Chapter 8

ASSET AND LIABILITY MANAGEMENT II: THE ALCO

We continue the discussion on bank asset‐liability management (ALM) with a review of the asset–liability management committee (ALCO). ALCO has a specific remit to oversee all aspects of asset–liability management, from the front‐office money market function, to back‐office operations, and middle‐office reporting and risk management. In the author's opinion it is the most important risk management committee in a bank because it is concerned wholly and solely with the balance sheet, more critically the long‐term viability of the balance sheet. For this reason, an effective ALCO governance process is vital for every bank, irrespective of size or business model.

In this chapter we consider the traditional role of ALCO and then go on to present recommended best‐practice principles, which may be applied in any bank.

TRADITIONAL ALCO MISSION

The ALM reporting process is overseen by the bank's ALCO. It is responsible for setting and implementing ALM policy. Its composition varies in different banks but usually includes heads of business lines as well as director‐level staff such as the finance director. It also oversees direction on issues such as strategy and risk hedging policy.

Table 8.1 is a summary overview of the traditional responsibilities of ALCO.

Table 8.1 ALCO traditional mission

| Mission | Components |

| ALCO management and reporting | Formulating ALM strategy |

| Management reporting | |

| ALCO agenda and minutes | |

| Assessing liquidity, gap, and interest‐rate risk reports | |

| Scenario planning and analysis | |

| Interest income projection | |

| Asset management managing | Bank liquidity book (CDs, bills) |

| Managing FRN book | |

| Investing bank capital | |

| ALM strategy | Yield curve analysis |

| Money market trading | |

| Funding and liquidity management | Liquidity policy |

| Managing funding and liquidity risk | |

| Ensuring funding diversification | |

| Managing lending of funds | |

| Risk management | Formulating hedging policy |

| Interest‐rate risk exposure management | |

| Implementing hedging policy using cash and derivative instruments | |

| Internal Treasury function | Formulating transfer‐pricing system and level |

| Funding group entities | |

| Calculating the cost of capital |

ALCO will meet on a regular basis; the frequency depends on the type of institution but is usually once a month. The composition of ALCO varies by institution but may comprise the heads of Treasury, trading, and risk management, as well as the finance director. Representatives from the credit committee and loan syndication may also be present. A typical agenda would consider all the elements listed in Table 8.1. Thus, the meeting will discuss and generate action points on the following:

- Management reporting: this will entail analysing various management reports and either signing them off or agreeing items to be actioned. The issues to consider include the lending margin, interest income, variance from last projection, customer business, and future business. Current business policy with regard to lending and portfolio management will be reviewed and either continued or adjusted;

- Business planning: existing asset (and liability) books will be reviewed and future business directions drawn up. This will consider the performance of existing business, most importantly with regard to return on capital. The existing asset portfolio will be analysed from a risk–reward perspective, and a decision taken to continue or modify all lines of business. Any proposed new business will be discussed and – if accepted – in principle will be moved on to the next stage.1 At this stage, any new business will be assessed for projected returns, revenue, and risk exposure;

- Hedging policy: overall hedging policy will consider acceptable levels of risk exposure, existing risk limits, and use of hedging instruments. Hedging instruments also include derivative instruments. Many bank ALM desks find that their hedging requirements can be met using plain vanilla products such as interest‐rate swaps and exchange‐traded short‐money futures contracts. The use of options and especially vanilla instruments such as FRAs2 is much lower than one might think. Hedging policy takes into account the cash book revenue level, current market volatility levels, and the overall cost of hedging. On occasion, certain exposures may be left unhedged because the costs associated with hedging them are deemed prohibitive. (This includes the actual cost of putting on the hedge as well as the opportunity cost associated with expected reduced income from the cash book.) Of course, hedging policy is formulated in coordination with overall funding and liquidity policy. Its final form must consider the bank's views of the following:

- Expectations on the future level and direction of interest rates;

- Balancing the need to manage and control risk exposure with the need to maximise revenue and income;

- Level of risk aversion, and the level of risk exposure the bank is willing to accept.

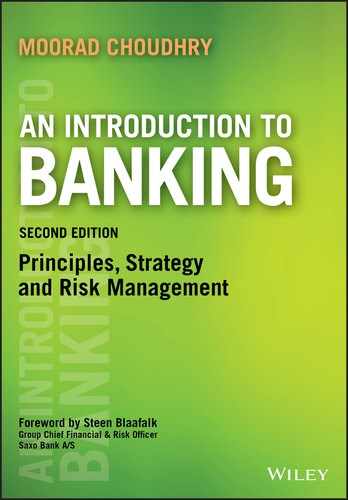

ALCO is dependent on management reporting from the ALM or Treasury desk – reports may be compiled by the Treasury middle office. The main report is the overall ALM report, showing the composition of the bank's ALM book. Other reports will look at specific business lines and consider the return on capital generated by these businesses. These reports will need to break down aggregate levels of revenue and risk by business line. Reports will also drill down by product type across business lines. Other reports will consider the gap, gap risk, the Value‐at‐Risk (VaR) or DV01 report, and credit risk exposures. Overall, the reporting system must be able to isolate revenues, return, and risk by country sector, business line, and product type. There is usually an element of scenario planning as well, which is expected performance under various specified macro‐level and micro‐level market conditions.

Figure 8.1 illustrates the general reporting concept.

Figure 8.1 ALCO reporting input and output

ALCO GOVERNANCE BEST‐PRACTICE PRINCIPLES

We consider here the role and best‐practice governance structure for the bank's asset‐liability committee or ALCO. But before we do, consider this question:

What executive committees have a responsibility for oversight of balance sheet risk?

- Executive committee;

- Risk management committee (CRO chaired);

- Credit risk committee;

- ALCO.

It is arguable that the only executive committee that is concerned wholly with balance sheet risk on a strategic and integrated basis (both sides of the balance sheet) is the Asset‐Liability Committee (ALCO). No other executive committee focuses solely on balance sheet risk management. In essence, given its mandate, membership and expertise, it should be ALCO.

As well as considering ALCO itself, banks should also seek to ensure the most effective way to ensure above‐satisfactory and effective governance of the bank from the Board's perspective.

ALCO principles

It is recommended that ALCO be constituted as a committee with Board‐delegated authority, ranking on a par with the executive committee, responsible for management of a bank's balance sheet with respect to liquidity, funding, capital, interest rate, and foreign exchange (FX) risk. Ideally, it would also have an oversight or policy overview function for credit risk, but this recommendation is controversial among some bankers.

The main responsibilities of ALCO are:

- Approves policy and direction with respect to all aspects of balance sheet management;

- Provides strategy and direction with respect to balance sheet structure and shape;

- Approval authority for new products and processes (delegated to the new products committee);

- Guides the management of the bank's liquid asset buffer;

- Responsible for ensuring the bank complies with all regulatory requirements on liquidity and funding;

- Held monthly with exceptions in stressed environments when frequency can be increased.

The author's template ALCO Terms of Reference (ToR) is given at Appendix 8.1.

The asset‐liability committee is mandated by executive authority to act as the primary risk committee responsible for asset–liability, liquidity, funding, and balance sheet management.

Managing risks: Liquidity, funding, capital, interest‐rate, and FX risk management:

- Effectively understanding, valuing, and managing risks on the balance sheet;

- Production of data measures and monitoring of positions against limits set by ALCO;

- Managing risk exposure through effective execution;

- External market access function;

- Management of liquid asset buffer;

- Review of limit breaches and remedial action.

Providing Treasury support:

- Design and implementation of Treasury policies across the business and ensuring compliance;

- Producing analysis and papers for monthly ALCO.

Providing Treasury services:

- Proactive support and involvement to new product development and pricing decisions;

- Prudent management of risk in line with bank policies.

Reporting, responsibility, and transparency

- For oversight of balance sheet risk to be effective throughout the cycle, the operating model has to be transparent and has to make clear who is responsible;

- The balance sheet triumvirate approach (see Chapter 7), together with the authority of ALCO as operating either with Board‐delegated authority or as a subcommittee of the Board, is the most effective because it is the only way to ensure that balance sheet metrics and exposure are at the forefront of governance culture throughout the cycle;

- The Board risk appetite statement (see Chapter 9) is the start of this process.

Organisation structure

The recommended organisation structure governing ALCO authority is shown in Figure 8.2.

Figure 8.2 ALCO governance organisation

The Board and technical competence

- Board members must be thoroughly attuned to balance sheet risk;

- The chairperson is not exempt (regulators note);

- Sustained through‐the‐cycle bank risk management dictates that the ultimate guardian of the balance sheet, ALCO, must not only be the premier executive risk committee of the bank but also the main driver of strategy and acceptable risk appetite;

- Approach strategy making by means of an integrated balance sheet approach – looking at both sides of the balance sheet;

- For the risk triumvirate, note that Treasury is the only part of the bank that oversees the whole balance sheet and crucially is both inward and outward facing.

ALCO membership

Members include:

- Chief Executive Officer;

- Chief Financial Officer (Chair);

- Head of Treasury (Deputy Chair);

- Head of Corporate Banking;

- Head of Retail Banking;

- Head of Private Banking;

- CRO;

- Head of Strategy.

In attendance are:

- Head of ALM/Money Markets;

- Head of Liquidity Risk;

- Head of Valuation Control/Product Control;

- MD, Products & Marketing;

- Internal Auditor;

Secretariat: Business Manager to Head of Treasury or Liquidity Manager

In addition there are two important subcommittees of ALCO (for all but the smallest banks), detailed below.

ALCO subcommittee: Balance Sheet Management Committee (BSMCO)

The BSMCO operates as a subcommittee of ALCO. It is a technical ALM forum.

- The purpose of BSMCO is to:

- Review the bank's balance sheet, monitor trends in deposits and earning assets, and assess the impact of economic scenarios on the group's NIM, assets, liabilities, and capital requirements;

- Determine actions to manage balance sheet resources in the light of economic forecasts, market trends, and regulatory demands;

- Discuss technical considerations with respect to capital, liquidity, and funding impacts on the balance sheet.

ALCO authorises BSMCO to:

- Investigate any activity within its Terms of Reference (ToR) and make recommendations to ALCO that it deems appropriate on any area within its remit where action is needed;

- Seek any information it requires from or request the attendance at any of its meetings of any director or employee of the bank (or group) and all directors and employees are expected to cooperate with any requests made by the committee.

In essence, BSMCO is necessary because ALCO has at most perhaps 2 hours a month to review the entire balance sheet (except where extraordinary ALCOs are called)…

…this is not necessarily sufficient to review the detail or – paradoxically – see the wood for the trees.

The existence of BSMCO is designed to ensure that the detail does not “fall through the cracks”. The membership may be comprised as:

- Head of Treasury (Chair);

- Deputy CFO;

- Deputy CRO;

- Head of Research or Strategy;

- Ad hoc as required from the business.

ALCO subcommittee: Deposit/Product Pricing Committee

The other recommended technical subcommittee of ALCO is the Product Pricing Committee/Deposit Pricing Committee. This is a smaller committee whose remit is to ensure that, as per the recommended model, “all pricing decisions are made by ALCO”.

It is a committee operating as a subcommittee of ALCO, which has ultimate responsibility for all liabilities/products pricing decisions.

The products in question would in the first instance be customer deposit products.

This may be extended to customer asset products if deemed necessary.

The Product Pricing Committee/Deposit Pricing Committee has delegated authority to approve specific changes to standard rates for one‐off transactions (for example, to improve a rate paid to a customer to retain a deposit).

Membership comprises:

- Treasury representative;

- Finance representative;

- Business line representative (retail and corporate banking).

Hedging policy

Overall hedging policy will consider the acceptable risk exposure, existing risk limits, and use of hedging instruments.

Hedging policy takes into account the cash book revenue level, current market volatility levels, and the overall cost of hedging. On occasion, certain exposures may be left unhedged because the cost associated with hedging them is deemed prohibitive. (This includes the actual cost of putting on the hedge as well as the opportunity cost associated with expected reduced income from the cash book.)

Hedging policy is formulated in coordination with overall funding and liquidity policy. Its final form will reflect the ExCo's views of the following:

- Expectations on the future level and direction of interest rates;

- Balancing the need to manage and control risk exposure with the need to maximise revenue and income;

- The level of risk aversion, and how much risk exposure the bank is willing to accept.

Best practice guidelines

The following PRA guidelines issued in January 2011 articulate best practice guidelines encouraged to be applied to ALCOs:

- Proactively controls the business in line with the firm's objectives; focuses on the entire balance sheet;

- Ensures risks remain within risk appetite;

- Considers the impact on earnings volatility of changing economic and market conditions;

- Ensures an appropriate funds transfer pricing mechanism that aligns to the firm's strategic objectives and risk appetite, and regularly reviews this mechanism;

- Acts as the arbitrator in the debate and challenge process between business lines;

- Focuses on effects of future plans/strategy at bank and business line level;

- Takes decisions to manage ALM risks or escalates issues to ExCo, rather than simply “observing” the risks;

- Ensures issues are fully articulated and debated;

- Considers recommendations from a tactical subcommittee (the ABC Bank BSMCO) that excludes the CEO and other ExCo members;

- Engages in active dialogue among various members and displays a strong degree of challenge;

- Minutes insight into the discussions and extent of challenge; does not only list action points.

Policy approval process

For non‐small banks, it is recommended to submit technical issues to a “technical ALCO” or “Balance Sheet Management Committee” (BSMCO) first – provided this adds value to ALCO itself!

- Papers submitted by business lines should include a section that covers off all Treasury‐related issues (capital, liquidity, funding, IRR, etc.):

- All new business or new limits to make explicit reference and detail to Treasury funding implications (see over).

- “Socialisation” of paper to members:

- Pre‐positioning.

- Discussion and debate at ALCO followed by approval (or not).

Forward agenda

Certain items (such as liquidity policy, LAB policy, FTP policy, etc.) should be reviewed on a regular basis at ALCO, say every 6 or 12 months.

To facilitate adequate time for discussion, papers, analysis, etc. these should be part of a forward agenda that is set at the start of the year so that everyone is aware of what is coming up when.

Dates should also be set on the same day each month and diarised in advance.

Holding ALCO in the last week of the month rather than the first or second means at least that the ALCO deck will be for last month's data rather than the data from the month before.

Figure 8.3 is an example of a bank forward ALCO agenda; only a sample of standing items are shown here. A bank would have its specific list added to this template, at the frequency required.

| Jan‐15 | Feb‐15 | Mar‐15 | Apr‐15 | May‐15 | Jun‐15 | Jul‐15 | Aug‐15 | Sep‐15 | Oct‐15 | Nov‐15 | Dec‐15 | ||

| Agenda item | |||||||||||||

| Market MI | x | x | x | x | x | x | x | x | x | x | x | x | |

| RWA | x | x | x | x | x | x | x | x | x | x | x | x | |

| Liquidity MI | x | x | x | x | x | x | x | x | x | x | x | x | |

| Credit VaR | x | x | x | x | x | x | x | x | x | x | x | x | |

| FTP curve | x | x | x | x | |||||||||

| For review and approval | |||||||||||||

| FTP policy | x | x | |||||||||||

| LAB policy | x | x | |||||||||||

| LAB IRR limits | x | x | |||||||||||

| Securities issuance policy | |||||||||||||

| For 2‐weekly Treasury review | |||||||||||||

Figure 8.3 Template for ALCO forward agenda planning

The ALCO pack

Key pointers for the ALCO MI deck are:

- Make it succinct and as accessible as possible;

- Relegate detailed MI to an appendix and just have key indicators and summaries at the front;

- Compare packs and agendas where possible (not easy…);

- Have a key message summary on each slide;

- Have forward agenda items;

- Include market data in summary fashion…see the following examples.

ALCO and the Board paper summary

Ideally, the main ALCO pack (minus the papers and the appendices with a note “available on request”) would be part of the Board papers – i.e. the balance sheet metrics and exposures with a 1‐page summary of “main messages”. If not, then ALCO delegated to Treasury should prepare a summary of 3–4 pages based on the main deck.

Revisit the MI pack

- Is it succinct, accessible, easy to read?

- Does it give the latest balance sheet information, within the first 5–6 pages, in a way that enables the reader to ascertain quickly what the current balance sheet risks are?

- Does it help ALCO/ExCo do its job?

- Is every item within it completely relevant and completely necessary?

- Is it completely bereft of spurious or surplus‐to‐requirement content?

- Is the summary risk metrics still fit for purpose? (regularly updated as relevant to bank business model and its current and expected environment)?

CONCLUSIONS

A bank is managed from the top down. The cultural attitude towards risk is driven from the top down. Hence, efficient management at operating levels requires clear strategy and direction from Board level. Once this is communicated, ALCO should be trusted to oversee operations and to have the final say on strategy and risk appetite. Clear direction must be set on what the bank is here to do. Of course, shareholders should proactively approve the Board's direction – not passively sign off on it – but the delegation is from the Board to ALCO. Therefore, the Board should set guidelines on risk appetite and delegate authority to ALCO to ensure this is carried out.

APPENDIX 8.1:

ALCO RECOMMENDED TERMS OF REFERENCE

Terms of Reference

| Chair |

|

| Members |

|

| Attendees |

|

| Additional invitees | As appropriate. |

| Deputies | If a Member is unable to attend a meeting, he/she shall appoint a deputy to attend on his/her behalf. Such deputy's attendance shall not count towards the quorum and the deputy shall not hold the right to vote. |

| Quorum | Three members, at least one of whom shall be the Chief Financial Officer or the Chief Executive Officer and at least one of whom shall be either the MD Corporate or MD Retail. |

| Meeting frequency |

Monthly and ad hoc as required by any member. Ad hoc meetings are permitted to take place via email if necessary. Rules regarding decision making and quorum remain the same as for face to face meetings. |

| Secretary | Provided by Treasury. |

| Committee authority | ALCO operates as a sub‐committee of the Board. |

| Authority delegated by the Committee |

ALCO may delegate any of its powers to a sub‐committee consisting of two or more ALCO members. Any sub‐committee so formed shall conform to any regulations that may be imposed on it by ALCO and the acts and proceedings of a sub‐committee shall be reported to ALCO. ALCO shall review and approve the ToR of those committees to which it has delegated authority at least annually and on an ad hoc basis should material amendment be proposed. The ABC Bank Products Pricing Committee will report as a sub‐committee of ALCO. The ABC Balance Sheet Management Committee will operate as a sub‐committee of ALCO. Specific delegated authorities are set out within “Scope of the Board/Committee's oversight and responsibility”. |

| Committee accountability | ALCO operates as a sub‐committee of the Board and reports to the [Executive Committee/Board]. |

| Escalation | Management decisions beyond this Committee's authority and matters which this Committee deems necessary for escalation will be escalated to the Board or appropriate other Board committees where relevant. |

| Purpose of the Committee |

It is responsible for identifying, managing and controlling the bank's balance sheet risks and capital management in executing its chosen business strategy. Balance sheet risks are managed by setting limits monitoring exposures and implementing controls across the dimensions of capital, funding, and liquidity and non‐traded interest rate risk. It is responsible for the implementation of ALCO strategy and policy for the bank's balance sheet. |

| Scope of the Committee's oversight and responsibility |

Strategic overview

|

Liquidity and funding

|

|

Other

|

|

| Board Administration/Secretariat |

The Treasury team is responsible for meeting administration. The draft agenda for each meeting is agreed with the Head of Treasury [and the Chief Financial Officer] in advance of meetings. Papers are circulated to Members and Attendees a minimum of two business days before each meeting. Draft minutes and agreed actions are circulated for approval as soon as possible after each meeting, preferably within a period of one week. The minutes of the meeting shall include:

Copies of the approved minutes and record sets for all meetings are retained by the secretary. |