CHAPTER 5

Establishing a Solid Lifeset

Tell me how you use your spare time, and how you spend your money, and I will tell you where and what you will be in ten years from now.

—Napoleon Hill

Mindset: A person’s way of thinking and their opinions.

Lifeset: A person’s way of living and their choices.

As discussed in Chapter 3, your mindset is the primary driver for your success and that mindset is most deeply impacted by the WHO, but how it plays out in your choices and everyday living is what we call your Lifeset.

“All you have to do is put your mind to it.” So untrue! Yes, of course, when you set your mind to a side hustle, you are focusing your attention and thoughts on it. But thoughts and mindset are not “doing.” You need action. You cannot just plan, you must live out your plan and also need follow-through—but it needs to be the correct action and correct follow-through. Many people fail to apply proper mindset, as it gets lost in translation when taking action and applying it in their lives. This is precisely why when we mentor other side hustlers, we advise them to begin looking at the results their mindset is producing, their Lifeset.

We can provide countless examples of those ready to side hustle, coming to us for advice or mentorship, but when their job is shaky, their finances are upside down, and their relationships are on the rocks, what real concrete business-building power moves can they actually make? Many people may understand a mindset principle conceptually, but it’s not reflected in their choices, leaving them without firm footing or a strong foundation to build upon.

You can categorize Lifeset into many different pillars in your life such as health, spiritual, relational, financial, and so on. There are ample books on each of these areas and we recommend making them all a priority. However, for the sake of this book, and when it comes to side hustling, we want to invest time into these two pillars: your career and your finances. Without making quality choices in these two categories, your foundation always remains unsteady, making it difficult to build that bodacious side hustle and manifest your dream life. Pillars are used in architecture for support, and when you have a stable career and strong personal finances, you can properly fund and support your side hustle in a sustainable way, and vice versa—creating a synergistic cycle.

To build wealth beyond the day job requires some form of investing. Investing time, money, and education (which often costs both). You also have to be willing to embrace some level of risk that it may not pay off. This requires an elevation of one’s Lifeset; however, most people don’t have close exposure to people living out the decisions and choices required to play at such an elevated level. Recall that without the WHO, a real example, it is difficult to piecemeal this together. This chapter is designed to help you build out the most relevant elements of a strong Lifeset, and as you seek out the WHO, your chances of your success radically improve.

Fortunately, you don’t have to start out with an immaculate Lifeset in any particular category. We have empowered many people to evolve in these key areas and have watched their careers and personal finances make massive leaps forward. We want to share these fundamental lessons with you now.

Winning in Your Career and Side Hustle(s)

We have seen scores of individuals fail in their side hustle because of a job, career, or other income-related challenges. Ironically, many people are building a side hustle to replace their job income, but the first thing most side hustlers move to the back burner when they have a career challenge is . . . their side hustle. Despite the millions of people talking about the value of a side hustle, we have yet to encounter any content that specifically speaks to this challenge or provides real hard-hitting content and advice. This section provides you with specific Lifeset choices and examples you can implement immediately.

One of the many perks of having a side hustle (or hustles) is that you don’t have to feel the need to put an overwhelming amount of pressure on your job. Once you have created a business of your own, your job no longer holds the responsibility of having to “complete you” or fill all of your emotional and financial needs. Having a side hustle gave us the freedom to look for a plan A that paid us well enough to generate extra cash to fund our side hustles, and provide us the flexibility we needed.

10 Tips for Winning in Both Your Career and Side Hustle

1. Find an industry or role that provides flexibility. We took roles in job sectors that were either standard banking hours or remote roles allowing us the freedom to run appointments for our side hustles. We cannot overstate the value of this. Had we taken jobs that buttoned us down tight for 50-plus hours a week, we would likely still be stuck there, too busy with our jobs to build a side hustle and create independence!

2. Get paid as much as you can—assuming it doesn’t seriously limit your capacity to run your side hustles. Over the years, we have generally advised people to take the promotion or the pay raise, but we have also advised many people to decline promotions. Sometimes an extra $5,000 or $10,000 wasn’t worth the stress or increased time investment that would pull them away from developing their side adventures and building wealth.

3. Maintain integrity in your job role. Don’t take a job that has a clear conflict with your other ventures, and always perform the responsibilities as assigned to you. You don’t want to sacrifice your honor to run a side hustle outside of your job. If there is a clear conflict, take this into consideration at the interview stage, consider switching roles, or perhaps put a temporary pause on your business activity.

4. Go early or stay late. We generally recommend going in early. This often gives you access to your boss, a jump on the day, and the ability to depart at closing time sharp, and go crush your side hustle.

5. When you’re at your job, be focused and productive. Don’t waste excessive time at the water coolers and the coffee pots of the corporate world. Do not invest a lot of time complaining about your job, the company, your coworkers, or your clients. In general, complaining is extremely unproductive and doesn’t serve the greater good. We found if we put our heads down and stayed focused on our roles at work and the things we could control, we were substantially more productive than our counterparts.

6. Work for competence and success—but establish boundaries for the time you invest in your job. Deliver quality, good work. Make sure your boss and clients are happy. At the same time, you don’t need to break any company world records. We were OK to invest up to 45 hours a week (as necessary) into our careers, but not 60 or 70. We had other assets to build and were interested in developing wealth, not just collecting extra kudos at the office. It requires immense discipline not to get swept up in the culture and grind of your job environment. Your managers and coworkers are likely one-sport athletes, but you have to think of yourself differently, and when the evenings, weekends, or lunch hours strike, be able to make a sharp pivot in a completely different direction.

7. Learn how to manage your manager. We always wanted our managers to realize we were on their team. We are not advising you to brown-nose—but make sure to let the captain of the team know you’re a team player and will do what it takes to support them. Your boss needs to know, if you’ve been handed a project or clientele, it will be handled—bottom line. Understand your boss’s priorities and underlying goals so you can help them. Our goal was to be the lowest-maintenance but highest-performing direct reports our managers had. As our side hustles grew, we didn’t need to have the top numbers at work, but we never complained or had personality issues. Their ROI on us was going to be solid. In turn, our bosses came to trust us; so if we wanted to leave early, work from home, or needed some extra time off, it was a nonissue.

Craig here. One year, instead of requesting an additional raise, I asked for an extra week of unpaid vacation (thanks for the tip, Dad). My manager wasn’t willing to do so above the table, but he was below the table. Comically, the same year I received the highest annual merit raise in our division. Post-review my boss laughed and shared, “Well, Craig, I can give you a bigger raise because 9 percent of not much (in reference to my salary) is still, well . . . not much.”

That extra week of vacation and flexibility gave us the peace of mind and freedom to hammer our side hustles in the evenings and weekends. Keep in mind, as someone building assets and businesses outside your job, your time is more valuable (monetarily) and has a greater opportunity cost. A day off or even an hour longer lunch meant a chance to buy our way out of a job faster.

8. Work your freaking face off. After writing several chapters in this book, we realized how little we have discussed our work ethic, or more important, the work ethic that necessitates building a successful side hustle. Now if you are smarter than us, are leveraging better systems than us, or were straight up dealt pocket rockets on your first hand at the table of entrepreneurship (poker reference for “extremely lucky”), you won’t have to do the following.

But personally, we worked 20- to 50-hour workweeks in addition to our jobs, through much of our twenties. Few business owners at high levels of success don’t work their guts out at some point in their journey. We don’t apologize for it, and I’m not saying you will or need to. A good rule of thumb if you are looking to create real momentum from your side hustle: for every hour we put into someone else’s business, we were willing to invest an hour into our own.

Keep in mind, being a successful entrepreneur is not a right, it is a privilege you earn with your toil, sweat, and willingness to learn and make smart, sometimes difficult decisions. We feel confident if you execute on much of the advice listed above, your capacity to crush your side hustle will improve.

Financial Management

To run a side hustle, you need capital (aka money). How much, how often, and where that money comes from varies, but most side hustlers fund their business via their personal savings or surplus cash flow from their job. Therefore, optimizing your personal finances supports your side hustle in three critical ways:

1. It supplies your side hustle with the capital and funding necessary to launch and continue in a sustainable way.

2. It disciplines and educates you to manage your money properly, so you can in turn manage your business’s finances well. If you cannot manage a $60,000 salary well, how will you possibly manage the cash flow of a $600,000 business?

3. Many aspiring side hustlers do not realize that banks and other lenders provide business loans based primarily off the proprietor’s personal finances and credit scores, not the businesses. Banks are unlikely to lend to a small business if the owner has few assets or marginal credit.

Essentially, your personal finances and side hustle’s finances will be married for years to come, potentially until death due you part.

Because of the importance of having all your personal finance ducks in a row, we want to take our time here and provide you as much value as we can through detailed and poignant Lifeset examples and tips. This section focuses primarily on your personal financial management for the preceding reasons. Please note, we build on this foundation and discuss how to raise additional capital for your business more specifically in Chapter 10.

We have met many smart people who make poor financial decisions due to a lack of either education, inexperience, or a low FEQ (financial emotional quotient). Learning how to optimize your resources provides you the best chance to invest in your side hustle.

Some disclaimers: We are not financial advisors, certified public accountants (CPAs), or attorneys. Craig does have degrees in finance and economics, a concentration in financial planning, and 15-plus years of experience in commercial finance and banking with some major financial institutions. As a former commercial credit analyst, risk analyst, and business banker, he has likely seen the guts of more financial statements than many surgeons have seen the actual guts of humans. On top of that, together we have scaled multiple businesses, assisted many aspiring entrepreneurs, and advised business owners and entrepreneurs how to run and financially manage their firms across many different industries. Most important, we earned the right to step away from our traditional jobs and control our time because we managed both our revenues and expenses effectively.

We will not focus on how to invest a $100,000 and turn it into $500,000 or how to short sell shares in Blockbuster. That’s not our expertise (although we certainly have our opinions). Instead, we focus on how to help you make smart Lifeset decisions and put yourself in the best position to cash flow your life.

People often come to us asking for financial advice—whether they should buy a particular car, put more money into their 401(k), or take an all-commission job with a higher-earning potential. The answer is: it depends.

It depends on your current state and your desired future state. What are you trying to accomplish? What is the destination? How does this decision impact your other assets or liabilities? What is your age, tax bracket, current debt? Be wary of anyone who is willing to dole out financial advice but doesn’t understand (or even ask) these questions. The saying “free advice is worth what you paid for it” is often spot on—and unfortunately, “free” can actually be extremely expensive.

We recommend side hustlers get into the simple groove of making more than they spend. If this is a large problem, we provide you with some basic guidelines, but there are additional books that go into much greater detail, like The Total Money Makeover by Dave Ramsey. These resources are particularly important if you are consistently upside down in consumer debt, as you likely have deeper systemic issues in your thinking.

Fortunately, Craig grew up in a family of relatively pragmatic and frugal engineers who helped him understand the importance of not spending money you do not have, and from a savings perspective, this has served us well. Unfortunately, many people are not taught this discipline growing up. The best thing you can do is learn it now and begin living it now, so your next generation has a good example.

However, if your goal is to build assets, businesses, or investments and step away from corporate America at an untraditional age, just saving money alone is likely not enough. You need to build on top of this foundational Lifeset to create wealth at a faster rate. As a result, your peers no longer become good markers of progress or the quality influence you need.

Step 1: Develop a Budget

The best way to know what direction to walk in next is to know where you want to go. The next best is to understand where you are. If you want to go to Chicago, should you go east or west? It depends if you live in Colorado or New York.

People often do not have a clean line of sight on their current financial situation. We have witnessed this firsthand as we have helped people from high school students to high-end income earners and entrepreneurs with their budgets.

Burying your head in the sand doesn’t make a hurricane go away. You need the financial courage to take a real look at what you’ve got and what you don’t.

There are two fairly elementary components to assessing your financial health: a balance sheet and an income statement. A balance sheet is a snapshot in time of all your assets and liabilities. The income statement is a list of all your incomes and expenses over a period of time. We generally recommend running a budget based on your monthly spending but basing these numbers off annual averages.

It is mind-numbing to us the level of detail people know about a professional sports team, their project at work, something in the political world, or the Kardashians, and yet have no idea how much money is in their 401(k) from their prior employer.

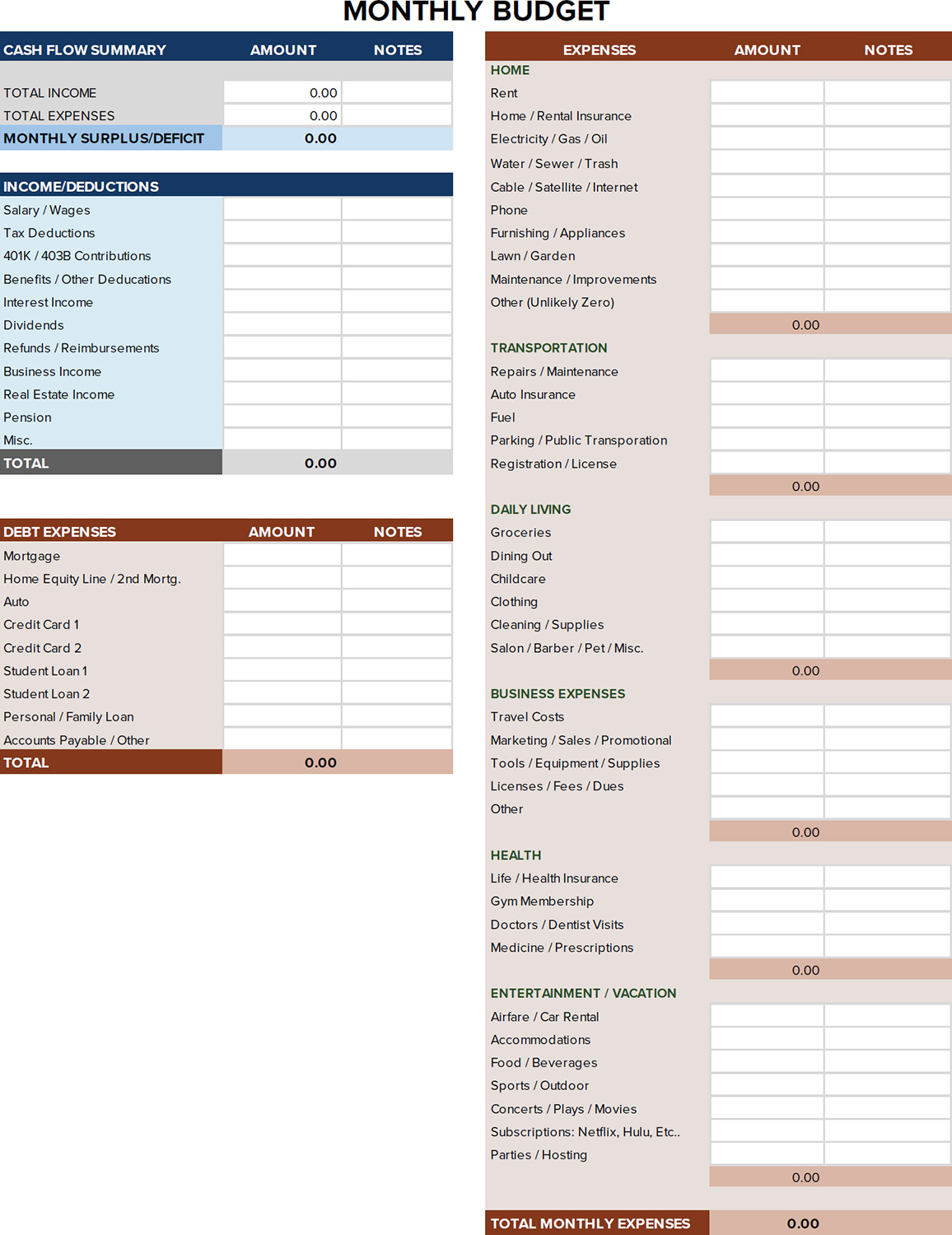

Figure 5.1 is a budgeting sheet that’s relevant for most people who read this book. (You can also find this document for download at tandemconsulting.co.) There are more detailed budgeting worksheets, but it’s important to use something that doesn’t feel overwhelming or intimidating and to work on the numbers that are relevant to the level in which you operate.

FIGURE 5.1 Personal Monthly Budget

Once you know where you stand financially and how you are cash flowing, and have taken an honest look at your real-life expenses, your debt structure, and what types of interest rates you may have, then you can decide how to apply your surplus cash or monthly cash flow.

Having a solid budget is one of the first steps in making major financial progress. If you don’t know what you have or what you owe, you cannot assemble a good plan. Here are some key elements to consider:

1. In general, do you make more money than you spend? If not, how can you begin cutting back expenses or increasing your income right away? If you do cash flow, how can you optimize it?

2. If you have debt, what type of interest rates do you have and how can you pay this off or move to lower interest rates? If you have debt, do not ignore it. Look at it directly and put a plan together right away. Even small amounts of progress paying off debt creates important forward momentum.

3. If you have savings or other assets, you can use these to enhance your wealth. Make sure your assets are in the right financial buckets and managed by quality money managers you trust.

4. What are your financial goals? What is the proper timing to achieve those goals based on where you are now?

For many people, simply having a fully completed balance sheet and listing out their incomes and expenses is in and of itself 80 percent of the work. Of course, if you have internally labeled yourself as not a “numbers person,” hiring someone else to go through this with you can be helpful.

Step 2: Earning Income

We believe if you are going to have a job, you should get the most leverage from it! Meaning, many people either don’t make enough income, or their time is so buried in their job they don’t have the freedom of flexibility to create income outside of their job, which is the point of a side hustle in the first place. Here are a couple challenging scenarios people may find themselves in that are not addressed in the prior section:

![]() Being underpaid at your current job. In this case your wage and skill sets would let you make more, but you haven’t fought, pushed, worked hard enough, or demanded better pay or a more flexible role that puts you in pole position to crush your side hustle. In these scenarios you need to step up and ask for it. Not in a demanding way, but in a well-thought-out, smart, and confident way.

Being underpaid at your current job. In this case your wage and skill sets would let you make more, but you haven’t fought, pushed, worked hard enough, or demanded better pay or a more flexible role that puts you in pole position to crush your side hustle. In these scenarios you need to step up and ask for it. Not in a demanding way, but in a well-thought-out, smart, and confident way.

![]() Assuming too much responsibility and work for the role you have. Remember, you don’t have to be the superstar anymore; you just need to do good quality work. There is a different set of goals for you. Learn how to manage your time, your boss, and your role more effectively so you can earn more flexibility, not just income.

Assuming too much responsibility and work for the role you have. Remember, you don’t have to be the superstar anymore; you just need to do good quality work. There is a different set of goals for you. Learn how to manage your time, your boss, and your role more effectively so you can earn more flexibility, not just income.

![]() You have not developed enough skills or marketability to acquire a role that sets your life up for foundational financial success. Let’s be honest, if you are working for $11/hour in the United States right now and trying to support a family or dependents, just paying your bills and managing life is likely a financial struggle. You are probably more focused on survival versus leveling up, because life is expensive. Carrie’s favorite quote from the play The Humans is “Why does it cost so much to be a human being?” Many can relate to this sentiment, whether fleeting or chronic, and no doubt many individuals face significantly more barriers in regard to the constraints they must overcome. We acknowledge life is not always an equal playing field. However, as much as possible you have to fight to develop new skills, habits, mindset, and associations that can support you in a positive spiral upward. Work to access a distant relative, community leader, or religious organization that you think will give you exposure to their mindset. And in the interim, cut back on any unnecessary expenses as you push yourself into a new environment, school, or other certification program where you can upskill your abilities, hourly wage, salary, or marketability and get the cash flowing. We cannot always guarantee a victory, but you owe it to yourself to fight for it.

You have not developed enough skills or marketability to acquire a role that sets your life up for foundational financial success. Let’s be honest, if you are working for $11/hour in the United States right now and trying to support a family or dependents, just paying your bills and managing life is likely a financial struggle. You are probably more focused on survival versus leveling up, because life is expensive. Carrie’s favorite quote from the play The Humans is “Why does it cost so much to be a human being?” Many can relate to this sentiment, whether fleeting or chronic, and no doubt many individuals face significantly more barriers in regard to the constraints they must overcome. We acknowledge life is not always an equal playing field. However, as much as possible you have to fight to develop new skills, habits, mindset, and associations that can support you in a positive spiral upward. Work to access a distant relative, community leader, or religious organization that you think will give you exposure to their mindset. And in the interim, cut back on any unnecessary expenses as you push yourself into a new environment, school, or other certification program where you can upskill your abilities, hourly wage, salary, or marketability and get the cash flowing. We cannot always guarantee a victory, but you owe it to yourself to fight for it.

![]() If necessary, get a part-time job or cash work to fund your side adventure; essentially, get a side hustle to fund the side hustle. There are many ways to make extra cash—from having a garage sale, becoming a bartender, selling shoes on eBay, driving for Uber, and so on. Figure out what you have to do temporarily for cash so you don’t have to give up on building a side hustle that can significantly impact your life.

If necessary, get a part-time job or cash work to fund your side adventure; essentially, get a side hustle to fund the side hustle. There are many ways to make extra cash—from having a garage sale, becoming a bartender, selling shoes on eBay, driving for Uber, and so on. Figure out what you have to do temporarily for cash so you don’t have to give up on building a side hustle that can significantly impact your life.

Step 3: Managing Expenses

Overspending and living beyond one’s means is a ubiquitous and systemic problem in our culture. We live in a consumer-based society that is constantly sending us subliminal and blatant messages that you are not good enough, sexy enough, or will not be happy unless you own the newest gadgets, nicest clothes, or fanciest car. Now, this is not to say we are against buying nice or even expensive things. But we have been relatively good about not buying fancy things, especially beyond our budget, solely to impress other people or to fulfill an emotional void.

Questions to Ask Yourself to Curb Overspending

![]() Is this the most valuable thing I could spend this money on?

Is this the most valuable thing I could spend this money on?

![]() Does this purchase bring me closer to my/our family’s Life Vision?

Does this purchase bring me closer to my/our family’s Life Vision?

![]() When I purchased these items in the past, did it improve or hurt my self-image?

When I purchased these items in the past, did it improve or hurt my self-image?

![]() Do I have the financial strength to afford this, and have I earned the right to this purchase?

Do I have the financial strength to afford this, and have I earned the right to this purchase?

![]() Would I or my loved ones feel more secure if this money was cash in our checking or savings account?

Would I or my loved ones feel more secure if this money was cash in our checking or savings account?

![]() Instead of spending this money, would I be happier if I invested it and had more in the future? (Consider, money invested now at a 10 percent rate of return will double in about 7 years and multiply by 10 times in 30 years.)

Instead of spending this money, would I be happier if I invested it and had more in the future? (Consider, money invested now at a 10 percent rate of return will double in about 7 years and multiply by 10 times in 30 years.)

When people spend money they haven’t earned yet, they sell themselves into financial bondage. They now must go to work for the next six months or several years just to pay for something they purchased today. This can be a painful cycle.

Example

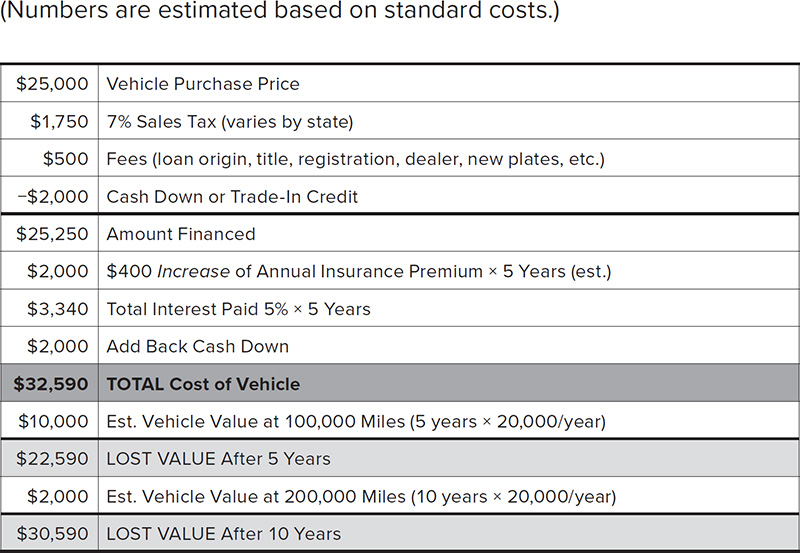

Suppose you buy a new car for $25,000. You don’t have the cash to pay up front, so you put down only $2,000 and finance the rest at 5 percent interest. Take a closer look at what the vehicle is actually going to cost you in Figure 5.2.

FIGURE 5.2 Vehicle Purchase

So if at the financial outset of your life, the biggest purchase you are going to make is theoretically worth $25,000, but you are paying $32,000-plus, and after 5 years it is worth $10,000 and after 10 years it is worth $2,000? Minus the value you got from driving, you just blew $30,590. Now if you are worth $800,000 and make $200,000 a year, go for it. But if your net worth is $50,000, you just blew over 60 percent of the entire net worth that it has taken your entire life to accumulate.

On a salary of $60,000 and take-home of $50,000, you literally have to work nearly 8 months of your life just to pay for a car that is worth almost nothing 10 years later. Now we are not anti-borrowing at all—it does provide a way to leverage the cash or assets you have—but if you do overspend on something, consider a home, land, or an education, as these typically provide or hold stronger value over time.

Homes also are taxed and require insurance but a $300,000 home after 10 years is usually worth around $300,000, not $3,000. Think about it. Buying an expensive vehicle is generally a cruel thing to do to your balance sheet and financial future. Of course, these are general numbers. Sometimes people get all uppity with us and say, “Well, my truck will be worth more than that after five years.” Great. The math is still inaccurate. If you would have bought a $10,000 used sedan with 60,000 miles (under warranty until 100,000) and put down $2,000, total cost of your taxes, depreciation, and interest are significantly less.

Until you have earned and saved $20,000, totally unencumbered in cash, you don’t truly understand the value of $20,000.

It is a completely different experience to write the check in cash because you have created the savings. If you have never created it, you don’t know how hard (or seemingly easy) it is. Interestingly, when you actually have money available to you and understand how hard you worked to generate it, you know what you truly value by how you spend it. One way we vote on our values is with our money. We acknowledge this mindset of “if you don’t have the money, don’t spend it” is considered contrarian by much of society, but so is building a successful business.

We are not saying you should or should not buy a quality vehicle. Buy whatever kind of vehicle you want. We simply want to empower you to think for yourself. This goes back to values; if you have young children and live in the mountains, and acquiring a safe vehicle is heavily valued, invest as necessary.

Now that you have our line of thinking you can apply this same mindset to other things you purchase. If you make $25/hour and you buy something for $500, you are also paying the sales tax on it, losing the time value of the money it could make on the market, and if you finance it, you are spending quite a bit more than $550. That’s 22 or 23 hours of your life you just traded for the “thing” you now own.

A few common problematic areas we see for many people are listed as follows. Please challenge yourself to consider if any of these categories are causing you unnecessary pain and if those resources could be better allocated toward building a side hustle!

![]() Vehicles, expensive clothes, jewelry, dining out

Vehicles, expensive clothes, jewelry, dining out

![]() Alcohol (in particular at bars, restaurants, etc.), junk food, cell phones, TVs, gadgets

Alcohol (in particular at bars, restaurants, etc.), junk food, cell phones, TVs, gadgets

![]() Cars, expensive vacations, concerts, sporting events, subscriptions (be wary as these are residual expenses!)

Cars, expensive vacations, concerts, sporting events, subscriptions (be wary as these are residual expenses!)

![]() More home than you need, and expensive toys such as snowmobiles, boats, motorcycles, etc.

More home than you need, and expensive toys such as snowmobiles, boats, motorcycles, etc.

Many struggle to see how they will supply the investment money or manage the operating cost of starting a business. When you minimize costs like the preceding, you may find you have enough money to fund your business. As you review your budget, continue to look for other opportunities. Perhaps it’s large items like rent or a car or smaller bills like your cell phone, internet, or auto insurance. Shop these services every couple of years to keep your current providers honest and competitive.

Managing Credit Cards

We run everything through our credit cards because of the rewards we receive and the average 40-day payment delay on the bill lets us keep extra cash on hand. We pay every bill off in full and do not pay fees or interest. If using a credit card to pay certain bills like car payments, tuition, and auto insurance requires an extra fee, we pay using cash or direct withdrawal from our checking. We don’t generally advise paying extra percentage points.

However, if historically you’ve had a problem overspending, then we do not recommend using credit cards. Until you have the self-discipline to properly manage them, you should not use them. If you charge it, you should have the cash in the bank to pay for it.

Unless an emergency, do not carry ongoing credit card balances and make sure all your payments are made on time or your interest rate and fees will go through the ceiling without you knowing. Also, if you do make a mistake and forget to pay a bill, credit card companies often waive many “annual fees” or even interest if you push hard enough. Fifty bucks here or there adds up. Again, this could be what you need to start your side hustle.

Owning Your Personal Credit Score

Building up a solid credit score can be helpful in many ways, especially when you do want to borrow money in the future, personally, or for your business! The best way to do this is to have a credit card, mortgage, or home equity line of credit and use them responsibly.

A good credit score usually involves having a lot of credit you do not use. For example, if you have a credit card with a $20,000 credit limit, but only borrow $1,000, you have $19,000 in available credit. The credit-scoring algorithms love this—along with those who pay their bills in full and on time.

If you do have bad credit you can acquire a free copy of your credit report and start working to pay off anything that may be late or dispute anything inaccurate! Go back to your budget and consider picking up another job or other forms of generating cash to accelerate paying these items swiftly if your side hustle isn’t ready to support this yet.

Managing Other Personal Debt

If you have a lot of personal debt, it can be overcome. You likely need to make some changes in your habits and educate yourself on better money management, but we have guided countless individuals to get out of $20,000, $50,000, or even a $100,000 of debt.

On debt you do carry, like anything, shop around. Identify the best price but do watch out for excessive loan fees. If you are unsure if you should make a change, you can always dollarize your savings, meaning determine how much savings a new interest rate saves you in actual dollars.

We don’t want to run through infinite different scenarios; we want you to understand this mindset so you can self-prescribe in the future and make stronger Lifeset decisions.

Step 4: Building Wealth

Building wealth requires an entirely different mindset, and corresponding Lifeset, compared to simply making money and managing expenses. To create wealth in your twenties or thirties takes an elevated game beyond what most of society does or teaches. Since creating wealth is often a primary purpose for building a side hustle, let’s take a deeper dive here.

The average twentieth-century game plan for a financially successful life was to get a good job, work hard, live humbly, and save. This works relatively well if you make a solid income, live humbly, and want to spend 40 years in a full-time career. But this plan also has several limitations and risks—we refer to this as the “pile” theory. Save enough money through your 401(k)s, or over the course of your life, then eventually you will have your $250,000, $1 million, or $2 million saved that you need to live comfortably. Combine this with social insecurity and you should be all set! If you are looking to bunt or only plan to get to first base in the game of finances, this is a relatively sound plan. But a few questions to ask yourself:

1. Will the pile be enough? The average current life expectancy in the United States is 79 years old. Of course, many live much longer since the average includes all causes of mortality. Where was medical science 40 or 50 years ago, and where will it be further into the twenty-first century? With the exponential growth rate of technology, planning to go out at 80 may not be conservative or wise. If you live to 90 or 100 and the markets dip at the wrong time or Social Security gets cut or reduced, what is your plan? Do you want to put extra financial stress on yourself, pick up a part-time gig at 85, or burden other loved ones?

2. Is the pile too big? Certainly a better side of the equation to be on, but who wants to work hard their whole life, limit their activities, only to realize too late they could have taken more vacations, given more to their grandchildren or children while alive, and enjoyed that giving? Most want to leave some money for their loved ones and children, but what is the right amount? Too much and they may become spoiled or disincentivized to do anything with their lives; not enough and they have to go through a similar hardship as you may have.

3. How will my pile be valued 40 years from now? Inflation, health issues, artificial intelligence (AI), globalization, and other automation all make it difficult to manage to this challenge. What will the dollar, euro, or rupee be worth in 40 years? How much will intensive medical care cost? What does health care even look like in 2050? All these variables present a unique challenge when you have only one lump sum pile of money without other forms of income.

Our solution: Roll with the pile theory and hedge against these challenges by also building assets that produce genuine cash flow (side hustles). If you own real estate, a business, or other forms of cash-producing assets that can generate ongoing revenue, then you have diversified and built a financial instrument that oftentimes hedges against inflation. In addition, you can usually sell the asset, or will the asset or cash flow to loved ones.

Ultimately, there only two reasonable options to building wealth. So let’s look at them both directly—as they are your only options.

Option 1: Systematic Savings and Investment

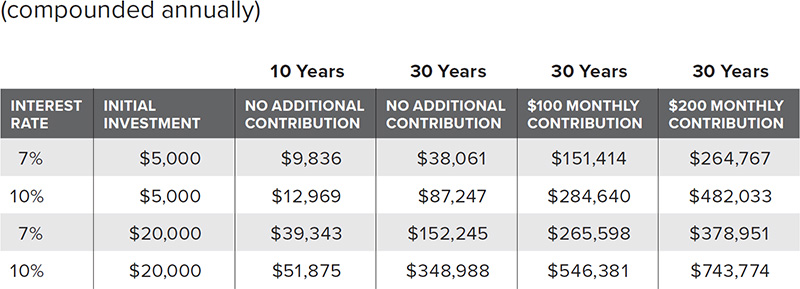

We cannot impress upon anyone enough the value of executing on both building your own business and systematically saving (aka the pile theory). You may have seen similar charts like Figure 5.3, but we encourage you to really look at this clearly and understand the magnitude of how saving a few thousand now can turn into tens of thousands in the future.

FIGURE 5.3 Investment Projections with Compound Interest Estimates

Imagine if after five years of losing $20,000 on the preceding vehicle purchase example you had instead invested that money and contributed $200 per month (some of which you could get from lower insurance rates). You would potentially create over $743,000 of investments 30 years from now. That’s just ONE purchase. If this doesn’t motivate you to manage your money in a more responsible way, we don’t know what will.

There are many online calculators you can use to run your own estimates, but a very simple one can be found on investor.gov.

Do not, we repeat, do not underestimate the value of systematic savings.

Option 2: Building a Business

The challenge with relying solely on investing is you need a lot of capital, time, skill, or luck. If you don’t have some or all of these and you truly want to build wealth, welcome to the world of business ownership. However, business ownership has its own form of investment, both in time and monetarily.

We have always contributed money to our 401(k)s when we had jobs and now to our 401(k)s as being self-employed. We have also played the IRA Roth game—but we didn’t stop there! Hence, again, the value of a side hustle.

Remember, to build wealth beyond the day job requires some form of investing. Investing in retirement and savings funds are normalized, but investing in a business that doesn’t always provide short-term returns is abnormal. Coming from middle-class backgrounds, we had to fight the mindset of saving less to spend more—essentially learning how to consider our “spending” on our side hustles as investments. From small things such as association dues, taking business trips, or investing in inventory, strong business owners see what they are purchasing as an eventual asset or something that will pay them more in the future for what the cost is today. For many aspiring side hustlers, this is a difficult mindset shift, and one they never make.

There are scores of examples. We can both recall booking flights in our first year of business ownership (when they were not producing income yet). We were both making around $30,000 in our jobs at that point. Booking $300 flights and $40 for luggage did feel crazy, as we were dropping 1 percent of our annual income on flights with no guarantees of creating any revenue from our trips. But if we hadn’t been willing to make these types of investments, we never would have been able to build what we have today.

We chose to live humbly and make our basic retirement contributions, and we were willing to essentially invest everything else into our side hustles. We funded our businesses instead of financing sporting outings, cable, big-screen TVs, cars, five-dollar mochas, or fancy vacations. In fact, we didn’t even own a TV for a decade (until our first business exceeded $1 million in revenue). This annoyed the daylights out of our parents and relatives . . . let’s just say no one was ever planning to watch the big game at C&C’s house! It’s unrealistic to expect uncommon results in life if you don’t do uncommon things.

In addition, for several years of our twenties we did not max out our Roth IRA contributions. We remember our financial planner (who is a couple years older than us) giving us a hard time about this. So we asked if he had maxed out his Roth contributions during the first couple years building his financial planning business, to which he replied: “No.” He does well now and so do we, but the businesses we built produce significantly more income than the $12,000 we missed out on from a handful of Roth contributions.

Now, being willing to invest money into your side hustle is the first step. When and how to invest that money in your business is the next level of thinking, which we discuss in upcoming chapters.