CHAPTER 14

CAPITAL ASSETS

Introduction

Capitalization Policy

Valuation of Assets Recorded

Capital Asset Accounting

Depreciation of Capital Assets

Modified Approach

Definition

Accounting and Financial Reporting for Intangible Assets Using the Economic Resources Measurement Focus

Internally Generated Intangible Assets

Internally generated computer software

Specific Amortization Issues

Impairment Indicator

Accounting and Financial Reporting for Intangible Assets Using the Current Financial Resources Measurement Focus

Impairment of Capital Assets

Definition of Impairment

Determining Whether a Capital Asset Is Impaired

Identifying events or circumstances that may indicate impairment

Testing for impairment

Measuring Impairment

Restoration cost method

Services unit method

Deflated depreciated replacement cost method

Reporting Impairment Losses

Insurance Recoveries

Disclosures Relating to Capital Assets

Service Concession Arrangements

Service Concession Arrangements within the Scope of GASBS 60

Transferor Accounting and Financial Reporting for Facilities and Related Payments Received from an Operator

Governmental Operator Accounting and Financial Reporting for the Right to Access Facilities and Related Payments to a Transferor

Accounting for Revenue Sharing Arrangements

Required Disclosures

Effective Date and Transition

Capitalization of Interest

Background

Amount of Interest to Be Capitalized

Capitalization Period

Capitalization of Interest Involving Tax-Exempt Borrowings and Certain Gifts and Grants

Disclosures

Summary

INTRODUCTION

Capital assets used in governmental activities under the pre-GASBS 34 financial reporting model were reported in the general fixed assets account group, which, as its name implies, was an account group and not a fund. GASBS 34 eliminated the use of the general fixed asset account group. Capital assets used in governmental activities are not reported in the fund financial statements, but are only reported in the government-wide statement of net assets. Capital assets used in proprietary funds are recorded by these funds. Information on recording capital assets in proprietary funds is included in Chapter 7.

This chapter describes the accounting and financial reporting basics. The following topics will be addressed:

- Basic accounting for capital assets

- Valuation of assets recorded, including accumulated depreciation

- Recording infrastructure assets

- Intangible assets

- Capital asset impairment

- Service concession arrangements

- Capitalization of interest

- Other financial reporting and disclosure considerations

Because of the nature of governmental financial reporting and operations, certain fixed assets are recorded in funds and others are recorded only in the government-wide financial statements. Generally, fixed assets for the proprietary funds (the enterprise funds and the internal service funds) are recorded in the funds themselves.

In addition, fixed assets associated with trust funds are accounted for through those trust funds. For example, the principal or corpus amount of private-purpose funds may include fixed assets. In such cases, the fixed assets should be accounted for in the appropriate private-purpose trust fund. This assists in compliance with terms of the trust instrument, provides a deterrent to mismanagement of trust assets, and facilitates accounting for depreciation where the trust principal must be maintained intact.

Capital assets other than those accounted for in the proprietary funds or trust funds are considered capital assets used in governmental activities, that are accounted for only in the government-wide financial statements rather than in the individual governmental funds.

The reason that capital assets used in governmental activities are not recorded in the governmental funds is that the measurement focus of the governmental funds is the current financial resources measurement focus. Capital assets do not represent current financial resources available for expenditure, but rather are considered items for which financial resources have been used and for which accountability should be maintained. Accordingly, they are considered not to be assets of the governmental funds, but are rather accounted for as assets of the government as a whole. NCGAS 1 determined that the primary purposes for governmental fund accounting are to reflect its revenues and expenditures (that is, the sources and uses of its financial resources) and its assets, related liabilities, and net financial resources available for appropriation and expenditure. To best meet these objectives, capital assets need to be excluded from the governmental fund accounts and instead be recorded only in the government-wide financial statements. Note that conceptually GASBS 34 is similar, as will be described later in this chapter. Instead of recording these fixed assets in an account group, however, they are recorded in the government-wide statement of net assets.

The types of assets that should be included as capital assets used in governmental activities are those typically termed capital assets; that is, those that meet the capitalization criteria of the government. The more common classes used to categorize capital assets by governments are as follows:

- Land

- Buildings

- Equipment

- Improvements other than buildings

- Construction in progress

- Intangibles

- Infrastructure

In addition, capital assets include those acquired in substance through noncancelable leases. Lease capitalization and disclosure requirements are more fully described in Chapter 19. The cost of infrastructure assets is also included in capital assets used in governmental activities. This requirement is discussed more fully in a later section of this chapter.

Capitalization Policy

To determine what assets will be treated as capital assets (regardless of whether it is a capital asset used in governmental or business-type activities or a capital asset of a proprietary fund) in practice, governments typically set thresholds for when assets may be considered for capitalization. For example, a government may determine that in order to be treated as a capitalized asset, an asset should cost at least $5,000 and have a useful life of five years. Note that this threshold applies only to items that are appropriately capitalizable by their nature. For example, a repair or maintenance expenditure of $7,000 would not be capitalized even if the threshold were $5,000. The threshold would apply to items that would normally be capitalized and is used to prevent too many small assets from being capitalized, which becomes difficult for governments to manage. Continuing the $5,000 threshold example, a personal computer purchased for $4,000 would not be capitalized. However, ten personal computers purchased as part of the installation of an integrated computer network would be eligible for capitalization in this example.

VALUATION OF ASSETS RECORDED

As a general rule, capital assets should be initially recorded at cost. Cost is defined as the consideration that is given or received, whichever is more objectively determinable. In most instances, cost will be based on the consideration that the government gave for the asset, because that will provide the most objective determination of the cost of the asset.

The cost of a capital asset includes not only its purchase price or construction cost, but also any ancillary costs incurred that are necessary to place the asset in its intended location and in condition where it is ready for use. Ancillary charges will depend on the nature of the asset acquired or constructed, but typically include costs such as freight and transportation charges, site preparation expenditures, professional fees, and legal claims directly attributable to the asset acquisition or construction. An example of legal claims directly attributable to an asset acquisition is liability claims resulting from workers or others being injured during the construction of an asset, or damage done to the property of others as a direct result of the construction activities.

It is relatively easy to ascertain the costs of capital assets that are purchased currently. Contracts, purchase orders, and payment information is available to determine the acquisition or construction costs. The cost of a capital asset includes not only its purchase price or construction cost, but also whatever ancillary charges are necessary to place the asset in its intended location and in condition for its intended use. Thus, among the costs that should be capitalized as part of the cost of a capital asset are the following:

- Professional fees, such as architectural, legal, and accounting fees

- Transportation costs, such as freight charges

- Legal claims directly attributable to the asset acquisition

- Title fees

- Closing costs

- Appraisal and negotiation fees

- Surveying fees

- Damage payments

- Land preparation costs

- Demolition costs

- Insurance premiums during the construction phase

- Capitalized interest (discussed later in this chapter)

The reporting of capital assets by governments was not always common. As governments worked to adopt the requirements of NCGAS 1, they were faced with the task of establishing capital asset records and valuation after many years of financial reporting without them. In these situations, many of the supporting documents and records that might contain original cost information were no longer available to establish the initial cost of these previously unrecorded assets.

Governments often found it necessary to estimate the original costs of these assets on the basis of such documentary evidence as may be available, including price levels at the time of acquisition, and to record these estimated costs in the appropriate fixed asset records. While this problem will diminish in size as governments retire or dispose of these assets with estimated costs, the notes to the financial statements should disclose the extent to which fixed asset costs have been estimated and the method (or methods) of estimation. Similar consideration needs to be made for the retroactive recording of infrastructure assets under GASBS 34.

Governments sometimes acquire capital assets by gift. When these fixed assets are recorded, they should be recorded at their estimated fair value at the time of acquisition by the government.

Capital Asset Accounting

As described earlier in this chapter, in the government-wide financial statements, capital assets should be reported at historical cost. Cost includes capitalized interest and ancillary costs (freight, transportation charges, site preparation fees, professional fees, etc.) necessary to place an asset into its intended location and condition for use.

One of the most significant aspects of GASBS 34 is its definition of what is included in capital assets: land, improvements to land, easements, buildings, building improvements, vehicles, machinery, equipment, works of art and historical treasures, infrastructure, and all other tangible and intangible assets that are used in operations and that have initial useful lives extending beyond a single reporting period. The GASB 34 Implementation Guide defines land improvements to consist of betterments, other than building, that ready land for its intended use. Examples provided of land improvements include site improvements such as excavations, fill, grading, and utility installation; removal, relocation, or reconstruction of the property of others, such as railroads and telephone and power lines; retention walls; parking lots, fencing, and landscaping.

Included in this definition are infrastructure assets. Previously, governments (not including proprietary funds) had the option of capitalizing infrastructure assets, and many, if not most, did not. (Infrastructure assets are defined by GASBS 34 as “long-lived capital assets that normally are stationary in nature and normally can be preserved for a significantly greater number of years than most capital assets.”) Examples of infrastructure assets are roads, bridges, tunnels, drainage systems, water and sewer systems, dams, and lighting systems.

All governments are required to report general infrastructure capital assets prospectively. Retroactive capitalization of infrastructure assets required by GASBS 34 becomes more complicated.

- Phase 3 governments (governments with total annual revenues of less than $10 million) did not have to retroactively record infrastructure assets, although they are encouraged to do so.

- Phase 1 governments (governments with total annual revenues of $100 million or more) and Phase 2 governments (governments with total annual revenues of $10 million, but less than $100 million) were required to retroactively report all major general infrastructure assets. Specifically, Phase 1 and Phase 2 governments are required to capitalize and report major general fixed assets that were acquired in fiscal years ending after June 30, 1980, or that received major renovations, restorations, or improvements during that period.

- The cost or estimated cost of a subsystem is expected to be at least 5% of the total cost of all general capital assets reported in the first fiscal year ending after June 30, 1999.

- The cost or estimated cost of a network is expected to be at least 10% of the total cost of all general capital assets reported in the first fiscal year ending after June 15, 1999.

DEPRECIATION OF CAPITAL ASSETS

Depreciation expense and the related accumulated depreciation are recorded in the government-wide statement of activities and in proprietary funds in a manner similar to that used by commercial entities.

In calculating depreciation, governments should follow the same acceptable depreciation methods used by commercial enterprises. There is actually very little authoritative guidance issued by the FASB and its predecessor standard-setting bodies. In fact, the financial statement preparer would need to go back to AICPA Accounting Research Bulletin 43 (ARB 43), Restatement and Revision of Accounting Research Bulletins, to find a definition of depreciation accounting, which is a system of accounting that aims to distribute the cost or other basic value of tangible capital assets, less any salvage value, over the estimated useful life of the unit (which may be a group of assets) in a systematic and rational manner. Viewed differently, depreciation recognizes the cost of using up the future economic benefits or service potentials of long-lived assets.

In addition to obtaining the original cost information described in the preceding section to this chapter, a government must determine the salvage value (if any) of an asset, the estimated useful life of the asset, and the depreciation method that will be used.

In practice, many governments usually assume that there will be no salvage value to the asset that they are depreciating. Governments tend to use things for a long time, and many of the assets that they record are useful only to the government, so there is no ready after-market for these assets. For example, what is the salvage value of a fully depreciated sewage treatment plant? Similarly, there is probably no practical use for used personal computer equipment, because governments are inclined to use these types of assets until they are virtually obsolete, which makes salvage value generally low. However, these governmental operating characteristics aside, if the government determines that there is likely to be salvage value for an asset being depreciated, the estimated salvage value should be deducted from the cost of the capital asset to arrive at the amount that will be depreciated. (In certain accelerated depreciation methods, such as the double-declining balance method, salvage value is not considered.)

Next, the government should determine the estimated useful lives of the assets that will be depreciated. Usually assets are grouped into asset categories and a standard estimated life or a range of estimated lives is used for each class.

Following are some common depreciable asset categories:

- Buildings

- Leasehold improvements

- Machinery and equipment

- Office equipment

- Infrastructure, including roads, bridges, parks, etc.

Two areas to keep in mind are that land is not depreciated, because it is assumed to have an indefinite life. Costs accumulated as on asset representing construction work in progress are also not depreciated until the assets being constructed are placed in service. In addition, as will be discussed in Chapter 22, capital assets that are recorded as a result of capital lease transactions are also considered part of the depreciable assets of a governmental organization.

The final component of the depreciation equation that a government needs to determine is the method that it will use. The most common method used by governments is the straight-line method of depreciation in which the amount to be depreciated is divided by the asset’s useful life, resulting in the same depreciation charge in each year.

Accelerated methods of depreciation, such as the sum-of-the-year’s digits and the double-declining balance methods, may also be used. However, their use is far less popular than the straight-line method. Although proprietary funds do use a measurement focus and basis of accounting that result in a determination of net income similar to that of a commercial enterprise, there is less emphasis on the bottom line of proprietary activities than there would be for a publicly traded corporation, for instance. Reflecting this lower degree of emphasis, governments sometimes elect to follow the straight-line method of depreciation more for simplicity purposes, rather than for analyzing whether their assets actually do lose more of their value in the first few years of use.

Governments should also disclose their depreciation policies in the notes to the financial statements. For the major classes of capital assets, the range of estimated useful lives that are used in the depreciation calculations should be disclosed. The governmental organization should also disclose the depreciation method used in computing depreciation.

Since the government-wide financial statements are prepared using the economic resources measurement focus, depreciation on capital assets is recorded. This was another highly controversial issue of GASBS 34. In response to commentary that infrastructure assets do not depreciate in value in the traditional sense, GASBS 34 allows a “modified approach” as to depreciation on qualifying infrastructure assets, as discussed below.

The theory behind using the modified approach is that infrastructure assets are different than what would be considered a “typical” capital asset. For example, say a garbage truck is a typical capital asset that has an estimated life of ten years. It would be expected that the government would sell or “junk” the truck after ten years and buy a new one. The cost of the original truck is charged as depreciation expense over its ten-year life, which matches the period over which its benefits were received by the government.

Now try to apply this theory to an infrastructure asset, such as a bridge. Even a newly constructed bridge has an estimated life of forty to fifty years; is it likely that the government will really stop using the bridge after forty or fifty years and build a new one? Probably not. What is more likely to happen is that the government will perform not only standard repair work on the bridge almost immediately after it is placed in service, but will also perform significant capital improvements to the bridge over time to keep it in a good state of repair throughout its existence. These capital improvements will likely extend the useful life of the bridge far beyond the otherwise expected useful life of forty or fifty years. The modified approach as applied to infrastructure assets is an attempt to recognize the existence of the fact pattern discussed in this paragraph. Depreciation on infrastructure assets under the optional modified approach is not recorded as long as the government keeps the asset (in this case the bridge) at a set level of condition or state of repair. All costs to keep the asset in the stated condition level are expensed as incurred, regardless of whether they are standard repairs or are part of a major capital improvement.

Basically, depreciation rules (aside from the modified approach) follow those currently used by proprietary funds, as well as by commercial enterprises, which are described earlier in this section. Capital assets are reported in the statement of net assets net of accumulated depreciation. (Capital assets that are not depreciated, such as land, construction in progress, and infrastructure assets using the modified approach, should be reported separately from capital assets being depreciated in the statement of activities.) Depreciation expense is recorded in the statement of activities and is reported as an expense of the individual programs or functions that have identifiable depreciable assets. Capital assets are depreciated over their estimated useful lives, except for land and land improvements and infrastructure assets using the modified approach.

Depreciation expense may be calculated by individual assets or by classes of assets (such as infrastructure, buildings and improvements, vehicles, and machinery and equipment). In addition, depreciation may be calculated for networks of capital assets or for subsystems of a network of capital assets. A network of assets is composed of all assets that provide a particular type of service for a government. A network of infrastructure assets may be only one infrastructure asset that is composed of many components. A subsystem of a network of assets is composed of all assets that make up a similar portion or segment of a network of assets. The GASBS 34 Implementation Guide provides the example of a water distribution system of a government, which could be considered a network. The pumping stations, storage facilities, and distribution mains could be considered subsystems of that network.

- The government estimates that it has 100 lane miles of road that it needs to capitalize. The current cost of constructing one lane mile of road is $1 million. The average age of a road is ten years, and the average estimated life of a road is twenty-five years. The average annual inflation rate for road construction projects over the last ten years is 4%. The government calculates that the current cost of constructing all of its roads is $100 million, which adjusted for ten years of inflation means that the average historical cost of a road is approximately $70 million. Using the straight-line depreciation method, accumulated depreciation is calculated at $28 million ($70 million divided by 25, multiplied by 10.)

- The government estimates that it spent $10 million each year on road construction over the last twenty years, for a total of $200 million. Each year it will capitalize the $10 million spent and depreciate 1/25 of the amount for the next twenty-five years, assuming the twenty-five-year estimated life. The calculation is repeated for each year of the prior twenty years, resulting in a total historical cost of $200 million and a cumulative amount of depreciation that would have been taken over the last twenty years.

Modified Approach

Infrastructure assets that are part of a network or subsystem of a network are not required to be depreciated if two requirements are met.

GASBS 34 requires that governments using the modified approach should document that

When the modified approach is used, GASBS 34 requires governments to present the following schedules, derived from asset management systems, as RSI for all eligible infrastructure assets that are reported using the modified approach:

The following are the GASBS 34 specified disclosures that should accompany this schedule:

Failure to meet these conditions would preclude a government from continuing to use the modified approach.

The GASB issued Statement 51, Accounting and Financial Reporting for Intangible Assets (GASBS 51), to address practice issues which had arisen as to the accounting and reporting for intangible assets and to provide guidance for how intangible assets, including internally developed intangible assets, should be accounted for and reported.

Definition

GASBS 51 defines an intangible asset as an asset that possesses all of the following characteristics:

GASBS 51 includes in its scope all intangible assets except for the following:

Accounting and Financial Reporting for Intangible Assets Using the Economic Resources Measurement Focus

GASBS 51 provides that all intangible assets included in its scope be classified as capital assets. Accordingly, existing authoritative guidance related to the accounting and financial reporting for capital assets, including the areas of recognition, measurement, depreciation (termed amortization for intangible assets), impairment, presentation, and disclosures should be applied to intangible assets, as applicable. The provisions of GASBS 51 described in the following paragraphs should be applied to intangible assets in addition to the existing authoritative guidance for capital assets.

An intangible asset should be recognized in the statement of net assets only if it is identifiable. GASBS 51 considers an intangible asset to be identifiable when either of the following conditions is met:

Internally Generated Intangible Assets

GASBS 51 considers intangible assets to be considered internally generated if they are created or produced by the government or an entity contracted by the government, or if they are acquired from a third party but require more than minimal incremental effort on the part of the government to begin to achieve their expected level of service capacity.

Outlays incurred related to the development of an internally generated intangible asset that is identifiable should be capitalized only upon the occurrence of all of the following:

Only outlays incurred subsequent to meeting the above criteria should be capitalized.

Outlays incurred prior to meeting those criteria should be expenses as incurred.

Internally generated computer software

Computer software is a common type of intangible asset that is often internally generated. Computer software should be considered internally generated if it is developed in-house by the government’s personnel or by a third-party contractor on behalf of the government. Commercially available software that is purchased or licensed by the government and modified using more than minimal incremental effort before being put into operation also should be considered internally generated for purposes of this Statement. For example, licensed financial accounting software that the government modifies to add special reporting capabilities would be considered internally generated.

The activities involved in developing and installing internally generated computer software can be grouped into the following stages:

Data conversion should be considered an activity of the application development stage only to the extent it is determined to be necessary to make the computer software operational, that is, in condition for use. Otherwise, data conversion should be considered an activity of the postimplementation/operation stage.

For internally generated computer software, the recognition criteria described above should be considered to be met only when both of the following occur:

Accordingly, outlays associated with activities in the preliminary project stage should be expensed as incurred. For commercially available software that will be modified to the point that it is considered internally generated, 1. and 2. above generally could be considered to have occurred upon the government’s commitment to purchase or license the computer software.

Once the recognition criteria have been met, as described above, outlays related to activities in the application development stage should be capitalized. Capitalization of such outlays should cease no later than the point at which the computer software is substantially complete and operational. Outlays associated with activities in the postimplementation/operation stage should be expensed as incurred.

GASBS 51 notes that the activities within the stages of development described above may occur in a sequence different from that shown. GASBS 51 provides that the recognition guidance for outlays associated with the development of internally generated computer software set forth above should be applied based on the nature of the activity, not the timing of its occurrence. For example, outlays associated with application training activities that occur during the application development stage should be expensed as incurred.

Outlays associated with an internally generated modification of computer software that is already in operation should be capitalized in accordance if the modification results in any of the following:

If the modification does not result in any of the above outcomes, the modification should be considered maintenance, and the associated outlays should be expensed as incurred.

Specific Amortization Issues

GASBS 51 provides that the useful life of an intangible asset that arises from contractual or other legal rights should not exceed the period to which the service capacity of the asset is limited by contractual or legal provisions. Renewal periods related to such rights may be considered in determining the useful life of the intangible asset if there is evidence that the government will seek and be able to achieve renewal and that any anticipated outlays to be incurred as part of achieving the renewal are nominal in relation to the level of service capacity expected to be obtained through the renewal. Such evidence should consider the required consent of a third party and the satisfaction of conditions required to achieve renewal, as applicable.

Under GASBS 51, an intangible asset is considered to have an indefinite useful life if there are no legal, contractual, regulatory, technological, or other factors that limit the useful life of the asset. A permanent right-of-way easement is the example provided of an intangible asset that should be considered to have an indefinite useful life. GASBS 51 provides that intangible assets with indefinite useful lives should not be amortized. If changes in factors and conditions result in the useful life of an intangible asset no longer being indefinite, the asset should be tested for impairment because a change in the expected duration of use of the asset has occurred. The carrying value of the intangible asset, if any, following the recognition of any impairment loss should be amortized in subsequent reporting periods over the remaining estimated useful life of the asset.

Impairment Indicator

In addition to the indicators included in GASBS Statement 42, Accounting and Financial Reporting for Impairment of Capital Assets and for Insurance Recoveries (which is discussed in the following section) a common indicator of impairment for internally generated intangible assets is development stoppage, such as stoppage of development of computer software due to a change in the priorities of management. Internally generated intangible assets impaired from development stoppage should be reported at the lower of carrying value or fair value.

Accounting and Financial Reporting for Intangible Assets Using the Current Financial Resources Measurement Focus

GASBS 51 provides that outlays associated with intangible assets subject to its provisions should be reported as expenditures when incurred in financial statements prepared using the current financial resources measurement focus.

Retroactive reporting of intangible assets considered to have indefinite useful lives as of the effective date of GASBS 51 is not required but is permitted. Retroactive reporting of internally generated intangible assets (including ones that are in development as of the effective date of GASBS 51) also is not required but is permitted to the extent that the approach in paragraph 8 can be effectively applied to determine the appropriate historical cost of an internally generated intangible asset as of the effective date of the Statement.

The provisions of GASBS 51 related to intangible assets with indefinite useful lives should be applied retroactively only for intangible assets previously subjected to amortization that have indefinite useful lives as of the effective date of the Statement. Accumulated amortization related to these assets reported prior to the implementation of the Statement should be restated to reflect the fact that these assets are not to be amortized.

Impairment of Capital Assets

The GASB issued Statement 42, Accounting and Financial Reporting for Impairment of Capital Assets and for Insurance Recoveries (GASBS 42) to provide guidance for accounting for the impairment of capital assets. GASBS 42 also addresses the accounting for insurance recoveries, but by far the most significant aspects of the new statement will concern impairment of capital assets. GASBS 42 applies to all of the capital assets of a government, including its infrastructure assets.

Many readers may be familiar with the Financial Accounting Standards Board’s Statement 144, Accounting for the Impairment or Disposal of Long-Lived Assets (SFAS 144). While GASBS 42 addresses the same basic topic as SFAS 144, its approach is actually quite different from what is found in the FASB Statement. In SFAS 144, determination of impairment is based upon expected cash flows from the asset that is being evaluated for impairment. In the governmental environment, many or most capital assets don’t provide cash flows, nor are they expected to provide cash flows. GASBS 42 presents the GASB’s solutions as to how to identify and measure impairment in the governmental environment.

Definition of Impairment

GASBS 42 defines asset impairment as a significant, unexpected decline in the service utility of a capital asset. The events or circumstances that lead to impairments are not considered normal and ordinary, meaning that they wouldn’t be expected to occur during the useful life of the capital asset at the time that it was acquired.

GASBS 42 provides guidance on what is meant by the term service utility. The service utility of a capital asset is the usable capacity that, at the time of acquisition, was expected to be used to provide service. The current usable capacity of a capital asset may be due to normal or expected decline in useful life or it may be due to impairing events, which are discussed in the following pages.

Determining Whether a Capital Asset Is Impaired

GASBS 42 provides a two-step process in determining whether a capital asset is impaired.

Each of these steps is described in greater detail below.

Identifying events or circumstances that may indicate impairment

The events contemplated by GASBS 42 that may indicate impairment are prominent events, meaning that they are conspicuous or known to the government, and would be expected to have been discussed by governing boards, management, and/or the media. The following are provided by GASBS 42 as indicators of impairment:

Testing for impairment

If an asset has been identified as potentially impaired by the indicators described above, the second step is to determine if impairment has incurred. GASBS 42 provides that the asset should be tested for impairment if both of the following factors are present:

- The magnitude of the decline in service utility is significant. GASBS 42 does not provide any specific methods to evaluate “significant” but does provide the example of expenses associated with the continued operation and maintenance or costs associated with restoration being “significant” in relationship to the current service utility of the asset.

- The decline in service utility is unexpected. This means that the restoration cost or other impairment circumstance is not part of the normal life cycle of the capital asset.

If both of these tests are met and the capital asset is determined to be impaired, the government would use the guidance of GASBS 42 in the following section to measure that impairment. If an asset was indicated to be impaired, but does not meet both of these two tests, GASBS 42 provides that the estimates used in depreciation calculations, such as remaining useful life and salvage value, should be reevaluated and changed if considered necessary.

Measuring Impairment

To measure the impairment for capital assets meeting the above tests, the government should next determine whether the impaired capital assets will be used by the government. Impaired capital assets that will no longer be used by the government should be reported at the lower of carrying value or fair value. This also applies to capital assets impaired from construction work stoppage, which are also reported at the lower of carrying or fair value.

For impaired capital assets that will continue to be used by the government, determination of the amount of the impairment (the historical cost that should be written off) is more complicated. GASBS 42 provides three different methods that are described below.

Restoration cost method

The amount of the impairment is derived from the estimated costs to restore the utility of the capital asset, not including any amounts attributable to improvements or additions. The estimated restoration cost is converted to historical cost by either restating the estimated restoration cost using an appropriate cost index or by applying a ratio of estimated restoration cost over estimated replacement cost to the carrying amount of the asset.

Service units method

The amount of the impairment is derived from isolating the historical cost of the service utility that cannot be used due to the impairment event or change in circumstances. The amount of the service units impaired is determined by evaluating the service units provided by the capital asset both before and after the impairment.

Deflated depreciated replacement cost method

The amount of the impairment is derived from obtaining a current cost for a capital asset to replace the current level of service estimated. The estimated current cost is then depreciated (since the capital asset being replaced is not new) and deflated to convert the cost to historical cost dollars.

GASBS 42 identifies generally which method should be used from the various causes of impairment as follows:

Reporting Impairment Losses

GASBS 42 provides that most impairment losses should be considered permanent (requiring a write-down of the asset) unless evidence is available to demonstrate that the impairment will be temporary. Impairment losses (other than temporary impairments) should be reported in the statement of activities and statement of revenues, expenses, and changes in fund net assets, if appropriate, as a program or operating expense, special item, or extraordinary item in accordance with the guidance of GASBS 34. If not apparent from the face of the financial statements, a general description, amount, and the financial statement classification of the impairment loss should be disclosed in the notes to the financial statements. The carrying amount of impaired capital assets that are idle at year-end should be disclosed, regardless of whether the impairment is considered permanent or temporary.

Once an impairment loss has been recorded for an asset, the value of that asset should not be written up in the future if events affecting the circumstances of the impairment change.

Insurance Recoveries

In the governmental fund financial statements, GASBS 42 provides that restoration or replacement of a capital asset should be reported as a separate transaction from the insurance recovery. The insurance recovery is reported as an other financing source or an extraordinary item, as appropriate.

In the government-wide financial statements (and in proprietary fund financial statements) the restoration or replacement of an impaired capital asset is also reported as a separate transaction from the impairment loss and associated insurance recovery. The impairment loss should be reported net of the associated insurance recovery when the recovery and loss occur in the same year. Insurance recoveries in subsequent years should be reported as program revenue or as an extraordinary item, as appropriate. Insurance recoveries should only be recognized when realized or realizable. If an insurance company has admitted or acknowledged coverage, an insurance recovery would be considered by GASBS 42 to be realizable.

If not apparent from the financial statements, the amount and classification of insurance recoveries should be disclosed.

DISCLOSURES RELATING TO CAPITAL ASSETS

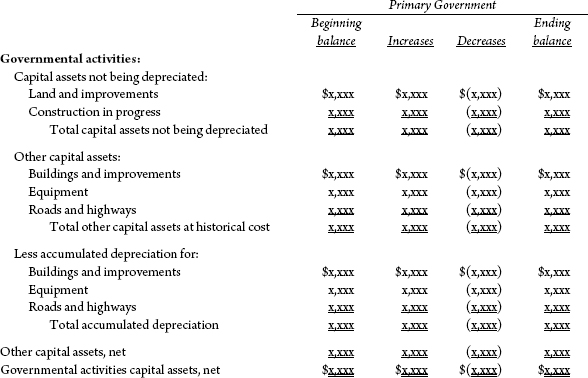

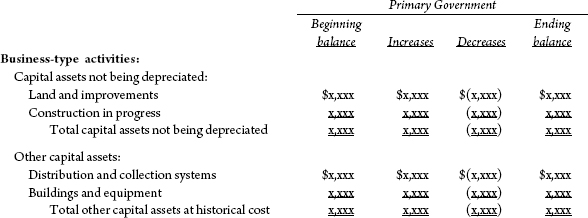

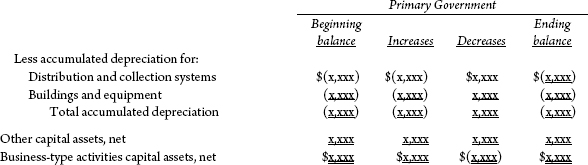

GASBS 34 requires that information about changes in capital assets used in governmental activities and business-type activities be disclosed about major classes of capital assets. Exhibit 1 is an illustrative note disclosure for capital assets.

| Governmental activities: | |

| General government | $ xxx |

| Public safety | xxx |

| Health and sanitation | xxx |

| Culture and recreation | xx |

| Transportation | xx |

| Total governmental activities depreciation expense | $x,xxx |

| Business-type activities: | |

| Water | $ xxx |

| Sewer | xxx |

| Total business-type activities depreciation expense | $x,xxx |

SERVICE CONCESSION ARRANGEMENTS

The GASB issued Statement No. 60 (GASBS 60), Accounting and Financial Reporting for Service Concession Arrangements, to provide accounting guidance for certain transactions that are broadly referred to as public-private (or public-public) partnerships, but more specifically called service concession arrangements. A service concession arrangement is an arrangement between a transferor (a government) and an operator (governmental or nongovernmental entity) in which (1) the transferor conveys to an operator the right and related obligation to provide services through the use of infrastructure or another public asset (a “facility”) in exchange for significant consideration and (2) the operator collects and is compensated by fees from third parties.

GASBS 60 applies only to those arrangements in which specific criteria determining whether a transferor has control over the facility are met. One of the key questions answered by GASBS 60 regarding these types of arrangements is what entity records the asset? Does the transferor government keep the asset on its books, or is the asset recorded by the operator? As will be discussed in greater detail below, GASBS 60 provides that a transferor reports the facility subject to a service concession arrangement as its capital asset, generally following existing measurement, recognition, and disclosure guidance for capital assets. New facilities constructed or acquired by the operator or improvements to existing facilities made by the operator are reported at fair value by the transferor. A liability is recognized, for the present value of significant contractual obligations to sacrifice financial resources imposed on the transferor, along with a corresponding deferred inflow of resources. Revenue is recognized by the transferor in a systematic and rational manner over the term of the arrangement.

In short, there are several key items to keep in mind when applying GASBS 60 to a service concession arrangement:

- The government transferring the operation of the asset (transferor) will keep the asset recorded on its books.

- A new or improved facility will be recorded by the government at present value.

- A liability may need to be recognized for obligations that the government undertakes as part of the arrangement

- The offset to a new asset recorded or a liability incurred is defined as a deferred inflow or outflow of resources that will be recognized over the life of the arrangement.

- Any up-front payment received (net of any obligations occurred) is also defined as a deferred inflow of resources and recognized over the life of the arrangement.

Keeping these basic tenets in mind will make understanding the specific requirements of GASBS 60 easier to achieve.

In addition, it’s important to note that the provisions of GASBS 60 are applied to the financial statements of governments that are prepared using the economic resources measurement focus, which would include proprietary funds as well as government-wide financial statements.

Service Concession Arrangements within the Scope of GASBS 60

GASBS 60 establishes guidance for accounting and financial reporting for service concession arrangements, which as used in GASBS 60 are defined as an arrangement between a government (the transferor) and an operator (which may be a governmental entity [governmental operator] or a nongovernmental entity) in which all of the following criteria are met:

GASBS 60 notes that service concession arrangements within its scope include, but are not limited to

Transferor Accounting and Financial Reporting for Facilities and Related Payments Received from an Operator

GASBS 60 provides that if the facility associated with a service concession arrangement is an existing facility, the transferor should continue to report the facility as a capital asset.

Further, if the facility associated with a service concession arrangement is a new facility purchased or constructed by the operator, or an existing facility that has been improved (i.e., increases the capacity or efficiency of the facility rather than preserve its useful life) by the operator, the transferor should report (1) the new facility or the improvement as a capital asset at fair value when it is placed in operation, (2) any contractual obligations as liabilities, and (3) a corresponding deferred inflow of resources equal to the difference between (1) and (2).

GASBS 60 also provides that a transferor should recognize a liability for certain obligations to sacrifice financial resources under the terms of the arrangement. Liabilities associated with the service concession arrangement should be recorded at their present value if a contractual obligation is significant and meets either of the following criteria:

After initial measurement, the capital asset is subject to existing requirements for depreciation, impairment, and disclosures. However, GASBS 60 provides that the capital asset should not be depreciated if the arrangement requires the operator to return the facility to the transferor in its original or an enhanced condition. The corresponding deferred inflow of resources should be reduced and revenue should be recognized in a systematic and rational manner over the term of the arrangement, beginning when the facility is placed into operation.

If a liability is recorded to reflect a contractual obligation to sacrifice financial resources as described above, the liability should be reduced as the transferor’s obligations are satisfied. As obligations are satisfied, a deferred inflow of resources should be reported and the related revenue should be recognized in a systematic and rational manner over the remaining term of the arrangement. Improvements made to the facility by the operator during the term of the service concession arrangement should be capitalized as they are made and also are subject to requirements for depreciation, impairment, and disclosures.

If a service concession arrangement requires up-front or installment payments from the operator, GASBS 60 provides that the transferor should report (1) the up-front payment or present value of installment payments as an asset, (2) any contractual obligations as liabilities, and (3) related deferred inflow of resources equal to the difference between (1) and (2). Revenue should be recognized as the deferred inflow of resources is reduced. This revenue should be recognized in a systematic and rational manner over the term of the arrangement. A liability should be recognized if the transferor has contractual obligations that meet the criteria described above.

Governmental Operator Accounting and Financial Reporting for the Right to Access Facilities and Related Payments to a Transferor

If the operator is a government operator, GASBS 60 provides that the governmental operator report an intangible asset for the right to access the facility and collect third-party fees from its operation at cost (such as the amount of an up-front payment or the cost of construction of or improvements to the facility). The cost of improvements to the facility made by the governmental operator during the term of the service concession arrangement should increase the governmental operator’s intangible asset if the improvements increase the capacity or efficiency of the facility. The intangible asset should be amortized over the term of the arrangement in a systematic and rational manner.

GASBS 60 notes that some agreements require a facility to be returned in a specified condition. If information that is prominent (conspicuous or known to the governmental operator) indicates the facility is not in the specified condition and the cost to restore the facility to that condition is reasonably estimable, then a liability and, generally, an expense to restore the facility should be reported. Governmental operators are not required to perform additional procedures to identify potential condition deficiencies beyond those already performed as part of their normal operations or those that may be required by the agreement.

Accounting for Revenue Sharing Arrangements

GASBS 60 also addresses service concession arrangements that include provisions for revenue sharing. A governmental operator that shares revenues with a transferor should report all revenue earned and expenses incurred—including the amount of revenues shared with the transferor—that are associated with the operation of the facility. In this circumstance, the transferor should recognize only its portion of the shared revenue when earned in accordance with the terms of the arrangement.

If revenue sharing arrangements contain amounts to be paid to the transferor regardless of revenues earned (for example, annual installments in fixed amounts), then the present value of those amounts should be reported by the transferor and governmental operators as if they were installment payments at the inception of the arrangement.

Required Disclosures

GASBS 60 provides that the following should be disclosed in the notes to financial statements of transferors and governmental operators for service concession arrangements:

GASBS 60 notes that some arrangements may include provisions for guarantees and commitments. For example, a transferor may become responsible for paying the debt of the operator in the event of a default, or the arrangement may include a minimum revenue guarantee to the operator. For each period in which a guarantee or commitment exists, GASBS 60 requires disclosures about guarantees and commitments, including identification, duration, and significant contract terms of the guarantee or commitment.

GASBS 60 provides that disclosure information for multiple service concession arrangements may be provided individually or in the aggregate for those that involve similar facilities and risk.

Effective Date and Transition

GASBS 60 is effective for financial statements for periods beginning after December 15, 2011, with earlier application encouraged. In the first period GASBS 60 is applied, changes made to comply with the statement should be treated as an adjustment of prior periods, and financial statements presented for the periods affected should be restated. If restatement is not practical, the cumulative effect of applying the statement, if any, should be reported as a restatement of beginning net assets for the earliest period restated. In the period the statement is first applied, the financial statements should disclose the nature of any restatement and its effect. Also, the reason for not restating prior periods presented should be explained.

CAPITALIZATION OF INTEREST

Some capital assets that are reported in proprietary funds are constructed. These funds would include in the cost of those constructed assets any interest cost that would ordinarily be capitalized under the accounting rules similar to those used for commercial enterprises. This accounting guidance is now promulgated for governments in GASBS 62, which adopted requirements essentially identical to those previously contained in FASB requirements.

Interest cost is capitalized for assets that require an acquisition period to get them ready for use. The acquisition period is the period beginning with the first expenditure for a qualifying asset and ending when the asset is substantially complete and ready for its intended use. The interest cost capitalization period starts when three conditions are met.

- Expenditures have occurred

- Activities necessary to prepare the asset (including administrative activities before construction) have begun

- Interest cost has been incurred

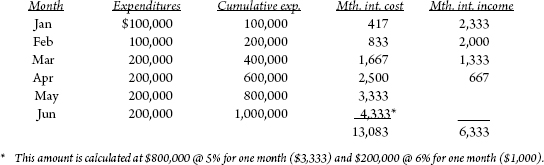

The amount of interest cost capitalized should not exceed the actual interest cost applicable to the proprietary fund that is incurred during the reporting period. To compute the amount of interest cost to be capitalized for a reporting period, the average cumulative expenditures for the qualifying asset during the reporting period must be determined. In order to determine the average accumulated expenditures, each expenditure must be weighted for the time it was outstanding during the reporting period.

To determine the interest rate to apply against the weighted-average of expenditures computed in the preceding paragraph, the government should determine if the construction is being financed with a specific borrowing. If it is, which in the governmental environment is fairly likely, then the interest rate of that specific borrowing should be used. In other words, this interest rate, multiplied by the weighted-average of expenditures on the qualifying assets, would be the amount of interest that is capitalized. If no specific borrowing is made to acquire the qualifying asset, the weighted-average interest rate incurred on other borrowings outstanding during the period is used to determine the amount of interest cost to be capitalized.

As stated above, the amount of interest capitalized should not exceed the interest cost of the reporting period. In addition, interest is not capitalized during delays or interruptions, other than brief interruptions, that occur during the acquisition or development phase of the qualifying asset.

Background

As described earlier in this chapter, the historical cost of acquiring an asset includes the costs incurred necessary to bring the asset to the condition and location necessary for its intended use. If an asset requires a period in which to carry out the activities necessary to bring it to that location and condition, the interest cost incurred during that period as a result of expenditures for the asset is part of the historical cost of the asset.

The objectives of capitalizing interest are the following:

- To obtain a measure of acquisition cost that more closely reflects the enterprise’s total investment in the asset, and

- To charge a cost that relates to the acquisition of a resource that will benefit future periods against the revenues of the periods benefited.

Conceptually, interest cost is capitalizable for all assets that require time to get them ready for their intended use, called the acquisition period. However, in certain cases, because of cost/benefit considerations in obtaining information, among other reasons, interest cost should not be capitalized. Accordingly, SFAS 34 specifies that interest cost should not be capitalized for the following types of assets:

- Inventories that are routinely manufactured or otherwise produced in large quantities on a repetitive basis

- Assets that are in use or ready for their intended use in the earnings activities of the entity

- Assets that are not being used in the earnings activities of the enterprise and are not undergoing the activities necessary to get them ready for use

- Assets that are not included in the balance sheet

- Investments accounted for by the equity method after the planned principal operations of the investee begin

- Investments in regulated investees that are capitalizing both the cost of debt and equity capital

- Assets acquired with gifts or grants that are restricted by the donor or the grantor to acquisition of those assets to the extent that funds are available from such gifts and grants (Interest earned from temporary investment of those funds that is similarly restricted should be considered an addition to the gift or grant for this purpose.)

- Land that is not undergoing activities necessary to get it ready for its intended use

- Certain oil- and gas-producing operations accounted for by the full cost method

After consideration of the above exceptions, interest should be capitalized for the following types of assets, referred to as qualifying assets:

- Assets that are constructed or otherwise produced for an entity’s own use, including assets constructed or produced for the enterprise by others for which deposits or progress payments have been made

- Assets that are for sale or lease and are constructed or otherwise produced as discrete projects, such as real estate developments

- Investments (equity, loans, and advances) accounted for by the equity method while the investee has activities in progress necessary to commence its planned principal operations, provided that the investee’s activities include the use of funds to acquire qualifying assets for its operations

Amount of Interest to Be Capitalized

The amount of interest cost to be capitalized for qualifying assets is intended to be that portion of the interest cost incurred during the assets’ acquisition periods that could theoretically be avoided if expenditures for the assets had not been made, such as avoiding interest by not making additional borrowings or by using the funds expended for the qualifying assets to repay borrowings that already exist.

The amount of interest that is capitalized in an accounting period is determined by applying an interest rate (known as the capitalization rate) to the average amount of the accumulated expenditures for the asset during the period. (Special rules may apply when qualifying assets are financed with tax-exempt debt. These rules are discussed later in this chapter.) The capitalization rates used in an accounting period are based on the rates applicable to borrowings outstanding during the accounting period. However, if an entity’s financing plans associate a specific new borrowing with a qualifying asset, the enterprise may use the rate on that specific borrowing as the capitalization rate to be applied to that portion of the average accumulated expenditures for the asset not in excess of the amount of the borrowing. If the average accumulated expenditures for the asset exceed the amounts of the specific new borrowing associated with the asset, the capitalization rate applicable to this excess should be a weighted-average of the rates applicable to the other borrowings of the entity.

GASBS 62 provides specific guidance on determining which borrowings should be considered in the weighted-average rate mentioned in the previous paragraph. The objective is to obtain a reasonable measure of the cost of financing the acquisition of the asset in terms of the interest cost incurred that otherwise could have been avoided. Judgment will likely be required to make a selection of borrowings that best accomplishes this objective in the particular circumstances of the governmental entity. For example, capitalized interest for capital assets constructed and financed by revenue bonds issued by a water and sewer authority should consider the interest rate of the water and sewer authority’s debt, rather than general obligation bonds of the government. The revenue bonds are likely to show a different, probably lower, rate than that of the general obligation bonds.

In addition to the above guidance on the calculation of the amount of capitalized interest, the amount of interest that is capitalized in an accounting period cannot exceed the total amount of interest cost incurred by the entity in that period.

Capitalization Period

Generally, the capitalization period begins when the following three conditions are met:

(The beginning of the capitalization period for assets financed with tax-exempt debt is described later in this chapter.)

Interest capitalization continues as long as the above three conditions continue to be met. The term activities is meant to be construed broadly. It should be considered to encompass more than physical construction. Activities are all the steps required to prepare the asset for its intended use, and might include

- Administrative and technical activities during the preconstruction phase

- Development of plans or the process of obtaining permits from various governmental authorities

- Activities undertaken after construction has begun in order to overcome unforeseen obstacles, such as technical problems, labor disputes, or litigation

If the governmental entity suspends substantially all activities related to the acquisition of the asset, interest capitalization should cease until activities are resumed. However, brief interruptions, interruptions that are externally imposed, and delays inherent in the asset acquisition process do not require interest capitalization to be interrupted.

When the asset is substantially completed and ready for its intended use, the capitalization period ends. The term substantially complete is used to prohibit the continuing of interest capitalization in situations in which completion of the asset is intentionally delayed. Interest cost should not be capitalized during periods when the entity intentionally defers or suspends activities related to the asset, because interest incurred during such periods is a holding cost and not an acquisition cost.

Capitalization of Interest Involving Tax-Exempt Borrowings and Certain Gifts and Grants

SFAS 62 addresses tax-exempt borrowings used to finance qualifying assets. Generally, interest earned by an entity is not offset against the interest cost in determining either interest capitalization rates or limitations on the amount of interest cost that can be capitalized. However, in situations where the acquisition of qualifying assets is financed with the proceeds of tax-exempt borrowings and those funds are externally restricted to finance the acquisition of specified qualifying assets or to service the related debt, this general principal is changed. The amount of interest cost capitalized on qualifying assets acquired with the proceeds of tax-exempt borrowings that are externally restricted as specified above is the interest cost on the borrowing less any interest earned on related interest-bearing investments acquired with proceeds of the related tax-exempt borrowings from the date of the borrowing until the assets are ready for their intended use.

In other words, when a specific tax-exempt borrowing finances a project, a governmental entity will earn interest income on bond proceeds that are invested until they are expended or required to be held in debt service reserve accounts. These interest earnings should be offset against the interest cost in determining the amounts of interest to be capitalized. Conceptually, the true interest cost to the government is the net of this interest income and interest cost. However, this exception to the general rule of not netting interest income against interest expense relates only to this specific exception relating to tax-exempt borrowings and where amounts received under gifts and grants are restricted to use in the acquisition of the qualifying asset.

Disclosures

In addition to the accounting requirements specified above, there are two disclosure requirements relating to capitalized interest.

SUMMARY

GASBS 34 significantly changes the way in which capital assets used in governmental activities of a government are reported. Implementation of the retroactive infrastructure reporting requirements is an important consideration for most governments, as are recent requirements for recording intangible assets and the impairment of assets.