CHAPTER 10

Home Habits

LIVE MORTGAGE FREE

It’s a rare week when someone doesn’t ask me about mortgages. Clients, radio callers, even friends—it seems like every single person wonders if, how, and when they should pay theirs off. There’s a lot of conflicting information out there, and nobody wants to get it wrong.

A mortgage is often the biggest expense we take on in our lifetimes. We spend more money buying a house than we do sending our kids to college. Unless you can buy your home outright, which 99.95 percent of Americans can’t afford to do, you end up with a mortgage, which is a pretty hefty chunk of debt.

Banks set up mortgages a long time ago under fairly nefarious terms, with long payment schedules that last 15, 30, even 40 years. In the classic 30-year mortgage, you basically end up paying for the house twice because of the interest. You also spread out your biggest payment over multiple decades.

While you have a mortgage, it’s the bill that’s always there, always lingering. It’s a constant, mind-numbing refrain that sticks in your head worse than an Alanis Morissette song. Gotta pay the mortgage. Gotta pay the mortgage. It’s your biggest single monthly outlay, and it follows you around relentlessly. No wonder there’s so much joy and comfort and happiness waiting just over the rainbow, once that mortgage is a thing of the past.

If you can afford to pay off your mortgage, do it. That’s the financial and lifestyle habit at the heart of this chapter. One irrefutable thing I’ve learned from my research over the years is that, regardless of your interest rate and the cost, getting rid of your mortgage by the time you retire is a powerful indicator of happiness.

In this chapter, we’ll look at several key home habits of the happiest retirees, including:

• HROBs pay off their mortgages. The happiest retirees have eliminated—or are very close to eliminating—their mortgage payments. We’ll discuss several important factors to consider when paying off your mortgage, including whether or not you can safely do so, using the One-Third Rule.

• Happy retirees live in nice houses, but not McMansions. It’s OK to be comfortable. It’s less OK to have exotic zebras grazing on the 400-acre ecofarm you call home.

• The happiest retirees know that neighborhoods and networks are more important than their four walls. It can be tempting to want to move to greener pastures. But sometimes, when you’ve spent years cultivating your community, the best nest might just be the one you’ve been roosting in all along.

• HROBs don’t downsize. This is a new habit gleaned from my most recent study. HROBs don’t downsize into a smaller place, mainly because they anticipate their kids and grandkids will be coming home to visit.

This chapter is meant to arm you with the right strategies to really get rolling. Hear that horn honking outside? That’s me, cruising up to the curb, ready to drive you to the happiest retiree block party. How do we get there? By helping you pay off your mortgage sooner than you thought.

SHOULD I PAY OFF MY MORTGAGE? THE ONE-THIRD RULE

To pay or not to pay. That is the question. It’s the question Hamlet would have asked if he’d survived long enough to buy his own castle in Denmark—and the question that still divides financial planners today.

Some money pros think you are better off investing your surplus money rather than using it to pay off or pay down your mortgage. They believe you will get a larger net return by continuing to pay interest on your house while investing leftover resources and earning a higher return in the stock market. Instead of using $100,000 to pay off a 4 percent mortgage, they’ll tell you to invest it in the market where you could see a return of, say, 8 percent. The result: a net 4 percent gain of $4,000.

Look, I get it. In theory, it makes sense. But last time I checked, we live in the real world, and often this strategy fails the real-world test. In the real world, the market could be flat for a decade, as it was in the 2000s, or it could crash and burn just before you need to cash in.

For me, paying off your mortgage takes out the guesswork. It’s a surefire thing. Once that prodigious debt is off your shoulders, no one gets to take a 4 percent bite out of your joy.

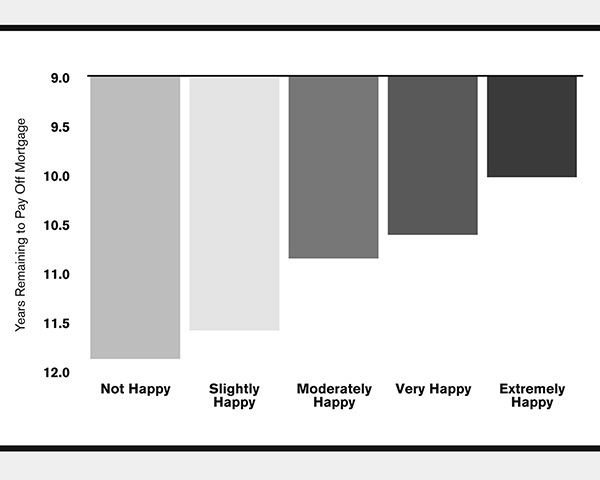

I’ve thrown a lot of charts and graphs at you in this book, and you’ve gamely caught every pass. The one in Figure 10.1 is a classic. Have you ever seen such clean, beautiful stairsteps? As the years to pay off the mortgage go down, happiness levels go up, smooth and simple.

FIGURE 10.1 Years Until Mortgage Is Paid Off

The happiest retirees report that there is a real sense of peace and serenity that comes from knowing you own your house free and clear. It just feels good as you enter a new phase of life. I call this the Ahhhh factor. When you relieve yourself of this financial and psychological burden, you can breathe a giant sigh of relief. Eliminating a house payment also dramatically lowers your monthly retirement living expenses, thus taking pressure off your nest egg and other sources of monthly income. Talk about a stress reliever!

There’s no one-size-fits-all solution when it comes to eliminating your mortgage. People have different circumstances, savings, and tolerance for risk. But if there’s one rule I’ve seen liberate thousands of retirees and pre-retirees, catapulting them toward happiness, it’s the One-Third Rule. If you can pay off your mortgage using no more than one-third of your nonretirement savings, do it.

Let’s say you have $300,000 in savings and your mortgage is $90,000. You have my blessing to take one-third of your after-tax money and pay it off. Boom! Done.

If you have $1 million in your IRA or 401(k) but only $100,000 in after-tax, and you have a $300,000 mortgage: do not pass go. The ratio doesn’t work because almost all of that is retirement money.

One of the most common questions I get is, “Do I pay off my mortgage with my retirement fund? I’ve got $400,000 in my 401(k) and my mortgage is $200,000. Shouldn’t I just pay it off?”

The answer is: absolutely not.

Let’s take a run at this from a slightly different perspective. If you’re still working and making, say, $100,000, and then you pull out another $200,000, all of a sudden, your income is $300,000. Your tax bracket goes through the roof. Now you’ve just had to pay a huge tax bill in order to pay off the mortgage. It creates a tax tsunami—and you’ll want to run for the hills.

You will almost never want to use retirement-account money—

IRAs, 401(k)s—to pay off a mortgage. Remember, paying off your mortgage is about creating peace of mind. Tapping your pretax retirement nest egg won’t do that. Reducing your hard-earned retire-

ment reserves undercuts your future security by decreasing actual cash and future income earnings on that account. (You can access those funds in a more tax-efficient way—we’ll talk about that in Chapter 11.)

The reason I like the One-Third Rule is that it makes things cut and dry. Can you pay off your mortgage and still have at least two-thirds of your after-tax money left? Excellent. Take the plunge. And if you can’t? Time for a different approach.

If the One-Third Rule isn’t in play for you, your next best option might be the Extra Payment Plan. This is where you either pay an additional amount of principal with each monthly payment, or make 13 mortgage payments per year instead of 12. In fact, most happy retirees who have paid off their mortgages did so by paying more than the minimum monthly payment each month over several years. In my experience, about 70 percent of retirees who are mortgage-free used this method to reach that goal.1

Here’s an example of how it might work. Let’s say you just bought a house last year. Welcome home! I’ll bring a bottle of gin as a housewarming gift.

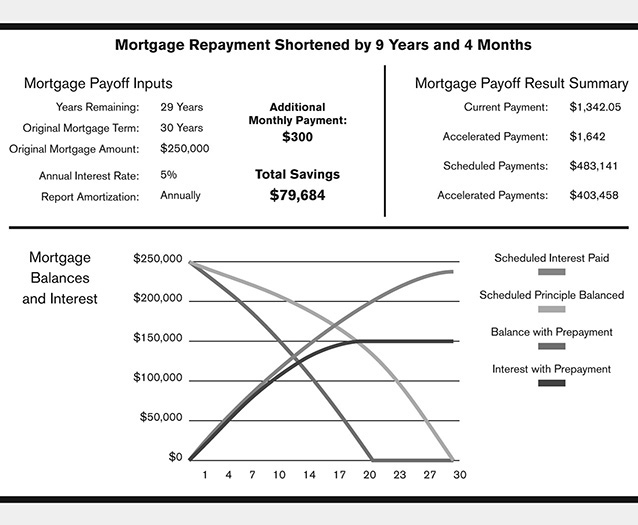

If you have just started a 30-year mortgage of $250,000 at 5 percent interest, your scheduled monthly payment will be $1,342. Adding $300 per month to that payment will slice nine years and four months off the life of the loan—and save $79,684 in interest (Figure 10.2).

FIGURE 10.2 Early Mortgage Payoff

You read that right. If you make an additional mortgage payment of just $300 a month—the price of two nice steak dinners—you shave nearly a decade off a 30-year mortgage. That’s pretty impressive.

If a monthly payment just isn’t doable, you might consider saving up to make an extra mortgage payment every year. You could structure your payment plan so that you pay 50 percent of your monthly obligation every two weeks. That’s a painless way to make an extra month’s payment every 12 months.

Or maybe you get a sudden windfall of cash after your wealthy Aunt Bertha passes away. You thought the woman hated your guts, but it turns out you were her favorite—and the lawyer of her estate calls to tell you just how much her affections were worth. If you can pay off your mortgage in a big chunk and still stay financially secure, do it. You just want to make a solid plan so that you’re either paid off or mostly paid off by the time you retire. If you’re 58 and you’re retiring at 65, let’s get a plan in place to pay your house off over the next five to eight years.

As I was writing this chapter, I met a couple who was facing the usual mortgage dilemma. We’ll call them Mitch and Morgan Mortimer. Morgan said to me, “Our mortgage is only 2.85 percent. I know we shouldn’t pay it off. We should invest it somewhere else because our money should be growing more than that.”

To which I replied, “In theory, you’re right. But I’m actually a big advocate for getting rid of the mortgage. Not only because a bird in the hand is worth two in the bush, but because you’re guaranteed to save the 2.85 percent year after year. And you’re getting this wonderful peace of mind by getting rid of the burden.”

I won’t beat around the bush. If you can abide by the One-Third Rule and pay off your mortgage, do it tomorrow. Better yet: do it today. It’s often said a house owns you, not the other way around. Make the right decision by getting rid of the mortgage, and you’ll win back some retirement freedom from that fickle mistress, Home Sweet Home.

THE MCMANSION IS NO HAPPY MEAL

My kids love modern mansions. I think it’s because of all the young YouTubers who get famous and buy ridiculous Hollywood mansions. They’re not buying traditional Tudors; they buy these big modern white houses with gigantic glass windows and 12 balconies, and then they turn the interior into a leisure center with a movie theater, bowling alley, golf simulator, and oxygen bar.

Spoiler alert: there are no happy retirees hiding behind those floor-to-ceiling glass windows. HROBs live in nice houses, but not McMansions.

In one of my first retirement research studies conducted back in 2013, the average HROB home value came out to around $355,000. I was amazed that even the happiest retirees didn’t have home values that exceeded $400,000 (on average).

Of course, real estate prices have jumped so dramatically, that number needs a face-lift. While many tried-and-true HROB statistics like income, spending, and liquid net worth still hold water, HROB home values have to be adjusted for 2021’s unprecedented housing market inflation. You could say the seeds were sown back in 2007 and 2008, when the mortgage bust led to a massive underbuilding of new homes—meaning there weren’t enough to meet demand when the current “work from anywhere” mega trend hit, with millions of Americans favoring home offices.

According to the Case-Shiller US National Home Price Index,2there was a staggering 65 percent increase in home values from 2013 to 2020. Using that number as a baseline, I’ve increased the HROB’s average home value by 65 percent to get today’s value of $585,000. A pretty impressive spike when you consider all an HROB had to do to their home was simply stay in it!

Staycations Just Don’t Work

Staying in your home long term is a good HROB move. Staying in your home and calling it a vacation? Not so good. After 2020, we’ve all had enough staycations to last a lifetime. But long before COVID-19 locked the world down and massively restricted travel, my happy retiree research showed that no matter what cute clever name you stick on it, staying in your home does not count as a vacation. If you’re not getting away, you’re not actually flipping your mindset to be somewhere else.

According to my data, if staycations were a person’s most common form of vacation, they were 2.5 times more likely to land in the unhappy camp. Happy retirees do not stay cooped up at home.

Yes, some HROBs do have modest vacation homes. I’m not saying you can’t stay in your vacation home and still be happy. We’ll talk about that next. Just know that a staycation isn’t a long-term substitute for the real thing. Sometimes you have to get away to get happy.

SHOULD WE GET A SECOND HOUSE?

I get this question all the time.

“We live in Charlotte. Should we get a place in Hilton Head?”

“We live in Atlanta. Should we get a place down in the Florida Panhandle?”

Couples want to know if they can afford to get a place somewhere in the mountains or on a lake that’s not going to be dramatically expensive.

If you want to have a second home somewhere magical, you’re certainly not alone. You may be daydreaming about buying a place in St. Augustine, Florida, one of America’s most wonderful historic cities. Or getting a ski condo up in Park City, Utah. Or purchasing a rustic ranch under the big sky in Jackson Hole, Wyoming. These all sound great.

But whenever people ask me about a second home, I first steer them back to the Holy Grail of house habits: have a plan to pay off your primary home mortgage first.

Burning the mortgage leaves you more money to follow your dreams and passions, including the ones that inspire you to leave home. The money you’ve been sending to Bank of America on the first of the month is now yours to use as you wish. You could spend it on more vacations, hobbies, or charitable giving—or you can use it to buy that cabin in Bozeman, Montana that you’ve been coveting since 2003.

Once you get rid of the debt on your primary residence, I’m all for you getting a second place on the coast or up in the Blue Ridge Mountains. As long as you’re not buying something too speculative, a vacation property can be a good investment, and it allows you to be flexible: even if you only keep it for a few years, you can ideally sell it for a similar or greater amount. If you can afford a second home, I think it’s a great option.

And in case you were wondering, there is no discernible difference in happiness when it comes to where that second home is located. In a recent research study, I tested houses on the beach versus in the mountains versus on the lake in relation to retiree happiness, and there was no uptick or downtick for any location. But I will tell you, I see utter and pure enjoyment when families are able to have some sort of second home or getaway that they go to over and over again.

We live in a world of Airbnb where we can rent a place in any location at any time. That’s great! I love Airbnb and have used it many times over the years. But what you don’t normally hear about is just how much you love going back to that exact same Airbnb with the whole fam. Even if you find one you love, it’ll probably be full next time you try to book it. Those places don’t become a second home or a second community.

But when retirees have some sort of secondary family gathering place? There is something very powerful, even magical about having a family cottage or cabin or lake house, some shared location where you go to spend time on a recurring basis. It doesn’t have to be fancy. What makes it special is that you are getting away together.

If you can afford to have someplace for the family to go as a group, very rarely will you regret it. One caveat, though: if you’ve got little kids, I can say from personal experience that it’s hard to utilize a second place because kids tend to get busy with school and sports and ballet and all of the activities they have. I’ve seen younger couples get frustrated when they’ve invested in a second home and then their kids’ schedules are too complicated for them to actually use it. However, as parents get a little older and their kids get a little more independent, a vacation home can be a wonderful gift to yourselves. The happiest retirees would rather have one modest home and a second beloved cabin for family getaways than one giant modern mansion.

Which brings me to my next topic.

Some retirees aren’t interested in a vacation home, but they are very much interested in getting a fresh start. Moving out of their current home into a brand-new one can seem like a magic elixir, a way to push the reset button on their lives. When housing markets are hot, relocating is extra tantalizing; a strong seller’s market dangles a most tempting carrot.

The truth, however, is that these decisions are about a lot more than dollars and cents.

To illustrate why that’s true, I’m going to pass the mic to Tidy-Up Tessa.

TIDY-UP TESSA: IT’S ALL ABOUT THE NEIGHBORHOOD

Tessa was a family friend. She’d lived in her home for many years, and happily so. But she had recently lost her husband, and in the wake of his death, she was thinking of downsizing. She wondered if a new home might help her move through her grief and into this new phase of her life.

As we talked, Tessa was very emotional. She truly loved her home, but it was hard for her to imagine staying in a house she’d shared with her husband for the last 30 years now that he was gone.

“Can you tell me what you love about where you live?” I asked.

Tessa’s whole face lit up. “Well, I love my neighborhood. There’s a group of women in our late fifties and early sixties—we have a book club and get together every week and drink wine. It’s a lot of fun. My neighbor Jack across the street has become a good friend, and he’s super helpful when I need house stuff done. He’ll come over and help me light the pilot on my gas fireplace, or troubleshoot when my heater or AC starts giving me trouble.”

“Sounds like you’ve got some really great neighbors,” I said.

She nodded. “There are also some younger thirtysomething couples down the street. I don’t know those families as well, but it’s nice to chat with them and see their little kids. Every year we do a neighborhood Easter egg hunt and a big Halloween costume parade.”

“Your neighborhood sounds pretty amazing,” I said, and she agreed.

“The thing is,” I said, “when you move, even if it’s only a few miles, your neighborhood does change. Yes, you can still drive to your book club, no question. But you can’t be quite so carefree about drinking wine when you have to get into a car instead of just strolling back across the street. And your neighborhood—there’s something to it. There’s something about chatting over the fence or running into a neighbor at the grocery store.”

I reminded Tessa that if she were to move farther than a mile or two—say 15 miles—then it’s a big deal. Moving is always a big deal, but at that distance, you’re definitely relocating your life to some extent. She would probably stop going to the book club eventually, even if at the beginning she tried to keep it up. If she moved to a new county or a new city, she might also need to find a new dentist, doctors, and other healthcare providers, as well as establishing other commercial and professional relationships. That includes the places she frequents on a day-to-day basis: grocery stores, dry cleaners, cafés and restaurants, hair and nail salons.

If you live in Atlanta and move to Alpharetta? That may be only a 30- to 40-minute drive, but in some ways, you might as well have moved out of state. Sure, you can still see people. You can always make the drive. But proximity is important. As we’ve discussed, it’s already more of a challenge to keep up your social network during retirement; once you throw physical distance into the mix, it’s an even bigger obstacle.

When your geography changes, so does your community. The intangibles—seeing kids, grandkids, friends—change dramatically with a long-distance move. Though I should note that if your adult children live 40 minutes (or miles) away, that still checks the HROB box for living close to at least half of your kids.

“Are you close to your friends and family?” I asked Tessa.

“Yes! My daughter lives about 10 minutes away. And most of my friends live nearby.”

I gently reminded her that if she moved to another county, she would most likely lose touch with some of her current friends and have to make new ones. But I said I also understood why the thought of keeping her old routines was painful, now that her husband was gone. After all, most of her friends had been their couple friends, and no one else had lost a spouse. That didn’t stop Tessa’s friends from being empathetic and loving—they brought her flowers, cooked casseroles, and sat with her while she cried. But it was still hard.

As for the house itself? Tessa was deeply conflicted. She loved the house, but she felt like there were reminders of her husband everywhere. She hadn’t been able to empty out his office; even looking at his lonely pillow made her sad. And there was clutter everywhere. She was the first to admit she hadn’t done a very good job keeping things tidy amid her grief.

“Some of our neighbors recently sold their house,” Tessa told me, “and they said it’s a very good seller’s market for homes in our area. If I want to get top dollar, doesn’t that mean I should act now?”

I explained to Tessa how, if the houses in her neighborhood were selling for top dollar, so were the houses in most other neighborhoods. She might be able to get top dollar, but she’d also be paying top dollar for another house anywhere in the same vicinity. If she wanted to sell her place for $550,000, which was the number she had in mind, a similar house that she liked and felt comfortable in was going to cost her at least the same amount somewhere else. If she moved farther away, we’d land right back at the 30-to-40-minutes-away conversation. The only way for her to make a sell-then-buy move financially attractive was to relocate somewhere that, at least geographically speaking, was dramatically different. And at that point, you might as well move out of state because you’re going to have to reestablish not just your neighborhood but your entire social network.

I said all this to Tessa, but it didn’t dissuade her. While she wasn’t sure if she was truly emotionally ready to move, she told me she had taken steps to list her home for sale.

“It’s a bittersweet decision,” she told me. “I still feel conflicted about it. But I have to see where this leads.”

So Tessa put the house on the market. She hired a professional stager, who told her she needed to do a good bit of work before her home would sell. The whole place needed to be decluttered and deep cleaned. The basement, which Tessa and her husband had primarily used for storage, was in dire need of a glow-up, a coat of fresh paint on the walls and concrete floors.

“We need new art,” the stager said, “better furniture and some bright new rugs. And you’ll want to hire someone to wash all the windows to really make them gleam. If you want to get top dollar for this house—and this is a pretty hot market in Atlanta—you’re going to need to spend a little time and money to spruce this place up.”

Tessa said, “OK. Let’s do it.”

So she scheduled the window washers. She called a handyman and a 1-800-GOT-JUNK-type service to come clean out the basement. While they were there, she realized she had junk all over the place, not just the basement. Tessa cleared out the master bedroom and the family den. She even recruited a couple of her book club friends to help her clean out her husband’s office. These women were happy to help.

“If we’re going to do this right,” Tessa said, “then let’s really tidy this place up.”

By the end of the week, the windows had been washed and the whole house had been decluttered. Tessa bought new rugs and a few pieces of not-too-expensive furniture from Pottery Barn and some gorgeous wall art at Pier 1. She got a new kitchen tablecloth, cream pillows and sheets for the master bedroom, and a lavender comforter set for the guest room. She changed all the light bulbs, dusted the fixtures, polished the sconces—a lot of little stuff that added up.

The stager suggested putting in a bigger flatscreen TV in the main living room. At first Tessa demurred—until she went online and saw how inexpensive it would be. She discarded her old clunker television from 1999 and got a TV big enough for all her kids and grandkids to crowd around for Disney movie nights.

Tessa’s house didn’t just look better. It looked spectacular. It looked like a new house! Not only did it sparkle—it smiled. All she had to do was roll up her sleeves and put a little work into it. As it turned out, staying active also helped Tessa move through her grief. She said she felt like she was finally coming back to life.

Can you see where this is going?

Tessa dressed up her house to sell it, only to realize: “Wait a minute. I don’t want to go!” Not only did she have a refreshed house that she remembered she loved; it looked better than ever. And she didn’t have to say goodbye to her neighbors and friends. There was no reason for her to leave.

Tidy-Up Tessa is still there to this day. If you ask her, she’ll tell you how happy she is that she didn’t pull the trigger on the sale of her house, but rather stayed in her beloved home.

When it comes to houses, the grass is always a little bit greener on the other side. That’s especially true when your neighbor keeps a well-manicured lawn. Very few of us love every single thing about our home. There’s always something we want to change or update.

Houses are not forever organisms. They leak, crack, fall into disrepair. They require a lot of maintenance as they slowly disintegrate over time. Most of us have at one time or another thought: “Hey, it’d be nice to have a new house. A fresh start.” I totally get that sentiment.

But the happiest retirees know that neighborhoods and networks are more important than their four walls. Sometimes, when you’re exhausting yourself looking everywhere for the perfect place to fix all your problems, you might realize yours was the best nest all along.3

That said, there’s no statistic that says that if you move, you’ll be unhappy. We’ve met plenty of extremely happy retirees in this book who have moved. Mary McCormick went to Big Canoe, and Paradise Paula went to the Florida Panhandle—both secondary homes that became their primary ones. Frank and Ava Johnson moved to California to be closer to their kids.

I’m not saying there’s one course of action that’s right for every retiree. What I am saying is that HROBs recognize the immense value of their neighborhoods and networks. Mary, Paula, Frank, and Ava all made a conscious choice to move toward family, core pursuits, and social connections, not away from them.

DON’T BE A DEBBIE DOWNER

We’re all familiar with the story of Don and Debbie Downer, even if we know them by other names. Now that Don and Debbie are retired and their kids are grown with kids of their own, the Downers don’t need a two-story, four-bedroom house in the heart of Atlanta, right? They’ve decided to downsize.

Bad news, Don and Debbie: the moving truck might be dropping you off on the unhappy block of your new neighborhood.

Happy retirees don’t downsize. My research has shown that the people who said they didn’t plan to downsize were more likely to be happy, and those who planned to downsize were more likely to be unhappy.

How do I interpret that data? In a couple of ways. If you need to sell your home, maybe you haven’t been able to pay off the mortgage, so you never freed yourself from that financial and mental burden. Perhaps you don’t love your neighborhood all that much to begin with. Unlike Tidy-Up Tessa, maybe you don’t get along with your neighbors, and there are no Easter egg hunts and happy hours masquerading as book clubs.

Personally, I think it goes deeper. I believe the real reason happy retirees don’t downsize is emotional. They love their neighborhoods, and they’ve established themselves in their communities. They feel genuine safety, trust, and intimacy within their social networks. That tracks, considering HROBs feel connected to the people around them, “plugged in” in all the ways that count.

Best of all, they like having a place where friends and family can gather. They know their kids and grandkids are going to come home to visit, and they want space to host everyone. Their homes become the warm, cozy nexus for birthdays and holidays—

Mother’s Day brunches, Fourth of July BBQ cookouts, Thanksgiving dinners. And don’t forget the bridal showers and baby showers, all the various celebrations that mark the most wonderful parts of a life.

The happiest retirees understand that a home is so much more than a mortgage. It’s more than a foundation, roof, and four walls. Home is where the heart is, a place where the people you love can come together around a crackling fire, sit side-by-side at a long harvest table, and feast on joy, health, and happiness until the cows come home.