CHAPTER 9

FINANCIAL STATEMENTS PREPARED BY GOVERNMENTS

Introduction

Basic Financial Statements

Management’s Discussion and Analysis

Government-Wide Financial Statements

Basis of accounting and measurement focus

Statement of Net Assets

Statement of Activities

Expense Presentation

Revenue Presentation

Extraordinary and special items

Eliminations and reclassifications

Fund Financial Statements

Governmental Fund Balance Reporting under GASBS 34

Nonspendable Fund Balance

Restricted Fund Balance

Committed Fund Balance

Assigned Fund Balance

Unassigned Fund Balance

Fund Balance Classifications

Stabilization Agreements

Fund Balance Display on the Balance Sheet

Disclosures

Budgetary Comparison Schedules

Notes and Other Disclosures

Loans

Reimbursements

Interfund Transactions—Fund Financial Statements

Intra-Entity Transactions—Government-Wide Financial Statements

Statement of Net Assets

Statement of Activities

Intra-Entity Activity

Reporting Deferred Inflows and Outflows of Resources

Display Requirements

Statement of Net Position

Net Investment in Capital Assets Component of Net Position

Restricted and Unrestricted Components of Net Position

Financial Reporting for Governmental Funds

Disclosures

Effective Date and Transition

Refundings of Debt

Nonexchange Transactions

Imposed nonexchange revenue transactions

Government-mandated nonexchange transactions and voluntary nonexchange transactions

Sales of Future Revenues and Intra-Entity Transfers of Future Revenues

Sales of future revenues

Intra-entity transfers of future revenues

Debt Issuance Costs

Leases

Initial direct costs of operating leases

Sale-leaseback transactions

Acquisition Costs Related to Insurance Activities

Lending Activities

Loan origination fees and costs

Commitment fees

Purchase of a loan or group of loans

Mortgage Banking Activities

Loan origination fees and costs

Fees relating to loans held for sale

Regulated Operations

General standards of accounting for the effects of regulation

Revenue Recognition in Governmental Funds

Use of the term deferred

Major fund criteria

Effective Date and Transition

Comprehensive Annual Financial Report

CAFR Requirements

Introductory section

Financial section

Statistical tables

Narrative Explanations

Transition

Cash Flow Statement Preparation and Reporting

When Is a Cash Flow Statement Required?

Objectives of the Statement of Cash Flows

Cash and Cash Equivalents Definitions

Classification of Cash Receipts and Cash Disbursements

Gross and net cash flows

Direct Method of Reporting Cash Flows from Operating Activities

Format of the Statement of Cash Flows

Summary

INTRODUCTION

This chapter describes some of the unique aspects of the financial statements prepared by governments. The information presented in this chapter is consistent with the financial reporting model promulgated by GASBS 34, as amended. This information also incorporates the more important guidance provided by GASB staff through the use of Questions and Answer Implementation Guides concerning the financial reporting model. While the basic financial statement elements of a balance sheet, operating statement, and in some cases cash flow statement exist in a significantly modified way for governments, there are many concepts unique to financial reporting for governments. These financial reporting concepts are discussed throughout this chapter.

This chapter also provides information and discussion on the following topics:

- Basic financial statements

- Interfund and intra-entity transactions

- Reporting deferred inflows and outflows of resources

- Comprehensive annual financial report

- Cash flow statement preparation and reporting

This chapter focuses on the overall financial reporting for governments. There are a number of specific reporting and presentation issues that relate to specific fund types. These issues are discussed in later chapters.

BASIC FINANCIAL STATEMENTS

The basic financial statements used for a governmental entity’s fair presentation in accordance with generally accepted accounting principles include both information reported on a government-wide basis and information presented on a fund basis. Certain budget to actual comparisons may also be required. Specifically, components of the basic financial reporting for the governmental entities included in the scope of the financial reporting model are as follows:

- Management’s discussion and analysis

- Basic financial statements

- Notes to the financial statements

- Required supplementary information (RSI)

Each of the elements is described more fully below.

Management’s Discussion and Analysis

Management’s discussion and analysis (MD&A) is an introduction to the financial statements that provides readers with a brief, objective, and easily readable analysis of the government’s financial performance for the year and its financial position at year-end. The analysis included in MD&A should be based on currently known facts, decisions, or conditions. For a fact to be currently known, it should be based on events or decisions that have already occurred, or have been enacted, adopted, agreed upon, or contracted. This means that governments should not include discussions about the possible effects of events that might happen. (Discussion of possible events that might happen in the future may be discussed in the letter of transmittal that is prepared as part of a Comprehensive Annual Financial Report.) MD&A should contain a comparison of current year results with those of the prior year.

GASBS 34 provides a listing of very specific topics to be included in MD&A, although governments are encouraged to be creative in presenting the information using graphs, charts, and tables. The GASB would like MD&A to be a useful analysis that is prepared with thought and insight, rather than boiler-plate material prepared by rote every year. However, the phrase “the minimum is the maximum” applies. This means that MD&A should address all of the applicable topics listed in GASBS 34, but MD&A should address only these topics. Of course, governments preparing Comprehensive Annual Financial Reports can include in the Letter of Transmittal any topic that would be precluded from being included in MD&A.

Current year information is to be addressed in comparison with the prior year, although the current year information should be the focus of the discussion. If the government is presenting comparative financial data with the prior year in the current year financial statements, the requirements for MD&A apply to only the current year. However, if the government is presenting comparative financial statements, that is, a complete set of financial statements for each year of a two-year period, then the requirements of MD&A must be met for each of the years presented. The requirements may be met by including all of the required information in the same presentation, meaning that two completely separate MD&As for comparative financial statements are not required, provided that all of the requirements relating to each of the years are met in the one discussion.

In addition, MD&A should focus on the primary government. For fund information, the analysis of balances and transactions of individual funds would normally be confined to major funds, although discussion of nonmajor fund information is not precluded. Governments must use judgment in determining whether discussion and analysis of discretely presented component unit information is included in MD&A. The judgment should be based upon the significance of an individual component unit’s significance to the total of all discretely presented component units, as well as its significance to the primary government.

The minimum requirements for MD&A are as follows:

- First, the relationship between MD&A and the letter of transmittal presented as part of a CAFR must be addressed. Including any information required in MD&A in a letter of transmittal does not fulfill any of the requirements for MD&A since MD&A is a required supplement to the basic financial statements of a government and the letter of transmittal of a CAFR is not. On the other hand, certain information that is required in MD&A may formerly have been included in the letter of transmittal. This information may be moved from the transmittal letter to MD&A. However, the Government Finance Officers Association’s (GFOA) GAFR includes guidance for the requirements of the letter of transmittal for its Certificate of Achievement for Excellence in Financial Reporting program upon adoption of GASBS 34. Governments that intend to apply for the GFOA Certificate of Achievement should make sure that they do not remove information from the letter of transmittal that is required by the Certificate Program.

- MD&A is a required supplement to the basic-financial statements of a government. These statements are frequently included in Official Statements prepared by governments when the governments are selling debt to the public. Official Statements generally include a significant amount of analytical information about the financial condition and financial performance of the government. Care must be taken that analytical information included in MD&A about currently known facts, decisions, and conditions are consistent with statements made in the Official Statement, after taking into consideration the passage of time between the issuance of financial statements and the issuance of an Official Statement.

Government-Wide Financial Statements

Government-wide financial statements include two basic financial statements—a statement of net assets and a statement of activities. These statements should include the primary government and its discretely presented component units (presented separately), although they would not include the fiduciary activities, or component units that are fiduciary in nature. The statements would distinguish between governmental activities (which are those financed through taxes, intergovernmental revenues, and other nonexchange revenues) and business-type activities (which are those primarily financed through specified user fees or similar charges). Presentation of prior year data on the government-wide financial statements is optional. Presenting full prior year financial statements on the same pages as the current year financial statements may be cumbersome because of the number of columns that might need to be presented. Accordingly, a government may wish to present summarized prior year data. On the other hand, if full prior year statements are desired (for presentation in an Official Statement for a bond offering, for example) the prior year statements may be reproduced and included with the current year statements. In this case, footnote disclosure should also be reviewed to make sure that both years are addressed.

Basis of accounting and measurement focus

The government-wide financial statements are prepared using the economic resources measurement focus and the accrual basis of accounting for all activities. Presentation of financial statement balances in the government-wide financial statements is discussed throughout the various specific topics covered in this guide. The following pages address the more important financial statement display issues when reporting under the new financial reporting model.

The government-wide financial statements should present information about the primary government’s governmental activities and business-type activities in separate columns, with a total column that represents the total primary government. Governmental activities generally include those activities financed through taxes, intergovernmental revenues, and other nonexchange revenues. Business-type activities are those activities financed in whole or part by fees charged to external parties for goods or services (i.e., enterprise fund activities). Discretely presented component units are presented in a separate column. A column which totals the primary government and the discretely presented component units to represent the entire reporting entity is optional, as is prior year data.

Reporting for governmental and business-type activities should be based on all applicable GASB pronouncements as well as the following pronouncements issued on or before November 30, 1989:

- Financial Accounting Standards Board (FASB) Statements and Interpretations

- Accounting Principles Board Opinions

- Accounting Research Bulletins of the Committee on Accounting Procedures

Consistent with GASB Statement 20, Accounting and Financial Reporting for Proprietary Funds and Other Governmental Entities, (GASBS 20) business-type activities may elect to also apply FASB pronouncements issued after November 30, 1989, except for those that conflict with or contradict GASB pronouncements. Consistent with GASBS 20, this option does not extend to internal service funds. The specific requirements of GASBS 20 are more fully described in Chapter 7.

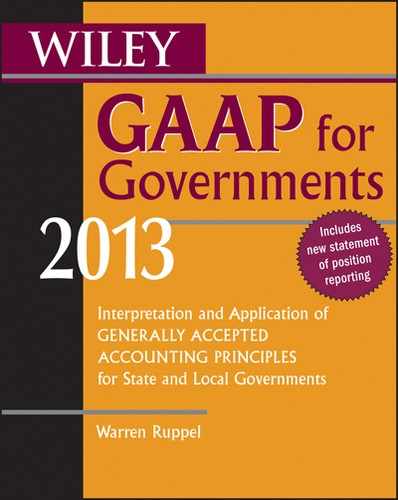

Statement of Net Assets

GASBS 34 provides several examples of how the statement of net assets may be presented. There are several key presentation issues that must be considered in implementing this Statement. These are summarized as follows:

- The difference between assets and liabilities is labeled “net assets.” GASBS 34 encourages the use of the format that presents assets, less liabilities, to arrive at net assets. This difference should not be labeled as equity or fund balance.

- Governments are encouraged to present assets and liabilities in order of their relative liquidity but may instead use a classified format that distinguishes between current and long-term assets and liabilities. An asset’s liquidity is determined by how readily it is expected to be converted to cash and whether there are restrictions on the use of the asset. A liability’s liquidity is based on its maturity or when cash is expected to be used to liquidate it. GASBS 34 allows that the liquidity of classes of assets and liabilities may be assessed using their average liquidity, even if some particular assets or liabilities are more or less liquid than others within the same class. Liabilities whose average maturities are greater than one year should be reported in two components—the amount due within one year and the amount due in more than one year.

- Net assets are comprised of three components.

- Invested in capital assets, net of related debt—This amount represents capital assets (including any restricted capital assets), net of accumulated depreciation, and reduced by the outstanding bonds, mortgages, notes or other borrowings that are attributable to the acquisition, construction or improvement of those assets. If there are significant unspent debt proceeds that are restricted for use for capital projects, the portion of the debt attributable to the unspent proceeds should not be included in the calculation of net assets invested in capital assets, net of related debt. Instead, that portion of the debt would be included in the same net asset component as the unspent proceeds, which would likely be net assets restricted for capital purposes. This net asset category would then have both the asset (proceeds) and the liability (the portion of the debt) recorded in the same net asset component. Note that if the amount of debt issued for capital purposes exceeds the amount of the net book value of capital assets, this number will be reported as a negative amount. For example, if a Phase 3 government that elected not to retroactively record infrastructure assets used debt to finance its infrastructure costs, it will have the debt issued for these assets recorded, but will have no corresponding asset recorded.

NOTE: Ongoing experience with determining the invested in capital assets net of related debt amount confirms that its computation can be difficult. For governments that have active capital programs that are financed with debt, the calculation of this amount can be very problematic. Often capital assets can be specifically identified with the debt that paid for them at the time that they are purchased or constructed. Over time, however, this linkage becomes difficult to maintain. The capital assets, in most cases, are being depreciated over various useful lives and, perhaps, using various depreciation methods. At the same time, the related debt is impacted by normal principal repayments and may as well be impacted by call features, premium or discount amortization, and refundings. Matching the book value of capital assets with the remaining outstanding balance of the debt that paid for them can result in a painstaking process to develop the financial statement amount.

- Restricted net assets—This amount represents those net assets that should be reported as restricted because constraints are placed on the net asset use that are either

Basically, restrictions are not unilaterally established by the reporting government itself and cannot be removed without the consent of those imposing the restrictions or through formal due process. Restrictions can be broad or narrow, provided that the purpose is narrower than that of the reporting unit in which it is reported. In addition, the GASB Implementation Guide clarifies that legislation that “earmarks” that a portion of a tax be used for a specific purpose does not constitute “enabling legislation” that would result in those assets being reported as restricted. In addition, the GASB Implementation Guide provides the example of a general state statute pertaining to local governments that provides that revenues derived from a fee or charge be not used for any purpose other than for which the fee or charge was imposed. In this case, the general statute applies to all jurisdictions in the state and creates a legally enforceable restriction on the use of the resources raised through fees and charges.

The GASB Implementation Guide also addresses two other common issues in determining restricted net assets. First, when assets in a restricted fund exceed the amounts required to be restricted by the external parties or the enabling legislation, the excess over the required amounts would be classified as unrestricted for financial reporting purposes. The second question addresses which component of net assets should be used to report unamortized debt issuance costs and deferred amounts from refundings. Basically, these amounts should “follow the debt.” For example, if the debt is capital-related, the net proceeds of the debt would be used in the calculation of invested in capital assets, net of related debt.

The GASB issued Statement 46, Net Assets Restricted and Enabling Legislation—An Amendment of GASB Statement 34 (GASB 46), addressing a specific issue as to classification of net assets into one of its three categories.

GASBS 46 addresses only the issue of net assets that are restricted by enabling legislation. It is one aspect of a broader examination of net asset categorization currently being undertaken by the GASB.

The basic issue that GASBS 46 addresses is how to interpret whether enabling legislation of a government imposes a restriction on net assets. In some jurisdictions, for example, a legislature cannot bind a future legislature. If the current legislature passes a law imposing a new tax that is restricted to a particular use, are net assets arising from that tax restricted or not? In this example, the subsequent legislature not only cannot be bound, but arguably, the current legislature has the ability to pass new legislation to remove the restriction.

GASBS 46 does not allow governments to make a blanket assessment that enabling legislation does not impose a restriction on net assets. GASBS 34 requires that net assets be reported as restricted when constraints are placed on the assets externally (creditors, grantors, etc.) or imposed by law through constitutional provisions or enabling legislation. Enabling legislation is that which authorizes the government to assess, levy, charge, or otherwise mandate payment of resources and includes a legally enforceable requirement that those resources be used only for the specific purpose stipulated in the legislation.

GASBS 46 provides a definition of “legally enforceable” to mean that a government can be compelled by an external party, such as citizens, public interest groups, or the judiciary, to use resources created by the enabling legislation only for the purposes specified in the legislation. It provides that generally, the enforceability of an enabling legislation restriction is determined by professional judgment, which may be based on actions such as analyzing the legislation to determine if it meets the qualifying criteria for enabling legislation, reviewing determinations made for similar legislation of the government or other governments, or obtaining the opinion of legal counsel. Enforceability cannot ultimately be proven unless tested through the judicial process, which may never occur. In addition, the determination that a particular restriction is not legally enforceable may lead a government to reevaluate the legal enforceability of similar enabling legislation restrictions, but should not necessarily lead a government to conclude that all enabling legislation restrictions are unenforceable.

GASBS 46 provides that if a government passes new enabling legislation that replaces the original enabling legislation by establishing new legally enforceable restrictions on the resources raised by the original enabling legislation, then from that period forward, the resources accumulated under the new enabling legislation should be reported as restricted to the purpose specified by the new enabling legislation. Professional judgment should be used to determine if remaining balances accumulated under the original enabling legislation should continue to be reported as restricted for the original purpose, restricted to the purpose specified in the new legislation, or unrestricted.

GASBS 46 further provides that if resources are used for a purpose other than those stipulated in the enabling legislation or if there is other cause for reconsideration, governments should reevaluate the legal enforceabiltity of the restrictions to determine if the resources should continue to be reported as restricted. If reevaluation results in a determination that a particular restriction is no longer legally enforceable, then from the beginning of that period forward the resources should be reported as unrestricted. If it is determined that the restrictions continue to be legally enforceable, then for financial reporting purposes, the restricted net assets should not reflect any reduction for resources used for purposes not stipulated in the enabling legislation.

GASBS 46 requires that net assets at the end of the reporting period that are restricted by enabling legislation be disclosed in the notes to the financial statements.

When permanent endowments or permanent fund principal amounts are included in restricted net assets, restricted net assets should be displayed in two additional components—expendable and nonexpendable. Nonexpendable net assets are those that are required to be retained in perpetuity.

- Unrestricted net assets—This amount consists of net assets that do not meet the definition of restricted net assets or net assets invested in capital assets, net of related debt.

Exhibit 1 presents a sample classified statement of net assets, based on the examples provided in GASBS 34.

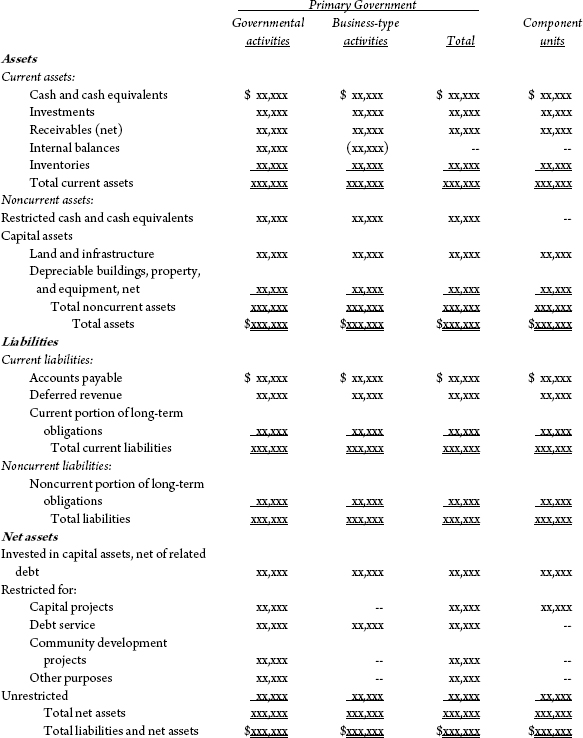

Statement of Activities

GASBS 34 adopts the net (expense) revenue format, which is easier to view than describe. See Exhibit 2 for an example of a statement of activities based on the examples provided in GASBS 34.

The objective of this format is to report the relative financial burden of each of the reporting government’s functions on its taxpayers. The format identifies the extent to which each function of the government draws from the general revenues of the government or is self-financing through fees or intergovernmental aid.

The statement of activities presents governmental activities by function (similar to the current requirements) and business-type activities at least by segment. Segments are identifiable activities reported as or within an enterprise fund or another stand-alone entity for which one or more revenue bonds or other revenue-backed debt instrument are outstanding.

Expense Presentation

The statement of activities should present expenses of governmental activities by function in at least the level of detail required in the governmental fund statement of revenues, expenditures and changes in fund balances. Categorization and level of detail are basically the same for governmental activities by function in pre-GASBS 34 financial statements. Expenses for business-type activities are reported in at least the level of detail as by segment, which is defined as an identifiable activity reported as or within an enterprise fund or another stand-alone entity for which one or more revenue bonds or other revenue-backed debt instruments are outstanding. A segment has a specific identifiable revenue stream pledged in support of revenue bonds or other revenue-backed debt and has related expenses, gains and losses, assets, and liabilities that can be identified.

Governments should report all expenses by function except for those expenses that meet the definitions of special items or extraordinary items, discussed later in this chapter. Governments are required, at a minimum, to report the direct expenses for each function. Direct expenses are those that are specifically associated with a service, program, or department and, accordingly, can be clearly identified with a particular function.

There are numerous government functions—such as the general government, support services, and administration—that are actually indirect expenses of the other functions. For example, the police department of a city reports to the mayor. The direct expenses of the police department would likely be reported under the function “public safety” in the statement of activities. However the mayor’s office (along with payroll, personnel, and other departments) supports the activities of the police department although they are not direct expenses of the police department. Governments are permitted, but not required, to allocate these indirect expenses to other functions. Governments may allocate some but not all indirect expenses, or they may use a full-cost allocation approach and allocate all indirect expenses to other functions. If indirect expenses are allocated, they must be displayed in a column separate from the direct expenses of the functions to which they are allocated. Governments that allocate central expenses to funds or programs, such as through the use of internal service funds, are not required to eliminate these administrative charges when preparing the statement of activities, but should disclose in the summary of significant accounting policies that these charges are included in direct expenses.

The reporting of depreciation expense in the statement of activities requires some careful analysis. Depreciation expense for the following types of capital assets is required to be included in the direct expenses of functions or programs:

- Capital assets that can be specifically identified with a function or program

- Capital assets that are shared by more than one function or program, such as a building in which several functions or programs share office space

Some capital assets of a government may essentially serve all of the functions of a government, such as a city hall or county administrative office building. There are several options for presenting depreciation expense on these capital assets. These options are

- Include the depreciation expense in an indirect expense allocation to the various functions or programs

- Report the depreciation expense as a separate line item in the statement of activities (labeled in such a way as to make clear to the reader of the financial statements that not all of the government’s depreciation expense is included on this line)

- Reported as part of the general government (or its equivalent) function

Depreciation expense for infrastructure assets associated with governmental activities should be reported in one of the following ways:

- Report the depreciation expenses as a direct expense of the function that is normally used for capital outlays for and maintenance of infrastructure assets

- Report the depreciation expense as a separate line item in the statement of activities (labeled in such a way as to make clear to the reader of the financial statements that not all of the government’s depreciation expense is included on this line)

Interest expense on general long-term liabilities should be reported as an indirect expense. In the vast majority of circumstances, interest expense will be displayed as a separate line item on the statement of activities. In certain limited circumstances where the borrowing is essential to the creation or continuing existence of a program or function and it would be misleading to exclude interest from that program or function’s direct expenses, GASBS 34 would permit that interest expense to be reported as a direct expense. The GASBS 34 Implementation Guide also prescribes that interest on capital leases or interest expense from vendor financing arrangements should not be reported as direct expenses of specific programs.

Revenue Presentation

Revenues on the statement of activities are distinguished between program revenues and general revenues.

- Program revenues are those derived directly from the program itself or from parties outside the government’s taxpayers or citizens, as a whole. Program revenues reduce the net cost of the program that is to be financed from the government’s general revenues. On the statement of activities, these revenues are deducted from the expenses of the functions and programs discussed in the previous section. The GASB Implementation Guide provides that separate columns may be presented under a particular revenue category heading. For example, if fines are a significant part of charges for services (defined below), a government may elect (but is not required) to have a separate column under the charges for services heading that breaks out fines as a separate column. There are three categories into which program revenues should be distinguished.

- General revenues are all those revenues that are not required to be reported as program revenues. All taxes, regardless of whether they are levied for a specific purpose, should be reported as general revenues. Taxes should be reported by type of tax, such as real estate taxes, sales tax, income tax, franchise tax, etc. (Although operating special assessments are derived from property owners, they are not considered taxes and are properly reported as program revenues.) General revenues are reported after total net expense of the government’s functions on the statement of activities.

Extraordinary and special items

GASBS 34 provides that a government’s statement of activities may have extraordinary and special items. Extraordinary items are those that are unusual in nature and infrequent in occurrence. This tracks the private sector accounting definition of this term.

Special items are a concept introduced by GASBS 34. They are defined as “significant transactions or other events within the control of management that are either unusual in nature or infrequent in occurrence.” Special items are reported separately in the statement of activities before any extraordinary items.

The GASBS 34 Implementation Guide cites the following events or transactions that may qualify as extraordinary or special items:

Extraordinary items

- Costs related to an environmental disaster caused by a large chemical spill in a train derailment in a small city

- Significant damage to the community or destruction of government facilities by natural disaster or terrorist act. However, geographic location of the government may determine if a weather-related natural disaster is infrequent.

- A large bequest to a small government by a private citizen

Special items

- Sales of certain general government capital assets

- Special termination benefits resulting from workforce reductions due to sale of the government’s utility operations

- Early-retirement program offered to all employees

- Significant forgiveness of debt

Eliminations and reclassifications

GASBS 34 requires that eliminations of transactions within the governmental business-type activities be made so that these amounts are not “grossed-up” on the statement of net assets and statement of activities. Where internal service funds are used, their activities are eliminated where their transactions would cause a double recording of revenues and expenses.

Fund Financial Statements

There are many similarities between the way in which fund financial statements under the new financial reporting model are prepared and the way in which they were previously prepared. One of the most notable similarities is that governmental funds continue to use the modified accrual basis of accounting and the current financial resources measurement focus in the fund financial statements. However, there are also many important differences in the way these statements are prepared. The following discussion highlights these differences.

Fund financial statements are prepared only for the primary government. They are designed to provide focus on the major funds within each fund type. Fund financial statements include financial statements for fiduciary funds, but they do not include financial statements for discretely presented component units. The following are the types of funds included in fund-type financial statements:

- Governmental funds

- Proprietary funds

- Fiduciary funds and similar component units

The following are the required financial statements for the various fund types. A reference to each exhibit that provides a sample of each of these statements is also provided.

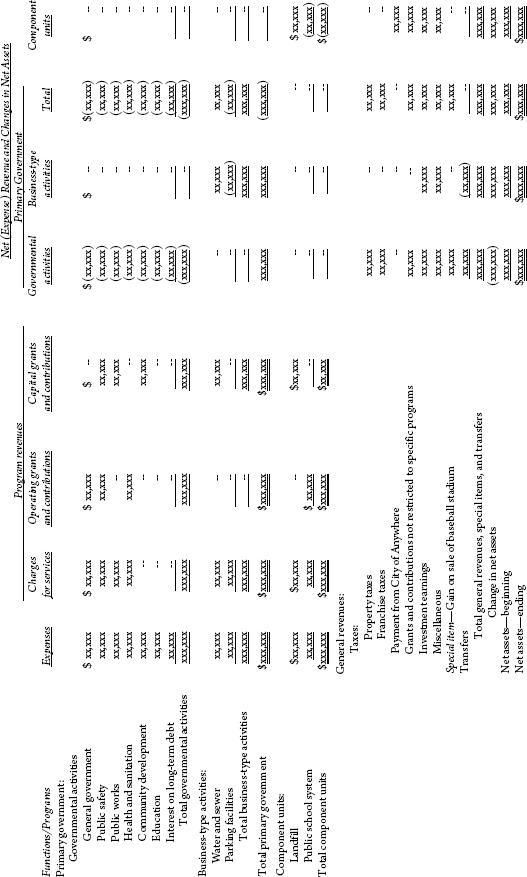

Governmental funds

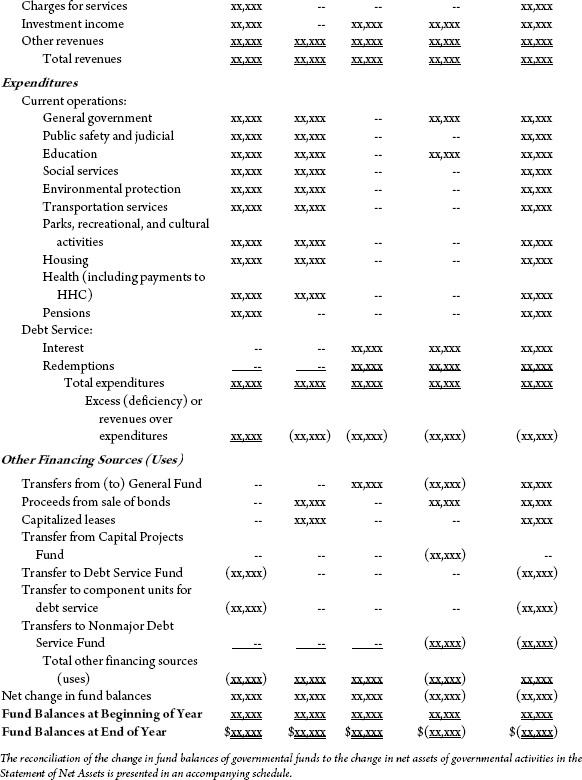

- Balance sheet (Exhibit 3)

- Statement of revenues, expenditures, and changes in fund balances (Exhibit 4)

Proprietary funds

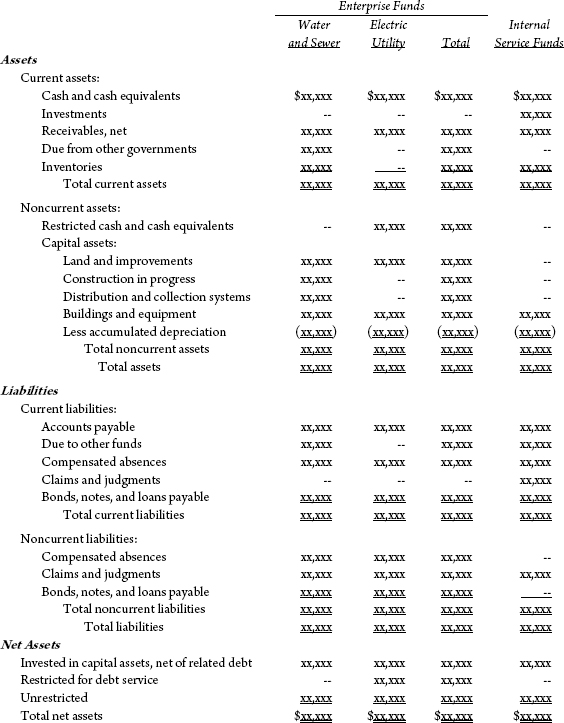

- Statement of net assets or balance sheet (Exhibit 5)

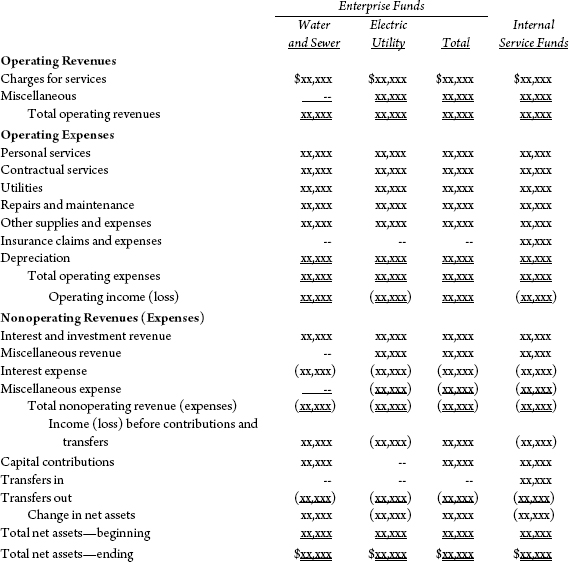

- Statement of revenues, expenses, and change in fund net assets or fund equity (Exhibit 6)

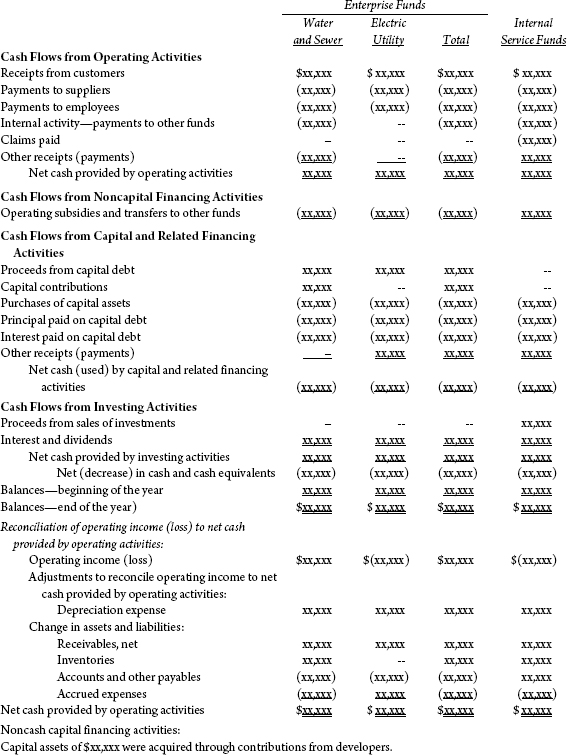

- Statement of cash flows (Exhibit 7)

Fiduciary funds

In preparing these fund financial statements, the following significant guidance of GASBS 34 should be considered:

- A reconciliation of the governmental fund activities in the government-wide financial statements with the governmental fund financial statements should be prepared. A summary reconciliation to the government-wide financial statements should be presented at the bottom of the fund financial statements or in an accompanying schedule. If the aggregation of reconciling information obscures the nature of the individual elements of a particular reconciling item, a more detailed explanation should be provided in the notes to the financial statements. Exhibits 10 and 11 provide examples of these reconciliations presented as a separate schedule.

- General capital assets and general long-term debt are not reported in the fund financial statements. (Note that capital assets and long-term debt are reported in propriety funds, however.)

- GASBS 34 requires activities to be reported as enterprise funds if any one of the following criteria is met:

Governmental Fund Balance Reporting under GASBS 34

GASBS 54, Fund Balance Reporting and Governmental Fund Definitions, changed the way in which governmental funds report their fund balance. Total fund balance is still the residual between a fund’s assets and liabilities. What changed is how the components of that total fund balance are displayed. Basically, fund balance is classified into these categories, as applicable:

- Nonspendable fund balance

- Restricted fund balance

- Committed fund balance

- Assigned fund balance

- Unassigned fund balance

As might be gleamed from the above list, the classification hierarchy is based on the extent to which the government is bound to honor constraints on the specific purposes for which amounts in those funds can be spent.

The following pages describe the definition of these classifications as promulgated by GASBS 54, certain specific accounting treatments relating to stabilization agreements, and disclosure requirements.

Nonspendable Fund Balance

GASBS 54 provides that the nonspendable fund balance classification includes amounts that cannot be spent because they are either

The “not in spendable form” criterion includes items that are not expected to be converted to cash, for example, inventories and prepaid amounts. (In existing GAAP, these amounts were usually reported as “reserved.”)

This category also includes the long-term amount of loans and notes receivable, as well as property acquired for resale. However, if the use of the proceeds from the collection of those receivables or from the sale of those properties is restricted, committed, or assigned, then they should be included in the appropriate fund balance classification (restricted, committed, or assigned), rather than nonspendable fund balance.

The corpus (or principal) of a permanent fund is an example of an amount that is legally or contractually required to be maintained intact. Permanent funds are used to account for and report resources that are restricted to the extent that only earnings, and not principal, maybe used for purposes that support the government’s programs, (i.e., for the benefit of the government and its citizenry). For readers familiar with not-for-profit accounting, the equivalent concept in that financial reporting model is referred to as permanently restricted net assets or, the more common terminology, an endowment fund.

Restricted Fund Balance

Amounts that are restricted to specific purposes, pursuant to the definition of “restricted” in GASBS 34 and 46 (as described previously in this chapter) should be reported as restricted fund balance, with the slight exception of the matter described in the Note above. Accordingly, under GASBS 54, fund balance should be reported as restricted when constraints placed on the use of resources are either

Enabling legislation, as the term is used in GASBS 54, authorizes the government to assess, levy, charge, or otherwise mandate payment of resources (from external resource providers) and includes a legally enforceable requirement that those resources be used only for the specific purposes stipulated in the legislation. Legal enforceability means that a government can be compelled by an external party—such as citizens, public interest groups, or the judiciary—to use resources created by enabling legislation only for the purposes specified by the legislation.

Committed Fund Balance

The concepts of nonspendable and restricted described above are readily understandable and have precedents in existing GAAP. Accordingly, their implementation should not result in significant implementation difficulties. However, the concepts of committed and assigned fund balances (discussed in this and the following section) are new, so implementation of GASBS 54 for these classifications may be a bit more challenging.

GASBS 54 provides that amounts that can only be used for specific purposes pursuant to constraints imposed by formal action of the government’s highest level of decision-making authority should be reported as committed fund balance. Those committed amounts cannot be used for any other purpose unless the government removes or changes the specified use by taking the same type of action (for example, legislation, resolution, ordinance) it employed to previously commit those amounts. The authorization specifying the purposes for which amounts can be used should have the consent of both the legislative and executive branches of the government, if applicable. Committed fund balance also should incorporate contractual obligations to the extent that existing resources in the fund have been specifically committed for use in satisfying those contractual requirements.

In contrast to fund balance that is restricted by enabling legislation, as discussed above, GASBS 54 states that amounts in the committed fund balance classification may be redeployed for other purposes with appropriate due process. Constraints imposed on the use of committed amounts are imposed by the government, separate from the authorization to raise the underlying revenue. Therefore, compliance with constraints imposed by the government that commit amounts to specific purposes is not considered to be legally enforceable.

GASBS 54 also provides that the formal action of the government’s highest level of decision-making authority that commits fund balance to a specific purpose should occur prior to the end of the reporting period, but the amount, if any, which will be subject to the constraint, may be determined in the subsequent period.

Assigned Fund Balance

GASBS 54 provides that amounts that are constrained by the government’s intent to be used for specific purposes, but are neither restricted nor committed, should be reported as assigned fund balance, except for stabilization arrangements, as discussed below. GASBS 54 states that intent should be expressed by (1) the governing body itself or (2) a body (a budget or finance committee, for example) or official to which the governing body has delegated the authority to assign amounts to be used for specific purposes.

In other words, assigned fund balance represents resources where the constraint is less binding than that for committed resources, but not so available to the government that they would be considered unassigned.

Both the committed and assigned fund balance classifications include amounts that have been constrained to being used for specific purposes by actions taken by the government itself. However, the authority for making an assignment is not required to be the government’s highest level of decision-making authority. Furthermore, the nature of the actions necessary to remove or modify an assignment are not as difficult to accomplish as they are for the committed fund balance classification. GASBS 54 notes that some governments may not have both committed and assigned fund balances, as not all governments have multiple levels of decision-making authority.

Applying the logic of the four classifications described above, GASBS notes that assigned fund balance includes

Why is 1. always true? By reporting particular amounts that are not restricted or committed in a special revenue, capital projects, debt service, or permanent fund, the government has effectively assigned those amounts to the purposes of the respective funds. By reporting resources in a governmental fund other than the general fund, the government is at least assigning those resources to the purposes for which those funds exist.

GASBS 54 does provide, however, that governments should not report an assignment for an amount to a specific purpose if the assignment would result in a deficit in unassigned fund balance. It also notes that an appropriation of existing fund balance to eliminate a projected budgetary deficit in the subsequent year’s budget in an amount no greater than the projected excess of expected expenditures over expected revenues satisfies the criteria to be classified as an assignment of fund balance. However, again, assignments should not cause a deficit in unassigned fund balance to occur.

Unassigned Fund Balance

Unassigned fund balance is the residual classification for the general fund. This classification represents fund balance that has not been assigned to other funds and that has not been restricted, committed, or assigned to specific purposes within the general fund. The general fund should be the only fund that reports a positive unassigned fund balance amount.

GASBS 54 provides, however, that in other governmental funds, if expenditures incurred for specific purposes exceeded the amounts restricted, committed, or assigned to those purposes, it may be necessary to report a negative unassigned fund balance, as discussed below.

Fund Balance Classifications

Sometimes, a government has expenditures for purposes for which both restricted and unrestricted (including committed, assigned and unassigned) resources exist. Which resources should the government consider to have been expended first? The government may adopt an accounting policy that states which resources it considers to have been spent in this case. In addition, the government may adopt an accounting policy which states which unrestricted classification of resources is considered to have been spent in a similar case where more than one classification of unrestricted resources are available. GASBS 54 permits the adoption and consistent application of these policies. If a government does not establish a policy for its use of unrestricted fund balance amounts, it should consider that committed amounts would be reduced first, followed by assigned amounts, and then unassigned amounts when expenditures are incurred for purposes for which amounts in any of those unrestricted fund balance classifications could be used.

GASBS 54 notes that in a governmental fund other than the general fund, expenditures incurred for a specific purpose might exceed the amounts in the fund that are restricted, committed, and assigned to that purpose and a negative residual balance for that purpose may result. If that occurs, amounts assigned to other purposes in that fund should be reduced to eliminate the deficit. If the remaining deficit eliminates all other assigned amounts in the fund, or if there are no amounts assigned to other purposes, the negative residual amount should be classified as unassigned fund balance. In the general fund, a similar negative residual amount would have been eliminated by reducing unassigned fund balance pursuant to the policy described above. A negative residual amount should not be reported for restricted, committed, or assigned fund balances in any fund.

Stabilization Agreements

GASBS 54 has special requirements pertaining to stabilization agreements. These types of agreements sometimes are referred to as “rainy day funds” as they are meant to set aside resources in favorable times to provide resources in times that are less favorable.

GASBS 54’s requirements relate to those agreements which are formal arrangements for amounts that are subject to controls that dictate the circumstances under which they can be spent. Many governments have formal arrangements to maintain amounts for budget or revenue stabilization, working capital needs, contingencies or emergencies, and other similarly titled purposes. The authority to set aside those amounts generally comes from statute, ordinance, resolution, charter, or constitution. Stabilization amounts may be expended only when certain specific circumstances exist. The formal action that imposes the parameters for spending should identify and describe the specific circumstances under which a need for stabilization arises. Those circumstances should be such that they would not be expected to occur routinely.

GASBS 54 provides the example of a stabilization amount that can be accessed “in an emergency” as not qualifying to be classified within the committed category because the circumstances or conditions that constitute an emergency are not sufficiently detailed, and it is not unlikely that an “emergency” of some nature would routinely occur. In addition, GASBS 54 provides that a stabilization amount that can be accessed to offset an “anticipated revenue shortfall” would not qualify unless the shortfall was quantified and was of a magnitude that would distinguish it from other revenue shortfalls that occur during the normal course of governmental operations.

For the purposes of reporting fund balance, GASBS 54 considers stabilization a specific purpose, as discussed above. Stabilization amounts should be reported in the general fund as restricted or committed if they meet the criteria for those classifications, based on the source of the constraint on their use. Stabilization arrangements that do not meet the criteria to be reported within the restricted or committed fund balance classifications should be reported as unassigned in the general fund. Further, a stabilization arrangement would satisfy the criteria to be reported as a separate special revenue fund only if the resources derive from a specific restricted or committed revenue source.

Fund Balance Display on the Balance Sheet

GASBS 54 provides that amounts for the two components of nonspendable fund balance—(1) not in spendable form and (2) legally or contractually required to be maintained intact— may be presented separately, or nonspendable fund balance may be presented in the aggregate. Restricted fund balance may be displayed in a manner that distinguishes between the major restricted purposes, or it may be displayed in the aggregate. Similarly, specific purposes information for committed and assigned fund balances may be displayed in sufficient detail so that the major commitments and assignments are evident to the financial statement user, or each classification may be displayed in the aggregate. Where aggregate disclosures are displayed, note disclosure of details will be required as described in the disclosure section below.

Disclosures

GASBS 54 requires governments to disclose the following about their fund balance classification policies and procedures in the notes to the financial statements:

The following additional disclosures are also required, where applicable.

| Pension and Other Employee Benefit Trust Funds | Agency Fund | |

| Assets | ||

| Cash and cash equivalents | $xx,xxx | $xx,xxx |

| Receivables: | ||

| Receivable for investment securities sold | xx,xxx | –– |

| Accrued interest and dividend receivable | xx,xxx | –– |

| Investments: | ||

| Other short-term investments | xx,xxx | –– |

| Debt securities | xx,xxx | xx,xxx |

| Equity securities | xx,xxx | –– |

| Guaranteed investment contracts | xx,xxx | –– |

| Mutual funds | xx,xxx | –– |

| Collateral from securities lending transactions | xx,xxx | –– |

| Due from other funds | xx,xxx | –– |

| Other | xx,xxx | xx,xxx |

| Total assets | xx,xxx | xx,xxx |

| Liabilities | ||

| Accounts payable and accrued liabilities | xx,xxx | xx,xxx |

| Payable for investment securities purchased | xx,xxx | –– |

| Accrued benefits payable | xx,xxx | –– |

| Due to other funds | xx,xxx | –– |

| Securities lending transactions | xx,xxx | –– |

| Other | xx,xxx | xx,xxx |

| Total liabilities | xx,xxx | xx,xxx |

| Net Assets | ||

| Held in trust for benefit payments | $xx,xxx | $–– |

| Pension and Other Employee Benefit Trust Funds | |

| Additions | |

| Contributions: | |

| Member contributions | $xx,xxx |

| Employer contributions | xx,xxx |

| Total contributions | xx,xxx |

| Investment income: | |

| Interest income | xx,xxx |

| Dividend income | xx,xxx |

| Net depreciation in fair value of investments | (xx,xxx) |

| Less investment expenses | xx,xxx |

| Investment loss, net | (xx,xxx) |

| Payments from other funds | xx,xxx |

| Other | xx,xxx |

| Total additions | (xx,xxx) |

| Deductions | |

| Benefit payments and withdrawals | xx,xxx |

| Payments to other funds | xx,xxx |

| Administrative expenses | xx,xxx |

| Total deductions | xx,xxx |

| Decrease in plan net assets | (xx,xxx) |

| Net Assets | |

| Held in trust for benefit payments | |

| Beginning of year | xx,xxx |

| End of year | $xx,xxx |

| Amounts reported for governmental activities in the Statement of Net Assets are different because: | |

| Total fund balances—governmental funds | $(xx,xxx) |

| Inventories recorded in the Statement of Net Assets are recorded as expenditures in the governmental funds | xx,xxx |

| Capital assets used in governmental activities are not financial resources and therefore are not reported in the funds | xx,xxx |

| Other long-term assets are not available to pay for current-period expenditures and therefore are deferred in the funds | xx,xxx |

| Long-term liabilities are not due and payable in the current period and accordingly are not reported in the funds: | |

| Bonds and notes payable | (xx,xxx) |

| Accrued interest payable | (xx,xxx) |

| Other long-term liabilities | (xx,xxx) |

| Net assets (deficit) of governmental activities | $(xx,xxx) |

| Amounts reported for governmental activities in the Statement of Activities are different because: | ||

| Net change in fund balances—total governmental funds | $(xx,xxx) | |

| Governmental funds report capital outlays as expenditures. However, in the statement of activities the cost of those assets is allocated over their estimated useful lives and reported as depreciation expense. This is the amount by which capital outlays exceeded depreciation in the current period. | ||

| Purchases of fixed assets | $xx,xxx | |

| Depreciation expense | (xx,xxx) | xx,xxx |

| The net effect of various miscellaneous transactions involving capital assets and other (i.e., sales, trade-ins, and donations) is to decrease net assets | (xx,xxx) | |

| The issuance of long-term debt (e.g., bonds, leases) provides current financial resources to governmental funds, while the repayment of the principal of long-term debt consumes the current financial resources of governmental funds. Neither transaction, however, has any effect on net assets. Also, governmental funds report the effect of issuance costs, premiums, discounts, and similar items when debt is first issued, whereas these amounts are deferred and amortized in the statement of activities. This amount is the net effect of these differences in the treatment of long-term debt and related items. | ||

| Proceeds from sales of bonds | (xx,xxx) | |

| Principal payments of bonds | xx,xxx | |

| Other | (xx,xxx) | (xx,xxx) |

| Some expenses reported in the statement of activities do not require the use of current financial resource and therefore are not reported as expenditures in governmental funds | (xx,xxx) | |

| Revenues in the statement of activities that do not provide current financial resources are not reported as revenues in the funds | (xx,xxx) | |

| Change in net assets—governmental activities | $(xx,xxx) | |

Budgetary Comparison Schedules

GASBS 34 requires that certain budgetary comparison schedules be presented in required supplementary information (RSI). This information is required only for the general fund and each major special revenue fund that has a legally adopted annual budget. Governments may elect to report the budgetary comparison information in a budgetary comparison statement as part of the basic financial statements, rather than as RSI.

The budgetary comparison schedules must include the originally adopted budget, as well as the final budget. The government is given certain flexibility in the format in which this information is present. For example, the comparisons may be made in a format that resembles the budget document instead of being made in a way that resembles the financial statement presentation. Of important note, the actual information presented is to be presented on the budgetary basis of accounting, which for many governments differs from generally accepted accounting principles. Regardless of the format used, the financial results reported in the budgetary comparison schedules must be reconciled to GAAP-based fund financial statements.

The GASB issued Budgetary Comparison Schedules—Perspective Differences (GASBS 41) to address the issue of governments which have significant budgetary perspective differences that result in their not being able to present budgetary comparison information for their general fund and major special revenue funds. This new Statement does not address instances where there are minor budgetary fund structures that have minor perspective differences from their fund structure used for reporting under generally accepted accounting principles (GAAP). These differences are usually readily handled in the required reconciliation between the budgetary perspective and the GAAP perspective. GASBS 41 addresses situations where there are significant perspective differences where budgetary structures prevent governments from associating their estimated revenues and appropriations from their legally adopted budget to the major revenue sources and functional expenditures that are reported in the general fund and major special revenue funds.

GASBS 41 requires that governments with significant budgetary perspective differences that result in a government’s not being able to present budgetary comparisons for the general fund and major special revenue funds present budgetary comparison schedules based on the fund, organization, or program structure that the government uses for its legally adopted budget. This comparison schedule must be presented as part of required supplementary information (RSI).

GASBS 41 essentially has two main points. First, if there are significant perspective differences between the budgetary perspective and the GAAP perspective, governments are still required to present budgetary comparison information for the general fund and major special revenue funds. The comparison should be presented in accordance with the format in which the budget is legally adopted. Second, where such perspective differences exist, governments do not have the option to present the budgetary comparison schedule as part of the basic financial statements. It must be presented as part of RSI.

Notes and Other Disclosures

The notes to the financial statements are an integral part of the basic financial statements. Because the basic financial statements and required supplemental information must be “liftable” from the CAFR (i.e., have the ability to function as freestanding financial statements), the notes to the financial statements should always be considered to be part of the “liftable” basic financial statements.

This section provides an overview of certain required disclosures in the notes and the various areas that the financial statement preparer should consider for disclosure in the notes. Almost every new accounting pronouncement issued by the GASB, however, contains some additional disclosures that must be included in the notes. Therefore, to use this book to properly prepare notes for a state or local government, the reader should consider the following broad outline of the financial statement notes described below, review each chapter that addresses specific unique accounting and financial reporting guidance on required disclosures, and consider the “Disclosure Checklist” included in this guide.

The notes to the financial statements are essential to the fair presentation of the financial position, results of operations, and where applicable, cash flows. Notes considered to be essential to the fair presentation of the financial statements contained in the basic financial statements include individual discretely presented component units, considering the particular component unit’s significance to all discretely presented component units, and the nature and significance of the individual unit’s relationship to the primary government. The notes prepared under the new financial reporting model should focus on the primary government, which includes blended component units.

Determining which discretely presented component unit financial statements should be included in the notes to the financial statements requires that the financial statement preparer exercise professional judgment. These judgments should be made on a case-by-case basis. Certain disclosures that may be required and appropriate for one component unit may not be required for another. As stated above, these considerations should be made based on the relative significance of a particular discretely presented component unit to all of the discretely presented component units and the significance of the individual discretely presented component unit to the primary government.

The GASB issued GASBS 38 as a result of its project to review financial statement note disclosures. A need to reevaluate note disclosures in the context of the new financial reporting model established by GASBS 34 provided the impetus for the GASB to issue this Statement before most governments begin implementing the new financial reporting model.

The GASB reevaluated note disclosures that have been in existence since 1994 and not under reevaluation under some other project. As a result of this evaluation, several new note disclosures have been added, while relief from previous disclosure requirements was rare. While the effect of the potential changes will vary from government to government, it appears that disclosures relating to interfund balances and transfers appear to be the most significant.

The Codification of Governmental Accounting and Financial Reporting Standards published by the GASB (GASB Codification) identifies the more common note disclosures required of state and local governments. The broad categories of notes that would normally be included in the financial statements of a state or local government would include the following:

- Summary of significant accounting policies, including

- A description of the government-wide financial statements, noting that neither fiduciary funds nor component units that are fiduciary in nature are included.

- The measurement focus and basis of accounting used in the government-wide statements.

- The policy for eliminating internal activity in the statement of activities.

- The policy for applying FASB pronouncements issued after November 30, 1989, to business-type activities and to enterprise funds of the primary government.

- The policy for capitalizing assets and for estimating the useful lives of those assets (used to calculate depreciation expense)

- Governments that choose to use the modified approach for reporting eligible infrastructure assets should describe that approach.

- A description of the types of transactions included in program revenues and the policy for allocating indirect expenses to functions in the statement of activities.

- The government’s policy for defining operating and nonoperating revenues of proprietary funds.

- That government’s policy regarding whether to first apply restricted or unrestricted resources when an expense is incurred for purposes for which both restricted and unrestricted net assets are available.

- Descriptions of the activities accounted for in each of the following columns (major funds, internal service funds and fiduciary fund types) presented in the financial statements.

- A brief description of the component units of the overall governmental reporting entity and the units’ relationships to the primary government. This should include a discussion of the criteria for including component units in the financial reporting entity and how the component units are reported. (The determination of the reporting entity is more fully described in Chapter 11.) The notes should also indicate how the separate financial statements of the component units may be obtained.

- Revenue recognition policies

- The period of availability used for revenue recognition in governmental fund financial statements.

- Policy on capitalization of interest costs on fixed assets

- Definition of cash and cash equivalents used in the statement of cash flows for proprietary and nonexpendable trust funds

- Cash deposits with financial institutions

- Investments

- Significant contingent liabilities

- Encumbrances outstanding

- Significant effects of subsequent events

- Pension plan and OPEB costs and obligations

- Significant violations of finance-related legal and contractual requirements and actions to address these violations

- Debt service requirements to maturity, as follows:

- Principal and interest requirements to maturity, presented separately for each of the five succeeding fiscal years and in five-year increments there-after. Interest requirements for variable-rate debt should be made using the interest rate in effect at the financial statement date.

- The terms by which interest rates change for variable-rate debt.

- For capital and noncancelable operating leases, the future minimum payments for each of the five succeeding fiscal years and in five-year increments thereafter should be disclosed.

- Details of short-term debt should be disclosed, even if no short-term debt exists at the financial statement date. Short-term debt results from borrowings characterized by anticipation notes, uses of lines of credit, and similar loans. A schedule of changes in short-term debt, disclosing beginning- and end-of-year balances, increases, decreases, and the purpose for which short-term debt was issued.

- Commitments under noncapitalized (operating) leases

- Construction and other significant commitments

- Required disclosures about capital assets

- Required disclosures about long-term liabilities

- Interfund balances and transfers

- For each major component unit, the nature and amount of significant transactions with other discretely presented component units

- Disclosures about donor-restricted endowments

- Any excess of expenditures over appropriations in individual funds

- Deficit fund balances or net assets of individual funds

- Balances of receivables and payables reported on the statement of net assets and balance sheet may be aggregations of different components, such as balances due to or from taxpayers, other governments, vendors, beneficiaries, employees, etc. When the aggregation of balances on the statement of net assets obscures the nature of significant individual accounts, the governments should provide details in the notes to the financial statements. Significant receivable balances not expected to be collected within one year of the date of the financial statements should be disclosed.

- For interfund balances reported in the fund financial statements, disclose the following:

- Identification of amounts due from other funds by individual major fund, nonmajor funds in the aggregate, internal service funds in the aggregate, and fiduciary fund type

- A description of the purpose for interfund balances

- Interfund balances that are not expected to be repaid within one year from the date of the financial statements

- For interfund transfers reported in the fund financial statements, disclose the following:

- Identification of the amounts transferred from other funds by individual major fund, nonmajor funds in the aggregate, internal service funds in the aggregate and fiduciary fund type

- A general description of the principal purposes for interfund transfers

- A general description and the amount of significant transfers that

- Are not expected to occur on a routine basis and/or

- Are inconsistent with the activities of the fund making the transfer—for example, a transfer from a capital projects fund to the general fund

The GASB Codification identifies the following additional disclosures that may apply to state and local governments:

- Entity risk management activities

- Property taxes

- Segment information for enterprise funds

- Condensed financial statements for major discretely presented component units

- Differences between the budget basis of accounting and GAAP not otherwise reconciled in the basic financial statements

- Short-term debt instruments and liquidity

- Related-party transactions

- The nature of the primary government’s accountability for related organizations

- Capital leases

- Joint ventures and jointly governed organizations

- Debt refundings

- Grants, entitlements, and share revenues

- Fund balance designation

- Interfund eliminations in the combined financial statements that are not apparent from financial statement headings

- Pension plans in both separately issued plan financial statements and employer statements

- Bond, tax, or revenue anticipation notes excluded from fund or current liabilities

- Nature and amount of any inconsistencies in the financial statements caused by transactions between component units having different fiscal year-ends or changes in component unit year-ends

- In component unit separate reports, identification of the primary government in whose financial report the component unit is included and a description of its relationship to the primary government

- Deferred compensation plans

- Reverse repurchase and dollar reverse repurchase agreements

- Securities lending transactions

- Special assessment debt and related activities

- Demand bonds

- Landfill closure and postclosure care

- Pollution remediation obligations

- On-behalf payments to fringe benefits and salaries

- Entity involvement in conduit debt obligations

- Sponsoring government disclosures about external investment pools reported as investment trust funds

- The amount of interest expense included in direct expenses in the government-wide statement of activities

- Significant transactions or other events that are either unusual or infrequent but not within the control of management

- Nature of individual elements of a particular reconciling item, if obscured in the aggregated information in the summary reconciliation of the fund financial statements to the government-wide statements

- Discounts and allowances that reduce gross revenues, when not reported on the face of the financial statements

- Disaggregation of receivable and payable balances

- Impairment losses, idle impaired capital assets, and insurance recoveries, when not otherwise apparent from the face of the financial statements

- The amount of the primary government’s net assets at the end of the reporting period that are restricted by enabling legislation

- Termination benefits

- Future revenues that are pledged or sold

- Derivative instruments

- Conditions and events giving rise to substantial doubt about the government’s ability to continue as a going concern.

The GASB Codification reiterates that the above list of areas to be considered for note disclosure is not meant to be all-inclusive, nor is it meant to replace professional judgment in determining the disclosures necessary for fair presentation in the financial statements. The notes to the financial statements, on the other hand, should not be cluttered with unnecessary or immaterial disclosures. The individual circumstances and materiality must be considered in assessing the propriety of the disclosures in the notes to the financial statements. Notes to the financial statements provide necessary disclosure of material items, the omission of which would cause the financial statements to be misleading.

GASBS 34 requires governments to provide additional information in the notes to the financial statements about the capital assets and long-term liabilities. The disclosures should provide information that is divided into the major classes of capital assets and long-term liabilities as well as those pertaining to governmental activities and those pertaining to business-type activities. In addition, information about capital assets that are not being depreciated should be disclosed separately from those that are being depreciated.

Required disclosures about major classes of capital assets include

- Beginning-and end-of-year balances (regardless of whether beginning-of-year balances are presented on the face of the government-wide financial statements), with accumulated depreciation presented separately from historical cost

- Capital acquisitions

- Sales or other dispositions

- Current period depreciation expense, with disclosure of the amounts charged to each of the functions in the statement of activities

Required disclosures about long-term liabilities (for both debt and other long-term liabilities include

- Beginning- and end-of-year balances (regardless of whether prior year data are presented on the face of the government-wide financial statements)

- Increases and decreases (separately presented)

- The portions of each item that are due within one year of the statement date

- Which governmental funds typically have been used to liquidate other long-term liabilities (such as compensated absences and pension liabilities) in prior years

In addition, GASBS 34 requires governments that report enterprise funds or that use enterprise fund accounting and financial reporting report certain segment information for those activities in the notes to the financial statements. A segment for these disclosure purposes is defined as “. . .an identifiable activity reported as or within an enterprise fund or another stand-alone entity for which one or more revenue bonds or other revenue-backed debt instruments (such as certificates of participation) are outstanding. A segment has a specific identifiable revenue stream pledged in support of revenue bonds or other revenue-backed debt, and business-related expenses, gains and losses, assets, and liabilities that can be identified.” GASBS 34 specifies that disclosure requirements be met by providing condensed financial statements and other disclosures as follows in the notes to the financial statements:

One accounting area of special interest to governments is that of interfund transactions. While the terminology used to refer to these transactions makes them appear more complicated than they actually are, the financial statement preparer and auditor must be familiar with the accounting for these transactions to properly reflect the financial position and results of operations of governmental entities. In addition, GASBS 34 provides guidance for certain transactions occurring between entities within the financial reporting entity, and low interfund balances and transactions should be presented.

The following sections describe the nature of and the accounting and reporting requirements for each of these types of interfund transactions. While this section addresses interfund transactions, consideration must also be given to transactions between a primary government and its component units. Transfers between the primary government and its blended component units and receivables and payables between the primary government and its blended component units are reported as described for interfund transactions by this chapter. However, for discretely presented component units, the amounts of balances and transfers between the primary government and its discretely presented component units should be reported separately from interfund balances and transfers from other funds. In addition, due to and due from amounts between the same two funds are allowed to be netted when a right of offset exists. Since component units are legally separate entities, it is not likely that a right of offset will exist for receivables and payables between one fund and a blended component unit. Care must be taken to ensure that amounts are not netted for blended component units when there is no right of offset.

Loans

Loans may be the easiest of the interfund transactions to understand and record. Loans between funds are treated as balance sheet transactions; the borrowing fund reports a liability and increase in cash, and the loaning fund reports a receivable and a decrease in cash. There is no effect on the operating statement for loans between funds.

In addition, these loans should be reported as fund assets or liabilities regardless of whether the loan will be repaid currently or noncurrently. Accordingly, governmental funds should report all interfund loans in the fund itself, rather than in the government-wide financial statements. For the funds that record a receivable as a result of an interfund loan, if the receivable is not considered an expendable available resource, a reservation of fund balance should be recorded.

| Due from capital projects fund | 10,000 | |

| Cash | 10,000 | |

| To record a loan to the capital projects fund |

| Cash | 10,000 | |

| Due to general fund | 10,000 | |

| To record a loan from the general fund |

The above example makes clear that the operating statements of the two funds that enter into a loan transaction are not affected. However, the substance of the transaction should also be considered. In a loan transaction, there should be an intent to actually repay the amount to the loaning fund. Without an intent to repay, the transaction might more appropriately be accounted for as a transfer, which is described more fully later in this chapter.

Reimbursements

A reimbursement is an expenditure or expense that is made in one fund, but is properly attributable to another fund. Many times, the general fund will pay for goods or services (such as a utility bill or rent bill) and is then reimbursed in whole or in part by other funds that benefit from the purchase. The proper accounting for reimbursements is to record an expenditure (or an expense) in the reimbursing fund and a reduction of expenditure (or expense) in the fund that is reimbursed.

| Expenditures—telephone | 5,000 | |

| Cash | 5,000 | |

| To record payment of telephone bill | ||

| Due from water utility fund | 1,000 | |

| Expenditures—telephone | 1,000 | |

| To record receivable for reimbursement for telephone bill |

| Expenditures—telephone | 4,000 | |

| Due from water utility fund | 1,000 | |