CHAPTER 23

Freedom 55: Myth or Reality?

Vignette: When I Turned 55

When I turned 55, my wife handed me a 1-million-dollar bill (fake of course). “This is to celebrate your first million in sales after only 1 year in business,” she said. Indeed, my newly acquired company was thriving; growth was promising, reflected with a steady increase in sales by aiming at new markets in Europe and Asia. A promising future ahead. Finally, I would be able to retire soon after my first IPO.

The result was not necessarily as expected. My company was acquired by an American competitor the next year. Not liking “doing nothing,” I soon invested the proceeds of the sale in another venture.

I was among those fortunate to be in this position.

Why Is the Retirement Age 65 in Most Developed Countries?

Otto von Bismarck, the German “Iron Chancellor,” implemented the Old Age and Disability Insurance Law in 1889 when he introduced a social security system to appeal to the German working class and combat the power of the German Socialist Party.

The old-age pension program insurance equally financed by employers and workers was designed to provide a pension annuity for workers who reached the age of 70. Unlike the sickness and accident insurance programs of 1883 and 1884, respectively, this program covered all categories of workers (industrial, agrarian, artisans, and servants) from the start. Also, unlike the other two programs, the principle that the national government should contribute a portion of the underwriting cost, with the other two portions prorated accordingly, was accepted without question. The disability insurance program was intended to be used by those permanently disabled. This time, the state or province supervised the programs directly.

One persistent myth about the German retirement program is that it adopted age 65 as the standard retirement age because that was Bismarck’s age. In reality, Germany initially set age 70 as the retirement age (and Bismarck himself was 74 at the time). The retirement age was lowered to 65 only 27 years later (in 1916). By that time, Bismarck had been dead for 18 years.i

When the United States finally passed a social security law in 1935 (more than 55 years after the conservative German chancellor introduced it in Germany), the average life expectancy in America was only 61.7 years.

According to the World Health Organization, life expectancy increased by 5 years between 2000 and 2015, the fastest increase since the 1960s. In Canada, life expectancy at birth m/f (years, 2016) was 81/85, whereas in the United States, life expectancy at birth m/f (years, 2016) was 76/81.ii

Working or Not, This Is Not the Question

According to Statistics Canada, the number of “seniors” (age 65 and older) working part-time or full-time has more than doubled in the past 20 years. Note that “65” is just a number; it is not an expiry date.

Nowadays, once people get to the age of 55, they still feel like they are fairly young—reaching what they consider middle age: 60 is the new 40.

In its 2016 report, the Broadbent Instituteiii found that fewer than 20 percent of middle-income Canadian earners have more than 5 years of savings. These people, now aged 55 to 64, face a dramatic drop in their standard of living in retirement, and many will spend their senior years in poverty, the think-tank says, basing its findings on Statistics Canada figures.

About 47 percent of Canadians currently have no employer pension, and even fewer younger workers have employer pensions.

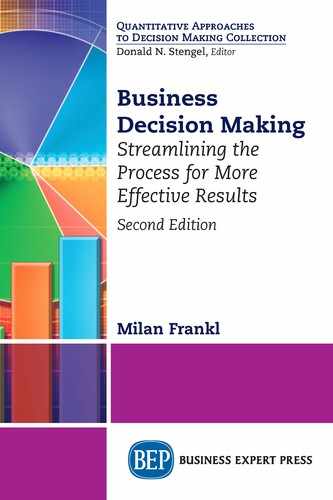

A U.S. confidence survey among workers about whether they will be able to lead the lifestyle they consider comfortable once they retire indicates that only 44 percent of generation X members were somewhat confident that they will be able to fully retire with a comfortable lifestyle (Figures 23.1 and 23.2).

Figure 23.1 U.S. workers’ retirement confidence survey conducted in 2018

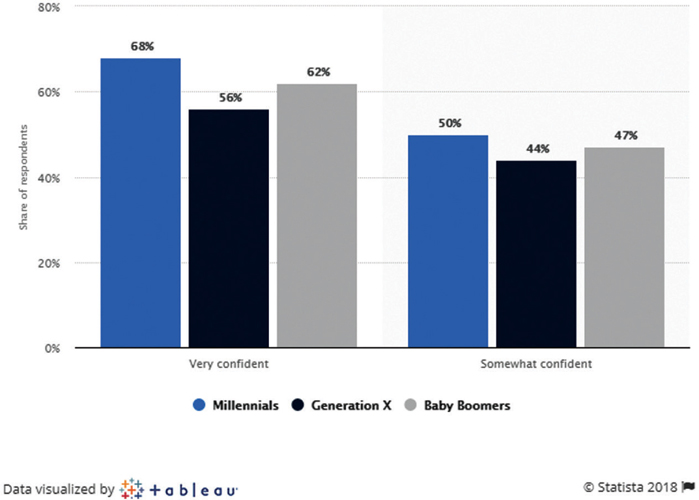

Figure 23.2 Where people are working beyond age 65

Source: https://www.statista.com/chart/12202/where-people-are-working-beyond-65

Most financial planning retirement experts cannot agree on how much one needs to live on in retirement.iv

Several “retirement rules” are used depending on what investment counseling firm one uses. The most common is the 70 percent rule, which assumes one is going to need 70 percent of one’s working income when reaching retirement. But not many financial planners hold to that number. A retirement full of travel, children who need support, and a period of long-term care could mean one would need as much in retirement as before retirement.

According to Fred Vettese, an expert on Canada’s retirement income system and chief actuary of Morneau Shepell, argues in his “The Essential Retirement Guide” that most people typically live on less than their full income before retirement; therefore, why would they need more in retirement?v

Vette goes on to state, Retirement planning is difficult enough without having to contend with misinformation. Unfortunately, much of the advice that is dispensed is either unsubstantiated or betrays a strong vested interest.

Remember that in retirement you are on your own. Retirement planning is difficult enough without having to deal with misinformation. Avoid unsubstantiated information. Be aware of vested interests of retirement planners—be they individuals or financial institutions.

Where to Begin?

One useful source would be the “Essential Retirement Guide” themes explored in a 10-part series published in the Financial Post in 2015.

• When it comes to tax and retirement, the United States and Canada are more similar than you might think.

Our savings vehicles may have different names, but whether you are Canadian or American, the really important retirement questions are essentially the same.

• Why 70 percent is not your retirement income target?

Our lives are longer and our working careers shorter than when the 70 percent income target was a sensible goal for retirement. So what should you be aiming for today? Frederick Vettese crunches the numbers.

• Why interest rates will stay low, and what does that mean for your retirement security?

A powerful source looks set to keep rates low for a long time so you had better start preparing for lower investment returns, higher savings rates, and a later retirement.

• Why your retirement income doesn’t need to keep pace with inflation?

Three studies done in different countries found that the older we get, the less we spend. When spending does go up, it’s usually because we need long-term care. But in most cases, that’s not until age 85 or later.

• Why you shouldn’t worry about saving for long-term care?

The most important fact about long-term care is that it is rarely needed until an advanced age, writes Fred Vettese. In a majority of cases, the long-term-care stay lasts 2 years or less.

• How to improve your odds of retiring well with a few simple strategies?

If you know how much you need to save every year, retirement planning becomes a lot less stressful. Here are two scenarios to help you figure out your personal savings rate.

• Are you playing rational roulette with your retirement plans?

You may not think you’re playing a game of chance with your retirement, but if you plan to make financial decisions as you age, you might be in a dicier position than you realize.

• What happens to your retirement finances after the death of your spouse?

No one plans to be widowed, but chances are good that one spouse will outlive the other. While the emotional impact can’t be ignored, the death of your spouse doesn’t have to devastate your finances.

ihttps://www.ssa.gov/history/age65.html.

iihttp://www.who.int/en/news-room/detail/19-05-2016-life-expectancy-increased-by-5-years-since-2000-but-health-inequalities-persist.

iiiThe Broadbent Institute is Canada’s leading progressive, independent organization championing change through the promotion of democracy, equality, and sustainability and the training of a new generation of leaders. (Source: http://www.broadbentinstitute.ca.)

ivhttp://www.cbc.ca/news/business/rrsp/retirement-savings-goal-1.3406502.

vhttps://www.morneaushepell.com/ca-en/insights/essential-retirement-guide-contrarian%E2%80%99s-perspective.