Chapter 16

Valuation Considerations on Rights Issues

16.1 INTRODUCTION TO RIGHTS ISSUES

One of the options available for a publicly listed company willing to raise equity by issuing new shares is to do so by offering preemptive rights to current shareholders. Equity offerings of this kind are commonly referred to as rights issues, due to the fact that existing shareholders are granted rights to subscribe for new shares proportionally to their current stake in the company and can either exercise such rights or sell them to other investors.

The1 price at which new shares are issued (subscription price) is set in advance by the issuer at a significant discount to the reference share price before the announcement of the offering terms. Preemptive rights can only be exercised during a limited time window (subscription period), during which the rights are detached from the shares and trade separately on the same stock exchange. For this reason, the first date of the subscription period is called ex-right date and the share price after detachment of the rights is also referred to as ex-right price (where “ex” stands for excluding). Unexercised rights at the end of the subscription period are often auctioned in a coordinated placement to the market called rump placement.

Investment banks can play an important role in rights issues, particularly as underwriters of the newly issued shares. In this case, the underwriting banks, often organized in a syndicate, guarantee the full proceeds to the issuer and commit to purchase any unsubscribed shares at the subscription price. On the contrary, in a non-underwritten rights issue, under specific market conditions, there is the possibility that some of the new shares remain unsubscribed.

From a valuation perspective, there are three main questions to be analyzed in relation to rights issues:

- How is the subscription price set by the issuer?

- What is the value of preemptive rights granted to existing shareholders?

- What is the impact of pricing on existing shareholders?

The next pages aim to provide simple answers to the above questions.

16.2 SETTING THE SUBSCRIPTION PRICE

A necessary condition for a rational investor to exercise preemptive rights and subscribe for new shares is that the subscription price must be below the ex-right price of existing shares. Otherwise, the investor would be better off buying shares directly on the secondary market where they are listed. Therefore, there is a clear incentive for the issuer to set the subscription price at a discount to the ex-right price.2 Intuitively, the discount should be large enough to ensure that the ex-right price will stay above the subscription price until closing of the subscription period. On the other hand, if the market believes the discount is too large, it could be read as a negative signal on the expected evolution of the share price of the issuer.

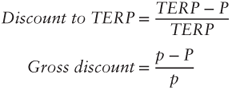

16.2.1 TERP and Discount to TERP

As mentioned in the first section of the chapter, the subscription price is announced by the issuer before the start of the subscription period. Therefore, when setting the terms, the issuer can only estimate what the expected ex-right price will be, based on the reference share price before the announcement of the terms (cum-right price). The expected ex-right price is called Theoretical Ex-Right Price or, in short, TERP. The discount applied on the subscription price is commonly expressed as a percentage of TERP (discount to TERP). An alternative way to express the discount is as a percentage of the cum-right price (gross discount).

There is a simple formula to compute the theoretical ex-right price:

| n | = | number of outstanding shares before announcement |

| p | = | reference share price before announcement (cum-right price) |

| N | = | number of new shares issued |

| P | = | subscription price |

| S | = | rights issue size ( |

In other words, TERP should be equal to the market cap of the issuer at announcement, plus the expected proceeds of the rights issue, all divided by the total number of shares outstanding after issuance of the new shares.

The discount to TERP and the gross discount are computed as follows:

It is possible to express the subscription price in terms of TERP and discount to TERP, and the number of newly issued shares as the ratio of the proceeds from the rights issue to the subscription price:

D = discount to TERP

As a result, the aforementioned formula to compute TERP can be restated as follows:

Although less intuitive, this second formula can be useful when it is necessary to compute TERP for given levels of discount to TERP and rights issue proceeds.

Some simple calculations will show that, for TERP to be strictly positive, the discount to TERP must be smaller than the ratio of the old market cap to the expected market cap following the rights issue. On the other hand, if the discount to TERP is zero, TERP will be equal to the reference share price before the announcement, making investors indifferent between exercising preemptive rights and buying shares on the secondary market. Therefore, it is sensible to conclude that the discount to TERP should be set in the following range of values:

The example shown in Exhibit 16.1 will help to clarify the concepts we have addressed in this chapter so far.

Exhibit 16.1 Calculation of TERP 3

| Market cap before rights issue announcement | ||

| Reference share price ($) | p | 100 |

| Outstanding shares (#) | n | 1,000 |

| Market cap ($) | 100,000 | |

| Rights issue terms | ||

| Rights issue size ($) | S | 20,000 |

| Discount to TERP | D | 25% |

| TERP ($) | 93 | |

| Subscription Price ($) | 70 | |

| New shares issued (#) | 286 | |

| Gross discount | 30% | |

| Expected market cap post-rights issue at announcement | ||

| Shares post-rights issue (#) | 1,286 | |

| Expected market cap ($) | 120,000 | |

| Equivalent to | 120,000 | |

It can be noticed that for ![]() . Therefore, in this example, any value between 0 and 83 percent would be accepted as a discount to TERP. In the next paragraph, we will discuss the factors considered by the issuer in the choice of the exact level of discount to TERP within the range of acceptable values.

. Therefore, in this example, any value between 0 and 83 percent would be accepted as a discount to TERP. In the next paragraph, we will discuss the factors considered by the issuer in the choice of the exact level of discount to TERP within the range of acceptable values.

16.2.2 Setting the Discount to TERP

As already mentioned, the issuer faces a trade-off between two contrasting needs in the choice over the level of discount to TERP. On the one hand, the company wants to minimize the probability that the ex-right price might go below the subscription price during the subscription period. On the other hand, the issuer does not want to communicate lack of confidence to the market by setting a discount to TERP which could be perceived as disproportionately low. Finally, additional constraints faced by the issuer are the willingness of investment banks to underwrite the rights issue below given levels of discount to TERP and the cost of underwriting corresponding to different values of discount.

In this context, the size of the rights issue, the market environment, and the level of discount set for previous offerings are all important elements to be taken into consideration by the issuer when pricing the rights issue.

Size of the Offering

As far as the size of the rights issue is concerned, one could expect the discount to TERP to get bigger, the higher the amount of proceeds to be raised in the offering. Intuitively, this is due to the fact that a larger offering would normally lead to a higher level of uncertainty regarding the outcome of the issuance. In analyzing the actual amount of risk associated with the size of the rights issue, the following factors should also be taken into account:

- The relative size of the offering vs. market cap before announcement: More indicative than its absolute size, it also makes a comparison with previous (if any) rights issues.

- The relative size of the offering vs. average daily volumes traded (ADTV): Liquidity of the stock is an additional element to be taken into account when assessing the risk associated with the size of the offering.

- Precommitments from major shareholders to exercise their rights: The announcement that some existing shareholders have committed to use their rights reduces the amount of rights to be placed in the market and decreases the level of uncertainty associated with the offering. The amount of proceeds linked to a lack of commitment from existing shareholders is also referred to as market risk.

- The capital structure/level of capitalization following the rights issue: If the level of capitalization after completion of the offering is perceived by the market as inadequate, it is likely that investors will be less eager to exercise rights and the risk of not achieving a successful completion will be higher. This effectively results from the fear of possible future capital increases and is especially true for financial institutions subject to capital requirements.

- The time frame linked with a rights issue: All else being equal, a shorter timeframe reduces the risk of significant price fluctuations and might lead to a less conservative discount to TERP. Such time frames are often dictated by national legislation and may vary significantly from one country to another.

Market Environment

Market conditions are also an important component influencing the level of discount to TERP. Differently from the size of the offering, the issuer has less control on this characteristic, especially when the need to raise capital does not leave much flexibility on timing. In particular, the following factors will need to be carefully analyzed:

- Historical and implied volatility of equity markets: A higher volatility in the stock market will add risk to the offering and will normally require a larger discount.

- Historical and implied volatility of the specific stock: Similarly to the previous factor, risk increases with a higher stock volatility, but the impact on the level of the discount might be even stronger in this case.

- Market sentiment on the company and the sector: A negative outlook on the sector and specifically on the issuer will make subscription of new shares less attractive and will potentially induce the issuer to increase the discount. Vice versa, a positive market sentiment toward the sector and the company issuing new shares might provide more flexibility to the issuer on the level of discount to TERP.

- Relative valuation vs. peers: An attractive valuation of the issuer with respect to comparable companies will provide higher incentives for investors to subscribe for the newly issued shares and increase the chances of successful completion of the offering. For this reason, rights issues are often announced by the issuer together with the presentation of a new business plan, also with the aim of highlighting the strengths of the company and its potentially attractive valuation.

Previous Offerings

The level of discount in previous rights issues, especially if peers' previous issues are available, provides relevant guidance to the issuer regarding the proper level of discount to TERP. On the other hand, it is also an important reference for investors who will check how the discount compares to previous offerings and, in case of divergence, will try to understand the underlying reasons.

It goes without saying that any benchmarking with respect to previous offerings will need to take into consideration comparability across the different dimensions discussed earlier and in particular:

- Rights issue size as a percentage of market cap

- Market risk as a percentage of rights issue size

- Market risk as a percentage of market cap

- Time frame

- Market environment at time of issuance

Exhibit 16.2 summarizes how the different factors analyzed above may influence the level of discount to TERP set by the issuer.

Exhibit 16.2 Influence of different factors on the level of discount to TERP

| Discount to TERP | ||

| Lower | Higher | |

| Rights issue size | ||

| Rights issue size as a percentage of market cap | Low | High |

| Rights issue size as a percentage of ADTV | Low | High |

| Market risk as a percentage of rights issue size | Low | High |

| Market risk as a percentage of market cap | Low | High |

| Level of capitalization post-rights issue | Adequate | Inadequate |

| Timetable | Short | Long |

| Market environment | ||

| Historical and implied volatility of equity markets | Low | High |

| Historical and implied volatility of the specific stock | Low | High |

| Market sentiment on the company and the sector | Positive | Negative |

| Relative valuation vs. peers | Attractive | Unattractive |

| Previous offerings | ||

| Discount to TERP in comparable offerings | Low | High |

16.3 VALUE OF PREEMPTIVE RIGHTS

In a rights issue, existing shareholders receive preemptive rights to subscribe for new shares at the subscription price. The reasons for setting the subscription price at a discount to TERP and the factors driving the level of discount were analyzed in the previous section. Our focus will now shift to the valuation of preemptive rights. In particular, we will show how to compute the expected value of rights at announcement of the terms and how such value should change during the subscription period based on the evolution of the ex-right price.

16.3.1 Theoretical Value of Rights at Announcement of the Terms

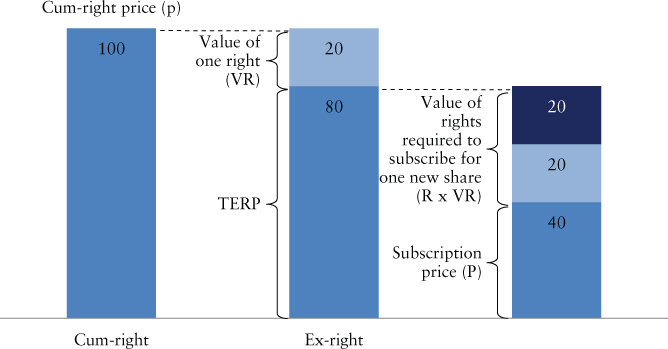

At announcement of the terms, the issuer communicates the size of the rights issue, the subscription price, and the number of newly issued shares to the market. Since one right is usually attached to each outstanding share, the ratio of new shares to old shares (subscription ratio) defines how many rights need to be exercised to subscribe for one new share. For instance, in an offering where the subscription ratio is 1:2 (one new share for two old shares), the subscriber will need to own and exercise two rights in order to subscribe for one newly issued share at the subscription price.

On the ex-right date, an investor willing to buy a share in the company will have two options:

- Purchase one share on the market at the ex-right price.

- Purchase the number of rights required to subscribe for one new share and pay the subscription price.

The two amounts should be the same or an arbitrage would be possible. If (A) was greater than (B), there would be a clear incentive to buy rights, and exercise them paying the subscription price. This would lead to an increase in the value of the rights toward the equilibrium price. Vice versa, if (B) was greater than (A), there would be no incentive to purchase rights and the resulting decrease in the value of rights should again adjust their price toward equilibrium.

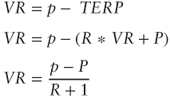

At announcement of the terms, the ex-right price cannot be observed but can be estimated by computing TERP as was previously shown in the chapter. Therefore, one way to estimate the expected value of one right at announcement is to use the following equation:

- R: number of rights required to subscribe for one new share

- VR: theoretical value of one right

Solving for VR:

By definition, as one right is attached to each outstanding share, the following should also hold:

Finally, the value of one right can also be expressed in terms of cum-right price and subscription price, leaving TERP out of the equation, proceeding as follows:

The example in Exhibit 16.3 and 16.4 will show how the above formulas can be used to compute the theoretical value of rights at announcement of the terms.

Exhibit 16.3 Calculation of the theoretical value of rights at announcement of the terms

| Market cap before rights issue announcement | ||

| Reference share price ($) | p | 100 |

| Outstanding shares (#) | n | 1,000 |

| Market cap ($) | n × p = m | 100,000 |

| Rights issue terms | ||

| Rights issue size ($) | S | 20,000 |

| Subscription ratio (new shares/old shares) | SR | 1/2 |

| Rights required to subscribe 1 new share (#) | 2 | |

| New shares issued (#) | 500 | |

| Subscription Price ($) | 40 | |

| TERP ($) | 80 | |

| Discount to TERP | 50% | |

| Gross discount | 60% | |

| Theoretical value of rights at announcement | ||

| Value of one right ($) | 20 | |

| Equivalent to | 20 | |

| Equivalent to | 20 | |

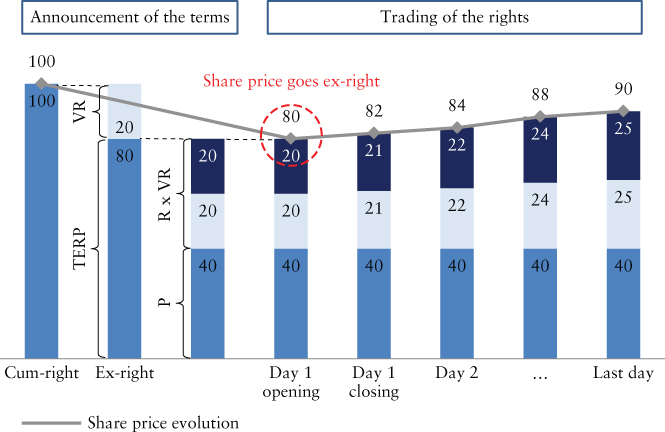

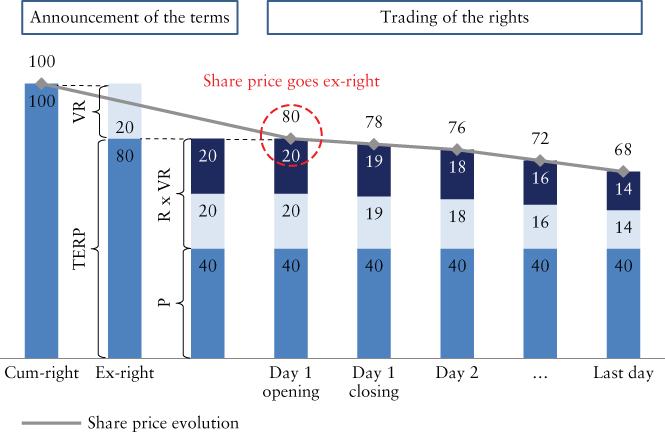

Exhibit 16.4 Separation of rights ($)

16.3.2 Theoretical Value of Rights During the Subscription Period

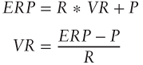

On the ex-right date, rights are detached from existing shares and start to trade separately on the same stock exchange. For the whole period in which rights are trading, the stock price is referred to as the ex-right price. The ex-right price will evolve from its theoretical value (TERP) during the subscription period as a result of new information flowing to the market. However, the following equation should be satisfied throughout the period in which rights are trading since an arbitrage would be possible otherwise:

ERP: Ex-Right Price

The examples in Exhibits 16.5 and 16.6 will show how the value of rights is expected to evolve in case of positive and negative share price evolution after detachment of the rights.

Exhibit 16.5 Separation of rights and positive share price reaction ($)

Exhibit 16.6 Separation of rights and negative share price reaction ($)

In reality, small differences between the levels at which rights are traded and their theoretical value can be observed. Among other factors, this can be due to the time value associated with rights, although such component is limited since the subscription period normally lasts only a few weeks. Discrepancies could also be the result of low liquidity in the trading of rights.

16.3.3 Impact of Pricing on Existing Shareholders

Provided with an understanding of the value attached to preemptive rights, it is now possible to discuss the implications caused by the subscription price set by the issuer to existing shareholders. This is equivalent to analyze whether the choice of the discount to TERP is neutral for current shareholders. Neutrality can be assessed under different dimensions. The focus of this section of the chapter will therefore be shareholders' net worth and dilution.

Shareholders' Net Worth

Before announcement of the terms, the net worth of an investor whose only asset is a shareholding in the company is the following:

| nw | = | net worth preannouncement |

| ns | = | number of shares owned |

At announcement of the terms, the expected net worth of the investor will be equal to the sum of the expected value of its shareholding and the expected value of rights.

| NW | = | net worth post announcement |

| nr | = | number of rights assigned |

Assuming that ![]() (as one right is normally assigned to each existing share), and considering that

(as one right is normally assigned to each existing share), and considering that ![]() , it is possible to express NW as follows:

, it is possible to express NW as follows:

It can be noticed that the level of net worth post-announcement is expected to be the same as before. In addition, such level does not depend on the discount to TERP set by the issuer.

Exhibit 16.7 compares the net worth of an existing shareholder before and after announcement of the terms for different levels of discount to TERP.

Exhibit 16.7 Shareholders' net worth should not be affected by the level of discount to TERP

| Case 1 | Case 2 | Case 3 | ||

| Market cap before rights issue announcement | ||||

| Reference share price ($) | p | 100 | 100 | 100 |

| Outstanding shares (#) | n | 1,000 | 1,000 | 1,000 |

| Market cap ($) | 100,000 | 100,000 | 100,000 | |

| Rights issue terms | ||||

| Rights issue size ($) | S | 20,000 | 20,000 | 20,000 |

| Subscription ratio (new shares/old shares) | SR | 1/5 | 1/4 | 1/2 |

| Rights required to subscribe 1 new share (#) | 5 | 4 | 2 | |

| New shares issued (#) | 200 | 250 | 500 | |

| Subscription Price ($) | 100 | 80 | 40 | |

| TERP ($) | 100 | 96 | 80 | |

| Discount to TERP | - | 17% | 50% | |

| Gross discount | - | 20% | 60% | |

| Value of one right at announcement ($) | - | 4 | 20 | |

| Investor's net worth before announcement | ||||

| Shares owned (#) | ns | 100 | 100 | 100 |

| Net worth ($) | 10,000 | 10,000 | 10,000 | |

| Investor's net worth at announcement | ||||

| Value of shareholding ($) | 10,000 | 9,600 | 8,000 | |

| Rights owned (#) | 100 | 100 | 100 | |

| Value of rights owned ($) | - | 400 | 2,000 | |

| Net worth ($) | 10,000 | 10,000 | 10,000 | |

| Delta net worth ($) | - | - | - | |

From Exhibit 16.7 it is also possible to appreciate how the lower value associated with the shareholding as a result of a larger discount to TERP is compensated with a higher value of rights.

Dilution

The only way for an existing shareholder not to be diluted in a rights issue is to fully exercise his/her rights and subscribe for newly issued shares pro-quota. It is easy to show that the amount of cash that the shareholder needs to invest not to be diluted is independent of the discount to TERP and is equal to the portion of total proceeds corresponding to his/her shareholding in the company:

| C | = | cash outlay not to be diluted |

| sh | = | investor's shareholding in percentage terms |

Any shareholder who is not willing to invest an amount of cash equal to C will be diluted as a result of a rights issue. The question is whether the extent of such dilution is impacted by the level of discount to TERP. As a larger discount to TERP results in a higher number of newly issued shares for a given amount of proceeds, one could be inclined to think that the dilution borne by an investor who does not intend to invest any additional cash in the company is higher for increasing levels of discount to TERP. In order to show why this is not the case, the concept of tail swallowing will be introduced.

In a tail swallowing, an existing shareholder decides to finance the purchase of new shares through the sale of rights. In particular, it is possible to compute the maximum number of new shares that can be bought in a cash-neutral transaction as follows:

- NS: new shares that can be bought in a cash-neutral transaction

The shareholding of the investor in percentage terms following the tail swallowing can be computed as:

- SH: investor's shareholding in percentage terms following the tail swallowing

Simple calculations will show that SH is not impacted by the level of discount to TERP and can be computed as the ratio of the value of the investor's shareholding before the rights issue to the expected market cap of the issuer following the rights issue:

Therefore, in terms of dilution, existing shareholders should be theoretically indifferent among the different possible levels of discount to TERP, even when they are not willing to participate in the offering.

Exhibit 16.8 compares the shareholding in percentage terms of an existing shareholder following the tail swallowing for different levels of discount to TERP.

Exhibit 16.8 Discount to TERP and dilution

| case 1 | case 2 | case 3 | ||

| Market cap before rights issue announcement | ||||

| Reference share price ($) | p | 100 | 100 | 100 |

| Outstanding shares (#) | n | 1,000 | 1,000 | 1,000 |

| Market cap ($) | 100,000 | 100,000 | 100,000 | |

| Rights issue terms | ||||

| Rights issue size ($) | S | 20,000 | 20,000 | 20,000 |

| Subscription ratio (new shares/old shares) | SR | 1/5 | 1/4 | 1/2 |

| Rights required to subscribe 1 new share (#) | 5 | 4 | 2 | |

| New shares issued (#) | 200 | 250 | 500 | |

| Subscription price ($) | 100 | 80 | 40 | |

| TERP ($) | 100 | 96 | 80 | |

| Discount to TERP | - | 17% | 50% | |

| Gross discount | - | 20% | 60% | |

| Value of one right at announcement ($) | - | 4 | 20 | |

| Tail swallow for an existing shareholder | ||||

| Shares owned (#) | ns | 100 | 100 | 100 |

| Shareholding at announcement | 10% | 10% | 10% | |

| Rights owned (#) | 100 | 100 | 100 | |

| New shares bought in a cash neutral transaction (#) | - | 4 | 25 | |

| Shares owned after tail swallowing (#) | 100 | 104 | 125 | |

| Shareholding after tail swallowing | 8.33% | 8.33% | 8.33% | |

| Equivalent to | 8.33% | 8.33% | 8.33% | |

In reality, other considerations might come into play and lead shareholders to prefer a higher or lower discount to TERP:

- Lower dilution for those investors who may not be familiar with the concept of tail swallowing (e.g., retail investors) in case of a lower discount

- Reduced execution risk associated with a higher discount

- Lower underwriting fees possibly associated with a higher discount (which reduces the risk borne by the underwriters)

- The possibility to appear stronger than other companies who have gone through the same process in previous years as a result of a lower discount to TERP

16.4 CONCLUSIONS

This chapter was meant to provide a simple explanation regarding the pricing of rights issues, the valuation of preemptive rights, and the implications that the pricing of new shares might have on existing shareholders.

It was shown that setting the subscription price at a discount to the theoretical ex-right price is critical for the successful completion of an offering. The level of the discount should be high enough to be confident that the ex-right price will not go below the subscription price during the subscription period. At the same time, the risk of sending a negative signal to the market by choosing a disproportionately high discount should also be avoided. The main elements to be considered by the issuer to determine the discount are the size of the offering, the market environment, and the levels of discount set in previous rights issues.

One way to estimate the theoretical value of preemptive rights is to do so by assuming that there should be no difference between buying a share by paying the ex-right price or by purchasing rights and paying the subscription price. If this was not the case, arbitrageurs could exploit such difference to lock in a profit and prices would adjust accordingly until the imbalance is eliminated. Among other factors, the time value of rights and low levels of liquidity could cause the price of rights to diverge from their theoretical value.

The level of discount to TERP should not have an impact on the net worth of existing shareholders. As a matter of fact, for a higher discount, the expected reduction in the value of their shareholding should be compensated with a higher value of their preemptive rights. In terms of potential dilution, a shareholder who does not intend to invest his/her own cash to participate in the offering should also be indifferent with respect to the discount level. As a matter of fact, after tail swallowing (i.e., financing the purchase of new shares through the sale of rights), the investor's final shareholding will be diluted but the extent of such dilution will not be affected by the level of discount to TERP. Therefore, the subscription price should be set to guarantee the successful execution of the rights issue, but it should also be theoretically neutral for existing shareholders.

A final remark should be made with respect to the diffusion of rights issues. Countries differ greatly with regards to the options available to perform an equity offering. In some jurisdictions, under certain conditions (e.g., above a certain percentage of the company's share capital), a rights issue becomes mandatory. In other jurisdictions, companies have the possibility to issue shares without granting preemptive rights to existing shareholders. Such differences might at least partially explain why rights issues have been much more common in Europe than in the United States.

____________________