Over the course of this book, we have drilled into various aspects of blockchains as well as use cases to help us focus on those aspects. In this chapter, we will take a step up and view the array of possibilities of use cases that were executed in various industries for various purposes. As we walk through this journey of use cases and the experience of building and executing some, the reader is required to refer back over the initial chapters to correlate the elements of blockchain and to map the appropriate tools, architectures, consensus, and so on. If a particular use case uses a particular stack, one can always challenge with better protocols and architectures to yield better throughputs and performances.

And as we upskill ourselves and improve our capabilities and our understanding to create, implement, and manage blockchain-based applications, we need to look around and understand the current use cases under implementation. Insight into such active use cases will give us a detailed understanding of the context in which blockchains can be used. Along with this, we will also be looking into some of the active use cases that have been developed for different industries and how Microsoft Azure Blockchain has been transforming the world from transport to trade.

While the preceding description of the chapter may seem daunting and like a lot of work, and make you feel like grabbing a cup of coffee to replenish your mind and energy, it would be fun for you to know that now even coffee and blockchains are related. This comes from Microsoft Azure’s collaboration with Starbucks, one of the world’s leading coffeehouses, and how their efforts have brought in more transparency and experientiality to the entire generation of third-wave coffee drinkers.

Decentralized customer engagement

Decentralized trade finance

Document signing and records management

Distributed entity such as content

Decentralized Customer Engagement

Attracting and engaging customers and giving them the best customer experience is one of the key focus areas of any business, be it a small corner shop or a megastore like Walmart. While this equation has been relevant since the time the traders took to the Silk Route to sell goods from China to the Middle East, the mechanisms and appeal of the customer experience keep changing with economics, market conditions, and customer maturity. We will explore two use cases in depth to understand how blockchains helped these companies stand out when it came to customer experience.

Bill’U: Your Personal ERP

Bill’U is a Singapore-based enterprise blockchain platform focusing on the experience of retail customers to enhance their shopping experience by digitizing shopping receipts and warranty cards.

Bill’U, a.k.a. TechMyBill.com, provides a decentralized peer-to-peer bill-sharing platform. It is an expense ledger of billing documents, such as bills, coupons, vouchers, warranties, user manuals, and so forth—a one-stop-shop solution to managing all billing documents securely. It allows users to create, scan, share, and store documents on the ledger. This cutting-edge platform has two of development tracks: research specific and application specific.

Blockchain research makes the platform a highly secure environment for retailers, customers, and all stakeholders to securely manage all their billing documents. Unlike the conventional options of mail or an online service that brokers user data, Bill’U brings end-to-end encryption and provides complete ownership of user data for all stakeholders involved. This part of the platform does not directly interact with the users in terms of features. However, data being the core asset, the presence of such a mesh of private and public blockchains is extremely crucial in terms of data security and data sensitivity. We shall elaborate the constructs of this in the use case below.

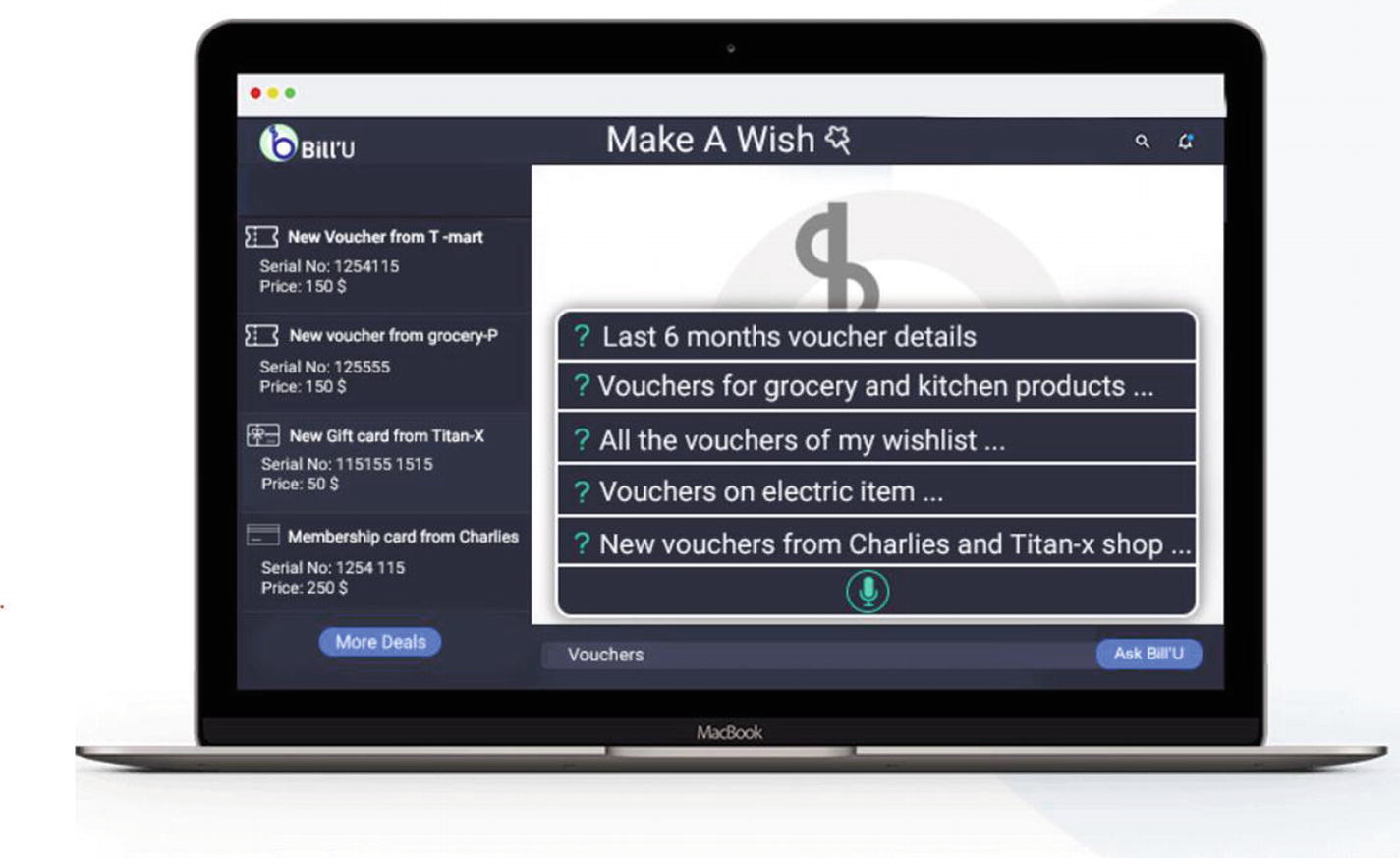

The application side of Bill’U embeds artificial intelligence to make the numbers more human readable and usable. Imagine reminders of your expiring coupons that always go unused or renewal of warranties so as to be covered for any damages. All bill documents on the ledger can be searched intelligently with the “ASK Bill’U” feature. The user can ask questions about grocery costs, monthly travel expenses, or any queries about the uploaded expenses.

The blockchain ledger and the AI-enabled application make Bill’U the next-generation platform for all billing documents.

Every node (over an edge device—mobile, desktop, or a cloud account) uploads bills/scans digital QR Bills that are locally preserved as the first reference. The AI is locally embedded inside each node. Every such node participates in the blockchain ecosystem. The data that is authorized to be shared anonymously flows onto the public blockchain, whereas when a consumer purchases an item from a retailer, the specific information that is confidential is encrypted and shared over the private chain exclusive to the rightful stakeholder.

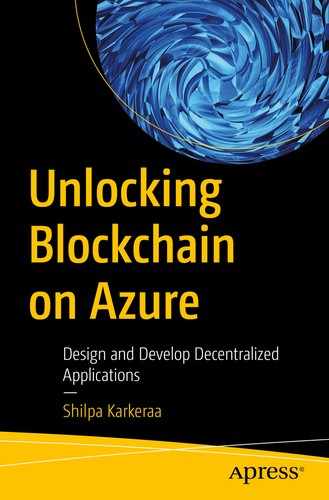

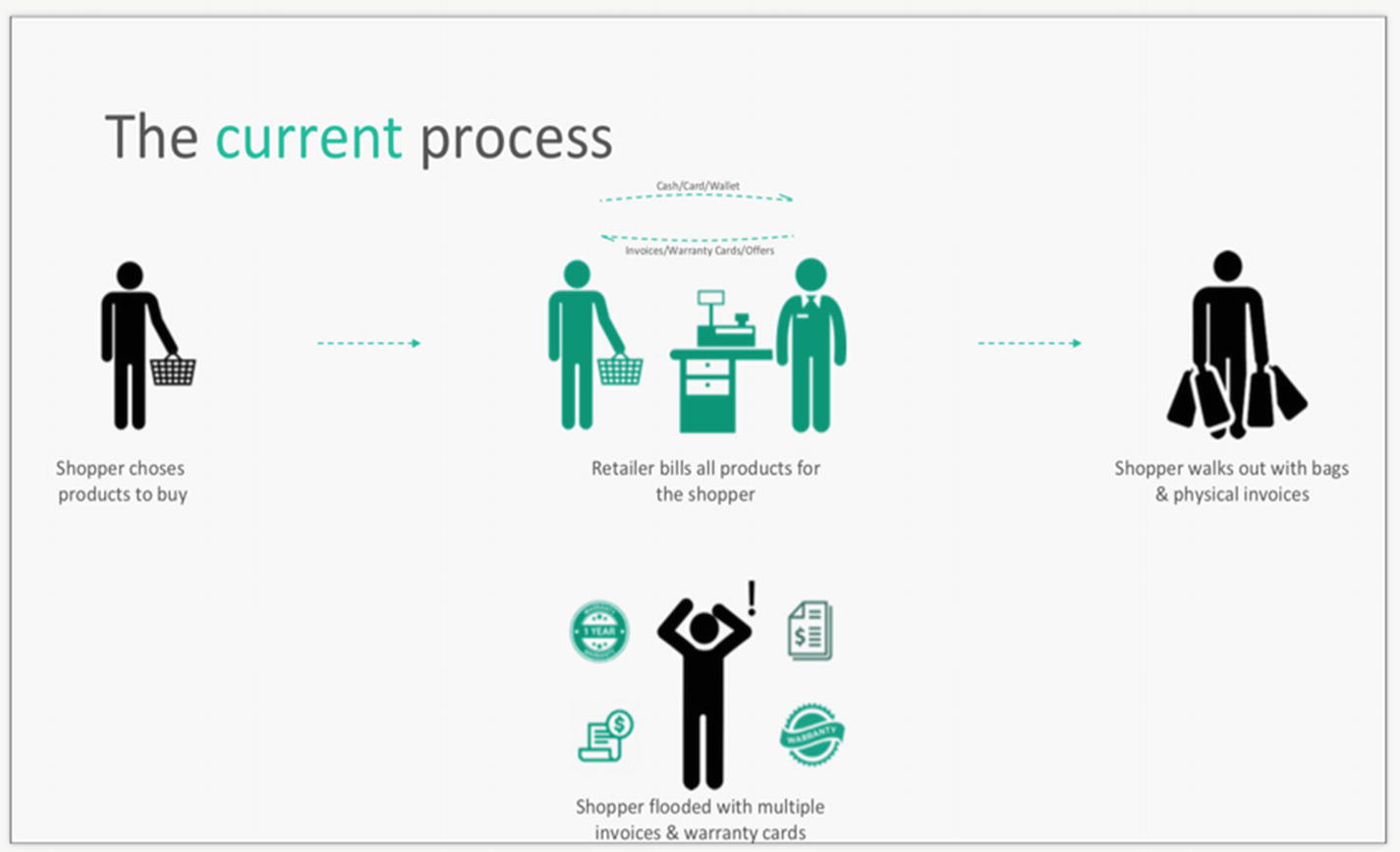

The current offline process of billing for a retail customer

Emphasis on the challenges faced by retail customers and retailers on centralized platforms and offline processes

As we can see, the conventional methods have multiple challenges related to storage, tracking, information capture, and expense management, to name a few for both the retailers as well as the shoppers. In order to overcome these, Bill’U uses a platform based out of AI and blockchains to ensure ease of service and customer data confidentiality.

Customer data confidentiality is one of the prime Unique Selling Points (USPs) of the product, as all of the alternates of this require the customer to furnish their personal information, like name, mobile number, and addresses, which is then used and over-used by retailers and has no clause around confidentiality of the data and further sharing of it.

In such scenarios, the customer ends up getting spammed instead of the information serving its intended purpose. Thus, Bill’U has been powered by a combination of public plus private blockchains that enable retailers to understand their customers’ data and provides them with insights and relevant data, all while masking the personal data of the user. As the personal data is masked but the other relevant data is available on the public chain, the retailer can create custom offers for clients and use insights for the benefit of the clients, all while shielding the client’s personal info, which is stored separately on the private chain of the hybrid blockchain, thus protecting the client’s data and giving them a “wow” retail experience, which helps them take care of all relevant details after shopping.

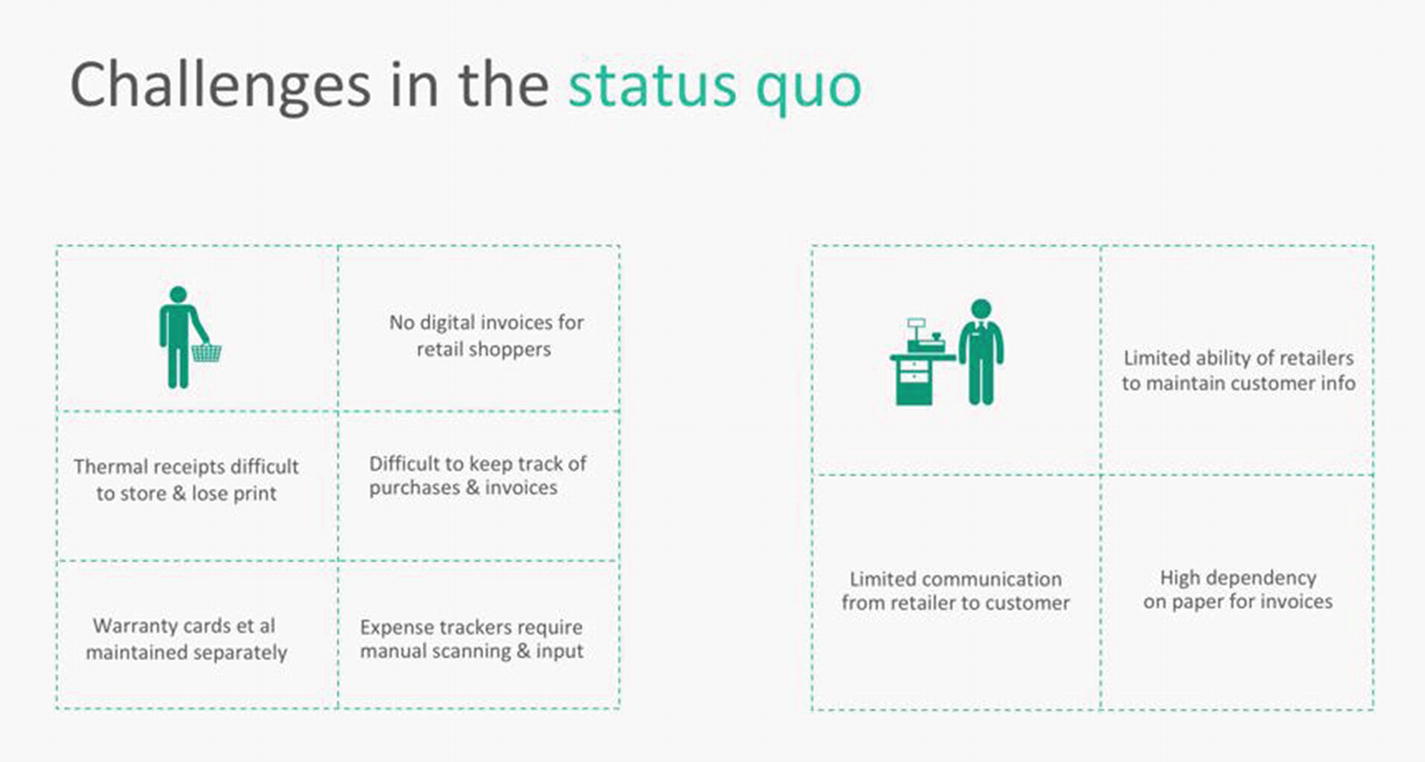

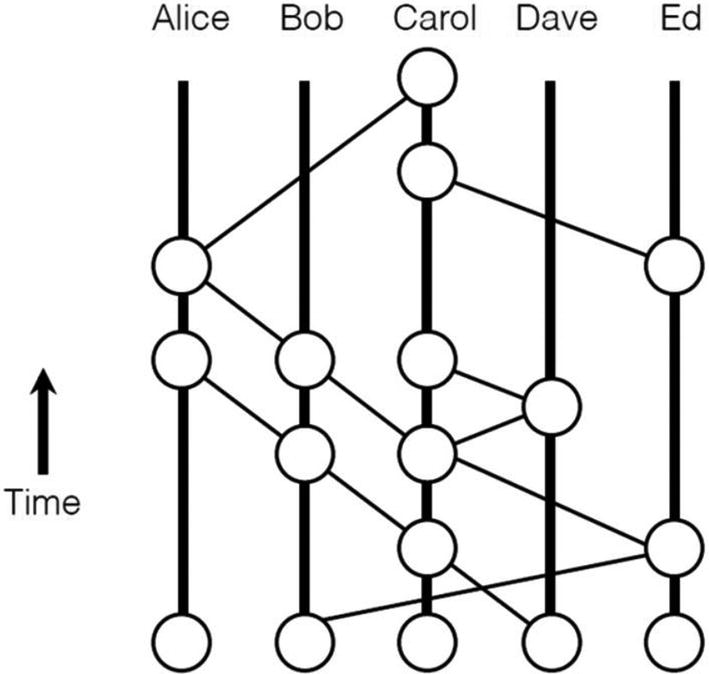

Chain representation based on the transaction between users. Each user in a node has its own AI module to avoid sharing of private data

Every user represents a peer node, whereas Bill’U performs the role of a validator node between billing transactions of documents between two stakeholders in a private chain. In the public chain, all peer nodes can derive trends, consumption demographics, and voucher offers from anonymous data distributed among all nodes. The AI processing of the Bill’U nodes is local to the user, which maintains the privacy of the most confidential documents on Bill’U. This prime feature of data security is rare to find in most AI applications, which compute on a server rather than on a device.

Here, the original data is kept secure as compared to the other AI services. The learnings from the nodes are on the public ledger, which do not expose the original data of users, thereby benefiting all stakeholders with recommended purchase trends and other recommendations with the Ask Bill’U service.

AI services being local to the user, Bill’U services are customer-centric. For example, when you use Ask Bill’U, it answers by learning from your data on your node and analyzing on the device itself. Meanwhile, Alexa or Siri go to some other server, taking all your data, analyze on the company server, and return back results that may or may not be biased.

Bill’U reminds the user about the expiry of warranties and prompts to use vouchers and birthday offers personal to the shopper. At the same time, it allows retailers to share bills wirelessly without any email or phone number dependency.

AI feature of Bill’U known as Make a Wish or Ask Bill’U that answers user’s queries with respect to his bills

This detailed look at the AI capabilities is to understand the role of the blockchain on this platform. When such care is taken toward not exposing any confidential data while delivering AI services, the process of data transfer requires a careful choice of technology. Therefore, we utilize the encryption, decentralization, and transparency of the blockchain platform for the transfer of anonymous data on public blockchains exclusive to the users of the blockchain only, and send the personal transaction data between buyer and seller on the private chain. Any user outside the chain will have to join the ledger to access the public data, and if a user wishes to access a private blockchain, it will require the consensus of the stakeholders of the chain. Also, many times when confidential data is limited to an edge device, there is a risk of losing data due to physical damage, corrupt files, etc. Bill’U provides a private blockchain option for users to back up and replicate the node on another device or a virtual machine, thereby making it fault tolerant, secure, and accessible over the cloud, with distributed security on a private blockchain, where the participating nodes are the sole user accessing it from different devices.

Digital vault for asset documents

Digital locker for purchase documents

Secure, encrypted, backed up personal ERP system

Decentralized AI with global and local learning models

Smart contract alerts for warranty expire, resale terms, etc.

Universal billing format enabling smart contracts for resell, warranty, etc.

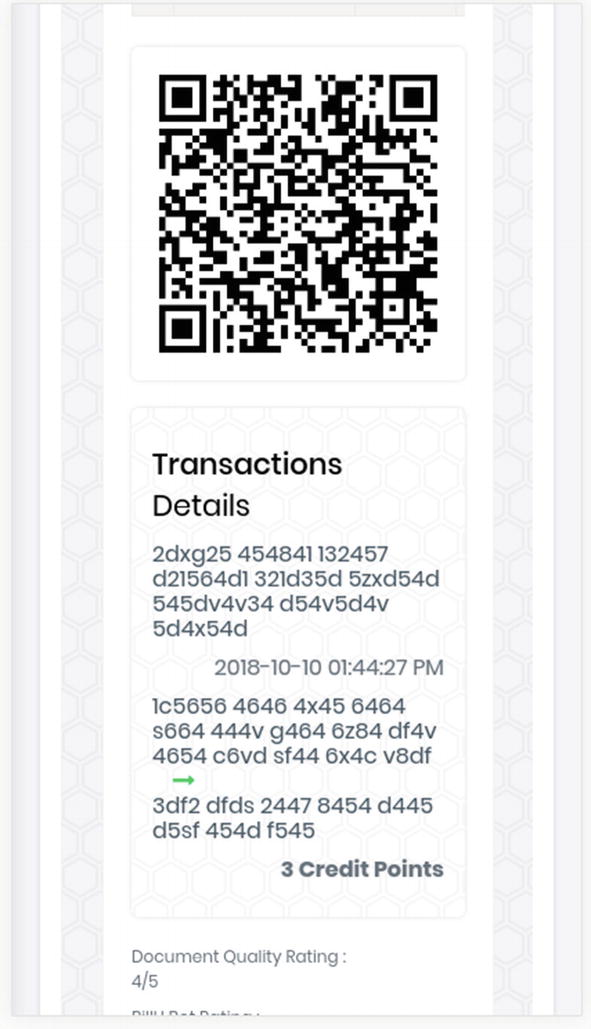

Wireless bill-sharing platform without exposing your email, ID, or phone number (ref Figure 9-5, QR-based bill)

Digitized bill on blockchains

Since this platform is B2B2C, the blockchain architecture will be a hybrid network of public and private permissioned ledgers. The genesis node of Bill’U will be connected to all other retailers in the form of different decentralized networks. Bill’U will be connected to all types of vendors that can scan their bills and upload on the platform, which will digitize all types of receipts collected from the grocery shops, big department stores, medical offices, taxi drivers, even small merchandise, hospitals, restaurants, and movie tickets.

Each asset will be stored on the blockchain, since it is a private permissioned blockchain. Once the new block is updated on the ledger, no one can change the block on the ledger. Each transaction on the blockchain will be immutable.

The end user receives a unique hashed identifier formed with the private key, and only enabled parts of the public data can be viewed with the public key. Using this unique identifier and private key, the end user can access his last expenses and get analytics and recommendations on top of it. However, this personal data remains anonymous with the unique hash ID.

This intermesh of chains with a common genesis, i.e., the Bill’U node, resembles several possible inter-chain architectures. One such architecture is formed by NTU’s COMMENDO, which is a lightweight blockchain that forms the underlying chain of data and data processes.

Being a B2B2C platform, the expansive requirements of such a hybrid chain requires high-speed data transactions as well as scalability in terms of storage.

To enable several asynchronous transactions among various private chains and the flow of public data onto the public blockchain, the blockchain works over Apache Cassandra—a distributed database system. This ensures high availability and high read-write throughput. Bill’U’s blockchain utilizes NTU’s COMMENDO blockchain to allow anonymous transactions with distributed asynchronous worker queues.

Similarly, check out Azure’s CosmosDB as a probable choice for a decentralized distributed database.

Azure CosmosDB is defined as Microsoft's globally distributed, fully decentralized, multi-mastered database service for mission-critical applications. It provides turnkey global distribution with multi-master replication, elastic scaling of throughput and storage worldwide, and single-digit millisecond write and read.

This is a major need of existing blockchains in terms of distributed large-scale storage.

To consider such a platform on an enterprise-grade ecosystem, it is crucial to identify a largely scalable database over a trustless and permissioned network. Consider Bill’U being used across enterprise businesses to store company bills, purchase orders, and so forth. Bill’U could track any changes made to the bills, purchase documents, and contracts. The interchain activities form a mesh of business nodes that form a consortium network.

The consortiums build shared applications on a blockchain to monitor the movement of those assets as they move across organizational trust boundaries and govern state changes with “on chain” logic in permissioned smart contracts. Use cases cover a range of scenarios that are asset- and workflow-centric, from claiming internal bills to tracking external purchase orders and contracts.

With such a secured end-to-end consortium of blockchains, the benefits of offers, vouchers, claims, resell, customer engagement, and customer satisfaction set up beautifully without compromising personal data.

While we see over here a very niche application that has been built with a combination of multiple emerging-tech softwares, let’s look at an example that is closer to a conventional brick-and-mortar setup and has managed to employ blockchains to provide an unparalleled customer experience.

Microsoft Azure and Starbucks

Technology and life have always gone hand in hand. The technologists envision improving life with technology, and the life or the living beings are the ones to shape technology. This symbiotic relationship brings about the confluence of two companies—Microsoft Azure and Starbucks—to blend their experiences to make technology improve human lives.

Starbucks has been experimenting with cutting-edge technologies such as blockchain, AI, and IoT with Microsoft Azure to accelerate productivity, efficiency, and transparency and to provide an experience to the customers that is customized and highly personalized.

Microsoft CEO Satya Nadella at the 2019 Microsoft Build conference presented on how Starbucks is using emerging technologies to deliver its unique customer experience. In order to offer a more personalized experience for customers who visit Starbucks, the coffeehouse chain is using reinforcement learning technology that learns to make decisions in unpredictable environments based upon external feedback.

Customers receive custom-made order recommendations through the reinforcement-learning platform—developed and hosted in Microsoft Azure—which helps them by suggesting things based on local store inventory, popular selections, weather, and time of day, community preferences, and previous orders.

If the demand and supply are in a closed loop, the profitability for the producer definitely increases on understanding the customers’ demands. A cocoa farmer far away from the customer would gain understanding of the scale of growth, the type of cocoa to grow, and the seasonality of the demands. In reality, this information outreach is still not completely achieved. With the Azure Blockchain Services, the vision is to expand the inclusion of stakeholders, from farmers to consumers, in a closed loop.

Conversely, the technology can help boost demand in areas where it was untried before. For example, if there is a group of consumers who are known to like strong Columbian coffee, the recommendation engine for the blockchain public data could boost the recommendation of strong Jamaican coffee to these very users to help boost the demand for such fantastic farm coffee from Jamaica. This reinforcement learning algorithm reduces the chances of recommending unlikeable coffee to consumers on-chain, thereby generating a win-win in terms of outreach for the farmers as well as on the consumer end, as both are supported in terms of sales and experience, respectively.

The primary focus here is to bring greater financial possibilities for coffee farmers and allow the customers to track their coffee back to its source, making it experiential. This is said to be an ideal use case for Ethereum due to its transparent multiple individual nodes that verify transactions. Every involved party can freely track every single transaction made on Ethereum through Etherscan.

Etherscan is a BlockExplorer for the Ethereum Blockchain. A BlockExplorer is basically a search engine that allows users to easily lookup, confirm and validate transactions that have taken place on the Ethereum Blockchain.

Starbucks envisions enhancing the consumer experience so they know the source of their coffee and have a direct understanding of its roots. At the same time, this process increases exposure to markets for the farmers.

For the effort, the coffee chain is working with Microsoft to harness its Azure Blockchain Service in tracking coffee shipments from across the world and bringing “digital, real-time traceability” to its supply chains, according to an announcement from Microsoft.

With the partnership, Microsoft’s blockchain service will record all changes along the journey of the coffee on a shared ledger, providing participants with a “more complete view” of the supply chain.

The app will also inform consumers of how Starbucks is supporting these growers, Microsoft indicated.

Stages of farm to cup for the coffee supply chain

Let us dig in deeper to analyze how the process might be broken down. As readers, one must try to correlate the use case with the technologies learned throughout the book. Remember: we are not reading facts and following them. We are inferring from the use cases to develop our solutions. Given the stage at which the technology is, one can always challenge with newer ways and constructs. So, let us break it down in a similar fashion and infer possibilities of implementations from understanding the use case.

Another important aspect of the use of blockchains is the automated efficiency and productivity they bring. Most of the time, in large enterprises and companies, the information flow of data reaches very late to the top management for effective direction. Even in the largest of the firms, the predictive approach is still not formulated, and digitization exists mainly in structured forms. Thus, Blockchains here enable digitization with credibility due to its immutable style of storage (add-only) & transparency across all processes involved. Thereby enabling the top management to drive data driven decisions based on the state of data/ information across different timelines.

For example, consider a factory that does milling through hulling machinery for coffee. There is a small accident with one of the hulling machines. This issue goes unreported for a day. The next day, the supervisor realizes that the supply generated would be reduced by 1/10 due to the faulty machinery. The report goes to the management after ten days. The information flows down to the sales department sitting in another country on the fifteenth day. The customer on the end does not receive the order and cancels the order or charges a late fee.

This shows the impact of having transparency of data and unmonitored productivity rates. Now, for a company like Starbucks, with more than 30,000 stores worldwide serving 100 million customers a week, staying profitable irrespective of the seasonality, calamities, loss of productivity, and so on is of huge importance. At the same time, they don’t want to reduce any experiential facilities for end customers.

Hardware-based root of trust: The device must have a unique, unforgeable identity that is inseparable from the hardware.

Small, trusted computing base: Most of the device’s software should be outside a small, trusted computing base, reducing the attack surface for security resources such as private keys.

Defense in depth: Multiple layers of defense mean that even if one layer of security is breached, the device is still protected.

Compartmentalization: Hardware-enforced barriers between software components prevent a breach in one from propagating to others.

Certificate-based authentication: The device uses signed certificates to prove device identity and authenticity.

Renewable security: Updated software is installed automatically, and devices that enter risky states are always brought into a secure state.

Failure reporting: All device failures, which could be evidence of attacks, are reported to the manufacturer.

An illustration of nodes that are IoT edge devices updating data to the blockchain

The confluence of predictive models that run locally on these intelligent edge devices at every stage of coffee manufacturing so as to run the recommendation engine for the consumer makes it a complete closed loop supply chain, thus enhancing experiences for all involved. Having all of this connected on a blockchain makes traceability and accessibility highly transparent to the management of the company so they can make pro-active decisions in favor of most stakeholders. Decentralization here provides a promise to reduce losses and envisions opening up new avenues with its means of providing transparency and accessibility to farmers, customers, and business owners alike.

Last month, the Indian Commerce Ministry launched a blockchain-based coffee e-marketplace app that conducts transparent coffee trade in the country. The app is believed to bring a positive transformation among consumers who look for real Indian coffee, as well as for the grower who is paid fairly for the coffee produced.

Similarly, several economies are now gearing up to boost the efficiency of their supply chain with the confluence of AI, IOT, and blockchains, making it end-to-end digitized, tangible, and provable.

Other Industries

The dairy industry, for which it is highly crucial to have transparency in terms of temperature control, shelf life of the product, conditions of transport and storage, etc.

- The health industry, where diet regimes have been a crazy fad across the social media. Many of us attempt to start and try various regimes without complete knowledge of our own bodies and the historical evidence of the diet. All that we have is a couple of internet searches and blogs telling us what to do. Visiting a dietician would surely be a credible source, as the time invested by the professional to understand your eating habits, regional differences, cultural impact, and medical history definitely would help.

- a.

Here, technology could assist the accessibility of such a professional.

- b.

Validate the data in terms of results on-chain with body monitors.

- c.

IoT devices that update weight parameters on blockchain and trace the impact of various diet regimes.

- a.

However, how many of us would want to share our weight online at first? How is the privacy of an individual secured with technology to help us in certain ways? This is the difference between using a blockchain over a centralized internet platform. In the blockchain, which is decentralized, the authority distributed to the stakeholders regulates the activities of the chain in such a way that any activity might require the consensus of the entire chain. On an internet platform that is hosted by one single party, that party might have full authority to misuse your data and gain profits.

Therefore, a blockchain might be appropriate for such a use case, with IoT that connects people to validated dieticians, maintains anonymous shared blockchain data to trace the success rates of users, and incentivizes the customers rather than one company itself.

Decentralized Trade Finance

One of the most common and foremost use cases of blockchains came out of the challenges faced in the conventional operation of trade finance; a more direct case is the international trade finance, where changes in banks, banking regulations, and international trade laws create processes that cause it to take days for transactions to be closed.

Another challenge that comes up in such scenarios is the lack of transparency in terms of transfer of payments and the goods/services that have been provided in exchange and the sheer dependence on banks for the transaction (in most cases the bank of the other party may not even operate in your home country to offer assistance).

Error-prone manual processes for creating, validating, and auditing trade data and documentation

Siloed data that is difficult to verify, leading to multiple versions of the truth and major fraud, compliance, and audit risks

Disconnected legacy systems that limit new business opportunities and make it difficult for small and medium-sized businesses to gain access to financing alternatives

Therefore, as we have studied the impact on customer experiences of the refining of supply-chain procedures with blockchain technology in the last section, let us deep dive into the trade finance processes that impact life, trade., and our finances in this section.

Microsoft Azure and Banks

Microsoft News mentions that more than 80 percent of the world’s largest banks are Azure customers.

To help solve the pain points mentioned under the “Decentralized Trade Finance” section, blockchains have been introduced and experimented with, and now are finally coming into mainstream use. Major players like Bank of America Merrill Lynch now called BofA Securities are taking the lead with Azure blockchains to create an ecosystem for trade finance that will be more transparent, and that too, as early as 2016, speaks volumes about the belief of the industry in the potential of blockchains. Banks like HSBC and ING Bank have followed suit, and the same phenomena is becoming popular across all financial institutions today.

To understand trade finance and the integration of blockchains better, let’s look into the Bank Of America Merrill Lynch case in depth.

Microsoft and Bank of America Merrill Lynch announced a collaboration to use blockchain technology to fuel the transformation of trade finance transactions as early as 2016.

As part of this collaboration, the two companies decided to build and test technology, create frameworks, and establish best practices for blockchain-powered exchanges between businesses and their customers and banks. Microsoft Treasury experts served as the advisors and initial test clients, establishing the first Microsoft Azure–powered blockchain transaction between a major corporate treasury and a financial institution.

As we all know, when digitization started, there were many ERP systems that came into existence. With such software, the banks started increasing data entry to such systems, making it highly inefficient for people to support such a task, where the credibility of the data lay in the hands of the data-entry personnel. Not just in the banks, but all parts of trade finance—the importer, the exporter, the banks, the customs people, and other stakeholders—all had to fill in various kinds of paper and digital forms. This was highly manual, time consuming, and many times faulty. These systems used to store such data in plain-text, as most of them at the early stage of that technology were focused on simply aggregating data. However, the tamper-proof methods of storing such data were missing.

With blockchains, processes can be digitized and automated, transaction settlement times shortened, and business logic applied to related data, creating a host of potential benefits for businesses and financial institutions, including more predictable working capital, reduced counterparty risk, improved operational efficiency, and enhanced audit transparency, among other benefits, in a closed-loop network of anonymous transactions.

With this, blockchains open the door for streamlined trade finance, enabling participants to exchange data easily and track assets in real time. Microsoft is leveraging Corda, an enterprise-grade ledger that enables banks to limit who sees what information and selectively share data with only relevant parties. The solution involves blockchain technology paired with Azure and APIs, and could be used in the future to involve technologies like AI, machine learning, IoT, and more.

Upon using blockchains for the processing of letters of credit, the turnaround time for issuing an SBLC was reduced to three to five days from the earlier benchmark of three to five weeks! Similarly, the transaction settlement time for overseas transactions was reduced drastically after automating conditions on smart contracts. Once the conditions are fulfilled, the transactions are settled immediately.

With the blockchain encapsulating the challenge with validator nodes that actively validate the transaction, the settlement is made clear a lot faster. However, in the absence of a blockchain, the transfer of data requests for clearance are dependent on non-standardized processes, scattered systems, and so forth.

Microsoft further partnered with JP Morgan Bank to promote the Blockchain Service on Azure with the Quorum Blockchain. It enables the setup with a couple of clicks over Azure, integrating the Active Directory, event registers, and Visual Studio to write contracts and so forth. It applies all policies of the consortium defined by the Quorum Blockchain.

“In a rapidly globalizing digital world, business processes touch multiple organizations and great sums are spent managing workflows that cross trust boundaries. As digital transformation expands beyond the walls of one company and into processes shared with suppliers, partners, and customers, the importance of trust grows with it. Microsoft’s goal is to help companies thrive in this new era of secure multi-party computation by delivering open, scalable platforms, and services that any company from game publishers and grain processors, to payments ISVs and global shippers can use to digitally transform the processes they share with others,” explained Mark Russinovich, Chief Technology Officer, Microsoft Azure.

Other Financial Industries

Decentralized KYC (Know Your Customer) and credit data validation

Reduced risk of fraud and lower compliance costs

New avenues of financing and tracing trade activities

As readers, one must question how the application is broken down into the real-life implementations. As we saw in the last chapter, the architecture for letters of credit involved an overseas trade activity.

Similarly, for these application use cases, let us speculate on the suitable tools, consensuses, and outcomes.

Decentralized KYC and Credit Data Validation

National and international governance bodies, such as the government, have been trying to standardize identity with the use of passports, biometric inclusions, Social Security numbers, and so forth. However, for financial institutions, the proof or onboarding of identity is usually a submission of non-standardized documents due to the diversity of cases of various individuals. Another dynamic to this situation is that during name changes or transfer of location, a lack of documents can cause great inconvenience to both parties—the financial institutions as well as the customer.

Here, the stakeholders of KYC are the prime customers and the businesses such as financial institutions that may transact with the customer. For any financial transaction, being it a bank account transaction, credit card transaction, deposits, or Mutual Funds (MFs), the bank needs to know the customer. This trust is established through the submission of authorized governmental documents or by referrals in some cases. However, the regulatory bodies that govern the safety of the financial economy require banks to spend time on regulation checks over KYC to avoid money laundering. Therefore, there is an increase in background checks, certificate authorization, and so on. Now imagine this check occurring on a blockchain network rather than in an offline process. In an offline process, a customer’s data has to be passed from one party to another in a manner that is non-transparent to the end customer. This increases the risk of leak of confidential data, and at the same time such documents could be forged in known ways, making it difficult to trace such fraud. In the coming sections, we shall see how proof of identity is transformed on a blockchain, which could enhance KYC for trade finance, thereby improving internal processes to gain LoCs and bank guarantees.

Reduced Risk of Fraud and Lower Compliance Costs

Imagine a fully connected trade finance network in a particular location. All trade activities are digitized onto a blockchain, with every known entity on-chain. No off-chain activities are allowed to cross the borders without an update on this chain. In such an ideal case, the flow of transactions is tracked anonymously. However, in case of fraud within such a network where cash is laundered, the repeated illegal activity could be identified. Similarly, when any trade entity attempts to bypass the conventional methods of trade by finding a loophole, the chain records could identify such an outlier case. This makes it easier for regulatory bodies to enforce Anti Money Laundering (AML) and avoid a disbalance of the economy.

In the interest of forming a Global Trade Connectivity Network (GTCN), Hong Kong and Singapore’s regulatory bodies—Hong Kong Monetary Authority (HKMA) and Monetary Authority of Singapore (MAS)—along with twenty banks collectively initiated digitization of trade flows for cross-border trade finance activities. Several other decentralized initiatives, with different banks forming consortiums, are We.Trade, Voltron, Trade Information Network, Marco Polo, BankChain, and more. All efforts are toward making data paperless and processes transparent and secure. From a technology standpoint, the pilot phases of several of these initiatives are still struggling with the choice of technology—whether to choose an enterprise close-sourced blockchain platform or an open-sourced blockchain platform. If one attempts to go enterprise, would the trust of the source code hosting the blockchain be blindly trusted by other stakeholders? Wouldn’t an open-sourced hard fork of the platform version be more openly accepted? Does it allow interoperability and encourage more and more stakeholders to join such an ecosystem? Is the current task force ready to integrate the existing systems with such cutting-edge technology? These are the questions that are yet to be tried, tested, and explored for an entirely decentralized system.

As technologists, we could contribute logic apps for smart contracts, create effective node systems that connect on interchain networks, and educate our task force on adaptability to such open, decentralized platforms. As major financial institutions are invested in opening cross-border relations and policies, proofs of concept developed for any of these use cases would definitely gain traction if they genuinely solved a pain point. For example, one could create a fraud-detection tool that reviews anonymous data on the blockchain network and alerts the chain in case of any piggybacking of cash flow over an invalid trade. Such a tool could be included among the validator nodes. Similarly, auto checks of a smart contract could checklist the compliance of all documents required to conduct trade.

New Avenues of Financing and Tracing Trade Activities

With the advent of cryptocurrencies, many forms of tokenomics came into existence. Several retailers started accepting such modes of payment. Micro-lending and financing through such schemes became a possibility. However, due to the lack of regulation, the credibility of the tokens was many times not within the framework of a country. However, Bitcoin and Ethereum have managed to gain a lot of traction since Bitcoin’s inception. With the micro-quantification of efforts and processes, incentivizing on-chain definitely provides advantages to the stakeholders.

Looking at another example that has been better enabled by blockchains, we will examine a leading organization that is a marketplace for the procurement of materials across the supply chain at the best prices across global markets. Ninety percent of world trade happens via the international shipping industry. Let us deep dive into the procurement cycles of the industry and how it is impacted by blockchain technology.

The Maritime Industry: Insurance, Procurement, and Trade

Let’s look at one of the oldest industries, one that has existed from the time of the silk route—the maritime industry.

Marine insurance

Maritime marketplace

Marine Insurance

In 2017, one of The Big Four consultancies - EY along with Guardtime, a software security company announced the world’s first blockchain platform for the field of marine insurance. The development and launch of this platform was a collaborative effort with A.P. Møller-Maersk A/S, ACORD, Microsoft, MS Amlin, Willis Towers Watson, and XL Catlin. The partners coming together for this went ahead with the move after a rigorous twenty-week POC.

The platform for this has been built on the Microsoft Azure global cloud technology and was the first of its kind in the insurance industry, and the phased rollout intends to cover end-to-end use across the marine industry.

The platform, based on a global platform, connects maritime clients, insurance brokers, insurance companies, and third parties to distributed common ledgers that help with the acquisition of data about identity, risk factors, and exposures. The same then integrates this information with insurance contracts. The platform can create and maintain asset data from multiple parties to link data to policy contracts; to receive and act upon information that results in a pricing or a business process change; to connect client assets, transactions, and payments; and to capture and validate up-to-date first notification or loss data.

Blockchain’s potential to transform the insurance ecosystem has always been clear. What we have done is to move forward from potential to reality. This solution is the first to apply blockchain’s transparency, security and standardization to marine insurance and is ready for commercial use. We look forward to deploying this technology across the marine insurance industry and are exploring how these findings and insights will be applied to other specialty insurance markets and beyond.

The platform deployed across the entire ecosystem of the marine insurance industry was built with the vision of addressing the challenges of its complex systems, which involve multiple parties, rules, duplication, and a lack of digital capture of data, along with issues with significant levels of reconciliation. The issues until then were causing problems with transparent access to data, linkage of data to the rest of the chain, and accuracy in underwriting risk by the insurance companies and the sharpening of their model with respect to the preceding issues.

It is a priority for us to leverage technology to streamline and automate our interaction with the insurance market. Insurance transactions are currently far too tedious and frictional. The distance between risk and capital is simply too far. Blockchain technology has the potential to facilitate the desired development that is long overdue.

Insurers can use this blockchain platform to improve their capital and gain efficiencies, with increased transparency and reduced manual data entry or reconciliation and administration costs. The platform has been built over the Keyless Signature Infrastructure, also known as the KSI platform.

Not just maritime, but all of the insurance industry can benefit from blockchain technology, as it has the potential to bring in transparency, remove time-taking activities, and reduce the cost at the same time. The entire series of benefits make risk assessment sharper and more in real time.

Microsoft believes blockchain is a transformational technology with the ability to significantly reduce the friction of doing business, especially streamlining business processes shared across multiple organizations. Marine insurance is a prime example of a complex business process that can be optimized with blockchain. We remain committed to bringing blockchain to the enterprise, and are glad to work with EY, Guardtime and other industry experts to develop and deploy blockchain solutions powered by Microsoft Azure.

As of now, blockchains are finding more and more use cases in the banking and financial services space owing to the ownership and transparency brought in by this technology. The initial example of trade finance has been picked up well, and now even lending, along with the insurance sector, is exploring the potential of blockchains.

Maritime Marketplace

Exploring another use case, one a little more on the technical side as we will explain the buildup of infrastructure and the flow of sequences, let’s discuss the case of a marketplace for the maritime industry.

Like any other online marketplace that has completely changed our shopping habits, consumer behavior, and patterns involving spending money, the maritime marketplace has seen changes, but within the context and constraints of the ecosystem.

Unlike traditional blockchains, where all stakeholders are part of every transaction or validation on public ledgers, a hybrid chain of private and public ledgers would be suitable to run a maritime marketplace. On such a platform, one could purchase goods overseas, such as machinery, metals, chemicals, container ships, oil and gas, maintenance parts, and so on.

Decentralized ledger technology maintains the proof of transaction and traces the credibility of doing business and trade on-chain. Complying with the best trade practices on-chain enables high credit ratings due to on-time deliveries, timely fulfillment, and proper procurement procedures. Stakeholders may gain access to credit guarantees from banks involved in the trade finance of such an ecosystem.

The architecture was designed in such a way that all customers/users of the ledger reside on the public chain (public to the company and its approved stakeholders only) to avail themselves of general listing information. The transactions between relevant stakeholders are conducted in a private chain.

The public ledger consensus works on Byzantine Fault Tolerance (BFT), whereas the private ledger is governed by the delegated proof of stake, where the initiator/block producers have a high stake through delegation and can share adequate stakes with other stakeholders of the transaction to conduct the business contract.

The contract state is stored on the private ledger, and the transaction directive is done through DAG (directed acyclic graph). This ensures that the transaction is super-fast and the storage is decentralized securely between only the relevant stakeholders.

Transactions on-chain: side chains

PROCESS | BLOCKCHAIN FEATURES |

|---|---|

Foundation | • Hybrid chain—role based • Azure-based environments for fast deployments • BFT for public blockchains and PoS for private blockchains |

Availability Check | • Ledger integration with POS • Decentralized ingestion of data • Validators and copy check • Distributed availability checker • Real-time, private chain creation based on availability and suitability |

Order Process | • Smart contract generation • Transaction conditions based on contract status • Event registers for contract status • Smart contract trigger events • System alerts for smart contract stakeholders |

Delivery Process | • Proof of work by document upload • Validators for confirmation • Auto-notification alert • MOSCORD auto checker by BFT • PO proof on immutable ledger |

Invoice Process | • Platform invoice generator integration with smart contracts • Term translation and actions • Maintain copy on private ledger • Maintain validators |

Payment Process | • ETH which is Ethereum’s native currency transaction/Hyperledger native currency value set up • Real-time financial transaction on private chain |

Such a decentralized platform could enable a decentralized marketplace, where the policies are governed by the consensus of the validating stakeholders. The flow of onboarding stakeholders to the platform would be to add the aggregators of suppliers and their product offerings. The platform would enable direct peer-to-peer trade and also allow network-based trade, where the network regulates and validates the smart contract. This would enforce close control of fraudulent activities and reduce defaults. To design the smallest pilot, one should consider a private chain of one buyer and two suppliers, along with the set of regulatory nodes participating in the trade. Here, the block of data would be for the purchase of machinery parts, power tools, and safety items that are crucial for delivery. The trade deal on-chain would be initiated by a smart contract. If all on-chain activities fulfilled the conditions of the smart contract, it would quickly facilitate the payments. In the case of an incorrect supply delivery, the conditions of the smart contract would not trigger, and it would require the alternate clause of the smart contract to be executed. As developers of smart contracts, one must ensure all cases are covered. As solution architects, we must ensure the platform does not have any loopholes, and as business developers, defining such use cases is most crucial.

The patterns of fulfilling or defaulting on such smart contracts generate the credit risk valuation of the stakeholders, thereby allowing a fair valuation via a predictive approach that helps banks provide correct letters of credit and bank guarantees. This helps to reduce trade losses as well as fraudulent activities.

Document Signing and Record Management

Do you remember the last time you went to a bank? The foot traffic in bank branches has been reduced drastically with digitization.

Banks have come a long way since the time when there were only tellers, which were then replaced or re-allocated when the automated teller or the ATM came in, and now we have digital banks, which rest in our pockets in the form of applications and websites. Any transaction, irrespective of its value or volume, goes through with the same velocity and requires absolutely no paperwork.

One of the core things that enabled this, along with the technology, is the fact that people trust the tap of a button to handle their money as much as they earlier trusted a piece of paper. It’s this trust—along with the plethora of benefits of digitization—that drove millions across the world, from a street vendor in India to a multi-billion-dollar fund manager in the United States, to move their banking online over a period of a few years.

Taking the premise of trust and digitization, let’s look into another use case for blockchains, this time in the field of document signing and record management.

We are all aware of global processes like KYC (commonly known as Know Your Customer) or the on-boarding procedures at jobs that require us to furnish proof related to our identity or documents related to our education certificates, respectively. In all such processes, we are required to submit our digital documents—or physical ones, in some cases, even today. While it is understood that some of these cases might take a lot of time even after deploying AI-based parsers, the process of validation of documents is still fairly manual and time consuming, and this is not even the primary concern.

The major concern with using documents to ascertain the identity of a person or something like a college degree is that it is highly personal and prone to misuse, as in the case of a security breach. The recent case of Cambridge Analytica opened up to the world the extent to which data can be used and the impact it can have. Thus, it is imperative to have a solution for this that keeps trust, transparency, and security in the forefront.

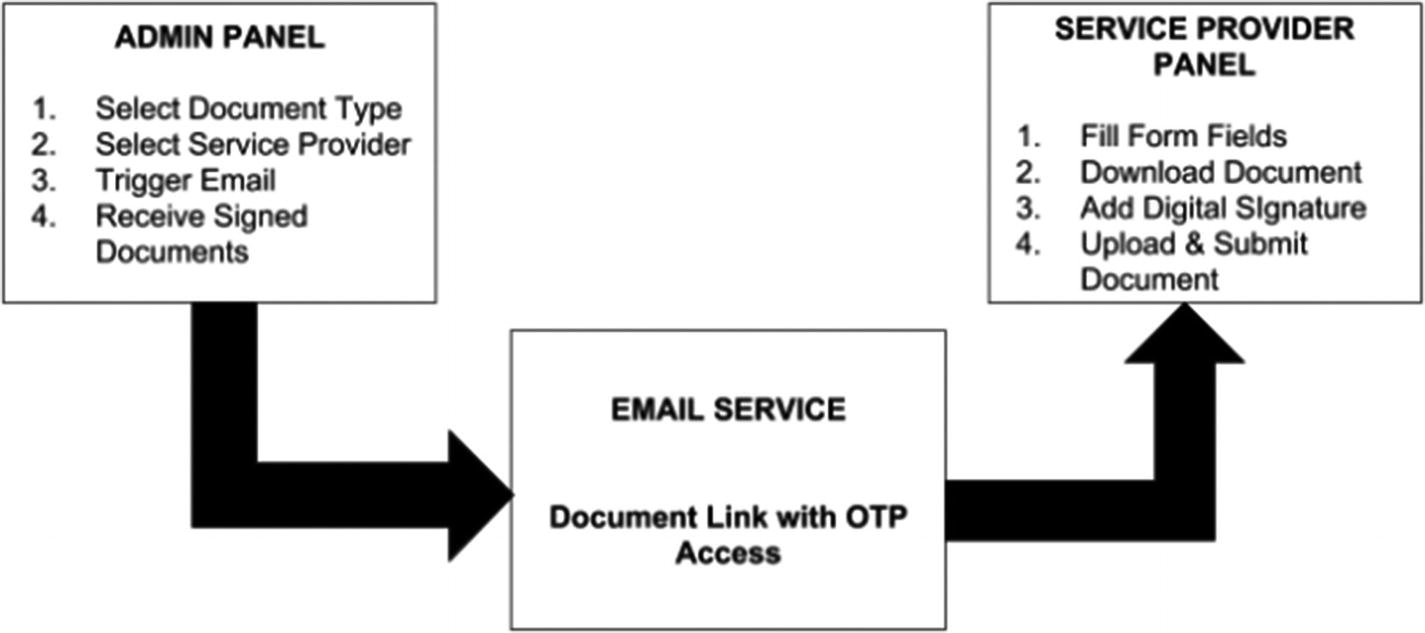

Recognizing these factors, governments, banks, legal firms, courts, and even document storage companies are now building POCs that allow limited access, sharing, and authentication of document validation over a shared ledger.

A traditional platform that is centrally hosted usually asks its stakeholders or third-party engagements to simply comply with the platform without any promise or means to maintain the security of the data. For example, while uploading scanned documents of identity, one is asked to attest to the physical signature and upload the scanned copy, and then it is verified manually even today.

A normally hosted service platform

In such a system, there is no attempt to reach consensus or provide a platform for such an option. It is a straightforward, single-focused platform. Similarly, in the education field our degree certificates are signed by the central authority of the education board.

During background checks, one of the most expensive processes is to trace the truth of the source and physically check its existence in their records. Now, when the data is collated on a single blockchain network of truth and trust where all—the source as well as the end destination nodes—exist, the blocks of data transmitted in encrypted formats ensure the data request is witnessed and that a fraudulent request may not occur in the first place. In simple words, consider a real use case where all educational certificates (data blocks) lie on the shared ledger, and where the university is the source node and the companies that require validation are the end destination nodes. The student/employee nodes initiate the validation request on-chain and get verified over the shared ledger. In such systems, a student may never be able to fake a certificate as the witness of the source is on-chain.

Another important aspect of using digital signatures for documents is that it leaves a machine fingerprint in the form of the address of the node. Therefore, such digital traces cannot be forged, and it is difficult to develop fakes.

In a smart contract that formulates the consensus of a chain, the digital signatures of documents would simply be the machine address captured upon accepting the conditions of the smart contract. Not all digital signatures are developed purely from the machine address, however. Many times it is a mathematical formula that encapsulates the hash address of the node along with the private key.

With such a valid digital signature for a document on the ledger, one would not be able to retract the signed block, thus embedding trust of the true source of the signature (authenticity) and ensuring no alteration of the data transmission.

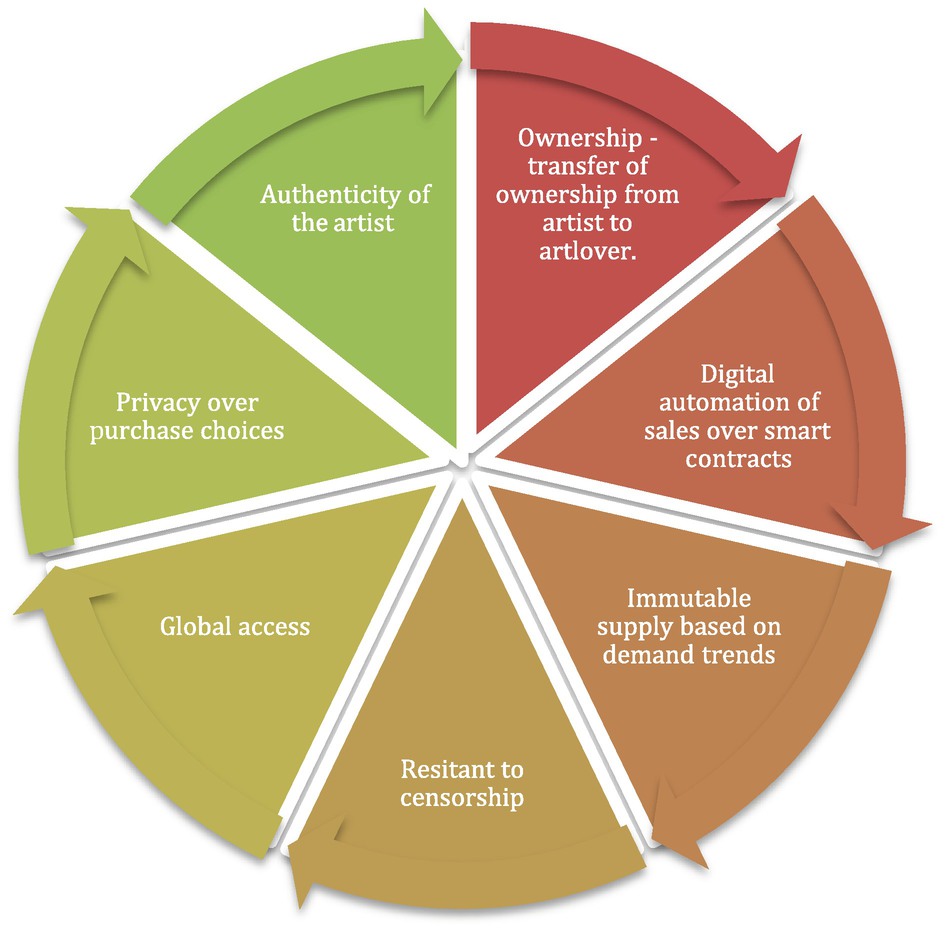

Actions taken over blockchain with respect to the artworks as assets

Cost savings – This is the most obvious benefit. Because blockchain transactions don't require intermediaries, processes can be made more efficient and less expensive. There's no need for auditors or legal professionals to validate the authenticity of information, so those costs come out of the process.

Efficiency – Fewer people means faster turnaround. Transactions that might take days waiting for multiple sign-offs can be concluded in seconds.

Security – The fewer participants there are in a transaction, the less risk there is that something could go wrong. Handoff points are a prime vulnerability, and blockchains effectively eliminate them.

Flexibility – Any digital asset can use a blockchain, including difficult-to-protect items like multimedia and email records.

Source: Iron Mountain

As we learn the extent of the applicability of blockchain technology and its advantages over traditional methods, we are going to look into another application that has been brought to the world by an organization that was once a giant in the field of photography and related devices and accessories and then picked up again with a pivot into tech with blockchain. The organization under discussion here is none other than Kodak.

The recent pivot of Kodak to blockchain has been on the public stage since Kodak’s announcement that it would build a new blockchain-based document management system. The service developed by the company does not depend on a third-party license and is completely developed and owned by Kodak.

Kodak Services for Business, as the suite is called, is a platform built with the aim to store and manage documents that are sensitive in nature in an efficient and secure manner. The Kodak Document Management Platform is intended to provide businesses and governments a facility to handle documents by storing them with security and regulating access over a blockchain.

Kodak estimates a 20 to 40 percent cost savings through the automation of workflows and decrease in human intervention in content, information, and documents. In January 2018, a third party licensed the Kodak brand name for KODAKCoin, which was designed to work with a blockchain developed to track image copyrights online.

Similar to how the supply chain was one of the foremost reasons for blockchains to scale up, the process of document management and security is becoming more popular in the blockchain space. It is not only Kodak that is looking at it as a potential offering to businesses.

Billon, a Polish-British fintech firm, is also working on a platform for a blockchain-based document management system.

The digitization of documents in the digital era, given the redundancy and reconciliation efforts wasted in hard copy, has driven companies to look into digitization and further builds a case for blockchains as the most viable option, considering security and access control.

With this, we come to the end of the part of the book where we reflect upon use cases and technical learnings. We envision helping you to evaluate your understandings and learnings in the next chapter. Chapter 10 further provides hands-on exercises.