DEADLY TEMPTATION #3

Precisely Calibrate Your Portfolio

We told you in Rule #3 that if you hear that asset allocation is the most important investment decision you can make—and that you must do it using a scientific optimization model—you should tune it out. Now we will tell you why you should tune it out.

Financial advisors will often give you the idea that they can very precisely control the risk and return of your portfolio. Their spiel often starts with “The most important thing is asset allocation.”

Back in 1986, a paper titled “Determinants of Portfolio Performance,” by Gary Brinson, Randy Hood, and Gil Beebower, was published in the Financial Analysts Journal.1 It got a huge amount of attention. It was cited, and re-cited, and cited again and again. Almost all of the references made to the article got its message completely wrong. It became conventional wisdom that “94% of investment performance is due to asset allocation.”

Well, that’s not what the paper said. The coauthors thought it must have been their title that threw people off—“Determinants of Portfolio Performance.” But, really, the confusion about what the paper actually said was largely due to the fact that misinterpreting it gave financial advisors a new lease on life. It offered them a new marketing pitch, which often sounded right to them but was a misconceived mish-mash of half-truths and falsehoods that they frequently passed on to clients for very substantial fees.

What the paper said was not that 94% of investment performance was due to asset allocation. It said that 94% of the variability of performance was due to asset allocation. That’s obviously not the same thing. Anyway, what’s it all about?

“ASSET ALLOCATION”

In the Brinson, Hood, and Beebower study “asset allocation” meant how an investor’s portfolio was divided among stocks, bonds, “cash equivalents,” and “other” investments. For example, the 91 pension funds they studied had an average allocation of 57.5% to common stock, 21.4% to bonds, 12.4% to cash equivalents, and 8.6% to other. Cash equivalents means short-term investments like short-term U.S. Treasury bills, commercial paper (short-term loans to corporations), and the like. Other investments could be anything that doesn’t fit into stocks, bonds, or cash—like crates of wine, art, gold, and so forth.

Stock prices are more variable—they go up and down more—than bond and cash equivalent prices. So it’s no surprise that the way in which the portfolio is divided among stocks, bonds, and cash goes a long way toward determining how variable the portfolio’s returns are. What the Brinson and colleagues’ study showed was that asset allocation among stocks, bonds, and cash explained much more of the variation in a portfolio’s returns than what the specific stocks in the stock portfolio were, or the particular bonds in the bond portfolio. In other words, you could guess right 94% of the time how variable the portfolio’s returns would be just by knowing how it was divided between stocks, bonds, and cash—without knowing what stocks or what bonds.

Somehow that simple point got conflated by the investment advisory profession (financial planners, brokers, etc.) into “You need us to help you determine the correct asset allocation because it’s the most important determinant of your investment performance.” Not only that, but the investment advisory profession also started to define asset allocation as something more complicated than what it really is. “Asset allocation” became how to divide your portfolio among several “asset classes.” These asset classes included subcatego-ries of stocks like growth stocks, value stocks, small stocks, and so on.

We’ll now explain what’s wrong with this. The main thing that’s wrong with it is that a lot of financial advisors are charging an awful lot for advice that provides no benefit to their clients.

NOBEL PRIZE-WINNING TECHNOLOGY

Let’s start with the “Nobel Prize-winning” technology that’s supposed to do the asset allocation for you. Many financial advisors use this approach. They sometimes make much of how “sophisticated” the technology is.

But here’s what it does: nothing. To explain this, we need to go back in history a few years.

Harry Markowitz’s Breakthrough

Investment risk used to be perceived as an attribute of an individual asset. A broker or financial advisor who recommended a stock to a client was held by law to be in breach of his duty if the stock was too risky for the particular client. This view changed with the publication of Harry Markowitz’s paper “Portfolio Selection” in the Journal of Finance in 1952.2 Markowitz’s most valuable contribution was to shift that view to the risk of a whole portfolio of investments. Because individual investments can be less than perfectly correlated, adding a risky stock to a portfolio might not add to the risk of the whole portfolio, but could even reduce it. That is, it might diversify the risk of the portfolio and thereby mitigate that risk. Markowitz went on to win the Nobel Prize in Economics in 1990, which made for a great marketing “hook” for the financial industry.

In his 1952 article, Markowitz stated this in a mathematical form. To do it, he needed to attribute three theoretical mathematical properties to securities:

![]() each security’s future expected return on investment,

each security’s future expected return on investment,

![]() the variability of that future return, that is, how much it fluctuates over time, and

the variability of that future return, that is, how much it fluctuates over time, and

![]() the correlation between returns on two securities, that is, to what extent they move up and down together.

the correlation between returns on two securities, that is, to what extent they move up and down together.

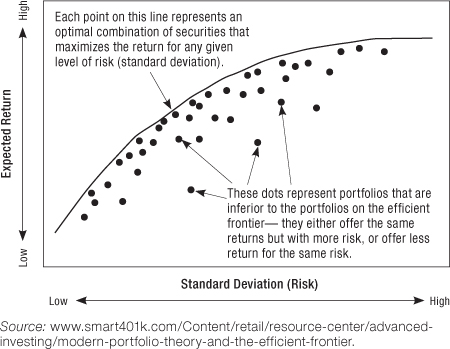

Using these three properties, Markowitz constructed in theory what he called the “efficient frontier” of portfolios. To create it, he needed a number for each portfolio he could call its “expected return” and a number he could call its “risk.” Technically speaking, the expected return and variability of a whole portfolio can be calculated from the properties he attributed to the individual securities in the portfolio. Hence, in Markowitz’s simplification, each portfolio of securities has two characteristics: its expected return, and its variability. Markowitz interpreted the variability of the portfolio’s return—how much it fluctuates—to be the portfolio’s risk. In theory, if you plot all portfolios’ risks versus their expected returns, you get a graph that looks like Figure 6.

FIGURE 6 Markowitz’s Efficient Frontier

Markowitz concluded that the best—the most “efficient”—portfolios were those on the curved upper line, which he called the efficient frontier. Any portfolio on the efficient frontier had a higher expected return than any other portfolio with the same level of risk, and a lower risk than any other portfolio with the same expected return. Hence, no other portfolio is superior to it in both risk and return.

Applying Markowitz’s Theory

Markowitz is a mathematician who was employed at the time at the RAND Corporation. RAND had been the innovator of important applied mathematics techniques in the field of operations research. Markowitz was now confronted with the mathematical challenge of finding out exactly which portfolios lay on the efficient frontier.

The solution method he devised involved a mathematical technique called quadratic programming (not to be confused with computer programming). This methodology excited people in the field, especially in academia, as well as newly minted graduates of academic programs in finance. They set about trying to apply the Markowitz quadratic programming algorithm to create the efficient frontier of portfolios of public stocks.

The first thing they realized was the sheer magnitude of the number of inputs that the method required. There were thousands of listed stocks. Markowitz’s algorithm required an expected return and variability for each of them, and the correlation for each pair. If portfolios were to be constructed from 1,000 stocks, the algorithm would require 501,500 inputs.

The second problem was that they needed to obtain numbers for the inputs. The obvious approach was to use historical data to estimate the inputs. So they tried using historical average returns for the expected returns, historical variabilities for the variabilities, and historical correlations for the correlations.

When those numbers were fed into the model, the results that came out were absurd. A model that was supposed to reduce risk through diversification might instead say that the efficient frontier consisted of combinations of only two stocks. The reason was that those stocks were the ones that had the highest historical returns, and therefore they had been assigned the highest expected returns; or they might be the ones with the lowest historical variabilities, and therefore they had been assigned the lowest future variabilities.

No matter what they did, the modelers found that the outputs of the model made no sense. Eventually, they employed a combination of trial and error and mathematical reverse engineering to see what inputs would produce acceptable outputs. (“Reverse engineering” means starting with a result and working backward to determine how it was produced, then using that knowledge to re-create the result.) In the end, this is precisely how the Markowitz model is used. Its inputs are laboriously rigged to produce outputs that the modeler feels are acceptable.

Oftentimes analysts find it too difficult or too much trouble to rig the inputs to produce the desired outputs. In that case, they simply force the output variables—the portfolio weightings—to come out as they wish, by imposing constraints on them. In other words, the desired outputs are specified and then the inputs and constraints are created in such a way as to force the model to produce them. In the end, the Markowitz model may be a neat formula, but trying to apply it in the real world is hopeless because there’s no way to get meaningful data to put into it, so in the end you just have to fudge it.

PORTFOLIO OPTIMIZATION AND ASSET ALLOCATION

Originally, programs that ran the Markowitz model to try to find the efficient frontier of stocks were called portfolio optimizers. They were supposed to find the optimum combination of stocks for a particular level of risk that would lie on the efficient frontier. As we’ve already seen, this proved extremely difficult.

Because running the Markowitz optimizer on a large number of individual securities is so cumbersome, and constraining it to produce acceptable results is so difficult, it is now used only for “asset allocation.” That is, the number of assets in a portfolio is reduced to a small number, such as 10 broad asset classes. For example, the asset classes may include categories like small value stocks, small growth stocks, large value stocks, large growth stocks, perhaps mid-cap stocks (stocks of mid-sized companies), and short-term, intermediate, and long-term bonds.

This exercise still requires rigging the inputs and, usually, constraining the outputs to be within acceptable ranges. Running an asset allocation on 10 asset classes still requires values for 65 input parameters. The end result has been the complete Orwellian perversion of the Markowitz model. Although financial professionals often boast that their firms use it, they don’t, really—its implementers only go through the motions, using it chiefly as a sales tool. The model has proven useful only for its basic conceptual insights, not for its practical application.

How Asset Allocation Is Actually Used

Most financial firms that offer financial advisory services perform an “asset allocation” for their clients (or prospective clients), usually presented as a very important part of their service. They let people know that a sophisticated computer model is used to create the asset allocation. Frequently, they add that it employs Nobel Prize-winning technology.

Through trial and error or other means, the investment firm has created (or outsourced the creation of) inputs to the model that produce an acceptable efficient frontier of outputs. They then ask the prospective client for her current portfolio. From that they construct her current asset allocation.

Invariably, an asset allocation on the firm’s efficient frontier will have a higher expected return for the same level of risk. That’s because, quite simply, the firm has constructed the outputs of the model—the efficient frontier—so that they have higher expected returns at each level of risk than any other portfolio. So if you input any other portfolio, it will fall below the efficient frontier. Since there are an infinite number of other portfolios, they will all seem to be “inefficient.” The result, however, is due to the arbitrary inputs they have created, not reality. The efficient frontier could be any one of an almost infinite number of arbitrary efficient frontiers, and still serve the same purpose. The model is used as a marketing device, not to solve any real-world problem.

THE HOAX THAT EVEN GOOD ADVISORS PERPETRATE

In short, the idea that asset allocation needs to be done using a sophisticated mathematical model is essentially a hoax. A lot of the time advisors don’t even know it. They buy software from some vendor and it does the asset allocation for them. The results of the asset allocation are determined by what the software provider put into the model. The results are whatever the software provider decided they should be. The model has little or nothing to do with it.

But a lot of the advisors who use it believe it does. Even the good advisors muddy up what they get right with use of the asset allocation model that seems to have become—in spite of its actual uselessness—a sine qua non of investment advising. So let’s first explain what the good advisors get right.

Passive Versus Active Investing

We’re going to make a different use of the terms “active investors” and “passive investors” than the meanings we assigned to them in Part I. There, we called “active investors” investors who invest in their own business—that is, a business they run or participate in or are employed by. “Passive investors,” by contrast, were investors who only buy the stocks or bonds of a business that they otherwise have no involvement in. All of the investors we are talking about here are passive investors in that sense.

But now we will mean something different by “passive investors” and “active investors.” Instead of picking and choosing stocks, passive equity investors just buy the whole stock market—or they buy all the stocks in some particular subcategory of the whole market. Some passive investment vehicles consist of bonds and buy a cross-section of the bond market. In contrast, active investors try to pick stocks (or bonds) that will beat the market. They do this in spite of the fact that—as we showed in Deadly Temptation #1—study after study after study shows how futile this is. That’s why more and more investors believe it’s better to invest passively at low cost to try to match the market averages, not beat them.

The best advisors know this and will tell you. Because this is now so thoroughly proven—and has been for a long time, yet active investment managers still dominate the market by cunning marketing—there is a large and growing minority of investment advisors and managers who recommend and practice passive investing.

Passive investing, actually, was originally derived from theoretical considerations, as the logical implication of Marko-witz’s theories. Markowitz’s theories—as further developed by Nobel laureates James Tobin and William F. Sharpe—implied that the best thing you could do as a stock market investor is diversify to the maximum. Diversifying to the maximum meant buying the whole market. That’s why we recommend just buying a world stock index fund.

If you buy the whole stock market, all you have to do is hold onto it, because it will always be the whole stock market. You don’t have to do any buying and selling—or hardly any, mainly only when a company pays a dividend that has to be reinvested, or when a new company goes public. If you own a world stock ETF, all that gets done for you by the ETF’s manager—and for a very low fee.

Feeding the Fee Machine

However, if you’re an advisor and you simply recommend to your clients that to invest in stocks they should just buy a single mutual fund or ETF—a total stock market fund—they’ll think you’re not doing much for them. They’ll think, “Well, what do I need you for? I could’ve done that myself.”

If you’re an index fund investor whose advisor has done an asset allocation for you, he won’t recommend just investing in one equity fund—a total market index fund. There’s not much asset allocation to do if you only invest in one equity fund. He’ll recommend that you invest in several asset groups that are sometimes called styles: for example, a large growth index fund, a large value index fund, a small growth index fund, and a small value index fund. And you run your asset allocation program among those—plus some bond categories.

And what does your asset allocator spit out? Almost always, the asset allocator will combine all the stock fund styles in a mix that nearly replicates—guess what?—a total market index fund. So instead of buying one total market index fund, you’ll be buying four to six style index funds that together make up a total market index fund.

What’s wrong with this? Well, several things.

First, the style index funds tend to charge more than a total market index fund. For one thing, they have to keep track of which stocks are in the style category. A “large value” fund is a fund that holds stocks in companies that are bigger than average and are trading for lower prices than you might expect given their fixed assets. To know which stocks to put in it and to keep in it, you have to do some data screening and know when a stock moves in or out of the category. This is a more “specialized” field of investing, supposedly, than just running a total market index fund, so the fund manager probably charges at least a little extra.

But there’s more wrong—much more. Because stocks move in and out of the large value category, you have to buy and sell more often than a total market index fund buys and sells. And to whom do you sell and from whom do you buy? Why, you sell to or buy from someone who runs one of your other sector index funds. For example, if a large value company stock’s market-to-book value ratio (a measure of its price compared to its fixed assets) goes too high to be in the large value category anymore, and thus becomes a large growth stock, then you can sell it to the manager of a large growth index fund. So your large value manager is going to be selling that stock to your large growth manager. There’s no change in your portfolio, but you have to pay the two-way transaction cost.

That’s kind of pointless, isn’t it? And it adds to the cost. So the asset allocation hoax not only doesn’t benefit you but also costs you something.

But it costs you more than that, because it’s one of the main things that you supposedly need to pay your advisor for. And your advisor, even if your advisor is saving you a bundle by recommending that you invest in low-cost passive index funds instead of high-cost actively managed funds, is still charging you a bundle himself. A typical “fee-only” advisor charges 1% of assets. We saw in Deadly Temptation #2 what 1% of assets in fees can do to your investments. And when you combine that with the little extra that is charged for style index funds, your investment gains may wind up being cut in half.

Yet all the conventional wisdom says how important asset allocation is, and it all comes from misinterpreting that 1986 Financial Analysts Journal article and misapplying Marko-witz’s portfolio optimization theory.

SUMMARY OF DEADLY TEMPTATION #3

1. A 1986 article in the Financial Analysts Journal said that asset allocation explains 94% of the variation of returns, not 94% of portfolio returns.

2. “Nobel Prize-winning” optimization technology can be applied to asset allocation only by jury-rigging the inputs to create acceptable outputs.

3. The end result of the theories of Nobel laureates in finance is that the most efficient portfolio is one that mirrors the whole market, a total market index fund.