The rich checklist: put it into practice

The first eight chapters of this book have been dedicated to giving you the information you need to manage, invest and protect your money effectively.

The rich deal with their money in a very different manner from the rest of us and I hope that I have impressed upon you the need to change the way you think about and, perhaps even more importantly, act with money if you are going to succeed in your bid for financial freedom. Indeed, this issue is so fundamental that I believe the most important changes you need to make bear repeating.

The checklist

Take a few moments to review the summary list below:

- Recognise financial advisers for what they are. There is no such thing as free professional advice! Those who tell you they are financial advisers but do not charge you a fee are not financial advisers, they are product-sellers. They are people paid on commission to flog you stuff. From time to time, in order to become truly financially free, you will require the assistance of an impartial financial adviser; hire one and pay him a fee. In my experience, a fee-based adviser can deliver value that far outweighs the costs of his services.

- Stop borrowing for consumer goods. The real ‘killers’ in this category are cars and many of you reading this will be paying out a fair chunk of your income each month on a car loan. Remember, every £1,000 you pay out in car repayments costs you about £2,000 in pre-tax income and could be better spent repaying a mortgage of about £163,000 over 20 years (based on a home loan interest rate of 4%).

Although cars are the main culprit, many of you will have borrowed also for furniture, home entertainment systems and holidays. Change the way you do things: repay existing consumer debt as fast as you can and never borrow for such items again. Do as your parents, my parents, did – save for the consumer items you want and buy them with cash. Not only will you appreciate them much more, but they will also be a lot cheaper. - Get rid of credit cards. As with consumer debt, the easy availability of credit is all part of making the rich that much richer and keeping the rest of us that much poorer. Do not fall for it. Do not imagine that you can have the trappings of wealth (the cars, the watches, the clothes, the holidays, etc) before you are wealthy. While it is physically possible to possess the items, possessing them is actually blocking your route to complete financial freedom. Repay those outstanding balances as fast as you can and get yourself a charge card. These offer all the convenience of a cashless transaction but require you to pay off the balance each and every month, thus preventing you from falling into debt.

- Pay attention to how you repay debt. All debt is not bad – indeed, some debt should be repaid over as long a period as possible. Commercial debt, where the interest payments to the bank are fully tax-deductible, should generally be arranged (or renegotiated, if you already have such debt) certainly up to the limits of your retirement allowances. As retirement contributions are also fully tax-deductible, arranging commercial debt in this manner effectively means you can repay the bulk of the debt with tax-free money.

- Consider everything before making a tax-based investment. Far too often, the sellers of such schemes (which include property, equity and capital allowance products) concentrate on the tax-break and people rush to buy. Losing money is even less pleasant than paying tax and often, in such schemes, the investor would have been better off paying the tax and putting the net amount on deposit. Remember, these are investments first and must be acceptable to you as investments before you take the tax benefits into account. The general rule of thumb should be, if you would not invest without the tax-break, you should not invest at all! Finally, never make a tax-based investment until you have used all your available retirement allowances; they are the safest, most predictable, tax savings you can make!

- Turn liabilities into assets. Resolve today to stop thinking of your home as contributing to your wealth – the only people who will benefit from its value are your heirs. Your home produces nothing, but consumes large amounts of your income and is, therefore (as far as financial freedom is concerned), a liability, not an asset. This is true until you start to treat it differently, either resolving to sell it at a later date in order to downsize or using the equity you have in it to raise additional finance for investment in other assets. Becoming financially free is only achievable if, once you create a little wealth, you leverage off the existing assets to create more.

- Change the way you earn your income. If you are a self-employed person, earning your income as a sole trader, resolve immediately to change to a private limited company structure. Yes, this will increase slightly the costs you incur each year to comply with Revenue rules and company law – however, the benefits far outweigh those costs.

If you are an employed person, at least have a conversation with your employer as to whether a private limited company structure would be acceptable. Do not forget there are benefits here for the employer, as they can make substantial savings too. - Ignore retirement allowances at your peril. Many pension plans for sale offer bad value for money and limited scope for real investment returns. However, there are a number of vehicles, collectively known as either self-administered or self-directed pensions, that offer superb value for money and the investment flexibility, including the ability to borrow within the fund, that will lead to the opportunity of substantial real returns.

Remember, investing in these structures allows you to keep more of the money you earn, immediately making you wealthier, and keeps your investment returns free from both income and capital gains tax. In short, the same money, invested in the same assets, achieving the same rates of return, will grow more income-producing assets inside a retirement vehicle. - Always remember (and use) the Golden Rules. Becoming financially free rarely, if ever, happens by accident: you must work at it. Using the two Golden Rules will make your journey to financial freedom that bit easier. The rules are:

- Rule 1: Make money with other people’s money.

- Rule 2: Make your investments before you pay tax.

Properly using Rule 2 means that you keep more of the money you earn (and, where retirement funds are concerned, more of the money you make on your investments) and becoming financially free has little to do with what you earn and everything to do with what you keep!

Now you have the top tips for becoming financially free and for becoming like the rich. Not everyone will be able to implement all tips; however, even implementing one of them will improve your financial well-being.

The plan

Armed with the tools of the rich that will make you financially free, what is your next step? Well, you have to draw up a plan. To be successful, any plan must adhere to the basic rules of planning:

- It must be written down. Without a written plan, all you have is a vague aspiration. Once it is written down, it is a plan and can be revisited from time to time as a reminder of why you are doing what you are doing.

- It must be achievable and it must have a deadline.

The remainder of this chapter is dedicated to helping you commit your plan to paper – a plan that is achievable, albeit with some effort on your part. This plan has five phases, each of which is described in this chapter.

Phase 1: Make sure that the money you spend today is spent as efficiently as possible

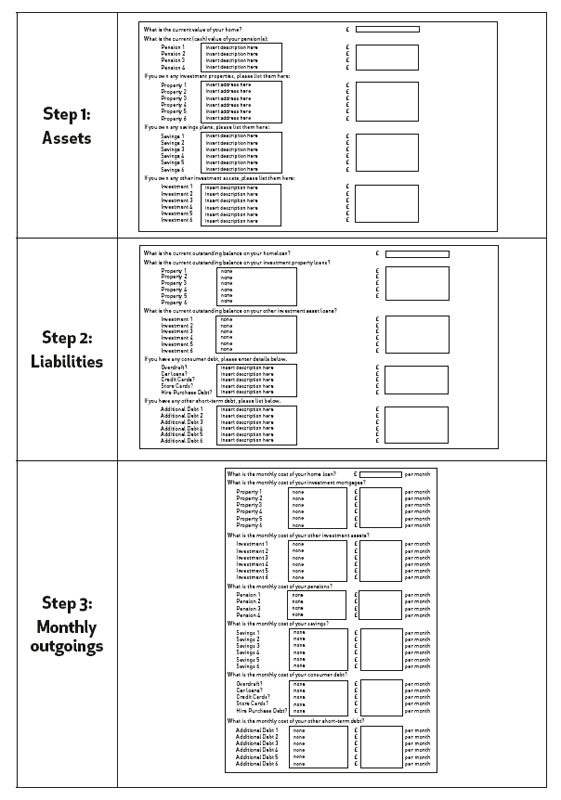

Set aside a morning or afternoon to spend with that shoe box, concertina file or overflowing kitchen drawer – wherever you keep all of your financial papers.

At the back of this book are a number of planning sheets and your first task is to list everything you have. List all of your assets and all of your debts and the annual costs of those debts on the first three sheets.

Once you have completed this task, you need to begin taking the new actions that are going to make you financially free. The place to start is with those consumer debts! You must plan to repay these as quickly as possible. ‘Where will the money come from?’, I hear you yell. This, of course, is where you start to sacrifice. It is most unlikely that any savings accounts you have, for example, are achieving returns in excess of the cost of these loans. So the first thing to do is to stop saving, cash in your chips and use the cash value to pay off the most expensive loan. If you have cash left, repay the second most expensive loan, and so on until your savings are spent. Now, use the money you were paying into the savings to accelerate the monthly repayments on the most expensive of the remaining loans. When that loan is repaid, apply the amount you had been paying to the next most expensive loan and continue to do this until all consumer debt has been repaid.

For some readers, repaying consumer debt will take months; for others, it may take years; but no matter how long it takes, it makes complete financial sense. You cannot invest money without surplus income and these debts are eating your income alive. Many readers will empathise with the situation where all of your income is committed even before you earn it and, in my experience, consumer debt is the major offender.

As you embark on the repayment of expensive debt, there are other things you can do as well. Next, you should concentrate on any commercial loans (typically, loans for a business or to purchase buy-to-let property) and call your lender for an appointment. At the meeting, you will tell your banker (and I mean tell, not ask) that you wish to change your loan(s) to a retirement-backed structure. Depending on your personal allowances, you may be able to alter all loans to this more tax-efficient repayment method, but you should be able to take some advantage at least.

One note of caution here: many of the major lenders either own, or are owned by, a life insurance company and may try to sell you the pension for the retirement-backed structure. Do not fall for this! The pension will be overladen with internal charges, which undermine its ability to perform. In truth, even for the most financially astute, it may be necessary to have a professional to assist you with this element of your financial restructuring. Make sure he is fee-based and agree the fee in advance.

Keep the tricks of the rich in mind: if you already have some form of retirement plan, it may be possible to use it for this restructuring. If not, then ensure your fee-based adviser can handle the retirement scheme too and will do so for a fee (quoted and agreed in advance). Once this restructuring is complete, you will be paying less income tax and, as a result, your loan(s) will be considerably cheaper to service and repay.

Phase 2: Set your financial freedom target

You are now on the road to financial freedom. You are changing the way you think about money and, all-importantly, the way you act with money. You have put some of these changes into action. It is now about time to identify where you are going. Phase 2 of your new plan is to set your target.

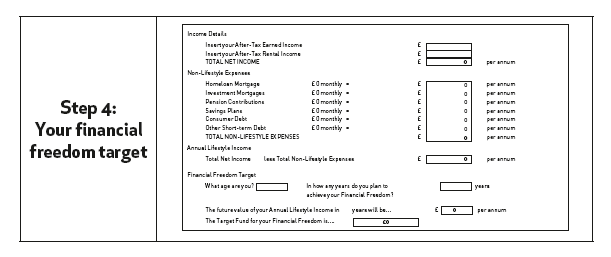

To identify your accurate lifestyle income, you must return to your spreadsheets and complete the final one.

Your lifestyle income is the average monthly amount you spend on light, heat, clothing, holidays, transport, etc. To calculate it, you need to take away from your income the non-lifestyle expenses (the mortgage, the car loan and other consumer debts) as well as the future savings being made (the pension contributions and other savings). The next thing to do is to inflate this figure into the future, to the date when financial freedom can be achieved. (See the future value calculator in Appendix 1 and multiply your current figure by the relevant number. Use the 4.5% per annum multiplier as that assumes that your income will rise at a slightly higher rate than the long-term inflation figure assumed throughout this volume.)

Figure 3 Completing your financial freedom planning sheet 2

Now you have your true lifestyle costs, inflated into the future, and you should turn to the ready reckoner on page 173 to find your financial freedom target. It may be difficult to decide on a period of time within which to achieve financial freedom, so my suggestion is that, at least initially, you start by planning to your 60th birthday – wouldn’t financial freedom make a nice birthday present! – or, if you are already close to or over 60, use a five-year period initially.

So you can now see that your financial freedom target is £___________ (insert your figure here) in ____ (insert the number of years to go here) years’ time.

Now, probably for the first time in your life, you have a specific financial target to meet in a specific timeframe – in other words, you have a plan to achieve financial freedom.

You have completed Phase 2 of your plan. You know exactly how much you need to accumulate in investment assets, over a specific timeframe, so that you can become financially free. Simply knowing this figure gives you a huge advantage over most people; it is a real number and, as high as it might seem, armed with your new-found financial knowledge, you can set about planning how you are going to get there.

You are moving into Phase 3 of your plan.

Phase 3: Calculate how far you have already travelled

Now that you have started to undo the errors of the past and are, for the first time, in possession of your financial freedom target, it is time to judge how much of the journey you have already completed.

Here, you will have to do a little work with your calculator. Set out in Appendix 1 of this book is a table that allows you to estimate the value of your existing financial freedom assets at your financial freedom target date. There are two future growth assumption columns: one that assumes those assets grow at 4.5% per annum, and the other which assumes 6% per annum. You now know that these figures are of little importance unless and until inflation is taken into account. Assuming a long-term inflation rate of 3% per annum, what these growth rates predict is that certain assets you hold will grow at a rate of 1.5% above inflation, while others will increase in value at 3% above inflation. Earlier I referred to this figure as the ‘real yield’, the only figure that is of importance as it expresses the growth above inflation. Do not forget that if you are getting a real yield of less than inflation, you are losing money, not making it, no matter whether the bottom-line value is increasing or not. If you have forgotten this message, please reread the section on risk in Chapter 4.

These are standard future value assumptions that we use in our business, where we use the real yield of 1.5% per annum above inflation to estimate the value of guaranteed investments, such as long-term (3 years+) deposit accounts and government loan stock (gilts/bonds). Typically, we use the 3% per annum real yield assumption for property or equity (stocks and shares) assets.

So, let us assume that you have a long-term cash deposit of £10,000 at present and that your financial planning period is 14 years. What will your deposit be worth in 14 years’ time? Table 4 tells us. You can see that the table tells us to multiply your £10,000 by 1.85, giving an estimated future value of £18,500.

Table 4 Extract from future value calculator*

* The full calculator is shown in Appendix 1.

Now let us assume that you have an investment property valued at £200,000. What will it be worth in 14 years’ time? This time the calculator tells us to use the multiple of 2.26, which gives us an estimated value of £452,000 in 14 years.

Continue down your list of assets, applying the appropriate multiple, and write down these values on a separate sheet. If you have regular savings plans, such as pensions, for example, you will need to write to the company or your adviser – or was he a ‘seller’ rather than an adviser? – and get estimated values at your financial freedom date. Once you get these, input them on your separate sheet. You should now be able to total your future value and compare this to the financial freedom target you calculated in Phase 20.

Any shortfall in your current planning is now obvious, as that shortfall is the difference between the figures you have just calculated and your financial freedom target.

Assuming you have identified a shortfall (most people do!), please fill it in the space below.

Shortfall: £__________

Having identified this shortfall, the first thing you can do is to investigate the possibility of raising further finance on your home: you should be able to raise the mortgage to at least 70% of the value of the house. Get out your calculator and calculate 70% of the value you have placed on your house and take from this figure the existing mortgage amount; now you have the amount of equity release a lender should offer. This figure becomes your 30% deposit on new property purchase.

Example 7

Equity release from your home

| Value of home | £300,000 |

| 70% of home value | £210,000 |

| Current mortgage | £100,000 |

| Equity release potential | £110,000 |

| New property purchase price | £366,650* |

*This is the amount that you could spend on new property investments (including all costs and fees)

I am not for a moment suggesting that getting this type of financial support from a bank is easy, especially now, as the credit crunch bites deepest. What I am drawing your attention to is the potential for the maximisation of your own financial future by using all of your assets to create sustainable financial security. That is one of the greatest tricks of the rich and is often what sets them apart from the rest. Some of the risks may be too high, but please remember there is also a substantial risk in doing nothing. If you cannot bring yourself to apply the tricks of the rich, then what type of financial future awaits? Without independently building your own financial security, you will be dependent on the state, and that is a future few relish.

Back to our example: always assuming a lender will grant you the 70% loan-to-value (LTV) debt, you could spend an additional £366,650 on investment properties. It is time to go and visit your lender, not yet time to try to find a suitable property!

Phase 3 of your plan is now all but complete. The only other matter you need consider is what to do with any surplus income your planning and restructuring has identified. Once again, I have no hesitation in recommending that any surplus should be put to work inside your retirement plan – at least until you have reached your maximum allowances. There is no better way of saving tax and, as long as the charges are not too prohibitive, no better way of building wealth. As suggested earlier, it is time to seek out some professional help and get yourself a private pension fund.

What to do now

Some of you may have even greater surpluses than can be taken care of by retirement allowances. Congratulations first of all – your restructuring has obviously been very successful! Second, you will need other things to do with your money and, hopefully, the previous chapters will have suggested some projects. If you need more help, here are a few tips.

Get yourself on as many mailing lists as you can

There are many, many money-making and tax-saving projects available to the private investor at any given time. Some will be the more ordinary, off-the-shelf, financial products, where you have to be very careful about the charges levied. Others will be more exclusive, and usually better-value, projects, generally promoted by one, or a small number, of the more innovative financial advisory firms.

You need to be aware of as many opportunities as possible, so let people know you are in the market. Contact a number of auctioneers and, having negotiated your finance deal, tell them the type of investment property you are after. Get in touch with some accountancy firms and tell them you are interested in tax-breaks. Call the fee-based financial advisers and tell them of your interests. These firms, which are always keen to win new clients, should have no problem in placing you on their marketing lists, thus substantially improving the number of investment and tax-saving opportunities that come your way.

Read everything you can about money, becoming rich, successful investing, etc

Knowledge is power and the more knowledge you possess, the more powerful, in financial terms at least, you will become.

Nobody is born knowing how to manage money; after all, money is not natural and so our instinct can do nothing for us. Not only this but also, for the most part, formal education teaches us little or nothing about money either. I had a meeting recently with a client who is a prosthodontist, a qualification for which he went through 22 years of formal education. He told me that, in those 22 years, he never received even one class about money and how to manage it – and he believed that was deliberate.

He is not alone. There is a school of thought which suggests that, based on the history of formal education, it is deliberate that most of us are taught very little about money. The modern education system, it seems, has its roots in the Industrial Revolution, when the schools were established with the help of the industrialists. These men were keen to have a more educated workforce, yet were not, it is said, keen to have their employees educated too much – otherwise they would be creating competition for themselves. Thus, the curriculum that was taught, and which, with just a few modern additions, is the curriculum that is still taught, did not teach the employees about money.

While my own knowledge of the history of formal education does not allow me to make a definitive conclusion, this version of its history has more than a ring of truth to me. Back then, just as it remains today, the vast majority of the world’s wealth was controlled by a tiny minority of the population and then, like now, the rich would like to keep it that way.

Whether this interpretation is true or not, the unarguable fact is that most of us, no matter how many years we spend in formal education, leave school knowing little or nothing about money. This means that it is up to us to educate ourselves and this is why I recommend you read everything you can about the subject.

Feel the fear, but do it anyway

The journey to financial freedom is not easy and one of the hardest things you will have to deal with is the voice inside your head which tells you that you cannot do this or that. We all experience it – it causes that feeling in the pit of your stomach, as if an invisible hand had reached in, grabbed your guts, and twisted them a half-turn. This is fear and it has the potential to paralyse us completely.

The first thing I want to assure you is that everyone feels fear – and I mean everyone! So the fact that you feel the fear is neither a flaw in your personality nor is it a barrier to you reaching financial freedom. It is how you deal with the fear that will dictate whether you actually achieve your dreams.

My father’s father was a medic at the Battle of the Somme, one of history’s most infamous battles, where far too many young men lost their lives due to the inadequacies of a small number of old men. You can imagine the fear that my grandfather and the rest of his comrades felt as they waited for the order to go over the top. However, it was the way these men dealt with the fear that made them heroes or cowards, not feeling the fear itself, since the fear was, according to my grandfather, universal.

I read a story recently about two men awaiting the order to go over the top; both had knotted insides; both shuffled from foot to foot, knuckles whitened as they held their rifles tightly. Both men thought of their loved ones back home and each fought back a tear as they admitted to themselves that they might never see them again. Both, quite frankly, were scared out of their minds, and who could blame them?

The order was given and both were helped over the top by the throng of soldiers waiting behind them, bullets immediately whizzing about their heads. One man stayed in control, charged an enemy machine gun and singlehandedly took the enemy position. The other man lost control and collapsed to the ground, tears flowing uncontrollably, paralysed and unable to move.

The first man was a hero and won a medal for his bravery, the second was branded a coward. Both men felt exactly the same emotion. Both were understandably scared. They just dealt with that emotion differently.

And here is the point: everyone feels fear where their money is concerned. You will feel it and it is completely understandable. How you deal with it will dictate your financial future.

Diversify and learn by your mistakes

Different types of investment assets perform at different stages of the economic cycle. Diversifying your investments should mean that, no matter what stage of the economic cycle, some of your investments are doing well.

Everyone knows the saying: ‘Don’t put all your eggs in one basket’. It’s just as relevant in the financial business as it is in any other. Learn about all of the different investment assets – property, stocks and shares, bonds and cash deposits – and invest across the range.

Also, do not expect that every investment you make will be successful. As in all walks of life, you will fail sometimes – although a diversified portfolio of investments means that any failure will have a limited impact on your overall wealth. Failure is not to be feared or frowned upon; it is, in fact, the greatest teacher of all. There is a saying: ‘Success is no teacher’, which is absolutely true. Indeed, it is a human trait that we learn by making mistakes. The problem with money is that making a mistake and losing a few bob tends to mean most people give up. Imagine if you had applied this logic to everything you have learned so far. Imagine if, when learning to ride a bike, you had given up when you had your first fall. You would never have learned to ride a bike. The same is true as you learn to become financially free; if you give up at your first mistake, then you will never get there.

You will make mistakes but, as with the fear discussed in the previous section, it is how you deal with the mistakes that will dictate the final outcome. Also, it is the damage to your overall plan that your errors cause that will impact on your planning process and this is why the broad spread of different investments is suggested. Of course, not everyone will be able to diversify immediately. You simply may not have enough capital to spread around. Do not let this fact stop you from starting your plan, but do pay attention as you progress that plan in the future.

Finally, remember this, if nothing else: the only person who never makes a mistake is the person who never tries!

Phase 4: What happens if ‘the wheels fall off’?

You have made a great start; your plan is in place; you know what your financial freedom target is and you know when it can be achieved. In addition, you have identified the major financial errors of the past and have started to put them right. For the first time in your financial life, you have started to take control and you deserve hearty congratulations for your efforts. Very few people have your financial ambitions and even fewer actually do anything about those ambitions.

You have already seen that an important part of financial planning is identifying the risks being taken. Phase 4 of your plan is about dealing with two of the greatest of these:

- What happens if you die?

- What happens if you get so ill that you cannot work?

Death and long-term disability are the two greatest risks to your long-term financial plan. Income is the lifeblood of financial planning and, without ongoing income, your plan will fail.

Death

If you plan to reach financial freedom, my view is that you should plan to reach it no matter what happens.

For those of you who are unattached, without dependants, the need for death insurance is limited. I believe that the only death cover needed in these circumstances is enough to cover your debts. No matter who might inherit your estate if you were to die prematurely, inheriting debt-free will mean a very easy inheritance. Inheriting assets that still have outstanding debts attaching will require a considerable amount of work, time and expense for the beneficiary. The real problem here is the expenses – it is not uncommon for many unstructured estates to give more value to the lawyers and financial advisers than to the actual beneficiary.

Death insurance to cover loans is relatively inexpensive, although it does pay to shop around. Do not simply accept the quote you are given by the lender. Take that quote to an impartial adviser and see what they can do for you. In most cases, the impartial adviser should be able to lessen the costs, improve the benefits or both.

If you have dependants – a spouse and/or children – you also need to cover all of your debts with death insurance and should follow the advice above. However, you have additional cover to implement.

As I travelled my own route to financial freedom, I wanted to ensure that, if I died before I got there, my wife and family were fast-tracked to financial freedom. If you think about it, Phase 2 of my plan told me what my financial freedom target was, while Phase 3 illustrated for me how far I had already travelled. The death insurance I needed was the gap between the two figures. Not only was the amount of cover needed quite obvious, but I only needed that cover until I reached financial freedom and, in any event, as the years passed by, my need for cover would reduce. As my assets increased in value, the gap between where I was and where I wanted to be would narrow, and so, the wealthier I became, the less death insurance I would need.

So why then did I have whole-of-life insurance that was escalating each year in line with inflation? The answer, of course, is that was what the insurance companies had told me I needed – not surprisingly, the ‘advice’ suited them more than me. Death insurance, (which is sold under the name of ‘life insurance’, as very few would buy it at all if it used its proper name) is mostly sold to us rather than being sought out. Commission (the way insurance salespeople are remunerated) is a percentage of the cost of such insurance; therefore, the higher the cost, the higher the income to the seller. As whole-of-life cover is significantly more expensive than the limited-term version, the income for the salesperson is considerably more.

Having performed the financial calculations of Phases 2 and 3, you know what death insurance you need. It is simply the gap between the financial freedom target and your current net asset value (NAV). While it could be argued that the amount of cover needed is actually somewhat less (since the financial freedom target is a future value and the NAV figure is a current value), it is too complex and beyond the scope of this book to outline how you might calculate annualised inflation discounts. If you use the figure I have suggested you will definitely have adequate cover, and perhaps a little extra that, let’s face it, would not go amiss if the family had just lost a parent and major breadwinner. If, God forbid, you were to die prematurely, your family would receive a major cash payment, immediately making them financially free. They will have problems, of course, after losing their spouse, mother or father, but they will not have financial problems.

Please fill in below the amount of death insurance that you have calculated you need:

Death insurance £__________

and how long until financial freedom:

____ years to financial freedom

This is the amount of life insurance you need and you only need it for the period of years shown.

You can now seek quotations for death cover for this figure over your planning term, making sure that you ask for a ‘convertible term’ policy. The ‘convertible’ element ensures that cover can be extended, without additional medical evidence having to be produced, if for some reason you fail to reach your financial freedom target in the original timeframe.

If you are lucky enough to have death benefit paid for you by your employer, via the company’s superannuation (pension) fund, then keep it – why not, if it is paid for by someone else!

Having calculated the cover required, you may find that you have it already; many of my clients actually have too much cover. No matter what cover is in place, you should now seek quotes, from an impartial agent, for replacement cover on a fixed-term convertible policy. Once you know the price of the new cover, you can decide whether to keep your existing cover or replace it.

Disability

Here I am referring to long-term disability, the kind that can leave you without any ability, or a much-curtailed ability, to earn money in the future. Many readers will have some existing protection in this area, again via your employer’s superannuation scheme. However, such cover is usually quite limited.

I am of the opinion that, in the event of long-term disability, your income should not be affected at all. Most disability benefit schemes (known as ‘permanent health insurance’) only provide a maximum benefit of two-thirds income, less the state disability benefits to which you are entitled. What this means is that, in the event that you suffer a long-term disability, your income is guaranteed to reduce by at least one-third. I say ‘at least’, because such cover generally only applies to basic salary, so any bonus or overtime income is not covered at all.

The only way that you can ensure your complete income is covered is to use a combination of two types of policy: the first being the permanent health insurance (PHI) mentioned already; the second being critical illness cover. PHI pays out an income, while critical illness policies pay out a lump sum.

If you already have some PHI benefits, subtract this figure from your gross income. You have now identified the amount of pre-tax income you would lose in the event of a long-term disability. (If you do not have any PHI benefits, then your total income needs to be covered in some other way.) This shortfall figure needs to be grossed up to an amount that (if you need to make a claim), once invested in a relatively risk-free environment, will replace lost income between the date of disability and your financial freedom target date.

Again, you need to get out the calculator here to calculate the amount of critical illness cover you need – Example 8 shows how you might do this for yourself; one set of calculations illustrates the lower income tax rate, the other the higher rate. All you need do is apply the same maths to your own figures and then you can set about buying the cover.

Note that this method of calculating the cover required is not ideal, as it takes no account of inflation into the future, which will erode your capital. However, without getting into truly complex financial calculations that are beyond the scope of this book, it will give you an excellent level of cover and will protect your income long-term, which is its purpose. For example, if we assume a 3% per annum erosion of capital due to inflation, the lump sums calculated in Example 8 would last for 33+ years, probably well beyond your financial freedom date.

Example 8

Calculating critical illness cover

If you do not have any PHI benefits, then the first thing to do (after you get details of your state benefits) is find out how much of your income can be covered by a personal PHI policy (talk to an independent agent) and, once you know that amount, follow Example 8 to calculate the amount of critical illness cover you require.

A few words of caution here. Firstly, you must realise that PHI benefits are very different from those provided by critical illness cover.

PHI pays a taxable income in the event of a successful claim and may pay that income, rising each year, up to a predetermined ‘retirement’ date (payments are reviewed regularly to ensure claimants are not abusing the system). A successful claim is any medically provable event that keeps you from working, with the claim being paid until either you return to work or you reach your ‘retirement’ date. (Proportionate claims can be made if you are able to return to a job that pays less than your pre-illness empolyment.) Thus, a PHI policy may pay a short-term claim – for example, if you broke both legs and your work requires you to drive – or a long-term claim in the event that your illness or injury keeps you from ever working again.

A critical illness policy, on the other hand, pays a one-off claim, as a tax-free lump sum, should you suffer one of the major illnesses as defined in the policy conditions. Therefore, it is not a policy designed to assist you in the ‘broken legs’ scenario, but only comes into play if you have suffered one of the ‘nasty’ illnesses (heart attack, cancer, stroke, etc). Your finances should be such that your financial freedom plan could survive a short-term drop in income (PHI generally has a ‘deferred period’, during which no income is payable), even if it could not survive a long-term drop. In the event that you are unfortunate enough to suffer long-term disability, you are more than likely to have suffered one of the ‘nasties’ and thus the critical illness plan should pay out exactly when you need it.

Once you have calculated the level of cover you need, look for a quotation. Make sure you choose an impartial financial adviser who has access to all of the product-providers, since this reduces the effort you need to make to get the best price.

Proper insurance cover is not cheap but, in my view, it is absolutely vital as you make your new financial plan. It is certainly one of the tricks of the rich to have enough (but never too much or too expensive) money made available to heirs after death, so that the other assets they built up are unencumbered (without debt attaching) and freely available to those they leave behind. None of these policies will pay out if you do not claim during the term (they will not have any investment element or any potential encashment value), and so could be viewed, especially in hindsight, as a waste of money. However, let me assure you, no widow or widower has ever complained about a waste of money as they receive their spouse’s life insurance cheque. I believe that your plan for financial freedom should not be dependent upon ‘luck’. Certainly, I would never promise my wife and family that we will be financially free as long as I do not die or do not get sick – that is no promise at all.

It is true that the right death and disability cover is expensive and probably will cost more money than you are used to paying for such cover. But remember, from the very start of this book, I challenged you to think differently about money, while also counselling you that, if you are not prepared to change your views, you cannot achieve financial freedom. Ensuring that, no matter what personal disaster strikes, including premature death or long-term disability, you achieve financial freedom for yourself or your family is one of those changes you have to make. The death notices in today’s papers are filled with the names of people who did not believe they would die yesterday. Our hospitals’ accident and emergency rooms today are filled with people who did not believe they would be sick yesterday. The greatest risk to your and your family’s financial future is your health. If, heaven forbid, you are struck down, do not let your financial dreams die (or let your family lose theirs) at the same time.

Phase 5: Review regularly

If there is one prediction one can make confidently about the future, it is that it will be different from today. Change is inevitable and marches on whether we like it or not. As it does so, your financial plan may need to change too.

Your own circumstances will alter: you may be promoted, change jobs, get married, get divorced, have a child (or more children), inherit money, win the lottery, etc. Any one of these changes in your circumstances will mean some knock-on changes to your plans: some will be positive, others negative, but, no matter which, you will have to react.

Outside your personal world, other changes may affect your plans: interest rate rises, currency revaluations, stock market fluctuations, the general economic climate, tax rates, legislative alterations, etc. Again, any one of these has the potential to change your overall plans – and you either react to such changes or you abandon your plan.

Planning your financial freedom is not only about putting things right today, but also ensuring that they remain right throughout the rest of your financial life. The way you used to deal with your money is most comfortable for you (it is only human nature to be attracted to the things we know best) and, unless you are diligent, you could lapse back into the old patterns.

For all of these reasons, it is imperative that you review your plan on a regular basis. At least once a year, sit down with your planning sheets or spreadsheet and fill in the new numbers, which will give you new targets. Each year, review your financial life, always asking whether you are getting the very best value for money.

Always ensure that your product-providers (banks, building societies, insurance companies, fund managers, etc) give you an annual report on the business you have with them and tell them when you want it. Get all of these reports at the same time of the year and sit down and review your plans.

Remember, pay attention to the two Golden Rules: simply applying them where you can will mean that you will become better off than you ever imagined possible.