Be advised like the rich and be advised by the right adviser

As I’ve mentioned, the fact that most of us enter our working lives with little or no knowledge of money means we are dependent upon getting advice from others. Although I am a firm believer in being like the rich and learning as much about money as you possibly can (hence, I have produced this book on the subject), I am also a realist and I recognise that to implement some of the structures that are described here, you will require outside assistance. So one of the first processes you may have to go through is choosing an adviser.

Even if you know everything there is to know about the financial world, an adviser may prove useful. In my own advisory firm, when meeting a potential client for the first time, I sometimes say: ‘It is a 24-hour-a-day job to earn the money you earn and to have a life. It is also a 24-hour-a-day job to manage your money to achieve financial freedom and to have a life. Even if you know all that I know, where will you find the time to do the second job?’

The typical answer is probably the one you are thinking of right now: ‘I will not be able to’.

So, as I often said to potential clients who give me this answer: ‘I am applying for the second job.’

How do you pick the right adviser? What tricks can the rich teach you about advisers?

Avoid ‘free’ advice

The first thing to do is to get a list of all fee-based advisers in your area.

But, I hear you ask: ‘Why do I need to pay a fee? Isn’t free advice available?’

Yes, there is much available that purports to be ‘free advice’, but it is not advice! If you are getting ‘free’ advice, then either you are getting that advice from a charitable institution or it is ‘free’ because someone else is paying the adviser. I am unaware of any institution in the financial planning world that operates in a charitable fashion and, therefore, if you are getting (or seek out in the future) ‘free’ advice, then it is probably because someone else is paying.

Do you know the saying, ‘He who pays the piper calls the tune’? The rich know that this is just as applicable to financial advice as it is to anything else. You need to be paying your financial adviser, otherwise he/she may well be playing to someone else’s tune.

For some reason, the selling of financial products and services, for most of us, is not considered selling at all – but, of course, it is! People paid a commission to sell us something, whether it is clothes, computer repairs or financial products, are salespeople; they are not advisers – no matter what their business card says. Just as a shopkeeper will not tell you that you can buy a better product at a lower price in a competitor’s shop, neither will a bank salesperson tell you about a competitor bank’s product, even if the competing product is better.

Those who offer ‘free’ advice are often paid a commission by the financial institutions that they represent. I call this kind of commission-remunerated advice biased and the rich know this too. No matter what your financial circumstances or requirements, salespeople will always try to sell you something – otherwise, they will not get paid. If you are attempting to create financial freedom, biased advice is to be avoided.

Avoid isolated advice

From the list of fee-based financial advisers that you’ve put together, you need to identify one who can deal with all aspects of your finances.

I do not mean that this person must do everything for you, but they must be able to consider your entire financial situation when giving advice. Otherwise, you may suffer the inefficiencies that isolated advice can cause. Your new adviser needs to prove to you that he/she has the knowledge to take any and all of the following into account as his advice is formulated:

- tax (both corporate and personal, covering income and capital taxes)

- investments (both on-shore and off-shore)

- risk evaluation

- mortgages and other loans (personal and corporate)

- retirement schemes (both private and ‘off-the-shelf’ versions)

- pensions

- life and health (all types) insurance

- legal issues

- succession planning and wills

- property (residential, commercial and retail).

It’s important to remember that your new adviser needs to be able to discuss each of these areas with some degree of expertise, simply because these subjects have the potential either to increase or decrease your wealth. I know it may be difficult to find one person with such breadth of knowledge and experience, but it should be easier to find a firm that will satisfy your requirements. So, in looking for an adviser, you should probably be looking for a firm of advisers, and thus you could discount any one-man-bands on the list.

I’m going to emphasise that you need this full range of expertise because I have so often witnessed how isolated advice can be detrimental to the creation of long-term financial security. I am sure that many of you will have heard the saying that my grandmother quoted nearly every day of her life: ‘Look after the pennies and the pounds will look after themselves.’ The problems caused by isolated advice generally affect the ‘pennies’ and, in my experience, many people ignore them because of the relatively small amounts involved. But these small amounts accumulate – and can cost you big-time!

Let’s view it another way. Your attempt to create financial freedom is like attempting to fill a wooden barrel with water. The barrel has a few small leaks, but you are able to get water in much more quickly than it leaks out, and so you succeed in filling the barrel to the brim. Congratulations! You’ve achieved your goal. But as we know, reaching the goal is only one part of the task; once you reach it, you want to maintain it. If you do not fix the leaks, then your water, however slowly, will drain away. And so with your finances – if you do not fix these leaks, no matter how small they are, eventually your assets will drain away. Also, I find that the very act of fixing the ‘small stuff’ in our financial world is extremely educational and means that such inefficiencies are unlikely ever to creep into your world again.

Financial inefficiencies and what to do about them

Let me give you an example of the type of financial inefficiencies that isolationist advice can lead to.

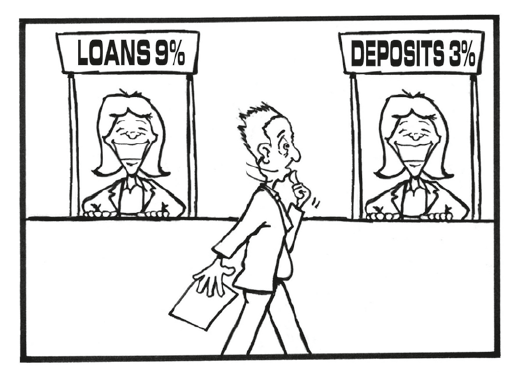

I’m hoping that none of you would be foolish enough to walk into a bank and borrow money at a rate of 9% per annum (that’s the fee they charge you to borrow money), and then cross the foyer and put the borrowed money on deposit at 3% per annum (that’s the fee a bank would pay you to borrow your money). However, if the clients that I advise are typical of the population in general, at least half the people reading this book do exactly that.

The problem is that most people separate these two transactions by time and institution – you make the two decisions at different times and with different advisers (or salespeople perhaps?) – so that you borrow money to buy a car on one date and, several months later, when a bonus comes your way, you tuck it away in a deposit account for a rainy day. The effect is the same: you are paying a higher interest rate on your borrowings than you are receiving on your savings, and you are borrowing your own money and paying for the privilege!

I understand why so many people make this mistake: not every financial decision is part of an integrated plan and time dulls the memory. We make financial decisions on the run, grabbing moments here and there to think about, and take action with, our own money and rarely, if ever, does our last (or second last, or third last …) financial decision impact on the one we are making right now.

However, if you have a good financial adviser in your corner, who knows your financial circumstances inside out and who has the experience and expertise to help in all areas of your financial life, then you will not make these mistakes and financial inefficiencies will not erode your pennies.

Other inefficiencies that could be keeping you from truly starting to generate financial freedom include:

- failing to take advantage of all tax concessions

- earning your income in an inefficient manner

- misunderstanding risk and reward

- taking financial advice from those paid commission to sell you ‘stuff’

- investing only in what you know, without making any attempt to expand your own knowledge

- accepting loan offers that are structured to the lender’s best advantage, rather than your own

- making offshore investments without fully investigating (and thus understanding) all the tax implications

- avoiding the world’s stock markets because you fear them

- over-accumulating assets in your own name and, by so doing, substantially increasing the taxes to be paid by your heirs

- borrowing for consumables

- not borrowing for investments

- failing to make a will and thus leaving the distribution of your assets to the state.

The list of potential inefficiencies could go on and on, but I will not labour the point any more. There is one more item I will add, however:

- failing to make, and to revisit, a plan.

Make a plan

When choosing your financial adviser, you now know that he/she must be fee-based and must demonstrate an ability to add value in all areas of your financial life. This probably leaves you with quite a short list of prospective advisers. I suggest it is time to go meet those remaining.

The first thing that I would insist upon is that any adviser worthy of consideration must mention a plan and explain how they would work with you to achieve that plan.

The main reason for writing this book is to demonstrate to the reader that creating financial freedom is as much about the ‘hows’ (how you act with, and around, your money), as it is about the ‘whats’ (what type of investments you use). The first ‘how’ is how to choose the right adviser. Working to a plan allows both you and the adviser to judge progress easily, simply by asking yourself regularly: ‘How are we doing with regards to our goals?’

Your first meeting with each of your short-listed advisers should cost you little or nothing. As an adviser, I always offered the first consultation for free. After all, I did not know whether I could help someone until I met with them and heard a little about them. If I did not yet know whether I could help, the potential client did not know either and, in such an engagement, I could not justify a fee.

At this first meeting, expect the adviser to give you a broad history of his business and details of the expertise of the firm’s staff. Expect him to ask some probing questions (without yet seeking in-depth and private information), to get a broad picture of your current financial circumstances. Then you should be told what the adviser believes he can do for you and how much you can expect to pay for the first phase. You should not make a decision on the spot, and if the adviser is pushing for an immediate decision, personally I would walk away and cross them off my list.

Remember the following rich trick, and

- Ask for all details discussed at your initial meeting to be confirmed in writing and on the headed paper of the adviser.

- Ask for a copy of the firm’s fee schedule and their terms and conditions of business.

- Ask for client testimonials from people who have already dealt with the adviser, including, if possible, one you can get verbally by contacting the person directly.

- Tell the adviser when they can expect you to make your decision on whether to engage their services. In my opinion, the adviser should be aware you are shopping around.

Once you have visited all of the advisers on your short list and have gathered the relevant information, you are in a position to make your final decision. Probably, there will be one adviser who stands head and shoulders above the rest, so, if you go through the process described, it’s likely that your adviser will have picked himself.