17

SHARE-BASED PAYMENT

INTRODUCTION

The IASB's Conceptual Framework defines equity as the residual interest in the assets of an entity after deducting all its liabilities. Shareholders' equity comprises all capital contributed to the entity (including share premium, also referred to as capital paid-in in excess of par value) plus retained earnings (which represents the entity's cumulative earnings, less all distributions that have been made therefrom).

In the past, the matter of share-based payments (e.g., share option plans and other arrangements whereby employees or others, such as vendors, are compensated via issuance of shares) has received significant attention. The IASB introduced a comprehensive standard, IFRS 2, Share-based Payment, which requires a fair value-based measurement of all such arrangements.

A major objective of the accounting for shareholders' equity is the adequate disclosure of the sources from which the capital was derived. The appropriate accounting treatment is dealt with in Chapter 16. Where shares are reserved for future issuance, such as under the terms of share option plans, this fact must also be made known. The accounting for this is addressed in this chapter.

| Source of IFRS |

| IFRS 2 |

SCOPE

IFRS 2 applies to the accounting for all share-based payment transactions, including:

- Equity-settled share-based payment transactions;

- Cash-settled share-based payment transactions; and

- Cash-settled or equity-settled share-based payment transactions (when the entity has a choice to settle the transaction in cash (or other assets) or by issuing equity instruments).

The standard may also apply in the absence of specifically identifiable goods and services but when other circumstances indicate that goods or services have been (or will be) received.

Furthermore—and very importantly—IFRS 2 applies to all entities (both publicly and privately held). Also, a subsidiary using its parent's or another subsidiary's equity as consideration for goods or services is within the scope of the standard. However, an entity should not apply the standard to transactions in which the entity acquires goods as part of the net assets acquired in a business combination (such transactions are within the scope of IFRS 3). In such cases, it is important to distinguish share-based payments related to the acquisition from those related to employee services and supply of goods and services. Also, IFRS 2 does not apply to share-based payment contracts within the scope of IAS 32 and IFRS 9.

IFRS 2 was amended in 2013 to provide for changes to the definition of vesting condition and market condition and separate definitions were also introduced for “performance condition” and “service condition.” The changes were applied for grant dates on or after July 1, 2014.

The definition of “fair value” used in IFRS 2 differs in some respects from that in IFRS 13, Fair Value Measurement. Thus, when applying IFRS 2 the “local” definition of “fair value” is utilised rather than the IFRS 13 definition.

DEFINITIONS OF TERMS

Cash-settled share-based payment transaction. A share-based payment transaction in which the entity acquires goods or services by incurring a liability to transfer cash or other assets to the supplier of those goods or services for amounts that are based on the price (or value) of equity instruments (including shares or shares options) of the entity or another group entity.

Employees and others providing similar services. Individuals who render personal services to the entity and meet one of the following additional criteria:

- The individuals are regarded as employees for legal or tax purposes;

- The individuals work for the entity under its direction in the same way as individuals who are regarded as employees for legal or tax purposes; or

- The services rendered are similar to those rendered by employees.

For example, the term encompasses all management personnel, i.e., those persons having authority and responsibility for planning, directing and controlling the activities of the entity, including non-executive directors.

Equity instrument. A contract that evidences a residual interest in the assets of an entity after deducting all of its liabilities. (A liability is defined in the Conceptual Framework as a present obligation of the entity to transfer an economic resource as a result of past events.)

Equity instrument granted. The right (conditional or unconditional) to an equity instrument of the entity conferred by the entity on another party.

Equity-settled share-based payment transaction. A share-based payment transaction in which the entity:

- Receives goods or services as consideration for its own equity instruments (including shares or share options); or

- Receives goods or services but has no obligation to settle the transaction with the supplier.

Fair value. The amount for which an asset could be exchanged, a liability settled, or an equity instrument granted could be exchanged, between knowledgeable, willing parties in an arm's-length transaction. It is pertinent to note that detailed guidance for measurement of fair value of shares and share options is provided in this standard, which may differ from the definition under IFRS 13.

Grant date. The date at which the entity and another party (including an employee) agree to a share-based payment arrangement, being when the entity and the counterparty have a shared understanding of the terms and conditions of the arrangement. At grant date, the entity confers on the counterparty the right to cash, other assets or equity instruments of the entity, provided the specified vesting conditions, if any, are met. If that agreement is subject to an approval process (for example, by shareholders), grant date is the date when that approval is obtained.

Intrinsic value. The difference between the fair value of the shares to which the counterparty has the (conditional or unconditional) right to subscribe or which it has the right to receive, and the price (if any) the counterparty is (or will be) required to pay for those shares. For example, a share option with an exercise price of €15, on a share with a fair value of €20, has an intrinsic value of €5.

Market condition. A performance condition upon which the exercise price, vesting or exercisability of an equity instrument depends that is related to the market price (or value) of the entity's equity instruments (or the equity instruments of another entity in the same group), such as:

- Attaining a specified share price or a specified amount of intrinsic value of a share option; or

- Achieving a specified target that is based on the market price (or value) of the entity's equity instruments (or the equity instruments of another entity in the same group) relative to an index of market prices of equity instruments of other entities.

A market condition requires the counterparty to complete a specified period of service (i.e., a service condition); the service requirement can be explicit or implicit.

Measurement date. The date at which the fair value of the equity instruments granted is measured for the purposes of IFRS 2. For transactions with employees and others providing similar services, the measurement date is the grant date. For transactions with parties other than employees (and those providing similar services), the measurement date is the date the entity obtains the goods or the counterparty renders service.

Performance condition. A vesting condition that requires:

- The counterparty to complete a specified period of service (i.e., a service condition); the service requirement can be explicit or implicit; and

- Specified performance target(s) to be met while the counterparty is rendering the service required in (1).

The period of achieving the performance target(s):

- Shall not extend beyond the end of the service period; and

- May start before the service period on the condition that the commencement date of the performance target is not substantially before the commencement of the service period.

A performance target is defined by reference to:

- The entity's own operations (or activities) or the operations or activities of another entity in the same group (i.e., a non-market condition); or

- The price (or value) of the entity's equity instruments or the equity instruments of another entity in the same group (including shares and share options) (i.e., a market condition).

A performance target might relate either to the performance of the entity as a whole or to some part of the entity (or part of the group), such as a division or an individual employee.

Puttable financial instruments. Shares which the holders can “put” back to the issuing entity; that is, the holders can require that the entity repurchases the shares at defined amounts that can include fair value.

Reload feature. A feature that provides for an automatic grant of additional share options whenever the option holder exercises previously granted options using the entity's shares, rather than cash, to satisfy the exercise price.

Reload option. A new share option granted when a share is used to satisfy the exercise price of a previous share option.

Service condition. A vesting condition that requires the counterparty to complete a specified period of service during which services are provided to the entity. If the counterparty, regardless of the reason, ceases to provide service during the vesting period, it has failed to satisfy the condition. A service condition does not require a performance target to be met.

Share-based payment arrangement. An agreement between the entity (including its shareholder or another group entity) and another party (including an employee) to enter into a share-based payment transaction, which entitles the other party to receive:

- Cash or other assets of the entity for amounts that are based on the price (or value) of equity instruments (including shares or share options) of the entity or another group entity; or

- Equity instruments (including shares or share options) of the entity or another group entity provided the specified vesting conditions, if any, are met.

Share-based payment transaction. A transaction in which the entity:

- Receives goods or services from the supplier of those goods or services (including an employee) in a share-based arrangement; or

- Incurs an obligation to settle the transaction with the supplier in a share-based payment arrangement when another group entity receives those goods or services.

Share option. A contract that gives the holder the right, but not the obligation, to subscribe to the entity's shares at a fixed or determinable price for a specified period of time.

Vest. To become an entitlement. Under a share-based payment arrangement, a counterparty's right to receive cash, other assets or equity instruments of the entity vests when the counterparty's entitlement is no longer conditional on the satisfaction of any vesting conditions.

Vesting condition. A condition that determines whether the entity receives the services that entitle the counterparty to receive cash, other assets or equity instruments of the entity, under a share-based payment arrangement. A vesting condition is either a service condition or a performance condition. (A non-vesting condition is not specifically defined in the standard. Accordingly, any condition which a vesting condition is not would be a non-vesting condition.)

Vesting period. The period during which all the specified vesting conditions of a share-based payment arrangement are to be satisfied.

OVERVIEW

In accordance with IFRS 2, a share-based payment is a transaction in which the entity receives goods or services as consideration for its equity instruments or acquires goods or services by incurring liabilities for amounts that are based on the price (or value) of the entity's shares (or other equity instruments of the entity). The concept of share-based payments is broad and includes not only employee share options but also share appreciation rights, employee share ownership plans, employee share purchase plans, share option plans and other share arrangements. The accounting approach for a share-based payment depends on whether the transaction is settled by the issuance of:

- Equity instruments;

- Cash; or

- Equity and cash.

The general principle is that all share-based payment transactions should be recognised in the financial statements at fair value, with an asset or expense recognised when the goods or services are received. Depending on the type of share-based payment, fair value may be determined based on the value of goods or services received, or by the value of the shares or rights to shares given up. In accordance with IFRS, the following rules should be followed:

- If the equity-settled share-based payment is for goods or services (other than from employees and others providing similar services), the equity-settled share-based payment should be measured by reference to the fair value of goods and services received;

- If the equity-settled share-based payment is to employees (or those similar to employees), the transaction should be measured by reference to the fair value of the equity instruments granted at the date of grant;

- For cash-settled share-based payments, the fair value should be determined at each reporting date; and

- If the share-based payment can be settled in cash or in equity, then the equity component should be measured at the grant date only, but the cash component is measured at each reporting date.

In general, then, transactions in which goods or services are received as consideration for equity instruments of the entity are to be measured at the fair value of the goods or services received by the reporting entity. However, if their value cannot be readily determined (as the standard suggests is the case for employee services) they are to be measured with reference to the fair value of the equity instruments granted.

In the case of transactions with parties other than employees, there is a rebuttable presumption that the fair value of the goods or services received is more readily determinable than is the value of the shares granted. This follows logically from the fact that, in arm's-length transactions, it should be the case that the value which the entity has received would be readily apparent (whether merchandise, plant assets, personal services, etc.) and that such data would not take undue effort to gather and utilise. Arguments to the contrary raise basic questions about managerial performance and corporate governance and can rarely be given much credence.

Additional guidance is also provided in the standard with regard to situations in which the entity cannot identify specifically some or all of the goods or services received. If the identifiable consideration received (if any) appears to be less than the fair value of the equity instruments granted or liability incurred, typically this situation indicates that other consideration (i.e., unidentifiable goods or services) has also been (or will be) received. The entity should measure the unidentifiable goods or services received (or to be received) at the grant date as the difference between the fair value of the share-based payment given or promised and the fair value of any identifiable goods or services received (or to be received). However, for cash-settled transactions, the liability is remeasured at each reporting date until it is settled.

Given the added challenge of estimating fair value for non-traded shares, this was a major point of contention among those responding to the initial draft standard. Realistically, entities granting share-based compensation to executives and other employees almost always have a sense of the value being transferred, for otherwise these bargained transactions would not make business sense, nor would they satisfy the demands or expectations of the recipients.

Where payment is made or promised in the reporting entity's shares only, the value is determined using a fair value technique that computes the cost at the date of the transaction, which is not subsequently revised, except for revised terms which increase the amount of fair value to be transferred to the recipients. In contrast, for cash-settled transactions, the liability should be remeasured at each reporting date until it is settled.

For transactions measured at the fair value of the equity instruments granted (such as compensation transactions with employees), fair value is estimated at the grant date. A point of contention here has often been whether the grant date or exercise date is the more appropriate reference point, but the logic of the former is that the economic decision, and the employee's contractual commitment, were made at the grant date, and the timing of subsequent exercise (or, in some cases, forfeiture) is not indicative of the bargained-for value of the transaction. The grant date is when the employee accepts the commitment, not when the offer is first made. Accordingly, IFRS 2 requires the use of the grant date to ascertain the fair value to be associated with the transaction.

When share capital is issued immediately, measurement is not generally difficult. For example, if 100 shares having a fair (market) value of €33 per share are given outright to an employee, the compensation cost is simply computed as €3,300. Since the grant vests immediately (no future service is demanded from the recipient), the expense is immediately reported.

The more problematic situation is when employees (or others) are granted options to later acquire shares that permit exercise over a defined time horizon. The holders' ability to wait and later assess the desirability of exercising the options has value—and the lengthier the period until the options expire, the more likely the underlying shares will increase in value, and thus the greater is the value of the option. Even if the underlying shares are publicly traded, the value of the options will be subject to some debate. Only when the options themselves are traded (which is rarely the case with employee share options, which are restricted to the grantees themselves) will fair value be directly determinable by observation. If market options on the entity's shares do trade, the value will likely exceed that to be attributed to non-tradable employee share options, even if they have nominally similar terms (exercise dates, prices, etc.).

The standard holds that, to estimate the fair value of a share option in the likely instance where an observable market price for that option does not exist, an option pricing model should be used. IFRS 2 does not specify which particular model should be used. The entity must disclose the model used, the inputs to that model, and various other information bearing on how fair value was computed. In practice, these models are all fairly sophisticated and complicated (although commercially available software promises to ease the computational complexities) and a number of the variables have inherently subjective aspects.

One issue that has to be dealt with involves the tax treatment of options, which varies across jurisdictions. In most instances, the tax treatment will not comply with the fair value measurement mandated under IFRS 2, and thus there will be a need for specific guidance as to the accounting for the tax effects of granting the options and of the ultimate exercise of those options, if they are not forfeited by the option holders. This is described later in this discussion.

In respect of the appropriate tax treatment of share-based payments, the Basis for Conclusions of IFRS 2 notes that in jurisdictions where a tax deduction is given, the measurement of the tax deduction does not always coincide with that of the accounting deduction. Where the tax deduction is in excess of the expense reported in the statement of profit or loss and other comprehensive income, the excess is taken directly to equity.

RECOGNITION AND MEASUREMENT

The entity recognises the goods or services received or acquired in a share-based payment transaction when ownership of the goods passes, or when the services have been rendered. A corresponding increase in equity is recognised if the goods or services were received in a transaction that was settled through the issuance of shares, or as an increase in liabilities if the goods or services were acquired in a cash-settled share-based payment transaction. If the goods or services acquired do not meet the qualification criteria for recognition as an asset, the transaction should be recognised as an expense.

Recognition When There are Vesting Conditions

In certain instances, equity instruments which vest immediately are granted to employees; as such, these instruments immediately accrue to the employees. In essence, this means that the employees are not required to provide any additional service to the entity or meet any performance condition before they are unconditionally entitled to those equity instruments. In the absence of facts that contradict this position, the entity is required to recognise the associated employee cost in full, with a corresponding increase in equity. It is presumed that the services rendered by the employee as consideration for the equity instruments have already been received by the grant date.

With equity instruments that do not vest until the employee completes a specified period of service or meets a specified performance condition, the entity assumes that the services rendered by the employee, as consideration for those equity instruments, will only be received in the future. As such, the entity accounts for those services as they are rendered over the vesting period with a corresponding increase in equity.

EQUITY-SETTLED SHARE-BASED PAYMENTS

Goods and Services

An entity is required to measure the goods or services received (debit) and the corresponding increase in equity (credit) based on the fair value of the goods or services received. In some instances, the fair value of the goods or services received cannot be estimated reliably, and in such a situation the entity should measure the value of the goods or services and the related increase in equity based on the fair value of the equity instruments granted. Fair value is determined as of the date when the entity obtains the goods or the service is rendered.

Employees

In respect of transactions with employees and other providers of similar services, the entity should determine the fair value of the services based on the fair value of the instruments issued. The presumption in such an instance is that one cannot reliably estimate the fair value of the services received.

The value of the instruments is determined at the grant date of such instruments. All market conditions and non-vesting conditions must be considered when the fair value of the instrument is calculated on the grant date with no subsequent adjustment for a different outcome. Service and non-market performance conditions must be considered when the number of shares that is expected to vest is estimated.

Service Conditions

A service condition is when a grant of shares or share options to an employee is conditional on the employee remaining in the entity's employment for a specified period of time. Service conditions are considered in determining the fair value of the shares or share options at the grant date. At each measurement date, the estimate of the number of equity instruments should be revised to equal the amount that will actually be issued to the employees or other parties. At the vesting date, the actual number of shares that vest is taken into consideration in the final estimation.

Market and Non-Market Performance Conditions

Market and non-market performance conditions may be included in the share-based transaction. An example of a market performance condition is a specified increase in the entity's credit rating. Market conditions are included in the estimation of the fair value on the grant date.

A non-market performance condition is, for example, an entity achieving a specified growth in revenue. Non-market conditions are taken into account in determining the quantity of the instruments that will be issued and not in the fair value of the instrument on the grant date.

A summary of the conditions can be categorised as depicted in the Implementation Guide to the Standard as shown below:

| Summary of conditions that determine whether a counterparty receives an equity instrument granted | ||||||

| Vesting conditions | Non-vesting conditions | |||||

| Service conditions | Performance conditions | |||||

| Performance conditions that are market conditions | Other performance conditions | Neither the entity nor the counterparty can choose whether the condition is met | Counterparty can choose whether to meet the condition | Entity can choose whether to meet the condition | ||

| Example conditions | Requirement to remain in service for three years | Target based on the market price of the entity's equity instruments | Target based on a successful initial public offering with a specified service requirement | Target based on a commodity index | Paying contributions towards the exercise price of a share-based payment | Continuation of the plan by the entity |

| Include in grant date fair value? | No | Yes | No | Yes | Yes | Yes(a) |

| Accounting treatment if the condition is not met after the grant date and during the vesting period | Forfeiture. The entity revises the expense to reflect the best available estimate of the number of equity instruments expected to vest | No change to accounting. The entity continues to recognise the expense over the remainder of the vesting period | Forfeiture. The entity revises the expense to reflect the best available estimate of the number of equity instruments expected to vest | No change to accounting. The entity continues to recognise the expense over the remainder of the vesting period | Cancellation. The entity recognises immediately the amount of the expense that would otherwise have been recognised over the remainder of the vesting period | Cancellation. The entity recognises immediately the amount of the expense that would otherwise have been recognised over the remainder of the vesting period |

| (paragraph 19) | (paragraph 21) | (paragraph 19) | (paragraph 21A) | (paragraph 28A) | (paragraph 28A) | |

| (a) In the calculation of the fair value of share-based payment, the probability of continuation of the plan by the entity is assumed to be 100 per cent. | ||||||

It would also be appropriate to consider the treatment for reload feature at this juncture. IFRS 2 prescribes that the reload feature shall not be considered when estimating the fair value of options granted at the measurement date. Such reload options, shall be treated as a fresh grant of option, if and when the reload option is subsequently granted.

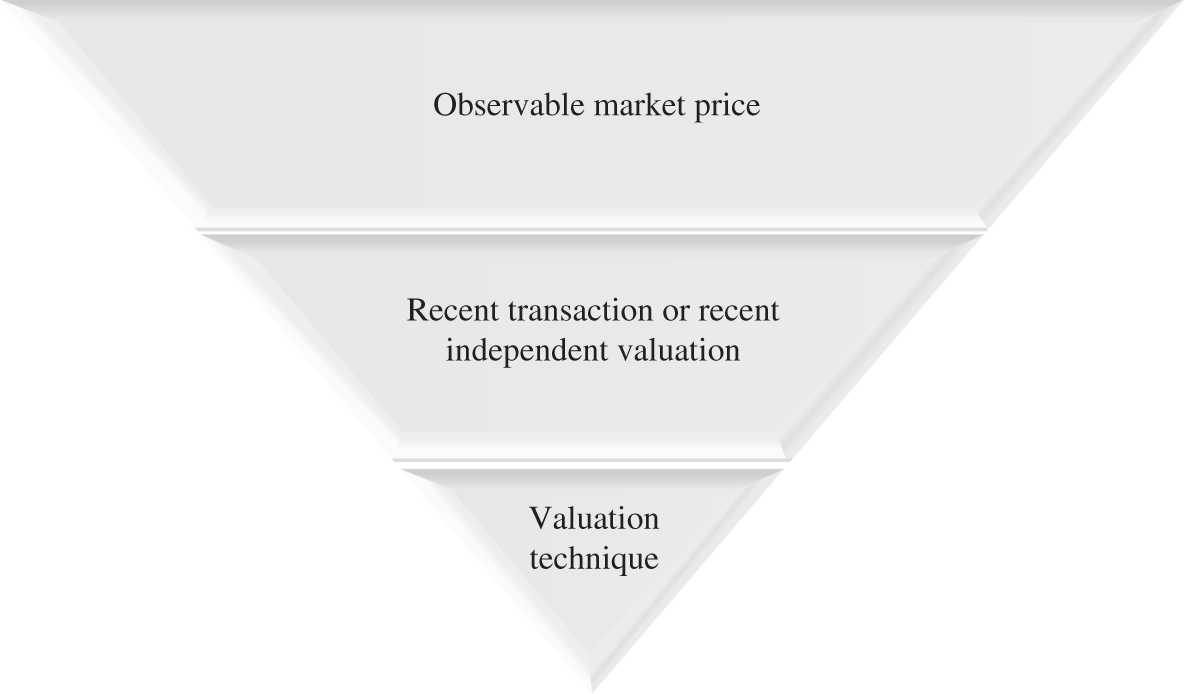

Measurement of Fair Value

If the fair value of the goods or services received cannot be measured reliably, the fair value of the shares, share options or equity-settled share appreciation rights must be determined using the three-tier measurement hierarchy included in Figure 17.1.

Observable market price of the equity instruments granted is only used if such a price is available. This is unlikely to be applicable where an entity is not listed on a stock exchange. In the absence of observable market prices, observable market data may be used, such as:

Figure 17.1 Fair value hierarchy

- A recent transaction in the entity's shares.

- A recent independent fair valuation of the entity or its principal assets.

If the value of shares cannot be measured by an observable market price, or reliable measurement under level two is impractical, the shares are measured indirectly by using a valuation method. A valuation method uses, to the greatest extent practicable, market data that can be externally verified to arrive at a value at which the equity instruments under consideration would be exchanged at the grant date between knowledgeable willing parties. Similarly, share options and share appreciation rights are valued under level three of the hierarchy by using an option pricing model. This would, in effect, be a directors' valuation, and as such the directors should apply their judgement in determining the amount. The valuation method should, however, comply with generally accepted methodologies for valuing equity instruments.

For a detailed example of calculating fair value for employee share options, see Appendix B of IFRS 2 and the Appendix of this chapter.

Modifications and Cancellations to the Terms and Conditions

Changes in the economic conditions or circumstances of the entity may sometimes make an entity change the vesting conditions that are attached to employee share ownership schemes. The entity may modify the vesting conditions in a manner that is beneficial to the employee (for example, by reducing the exercise price of an option, or reducing the vesting period, or by modifying or eliminating a performance condition). Modification to vesting conditions is only considered if it is beneficial to the employees.

Such changes should be taken into account in accounting for the share-based payment transaction as illustrated in Figure 17.2.

If the Modification Increases the Fair Value

If the modification to the scheme increases the fair value of the equity instruments granted, or the number of equity instruments granted, the entity should account for the incremental total fair value equity instruments granted as a share-based payment expense. The incremental fair value is the difference between the fair value of the modified equity instrument and the original equity instrument on the date of the modification. The balance of the original equity instruments granted is recognised over the remainder of the original vesting period.

Figure 17.2 Modifications and cancellations to the terms and conditions

On January 1, 202X+1, the share price of Brno shares decreased to €18. The directors expressed concern that their options carried no value, and requested that the entity decrease the consideration price to be paid to €15. The entity decreased the purchase consideration from €20 to €15; a valuation expert calculated the fair value of the €20 share option to be €2 and a €15 share option to be €8 as at January 1, 202X. All the directors exercised their options on December 31, 202X+1.

| Calculation | |

| Original issue | € |

| Total benefit | 11,000 |

| (10 directors × 100 options each × €11) | |

| Previously recognised | 5,500 |

| Amount still to be recognised | 5,500 |

| Modification |

Since the incremental fair value is positive (€8 − €2), the value of the modification based on the incremental fair value is included in the share-based payment expense. The value is €6,000 [10 directors × 100 options each × (€8 − €2) incremental fair value of options at modification date × 1/1 completed service period].

| Current year expense | ||

| €11,000 (original issue) + €6,000 (modification) − €5,500 (prior year) = €11,500 | ||

| Journals | ||

| December 31, 202X+1 | € | € |

| Employment cost (P/L) | 11,500 | |

| Equity reserve (Equity) | 11,500 | |

| Accounting for the 202X+1 employment cost. | ||

| Bank (SFP) | 15,000 | |

| (10 directors × 100 shares × €15) | ||

| Equity reserve (Equity) | 17,000 | |

| [€5,500 (20X1) + €11,500 (202X+1)] | ||

| Share capital (Equity) | 1,000 | |

| (10 directors × 100 Brno shares) | ||

| Share premium (Equity) | 31,000 | |

| Accounting for the issue of the share capital to honour the shares issued. | ||

If the Modification Decreases the Fair Value

If the modification reduces the total fair value of the share-based payment arrangement, or the terms are changed in such a way that the arrangement is no longer for the benefit of the employee, the entity is still required to account for the services received as consideration for the equity instruments granted as if that modification had not occurred. No changes are therefore made to the accounting for the share-based payment arrangement. Therefore, in the above example, only the €11,000 expense relating to the original issue would be recognised over the vesting period.

Cancellations and Settlements

Where an entity cancels or settles an equity-settled share-based payment award, it accounts for such cancellation or settlement as an acceleration of vesting. The entity, therefore, recognises immediately in profit or loss the amount that otherwise would have been recognised for services received over the remainder of the vesting period.

Employee Share Options with Graded Vesting Characteristics and Service Conditions

Under IFRS 2, the compensation expense for share options with graded vesting characteristics and service conditions must be made on an accelerated attribution basis. IFRS does not permit the straight-line method for attribution of the compensation cost of share options with service conditions and graded vesting characteristics. A graded vesting plan assigns the share options to the period in which they vest. This is because IFRS 2 views each tranche of vesting as a separate grant for which services have been provided since the date of the original grant.

The mandatory use of the accelerated amortisation method for share options with graded vesting features results in a higher compensation cost in the earlier years of the vesting period as shown in the example below.

CASH-SETTLED SHARE-BASED PAYMENTS

Generally, when goods and services are provided, the seller of the goods and services is paid in cash and the transaction ends. In some cases, the seller expects that the value of the buyer's entity will increase substantially because of the unique nature of or value added by the goods and services provided. In such cases, the seller might prefer to receive a share in the appreciation of the buyer's value and thus structures the “price and payment” to incorporate payment by way of shares in the buyer's entity. Such arrangements amount to a share-based payment. If the buyer does not want to dilute its shareholding, but still wants to pass on a portion of the appreciation to the seller, they could enter into a cash-settled share-based payment. In other words, the cash amount ultimately paid is based on the value of the shares of the buyer.

By the nature of such settlement, these transactions are long term (beyond 12 months). For instance, if they are cash settled immediately or within the financial year, the same accounting entries would be made as for any other cash transaction and recognised as such. However, the objective in cash-settled share-based transactions is to benefit from the potential increase in value of the buyer entity. Therefore, in such transactions an entity should recognise the goods or services either as assets or expenses as the case may be and simultaneously recognise a liability incurred at the fair value of the liability. Until the liability is settled, the entity shall remeasure the fair value of the liability at the end of each reporting period and at the date of settlement. Any changes in fair value of the liability shall be recognised in profit or loss for the period.

In case of services rendered in exchange for share appreciation rights, it may vest immediately or after fulfilment of service conditions.

For example, employees may receive share appreciation rights as part of their remuneration package. In some instances, these share appreciation rights vest immediately, and the employees are not required to complete a specified period of service to become entitled to the cash payment. In these instances, the entity shall immediately recognise the services received and a liability to pay for those services.

If the share appreciation rights do not vest until the employees have completed a specified period of service, the entity shall recognise the services received and the corresponding liability as the employees render services over the period required.

Measurement

Fair value of the liability is measured (initially, and at each subsequent reporting period) by applying an option pricing model, taking into account the terms and conditions on which the share appreciation rights were granted and the extent to which the services required have been rendered. If the contract also includes services, then the extent of service provided shall also be considered.

Treatment of Vesting and Non-Vesting Conditions

A cash-settled share-based payment transaction might be conditional upon satisfying specified vesting conditions as below:

- Performance conditions—Such as the entity achieving a specified growth in profit or a specified increase in the entity's share price.

- Market conditions—Such as attaining a specified share price or a specified amount of intrinsic value of a share option and the like.

If the vesting conditions are performance based, then while estimating the fair value of liability, the value is not changed, but the number of awards of “rights” included in the measurement is adjusted.

The following steps will be useful in this regard:

- Recognise an amount for the goods or services received during the vesting period.

- That amount shall be based on the best available estimate of the number of awards that are expected to vest.

- Revise that estimate, if necessary, if subsequent information indicates that the number of awards that are expected to vest differs from previous estimates.

- On the vesting date, finally revise the estimate to equal the number of awards that ultimately vested.

If the vesting conditions are market based, then the fair value is changed based on the market price every time the estimate is remeasured and at the end of the reporting date and at final settlement.

Share-Based Payment Transactions with a Net Settlement Feature for Withholding Tax Obligations

The tax laws or regulations in some countries may require the payee to withhold an associated tax at the time of payment and pay such money directly to the tax authorities on behalf of the recipient. Simply because a payment is made by way of shares (share-based payment) may not remove such withholding tax obligations. The entity that makes a share-based payment may well still have the obligation to withhold tax and pay it to government.

To fulfil this obligation and using the example of a share-based payment to employees, the terms of the share-based payment arrangement may permit or require the entity to withhold the number of equity instruments equal to the monetary value of the employee's tax obligation from the total number of equity instruments that otherwise would have been issued to the employee or other sellers of goods and services upon exercise (or vesting) of the share-based payment. This arrangement is called the “net settlement feature.”

The payment made shall be accounted for as a deduction from equity for the shares withheld, except to the extent that the payment exceeds the fair value at the net settlement date of the equity instruments withheld. Any excess is to be recorded as an expense. In spite of the fact that payment to the tax authorities will involve a cash payment, transactions with “net settlement features” shall be classified in their entirety as an equity-settled share-based payment transaction if they would have been so classified in the absence of the net settlement feature.

The entity shall disclose an estimate of the amount that it expects to transfer to the tax authority to settle the employee's (or other sellers') tax obligation when it is necessary to inform users about the future cash flow effects associated with the share-based payment arrangement.

Classification in its entirety as equity-settled share-based payment is allowed only where the net settlement is because of a tax obligation. It does not apply to:

- A share-based payment arrangement with a net settlement feature for which there is no obligation on the entity under tax laws or regulations to withhold an amount for an employee's tax obligation associated with that share-based payment; or

- Any equity instruments that the entity withholds in excess of the employee's tax obligation associated with the share-based payment (i.e., the entity withheld an amount of shares that exceeds the monetary value of the employee's tax obligation). Such excess shares withheld shall be accounted for as a cash-settled share-based payment when this amount is paid in cash (or other assets) to the employee.

Modifications to the Terms and Conditions of a Cash-Settled Share-Based Payment

IFRS 2 did not originally specifically address situations where a cash-settled share-based payment changes to an equity-settled share-based payment because of modifications of the terms and conditions. The IASB subsequently introduced the following clarifications.

On such modifications, the original liability recognised in respect of the cash-settled share-based payment is derecognised and the equity-settled share-based payment is recognised at the modification date fair value to the extent services have been rendered up to the modification date.

Any difference between the carrying amount of the liability as at the modification date and the amount recognised in equity at the same date would be recognised in profit and loss immediately. Guidance on the above is set out in paragraphs B44A–B44C in Appendix B to IFRS 2.

SHARE-BASED PAYMENT TRANSACTIONS WITH CASH ALTERNATIVES

Some share-based payment agreements give the parties a choice of settling the transaction in cash or through the transfer of equity instruments. The choice could be with the counterparty or with the entity.

Where the counterparty has the right to choose and the settlement is not akin to a cash settled share appreciation rights, the grant of the option is similar to a compound financial instrument and the debt component and the equity component are separately to be computed. For the debt component, the entity shall recognise the goods or services acquired, and a liability to pay for those goods or services, as the counterparty supplies goods or renders service, in accordance with the requirements applying to cash-settled share-based payment transactions. For the equity component (if any), the entity shall recognise the goods or services received, and an increase in equity, as the counterparty supplies goods or renders service, in accordance with the requirements applying to equity-settled share-based payment transactions.

Where the entity holds the right to choose to settle by way of equity or cash, then if the entity has a present obligation to settle in cash, it shall account for the transaction in accordance with the requirements applying to cash-settled share-based payment transactions. Otherwise, the entity accounts for the same in accordance with the requirements applying to equity-settled shared based payment transactions.

Where a choice exists for settlement in cash at the value of equity at the time of settlement (similar to a cash settled share appreciation rights), the transaction is accounted for as a cash-settled share-based payment transaction unless either of the following criteria is met:

- There has been a past practice of settling obligations by issuing equity instruments (which can be demonstrated).

- The choice has no commercial substance because the cash settlement amount bears no relationship to, and is likely to be lower in value than, the fair value of the equity instrument. As such, the likelihood of the settlement taking place in cash is, at best, very remote.

If either of these two criteria is met, then the entity can account for the transaction as an equity-settled share-based payment transaction.

SHARE-BASED TRANSACTIONS AMONG GROUP ENTITIES

The 2009 amendments to IFRS 2 incorporated the guidance contained previously in IFRIC 11 (and IFRIC 11, Group and Treasury Share Transactions, accordingly, was withdrawn). For share-based transactions among group entities, in its separate or individual financial statements, the entity receiving the goods or services should measure the expense as either an equity-settled or cash-settled share-based transaction by assessing:

- The nature of the awards granted; and

- Its own rights and obligations.

The entity receiving goods or services may recognise a different amount than the amount recognised by the consolidated group or by another group entity settling the share-based payment transaction.

The entity should measure the expense as an equity-settled share-based payment transaction (and remeasure this expense only for changes in vesting conditions) when:

- The awards granted are its own equity instruments; or

- The entity has no obligation to settle the share-based payment transaction.

In all other cases, the expense should be measured as a cash-settled share-based payment transaction. In group transactions based on repayment arrangements that require the payment of the equity instruments to the suppliers of goods or services, the entity receiving goods or services should recognise the share-based payment expense regardless of repayment arrangements.

For example, there are various circumstances whereby a parent entity's equity shares are granted to employees of its subsidiaries. One common situation occurs where the parent is publicly traded but its subsidiaries are not (e.g., where the subsidiaries are wholly owned by the parent company), and thus the parent company's shares are the only “currency” that can be used in share-based payments to employees. If the arrangement is accounted for as an equity-settled transaction in the consolidated (group) financial statements of the parent company, the subsidiary is to measure the services under the equity-settled share-based payment transaction. A capital contribution by the parent is also recognised by the subsidiary in such situations.

Furthermore, if the employee transfers from one subsidiary to another, each is to measure compensation expense by reference to the fair value of the equity instruments at the date the rights were granted by the parent, allocated according to the relative portion of the vesting period the employee works for each subsidiary. There is no remeasurement associated with the transfer between entities. If a vesting condition other than a market condition (defined by IFRS 2, Appendix A) is not met and the share-based compensation is forfeited, each subsidiary adjusts previously recognised compensation cost to remove cumulative compensation cost from each of the subsidiaries.

On the other hand, if the subsidiary grants rights to its parent company's shares to the subsidiary's employees, that entity accounts for this as a cash-settled transaction. This means the obligation is reported as a liability and adjusted to fair value at each reporting date.

In group transactions based on repayment arrangements that require the payment of the equity instruments to the suppliers of goods or services, the entity receiving goods or services should recognise the share-based payment expense regardless of repayment arrangements.

DISCLOSURE

IFRS 2 imposes extensive disclosure requirements, calling for an analysis of share-based payments made during the year, of their impact on earnings and financial position, and of the basis upon which fair values were measured. An entity should disclose information enabling users of the financial statements to understand the nature and extent of share-based payment transactions that occurred during the period.

Each type of share-based payment transaction that existed during the year must be described, giving vesting requirements, the maximum term of the options and the method of settlement (but entities that have several “substantially similar” schemes may aggregate this information). The movement (i.e., changes) within each scheme must be analysed, including the number of share options and the weighted-average exercise price for the following:

- Outstanding at the beginning of the year;

- Granted during the year;

- Forfeited during the year;

- Exercised during the year (plus the weighted-average share price at the time of exercise);

- Expired during the year;

- Outstanding at the end of the period (plus the range of exercise prices and the weighted-average remaining contractual life);

- Exercisable at the end of the period.

The entity must disclose the total expense recognised in the statement of profit or loss and other comprehensive income arising from share-based payment transactions, and a subtotal of that part which was settled by the issue of equity. Where the entity has liabilities arising from share-based payment transactions, the total amount at the end of the period must be separately disclosed, as must be the total intrinsic value of those options that had vested.

The fair value methodology disclosures apply to new instruments issued during the reporting period, or old instruments modified in that time. Regarding share options, the entity must disclose the weighted-average fair value, plus details of how the fair value was measured. These will include the option pricing model used, the weighted-average share price, the exercise price, expected volatility, option life, expected dividends, the risk-free interest rate and any other inputs. The measurement of expected volatility must be explained, as must be the manner in which any other features of the option were incorporated in the measurement.

Where a modification of an existing arrangement has taken place, the entity should provide an explanation of the modifications, and disclose the incremental fair value and the basis on which that was measured (as above).

Where a share-based payment was made to a non-employee, such as a vendor, the entity should confirm that fair value was determined directly by reference to the market price for the goods or services.

If equity instruments other than share options were granted during the period, the number and weighted-average fair value of these should be disclosed together with the basis for measuring fair value, and if this was not market value, then how it was measured. The disclosure should cover how expected dividends were incorporated into the value and what other features were incorporated into the measurement.

Financial Statement Presentation under IFRS

The following is an illustration of the treatment of equity that may be required in the financial statements.

EXAMPLES OF FINANCIAL STATEMENT DISCLOSURES

| Exemplum Reporting PLC Financial Statements For the Year Ended December 31, 202X | ||||

| xx. Share-based payments | ||||

| [A description of each type of share-based payment arrangement that existed at any time during the period, including the general terms and conditions of each arrangement, such as vesting requirements, the maximum term of options granted and the method of settlement (e.g., whether in cash or equity)]. | ||||

| 202X | 202X-1 | |||

| Options | Weighted-average exercise price | Options | Weighted-average exercise price | |

| Outstanding at the beginning of the period | X | X | X | X |

| Granted during the period | X | X | X | X |

| Forfeited during the period | X | X | X | X |

| Exercised during the period | X | X | X | X |

| Expired during the period | X | X | X | X |

| Outstanding at the end of the period | X | X | X | X |

| Exercisable at the end of the period | X | X | X | X |

| The weighted average share price of share options exercised during the period at the date of exercise was €X. | ||||

| Share options outstanding at December 31, 202X had a weighted average exercise price of €X and a weighted average remaining contractual life of X years. | ||||

| [Disclose information that enables users of the financial statements to understand how the fair value of the goods or services received, or the fair value of the equity instruments granted, during the period was determined.] | ||||

| The fair value of the share-based payment instruments were determined by the Black–Scholes–Merton model. The effect of non-transferability has been taken into account by adjusting the expected life of the instruments. Volatility was calculated based on the share price volatility over a similar period preceding the grant date. | ||||

| Inputs into the model | X | |||

| Grant date share price | X | |||

| Exercise price | X | |||

| Expected volatility | X% | |||

| Option life | X years | |||

| Dividend yield | X% | |||

| Risk-free interest rate | X% | |||

| 202X | 202X-1 | |||

| Total expense recognised from share-based payment transactions | X | X | ||

| Equity-settled share-based payment expense | X | X | ||

| Share-based payment liability | X | X | ||

| Intrinsic value of liabilities arising from vested rights | X | X | ||

US GAAP COMPARISON

Stock Compensation is found in Topic 718 under US GAAP Codification. ASU No. 2018-07 Compensation-Stock Compensation (Topic 718) amends the way that non-employee stock compensation is accounted for under US GAAP. Historically, fair value of the stock was used, now the compensation is calculated similarly using the grant date to be consistent with employee-based compensation and evidence of the completion of the service or delivery of the product which is consistent with the new revenue recognition standard. This “applies to all share-based payment transactions in which a grantor acquires goods or services to be used or consumed in a grantor's own operations by issuing share-based payment awards” and is effective for years beginning after December 15, 2018 for public entities and December 15, 2019 for all other entities.

APPENDIX: EMPLOYEE SHARE OPTIONS VALUATION EXAMPLE UNDER IFRS

An entity should expense the value of share options granted to an employee over the period during which the employee is earning the option—that is, the period until the option vests (becomes unconditional). If the options vest (become exercisable) immediately, the employee receiving the grant cannot be compelled to perform future services, and accordingly the fair value of the options is compensation in the period of the grant. More commonly, however, there will be a period (several years, typically) of future services required before the options vest (and may be exercised); in those cases, compensation is to be recognised over that vesting period. There are two practical difficulties with this:

- Estimating the value of the share options granted (true even if vesting is immediate); and

- Allowing for the fact that not all options initially granted will ultimately vest or, if they vest, be exercised by the holders.

IFRS 2 requires that where directly observable market prices are not available (which is virtually always the case for employee share options, since they cannot normally be sold), the entity must estimate fair value using a valuation technique that is “consistent with generally accepted valuation methodologies for pricing financial instruments, and shall incorporate all factors and assumptions that knowledgeable, willing market participants would consider in setting the price.” No specific valuation method is endorsed by the standard, however.

Appendix B of the standard notes that all acceptable option pricing models take into account:

- The exercise price of the option;

- The current market price of the share;

- The expected volatility of the share price;

- The dividends expected to be paid on the shares;

- The risk-free interest rate; and

- The life of the option.

In essence, the grant date value of the share option is the current market price of the share, less the present value of the exercise price, less the dividends that will not be received during the vesting period, adjusted for the expected volatility. The time value of money, as is well understood, arises because the holder of an option is not required to pay the exercise price until the exercise date. Instead, the holder of the option can invest his funds elsewhere, while waiting to exercise the option. According to IFRS 2, the time value of money component is determined by reference to the rate of return available on risk-free securities. If the share pays a dividend or is expected to pay a dividend during the life of the option, the value to the holder of the option from delaying payment of the exercise price is only the excess (if any) of the return available on a risk-free security over the return available from exercising the option today and owning the shares. The time value of money component for a dividend-paying share equals the discounted present value of the expected interest income that could be earned less the discounted present value of the expected dividends that will be forgone during the expected life of the option.

The time value associated with volatility represents the ability of the holder to profit from appreciation of the underlying shares while being exposed to the loss of only the option premium, and not the full current value of the shares. A more volatile share has a higher probability of big increases or decreases in price, compared with one having lower volatility. As a result, an option on a highly volatile share has a higher probability of a big payoff than an option on a less volatile share, and so has a higher value relating to the volatility fair value component. The longer the option term, the more likely, for any given degree of volatility, that the share price will appreciate before option expiration, making exercise attractive. Greater volatility, and a longer term, each contribute to the value of the option.

Volatility is the measure of the amount by which a share's price fluctuates during a period. It is expressed as a percentage because it relates share price fluctuations during a period to the share's price at the beginning of the period. Expected annualised volatility is the predicted amount that is the input to the option pricing model. This is calculated largely from the share's historical price fluctuations.

To illustrate this basic concept, assume that the present market price of the underlying shares is €20 per share, and the option plan grants the recipient the right to purchase shares at today's market price at any time during the next five years. If a risk-free rate, such as that available on government treasury notes having maturities of five years is 5%, then the present value of the future payment of €20 is €15.67 {= [€20 ÷ (1.05)5]}, which suggests that the option has a value of (€20 − €15.67 =) €4.33 per share before considering the value of lost dividends. If the shares are expected to pay a dividend of €0.40 per share per year, the present value of the dividend stream that the option holder will forgo until exercise five years hence is about €1.64, discounting again at 5%. Therefore, the net value of the option being granted, assuming it is expected to be held to the expiration date before being exercised, is (€4.33 − €1.64 =) €2.69 per share. (Although the foregoing computation was based on the full five-year life of the option, the actual requirement is to use the expected term of the option, which may be shorter.)

Commercial software is readily available to carry out these calculations. However, accountants must understand the theory underlying these matters so that the software can be appropriately employed, and the results verified. Independent auditors, of course, have additional challenges in verifying the financial statement impacts of share-based compensation plans.

Estimating volatility does, however, involve special problems for unlisted or newly listed companies, since the estimate is usually based on an observation of past market movements, which are not available for such entities. The Basis for Conclusions says that IASB decided that, nonetheless, an estimate of volatility should still be made. Appendix B of IFRS 2 states that newly listed entities should compute actual volatility for whatever period this information is available and should also consider volatility in the prices of shares of other companies operating in the same industry. Unlisted entities should consider the volatility of prices of listed entities in the same industry, or, where valuing them on the basis of a model, such as net earnings, should use the volatility of the earnings.

IASB considered the effect of the non-transferability on the value of the option. The standard option pricing models (such as Black–Scholes) were developed to value traded options and do not take into account any effect on value of non-transferability. It came to the view that non-transferability generally led to the option being exercised early, and that this should be reflected in the expected term of the option, rather than by any explicit adjustment for non-transferability itself.

The likelihood of the option vesting is a function of the vesting conditions. IASB concluded that these conditions should not be factored into the value of the option but should be reflected in calculating the number of options to be expensed. For example, if an entity granted options to 500 employees, the likelihood that only 350 would satisfy the vesting conditions should be used to determine the number of options expensed, and this should be subsequently adjusted in the light of actual experience as it unfolds.

Employee Share Options: Valuation Models

IFRS 2 fully imposes a fair value approach to measuring the effect of share options granted to employees. It recognises that directly observable prices for employee options are not likely to exist, and thus that valuation models will have to be employed in almost all instances. The standard discusses the relative strengths of two types of approaches: the venerable Black-Scholes (now called Black–Scholes–Merton, or BSM) option pricing model, designed specifically to price publicly traded European-style options (exercisable only at the expiration date) and subject to criticism as to possible inapplicability to non-marketable American-style options; and the mathematically more challenging but more flexible lattice models, such as the binomial. IFRS 2 does not dictate choice of model and acknowledges that the Black-Scholes model may be validly applied in many situations.

To provide a more detailed examination of these two major types of options valuation approaches, several examples are presented below.

Both valuation models (hereinafter referred to as BSM and binomial) must take into account the following factors, at a minimum:

- Exercise price of the option.

- Expected term of the option, taking into account several things, including the contractual term of the option, vesting requirements and post-vesting employee termination behaviours.

- Current price of the underlying share.

- Expected volatility of the price of the underlying share.

- Expected dividends on the underlying share.

- Risk-free interest rate(s) for the expected term of the option.

In practice, there are likely to be ranges of reasonable estimates for expected volatility, dividends and option term. The closed form models, of which BSM is the most widely regarded, are predicated on a set of assumptions that remain invariant over the full term of the option. For example, the expected dividend on the shares on which options are issued must be a fixed amount each period over the full term of the option. In the real world, of course, the condition of invariability is almost never satisfied. For this reason, current thinking is that a lattice model, of which the binomial model is an example, would be preferred. Lattice models explicitly identify nodes, such as the anniversaries of the grant date, at each of which new parameter values can be specified (e.g., expected dividends can be independently defined each period).

Other features that may affect the value of the option include changes in the issuer's credit risk, if the value of the awards contains cash settlement features (i.e., if they are liability instruments), and contingent features that could cause either a loss of equity shares earned or reduced realised gains from sale of equity instruments earned, such as a “clawback” feature (for example, where an employee who terminates the employment relationship and begins to work for a competitor is required to transfer to the issuing entity shares granted and earned under a share-based payment arrangement).

Before presenting specific examples of accounting for share options, simple examples of calculating the fair value of options using both the BSM and the binomial methods are provided. First, an example of the BSM, closed-form model is provided.

BSM actually computes the theoretical value of a “European” call option, where exercise can occur only at the expiration date. “American” options, which describes most employee share options, can be exercised at any time until expiration. The value of an American-style option on dividend-paying shares is generally greater than a European-style option, since pre-exercise, the holder does not have a right to receive dividends that are paid on the shares. (For non-dividend-paying shares, the values of American and European options will tend to converge.) BSM ignores dividends, but this is readily dealt with, as shown below, by deducting from the computed option value the present value of the expected dividend stream over the option holding period.

BSM also is predicated on constant volatility over the option term, which available evidence suggests may not be a wholly accurate description of share price behaviour. On the other hand, the reporting entity would find it very difficult, if not impossible, to compute differing volatilities for each node in the lattice model described later in this section, lacking a factual basis for presuming that volatility would increase or decrease in specific future periods.

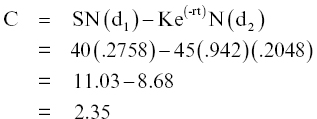

The BSM model is:

where:

| C | = | Theoretical call premium |

| S | = | Current share price |

| t | = | Time until option expiration |

| K | = | Option striking price |

| r | = | Risk-free interest rate |

| N | = | Cumulative standard normal distribution |

| e | = | Exponential term (2.7183) |

| d1 | = |  |

| d2 | = | d2 = d1 – s |

| s | = | Standard deviation of share returns |

| 1n | = | Natural logarithm |

The BSM valuation is illustrated with the following assumed facts; note that dividends are ignored in the initial calculation but will be addressed once the theoretical value is computed. Also note that volatility is defined in terms of the variability of the entity's share price, measured by the standard deviation of prices over the past three years, which is used as a surrogate for expected volatility over the next 12 months.

With these assumptions the value of the share options is approximately €2.35. This is derived from the BSM as follows:

The forgone two-year stream of dividends, which in this example are projected to be €0.50 annually, have a present value of €0.96. Therefore, the net value of this option is €1.39 (= €2.35 − 0.96).

The foregoing was a simplistic single-period, two-outcome model. A more complicated and realistic binomial model extends this single-period model into a randomised walk of many steps or intervals. In theory, the time to expiration can be broken into a large number of ever-smaller time intervals, such as months, weeks or days. The advantage is that the parameter values (volatility, etc.) can then be varied with greater precision from one period to the next (assuming, or course, that there is a factual basis for these estimates). Calculating the binomial model then involves the same three calculation steps. First, the possible future share prices are determined for each branch, using the volatility input and time to expiration (which grows shorter with each successive node in the model). This permits computation of terminal values for each branch of the tree. Secondly, future share prices are translated into option values at each node of the tree. Thirdly, these future option values are discounted and added to produce a single present value of the option, taking into account the probabilities of each series of price moves in the model.

A big advantage of the binomial model is that it can value an option that is exercisable before the end of its term (i.e., an American-style option). This is the form that employee share-based compensation arrangements normally take. IASB appears to recognise the virtues of the binomial type of model, because it can incorporate the unique features of employee share options. Two key features that should generally be incorporated into the binomial model are vesting restrictions and early exercise. Doing so, however, requires that the reporting entity will have had previous experience with employee behaviours (e.g., gained with past employee option programmes) that would provide it with a basis for making estimates of future behaviour. In some instances, there will be no obvious bases upon which such assumptions can be developed.

The binomial model permits the specification of more assumptions than does the BSM, which has generated the perception that the binomial model will more readily be manipulated so as to result in lower option values, and hence lower compensation costs, when contrasted to the BSM. But this is not necessarily the case: switching from BSM to the binomial model can increase, maintain or decrease the option's value. Having the ability to specify additional parameters, however, does probably give management greater flexibility and, accordingly, will present additional challenges for the auditors who must attest to the financial statement effects of management's specification of these variables.