, Mother’s Day, and Christmas. Or, a business such as a surfboard company is definitely going to be slower in the winter months. Cash flow planning and alternate methods of revenue generation need to be in place for that time period to help offset the dry spell.

In order to be prepared for your inevitable cash flow crunches, you must be as revenue-focused as possible through sales, marketing, and relationship-building efforts. If you can generate enough cash flow and reserves, you’ll rely less upon money from investors and require fewer partners. You’ll gain the immediate luxury of more freedom and independence and some wiggle room to experiment and fail before everything clicks.

On the other side of the equation for many companies are the systems. CEOs of various start-ups often feel that they can’t function without a substantial amount of seed money to build their supportive systems. They end up rapidly depleting their cash because they don’t understand how to build or scale a company. When the money diminishes, they have to start raising money all over again – which is a ton of work and an unbelievable amount of stress.

Before bringing in investors, I believe it’s far better that you first build your systems, foundation, and revenue model on a shoestring to get your sales cranking. Once you have a flowing revenue stream – even if it’s just a trickle at first – you can go after investors. This way you’ll be more likely to spend the money where it needs to be spent, rather than on trying to figure out your business model and then blowing through everything provided to you. Steve Jobs did not have investors when he started out in that garage. He worked hard at selling a bunch of computers.

I’m convinced that many of the start-ups that fail do so because they receive gobs of money and react as if this is the end-all panacea – when it’s not. What truly gets a start-up off the ground and flying are sales, sales, and more sales; the revenue model; the people; the product/service creation; cost-efficient, high ROI (return on investment) marketing; and the bare-bones systems that are just enough to bring in some revenue.

Know Your Numbers

I cannot tell you how many times I have worked with entrepreneurs who are not aware of their cost of doing business, percentage of growth (or loss) over time, and their net profit. Ultimately, the most important number is your profit: how much is left to walk home with at the end of the day.

As your company grows and scales, the bookkeeper and accountant that you started with may not be the ones that you continue with because those individuals are likely stuck in “scrimp-and-save” mode and not knowledgeable enough in bigger pictures areas of expanding into an enterprise, such as mergers and acquisitions (M&A). This is when it may be the time to bring on an experienced controller or chief financial officer (CFO), who has experience at the enterprise level and has been involved in big deal-making. Make sure you surround yourself with the right team to help you scale and add to your organization’s body of knowledge.

Your Plates and Platters

Here’s a simple technique to keeping your target numbers straight. Divide your financial goals into these three levels:

- Your Blue Plate Special Number is the amount of revenue you must bring in to keep the lights on and meet the payroll.

- Your Silver Platter Number is the amount of revenue that you need to breathe in your business. You can sleep at night comfortably without worrying about paying your bills. You have enough to invest in marketing and growth and to live a comfortable lifestyle, in which you can spend time doing what brings you joy with the people you love most.

- Your Gold Platter Number usually comes into play as you scale, once your products, team, and systems are in place. This is where you see great traction in your growth, and your revenue and profits are on the rise. As they say in the Olympics, “Go for the gold, baby!”

Get clear on these three numbers, so you know what to reach for on a yearly, quarterly, and monthly basis – and then increase these numbers as you grow. Michelangelo said it perfectly: “The greater danger for most of us lies not in setting our aim too high and falling short; but in setting our aim too low, and achieving our mark.”

It’s All About the Sales

What do you suppose is the very first thing you should do every single day at work? Focus on sales, that’s what!

The first three hours of every business day must be focused on sales (unless you have a sales team, and then it’s a 24/7 deal) to generate cash flow that can help safeguard your business against any kind of inclement weather. This is time spent strategizing with your sales team, reaching out, seeking referrals, following up on leads, setting up meetings, and so on.

Rinse and repeat each and every day: sales, sales, and more sales! Remember, sales is sharing. If you truly believe you have the best product or service, get it into as many hands as possible.

Your knowledge is less important than how much you truly care. That is why people do business with you. Make people feel good and they will buy into your ideas.

—Excerpt from my interview with Michael Bernoff, CEO of Human Communications, Inc. To watch the full interview, go to: www.ScaleorFail.com/bonus.

Companies that are focused on revenue don’t struggle with cash flow as much as others. As the CEO of your company, you always have to be the chief convincing officer. You must stay on top of your numbers and your sales team. Everyone in your company must be focused on the sales target, including the marketing department and your assistant. The entire organization must know the number of leads it takes to convert a sale, so you can work together as a team and make that target.

When my dad operated his women’s clothing chain, every manager knew the daily sales goal. He was obsessed with the sales targets and constantly called every store to check in so that everyone stayed focused on the daily target. This was back in the day – but his company even had different color phones for each store for check-ins from the main warehouse: pink, green, turquoise, and so on. It might sound a bit overboard, but it worked.

Get a Credit Line

There’s one lesson I learned early on that may sound a bit counterintuitive: Borrow money when you don’t need it. It’s a lot easier to get a loan when you’re not in a desperate situation. Having the cash to draw from during a slow period – or during the float period between when you purchase your products and when you get paid – takes off a ton of pressure. Then you pay it back once you are busy again. Debt is not a bad thing when you’re using it to grow. If you go on an unnecessary shopping spree buying things that have absolutely no return, that’s one thing. Investing in your company – an asset with unlimited yield potential – is the smartest investment you can make.

Are You Ready to Scale?

When I am instructing a group on scaling, this is one of the first things I ask: “Is your business scalable?” The question hits most people sharply. It’s surprising how rare business owners are asked (or ask themselves) this all-important question. If the CEO is doing all of the sales herself, for example, I can pretty much deduce right off the bat that the company is not super-scalable.

Being ready to scale means you have a system in place in which you have customers who are coming back to you on a regular basis and are generating reliable cash flow. Recurring revenue might include membership fees, subscriptions, courses, or payments for ongoing services.

There are so many ways to generate recurring revenue. For example, a lawn-mowing company might offer a special price for cutting grass on a weekly basis if a customer locks in for one year. Plus, the company could throw in a cross-sell for seasonal weeding, raking, or mulching. A membership program could be as low as $15 a month, but this adds up if you have hundreds or even thousands of people paying that amount. It may not necessarily be the core of your business – it’s an extra – but it provides something additional and sustaining.

Once you have a sustainable, recurring model and know where the cash flow is going to come from, your business starts to snowball. It starts small, but gets bigger and bigger and gains momentum as it moves forward.

You’ve probably heard of valuation. In simple terms, this is the value of your business should you decide to sell it. If your business generates static revenue – meaning earnings from a one-time sale – that would be considered a one-time valuation. However, if your business model involves recurring revenue, such as monthly or annually, then it’s a three-to-five valuation. This means that it’s worth three times the value when you go to sell it than if you just had static revenue because the sales happen on an ongoing, predictable basis. Venture capitalists salivate over the growth and ROI possibilities of businesses that have recurring revenue.

So ask yourself: Is your business ready to scale? Is your snowball gaining speed? Is it doing so on its own with minimum additional effort?

The Yellow Brick Roads to Scaling

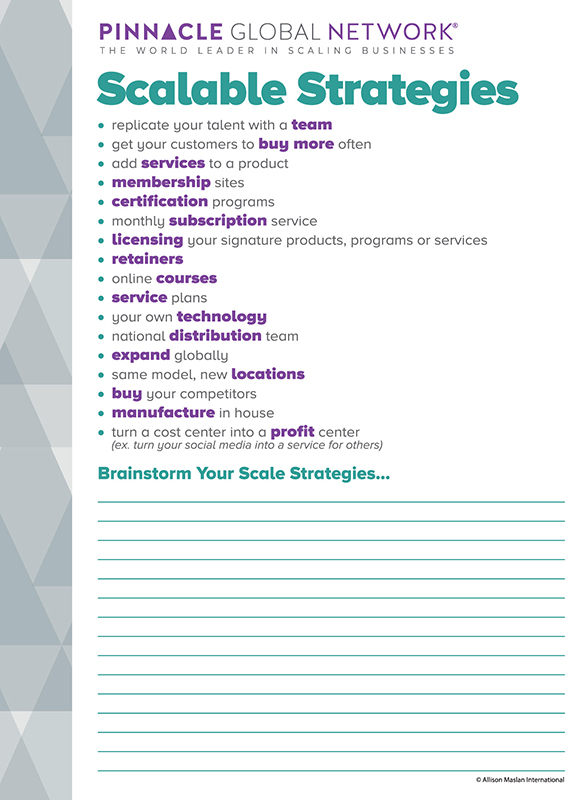

There are several ways to safeguard cash flow while scaling your business. You need to be creative and nimble in order to recognize and take advantage of these strategies. Depending on your type of business, you might be able to merge your current strategies with new ones. Take a look at the Scalable Strategies worksheet (Figure 3.1) to see if any of these might apply to your business. Brainstorm with your team to see if there are any others they can come up with.

Figure 3.1 Determine what strategies you can add to grow your cash flow.

Leverage It

Once you have your model nailed down, you can leverage it into different markets. That could potentially mean expanding into different physical locations, marketing your product or services to a different customer base, or adding a natural extension onto something your business is already doing.

This is how the grocery business works: basically, the large food and beverage companies buy space. It’s all about buying real estate.

In my company, we realized that we weren’t going to get any more space for our beverage than maybe 10% to 15%. We needed to come up with cash in order to grow. But we were never going to be able to write $30–60 million checks for that.

I decided that my growth was going to be capped if we decided to play in this game. We started doing business with Amazon and did really well in that channel. One day at a meeting with them, I said, “I really want to understand who’s buying.”

They said, “Well, we can’t give you the names, but we’ll give you a glimpse of who’s buying.”

It turned out that the people who were buying our product were also buying diabetes monitors. They were buying pregnancy-related items. “Great,” I said. “I want to go out and talk to them.”

The Amazon team said, “No, we’re not able to give you that data.”

It was at that moment that I realized that I didn’t have control of my customer. I didn’t know anything about my customer at Publix, Whole Foods, or anyplace else, either.

I had grown up in a place where data was so important to me, and yet suddenly I didn’t know who my customer was. I went back to my board, and I said, “We’re going to launch our website at drinkhint.com, and we’re going to start selling cases of Hint, and if consumers want us to sell it to them on auto shipment every week, or every month, then we’re going to do that. If they want to change flavors, we’re going to do that, too.”

I didn’t know if it was going to work, but I thought, Let’s just throw it out there and see what happens.

Two and a half years later, this channel became almost 40% of our overall business. The great thing is that when we decided to launch a product like sunscreen, we were able to go back to our database.

We have a lot of consumers who are coming to us and saying, “If you guys do those kind of trials, we would love to be a part of it.”

When I talk to other food and beverage companies about their online businesses I ask: “Oh, are you guys online?”

They say, “Oh, yeah, we sell through Amazon.”

This is fine, but they don’t know who their customers are or anything about them. They don’t actually understand what kind of problems they can solve for their customers. To them, it’s really just about the dollar sales. This is important, but it’s not everything.

—Excerpt from my interview with Kara Goldin, CEO and founder of Hint Inc. For the full interview, go to: www.ScaleorFail.com/bonus.

Here’s a quick example. A client of mine, Lisa Miller, who ran a photography business for several years called me one day and told me that her husband was recovering from a recent stroke. Then she said, “This was his wake-up call. He is serious about going after his dream of running a winery.” I said, “Fantastic. Let’s make it happen!” Together they created Koi Zen Winery, where they crush their own grapes and bottle their own signature brand of select wines. Now, four short years later, they have more than doubled their space and won several international wine awards, including double gold and best of class for his 2015 Malbec. One of the smartest moves they made was starting a subscription-based wine club that now has over 500 members. (I am one of them, of course!) Limiting their growth to one retail location would not be scalable; however, with their own brand of wine and monthly recurring revenue of their wine club, the skies are the limit!

Replicate Yourself

If only we could clone ourselves – wouldn’t that be wonderful? We would get so many more things done! Well, until science figures out how to accomplish this, we must improvise.

Business owners often cling to the misguided belief that they are the only ones who can handle certain tasks. They are also convinced that they are the only ones who can manage certain clients, who want to work only with them. If you are one of these owners, this is your ego speaking. Yes, there are things that you can do (talent) and know (experience) that your team may not have – at first. It’s up to you to open up your mind to the idea that you shouldn’t be handling so many tasks and client relationships yourself. If you hired the right people, you must trust that they can be trained and entrusted with your wisdom to do the same things you do.

It all needs to be systematized, so that your team understands how you operate, how you work with clients and customers, and how you want your products represented to the outside world. Once you have been “replicated” and your team is doing the things that you used to do, you have the time and bandwidth to scale your business in a number of different ways – including replicating yourself and your team as you establish various business extensions.

I worked with a company for a few years that owns a healthy food delivery service in Fort Worth, Texas. That is a low margin business because the ingredients are expensive and there is only so much people will pay for food. She was working so hard – even building a team – but profits were only inching along. I helped her brainstorm and develop a program to train other personal chefs across the country how to build a successful business. Not only did she win Personal Chef of the Year, but that business ended up bringing in at least three times more revenue than her food delivery business.

This is a great example of how to replicate, multiply, and give back, all at the same time. It’s interesting because I often find that the most creative revenue ideas come when you hit a wall – hard. Stress can be a good thing when it forces you to get creative and think in a new way to come up with quick solutions. If you’re moving along okay, even at a slower pace, what will compel you internally to think outside of the box? Nothing.

Hiring Forward

People have occasionally come up to me and asked these questions:

- How do you know when you’re ready to hire?

- How much money must you have in the bank before you hire?

The answer that I generally provide is that most businesses don’t have a chunk of change sitting in their bank accounts to cover their new employees’ salaries for a long period of time. When you hire the right employees, they will pay for themselves in increased revenue or productivity. If this position will help you produce a lucrative product faster or drive greater sales and revenue, your company has an opportunity to grow to a much larger scale. If you hold back on hiring to fill these positions – which might be sales oriented or on the creative side – you may end up missing great revenue opportunities.

Even adding an administrative position will create more productivity, taking work off your plate to assist getting your products or service out to the marketplace faster, with better customer service behind it. What happens next? Reorders, referrals, and happier clients for longer periods of time. Your lifetime value of a client goes up, and so do your profits.

Look for the holes in your company, and also in which areas you want to grow. Adding the right support there is like adding Miracle Grow to your business. It’s not as if I have six months of salary sitting in the bank for staffing. But I’ve found that, when I take a risk and add a key position in and hire the right person, the money always comes. The business grows. I call this hiring forward.

For me, as a top line operator, I hire ahead of time. I know more is always coming.

—Excerpt from my interview with Gary Vaynerchuk, CEO, VaynerMedia. For the full interview, go to: www.ScaleorFail.com/bonus.

When you hire forward, you identify an area of business growth, onboard someone into a brand new role to own it, and then watch your business organically grow. Your mind may try to tell you that you are adding expense in an uncharted area which makes it “high risk,” but that’s not the case. It’s not about recruiting someone who will add to your overhead. You do this so your business will get to the next level. If you’re waiting for that money to magically appear in your account on its own, it’s never going to happen. You need to bring in people with talent and contacts so you can extend your business vision. Then your cash flow will soar.

Get Your Customers to Buy from You More Often

This may seem obvious, but you need to get your customers to buy from you more often. Sometimes the upselling opportunities are staring you in the face and you don’t think to take advantage of them. Offering existing customers a service plan or a warranty is one obvious way of upselling. Car manufacturers do this all the time with maintenance agreements.

Statistically speaking, on average existing clients account for 41% of your income. They are apt to spend five times more than new clients because you already have a relationship with them. They already trust you and know what you can do. Many customers love the idea of a “one-stop shop” where they can have all of their needs provided by one partner or vendor. Wherever possible, you should strive to become that one-stop shop.

New customers can be cagey and skeptical and often want to take things slowly, one step at a time. You have to prove yourself and your company’s value. Often it takes time to figure out the onboarding process with a new customer. From your standpoint, you have no idea if this new client will be a good one or not and pay bills on time.

With your existing customers, look both inside and outside the box to answer these questions:

- What three additional products or services can you find to upsell or cross-sell?

- What are they getting somewhere else that you can offer at better quality, with a higher level of service, or at a better price?

- What products or services do you currently provide free of charge that could be bundled for a fee?

With regard to the last point, above, are you giving away too much for free because you are afraid of losing a customer? Trust me when I say this: Free is not a sustainable business model. You should be working to monetize every aspect of your business. You are in business to make a great profit. This is how you will scale, give back to your team and their families, and take that leap from entrepreneur to enterprise.

One of my clients, an event planner, also books hotel rooms for out-of-town attendees of major events. While speaking to her I realized that she and her team were spending hours upon hours on this service and not charging for it, losing valuable time (which is money) and significant potential revenue. It is great to give over value, but leaving an entire revenue stream is crazy-making. I told her to package this service with her main on the table event-planning service and offer it as her premium product for a higher-priced revenue offering.

When it comes to shaking the trees for revenue from your existing customers, there are many things you can do. If you are in doubt about where to start, look at other industries, such as credit-card companies, hotels, and airlines, which constantly offer special memberships, VIP perks, and loyalty programs. It seems as if every day Starbucks has a different incentive to lure you into the store and buy coffee: iced drinks $2 after 2:00, or extra bonus stars if you order the macchiato on a certain day, and so on.

What can you offer to entice your existing customers to buy more?

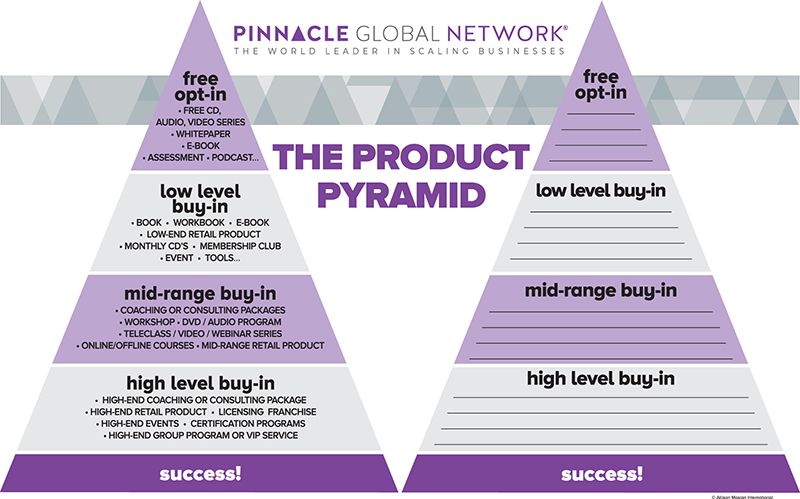

The Product Pyramid

The Product Pyramid is a multitiered approached to bringing in customers at every level. Presently, you may be hitting on only one or two of these levels – but you have the potential to build your customer base to establish relationships with customers in every single one of them.

Let’s stick with the coffee example, since we were just reflecting on Starbucks. Suppose you’re a coffee customer who wants to make a good, no-frills cup of coffee at home. There are many ways to go about doing this. If you just want something down-and-and-dirty right away, you’d go online and buy a coffee maker for maybe $79. Done.

But let’s say you’re a real coffee aficionado. You love the experience of coffee and want the absolute best shot of espresso every morning right in your home. You don’t mind taking the time to go to Starbucks or another coffee vendor to check out all the brewing options. You end up spending $2,999 on a top-of-the-line coffee maker that features the most innovative technology so that you can make you the perfect cup of espresso.

All of these two extreme ends of the customer spectrum – as well as the ones in the middle – apply to your business. There should be a customer for every level of your offerings.

Now take a look at the Product Pyramid worksheet (Figure 3.2). You can upload this at: www.ScaleorFail.com/bonus.

Figure 3.2 Engaging customers at every level of interest

At the top level of the pyramid is your free offering. This is how you get people into your database. This is where customers enter your world and learn about what you can do. They learn about your value, quality, and wisdom, as well as develop trust in your business.

At the next level, take your main revenue steam and consider what you could add to it to give it more touch points with your customers. If you would like to double or triple your price, for example, what bells and whistles could you add on that would match, or even exceed, that extra value? Everyone loves a premium service, and I guarantee there are plenty of customers out there for you within this tier.

In the third tier, you are thinking about what you could create that has a few touch points. Think of it as a watered-down version of what your business offers. Often you are bundling and packaging an assortment of items that’s more in total but less than how you would price them individually. The customer sees this as a bargain and a way to scoop up a range of offerings all at once.

At the bottom of the pyramid is the “concierge” level, where you have earned “high-level buy-in” from customers. You have built a relationship and earned their trust: Now is your time to shine and show them what you can really do! This is where you create a true experience for your customers and add extra attention and luxurious choices. One example might be to create a high-end event just for these elite customers. This is your chance to exceed expectations and wow them.

There may be some customers who stop at the second or third tier. That’s okay! The main thing is that your business model includes opportunities to welcome customers now or later at every level. They could buy the $79 coffee maker, the $2,999 coffee maker, or a variety of coffee makers in between. In the middle of these offerings, you may bundle in specialty espresso beans, coffee grinders, fancy espresso cups and saucers, or whatever makes sense for your particular business and customer.

Licensing

Another great way to expand a business without stretching yourself too thin is through licensing. Some business owners feel that licensing their brands, products, or services is the equivalent of giving away their children – but it’s not. If anything, it’s a less taxing way to make more children (i.e., products, services, etc.) without having to do any of the work. Once an agreement is done, licensing becomes primarily a bookkeeping function that brings in regular income.

A few years ago, I created an idea for software while I was relaxing near the water with my husband in Laguna Beach. From this burst of creativity, I went on to develop Interactive Life Coach to help business owners stay on track with their goals and dreams. Several people liked it so much they wanted to license and white-label it. I had no problem with the arrangement. For me, it was revenue for doing hardly anything. For the licensees, it was a way to have a proven product ready without having to start from square one. Software is a tremendous platform for scaling, since your investment is primarily in the initial build and overhead does not need to grow at the rate of your expansion.

In my organization’s Pinnacle Global Network, we work with Jon and Gila Kurtz, the cofounders of Dog Is Good, a lifestyle brand for people who love dogs. When the couple began working with us, they were primarily creating revenue through wholesaling their products to retail stores. At the time, Gila had lost her passion for the business because she was stuck in a cycle of working on areas of the business that did not make her sing. In mentoring her and her husband to build a much more scalable enterprise, my team found several ways to help them develop other revenue streams without adding tremendous overhead, so they could scale. First, we helped guide them to expand their licensing program to other product manufacturers, which has created dramatic financial growth and has exponentially expanded their brand recognition. Gila was able to step back a few steps from working in the business and create Fur-Covered Wisdom, where she shares her passion about the power of dogs and personal growth. This rebooted her passion for building her company. We also helped them design their own Signature Exhibitor Program, which became known as the Dog Is Good Mobile Pop-Up Shop and has resulted in an entire sales force of individuals hosting pop-up shops of Dog Is Good products across the country.

I can’t even begin to tell you what is happening with this program! It’s giving me an entirely new meaning in this business. I feel I’m really making a difference for these individuals who are coming on board.

—Gila Kurtz, cofounder, Dog Is Good

On top of all this, after applying my Pinnacle Signature Program Method, Gila and Jon developed Dig Delivery Auto-Ship – a monthly subscription program for retailers. This puts their purchases on autopilot! No more one-time sales. They now have recurring revenue, which is a business owner’s dream and perfect a formula for scaling. Through all of this expansion and awareness, their online sales more than doubled.

Retainers

Retainers are an excellent way for you to generate recurring revenue and reliable cash flow. This is where you can be creative in terms of thinking about what services you might provide that your clients consider valuable on a regular (i.e., monthly) basis. Rather than getting paid per project or by the hour, you are receiving a standard payment every month ($2,500, $5,000, etc.). It could be in the form of a marketing retainer, a public relations retainer, a consulting retainer, and so on. People with small tech companies can offer a range of extra services on retainer – from managing servers, databases, and websites to repairing and/or ordering software and hardware.

Best of all, when you are on retainer you don’t have to feel like you are nitpicking and justifying every hour of work you put in. Then you have the freedom to be more creative and provide a higher-level of value and ongoing support, resulting in happier clients – which is what we all want.

Some people get caught up in the “dollars for hours” model, which is very difficult to scale. One of the things I teach clients is how they can create their own signature programs and add more value to their offerings. This means you can bill more per month than what you would earn on an hourly or project-by-project basis. Instead of your clients thinking of you in terms of an hourly freelancer, they see you as an authority – an expert. In reality, they are not paying you for your time. You are worth much more than that. What they are really paying you for is your wisdom, years of experience and study, capabilities, skills, ideas, insight, and the proprietary process that you have developed.

These combined processes and unique style are what set you apart from everyone else. When you pull of your processes together in a sequential format and name each process in a unique way, the value of your offering goes way up. For instance, the SCALEit Method is a compilation of my years of in-the-trenches experience, solutions to challenges, and step-by-step processes to add clarity, ease, and faster breakthroughs and results in a more streamlined process of scaling your company. That is very different than throwing a hodge-podge of knowledge or services at your client.

Franchising

Once you have your model down and have established a couple of locations that build your profitability, you can sell your concept, systems, and marketing to others to create franchises. All you need to do in this case is develop a “business-in-a-box” that franchisees can step into and run and then help them find prime locations.

The pros of this are pretty obvious: You save the time and investment in starting up each individual new business location. Once a franchise gets going, you get to count the residuals.

It is super-important that you have a strong support system in place for your franchisees. They often do not have business experience, and that is why they are buying a franchise in the first place. The more support you offer in the way of negotiating leases, marketing, and sales, the more successful they will be; this will result in more people wanting to buy more franchises. Too many franchisors do not offer enough support to their franchisees. Sadly, this sets franchisees up to fail.

Also, franchises can be unpredictable in terms of knowing which ones will catch on, spread into other areas, and have long-term staying power. The biggest franchises – McDonald’s, 7-Eleven, Dunkin’ Donuts, and the UPS Store – have all become monster successes and have withstood fierce competition over the years, as well as thriving during changing economic climates.

On the flip side, it’s all too easy for a franchise to plummet while expanding, as was the case with Subway. The sandwich chain went through the roof during the Great Recession, adding 2,300 locations from 2007 to 2009 and another 4,000 in the United States over the next five years. But then things started to slip and locations began to close. Why? They expanded too aggressively and lowered their prices too much. The model might have worked during the Recession, but it didn’t sustain itself after that.

If your business is a “monkey business” in which you are not reliant on skilled workers, the franchise model will have more success. The way to build it is with area developers in mind, not as a onesie and twosie strategy.

Area developers are experienced business people who purchase large territories and develop them on a timely schedule. This helps create the brand footprint quicker. It’s easy to get carried away once you have a taste of success. Test locations out in the right territories to ensure the model fits everywhere and can weather – or even take advantage of – any economic storm.

Certification Programs

Perhaps your business lends itself to creating a certification program. If you and your team have expertise in an area, you can build a program that trains others to become experts as well. This is a terrific way to scale because you are getting people to sign up for a number of sessions or events so they may fulfill the certification obligation, which means consistent cash flow with people paying up front. This also expands the reach of your craft, positively impacting so many more people than you or your team can do on your own.

Get creative and develop a certification program in an untapped area. For example, I have a client who owns a cold-storage company. She’s created a certification program to help contractors become certified in cold storage. Nobody has ever done this before, and now she has an entirely new revenue stream for her company. Not only that, she has confidence in knowing she has a team of well-trained contractors to provide their cold-storage methods.

When I built the Homeopathic Academy of Southern California in 1999, I created a three-year certification program that trained hundreds of homeopaths to go out and improve thousands of people’s lives. I knew that I could see only so many clients on my own and, if I was going to make a significant difference, I needed to expand my reach. I sold the school in 2005. Because the curriculum and systems were in place, it continued to support and build the homeopathic community for years to come. When a labor of love does good things for people exponentially and creates great profit, you have a winning model.

You are probably thinking: “Aren’t I creating competition for myself by doing this?” Maybe. Then again, some of the people who become trained and certified might be so good you want to hire them yourself. If this isn’t the case, certifying others to become competition is still a lot more lucrative than soliciting new clients one by one. And, if you’re the company creating the certification process, you are now elevated as the authority in your industry, resulting in higher fees and much more business. As you certify, you shift from one to many, making it a perfect model to scale.

Buy Your Competitors

Sometimes the best way to scale is to buy your competition. They have a team that knows your industry and a built-in customer base. Occasionally, with the art of negotiation working for you, you can catch a company at just the right time.

This can create a quick boost to your growth without years of building. Whether this competitor has been a thorn in your side or a supportive peer, this smart purchase will give you a big leg up in the scaling process.

One of my clients owns a machine-calibrating company. One way they’ve scaled is by buying several competitors who do the same exact thing. They’ve rid themselves of their competition and grown their businesses, to boot. This is a quick way to scale without starting at ground zero.

There are challenges in buying other companies. First, of course, there are the financials and making 100% certain that the prospects are profitable and solid and the books are clean. Then you have to make sure the new team fits in with your culture and that the employees are motivated and skillful with your processes. Once you employ them, you must train them and make them feel as if they are an equal part of the team so they can get on board with your Big Picture Vision.

Your Business Blueprint: Marketing and Cash Flow

Business without marketing is no business at all. You won’t have cash flow if you aren’t getting the word out about your product or service. If you know how to reach and market to your customer, you can pretty much build any type of business successfully. I am so grateful that my first company was an advertising/PR firm. I had no idea what I was doing in the early years. It was education by fire (and there were lots of fires). I have been able to apply that marketing knowledge to all of my nine subsequent companies.

The first order of business is targeting the right customer. You need to identify:

- Who is your ideal customer?

- What does she/he desire?

- Can you reach her/him?

- Is this customer willing to pay for your product or service?

- Who is the competition?

- What is their message and how can you do it better?

If you can’t answer the above questions, you’ll go too broad or too narrow with your marketing and will completely miss the target. So many marketers bang their heads against a wall because they are trying to get the wrong customer to buy. It’s way too easy to keep throwing money away like that.

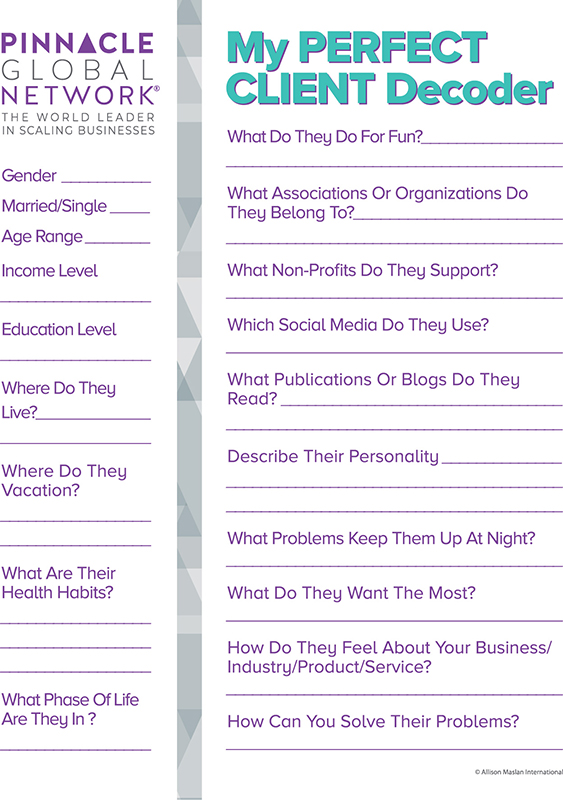

My Perfect Client Decoder

Take a look at the worksheet entitled My Perfect Client Decoder (Figure 3.3), copy it, and fill in the blanks on a separate sheet of paper. Essentially, you are looking to identify your customer demographic and psychographic. It’s not just honing in on obvious things such as gender and age, it’s also pinpointing your customers’ phase in life. Where are they currently? What are their buying habits and their values? Why do they buy?

Figure 3.3 Identifying the perfect client.

You might, for example, identify that your customer is in the life phase of having babies. Well, that is a pretty big age range; moms can be anywhere between their 20s and 50s. As you can imagine, marketing to a 20-something is quite different from marketing to a 50-something, even though they share the commonality of having babies.

Once you have a crystal clear picture of your customer, then you can figure out how and where to reach them and the best way to catch their attention and communicate with them. One of the easiest, least expensive, and most accurate ways of doing this is to go direct to the source. Take your best clients to lunch. Tell them they are your favorite clients and why you love working with them. Ask if they would be open to your interviewing them to learn more about the their patterns because you want more clients just like them!

Find out the following:

- What blogs do they read?

- What books do they read?

- What sporting events do they attend?

- What hobbies are they interested in?

- What charities are they involved in?

- What TV shows do they watch?

- What things excite them?

- What things make them angry? (This is where their passion and pain lies. If you can speak to this, your chances of capturing their attention go way up.)

Once you have figured these things out, then you must decide on the vehicle, or the marketing medium, that you’re going to use to reach them – whether it’s social media, pay- per-click ads, TV commercials, email lists, or some other method.

Your Database Is Your Gold

One of the best, most effective kinds of marketing is one that can be automated so you’re developing relationships with your customers and building on them over time. Pay close attention to this: Automating the relationship does not mean setting things on autopilot. It does mean knowing your customers so well that you have identified their interests, can market to them on a dime, and always have them on your hook to buy more.

Continuity marketing programs accomplish this exceptionally well. Similar to the offer process, from entry level to premium choices, mentioned earlier in this chapter, by giving customers an opportunity to opt-in their contact information for a free gift that is of great value, you begin to build your database, which is your gold. You don’t own your list on social media. The social media platforms do. When they opt-in to your list, this actually increases the valuation of your company when you go to sell it. When Borders Group national book chain went out of business, Barnes & Noble did not want their furniture; instead, they bought their database! Once you have established this connection, you can build a long-term relationship that ultimately turns into a customer. After a period of nurturing with great educational, entertaining, and authentic content that speaks to the customers’ pain points, you can ask for the sale, starting with a lower-level offering and building on up to your premium offer. By continually staying in front of them, by being a giver of good content, great service, and following through on your promises, your customers will continue to come back for more at a higher price.

Perhaps you are old enough to remember one of most famous of these, Columbia House, which back in the 1970s and 1980s offered records and cassettes for only a penny apiece. For your investment of only one penny, you could get something like thirteen records. After that, you were obligated to purchase records at full price – by which point you’d pretty much exhausted any music they had that you’d actually want to hear.

The genius of Columbia House wasn’t just that they were reeling you in to buy all those records. What they were really doing was building their customer database (okay, at the time it was known as a “mailing list”) in order to create relationships and sell more stuff to the same customers. In all likelihood, they were probably selling those mailing lists as well.

Earlier in this chapter I stressed that “free isn’t a business model.” This only applies to your products and services, not to your marketing. Think about what you can offer of value to your customers free of charge that costs you pennies, but has great upside when those customers come back to you later for more. Don’t be afraid to share your great wisdom, ideas, insights, in the form of downloads, so that they can get to know the value of your expertise. This positions you as the expert in your arena and sets you apart from your competition. They’ll say, “Wow, Allison really offers some interesting things. I’m not ready to buy, but when I am she’s the one.”

Nurturing trust at this stage is crucial. If you are too aggressive and push too hard for the sale, you risk sounding desperate and putting people off. It’s okay if they don’t buy from you right when they receive your free gift. The fact that you aren’t being too pushy is actually appreciated by most customers and then they want to buy from you.

Think about it this way: Would you ask someone to get married on the first date? (I retract this – maybe it can happen. One of the business mentors on my team met a woman at a bar in Las Vegas. They got married that night and they’ve been happily married for eight years. There are outliers to everything, I suppose.)

Raving Fans Become Your Sales Force

I’m not going to get into the nuances of which social media platform is the best to use for marketing purposes because they are changing all the time, along with our technology. Whichever platform you choose to use, depending on your target market, you need to focus on how to generate buzz and excitement and build a raving fan community.

The important note here is “the unexpected gift of support.” Most people get a sense of when to expect promotions or giveaways, but when you give your prospect or customer a forward-thinking product or service that is in line with what he or she desires, needs, and expectations and then give him just a little bit more, you’re well on your way toward creating a raving fan.

When you have dedicated, faithful customers online or offline, these individuals automatically become voices for your product. In a sense, these raving fans become part of your sales force. They offer five-star reviews, comment and share your online content, and go out of their way to support you and introduce you to their favorite connections. This is how you build a tribe and a movement gets started.

When I began putting a good portion of my marketing dollars into more customer love and appreciation, the referrals and renewals jumped up dramatically. This is one of the best returns on investment you can get – and it feels rewarding, too.

How Much Do I Invest in Marketing?

When determining how much to invest in your marketing, you first must back up and determine your Customer Lifetime Value (CLTV), which is a prediction of the net profit attributed to the entire future relationship with your customer. Here is a simple formula:

average value of a sale × number of repeat transactions × average retention time in months or years for a typical customer = CLTV

For instance, if your customer lifetime value is $3,000, and it costs you $500 to acquire that customer, you will happily spend that $500. The point is, you’ll never know how to develop a solid marketing budget unless you know what the return on your investment needs to be. This knowledge is vital because it will help you make marketing decisions based on the reality of your own numbers, rather than the promises of some new media program.

The Richness Is in the Relationship

I invest a lot of time and money in building relationships. In over 30 years of business, relationship building is at the top of the list with regard to how I grow my companies; it’s also one of my favorite parts of being a CEO. I invest well over $150,000 a year on getting in front of the right people. This includes being in a high-level mastermind – which I will soon explain – and attending events or cruises filled with influencers, the people who can open doors for you. One right connection can save you years of trying to reinvent the wheel.

Greek shipping magnate Aristotle Onassis was known for telling the story of what he would do if he lost his fortune. He said he would take on three jobs. From his earnings, he would carve out and save $500. He would spend all of it on one expensive meal – just to get close to someone who could open doors for him. Sitting next to the right person and making a connection with him or her is the fastest way to create your fortune.

What tribes are, is a very simple concept that goes back 50 million years. It’s about leading and connecting people and ideas. And it’s something that people have wanted forever.

—Seth Godin, bestselling author, marketing authority, and entrepreneur

I’m constantly giving my clients strategies intended to help them get in front of the right people. “One connection can potentially be worth millions of dollars.”

Make a list of some big goals you would like to accomplish. Think about someone whom you may know or do not know that could possibly help you make these goals a reality through his or her own resources or network. This may be a well-connected business owner, a celebrity, or anyone who is well known in your industry. First, make the intention that you will meet that person. Then research the best ways to make that connection. This could be through an introduction, a charity, an event, an email, or even a letter or phone call. It may take a combination of phone calls and emails. Get creative! It may not happen overnight, but persistence always pays off.

When I had my ad agency, I wanted to meet Larry Lawrence, the owner of Charlotte Russe clothing chain. I called his office at least a dozen times without success. Then, one day he finally called me back and said, “I am calling you, so you will stop calling me.” He ended up becoming my biggest client and we helped Charlotte Russe take their stores from 15 to 50. I made enough money to put a down payment on a home within six months.

Being a connector also means taking the initiative to connect other people without any specific benefit to you – except that you develop a reputation as someone who helps others and then it becomes even more likely that people will help you without you even trying. If you want people to connect to you, you must reciprocate and be a connector for them as well. For example, if you know someone who just finished writing a book and you happen to be good friends with a literary agent, you might introduce the two.

Life gives to the giver and takes from the taker.

—Joe Polish, marketing authority, entrepreneur, and innovator

Networking does not mean meeting people; it means becoming the type of person other people want to meet.

—Jay Conrad Levinson and Jeannie Levinson, authors of Guerrilla Marketing

Factoring

If your profit margin allows for it, you can factor your accounts receivable at 4–5% of your committed invoices. The way this works is that you receive money up front from the factoring company and then they collect the payment from your client. For instance, if your Net 30 invoice is $1,000, the factoring company will pay you $960 and collect $1000 from the client. You receive payment faster, so you can use that money to buy inventory or even reinvest it for more business. It is an easier qualifying strategy because they are looking at the strength of your customer, rather than your financial statements.

Presales Is Where It’s At

Amazon does it. Apple does it. Nearly every innovative company does it: preselling their products before they are ready and available. Giving customers a tease or taste of coming generates curiosity and buzz. Apple is brilliant at tantalizing its customers into jumping to buy the next generation iPhone. In addition, preselling gets your production and sales teams pumped in anticipation, which leads to great things happening up until the very end. You also gain the benefit of getting insights into customer reactions early, which can help you forecast inventory to meet demand.

Many of the products we have sold in my companies started as presales. Do your marketing first, then deliver your product. You can perfect it along the way. There is a saying that I love: “Build the plane while you fly it.” In other words: Don’t wait until it’s all finished and tied with a bow to start selling the product. Get your marketing going, create a buzz of excitement, and attract some cash flow. Then, when your launch happens, you’ll already be sitting pretty with sales.

Are You Undervaluing Your Products?

While I’m an advocate of promotional discounts in some instances and other marketing incentives, I am equally as dedicated to opposing pricing models that are too low and undervalue your products and services. Some business owners become afraid that customers won’t buy from them unless they are priced lower than their competitors. The truth is, you may get a customer through a lower price offering – but you won’t keep a customer this way. You want to attract customers who truly value you and what you offer. If you drop your prices too low, what you are projecting to the marketplace is that you don’t believe your product is worth that much. Studies have shown that customers believe higher-priced products are more attractive and more valuable. Timex is said to be a better-made watch than Rolex. However, Rolex has built a brand identity that expresses longevity and success, which allows them to charge a lot more. People will invest to be associated with a brand of such stature and prestige.

A few years back, I was speaking on the phone with a woman who offered a workshop I was interested in attending. She quoted a price of several thousands of dollars. Although it was expensive, I was still highly interested because I believed the workshop offered something that would help me immensely. I paused for a moment to think about it. That silence must have made her nervous because she dropped her price – and then again a few seconds later. In that moment, I completely lost interest. She did not have confidence in her product; therefore, I lost confidence in her ability to deliver it. If she had held her price, I have no doubt I would have made the purchase.

The key is that the price must match the value you’re offering. Would $1 extra per unit matter to the customer? $10? $100? $1,000? If your customers want to work with you and care about you, they will stay with you and trust your judgment on pricing. If one of my dedicated vendors were to raise her prices, I won’t just jump ship and go somewhere else. In most cases, I trust my vendors so much I would believe that the increase is justified and that they deserve it.

Your goal is to expand your margin as much as possible. Match your fee with the value you are offering. If you’re working day and night and not making money, you’re not charging enough.

Being Change Adaptive to Make Some Change

Lastly, when it comes to marketing or any plan of action, you need to be flexible and change on a dime when your market changes or your strategy is not working. Business is a living, breathing, ever-changing dynamic, so you must always be testing and tracking your metrics to see what is working and what is not. Just because a marketing strategy worked for years does not mean it will continue to do so. Businesses get left in the dust or disrupted all the time because they do not stay nimble. Look at what is working and what is not. Then be willing to move quickly.

Mike, my husband (yes, I did finally find my forever Prince Charming), has run a company called CA Office Liquidators in the office furniture industry for over three decades. When large companies are moving or going out of business, his company buys their used furniture (cubicles and workstations) and then sells them to other companies. A few years ago, he realized his competitive advantage was his unique method of brokering the entire inventories to other new and used office dealers versus retailing the furniture in smaller sales to the end users. This was much more profitable and enjoyable rather than dealing with the onesie, twosie sales to the end user. This sharp pivot drastically reduced his overhead because he did not need massive warehouse space. The end result was that it increased his profits by 40% within six months.

In your business, you must be willing to monitor the results of your cash flow and marketing tactics and react appropriately in the moment. Often a small shift can be life changing for all involved.