Appendix II

Financial Statements

APP 2-1. COMBINED RECORD PLANT INC AND SUBSIDIARIES, ALL DIVISIONS—ASSETS

BALANCE SHEET

|

ASSETS |

|

Current Assets |

|

|

Cash in Bank and on Hand |

64,096.54 |

|

Accounts Receivable |

392,494.36 |

|

Receivables from Related CO's |

214,633.59 |

|

Tape Inventory |

19,078.87 |

|

Prepaid Expenses |

27,768.79 |

|

Total Current Assets |

|

718,072.15 |

|

|

|

Fixed Assets |

|

|

Land Purchase |

900,000.00 |

|

Parking Lot |

138,000.00 |

|

Leasehold Improvements |

2,659,930.98 |

|

Recording Equipment |

2,999,195.05 |

|

Furniture & Fixtures |

281,111.04 |

|

Office Equipment |

161,007.50 |

|

Film Equipment |

109,512.02 |

|

Computer Software |

31,229.98 |

|

Trucks & Automobiles |

125,711.64 |

|

Depreciation and Amortization |

(3,169,773.50) |

|

Total Fixed Assets |

|

4,235,924.71 |

|

|

|

Other Assets |

|

|

Security Deposits |

30,057.73 |

|

Mortgage Loan Fees |

34,500.00 |

|

Mortgage Loan Reserve-Back 40 |

200,000.00 |

|

Startup Costs—Stage “L” |

3,935.38 |

|

Investment in Studio M Inc. |

1,000.00 |

|

Deposits |

14,583.33 |

|

Total Other Assets |

|

284,076.44 |

|

|

|

TOTAL ASSETS |

|

5,238,073.30 |

APR 2-2. COMBINED RECORD PLANT INC AND SUBSIDIARIES, ALL DIVISIONS—LIABILITIES

BALANCE SHEET

|

LIABILITIES |

|

Current Liabilities |

|

|

Accounts Payable |

422,384.5 |

|

Accrued Expenses |

29,243.27 |

|

Clients’ Deposits |

31,235.3 |

|

B.T. Loan Fee-Current Portion |

33,336.0 |

|

B.T. A/R Loan |

845,396.02 |

|

Current Notes Payable |

81,413.90 |

|

AFCO-Insurance Financing |

17,698.17 |

|

Current Leases Payable |

131,069.56 |

|

Sales Tax Payable |

14,113.44 |

|

Income Taxes |

22,403.92 |

|

Total Current Liabilities |

|

1,628,294.20 |

|

|

|

Long-Term Liabilities |

|

|

B.T. Corp-Construction |

645,727.00 |

|

B.T. Commercial Loan Fee |

11,104.00 |

|

Building Mortgage |

1,691,103.09 |

|

Non-Current Notes Payable |

313,949.47 |

|

Non-Current Leases Payable |

178,604.95 |

|

Total Long-Term Liabilities |

|

2,840,488.51 |

|

|

|

Capital |

|

|

Common Stock |

9,730.00 |

|

Paid-In Capital |

41,777.20 |

|

Retained Earnings |

679,329.76 |

|

Net Income |

38,453.63 |

|

Total Capital |

|

769,290.59 |

|

|

|

TOTAL LIABILITIES & CAPITAL |

5,238,073.30 |

|

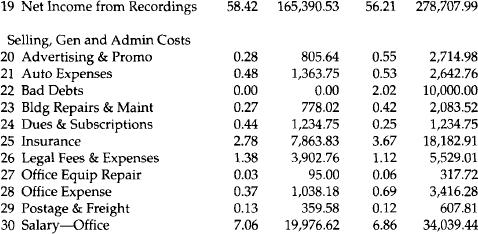

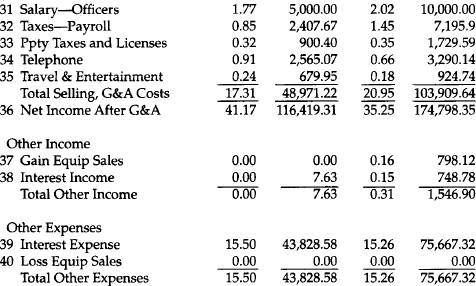

APP. 2-3. COMBINED RECORD PLANT INC AND SUBSIDIARIES, ALL DIVISIONS

PROFIT AND LOSS STATEMENT

Notes:

1,5 Taxable time sales and nontaxable time sales had to be segregated for sales tax reports required by the state. Time was not taxable if the engineer was not an employee of the studio and billed the record label separately and independently for engineering services.

3 Miscellaneous sales—usually rentals, and taxable.

4 Nontaxable sales—used for late cancellation fees, travel days for remote recording dates, etc.

6 Union labor rebilled to client as separate line item on invoice.

17 Non-owned recording space rentals.

36 Do not assume that “Net Income After G&A” is the amount of money you have to spend. You must have your bookkeeper/accountant prepare a cash flow statement for that information. The “Net Income” figure simply shows you whether or not your studio operation is profitable.

37–40 This is where extraordinary income and expenses are shown.

41, 42 The Federal Government will allow you to expense the cost of your equipment and leasehold improvements, but not all in one year.

Depreciation is the vehicle for expensing only a portion of the equipment cost each year. Amortization is the way you expense a portion of the leasehold improvement costs each year.