Market Survey and Mission Specification

Abstract

An introduction to the commercial airplane market and its prospects for growth over the next 20 years is presented in terms of numbers of new deliveries and the associated market value. The size and make-up of the fleet and the geographical distribution of the market value of purchases is discussed. Technology drivers such as fuel efficiency, weight reduction, drag reduction, engine design, carbon footprint, biofuels, alternative fuels and power sources, and noise and vibration are described, along with brief comments on cargo aircraft. A summary of the actions necessary to initiate a design project for a proposed commercial airplane including the development of a detailed mission specification and a market survey is presented.

Keywords

Commercial aircraft markets

Fuel efficiency

Drag reduction

Noise

Carbon footprint

Biofuels

Design project

1.1 A growing market for commercial aircraft

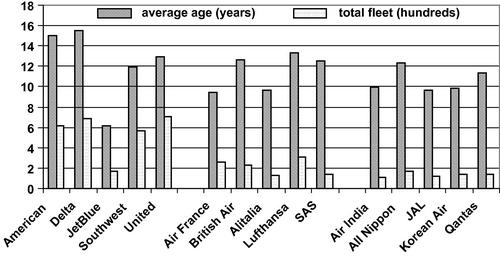

The fleet of commercial aircraft is aging and new market pressures portend a large and growing market for new aircraft. Approximate average ages of the fleets of representative US and international airlines as of the end of 2011, according to Airfleets (2012), are shown in Figure 1.1.

Figure 1.1 Size and average age of the fleets of US international airlines as reported by Airfleets (2012).

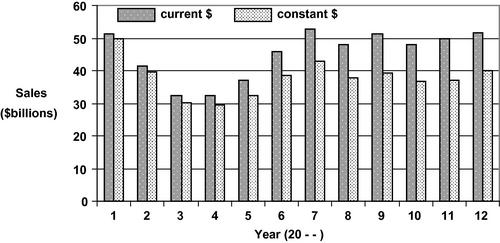

The escalation of fuel prices, increased concern over environmental effects, and changes in the nature of airline services to passengers are pushing airline operators into renewing their fleets. Manufacturers are therefore putting intense efforts into designing and producing aircraft that will provide superior economic and environmental performance. Sales of US commercial aircraft rose from a low point in 2003 up to a fairly constant value starting in 2007, as can be seen in Figure 1.2, as reported by the Aerospace Industries Association (2012).

Figure 1.2 Annual sales of US civil aircraft over the period 2001–2012 as reported by the Aerospace Industries Association (2012). The numbers for 2012 are estimates. The deflator used by the AIA assumes 2000 as the base year.

Airbus has had some setbacks, in both the new A380 and the developing A350, and now has somewhat more than 40% of market share, a figure that is often taken as an indicator of serious competition. The Airbus figures owe a great deal to the continued success of the narrow-body A320. However, in the wide-body field it is losing out to Boeing, whose 777, 747-8, and the new 787 are all doing very well in terms of orders, in part because of A350 development delays and A380 operational problems, like wing cracks, described by Flottau (2012). Though it is anticipated that sales will grow somewhat, as shown in Figure 1.2, there is concern that the world economic situation in general, and the rapidly escalating fuel prices in particular, may reduce these estimates. The former suggests possible drops in demand while the latter forces fleet upgrades to newer, more fuel-efficient aircraft. The net result is currently uncertain, though precipitous drops in sales are unlikely. In any event, the backlog of orders is currently so large that if there is a drop-off in sales the effects won’t be felt for several years, giving manufacturers an opportunity to revise their business strategies.

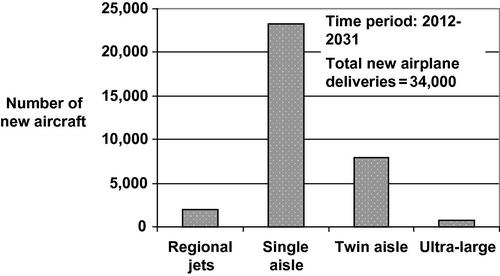

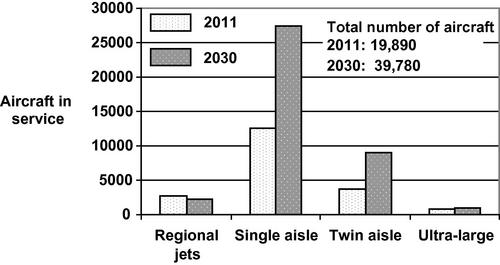

The Boeing Current Market Outlook (2012) calls for about 34,000 new commercial aircraft to be delivered over the next 20 years, as shown in Figure 1.3, constituting a doubling of the fleet in service. The major segment of this new growth in airplane deliveries is predicted to be in single-aisle, or narrow-body, aircraft, a segment expected to more than double in size. This reflects Boeing’s confidence in the move toward more direct flights, rather than hub and spoke flights, and this outlook is felt to be in response to passenger demand, as well as the prospect for reduced fuel burn by using more direct flights.

Figure 1.3 Number of new aircraft deliveries forecast by Boeing Current Market Outlook (2012) for the period 2011–2030 grouped according to aircraft type.

This potential growth is also encouraging new aircraft manufacturers. China, Russia, and Japan are all developing 70–90-seat regional jets providing direct competition to current regional jet leaders Embraer and Bombardier. However, the regional jet market is seen to be relatively weak and all these manufacturers are contemplating moves toward larger size (100 plus seats) jets where they will be starting to compete with Boeing and Airbus. The short-range, or regional, market is slowly returning to turboprop-powered aircraft, largely because of the better fuel economy they offer.

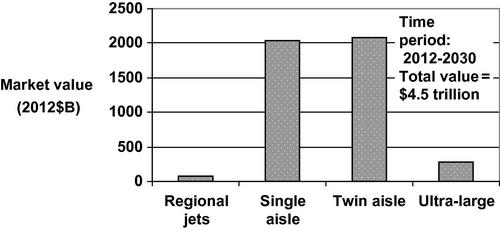

However, another passenger demand is increased comfort and this is best filled by twin-aisle, or wide-body, aircraft. Not only are pressures from business travelers making international carriers expand their business class sections, but now seats that fold flat into beds are becoming a major factor in airline competition. The long-range capabilities of newer aircraft make these upgrades increasingly important. It is not unusual to have 16- and even 18-hour flights, like Singapore Airlines’ direct flight from Singapore to Los Angeles and to Newark. Although the projected number of twin-aisle aircraft to be delivered in the 20-year period is only about one-third that of single-aisle aircraft, the market value of the twin-aisle aircraft is about the same as that of the single-aisle aircraft, as illustrated in Figure 1.4. The Boeing Current Market Outlook (2012) forecast for the change in the size and make-up of the fleet is summarized in Figure 1.5 which shows the fleet complexion in 2011 compared to that projected for the year 2030.

Figure 1.4 Market value of new airplane deliveries forecast by Boeing Current Market Outlook (2012) for the time period 2012–2030 grouped according to aircraft type.

Figure 1.5 Forecasts for the change in the size and make-up of the fleet by the year 2030 grouped according to aircraft type.

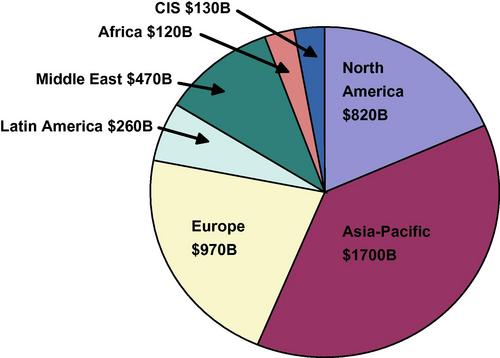

The Boeing Current Market Outlook (2012) also highlights the rapid growth and industrialization of the Asia-Pacific region as illustrated by the market value share breakdown according to region shown in Figure 1.6. China is expected to lead in capacity growth over the period considered, at a rate of about 8% and by 2027 will have half the traffic of the North American market. Currently it has less than 20% of that market. Expansion of the European Union and the Commonwealth of Independent States of the former Soviet Union is expected to result in their domestic traffic overtaking the North American domestic traffic in the near term, then falling back to a lesser value by 2026.

Figure 1.6 Forecast of the market value of the purchases of new aircraft during the time period of 2012–2031. Total market value = $4.5 trillion.

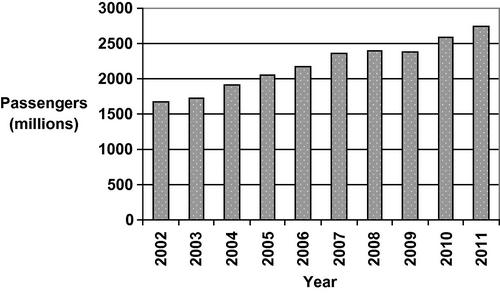

The International Civil Aviation Organization (ICAO) released preliminary figures for the year ending 2011 indicating that passenger traffic on the world’s airlines increased by about 6.5% over 2010, in terms of passenger-kilometers performed, according to ICAO (2011). Passengers carried on scheduled services grew by around 5.6% to 2.7 billion; the trend over the past 10 years is illustrated in Figure 1.7. Statistics supplied by ICAO’s 190 Contracting States also show an overall increase of about 4.3% over 2010 based on metric ton-kilometers performed; this is a measure which includes passenger, freight, and mail traffic. The global passenger load factor was 78%, about the same as in 2010. Freight carried worldwide on scheduled services in 2011 went up to approximately 51.4 million metric tons compared with about 50.7 million metric tons in 2010.

Figure 1.7 Airline passengers carried over the 10-year period 2002–2011 as reported by the ICAO (2011).

The ICAO points out that the continued high growth rates in passenger traffic across all regions in a difficult world economic environment was a positive for 2011. They forecast 3.5% growth in the world economy over the next 2 years resulting in a 6% growth in revenue passenger-kilometers over the same period. However, the uncertainty regarding the weakly growing economy in the United States and Europe, which could expand to other regions, coupled to the erratic behavior of growing fuel prices makes predictions questionable.

1.2 Technology drivers

Airliner design is a rather mature field and it is unlikely that improvements will involve breakthroughs. Instead, the persistent application of small cumulative advances will provide competitive advantages for the manufacturer that can successfully integrate them into their product. The areas of greatest promise center around reductions in weight, drag, and engine emissions, as well as noise abatement techniques. Wall (2006) reported on the initiation of a “Clean Sky” program by the European Union as a major part in the Aeronautics and Air Transport portion of its 7-year, $69 billion, Seventh Framework Program. The objective was to research an array of emissions-reducing technologies that could be ready enough to be incorporated into designs for aircraft entering service around 2020. This aeronautical research program, which included demonstrator engines, was funded at a level of about $2 billion and now a second, larger phase, to run through the 2014–2016 period is being drawn up, according to Warwick (2012).

In the summer of 2006 jet fuel prices rose to over $2.20 per gallon in New York and remained fairly stable through the summer of 2007. However, by the summer of 2008 the price almost doubled, increasing to almost $3.85 per gallon. During the global economic slump of 2008–2009 the price dropped back down to about $1.25. By 2011 the price had slowly climbed back up to around $3.00 and has remained around that value through the middle of 2012. Crude oil futures costs are volatile and are expected to average $115 per barrel, leaving most manufacturers feeling the pinch to improve fuel economy. After a brief period of profitability following the losing years between 2002 and 2006, the airlines are again facing the prospects of substantial losses and are seeking new ways to reduce costs. Boeing’s emphasis on designing the new 787 as a particularly fuel-efficient airliner has proven to be a remarkably good decision. Airbus has looked to the A350 to provide similar attractiveness to the airlines. In the high-volume single-aisle narrow-body aircraft category the fuel efficiency mantra has been at the center of the heated battle between the B737Max and the A320Neo, even though both are still in the development stage, as noted by Norris (2012). The high oil prices have also served to cool off the market for regional jets as airlines look to larger-capacity aircraft which have lower fuel costs per seat.

Environmental concerns are pushing airlines to demand “greener” and more fuel-efficient aircraft. This is of particularly acute concern since airline fleets are aging and next-generation replacements for the immensely popular single-aisle aircraft like the Boeing B737 and Airbus A320 are now being designed. Operators would like to phase out older aircraft for new ones that burn less fuel, can meet more stringent environmental regulations that are looming in the future, and can spend more flight time between overhauls. Currently the fleet average fuel economy is about 20 km/l (48.2 mpg) per passenger and this is expected to rise to about 34.5 km/l (83.4 mpg) as new products with performance like the B787 and A350 are fully in service with the airlines.

Reducing the perceived and actual environmental impact of aircraft operations is being sought both by manufacturers and operators. Although a major effort in such areas is bound to involve political solutions ranging from taxes for exceeding tightening standards to sophisticated emissions brokering for trading credits on pollutants, the returns from technological improvements in all aspects of aircraft design, manufacture, and operation will likely be more rewarding. The effects of gaseous pollutants from engines, noise from engines and airframes and terminal maneuvers, and toxic materials used in production are the major issues under study.

1.2.1 Fuel efficiency

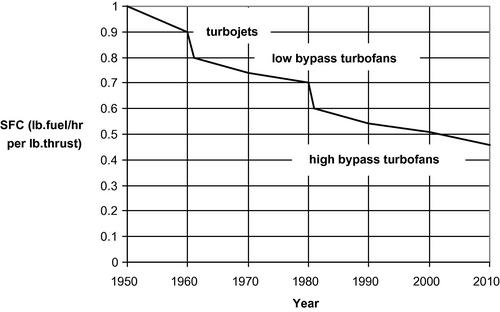

Aboulafia (2012) presents an interesting forecast of the airline business based on the changes brought by the operational and structural improvements forced by intense competition over the last decade. He suggests that the deciding factor for airline success is in the exploitation of technological advances that reduce fuel burn. The figure of merit for fuel efficiency is the specific fuel consumption which is defined as the weight of fuel consumed per hour per unit of thrust. Improvements in specific fuel consumption over the time period since the introduction of jet engines into commercial service are indicated by the trend line shown in Figure 1.8. The major contribution to the improvements arises from the introduction and development of the turbofan engine as discussed by Sforza (2012).

Figure 1.8 Trend in specific fuel consumption (SFC) since the introduction of the jet engine into commercial service.

Airline operators have seen fuel costs overtake labor costs as the largest item in the breakdown of operating costs as we will show in Chapter 11. US airlines spent over $50 billion on fuel alone in 2011, according to Anselmo (2012), helping keep airline profit margins down to 2%. Though airlines have grown sophisticated in hedging the cost of crude oil purchases, there is an additional cost premium for refined jet fuel. The volatility of these premiums has caused one airline, Delta, to develop a subsidiary, Monroe Energy, with its own fuel refinery in an attempt to have additional control over fuel prices. The promising capabilities of new aircraft, like the competing single-aisle offerings of Boeing’s B737Max and Airbus’s A320Neo, will push production up as airlines move to upgrade their fleets. The larger two-aisle wide-body aircraft are less technology-dependent, Aboulafia contends, and carriers can lean on equipment upgrades, particularly in the area of premium seating accommodations and cabin refinements.

Another turnabout caused by the rise in fuel costs is the revival of interest in turboprop aircraft. The common vision in the airline industry was that turbofan aircraft were more attractive to travelers than turboprops in the short-range regional market. However, the unrelenting increase in fuel costs prompted a second look at turboprops, especially because they can save as much as 30% in fuel consumption per seat compared to jets. Although projections for the growth of the near-term market for turboprop aircraft currently appear modest, the outlook for a decade into the future seems to be brightening. That this is the case is fortified by the news that five aircraft manufacturers are considering developing new, larger (90-seat) turboprop aircraft, according to Perrett (2013). The companies are widely spread internationally, with Asian entries from China, India, and South Korea, as well as the current Western manufacturers ATR in Europe and Bombardier in Canada.

1.2.2 Weight reduction

Weight reduction and control is a central theme in airplane design since it is the major determinant in performance. Part of the performance is connected with fuel burn since a more fuel-efficient aircraft needs less volume to store the fuel, reducing the empty weight of the airframe. Furthermore, requiring less fuel per trip means a reduced takeoff weight, and reduced total weight requires less thrust in takeoff and climb. Naturally, burning less fuel per trip also reduces the emissions of CO2, NOx, and other pollutants, making the airplane more environmentally efficient. With fuel costs becoming increasingly important in revenue operations, the ability to reduce fuel usage then reduces both costs and environmental impact.

The new Boeing B747-8, a successor to the B747-400, has a market niche in between the 365-seat B777-300ER and the 525-seat Airbus A380. Norris and Flottau (2012) report that Lufthansa’s first revenue transatlantic flight of the B747-8 showed about 3% lower fuel burn than would have been achieved with their B747-400 aircraft. Planned performance improvement packages for the larger General Electric GEnx-2B engine will help reduce fuel burn, but in addition, weight reductions of up to 5000 lb are planned, as are aerodynamic enhancements. That weight reductions are seen as very important in this regard is made clear when it is realized that this planned weight reduction is quite small, amounting to only about 1% of the empty weight of around 470,000 lb, which, in turn is about 48% of the planned maximum takeoff weight of 987,000 lb. Other relatively small, but cumulatively important weight savings accrue from details like reduced galley equipment and cargo container weight, reducing the potable water carried, maintaining control of the amount of contingency fuel carried, and using lighter seats.

The move toward composite materials in airframe, engine, and cabin equipment is part of the drive to reduce aircraft empty weight. The last decade has seen the weight fraction of composite material used in commercial aircraft rise from about 10% to over 50% in the search for weight reductions. This deep penetration of composites into major structural members is characteristic of new programs. For example, the next-generation Boeing 777X is planned to have all-composite wings which are expected to yield substantial weight savings. The B787 uses composite structures for the fuselage where their increased resistance to hoop stresses allows substantial cabin pressure increases. Previously, aircraft cabins were pressurized to the equivalent of 8000–9000 ft altitude. Now the B787 can safely provide a cabin pressure equivalent to a 6000 ft pressure rating which results in increased comfort for passengers.

However, uncertainties concerning the effects of long-term exposure to extreme environmental conditions on the structural and functional properties of polymer matrix composites have thus far been a deterrent to their widespread use. There are challenges in engineering polymer matrix composites and the cost of testing and quality assurance costs can limit the benefits of their use. Because the movement is continually in the direction of increasing use of composite materials, the aircraft manufacturers, airline operators, and regulatory bodies are cooperating on the standardization of materials, techniques, and training certification.

1.2.3 Drag reduction

Drag reduction and overall improvements in flow control are expected to yield continuing improvements in performance. Aerodynamic improvements of airliner wings are focused on wingtip treatments, both in planform shape and in continually evolving winglet designs aimed at reducing lift-induced drag in cruise. Both the B737Max and the A320Neo are using the latest version of winglet which incorporates two fins, one tilted up and one down, on each wingtip. Vortex generators are used on wing surfaces to energize boundary layers thereby avoiding separation and extending the range of attached flow. Greater attention to detail, such as improving seals and minimizing gaps on aerodynamic surfaces, has become a necessity in the drive to reduce drag. Similarly, simple operational improvements like keeping aircraft surfaces washed and free from the roughness caused by dust, insects, etc., can pay a dividend in reduced drag.

A new area of practical drag reduction involves exploiting many years of research in boundary layer control, particularly techniques to maintain laminar flow over large surface areas. Boeing is introducing hybrid laminar flow control on the horizontal and vertical stabilizers on their new stretched B787-9 in an attempt to reduce profile drag by 1%. If this technique, which has been flight-tested, can be effectively employed on the wings, fuel burn may be reduced by as much as 20% on typical flights. Research is also being carried out in relatively new areas such as synthetic microjets for localized flow management and plasma generators embedded in aircraft skin which can locally ionize the flow and achieve electromagnetic control of the flow.

1.2.4 Engine design

The availability of new engines that promise greatly improved fuel efficiency is the basis for the advanced single-aisle B737Max and A320Neo aircraft. In mid-2008 Pratt & Whitney introduced the PW1000G, the geared turbofan, which incorporates the results of research initiated a decade earlier. This engine improves fan performance by matching its speed to the driving turbine more effectively as well as by incorporating a variable area fan nozzle. The PW1000G, which has completed over one hundred hours of flight testing, is the first in a line labeled “Pure Power” engines by Pratt & Whitney. CFM International, a joint venture by GE Aviation and SNECMA that brought out the successful CFM56 series, is bringing out the new LEAP-X (Leading Edge Aviation Propulsion) engine. This engine utilizes GE’s advanced combustor technology along with composite, rather than titanium, fan blades to provide its performance improvements.

One of the other approaches for improved fuel efficiency is the revisiting of the unducted fan, now often called the open rotor, which sacrifices some turbofan speed for improved fuel economy. This engine, which lies between a conventional turboprop engine and a turbofan engine, was extensively studied in the 1980s when inflation and increased oil costs made fuel economy a major issue. The higher propulsive efficiency of a propeller is achieved at the cost of maximum speed, as shown by Sforza (2012) and the unducted fan may be an optimal solution for some airplanes. In this regard it is interesting to note that in 2004 the turboprop fleet constituted 23% of the world passenger fleet and is expected to continually drop over the next 20 years to the point where they will comprise only 1% of the world fleet. There is also seen a continuing trend of reduced travel on 300-mile routes, apparently indicating a growing preference to drive rather than fly over those distances. But skyrocketing fuel prices are forcing manufacturers to reconsider turboprops in new airplane designs. Turboprops are much more fuel-efficient than turbofans and are well-understood propulsion systems, but after weaning the public away from propellers to jets the industry faces the challenge of winning them back to propellers. The widespread public awareness of environmental issues, as well as the economic factor, will be helpful in this regard.

Engine design is aimed at producing the least polluting strategies for combustor design over the entire operating regime of the engine. This is part of a much larger research program covering combustion in all its guises, including automobiles, trucks, off-road equipment, and stationary power plants. At the heart of the matter is the extent to which the combustion of hydrocarbon fuels produces two important gases: CO2 and NOx, both of which are associated with atmospheric degradation. The former is a so-called greenhouse gas whose molecules are effective in trapping the infrared radiation emitted by the surface of the Earth and reducing the possible cooling effect. The latter is a chemically active gas involved in complex reactions with other gases in the atmosphere, and can contribute to depletion of ozone in the upper atmosphere that otherwise would help reduce the ultraviolet radiation from the sun from reaching the Earth’s surface. Unfortunately, the production of CO2 and NOx is closely related and when the concentration of one is reduced, that of the other is increased. Therefore, very strict combustion control is necessary to find an optimal middle ground for the acceptable production of each. Some current research programs in these areas are reported by Chang et al. (2013).

1.2.5 Carbon footprint

The entire aviation industry is considered to produce around 2% of the CO2 emissions produced by fuel-burning activities in the world (for comparison, the electricity and heating sector produces about 32%) and is becoming keenly aware of its role in terms of its “carbon footprint.” The European Union has developed rules concerning the inclusion of aviation in its emissions trading scheme and it is likely that the US, and ultimately the rest of the world, aviation community will come under some similar kind of regulatory system. As emissions trading protocols involve economic penalties for producing more than some baseline amount of emissions, there is considerable scrutiny of the means to achieve the required regulatory goals. The carbon footprint for an individual passenger flying between two cities may be estimated using the online calculator available from ICAO (2012). For example, one passenger flying a round trip from JFK airport in New York to FCO airport in Rome generates an average of about 900 kg of carbon dioxide. The methodology used to form the estimate is also described. Information based on modeling analyses of this type is used in determining carbon offsets for use in different environmental trading programs.

1.2.6 Biofuels

Fuel cost and availability concerns caused increased attention to be paid to synthetic hydrocarbon fuels as an alternative to standard Jet-A fuel. Synthetic paraffinic kerosene (SPK) is generally made by converting coal or natural gas into a liquid fuel (often designated as CTL or GTL products, respectively) using the Fischer-Tropsch process, a technique developed in Germany in the 1920s and used to produce fuel during World War II. However, such fuels, and others derived from ethanol, are often less energetic than Jet-A, and suffer from other operational disadvantages, such as their behavior at the low temperatures typically met at operational altitudes. Tests at Tinker AFB in Oklahoma on a TF33 engine burning a half-and-half blend of synthetic kerosene and JP-8 performed the same as 100% JP-8. The combustion of the synfuel blend resulted in a 50% drop in sulfur emissions, since the Fischer-Tropsch process produces no sulfur in the synthetic kerosene. This elimination of sulfur is one of the major advantages of CTL and GTL fuels since coal and natural gas are generally quite rich in sulfur, while a disadvantage is that the process itself is energy-intensive. The test was carried out using fuel produced by Syntroleum, a Tulsa, Oklahoma refinery. Flight tests using different fuels have been carried out at an increasing rate and the degree of success in these tests may influence the commercial sector in turning to a blend of Jet A and synfuels, and ultimately perhaps to pure synfuels. South African Airways has been flying blends of CTL and Jet A for many years. The CTL is produced by Sasol in Secunda, South Africa.

Because of the growing number of possible synthetic or biofuel production mechanisms the technical standards organization ASTM International has been active in streamlining processes for approving new fuels to replace the standard jet fuel, known as Jet A, including CTL and GTL synthetic fuels, and examining the possibility of including biofuels. The ASTM has developed the D7566 specification for synthetic jet fuels including Fischer-Tropsch fuels and hydroprocessed esters and fatty acids (HEFA) fuel. In any event the inclusion of those fuels will generally only be permitted blends of up to 50% with ordinary petroleum-based fuel. Tests of biofuels produced from vegetable oils (Generation 1 biofuel) have been carried out, but concern about diversion of food stocks to fuel has turned emphasis to pursuing non-food sources, such as cellulose waste, non-food plant oils, and algal oils (Generation 2 biofuel). Current interest centers on non-food plants like Jatropha in Africa, Pongamia in India, and the castor oil plant in Brazil, while algal oils are considered to be later entries into the alternative fuel competition. Warwick (2012a) presents a brief but comprehensive review of the many directions biofuel producers are considering.

1.2.7 Alternative fuels and power sources

Hydrogen, which is often touted as an alternative to hydrocarbon fuels because of its clean-burning characteristics and high energy content per unit mass, suffers from an inadequate infrastructure for producing, distributing, and storing the product for use on a large scale. In addition, because of its low density, hydrogen suffers from relatively poor energy content per unit volume, a characteristic that necessitates larger tanks, and therefore larger and heavier aircraft. There is also interest in fuel cells, which still require fuel, generally hydrogen, with all the problems mentioned earlier. However, for the airline industry the application of fuel cells will likely be for onboard electrical power generation rather than propulsion. In this manner the propulsive fuel burn will be reduced since the main engines will not need to provide for all the auxiliary power demands. For example, electricity provided by fuel cells can power electric motors mounted in the landing gear and would be used to taxi the aircraft.

Surface treatments of airplanes to control corrosion often include toxins, like cadmium and chromium, which manufacturers would like to replace with environmentally benign substances. Even at the end of an aircraft’s life there is concern about its environmental impact and manufacturers are seeking ways to improve the recycling capability of its aircraft. Boeing has teamed with a group of companies to form the Aircraft Fleet Recycling Association whose goal is to establish standards for disposing of aircraft. Wall (2008) reported on efforts carried out by Airbus which showed the possibility of converting 85% of the aircraft weight into salable products, typically as secondary raw material. The large percentage of aluminum in aircraft currently reaching the end of their life cycle is particularly valuable since its production is energy-intensive and recycling it uses 90% less energy. Composite materials are less of a concern at the moment because they are just entering the fleet and have considerable lifetime remaining before their disposal is imminent.

1.2.8 Noise and vibration

Noise and vibration control is another area of strong environmental concern and involves engine and airframe design, as well as operational factors such as terminal maneuvers and trajectories. Quieting the cabin during long cruise periods is of great concern to passengers, while sideline noise and flyover noise footprint is important to airport staff and residents in the airport operational area. To deal with these issues, research by engine manufacturers is ongoing in improving the design of inlets, fan and compressor blades, and nozzles, while airframe builders are studying landing gear and flap design, and airline operators are examining flight operations and trajectories that would alleviate some of the noise problems.

The largest European Commission research project dedicated to aircraft noise reduction, SILENCE(R) was started in April 2001 with the French engine manufacturer Snecma acting as project coordinator. By completion of the project in late 2007, improvements in noise reduction technology had been achieved in several areas. Because engine and airframe each generate about equal contributions to the total noise produced by an aircraft both contributions were studied. In the area of airframe noise, an important practical improvement was made on acoustic liners for engine nacelles by the development and assessment of zero-splice inlet liners. Since conventional liners are manufactured in several pieces (typically three), splices are necessary to join the pieces together. It is well known that these splices have a negative effect on the performance of the liners. This is not only because of the reduced area covered by the lining material, but also because the splices cause the prevailing circumferential acoustic modes to scatter to other modes, which are less effectively attenuated. Large-scale research on zero-splice inlet liners has been conducted on the Rolls-Royce Trent engine. Airbus has already patented the zero-splice inlet and installed it on all A380 engines, contributing to the remarkably low-noise levels registered during the aircraft’s acoustic certification process. In future, it will be fitted as standard on all new Airbus aircraft and may well be adopted by other manufacturers as well. The extensive airframe noise tests also focused on technologies to reduce landing gear noise and noise generated by high lift devices. Flight tests were carried out on an Airbus A340 with landing gear fitted with low-noise fairings. For future applications, more comprehensive changes to the landing gear configuration may be needed to reduce noise.

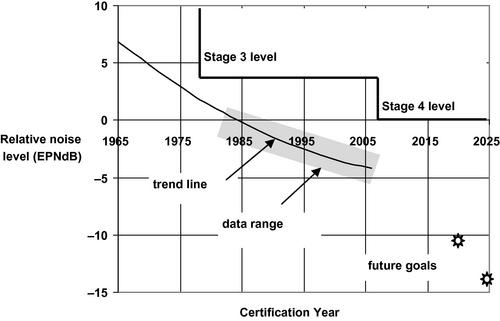

Envia (2012) describes NASA’s current and future engine noise reduction research, focusing on three areas: alterations to the engine cycle, application of noise reduction materials, and reducing engine noise propagation by judicious shielding of the engine by airframe components. The trend of noise reduction with year of aircraft certification is shown in Figure 1.9. The noise level is given in terms of effective perceived noise level measured in decibels (EPNdB) which according to FAR Section A36.4 is a single number evaluator of the subjective effects of airplane noise on human beings. It consists of the instantaneous perceived noise level corrected for spectral irregularities and for duration. The stage levels shown in Figure 1.8 correspond to the maximum noise levels permitted as described by the FAA Part 36 regulations. The research goals for the 2020–2025 time frame are also shown in Figure 1.9.

Figure 1.9 Noise levels for jet transport aircraft as a function of the year of aircraft certification relative to Stage 4 airplane requirements. Also shown are the goals of current research.

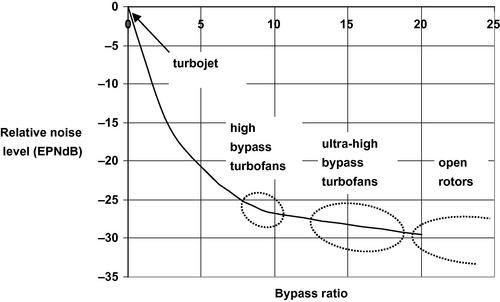

The most effective engine cycle change for reducing noise involves increasing the bypass ratio, that is, the ratio of mass flow of air passing through the engine fan to the mass flow of air passing through the engine core where the fuel is added and burned. The turbojet engine, which has a bypass ratio equal to zero, became the engine of choice for airliners in the mid-20th century because of its ability to maintain high thrust at high speeds, unlike propellers. However, incorporating a fan into the turbojet engine can provide substantial improvements in fuel efficiency without significant reductions in thrust at high speed, as shown by Sforza (2012). The turbofan engine became the engine of choice in the latter part of the century accompanied by continuing increases in the bypass ratio. Currently the largest turbofan engines, the GE90 and Rolls-Royce Trent 1000, have bypass ratios between 9 and 10. The improvements in fuel efficiency as the bypass ratio grew also provided a reduction in the engine noise level. Carrying the high bypass ratio to even higher levels brings one to the realm of ultra-high bypass turbofans and ultimately to the open rotor, or unducted fan, as indicated schematically in Figure 1.10.

Reduction and containment of engine noise may be achieved by constructing the fan casing of a sound-absorbing material. Foamed metal material like cobalt or an iron-chromium-aluminum alloy is used within the casing surrounding the fan. The pores in the metal are instrumental in dissipating the acoustic energy of the noise. Another engine structural modification aims at mitigating noise associated with the interaction of the aerodynamic wake of the moving fan rotor with stationary guide vanes. The so-called soft vane concept is based on providing hollow chambers within the stationary vane, each of which is sized to act in damping specific frequencies of the spectrum of time-varying pressure field seen by the vane.

Noise blocking by appropriate integration of the airplane structure with the engine placement is another approach. To be most effective, the engines must be placed above the wing or fuselage so that those structures can block some of the radiated engine noise from reaching the ground. In a similar manner tail surfaces may serve to block sideline engine noise. Of course, such alterations in the aerodynamic shape must be carefully analyzed to ensure that achieving noise reduction does not cause degradation of the overall airplane performance. For example, a negatively scarfed, or raked-back inlet face, can change the directional pattern of the radiated engine noise, so that more noise will be directed upward, and less noise downward. However, application of the concept to existing aircraft requires extensive redesign and is unlikely to be economically viable.

1.3 Cargo aircraft

Globalization and the attendant increase in international trade make air freight an increasingly important component for the movement of goods. In addition, growing concerns about environmental impact make fleet modernization a necessity. The market for cargo aircraft is estimated to be in the range of $100 billion and this is driving aircraft manufacturers to be competitive. The Boeing B747-8F is a new freighter aircraft that was first delivered in late 2011. It is the counterpart of the international passenger version, the B747-8I. Operators of the B747-8F are reporting fuel burn about 1% better than expected in the first group of aircraft in service. But Boeing is targeting additional improvements in performance as production continues. The Airbus A380F was in development but has been put on hold in order to concentrate on issues with the A380 passenger version that were considered more pressing. The A330-200F, a freighter based on the A330 family, entered service late in 2010. A substantial fraction, around 20%, of earlier wide-body passenger aircraft that are being retired in favor of newer, more fuel-efficient aircraft, will be converted to freighters. These include earlier aircraft like the following: McDonnell Douglas MD10 and MD11, Boeing B747-200, and Airbus A300B, and later aircraft like Boeing’s B747-400 and B767 and Airbus A300-600. This will provide additional work for maintenance, repair, and overhaul companies (MROs) around the world.

More than half of international air cargo shipments are carried on pure freighters with the remainder carried aboard passenger aircraft and this fraction is expected to grow in coming years. The impetus for shipping by air is delivery speed, but this is tempered by the increased cost, and if costs can be trimmed there will be even greater demand for air cargo transport. Although freight operations constitute an important segment of the aircraft industry, the study of some of the specialized aspects of freighter aircraft design is outside the scope of this book.

1.4 Design summary

1.4.1 Mission specification

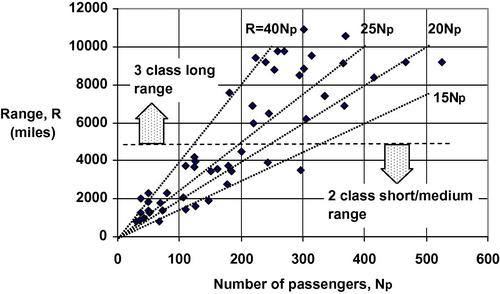

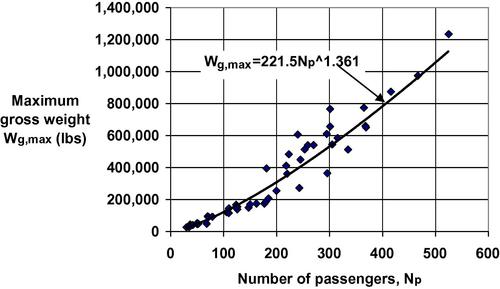

The objective of the academic design project is to develop a preliminary design for a commercial aircraft which will best satisfy a particular mission requirement. The mission is basically defined in terms of the range over which a specific payload is to be transported at a desired speed. In the case of commercial airliners the payload is generally stipulated in terms of the number of passengers to be carried. Generally, each student or group of students is assigned a different mission to be satisfied. Data for 46 operational commercial jet transport aircraft are shown in Figure 1.11 illustrating the relationship between the two basic mission specifications, range R and the number of passenger seats Np. It is obvious from Figure 1.11 that there is a broad R−Np design space available to airline operators and a wide array of aircraft from which to choose. For ranges greater than around 5000 mi aircraft cabins are typically configured for three classes: first, business, and economy, while for ranges less than 5000 mi the cabins are mostly two class configurations. Although there is a broad R−Np space, the same is not true when we consider the relationship of the maximum gross weight Wg,max to the number of passengers Np. The correlation between Wg,max and Np is quite close, as shown in Figure 1.12, and may be approximated by the following equation:

![]()

Figure 1.12 Take-off weights versus number of passenger seats for 46 operational commercial jet transports.

1.4.2 The market survey

Prior to designing any new aircraft, it is essential to see what the competition is offering. If your aircraft is not decidedly better than what exists in the market, it would be foolish to “bet your company” on developing a new design. By the same token, if it would serve a market that doesn’t show promise of growth, or at least robustness, a new design would be unlikely to succeed. For example, Singapore Airlines (SIA) was the first operator of the super-jumbo Airbus A380 which entered service with the airline in late 2007. They acquired these airplanes because they felt that new planes have very strong passenger appeal, and their Boeing B747-400 aircraft were aging. The A380 delivers 12–15% lower seat-mile costs while its large size permits revenue growth in dense, heavy routes with slot-constrained airports. In 2012 there were 75 A380 aircraft in commercial service. Passenger handling issues in very large aircraft pose some challenges and airlines often configure their A380 aircraft to seat fewer than the nominal 555 passengers, perhaps around 480 seats. This has also been the case with B747 flights, where seating is often kept in the range of 380–385 rather than the nominal 440. But the airlines are keenly aware that they need to sell more seats rather than fewer to prosper. The difficulties faced by Airbus in bringing the very large A380 into production and service have been exploited by Boeing deciding to build the B747-8, the third-generation 747. For the purposes of a preliminary design, the best business case must be made by the design teams to identify a suitable niche exists for the designs assigned, and the purpose of the exercise is to make the best aircraft to meet the specifications.

There is a second reason for reviewing existing aircraft designs. It is usually not necessary to reinvent the wheel. Designers do not start with a blank sheet of paper. It is generally useful to follow what others have done in a preliminary feasibility study. Similar aircraft will suggest the type of engines, flaps, airfoils, wing geometries, fuselage sizes, etc. to be used as first cut designs.

The market survey should rigorously examine three or four existing aircraft for which information is available and which most closely satisfy the assigned mission. Major sources of detailed technical information may be found in Janes’ All the World’s Aircraft (2012), Aviation Week and Space Technology, especially the annual inventory issue, like Aerospace (2012), and other sources, such as books and trade journals, as well as on-line sources; for example, see the websites of aircraft manufacturers like Boeing, Airbus, Embraer, Bombardier, etc. It is not expected that all required information will be easily available for all aircraft. It is valuable to gather three-view scale drawings, so that data may be estimated from the diagrams. Scale drawings and photographs can provide much useful data not generally presented in tabular form. In addition, models of all commercial aircraft, typically in the scale of 200:1, are readily available and inexpensive. Purchasing a model of one or more of the market survey aircraft to aid in visualizing subtle design features not noticeable in drawings can also be quite helpful. These other aircraft are the “competition” and the proposed design should turn out to be “better.” Collecting copies of photographs and three-view drawings of these aircraft for use in the final design report, always adhering to the applicable copyright rules, is important. There are a fairly large number of photographs of jet transports which are in the public domain and can be used freely. It is a good idea to keep an eye out for aircraft details when flying on commercial airlines and taking photographs for use in the design report when permission is granted by the flight crew.

Thus Chapter 1 of a design report should introduce the reader to the mission specification, the competitor aircraft and their characteristics, and the special attributes which the proposed design aircraft will possess. The detailed quantitative data for the competitor aircraft should be presented in tabular form, along with three views, in an Appendix for easy reference. However, photos of competitor aircraft should appear in the body of Chapter 1 along with the descriptions of these aircraft. Note that all tables should be numbered and titled, as should all figures.

Keep in mind that the United States government, through the Federal Aviation Agency (FAA), establishes airworthiness requirements to ensure public safety in aviation. The FAA, which is part of the US Department of Transportation, issues Federal Aviation Regulations (FAR) and FAA Advisory Notes which lay down rules for aircraft and their operation. The FAR are published as Title 14 of the Code of Federal Regulations and are available online in Federal Air Regulations (2012).

References

1. Aboulafia R. Jetliner demand: the changing landscape. Aerospace America. 2012;50(5):22-25.

2. Aerospace. Aviation Week and Space Technology. 2012:23-30.

3. Aerospace Industries Association, 2012. <www.aia-aerospace.org/assets/Table 1.pdf![]() >.

>.

4. Airfleets, 2012. <www.airfleets.net/home/![]() >.

>.

5. Anselmo JC. Airlines to wall street: where is the love? Aviation Week & Space Technology. 2012:12.

6. Boeing Current Market Outlook, 2012. <www.boeing.com/commercial/cmo/index.html![]() >.

>.

7. Chang CT et al. NASA Glenn combustion research for aerospace propulsion. Journal of Aerospace Engineering. 2013;26(2):251-259. doi:10.1061/ (ASCE)AS.1943-5525.0000289.

8. Envia, E., 2012. Emerging Community Noise reduction Approaches, NASA TM-2012-217248.

9. Federal Aviation Regulations, 2012. <http://rgl.faa.gov/Regulatory_and_Guidance_Library/rgWebcomponents.nsf/![]() >.

>.

10. Flottau J. Wing worries. Aviation Week & Space Technology. 2012:45-46.

11. ICAO, 2011. <www.icao.int/icao/publications/Documents/9975_en.pdf![]() >.

>.

12. ICAO, 2012. <www.icao.int/environmental-protection/CarbonOffset/Pages/default.asp![]() >.

>.

13. Janes’ All the World’s Aircraft, 2012–2013. IHS Global, Englewood, Colorado (published annually).

14. Norris G. Actual mileage may vary. Aviation Week & Space Technology. 2012:46-47 April 2.

15. Norris G, Flottau J. Big promises. Aviation Week & Space Technology. 2012:28-31.

16. Perrett B. Field of five. Aviation Week & Space Technology. 2013:38-40.

17. Sforza PM. Theory of Aerospace Propulsion. New York: Elsevier; 2012.

18. Wall R. Cleaner from cradle to grave. Aviation Week & Space Technology. 2006:134-138.

19. Wall R. Waste management. Aviation Week & Space Technology. 2008:44.

20. Warwick G. Coming together. Aviation Week & Space Technology. 2012:31-33.

21. Warwick G. Spreading the bet. Aviation Week & Space Technology. 2012a:42-44.