Chapter 5

Disability Income Benefits

Learning objectives

- Recall the relationship between Social Security disability income benefits and retirement benefits.

- Identify how claims for Social Security disability income benefits are made.

- Recognize the relationship between Social Security disability income benefits and Medicare.

- Recall how Supplemental Security Income (SSI) operates.

Overview

An individual’s chances of becoming disabled are greater than most people think. Studies conducted by the Social Security Administration (SSA) show that a 20-year-old worker has a 3-in-10 chance of becoming disabled before reaching his or her full retirement age.

Social Security disability insurance, or SSDI, is a federally operated and regulated disability insurance program. Workers pay for this federal insurance through Federal Insurance Contribution Acts (FICA) taxes. SSDI is distinct from Medicare, Medicaid, and the needs-based SSI programs. SSDI provides monthly benefits to eligible workers who have not attained their full or normal retirement ages (65–67) and can no longer work because of a significant disability that is expected to last 12 months or more, or is expected to be terminal. As in the case of other types of Social Security benefits, the SSDI benefit is based on the recipient’s FICA-covered earnings history. However, benefit limits are substantially lower.

Among the numerous and rigorous requirements for disability income benefit eligibility, the impairment or combination of impairments must be so severe that the applicant can no longer perform his or her pre-disability job. Still, the applicant must also be unable (considering his or her age, education, and work experience) to work in any other kind of substantially gainful work operating within the American economy.

Americans are likely to focus on succeeding in their jobs and careers. Relatively few among us plan for a cushion on which to fall back on in case we become unable to earn income due to a significant disability. Social Security can provide an ongoing disability benefit. However, private disability income insurance should not be ruled out because eligibility for SSDI is strict and initial denial of claims is typical.

SSDI beneficiaries often suffer from multiple impairments. According to the most recent statistics from the SSA, of the 11 million individuals receiving disabled worker benefits, 30% had mental impairments as the main disabling condition (primary diagnosis). They include 10% with schizophrenia and 20% with other mental disorders. Musculoskeletal conditions such as arthritis, back injuries, and other disorders of the skeleton and connective tissues were classified as the primary diagnosis for 32% of the workers receiving Social Security disability benefits.

Musculoskeletal conditions were more prevalent among beneficiaries over age 50. Approximately 8% claimed benefits from disabilities were pegged to heart disease or circulatory diseases. Another 10% suffered impairments of the nervous system and sense organs. The remaining 20% include those with injuries, cancers, infectious diseases, metabolic and endocrine diseases, such as diabetes, diseases of the respiratory system and diseases of other body systems.

Characteristics attributable to disabled-worker beneficiaries

Disabled-worker beneficiaries face unpleasant economic challenges. About 34% of disabled workers versus 13% of other working age adults have incomes less than 125% of the poverty threshold.

SSDI recipients are also more likely to be older, with the average age of beneficiaries at 53. Within this group, almost 70% are over 50 years old whereas about 30% are over 60 years old. Many recipients would be considered as terminally ill. Approximately 20% of male beneficiaries and one in seven female beneficiaries die within the first five years after receiving their first disability income benefit from Social Security.

Determining the benefit

The amount of the monthly SSDI benefit is based on a weighted formula that the Social Security Administration applies to calculate benefits for each approved applicant. Social Security bases both retirement and disability benefits on the amount of FICA income attributable to the covered worker, the so-called “covered earnings.” As with retirement benefits, the formula consists of fixed percentages of different amounts of income (called “bend points,” which are adjusted each year).

Bend point mini case

Recall that bend points represent portions of a worker’s average annual FICA income (average indexed monthly earnings or AIME) in specific dollar amounts indexed each year, based upon the average wage index (AWI) series.

It is noteworthy that AWI figures are always two years in arrears. Therefore, the AWI figure used to determine the 2019 bend points is based on 2017 wage averages.

The bend points for 2019 are $926 and $5,583.

Here is how this applies:

Matt Kincaid becomes eligible for SSDI benefits in 2019. His AIME is $6,500. Ninety percent of the first $926 of his AIME is included in his primary insurance amount (PIA), plus 32% of his AIME from $926 to $5,583 plus 15% of Matt’s AIME over $5,583. The amounts are added up to determine Matt’s PIA as follows:

| $926 × .90 = | $833.40 |

| + $4,657 × .32 = | $1,490.24 |

| + $917 × .15 = | $137.55 |

| Matt’s PIA | $2,461.19 |

(Per the preceding calculation, $5,583 – $926 = $4,657; and $6,500 – $5,583 = $917.)

Relationship between retirement and disability income benefits

Generally, a worker may not receive Social Security retirement benefits and disability benefits at the same time. SSDI operates to provide disability benefits to disabled individuals who are too young to receive Social Security old age (retirement) benefits.

An exception

There is, however, an exception when an individual draws less than a full monthly retirement benefit for a period and is approved for disability benefits; Social Security will make up the difference between the early retirement amount and the full disability amount for those months the individual was disabled but receiving early retirement benefits (retroactively).

Disability benefit eligibility

The number of Social Security credits or quarters that a disabled applicant needs to qualify for disability benefits depends on the age at which the applicant becomes disabled. Generally, an applicant needs 40 credits, 20 of which were earned in the last 10 years ending with the year in which the disability started. Keep in mind, that unlike retirement benefits in which 40 quarters establishes a fully insured status going forward, for SSDI benefits, the covered quarters needed to have occurred immediately before the disability began.

However, younger workers may qualify with fewer credits. The rules are as follows:

- Before age 24—A disabled applicant may qualify having earned six credits in the three-year period ending when the disability begins.

- Age 24 to 31—A disabled applicant may qualify having credits attributable to working half the time between age 21 and when the disability commences.

- For example, if Tiffany became disabled at age 27, she would need to have FICA credits or quarters for three working years (12 credits) out of the past six years (between her ages 21 and 27).

- Age 31 or older—In general, the disabled applicant must have earned the number of work credits shown in the chart that follows.

Unless the applicant is blind, he or she must have earned at least 20 of the credits in the 10 years immediately preceding the onset of disability.

| Born after 1929, became disabled at age | Number of credits needed |

| 31 through 42 | 20 |

| 44 | 22 |

| 46 | 24 |

| 48 | 26 |

| 50 | 28 |

| 52 | 30 |

| 54 | 32 |

| 56 | 34 |

| 58 | 36 |

| 60 | 38 |

| 62 or older | 40 |

Source: SSA |

|

For example, if Sylva was born in 1980 and became disabled at age 48, she would need 26 credits or quarters to be eligible for Social Security disability benefits.

Unique rules for blind applicants

There are special rules for people who are blind or who suffer from very low vision. The SSA considers an applicant for SSDI benefits to be legally blind under Social Security rules if that individual’s vision cannot be corrected to better than 20/20 in the better eye, or if the individual’s visual field is 20 degrees or less, even with a corrective lens. Certain applicants who qualify for disability benefits may still have some sight and may be able to read large print and ambulate without a cane or a guide dog.

If an applicant does not satisfy the SSA’s definition of blindness, he or she may still qualify for disability benefits if vision problems alone or combined with other health problems impair the individual’s ability to earn income from working.

There are a number of special rules for people who are blind that recognize the severe impact of blindness on a person’s ability to work. For example, the monthly earnings limit for people who are blind is generally higher than the limit that applies to nonblind disabled workers. In 2019, the monthly earnings limit for a blind disability income benefit claimant to still be considered disabled is $2,040.

Obtaining benefits

Unlike retirement benefits, one cannot complete the application process for SSDI benefits entirely online (although certain documents may be submitted online). Typically, the applicant or a representative of the applicant must make an appointment to appear at a local Social Security office.

Compassionate allowances

Social Security has developed a list of more than 225 compassionate allowances currently, which, if the insured person has one of these conditions, shortens the time frame for being approved for disability benefits to approximately two weeks.

The allowances can be found at http://ssa.gov/compassionateallowances/conditions.htm

Region 1: Boston Social Security Disability

- Connecticut Social Security Disability

- Maine Social Security Disability

- Massachusetts Social Security Disability

- New Hampshire Social Security Disability

- Rhode Island Social Security Disability

- Vermont Social Security Disability

Region 2: New York Social Security Disability

- New Jersey Social Security Disability

- New York Social Security Disability

- Puerto Rico Social Security Disability

- U.S. Virgin Islands Social Security Disability

Region 3: Philadelphia Social Security Disability

- Delaware Social Security Disability

- Maryland Social Security Disability

- Pennsylvania Social Security Disability

- Virginia Social Security Disability

- West Virginia Social Security Disability

- District of Columbia Social Security Disability

Region 4: Atlanta Social Security Disability

- Alabama Social Security Disability

- Florida Social Security Disability

- Georgia Social Security Disability

- Kentucky Social Security Disability

- Mississippi Social Security Disability

- North Carolina Social Security Disability

- South Carolina Social Security Disability

- Tennessee Social Security Disability

Region 5: Chicago Social Security Disability

- Illinois Social Security Disability

- Indiana Social Security Disability

- Michigan Social Security Disability

- Minnesota Social Security Disability

- Ohio Social Security Disability

- Wisconsin Social Security Disability

Region 6: Dallas Social Security Disability

- Arkansas Social Security Disability

- Louisiana Social Security Disability

- New Mexico Social Security Disability

- Oklahoma Social Security Disability

- Texas Social Security Disability

Region 7: Kansas City Social Security Disability

- Iowa Social Security Disability

- Nebraska Social Security Disability

- Kansas Social Security Disability

- Missouri Social Security Disability

Region 8: Denver Social Security Disability

- Colorado Social Security Disability

- Montana Social Security Disability

- North Dakota Social Security Disability

- South Dakota Social Security Disability

- Utah Social Security Disability

- Wyoming Social Security Disability

Region 9: San Francisco Social Security Disability

- Arizona Social Security Disability

- California Social Security Disability

- Hawaii Social Security Disability

- Nevada Social Security Disability

- American Samoa, Guam, and Northern Marina Islands Social Security Disability

Region 10: Seattle Social Security Disability

- Alaska Social Security Disability

- Idaho Social Security Disability

- Oregon Social Security Disability

- Washington Social Security Disability

If someone suffered a disabling injury in January and met Social Security’s disability definition, he or she would become eligible for the first disability payment for July. The average SSDI payment in July of 2018 is $1,199. The maximum disability benefit in 2019 is $2,861.

Denial of claims

If an individual’s application for SSD is denied (we can see from the following table that most initial applications are), he or she can appeal the decision. A denied applicant must request a review of the denial within 60 days from the date of the denial letter. The first step of the appeal process in most states is the request for reconsideration, a review of the claimant’s file by another claims examiner. If the applicant is denied again, he or she may appeal to the next level by requesting a hearing with an administrative law judge who works for the SSA.

The SSA recently met its goal to increase the number of administrative law judges to more than 1,500. With more than 255,000 hearing requests in 2017, individuals should consider legal representation when preparing for their disability appeals.

Selected data from Social Security’s disability program

The following table presents unedited data (including corrections, if any) on disabled worker beneficiaries paid from Social Security’s Disability Insurance Trust Fund. In particular, unedited award data may contain duplicate cases.

| Disabled worker beneficiary statistics by calendar year, quarter, and month | |||||||||||

| Awards | In current payment status | Terminations e | |||||||||

| Time period | Number of applications | Number c | Increase over prior period | Ratio to applications d | Number at end of period | Increase over prior period | Number | Increase over prior period | Termination rate | ||

| Field office receipts a | Initial DDS receipts b | Field office receipts | Initial DDS receipts | ||||||||

| —By Calendar Year — | |||||||||||

| 2004 ..... | 2,137,531 | 1,561,059 | 797,226 | 2.48% | 37.30% | 51.07% | 6,201,362 | 5.58% | 466,332 | 3.46% | 7.32% |

| 2005 ..... | 2,122,109 | 1,482,475 | 832,201 | 4.39% | 39.22% | 56.14% | 6,524,582 | 5.21% | 494,592 | 6.06% | 7.36% |

| 2006 ..... | 2,134,088 | 1,471,122 | 812,596 | -2.36% | 38.08% | 55.24% | 6,811,679 | 4.40% | 513,292 | 3.78% | 7.28% |

| 2007 ..... | 2,190,196 | 1,470,748 | 823,106 | 1.29% | 37.58% | 55.97% | 7,101,355 | 4.25% | 525,012 | 2.28% | 7.14% |

| 2008 ..... | 2,320,396 | 1,527,108 | 895,011 | 8.74% | 38.57% | 58.61% | 7,427,203 | 4.59% | 564,518 | 7.52% | 7.34% |

| 2009 ..... | 2,816,244 | 1,798,975 | 985,940 | 10.16% | 35.01% | 54.81% | 7,789,113 | 4.87% | 628,478 | 11.33% 7.79% | |

| 2010 ..... | 2,935,798 | 1,926,398 | 1,052,551 | 6.76% | 35.85% | 54.64% | 8,204,710 | 5.34% | 646,387 | 2.85% | 7.64% |

| 2011 ..... | 2,878,920 | 1,859,591 | 1,025,003 | -2.62% | 35.60% | 55.12% | 8,576,067 | 4.53% | 656,902 | 1.63% | 7.42% |

| 2012 ..... | 2,824,024 | 1,808,863 | 979,973 | -4.39% | 34.70% | 54.18% | 8,827,795 | 2.94% | 726,432 | 10.58% | 7.90% |

| 2013 ..... | 2,653,939 | 1,702,700 | 884,894 | -9.70% | 33.34% | 51.97% | 8,942,584 | 1.30% | 767,738 | 5.69% | 8.17% |

| 2014 ..... | 2,536,174 | 1,633,652 | 810,973 | -8.35% | 31.98% | 49.64% | 8,954,518 | 0.13% | 793,646 | 3.37% | 8.37% |

| 2015 ..... | 2,427,443 | 1,552,119 | 775,739 | -4.34% | 31.96% | 49.98% | 8,909,430 | -0.50% | 817,045 | 2.95% | 8.62% |

| 2016 ..... | 2,321,583 | 1,473,700 | 744,268 | -4.06% | 32.06% | 50.50% | 8,808,736 | -1.13% | 830,044 | 1.59% | 8.81% |

| 2017 ..... | 2,179,928 | 1,377,803 | 762,141 | 2.40% | 34.96% | 55.32% | 8,695,475 | -1.29% | 868,795 | 4.67% | 9.30% |

| 2018 ..... | 2,073,293 | 1,300,668 | 733,879 | -3.71% | 35.40% | 56.42% | 8,537,332 | -1.82% | 888,214 | 2.24% | 9.63% |

| —By Quarter— | |||||||||||

| 2015 Q2 | 638,754 | 414,104 | 206,392 | 9.83% | 32.31% | 49.84% | 8,937,961 | 0.03% | 202,486 | -1.88% | 2.21% |

| 2015 Q3 | 614,438 | 392,361 | 194,443 | -5.79% | 31.65% | 49.56% | 8,921,350 | -0.19% | 209,710 | 3.57% | 2.29% |

| 2015 Q4 | 565,932 | 360,956 | 186,983 | -3.84% | 33.04% | 51.80% | 8,909,430 | -0.13% | 198,493 | -5.35% | 2.17% |

| 2016 Q1 | 578,655 | 363,223 | 185,123 | -0.99% | 31.99% | 50.97% | 8,888,588 | -0.23% | 203,524 | 2.53% | 2.23% |

| 2016 Q2 | 598,009 | 379,566 | 196,205 | 5.99% | 32.81% | 51.69% | 8,872,165 | -0.18% | 206,988 | 1.70% | 2.27% |

| 2016 Q3 | 627,794 | 400,933 | 190,045 | -3.14% | 30.27% | 47.40% | 8,841,345 | -0.35% | 216,542 | 4.62% | 2.38% |

| 2016 Q4 | 517,125 | 329,978 | 172,895 | -9.02% | 33.43% | 52.40% | 8,808,736 | -0.37% | 202,990 | -6.26% | 2.24% |

| 2017 Q1 | 561,965 | 352,802 | 193,674 | 12.02% | 34.46% | 54.90% | 8,778,443 | -0.34% | 221,796 | 9.26% | 2.45% |

| 2017 Q2 | 562,813 | 356,315 | 196,430 | 1.42% | 34.90% | 55.13% | 8,755,405 | -0.26% | 214,630 | -3.23% | 2.38% |

| 2017 Q3 | 548,088 | 341,902 | 201,820 | 2.74% | 36.82% | 59.03% | 8,736,086 | -0.22% | 222,406 | 3.62% | 2.47% |

| 2017 Q4 | 507,062 | 326,784 | 170,217 | -15.66% | 33.57% | 52.09% | 8,695,475 | -0.46% | 209,963 | -5.59% | 2.34% |

| 2018 Q1 | 538,077 | 327,935 | 188,681 | 10.85% | 35.07% | 57.54% | 8,653,039 | -0.49% | 228,986 | 9.06% | 2.56% |

| 2018 Q2 | 549,790 | 342,870 | 189,439 | 0.40% | 34.46% | 55.25% | 8,622,658 | -0.35% | 215,663 | -5.82% | 2.42% |

| 2018 Q3 | 548,872 | 335,906 | 190,492 | 0.56% | 34.71% | 56.71% | 8,585,452 | -0.43% | 229,348 | 6.35% | 2.58% |

| 2018 Q4 | 436,554 | 293,957 | 165,267 | -13.24% | 37.86% | 56.22% | 8,537,332 | -0.56% | 214,217 | -6.60% | 2.42% |

| 2019 Q1 | 501,029 | 318,441 | 193,127 | 16.86% | 38.55% | 60.65% | 8,504,781 | -0.38% | 226,238 | 5.61% | 2.57% |

| —By Month— | |||||||||||

| 2018 Jan | 156,670 | 91,564 | 67,036 | 16.51% | 42.79% | 73.21% | 8,677,460 | -0.21% | 82,688 | 15.93% | 0.93% |

| 2018 Feb | 169,070 | 104,115 | 51,934 | -22.53% | 30.72% | 49.88% | 8,663,192 | -0.16% | 67,621 | -18.22% | 0.76% |

| 2018 Mar | 212,337 | 132,256 | 69,711 | 34.23% | 32.83% | 52.71% | 8,653,039 | -0.12% | 78,677 | 16.35% | 0.89% |

| 2018 Apr | 172,088 | 108,698 | 65,387 | -6.20% | 38.00% | 60.15% | 8,645,567 | -0.09% | 71,700 | -8.87% | 0.81% |

| 2018 May | 170,296 | 107,301 | 59,876 | -8.43% | 35.16% | 55.80% | 8,633,765 | -0.14% | 69,550 | -3.00% | 0.79% |

| 2018 Jun | 207,406 | 126,871 | 64,176 | 7.18% | 30.94% | 50.58% | 8,622,658 | -0.13% | 74,413 | 6.99% | 0.84% |

| 2018 Jul | 164,037 | 100,311 | 66,154 | 3.08% | 40.33% | 65.95% | 8,611,522 | -0.13% | 77,677 | 4.39% | 0.88% |

| 2018 Aug | 219,272 | 135,213 | 60,048 | -9.23% | 27.39% | 44.41% | 8,596,559 | -0.17% | 75,852 | -2.35% | 0.86% |

| 2018 Sep | 165,563 | 100,382 | 64,290 | 7.06% | 38.83% | 64.05% | 8,585,452 | -0.13% | 75,819 | -0.04% | 0.86% |

| 2018 Oct | 143,689 | 101,512 | 63,366 | -1.44% | 44.10% | 62.42% | 8,573,763 | -0.14% | 76,413 | 0.78% | 0.87% |

| 2018 Nov | 169,792 | 111,839 | 47,715 | -24.70% | 28.10% | 42.66% | 8,557,051 | -0.19% | 65,266 | -14.59% | 0.74% |

| 2018 Dec | 123,073 | 80,606 | 54,186 | 13.56% | 44.03% | 67.22% | 8,537,332 | -0.23% | 72,538 | 11.14% | 0.83% |

| 2019 Jan | 144,192 | 90,450 | 65,077 | 20.10% | 45.13% | 71.95% | 8,520,503 | -0.20% | 81,602 | 12.50% | 0.93% |

| 2019 Feb | 151,863 | 95,912 | 58,088 | -10.74% | 38.25% | 60.56% | 8,510,897 | -0.11% | 69,098 | -15.32% | 0.79% |

| 2019 Mar | 204,974 | 132,079 | 69,962 | 20.44% | 34.13% | 52.97% | 8,504,781 | -0.07% | 75,538 | 9.32% | 0.87% |

aThe number of applications is for disabled-worker benefits only and, as such, excludes disabled child's and disabled widow(er)'s benefits. These applications are those received at Social Security field offices, teleservice centers, and claims filed electronically on the internet. Applications ultimately result in either a denial or award of benefits. These counts include applications that are denied because the individual is not insured for disability benefits. Because the application data are tabulated on a weekly basis, some months include 5 weeks of data while others include only 4 weeks. This weekly method of tabulation accounts for much of the month-to-month variation in the monthly application data. This method also occasionally causes quarterly data to have either 12 or 14 weeks of data instead of 13 weeks, annual data may include an extra week of data. bReceipts at State Disability Determination Services (DDS), Federal Disability Units, Disability Processing Branches, and Extended Service Team Sites for an initial evaluation of whether the claimant's disability meets the definition of disability as set forth in the Social Security Act and appropriate regulations. cAward data prior to 2014 are unedited and may contain duplicates. dAwards as a ratio to applications is a crude measure and does not represent an allowance rate. This ratio expresses the number of awards in a given time period as a ratio to the number of applications in the same time period. Some of the awards in any time period, however, resulted from applications in previous time period(s). eThe number of terminations is the number of beneficiaries who leave the disability rolls for any reason. The number is calculated on the basis of the change in the total number of entitled beneficiaries (those in current payment status plus those whose benefits are withheld for any reason) and the number of awards. The termination rate is the ratio of the terminations to the number of beneficiaries who could potentially leave the rolls. This latter number is approximated as the sum of the number entitled at the beginning of the time period plus half the number of awards in that period. |

|||||||||||

Reducing benefits due to payments by other government type disability payments

If someone is entitled to receive disability benefits from private long-term disability insurance benefits, these benefits will have no impact on the insured’s SSDI benefits. However, if someone is claiming SSDI benefits and simultaneously receives government-regulated disability benefits, such as workers’ comp benefits or temporary state disability benefits, they can end up reducing SSDI benefits. The rule is that a disabled SSDI recipient may not receive more than 80% of the average amount earned before the disability ensued in combined SSDI and other disability benefits. If that occurs, the SSDI benefit will be reduced. SSI and Veterans Benefits Administration (VA) benefits (not disability benefits) will not reduce an individual’s SSDI benefit.

No disability payments at full retirement age and older

If one is still receiving disability insurance by the time of his or her full retirement age, the payments morph into retirement benefits. The amount of the retirement payments remains the same.

Back pay for delayed benefit approval

Because initial denial of claims for SSDI occur in roughly 60% of situations, when approval finally happens, retroactive benefits—back pay—is not uncommon. The amount available in back pay, of course, depends on the applicant’s SSDI monthly amount. The number of months of back payments one gets will be determined by the months between the application date and the established date of onset (when the applicant’s disability started). If an individual previously applied for disability benefits, he or she may be able to get back pay going back to the original application date.

Waiting or elimination period

Disability benefit payments start only after the applicant has been disabled for five months, then continue until the benefit recipient’s condition has improved to the level that he or she is able to return to work.

Knowledge check

- What is the waiting period for SSDI benefits?

- 3 months.

- 5 months.

- 9 months.

- 24 months.

Generally no benefit for disabled children

Generally, children cannot qualify for SSDI because such benefits are available only to disabled workers having sufficient FICA credits or quarters. (However, if a disabled child’s parent is eligible for Social Security retirement or disability, the child may be able to receive a dependent’s benefit called the disabled adult child benefit after turning 18.)

If a worker’s adult child is disabled before the age of 22, he or she can qualify for benefits based on a parent’s earnings record. Anyone who becomes disabled after turning 22 needs to pass the recent work test, a measure of how many years of work the disabled individual has performed depending on his or her age.

The Medicare or Medicaid piece

After collecting disability benefits for 24 months, a beneficiary will become eligible for Medicare, regardless of that beneficiary’s age. In the interim, if the disabled individual’s income and assets fall less than certain benchmarks, that person may qualify for Medicaid benefits.

Medical eligibility for Social Security disability income benefits

An applicant must suffer from a medical condition that meets the SSA’s definition of disability. SSDI benefits are eligible only to those with a severe, long-term, total disability. Severe means that the condition must interfere with work-related tasks. Long term means that the claimant’s condition has lasted or is expected to last at least one year.

A crucial part of claiming benefits under either Social Security program is proving that one is severely disabled—essentially that the claimant has a physical or mental condition that prevents him or her from doing any substantial gainful activity (SGA) and will last at least one year or will cause that individual’s death.

The fact that one’s doctor may have advised someone not to work, or that he or she feels too ill to work, does not necessarily mean that the SSA will consider that individual to be disabled.

The SSA evaluates disability using its own medical experts, based on a list of physical and mental conditions contained in its regulations.

Furthermore, the impairment or combination of impairments must be of such severity that the applicant is not only unable to do his or her previous work but cannot, considering his or her age, education, and work experience, engage in any other kind of substantial gainful work which exists in the national economy.

Defining total disability

Total disability means the inability to perform SGA for at least one year. If a claimant is currently working and makes more than $1,220 per month in 2019, ($2,040 for blind applicants), the SSA will deem that individual to be performing SGA and not disabled enough to qualify for SSDI benefits.

Can one have earnings and still collect benefits?

| Monthly substantial gainful activity amounts by disability type | ||||||||

| Year | Blind | Non-blind | Year | Blind | Non-blind | Year | Blind | Non-blind |

| 1975 | $200 | $200 | 1990 | $780 | $500 | 2005 | $1,380 | $ 830 |

| 1976 | 230 | 230 | 1991 | 810 | 500 | 2006 | 1,450 | 860 |

| 1977 | 240 | 240 | 1992 | 850 | 500 | 2007 | 1,500 | 900 |

| 1978 | 334 | 260 | 1993 | 880 | 500 | 2008 | 1,570 | 940 |

| 1979 | 375 | 280 | 1994 | 930 | 500 | 2009 | 1,640 | 980 |

| 1980 | 417 | 300 | 1995 | 940 | 500 | 2010 | 1,640 | 1,000 |

| 1981 | 459 | 300 | 1996 | 960 | 500 | 2011 | 1,640 | 1,000 |

| 1982 | 500 | 300 | 1997 | 1,000 | 500 | 2012 | 1,690 | 1,010 |

| 1983 | 550 | 300 | 1998 | 1,050 | 500 | 2013 | 1,740 | 1,040 |

| 1984 | 580 | 300 | 1999 | 1,110 | 700a | 2014 | 1,800 | 1,070 |

| 1985 | 610 | 300 | 2000 | 1,170 | 700 | 2015 | 1,820 | 1,090 |

| 1986 | 650 | 300 | 2001 | 1,240 | 740 | 2016 | 1,820 | 1,130 |

| 1987 | 680 | 300 | 2002 | 1,300 | 780 | 2017 | 1,950 | 1,170 |

| 1988 | 700 | 300 | 2003 | 1,330 | 800 | 2018 | 1,980 | 1,180 |

| 1989 | 740 | 300 | 2004 | 1,350 | 810 | 2019 | 2,040 | 1,220 |

a $500 amount applied in the first half of 1999. |

||||||||

In some cases, earnings can be reduced by the costs associated with work, such as paying for a wheelchair or services of an attendant. If an individual qualifies for disability benefits, he or she will not receive SSDI benefits until that individual has satisfied a five-month waiting (elimination) period. If the disabled beneficiary’s application is approved, the first Social Security benefit will be paid for the sixth full month after the date when the SSA deems the beneficiary’s disability to have begun.

In July 2018, the average monthly SSDI benefit was $1,199.

In reality, it is a six-month wait. Social Security benefits are paid in the month following the month for which they are due. In other words, the benefit due for December would be paid in January of the following year, and so on.

Knowledge check

- Unless an applicant is relatively young, what is the general eligibility requirement for Social Security disability income benefits?

- Forty credits, 20 of which were earned in the last 10 years ending with the year in which the disability started.

- Six credits in the three-year period ending with the year in which the disability started.

- Three working years (12 credits) out of the past six years, ending with the year in which the disability started.

- 20–40 work credits.

Back (retroactive) pay

Even if the applicant is approved immediately (for example, because he or she recently had a lung transplant), that individual would have to wait. Typically, an applicant is not approved for six months to a year (after at least one level of appeal). In that situation, when the claim is finally approved, that claimant would be paid disability back pay starting with the sixth month after the disability began (the disability onset date).

After an applicant is paid any outstanding back pay, a monthly disability benefit follows. That benefit may or may not be taxable. A disabled claimant’s family members may also be eligible for a monthly benefit that is generally less than the benefit paid to the eligible disabled worker.

Please see the chapter on Taxation of Social Security Benefits for a discussion on the taxation of back pay.

Working while collecting disability benefits

Trial work period—The trial work period allows a patient to test his or her ability to work for at least nine months. During the trial work period, the patient will receive full Social Security benefits regardless of how much is being earned as long as he or she reports the work and continues to have a disability. In 2019, a trial work month is any month during which total earnings are more than $880. If the patient is self-employed, he or she has a trial work month when he or she can earn more than $880 (after expenses) or work more than 80 hours in his or her own business. The trial work period continues until the patient has worked nine months within a 60-month period.

Extended period of eligibility—After the trial work period, the patient has 36 months during which he or she can work and still receive benefits for any month that earnings aren’t substantial. During a trial work period, neither a new application nor disability decision is necessary to get the Social Security disability benefit.

Expedited reinstatement—If benefits stop because of substantial earnings, the patient has five years to ask the SSA to restart the benefits if the patient is unable to keep working because of the condition. The patient won’t have to file a new application or wait for benefits to restart while the medical condition is being reviewed.

Continuation of Medicare—If Social Security disability benefits stop because of earnings, but the patient is still disabled, free Medicare Part A coverage will continue for at least 93 months after the 9-month trial work period.

Continuing disability review

The SSA is required by law to periodically review the case of every person who is receiving Social Security Disability (SSD) or SSI disability benefits. This process is called a continuing disability review (CDR). Its purpose is to identify beneficiaries who may no longer qualify as disabled. If, during a CDR, the SSA finds that a claimant’s medical condition has improved enough so that he or she can work, that individual’s Social Security benefits will end.

In general, it is much easier for a disabled individual to pass a CDR than it is to be granted benefits initially.

The frequency at which CDRs occur will vary.

CDRs for adults

Most claims are set for review every three or seven years, depending on the likelihood that a benefit recipient’s condition will improve. If a claimant has a condition that is expected to medically improve, a CDR may be conducted even sooner than three years. In contrast, Social Security beneficiaries whose condition is not expected to improve or are disabled due to a permanent condition (such as a lost limb or impaired intellectual functioning) may have their claim reviewed even less than every seven years.

However, even those with permanent disability conditions may be eventually subject to CDRs. Further, CDRs are also more frequently conducted for beneficiaries who are age 50.

CDRs for children receiving disability benefits under SSI

Children who are receiving (needs based, not regular Social Security) SSI disability benefits will automatically have their claims reviewed when they turn 18. The standards that must be met for an adult to be considered disabled are different from those for a child. Therefore, at age 18, the child will be evaluated under the adult standards. Newborns who receive SSI due to a low-birth weight will have their claim reviewed prior to the one-year mark.

Knowledge check

- According to the SSA, what does total disability mean?

- The inability of the insured to perform any substantial gainful activity for at least one year.

- The inability of the insured to perform the tasks associated with the job at which he or she was employed when the disability began.

- The inability to stand or sit for extended periods.

- That one’s doctor has advised someone not to work.

Triggered continued disability reviews

In addition to the regularly scheduled CDRs, the SSA may conduct a CDR in any of the following situations:

- The benefit recipient returned to work.

- The benefit recipient informed the SSA of an improvement in condition.

- Medical evidence indicates that the benefit recipient’s condition has improved.

- A third party informs the SSA that the benefit recipient is not following treatment protocol.

- A new treatment for the benefit recipient’s disabling condition has recently been introduced.

Continuing disability review process

If a disability income benefit recipient’s Social Security claim is up for review, the SSA will notify that individual by mail. The SSA will send either a copy of the short form, Disability Update Report (SSA-455-OCR-SM) or the long form, Continuing Disability Review Report (SSA-454-BK), announcing a CDR. The short form is generally for those whose condition is not expected to improve, and is only two pages long.

If a benefit recipient’s condition could improve, or if his or her answers on the short form concern the SSA, the agency will respond by sending the benefit recipient the long form. The long form is similar to the initial disability application at 10 pages long. The form will question whether the benefit recipient saw a doctor, was hospitalized in the past year, whether the recipient underwent medical tests in the past year, such as electrocardiograms, blood tests, or x-rays, and, whether that disability income benefit recipient was working.

A benefit recipient is encouraged to submit any updated medical evidence to the SSA, although the SSA may also obtain such information on their own. In general, the SSA will be reviewing the period of 12 months prior to the notice, although the agency can examine evidence from any time after a recipient was initially granted benefits.

Medical improvement review standard

Assuming that an SSDI benefit recipient has not returned to work, the SSA will first determine whether there has been medical improvement in that claimant’s condition. If improvement is not substantiated then the CDR process is complete, and the disabled individual’s benefits (and auxiliary benefits) will not be affected.

In contrast, if the answer is yes, the SSA will then decide if the medical improvement affects the benefit recipient’s ability (or inability) to work. Assuming it does not, the disability benefits would continue. But if the SSA comes to the conclusion that the benefit recipient’s condition has improved to the point where he or she can return to work, that person will be notified that benefit payments will stop and will be given the chance to appeal the decision.

If the SSA feels that the evidence is insufficient to decide, or if there are inconsistencies between what the benefit recipient reports and medical evidence, the benefit recipient may be required to participate in for a consultative examination, which is an examination by a doctor that is paid for by Social Security.

Timelines for requesting continued benefits

Certain deadlines for requesting that disability benefits continue apply to both SSDI and SSI.

A request for reconsideration must be filed within 60 days after receiving a notice of determination.

Users generally have three options when requesting reconsideration, as follows:

- Case review—An independent review of the record with or without additional evidence. This is the only option available in cases involving the medical aspects of a disability denial of an initial application.

- Informal conference—A review as in (1) in which users may participate. Users may present witnesses and may present the case in person.

- Formal conference—Same as (2), and user may request that adverse witnesses be issued a subpoena and cross-examined by the user or a representative. This type of reconsideration applies only in adverse post-eligibility situations (that is, when SSI payments are going to be reduced, suspended, or terminated).

Request for reconsideration

If benefits were stopped because of medical improvement, the individual who claims to continue to meet Social Security’s definition of disability can request a face-to-face hearing with a disability-hearing officer, even at the reconsideration stage.

Request for hearing

If the claimant’s request for reconsideration is denied, the claimant must file a request for hearing, and a request for continuing benefits, within 10 days after receiving the notice of adverse action. One may elect continuing benefits along with a hearing request even if he or she did not elect continuing benefits when filing the initial request for reconsideration. To continue receiving benefits, one must file a request for reconsideration (appeal) within 10 days of receiving the notice of cessation along with a request for continuing cash benefits, Medicare, or both. Note that this time limit is much shorter than the 60 days for the appeal itself.

If the claimant files the request for continuing benefits later than 10 days after receiving the notice of cessation or reconsideration, Social Security will deny the request for continuing benefits, unless the person making the request can show good cause for the late filing.

Further appeals

If one’s appeal is denied at the hearing level and that individual still wishes to appeal to the Appeals Council, he or she will no longer continue to receive disability benefits. However, if the Appeals Council remands the appellee’s case for a new hearing, benefits will continue with no action on the appellee’s part. One can also choose to continue benefits for others (such as children) receiving benefits based on the covered worker’s earnings record.

Completing the benefit election request form

The benefit election request form, Form SSA-795, Statement of Claimant or Other Person, can be downloaded from the Social Security website (SSA.gov). The form has a simple checkbox format, but an accompanying letter should also explain briefly, but specifically, why benefits should continue.

Continuing disability benefits for others

When a claimant requests to have one’s own benefits continued while appealing the cessation of his or her benefits, that appealing party should also request to continue benefits for others that were based on the appellee’s earnings record. However, the other persons receiving benefits based upon the appellee’s earnings record must also make their own election to receive continuing benefits: Each beneficiary must also make his or her own election to receive continuing benefits during the appeal period.

After the appellee requests continuing benefits for others receiving benefits on his or her earnings record, Social Security will advise those people of their right to elect to receive continuing benefits, and they then can respond with their own elections to receive (or not receive) continuing benefits.

Continuing SSI and Medicaid benefits

If one elects continuing SSI benefits and was eligible for Medicaid before receiving a cessation notice, Medicaid benefits will continue automatically. One’s needs-based SSI benefits may be suspended or changed while his or her appeal is pending if the appellee’s living circumstances change (typically changes in income, excess resources, or different living arrangements).

Working while appealing

If an individual received SSDI and worked at what would be considered substantially gainful employment during a trial work period while waiting for an appeal, that person’s SSDI benefits may be suspended.

When SSDI benefits will end

The general rule is that a claimant is no longer considered as disabled for purposes of receiving SSDI benefits in the month in which the cessation notice is mailed to the benefit recipient. Presuming that the recipient does not request a continuation of benefits, then his or her SSDI or SSI benefits will continue during the disability cessation month and the following two months (the grace period).

For example, on July 15, Carolyn received an SSDI cessation notice. She has responded well to a new drug and has experienced meaningful medical improvement. The last month for which she is able for the disability month is September unless she elects continuing benefits within 10 days after receiving the notice of cessation (and that the SSA receives it within 15 days).

Keep in mind that a claimant’s disability benefits might be suspended for specified reasons during the CDR process, such as failure to cooperate with Social Security by refusing a medical exam, the inability of Social Security to establish the claimant’s whereabouts, or unjustified failure to follow prescribed treatment. Even in these cases, the claimant has the same 10-day period from the receipt of the notice of cessation to elect continuing benefits.

Knowledge check

- Helen is currently receiving Social Security disability income benefits. However, there is a real possibility that her condition may improve. In typical circumstances, how frequently will Social Security review whether her disability benefits should continue?

- Five months.

- Annually.

- Every three years or fewer.

- Every seven years or more.

Repayment of denied benefits

If appeal is unsuccessful at any level, Social Security will ask the individual whose claim has been denied to repay the SSDI or SSI cash benefits that were paid while the appeal was pending. Social Security will not require repayment of the value of any Medicare or Medicaid benefits that continued while the appeal was pending.

Waiver opportunity

Social Security will consider waiving the recovery of disability benefits paid while an appeal is pending as long as the person who had received the benefits before the denial had appealed the cessation of benefits in good faith. An appeal is presumed to be made in good faith unless the individual filing the appeal failed to cooperate with Social Security during the appeal. Not cooperating generally means failing without good reason to provide medical or other information requested by Social Security or failing without good reason to attend a physical or mental examination.

Supplemental Security Income

SSI is a federal program that pays monthly benefits to low-income aged, blind, and disabled individuals. The SSA runs the program, which is financed from general tax revenues, rather than from Social Security (FICA) taxes. The SSI definition of disability for adult applicants is the same as the test in the SSDI program. Only individuals having low incomes and limited financial assets are eligible for SSI. Women comprise the majority of adults receiving SSI.

Although the SSI program is run by the SSA, operationally, it is actually a cooperative program between the SSA and the applicant’s state’s government. In that light, one’s eligibility, as well as the amount of benefits receivable, ultimately depend on the applicant’s state of residence. For federal SSI purposes (and most states reasonably follow these guidelines), one must meet all the following three criteria:

- Be blind, disabled, or age 65 or over

- Be either a citizen of the United States, or meet very narrow requirements based on U.S. permanent residency, military service, or political asylum or refugee status

- Have a low income

- Only about half of the beneficiary’s actual income will be considered, but this counted income cannot be higher than an amount set by the applicant’s state of residence, typically from $700 to $1,400 per month. However, some states allow people with higher incomes to receive state benefits.

- The assets owned (minus certain items, such one auto and the home) must be worth less than $2,000, ($3,000 for a couple).

If the application is approved, SSI benefits will include cash payments at a minimum of $771 per month for an individual or $1,157 per month for a couple (2019). The applicant’s state of residence may supplement this amount with an additional payment (the State Supplementary Payment). Any federally provided SSI benefits have been adjusted for annual inflation.

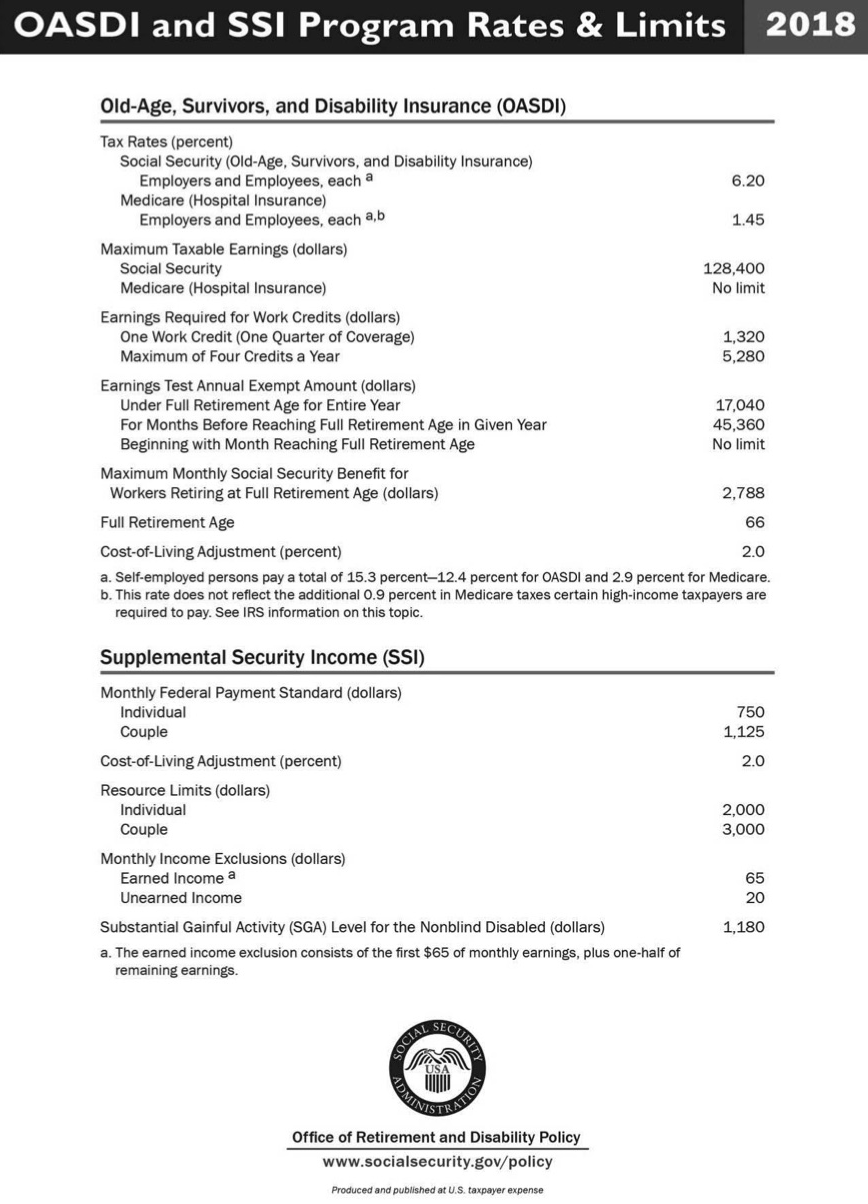

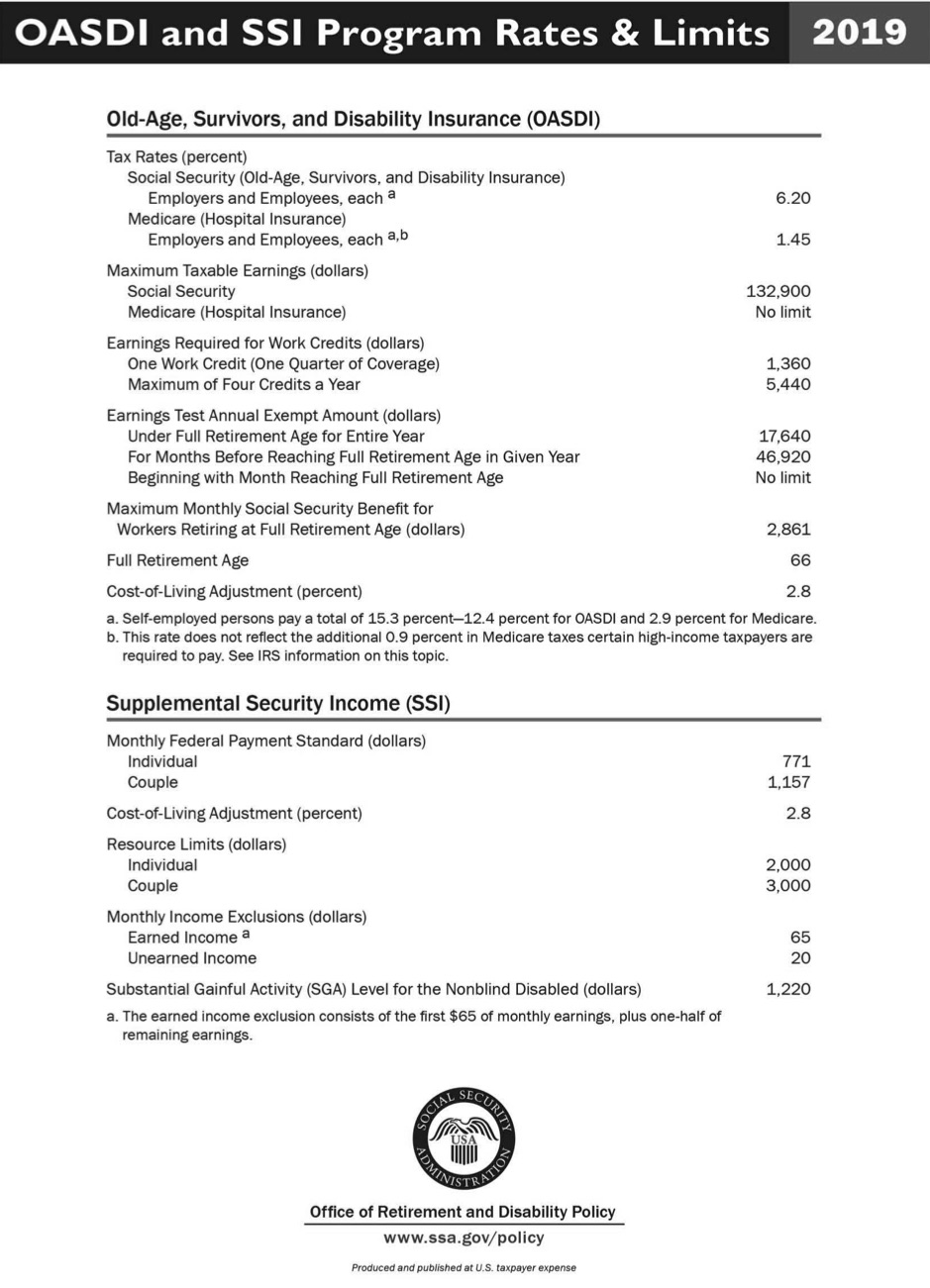

| SSI and old-age, survivors, and disability insurance (OASDI) program rates and limits |

See appendix A for 2019 rates and limits and appendix B for 2018 rates and limits This data can be found at: https://www.ssa.gov/policy/docs/quickfacts/prog_highlights/index.html. |

Knowledge check

- In March of the current year, the SSA notified George that he is no longer eligible for Social Security disability income benefits. Presuming that George does not appeal the decision, for how long, if at all, would his benefits continue?

- He would receive a check for March and benefits would stop immediately after.

- He would receive checks for March and April.

- He would receive checks for March, April, and May.

- He would receive checks for March and through the following six months.

Summary

We learned the importance of SSDI for many Americans. We examined how work history affects benefit eligibility, as well as the amount of the benefit itself. Social Security’s stringent definition of disability is arguably harsh. Its process for reviewing claims from a medical perspective operates at several levels. Because most initial claims for Social Security disability benefits are denied, it is important to understand the appeal process and how benefits may be paid during the appeal or that back pay can be the result of the delay and ultimate approval. Briefly, we covered how SSI operates as a needs-based program distinct from traditional Social Security.

Appendix A

OASDI AND SSI PROGRAM RATES & LIMITS 2019

Appendix B

OASDI AND SSI PROGRAM RATES & LIMITS 2019