CHAPTER 12

The Art and Science of Accurate Estimating

INTRODUCTION

“Kris, how long will it take to implement this new design?”

“If you mean how long until we produce a product with the new design feature, I'd guess eight months.”

“You guess? Come on, we need something firm.”

“All right. I estimate it will take eight months.”

“Great. Let's do it.”

This kind of dialogue is exchanged on thousands of projects every year. Simple as it is, it points up some of the key issues in accurate estimating. First, notice how Kris tried to clarify what was being requested before venturing a guess. Second, note that guessing wasn't acceptable; it was only when he changed his guess to an estimate that it was taken seriously.

Estimating is forecasting the future, trying to predict the time and money necessary to produce a result. Because forecasting the future is an uncertain business, it should come as no surprise when an estimate turns out to be wrong. But a wrong estimate isn't good enough for most project stakeholders; customers, especially, want the product on time and within the promised budget. This means that we need to focus on estimating accurately; we need to be able to predict the future in an uncertain world.

Professional estimators—those people who make their living by developing cost and schedule estimates—have developed many methods of predicting the future. When you consider how many formulas and calculations these professionals work with, it would seem reasonable to define estimating as a science. We will see, however, that art plays a critical role in estimating. (It may be that those with extremely accurate methods for predicting the future have left the pedestrian field of project management and are applying their expertise in locales where the fruits of their labor are seen more quickly and are more tangible, such as Wall Street or Monte Carlo.) This chapter confronts the difficulty of forecasting the future. We examine the factors that make our estimates wrong and suggest techniques that can make them more accurate. You'll find a Planning Checklist online that you can use as you complete your project plan to ensure you've covered all the bases described in this chapter and the other chapters in Part 3.

ESTIMATING FUNDAMENTALS

As we've observed many times, all projects are unique. In fact, the more unique they are, the more difficult they are to estimate; the less unique, the easier to estimate. Research and development (R&D) projects, for instance, are extremely difficult to estimate, because they are attempting to solve new problems. But every project will produce a unique product, which means that a different combination of tasks will be employed. In addition, there are usually a number of other unique or unpredictable factors on any project:

- The people on the project team may be unknown to the manager. However, their particular skills and knowledge will affect their productivity, and the more complex the tasks are, the more this productivity factor counts.

- Projects that rely on new technology face questions about the reliability of the new technology and the learning curve of the team.

- Since estimates are used to coordinate activities and forecast resources, incorrect timing predictions will cost money. If the project is behind schedule when a subcontractor arrives, you may have to pay the subcontractor to sit around and wait. If it is so far behind schedule that the vendor must be sent away, then this vendor may not be available when needed.

Avoid the Classic Mistakes

Avoid the Classic Mistakes

Common sense is not all that common. There are certain mistakes that many of us seem to fall into, even though common sense may warn us to avoid them. Following are the most common.

Making “Ballparks in Elevators”

Maybe it's their authority, or maybe it's that you're off guard, but whenever a high‐level manager or customer catches you in an elevator, hallway, or break room and asks for an estimate, you inevitably respond with an optimistic, seat‐of‐the‐pants guess that you regret the moment it escapes your mouth. The problem is compounded if that manager happens to be on the way to a meeting where your “estimate” will be the topic of discussion. The trouble here is obvious: It's impossible to consider all the details required for an accurate estimate when you're riding between the fourth and tenth floors. But the question is how to avoid this optimistic guessing. Here are a few suggestions:

- Assume a thoughtful, concerned expression and respond to the manager, “There are a lot of factors that will impact the effort required.” Then list a few of these factors and add, “I wouldn't want to mislead you by offering a guess on that.”

- Offer to get a sheet of paper and write down exactly what the manager is requesting. At the same time, start listing the questions that need to be answered before a useful estimate can be produced. If the manager has a hard time being specific about what he or she wants—and you can produce several questions he or she can't answer—this should help the manager to understand that there are too many unknowns to make a responsible estimate.

- If all this maneuvering fails and the manager or customer continues to press you, it's time for the art of “ballparking.” There can be three possible responses when using this technique: (1) Respond with the best guess you've got, while trying to factor in everything that could make it wrong. This response is appropriate for people who can be trusted not to use this figure against you later on. (2) Take your very best guess and double it. Then double it again. This is obviously not a rational way to make estimates, but then again, the manager or customer is hardly being rational by asking you for an estimate in the elevator. (3) Refuse to give an estimate without further specifications and planning time.

Estimating Without Complete Specifications

This is the type of mistake that a contractor might make if asked to estimate a construction project without a blueprint. Realistically, developers and contractors rarely make this mistake more than once. On the other hand, new product development, process improvement, and information systems projects seem to make this mistake regularly. Someone has an idea, the idea is approved, with a budget and a deadline, and off they go! They don't seem concerned that the specifics of implementing the idea won't be known until they are halfway through the project. The allure of this mistake is that it seems as if team members are adopting good business practices; after all, they do have a budget and schedule attached to the new initiative. But without complete specifications, it isn't clear what the project will be producing, so there is no basis for an accurate estimate.

One thing that new product development, process improvement, and information systems project all have in common is that they are solving a problem first, then creating the solution. Even software projects using agile methods need to be careful about jumping into a new project without a clear vision of what they'll be producing. All these projects should start with a business case that includes estimates. The mistake is putting too much confidence in the initial estimate when there are more assumptions than facts.

Confusing an Estimate with a Bid

Bids and estimates are not the same thing. An estimate is a projection of how much and how long a project will take, while a bid is the schedule and budget a subcontractor offers to deliver the project. The bid will quite likely be made up of estimates, but it will also include profit margins for the subcontractor. The important distinction is that a bid is calculated to be both attractive to the customer and profitable to the bidder, while an estimate is a prediction of what it will really take to deliver. The best bidders—the ones who make both themselves and their customers happy—are also good estimators.

Padding the Estimate

There are many legitimate reasons for adding time or money to an estimate. Contingency funds may be added for risks identified during the risk management process. Extra time is usually added to allow for inevitable delays due to illness or vacations. But padding the estimate is different. Adding time and money to the estimate solely for the purpose of bringing the project in early and under budget is neither legitimate nor productive. The best strategy is to offer honest, detailed estimates. Then, if they are cut, you can use the actual performance data during the project to fight for acceptance of the original estimate. Eventually, this kind of straight dealing will gain you a reputation as an honest estimator who delivers on promises.

Table 12.1 shows how adding to the cost and schedule just to be safe is counterproductive in two ways. First, a valuable project may not be approved because the artificially high estimate makes it look like a bad investment. Second, if the project is approved with an inflated budget, this means it is taking money away from other potentially valuable projects.

Follow the Golden Rules

Just as there are classic estimating mistakes to avoid, there are certain golden rules that apply at all times to all projects. These rules emphasize the appropriate attitude toward estimating.

Have the Right People Make the Estimates

Three factors define who the right people are:

- The estimators must be experienced with the work they are estimating. No matter which techniques are used, estimating is always based on an understanding of the work to be done.

- The people who will actually perform the work should also be involved in estimating it. They will have the best grasp of their own limitations. They will know, for example, just how much time their schedule will allow them to work on this project; they will also know whether they will need a steep learning curve before they are productive. Most important, when people make an estimate for their own work, they are usually more motivated to achieve it than when the estimate comes from the outside.

- The estimators must understand the goals and techniques of estimating. Even when people understand the task at hand, they should not be allowed to estimate their own work until they learn both how to estimate and the goal of estimating, which is to produce accurate estimates that will come true, not optimistic projections of the best possible performance.

TABLE 12.1 Artificially Inflating Project Estimates Can Hurt The Bottom Line

| Project | Priority | Best Estimate | Inflated 20% | Revenue Year 1 |

|---|---|---|---|---|

| Blue | 1 | $300,000 | $360,000 | $1,000,000 |

| Red | 2 | 150,000 | 180,000 | 750,000 |

| Orange | 3 | 200,000 | 240,000 | 750,000 |

| Green | 4 | 200,000 | 240,000 | 600,000 |

| Black | 5 | 150,000 | 180,000 | 500,000 |

| Total | $1,000,000 | $1,200,000 | ||

| ||||

Base the Estimate on Experience

Even though no two projects are alike, there are often enough similarities that performance data from past projects are useful in estimating future ones. Professional estimators constantly use new performance data to refine their estimating models. Building this type of database is beyond the scope of the individual project manager; the organization must take responsibility for it. With this kind of database, project estimates can become more and more accurate. Without it, every project team must start from scratch and rely solely on each member's memories and gut feelings. Past performance data will make every estimating technique in this chapter more accurate.

Don't Negotiate the Estimate—Negotiate the Equilibrium

Don't Negotiate the Estimate—Negotiate the Equilibrium

There are effective ways of countering attempts to meddle with an estimate. Consider the following scenario.

A project estimate has been developed by experienced estimators using past performance data from similar projects and employing sound estimating techniques. The project manager brings the estimate to management or customers and they begin to whittle away at the schedule and budget. (Or perhaps they may even take out a cleaver and whack away a big part of both.) At first the project manager stands her ground, but under continuing pressure she begins to give up cost and schedule, slowly letting the finish date move earlier and the budget get smaller.

Stop! This estimate was built from the product specifications, and it represents a realistic balance of cost, schedule, and scope. Dickering over cost or schedule alone throws the entire estimate out of equilibrium. While no estimate will go unchallenged, the proper defense is to demonstrate how the estimate is tied to the product specification and work breakdown structure. When estimates are developed correctly, they can be reduced only by changing the product or the productivity of the workers.

Three Levels of Accuracy

Everyone wants accurate estimates, but accuracy costs money. It makes sense, therefore, to use different estimating techniques for the different decision points in a project. For example, initial evaluation of a project idea shouldn't take as much time and effort (or money) as the detailed planning necessary for formal project approval. Let's look at three levels of accuracy at different stages in a project.

Idea Evaluation or Ballpark Estimate

This is the estimate we all try to avoid giving. Ballpark estimates can be off by as much as 90 percent, yet they are still useful for initial sizing. These estimates take almost no time—they are the result of a gut feeling from an expert. Their accuracy relies on the estimator's knowledge. The only function of a ballpark estimate should be to evaluate whether it would be useful to get a more accurate estimate.

Project Selection or Order of Magnitude

Also known as ROM, for rough order of magnitude, this estimate also has a wide variance, but is based on extrapolations from other projects instead of the gut feelings of the ballpark estimates. The main difference between a ballpark estimate and an order‐of‐magnitude estimate is represented by a few hours of effort comparing the proposed project to past projects. For example, a builder may find that a proposed building is about twice the size of a similar one he has built and will therefore estimate the new one at twice the cost. If he decides that the proposed site for the new building will be more challenging, he might add another 10 to 20 percent. We call this type of comparison an analogous estimate. If an order‐of‐magnitude estimate is acceptable, several actions may result: A project may be formally initiated, a project manager identified, account codes set up, and the work begun on defining and planning the project. This planning is where the real work of creating an accurate estimate will take place.

Detailed Estimates

Detailed estimates are sometimes referred to as bottom‐up estimates, because they are based on all the various steps involved in project planning. A detailed estimate includes all of the schedule and resource information (as discussed in Chapter 10) and a forecast of a project's budget and cash flow (described later in this chapter). This is the estimate that will be used to manage the project and evaluate its success.

There is a huge difference in accuracy between an order‐of‐magnitude estimate and a detailed estimate, because the latter assumes a detailed understanding of the product and is based on the availability of key resources. Enormous amounts of work specifying product requirements and design work take place between the order‐of‐magnitude estimate, when there are no specifications, and the detailed estimate, which is based on specifications. This work requires large expenditures of time and money, but this money is not spent until the inexpensive ballpark and order‐of‐magnitude estimates determine that the project is feasible.

ESTIMATING TECHNIQUES

Good project managers realize that it takes time and effort to produce accurate estimates, so they choose among a variety of estimating methods to get the accuracy they need. There is no shortage of information in this field. A number of books have been written on estimating alone. Computer‐based estimating models with proprietary algorithms cost thousands of dollars. Entire seminars are taught on estimating software projects, construction projects, and pharmaceutical development projects. This book cannot make an exhaustive presentation of all these estimating methods; instead, our purpose is to help you understand the dynamics of accurate estimating by presenting a variety of established estimating techniques—the basic building blocks used by all skilled estimators.

Phased Estimating

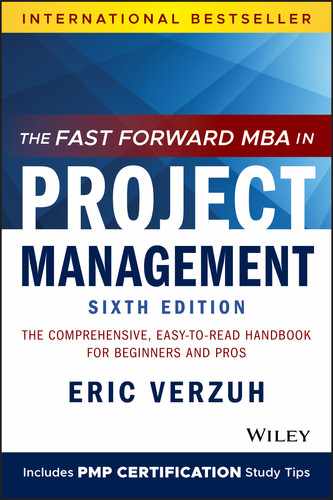

Phased estimating is a favorite among project managers because it requires cost and schedule commitments for only one phase of the project at a time. The phased estimating approach recognizes that it is impractical to demand a complete estimate at the beginning of the product life cycle. Instead, it breaks down the full product life cycle into phases, each of which is considered a project (see Figure 12.1). If you recall from Chapter 4, the product development life cycle describes the work required to create a new product, while the project life cycle focuses on managing the work. A number of projects can be involved in the development of a new product.

Phased estimating revisits the original business case as each phase ends and asks executive management to renew authorization for the project using updated estimates.

FIGURE 12.1 Phased estimating.

There is an enormous amount of uncertainty at the beginning of every development life cycle, but this uncertainty is reduced as the project progresses and more information is gathered. This presents a dilemma, because the customer, more than any other stakeholder, wants an accurate time and cost estimate for the complete development life cycle. This demand is easy to understand because the customer is trying to make an investment decision. The problem is that there is so much uncertainty when the product development effort is first considered that an accurate cost and schedule projection is impossible to produce.

The phased estimating approach recognizes this impossibility and instead breaks down the full product life cycle into phases, each of which is considered a project. Here is what this process looks like:

- The first phase is initiated with an order‐of‐magnitude estimate for the full development life cycle combined with a detailed estimate for the first phase. This detailed estimate is considered a commitment by the project team; this commitment signals an end to the uncertainty that surrounds a new project. By agreeing to a detailed plan with a fixed completion date, the team becomes more focused and productive.

- At the end of the first phase, a new authorization for the second phase starts this cycle once more. A new order‐of‐magnitude estimate is developed for the remainder of the product life cycle, together with a detailed estimate for the second phase. The new order‐of‐magnitude estimate will be much more accurate than the previous one because so much has been learned from the first development phase. This cycle of phase authorization will be repeated at each phase gate, and each time the order‐of‐magnitude estimate will become more accurate.

Project managers and teams like phased estimating because they are only required to commit to cost and schedule estimates for one phase at a time, what we call a “realistic planning horizon.” The benefit to the people funding the project is not always so clear. To them, it appears that the project team just keeps asking for more money and time at every phase review, with no accountability to project budgets and schedules.

What this customer group needs to realize, however, is that phased estimating is a risk‐reduction technique that also works in their favor. If the project team is required to commit to a cost and schedule estimate for the full product development life cycle before it has enough information about the product, this will place everyone at risk. This is because the team is likely to come up with an inaccurate estimate at this early phase.

Customers often believe that getting a firm commitment from the project team is their safeguard against runaway budgets, but, in this case, they are mistaken. Without a realistic budget, unforeseen costs are likely to crop up as the project progresses—and the customer will be the one to pay for them. This will be true even if the project team is an external firm with a fixed‐price contract. If these overruns become too extreme, this team may simply leave, preferring damage to its reputation to bankruptcy. At this point, the customer will have lost money, and the project will still be incomplete. Without the accurate estimate, both sides will lose.

On the other hand, if the customer and project team work for the same organization—as is the case with many product development projects—then it is obvious who will pay for cost overruns: the company that both work for. If the original estimate was too low, no amount of pressure from above will get the project team to meet it. Again, both sides lose.

Customers will embrace phased estimating when they understand that every new phase gives them an opportunity to completely reevaluate the effort, or even cancel it if it looks too expensive. If they like the product but don't like the project team, then this is the obvious time to choose another. While it's true that canceling will mean that they have no end product to show for their money, at least they will have canceled an unrealistic project before it costs them even more.

Phased estimating is always used on construction projects. If you planned to build a house, no contractor would commit to a bid until you knew the location and had a blueprint. After the design was complete, you might find that the cost of the house was too high and decide not to pursue the project. This realization didn't come without cost, because you had to spend time and effort to find the location and pay for the design of the house. But it was smart to do your homework before you started digging a hole for a house you couldn't afford!

Successful project managers treat every phase of the development life cycle as a project. They use the phased estimate approach to formally review the cost‐schedule‐scope equilibrium several times during the product development life cycle. The great advantage to this method is that it allows the project to be directed by many small, informed decisions rather than one large, premature decision.

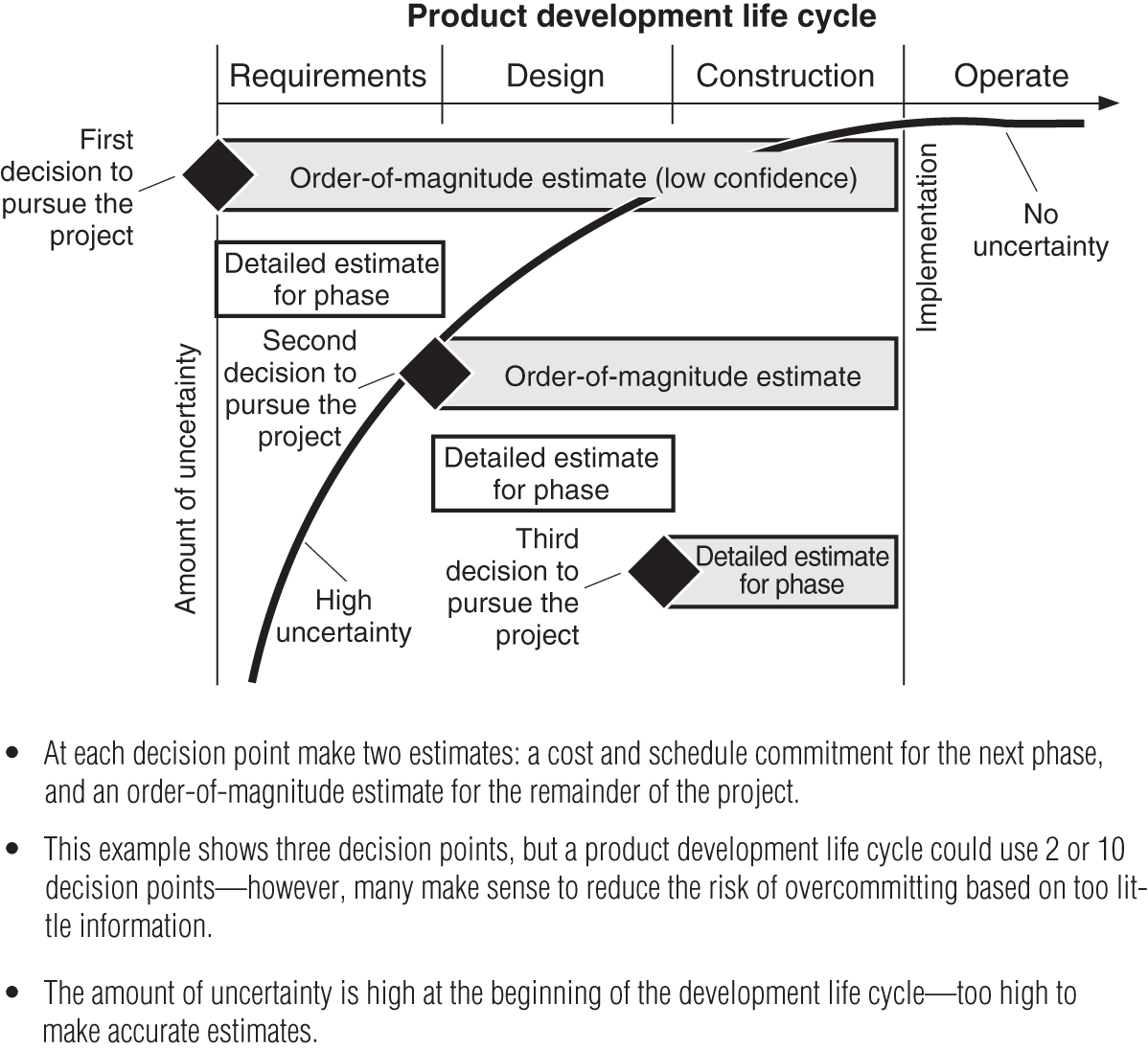

Apportioning

Also known as top‐down estimating, apportioning begins with a total project estimate, then assigns a percentage of that total to each of the phases and tasks of the project. The work breakdown structure provides the framework for top‐down estimating (as shown in Figure 12.2). Making useful top‐down estimates relies on some big assumptions, among them:

- Since apportioning is based on a formula derived from historical data of other, similar projects, the historic projects must be very similar to the project at hand for the formula to be accurate.

- Since apportioning divides a total project estimate into smaller pieces, it will be accurate only if the overall estimate is accurate.

Although apportioning is rarely as accurate as a bottom‐up estimate, it is an appropriate technique for selecting which projects to pursue. Despite its wide accuracy variance, it allows a project selection committee to approximate the length of project phases; this information then helps the committee decide which projects can be initiated and executed during a given budget period (see Table 12.2).

Apportioning is a valuable technique when used in conjunction with phased estimating. During phase reviews, the formula for apportioning can use the figures from the actual cost/effort of completed phases to increase the accuracy of the order‐of‐magnitude estimate (see Figure 12.3). For instance, if the original top‐down estimate dictated a phase‐one cost of $75,000, and the actual phase‐one cost was $60,000, this means that the overall project estimate should be reduced by 20 percent. Again, notice the need for an accurate apportioning formula.

FIGURE 12.2 Work breakdown structure as a basis for apportioning.

Parametric Estimates

As the name implies, the parametric technique seeks a basic unit of work to act as a multiplier to size the entire project. The golden rules of estimating really apply with this technique: It is always based on historical data, and the estimator must develop a solid parametric formula. To see how parametric estimating works, consider the following examples:

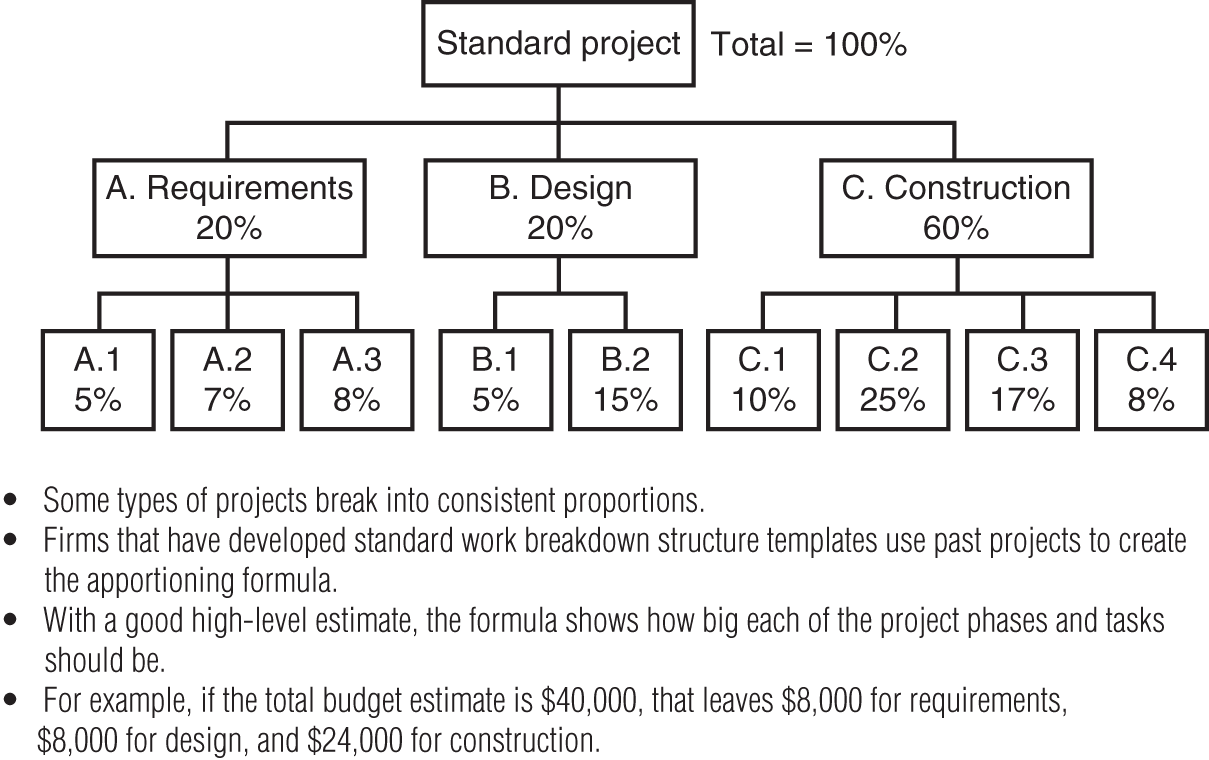

- A cycling group in Dallas, Texas, was planning a cross‐country bicycle trip, starting in Seattle, Washington, and ending in Miami, Florida. Based on their experience riding together every Saturday for 2 months, they figured they could average 80 miles per day comfortably. A road atlas put the total trip distance at 3,334 miles. Dividing 3,334 by 80, they estimated the total trip would last 42 days. At this point, the only parameter was this normal daily rate of 80 miles. But when one of the riders pointed out that all their practice rides had been on relatively flat terrain in dry weather, they made changes to their model. They reduced their average daily mileage to 30 for the mountainous parts of their route (the route had about 200 miles of mountain crossing), and they added 10 percent for weather delays. This changed the formula from one to three parameters: normal daily rate, mountain rate, and weather factor. The new parametric formula looked like this:

- A manufacturing company needs to have its 340‐page user manual localized into several languages. Based on past localization projects, the staff has created a parametric estimating model. The basic unit of work is a page. On average, 15 pages per day can be localized into the target languages. This parameter assumes two people working together on every target language. If the number of people is increased or decreased, the parameter changes. But if they add a new language and therefore new members to the team, the parameter of 15 pages a day is probably too optimistic for the first document.

- To estimate the carpet allowance on a house remodel, the project manager figured a cost of $5 per yard for purchasing the carpet and $4 per yard to install it, or $9 total cost. Then he measured the length and width of all the rooms, calculated the area in square yards, and multiplied by $9. Construction projects are full of parametric estimates of this kind.

- On a defense program to build a new jet fighter, the total number of engineering drawings required was estimated from a conceptual model of the proposed aircraft. Thousands of drawings would be created from this model, and, based on past experience, the staff estimated that the average drawing would take 200 engineering hours. With the drawing as the basic unit of work, this simple parametric model allowed them to estimate the total engineering effort. By dividing the total number of hours by the number of engineers they assigned to the project, they set the high‐level schedule. Obviously, this was not sufficient detail for managing all the work, but because their parametric model allowed them to accurately estimate both the number of drawings and the average time per drawing, at least the engineering phase was accurately sized.

Three lessons can be distilled from these examples:

- While it's possible to use parametric models to create either project‐level or task‐level estimates, the estimates will be more accurate at the lower level. Nevertheless, high‐level parametric estimates make excellent order‐of‐magnitude estimates and are accurate enough for the process of project selection.

- When building detailed estimates, greater accuracy is achieved by first estimating the low‐level tasks (work packages) using parametric models, then combining all these work package estimates to build the project or phase estimate. It is useful to employ parametric modeling at all decision points (phase gates) in the phased estimating approach, both to create the high‐level estimate and to ensure the next phase commitment.

- The variables in the parametric formula almost always require detailed product specifications. The more accurate the specifications, the more accurate the model. For example, the translation project required a completed user guide in the original language. Construction projects require blueprints. Both of these examples make one important point: Parametric estimating is usually applied to the construction phase of a product life cycle.

FIGURE 12.3 Apportioning works with phased estimating.

Bottom‐Up Estimating

Bottom‐up estimating requires the most effort, but it is also the most accurate. As the name implies, all the detailed tasks are estimated and then combined, or rolled up (see Figure 12.4). Bottom‐up estimating is another name for the planning model presented in Chapters 9 and 10 (see Figure 9.1 in Chapter 9). The final component of that model, building a project budget and cash flow, is described at the end of this chapter.

Within the planning model, step three calls for estimating work packages. (Recall that work packages are the lowest‐level tasks on the project.) The accuracy of the entire model is dependent on the accuracy of these work package estimates. (Recall from Chapter 9 the rules for work package size and from Chapter 10 the many variables that affect work package estimates.)

TABLE 12.2 Apportioning Supports Annual Budget Development

FIGURE 12.4 Bottom‐up estimating.

If bottom‐up estimating is so accurate, why isn't it always used? It would seem the accuracy justifies the additional time to build the schedule. The answer is that at the very beginning of a product development life cycle, there just isn't enough information to develop a detailed bottom‐up estimate for the entire life cycle. So bottom‐up estimating works only to build the detailed phase estimates.

Agile Estimating Practices

A significant factor in the growth of agile methods was the difficulty of estimating software projects. Projects that use agile still make estimates, but the purpose and mindset is different than for projects using a predictive development approach.

Project‐level estimates are necessary for project selection and prioritization. Organizations that use agile methods have limited budgets, and before starting a project they need estimates. The top‐down analogous and parametric methods mentioned earlier in this chapter are relevant here. As a new project is contemplated, the key question is, “How is this project similar to previous projects?”

Sprint, or iteration estimating, turns the estimating question inside out. Since each sprint is the same duration and the size of the team doesn't change, the schedule and cost are fixed. Estimating is focused on what scope can be accomplished by the team within the available time.

One of the most common approaches to estimating scope for a sprint is to create a sizing scale and assign a relative size to the highest‐priority items in the product backlog. An example of a common sizing strategy is shown in Table 12.3. The key to using this approach is to accept that there is no universal definition of small or medium. Instead, the scale is only intended for use within the project. As long as the team uses a consistent scale for all sprints, the scale is meaningful within the project.

Teams assign each item of scope a “T‐Shirt Size.” The size indicates the relative effort required. The Fibonacci sequence allows a wide range within five sizes.

Assigning points to each item in the backlog allows a team to define the amount of scope for a sprint by points. A team might, for example, set a goal to accomplish 150 points worth of scope in every 2‐week iteration.

BUILDING THE DETAILED BUDGET ESTIMATE

Project budget estimates can be “ballparked,” calculated with parametric formulas, and determined through apportioning. While these high‐level estimates are useful in the process of selecting projects, they are not accurate enough for managing a project. Once the project is approved, there is a need for a detailed, accurate cost estimate.

The detailed cost estimate becomes the standard for keeping costs in line. Everyone—customer, management, project manager, and team—is better served when a cost target is realistically calculated from a detailed plan. The team understands how the goal was created, and customers and management can be more confident that the project will stay within budget. Forecasting cash flow enables the project's funding to be planned and available when needed. And finally, during the course of the project, this detailed cost information will help in controlling the project, monitoring the progress, identifying problems, and finding solutions.

TABLE 12.3 A Sprint Estimating Scale

| T‐Shirt Size | Extra‐Small (XS) | Small (S) | Medium (M) | Large (L) | Extra‐Large (XL) |

|---|---|---|---|---|---|

| Fibonacci Number | 1 | 2 | 3 | 5 | 8 |

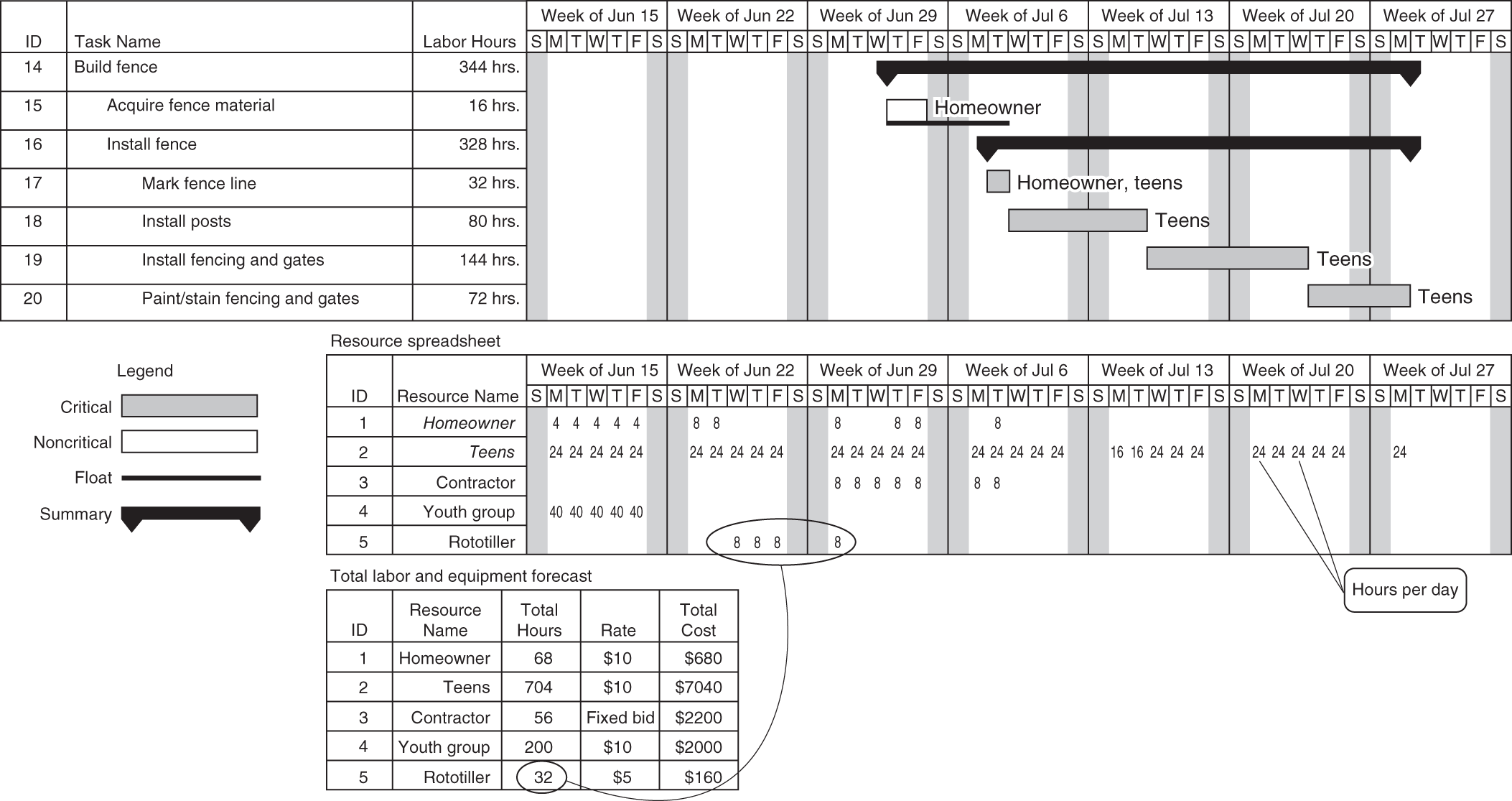

FIGURE 12.5 Calculated labor and equipment costs using the project plan with resource spreadsheet.

Sources of Data for the Detailed Budget

The actual calculation of a budget is pretty straightforward; it simply involves adding up figures. Just about any spreadsheet program is a good tool for the total budget calculation. What isn't easy is creating the numbers that go into the overall calculation. The following categories are the basis for the budget calculation. (Keep in mind that these are high‐level categories. Depending on the size and nature of any project, some categories may be eliminated or may need to be broken down to be more specific.)

Internal Labor Cost

Internal labor costs represent the effort of people employed by the firm. The planning model discussed in Chapters 9 and 10 forms the basis for estimating the total labor costs (see Figure 9.1 in Chapter 9).

The detailed source for all labor estimates comes from estimating the individual tasks. Including the sequence constraints and leveling the resources presents a realistic view of how many people are required. The resource projection represents the total effort. All that remains is to multiply each resource by its hourly (or daily, weekly, or monthly) rate to derive the total internal labor cost for the project. Figure 12.5 shows the total resource projection derived from the detailed schedule, the labor rates, and the total project labor cost.

Use the Burdened Labor Rate

![]() The actual hourly pay of salaried employees varies from person to person, often for no discernible reason. But it is rare to have to worry about actual pay when estimating labor costs. Instead, look to the finance department to establish a standard burdened labor rate for each labor type. A burdened rate is the average cost of an employee to the firm. It includes wages, benefits, and overhead. Overhead represents the many fixed costs that are spread over all projects, such as functional management, workplace facilities and equipment, and non‐project costs like training. It’s not necessary for a project manager to figure out this rate; nearly every company has an established burdened labor rate on record.

The actual hourly pay of salaried employees varies from person to person, often for no discernible reason. But it is rare to have to worry about actual pay when estimating labor costs. Instead, look to the finance department to establish a standard burdened labor rate for each labor type. A burdened rate is the average cost of an employee to the firm. It includes wages, benefits, and overhead. Overhead represents the many fixed costs that are spread over all projects, such as functional management, workplace facilities and equipment, and non‐project costs like training. It’s not necessary for a project manager to figure out this rate; nearly every company has an established burdened labor rate on record.

Don't Leave Out the Cost of Staffing the Project

A big mistake—which, unfortunately, is made on a routine basis—is leaving out the cost of internal staff in the project budget. The usual justification for this folly is that “these workers are free to the project because their salary is a constant.” But this statement would be true only if salaried employees had infinite hours available to work on projects. Including internal labor cost in a project budget is necessary to build the kind of realistic budget that will allow management to choose among multiple project opportunities.

Internal Equipment Cost

Internal equipment costs apply to special equipment that is not routinely available. They do not apply to the kind of equipment that is standard or assumed for all workers. Technical writers, for example, are assumed to have computers with word processing software; street repair crews are assumed to have shovels. But if that street repair crew needs a backhoe, the cost for this special equipment needs to be estimated separately. This separate estimate allows the purchase and maintenance costs of the internal equipment to be passed on to the customer.

These internal equipment costs can be estimated using the same steps used in estimating internal labor costs. Figure 12.6 shows equipment use on the resource plan.

Estimating Equipment That Will Be Used Up

![]() If equipment will be purchased and used up on a single project, then all you will need to do is add up the pieces of equipment and the cost of each (a parametric estimate). For example, a boring machine used to dig utility tunnels uses up drill bits at the rate of 1 every 50 feet. So a 1,300‐foot tunnel will require 26 drill bits (1,300 divided by 50).

If equipment will be purchased and used up on a single project, then all you will need to do is add up the pieces of equipment and the cost of each (a parametric estimate). For example, a boring machine used to dig utility tunnels uses up drill bits at the rate of 1 every 50 feet. So a 1,300‐foot tunnel will require 26 drill bits (1,300 divided by 50).

Estimating Equipment Used on Multiple Projects

![]() Use a unit cost approach to estimate equipment purchased for one project but expected to be used on many others. Here's an example.

Use a unit cost approach to estimate equipment purchased for one project but expected to be used on many others. Here's an example.

R&D engineers for an aerospace company needed an expensive computer to run complex tests. At $50,000, the computer would double the project budget, and this extra cost would probably prevent the project from being approved. But since they could identify five other potential projects that would use the machine in the immediate future, they were able to justify the cost of the new computer by spreading its cost over the expected use for the next 2 years. The formula used to spread the cost across several projects gave them a unit cost (hourly rate) that they could apply to their project estimate.

External Labor and Equipment Costs

It's possible to use the same approach in estimating external labor and equipment costs as in estimating internal labor and equipment. The only differences will stem from the type of contract negotiated with the external contractor or vendor. Under a cost‐plus contract, the labor and equipment rates are written into the contract, and the vendor bills the project for the amount of labor, equipment, and materials supplied to the project. In this case, either the project manager or the vendor can estimate the work and arrive at the total cost by using the same bottom‐up method described for internal costs. In the case of a fixed bid, however, the vendor will estimate the total cost of labor and equipment for its part of the project and will be held to this figure (that's why it's called a fixed bid). In this latter case, the vendor has performed the necessary estimating; all that's needed is to add this estimate into the total labor and equipment costs. (See Chapter 8 for more on the difference between fixed bids and cost‐plus contracts and their impact on estimating accuracy.)

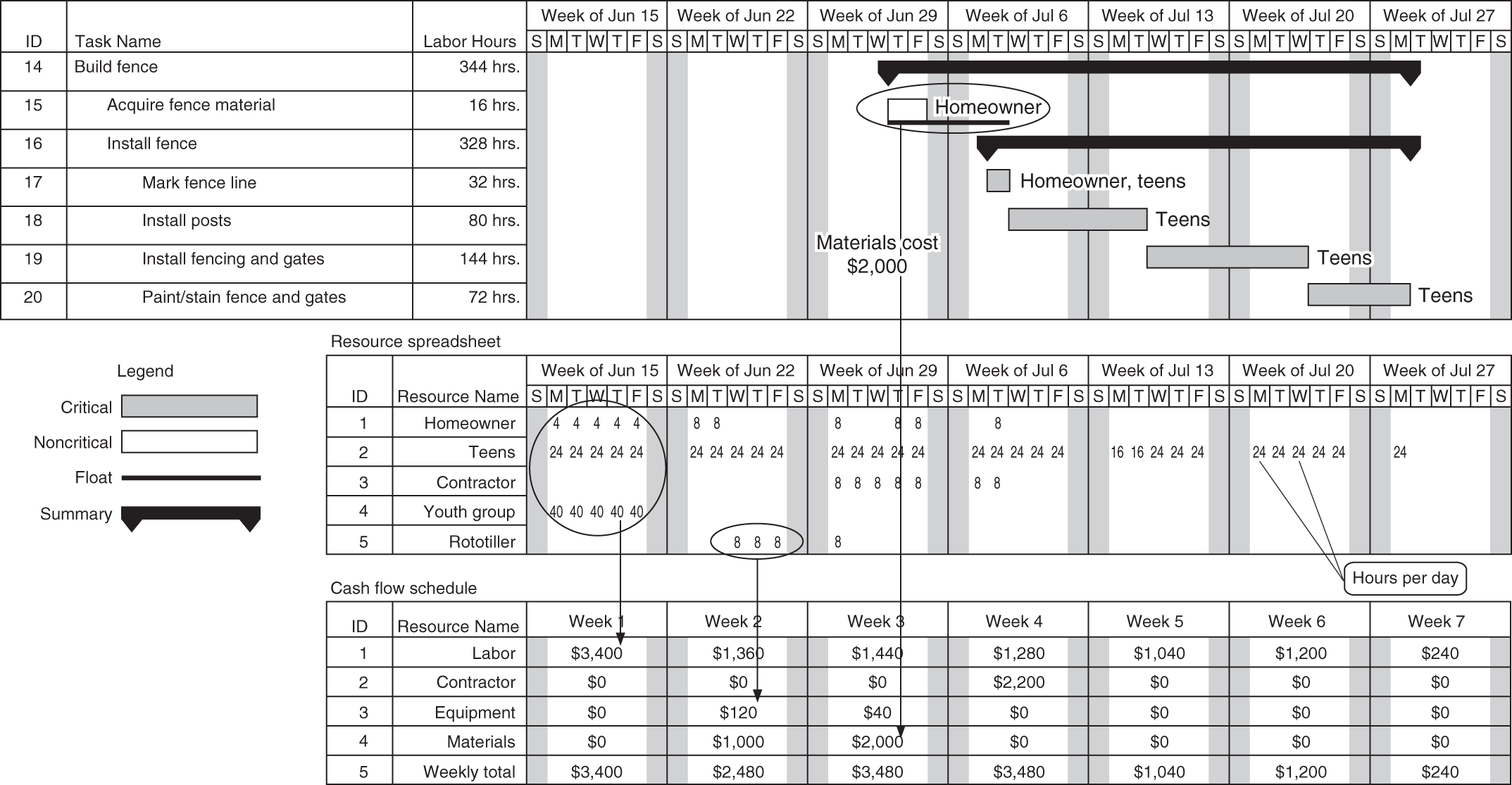

FIGURE 12.6 Calculate a cash flow schedule using the project plan with resource spreadsheet.

Materials Costs

Materials are the “things” that go into a finished product. For some projects, materials represent half or more of the total costs, while for others, materials costs are inconsequential. A software development project, for example, may produce millions of lines of code, but no tangible materials are required. Materials can be raw, such as plywood, concrete, or welding rod, or materials can be subcomponents of your product, such as computer hardware, telephone switches, or air‐conditioning units.

Until now, we've stressed the value of the work breakdown structure as the basis for identifying all costs. When it comes to materials costs, however, the WBS is relegated to second place. The first place to look is the product specification. For example, the blueprint for a building is the basis for calculating how much concrete, plywood, plumbing, or flooring to purchase. It shows the number of sinks, doors, windows, and elevators to order. Similarly, the network design will determine the number of workstations, routers, hosts, and telephone switches required for a computer network.

The work breakdown structure can be used to ensure that every task that requires materials will have them. This is done by planning order and delivery tasks. Include the payment dates as tasks, and you'll have all the information you need to build a cash flow schedule for the project.

GENERATING THE CASH FLOW SCHEDULE

Knowing when money will be spent is almost as important as knowing how much will be spent. Companies that depend on operations to generate the cash to fund projects need to control the rate at which money goes into the project. Let's look at a couple of operations that depend on cash flow schedules:

- A small housing developer plans to build five houses, sell them, and build five more. By keeping his rate of production constant, he intends to keep all of his employees busy at a steady rate. By staggering the starting dates of all the houses, he can move crews from one house to the next and, he hopes, sell house number one before it's time to start house number six. Timing is everything in his plan. If there are too many people on a framing crew, the job will get done too fast and the next house may not have the foundation ready for the crew. If the completed houses don't sell within his planned time frame, he won't be able to fund new houses and will have to lay off workers.

- A municipal engineering department spreads all street maintenance projects across its fiscal year in order to keep its use of people and equipment steady. Large engineering projects that span fiscal years are also carefully timed. The department heads make sure that they spend only the amount of budget allotted per year, but they need to stretch out this budget to the very end of the year so a project doesn't have to stop and wait for the new fiscal year to begin.

Once the project's schedule and costs have been estimated, generating a cash flow projection is pretty simple. Figure 12.6 shows the information from the project schedule that determines the cash flow. It's easy to see how project management software can readily calculate cash flow from all the other data that has been entered.

![]() Calculating a total project budget and cost performance baseline are important topics for the PMP Exam. These are covered in the PMP® Exam Prep bonus video The Project Cost Target, which is found at www.VersatileCompany.com/FastForwardPM.

Calculating a total project budget and cost performance baseline are important topics for the PMP Exam. These are covered in the PMP® Exam Prep bonus video The Project Cost Target, which is found at www.VersatileCompany.com/FastForwardPM.

END POINT

END POINT

Estimating will never be a science that produces results that are 100 percent accurate. In all the estimating techniques presented in this chapter there are consistent lessons:

- It takes time and costs money to develop accurate estimates.

- Every technique gives better results when it is used consistently. The lessons of the past improve the forecasts of the future.

- Comparing actual performance to estimates is essential to refining the estimating model. Without this comparison there is no science in the process, only gut feelings.

Perhaps the most important lesson we can learn about estimating is that all the stakeholders are responsible for accurate estimates. Customers, sponsors, and management, for example, have more control than the project team over factors such as the stability of the specifications, the availability of personnel, and the deadline pressures. A cooperative approach among these stakeholders will yield positive results. When estimating becomes an adversarial game between the project team and the customer, there will always be a loser. On the other hand, if all stakeholders understand the dynamics of estimating and work honestly to reduce the uncertainty of the project, everyone will win.

FAST FOUNDATION IN PROJECT MANAGEMENT

FAST FOUNDATION IN PROJECT MANAGEMENT

A thorough project plan is the foundation of a strong project. Download a Planning Checklist to guide your team and yourself to ensure that you've covered all the bases.

The planning checklist is available for download at www.VersatileCompany.com/FastForwardPM. As you and your colleagues use this checklist, you'll find new items to add, customizing it to better fit your projects.

PMP Exam Prep Questions

- The project manager is creating an estimate for building a warehouse and distribution center. It is a project similar to those he executes about three times a year. He is using the rule of thumb of $100 per square foot to calculate the estimate. What type of estimate is this?

- Parametric

- Analogous

- Gut feel

- Bottom‐up

- The construction team is building a new addition to a distribution warehouse. According to the site manager, a key to success will be to have an extremely accurate estimate of the resource needs for the project, especially because the company is resource constrained. Which type of duration estimating approach is the most accurate?

- Parametric estimating

- Bottom‐up estimating

- Analogous estimating

- Fast tracking

- The management team is calculating the cost range for a project to develop a product that targets an unfamiliar market. What is the key principle that governs the cost range tolerance?

- The less known, the wider the range

- The more known, the wider the range

- The earlier in the project, the narrower the range

- −50 percent to +50 percent

- To ensure that all the project work is considered, the project manager and his team create a bottom‐up estimate. Of the following, which is not an advantage of creating such an estimate?

- The estimate provides team buy‐in since the team is involved in its creation.

- The estimate takes a great amount of time to create.

- The estimate provides supporting detail.

- The estimate has a greater degree of accuracy than other estimates because of the detail.

Answers to these questions can be found at www.VersatileCompany.com/FastForwardPM.