Chapter 2

Lessons Not Learned

Timothy Geithner, who studied Japanese in college and served as the deputy financial attaché at the U.S. embassy in Tokyo in the early 1990s, wrote a memo a few years later to his bosses at the Department of the Treasury, detailing the problems with the Japanese banks. Geithner explained that the country’s banks were riddled with losses and couldn’t raise capital because investors suspected the value of the assets on their balance sheets to be lower than they’d declared. The memo got to Robert Rubin, then Secretary of the Treasury, who was very impressed with Geithner’s analysis and promoted Geithner to Assistant Secretary for International Affairs so he could help with the Asian crisis unfolding after years of zero interest-rate policy in Japan.

Around the same time, Professor Edward Kane penned a paper about the lessons Japan could draw from the mistakes U.S. authorities had made in the handling of their savings-and-loans crisis. Kane presented his paper to the Asian country’s finance ministry officials. The Japanese bureaucrats weren’t impressed though. They told Kane that his paper was useless because “they were much smarter than the Americans,” Kane recalls. Almost two decades later, Geithner seemed to be in the same frame of mind as those Japanese officials. First as the chairman of the Federal Reserve Bank of New York, and again after January 2009 as the Treasury Secretary, Geithner rejected any similarities with Japan and argued that Washington had acted more forcefully and with the right tools. In other words, we’re smarter than the Japanese, so why bother with the lessons from their crisis? His inability to see the parallels is hard to fathom when one considers Geithner’s own personal experience in Japan and his keen analysis of their problems at the time. Even so, when it comes to the problems of his own country’s banks, Geithner seems to have forgotten all the lessons from Japan he once pointed out.

Geithner, other U.S. officials, and their counterparts in Europe have all had the opportunity to learn from past mistakes. Most recently, the U.S. savings-and-loan crisis of the 1980s and Japan’s bank crisis in the 1990s give us a blueprint for how not to handle zombie banks. The problems today in the United States and throughout the European Union are like a nasty flashback.

The U.S. Thrift Crisis

Savings and loans banks—also referred to as thrifts or S&Ls—started out with a simple business model in the early nineteenth century. They would pool the savings of the local community to provide home loans to its members. That model worked most of the time in the next two centuries. Even after being devastated by the collapse of the housing market during the Great Depression, the industry made a successful comeback after World War II and accounted for two-thirds of mortgage loans in the country by the 1960s.1 This simple model exposed the thrifts to a major risk, though: the rise in interest rates. The interest rate they paid out to depositors went up as rates rose, but mortgages were much longer term with fixed rates. This became a real problem in the 1970s and early 1980s when, in an effort to bring down rampant inflation, the Federal Reserve jacked up interest rates consistently all the way up to 20 percent. Inflation was tamed, but many S&Ls had racked up losses as they paid out more than they were taking in.

Instead of shutting down the insolvent thrifts, the regulators overseeing the industry at the time allowed the weakened institutions to remain in the game with the hope that they would earn their way out of trouble. So the troubled banks doubled down—they expanded outside their traditional area of home mortgages, making loans to and investments in riskier real-estate developments. They also increased their leverage—the amount of money they borrow in relation to their capital—as the regulators lowered capital requirements, so they could make bigger bets. To be able to borrow more, the zombies jacked up the interest rates they were offering depositors, which had to be followed by relatively healthier thrifts as well so they could remain competitive and not lose their depositors. Accounting rules were changed so the S&Ls could book loan-origination fees upfront and postpone the costs of servicing the loan.2

When the United States finally came to terms with the problems of the industry and Congress passed a recovery act authorizing their cleanup in 1989, the problems had spread to more institutions and losses had multiplied. In the next six years, authorities closed half of the 3,234 thrifts and transferred their bad assets to a resolution trust to be wound down over time. The house cleaning cost $153 billion, triple the original estimates, most of it borne by the taxpayers.3

Japan’s Lost Decade

As the United States was coming out of its thrift crisis, Japan was entering its infamous Lost Decade after its property bubble burst. Japan had an asset bubble in the making during the 1980s, when housing prices doubled, stock indices tripled. At the same time, Japanese banks grew to be the world’s largest financial institutions, dwarfing their competitors in the United States and Europe. By 1988, nine of the top 10 banks in the world were Japanese, among them well-known names such as Sumitomo, Fuji, and Mitsubishi. Deregulation of the sector led to an increase in riskier lending by the banks as well as loosening of credit standards. The bubble popped at the end of the decade. As house prices started falling and economic growth stagnated, the banks were saddled with bad loans. Their capital base was also shaken because it was largely made up of shares in other companies, and the crash of the stock market reduced the value of those shares.4

The banks were hesitant to recognize these losses though. They didn’t raise their standard loan-loss reserve ratio—set at 0.3 percent of total lending—even as mortgages and other loans were going bad. Banking regulators, just like their U.S. counterparts dealing with the thrifts’ problems a decade earlier, turned a blind eye to this deficiency and allowed them to keep underreporting nonperforming assets.5 In fact, some critics have claimed that the finance ministry was directing the banks to hide their toxic waste so they would look healthier.6 The authorities were being lenient toward the weakened banks with the hope that the economy would recover and cure their problems.

The banks had the same hope, so they rolled over bad debt to failing companies with the expectation that they would recover and pay back or at least they would have enough time to make profits over time and recognize the losses then. This evergreening of nonperforming loans was widespread during the 1990s in Japan.7 So the zombie banks created zombie companies, whose death was postponed because banks didn’t want to recognize their losses. In 1993, the banks created a bad-debt-resolution firm and transferred some of their nonperforming assets there, but this was mostly a ploy to earn tax benefits while still avoiding the real losses. The banks in effect swapped the bad loans on their books with debt from the resolution company, which was also not paying them any interest.8 Because investors didn’t believe in the values of their assets, Japanese banks couldn’t raise new capital during this period, but they managed to stay within required capital ratios by selling subordinated debt, which was treated as secondary form of capital. Implementation of new international banking regulations requiring them to increase capital was postponed by regulators.9

As the day of reckoning was delayed, it had multiple negative consequences on the Japanese economy. Lending to healthy firms declined while loans to zombie companies were rolled over. Even as the Bank of Japan, the nation’s central bank, cut interest rates down to 0.5 percent by 1995, the cheap money didn’t filter into the domestic economy (Figure 2.1). Japanese banks instead expanded lending to other Asian countries where they could earn more; they were gambling for resurrection. The banks also preferred to lend to the government since it was more lucrative for them than lending to consumers or corporations and public debt was growing steadily thanks to attempts at fiscal stimulus to jumpstart the economy. In 1996, there was a temporary recovery when the economy grew above 3 percent. The following year, asset bubbles in Thailand, Malaysia, Indonesia, and other Asian countries popped, dumping more losses on Japanese banks who were lending what they borrowed at zero percent from the Bank of Japan to neighboring countries at above 10 percent.10

Figure 2.1 Japan’s unemployment rate rose steadily as the economy stagnated, even as interest rates were cut to zero.

SOURCES: Bank of Japan, Economic and Social Research Institute (Japan), Bloomberg LP.

By 1998, the authorities could no longer look the other way because the banks’ losses were too large to ignore. In various stages over the next five years, the government and regulators moved to resolve the banking crisis. Initially, they tried to provide capital to the zombie banks. When that didn’t work, they nationalized and shut down or merged some of the biggest institutions that were in trouble. They also formed a resolution trust to take over banks’ bad assets, and this time they aggressively pushed the banks to comply. When it was all over, the banks had written off about $1 trillion in bad assets, about 20 percent of the nation’s annual output. The cleanup cost the government more than $200 billion. Worst of all, Japan’s economic growth averaged 1 percent between 1992 and 2002, while unemployment more than doubled to 5 percent.11

Even to this day, Japan has not been able to shake off the deflationary trap it was caught in during the crisis. Unemployment has still not come down from the levels it reached during the Lost Decade. The country slips into recession faster than any other developed economy. Following two years of contraction and a temporary recovery in 2010, Japan’s economy contracted by 1 percent in the first quarter of 2011, even as most of its peers managed to continue their growth, albeit more slowly. Decades of government’s fiscal efforts to stimulate the economy have also boosted Japan’s debt level to one of the highest in the world.12

Delaying the Fix Increases Costs

Some of the similarities between the current global crisis and Japan’s experience two decades ago are easy to spot. The meltdown that started in 2008 was the result of an asset price bubble in the United States and several European countries. Japanese house prices had jumped 142 percent in seven years prior to 1991. The comparable figure was 138 percent for the U.S. housing market until its 2006 peak. In European countries, where the peak occurred in 2007, the seven-year run-up was 136 percent for Spain, 127 percent for the United Kingdom, and 106 percent for Ireland.13 Banks in Europe and the United States have written off about $1.6 trillion related to the crisis, yet another $550 billion looms, according to the International Monetary Fund (IMF). Interest rates were cut to 0 percent in the United States and 1 percent in the European Union (EU). Although the EU started to increase its benchmark rate in 2011, the U.S. Federal Reserve still has no intentions of doing so three years after having reduced it to zero. The free money from the West is fueling asset-price bubbles in emerging markets, just as it did in Asia in the 1990s.

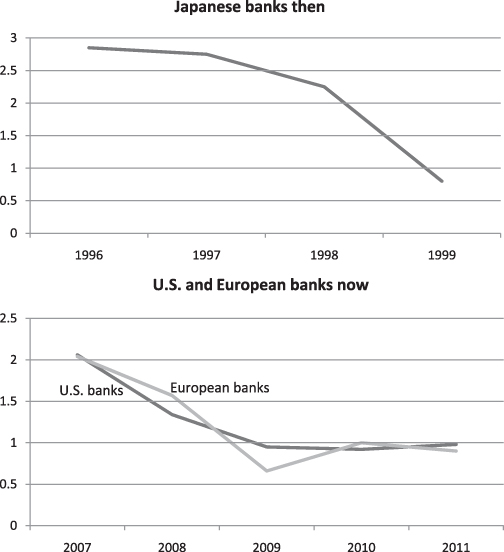

The United States, and the European Union to a lesser extent, moved to capitalize their troubled banks much faster than Japan did in the 1990s. Still, there are many undercapitalized banks that cannot handle future financial shocks and with too many unresolved bad assets on their balance sheets, the IMF reckons. Damon A. Silvers says an IMF official told him once that there were three stages to every financial crisis: denial, propping up, and nationalization. The longer a country takes to get to the final stage, the more harm is done to its economy, this official told Silvers, who is director of policy at AFL-CIO, one of the largest labor unions in the United States. Silvers says governments moved to the second phase much faster this time around than Japan had done, yet the third and final phase of actually cleaning up the balance sheets of the troubled banks hasn’t happened. Anil Kashyap, a University of Chicago finance professor who has studied the Japanese banking problems extensively, agrees. Even though the troubled banks were forced to raise enough capital to remain technically solvent, they need more capital to expand lending and support economic growth, Kashyap says (Figure 2.2).

Figure 2.2 The price-to-book value of Japanese banks fell in the 1990s as the troubles on their balance sheets became apparent. The same has happened in Europe and the United States since 2008.

SOURCES: Charles W. Calomiris and Joseph R. Mason, “How to Restructure Failed Banking Systems: Lessons from the U.S. in the 1930s and Japan in the 1990s,” in Governance, Regulation, and Privatization in the Asia-Pacific Region, NBER East Asia Seminar on Economics, Volume 12, ed. Takatoshi Ito and Anne Krueger (Chicago: University of Chicago Press, 2004), 375–423.

Both the U.S. thrift crisis and Japan’s Lost Decade showed that leaving bad assets on the books of banks with weak capital positions results in either reduced lending by those institutions or gambling on resurrection through risky bets. Both crises were solved only after the nonperforming assets were taken off, the losses fully recognized, and the weakest lenders shut down or sold off. That is the most crucial lesson ignored in today’s policy response. With accounting rules changed on both sides of the Atlantic so that recognition of losses can be postponed, the U.S. banks are putting off dealing with further losses from the housing market collapse while the EU is delaying the resolution of some member countries’ unsustainable debt problems because its banks cannot cope with potential losses. The delay in facing these problems head on is prolonging the housing rut in the United States and the sovereign debt scare in the EU. Even though economic growth recovered in 2010—mostly due to fiscal stimuli and the incredible amount of monetary easing—it can be lost easily when banking problems aren’t solved thoroughly, Japan’s experience reminds us.

When Japan finally moved to clean up its banking system in the late 1990s, it bought bad assets at deep discounts, which meant some of the weakest banks became insolvent and had to be shut down while others needed further capital injections. Even though the government spent about $495 billion for these efforts initially, it managed to recoup about half its investment when selling the bad assets in the next three years, reducing the final bill for the taxpayer greatly. The resolution of the seized banks and the sales of bad assets didn’t disrupt markets.

By providing implicit and explicit guarantees to their major banks, countries from the United States to Ireland have increased the risks for the taxpayers even further during the current crisis, says Professor Kane, who coined the term zombie bank. The strongest lesson he has learned observing the S&L crisis and the Japanese problems is that the final reckoning might be put off for quite some time, despite all the odds, Kane says. When it comes to dealing with today’s zombie banks, the same may be true, and it might take another four to five years for the full resolution. As we’ve seen from the thrift and Japanese crises, that delay will only increase the costs to society and hold back economic recovery.

Notes

1. Office of Thrift Supervision, About the OTS: History, www.ots.treas.gov/?p=History.

2. Edward J. Kane, “What Lessons Should Japan Learn from the U.S. Deposit-Insurance Mess?” Journal of the Japanese and International Economies 7, no. 4 (December 1993): 329–355; Edward J. Kane,. The S&L Insurance Mess: How Did It Happen? (Washington, DC: The Urban Institute Press, 1989).

3. Timothy Curry and Lynn Shibut, “The Cost of the Savings and Loan Crisis: Truth and Consequences,” FDIC Banking Review 13, no. 2 (December 2000): 26–35.

4. Takeo Hoshi and Anil Kashyap, “The Japanese Banking Crisis: Where Did It Come from and How Will It End?” NBER Macroeconomics Annual 14 (1999): 129–212; Akihiro Kanaya and David Woo, The Japanese Banking Crisis of the 1990s: Sources and Lessons (Princeton: Princeton University Printing Services, 2001); Richard C. Koo, “Lessons from Japan’s Lost Decade: Why America’s Experience May Be Worse,” The International Economy, (Sept. 22, 2008); Daniel K. Tarullo, Banking on Basel: The Future of the International Financial Regulation (Washington, DC: Peter G. Peterson Institute for International Economics, 2008).

5. Tim Callen and Martin Mühleisen, “Current Issues Facing the Financial Sector,” in Japan’s Lost Decade: Policies for Economic Revival (Washington, DC: International Monetary Fund, 2003), 17–42; Mitsuhiro Fukao, “Japan’s Lost Decade and Its Financial System,” in Japan’s Lost Decade: Origins, Consequences and Prospects for Recovery, ed. Gary R. Saxonhouse and Robert M. Stern (Malden, MA: Blackwell, 2004), 99–118; Hoshi and Kashyap, “The Japanese Banking Crisis.”

6. Anthony Randazzo, Michael Flynn, and Adam B. Summers, “Turning Japanese: Japan’s Post-Bubble Policies Produced a ‘Lost-Decade.’ So Why Is President Obama Emulating Them?” Reason (July 1, 2009).

7. Rishi Goyal and Ronald McKinnon, “Japan’s Negative Risk Premium in Interest Rates: The Liquidity Trap and the Fall in Bank Lending,” in Saxonhouse and Stern, Japan’s Lost Decade, 73–98; Dick K. Nanto, “The Global Financial Crisis: Lessons from Japan’s Lost Decade of the 1990s,” Congressional Research Service Reports and Issue Briefs (May 4, 2009); Yuri N. Sasaki, “Has the Basel Accord Accelerated Evergreening Policy in Japan? A Panel Analysis of Japanese Bank Credit Allocation,” working paper, December 2008.

8. Kanaya and Woo, The Japanese Banking Crisis of the 1990s.

9. Kentaro Tamura, “Challenges to Japanese Compliance with the Basel Capital Accord: Domestic Politics and International Banking Standards,” Japanese Economy 33, no. 1 (Spring 2005): 23–49.

10. Charles W. Calomiris and Joseph R. Mason, “How to Restructure Failed Banking Systems: Lessons from the U.S. in the 1930s and Japan in the 1990s.” in Governance, Regulation, and Privatization in the Asia-Pacific Region, NBER East Asia Seminar on Economics, Volume 12, ed. Takatoshi Ito and Anne Krueger (Chicago: University of Chicago Press, 2004), 375–423; Tim Callen and Jonathan D. Ostry, “Overview,” in Japan’s Lost Decade: Policies for Economic Revival, 1–16; Randazzo, Flynn, and Summers, “Turning Japanese”; Hoshi and Kashyap, “The Japanese Banking Crisis”; Jeff Madura, International Financial Management (8th ed.) (Mason, OH: Thomson South-Western, 2006); Winston T. H. Koh, Roberto S. Mariano, Andrey Pavlov, Sock Yong Phang, Augustine H. H. Tan, and Susan M. Wachter, “Bank Lending and Real Estate in Asia: Market Optimism and Asset Bubbles.” Journal of Asian Economics 15, no. 5 (January 2005): 11-3-1118; Sasaki, “Has the Basel Accord Accelerated Evergreening Policy in Japan?”

11. Takatoshi Ito, “Retrospective on the Bubble Period and its Relationship to Developments in the 1990s,” in Saxonhouse & Stern, Japan’s Lost Decade, 17–34; Nanto, “The Global Financial Crisis”; Calomiris and Mason, “How to Restructure Failed Banking Systems”; Koo, “Lessons from Japan’s Lost Decade”; Mitsuhiro Fukao, “Japan’s Lost Decade and Its Financial System,” in Saxenhouse and Stern, Japan’s Lost Decade, 99–118; Kanaya and Woo, The Japanese Banking Crisis.

12. Statistics Bureau. “Japan Monthly Statistics.” June 2011; International Monetary Fund, “World Economic Outlook,” April 2011.

13. Patrick Lee, Carlo Tommaselli, and Omar Keenan, “Spanish Banks,” Société Générale research report, January 28, 2011.