2.2.2.2 Health Insurance

Cutler and Zeckhauser (2000) review a large literature that tends to find a positive correlation between insurance coverage and risk occurrence in health insurance. Conditional on the menu of contracts offered to them, individuals with more health insurance tend to have higher medical spending than individuals with less insurance. This literature provides a nice example of the substantive importance of conditioning on the observable characteristics of the individual that determine the menu of contracts offered to him, as emphasized by Chiappori and Salanie (2000). In particular, since employer offering of health insurance is such a major determinant of coverage, some of the most convincing implementations of the positive correlation test compare health insurance coverage and medical spending among individuals within the same employer, who therefore all face the same option set. Indeed, without such conditioning, one can get the opposite result suggesting that the insured have lower medical spending than the uninsured, driven by the difference in who is offered health insurance.

In the case of health insurance, the potential moral hazard effects are non-negligible. There is compelling evidence—including results from randomized trials (Finkelstein et al., 2011; Newhouse & RAND Corporation, 1996)—that health insurance has a causal effect on medical spending. As a result, the large body of evidence on the “positive correlation” property in health insurance suggests that asymmetric information exists in health insurance, but does not itself provide direct evidence of selection.

The task of trying to separate selection from treatment effects is greatly aided by the availability of variation in the offered contracts that is uncorrelated with demand. Arguably the most compelling evidence of adverse selection in health insurance markets comes from observing “death spirals” brought about by changes in the contract set. For example, Cutler and Reber (1998) examine the response to a change in health insurance pricing at Harvard University that required employees to pay more on the margin for more comprehensive coverage. The introduction of this pricing change was staggered over time across different employees. They document a death spiral dynamic whereby the pricing change produced a decline in enrollment in the more comprehensive plan that was particularly concentrated among lower cost (specifically, younger) employees. This prompted a further price increase in the more comprehensive plan to prevent it from losing money, which in turn prompted further exit by disproportionately younger individuals. More recently, Einav et al. (2010a) implemented the “cost curve” test for selection using data from a large firm and variation across employees within the firm in the relative price they faced for more comprehensive coverage. They estimate a downward sloping marginal cost curve, providing direct evidence of selection distinct from moral hazard.

We conclude that in the market for acute medical insurance in the United States, there seems to be compelling evidence of the presence of adverse selection. The findings in two other health insurance markets—specifically Medigap and long-term care insurance—are more mixed. While there is compelling evidence of private information in these markets, the evidence suggests that the resulting selection is advantageous rather than adverse (Fang et al., 2008; Finkelstein & McGarry, 2006; Oster, Shoulson, Quaid, & Dorsey, 2010).

2.2.2.3 Disability Insurance, Unemployment Insurance, and Worker’s Compensation

In contrast to the study of selection in annuity and health insurance markets there is, to our knowledge, a dearth of work on adverse selection in several settings where there are important social insurance programs including disability insurance, unemployment insurance, and worker’s compensation.11 It would be interesting to test for selection in these markets, although the lack of a robust private market for these risks makes it much more challenging to implement the tests described above. To make progress, one would need to develop tests that—unlike the existing positive correlation or cost curve tests—do not require observing individual choices. In this respect, Hendren’s (2012) development of a method for characterizing the distribution of private information in a market where trade is not observed likely represents an important step forward for empirically based estimates of private information in non-existent or virtually non-existent markets. He develops a method to infer agents’ private information based on subjective probability elicitations which he models as noisy measures of their beliefs. His results provide, among other things, the first evidence of private information about risk type in the disability insurance setting.

2.2.3 Welfare Consequences

The tests for asymmetric information described above are relatively uninformative about the welfare impacts of interventions. Markets that appear to be “more adversely selected” by the positive correlation metric—i.e., in which there are larger differences between the expected costs of the insured and uninsured—are not necessarily ones in which there is a greater welfare cost imposed by that selection. Einav and Finkelstein (2011) provide a graphical illustration of this point. Intuitively, the degree of positive correlation is a statement about the shape of the cost curves in e.g., Figure 3 or 5. However, the welfare cost of adverse selection—i.e., the magnitude of the “deadweight loss triangle” CDE depends not only on the shape of the cost curve but also on that of the demand curve.

This problem has motivated recent empirical work that quantifies the welfare losses from asymmetric information and the potential impact of government policies such as mandates, pricing restrictions, and taxes. Conceptually, one must estimate both the demand and marginal cost curve to pin down the welfare cost of adverse selection. Once these have been estimated, one can identify the efficient allocation and compare it to alternative allocations induced by various government policies.

Abstractly, there are two approaches one can take to recovering the demand and marginal cost curves. The first is to estimate these curves directly without estimating the underlying primitives that generated these curves. It might be usefully called a “plan valuation” approach and is similar in approach to traditional discrete choice demand analysis. Einav et al. (2010a) develop and implement such an approach to estimating the welfare cost of selection. They show that the demand and cost curves shown in the prior figures are sufficient statistics for welfare analysis of equilibrium and non-equilibrium pricing of existing contracts. That is, different underlying primitives (i.e., preferences and private information as summarized by ![]() ) have the same welfare implications if they generate the same demand and cost curves. As a result, the identifying variation used to trace out the demand and cost curves for the “cost curve” test of selection provides the estimates needed to estimate the welfare cost of adverse selection (triangle CDE in Figure 3).

) have the same welfare implications if they generate the same demand and cost curves. As a result, the identifying variation used to trace out the demand and cost curves for the “cost curve” test of selection provides the estimates needed to estimate the welfare cost of adverse selection (triangle CDE in Figure 3).

Einav, Finkelstein, and Cullen’s approach to estimating welfare is attractive for its transparency and its reduced reliance on assumptions about consumer preferences or the nature of their ex-ante information. Moreover, it is relatively straightforward to implement in terms of data requirements. Data on costs and quantities in insurance markets are relatively easy to obtain—as evidenced by the widespread application of the “positive correlation” test which requires both of these data elements. The key additional data requirement is exogenous price variation. While naturally more challenging to obtain, the near-ubiquitous regulation of insurance markets offers many potential opportunities to isolate such variation.

A major limitation of this approach, however, is that the analysis of the welfare cost of adverse selection is limited to the cost associated with inefficient pricing of a fixed (and observed) set of contracts. It does not capture the welfare loss that adverse selection may create by distorting the set of contracts offered, which in many settings could be the primary welfare cost of adverse selection. Intuitively, in order to analyze the welfare effects of introducing contracts not observed in the data, one needs a model of the deeper primitives (![]() ).

).

This limitation partly motivates the second approach that researchers have taken to estimating the welfare costs of selection, which is to directly estimate these primitives and then simulate the welfare cost of alternative policies. For example, Einav et al. (2010c) estimate a model of demand for annuities in which the utility from different annuity contracts depends on underlying consumer primitives (![]() ). Specifically, they examine the semi-compulsory market for annuities in the United Kingdom in which individuals who have saved for retirement through certain tax preferred retirement vehicles are required to annuitize their savings but face a choice over some of the contract features. They focus on the choice of “gaurantee period,” the number of years in which the annuity is guaranteed to pay out even if one has already died. The demand for guarantees depends on both indivdiuals’ unobserved risk type (i.e., survival probability) and unobserved preferences (i.e., for wealth when alive relative to wealth after death). All else equal, longer guarantee periods are more attractive both to individuals who believe they have high mortality and to individuals who have a greater value for wealth after death. Using the model, together with individual-level data on annuity choices and ex-post survival length, they recover the joint distribution of survival types and preferences for wealth after death. Unlike the plan valuation approach, this realized utility approach allows recovery of the underlying consumer primitives (

). Specifically, they examine the semi-compulsory market for annuities in the United Kingdom in which individuals who have saved for retirement through certain tax preferred retirement vehicles are required to annuitize their savings but face a choice over some of the contract features. They focus on the choice of “gaurantee period,” the number of years in which the annuity is guaranteed to pay out even if one has already died. The demand for guarantees depends on both indivdiuals’ unobserved risk type (i.e., survival probability) and unobserved preferences (i.e., for wealth when alive relative to wealth after death). All else equal, longer guarantee periods are more attractive both to individuals who believe they have high mortality and to individuals who have a greater value for wealth after death. Using the model, together with individual-level data on annuity choices and ex-post survival length, they recover the joint distribution of survival types and preferences for wealth after death. Unlike the plan valuation approach, this realized utility approach allows recovery of the underlying consumer primitives (![]() ).

).

Einav, Finkelstein, and Levin (2010b) provide more discussion of these two different approaches and their relative attractions. Broadly speaking, the choice between the realized utility approach and plan valuation approaches involves a standard tradeoff. The realized utility approach requires stronger assumptions about how consumers derive value from insurance, but allows the researcher to use the resulting estimates to (at least in principle) examine counterfactual allocations that are much further from the observed data.12 For instance, papers that model realized utility directly as a function of individual primitives such as risk aversion and beliefs about risk type are able in principle to analyze choice and welfare over contracts that vary over dimensions over which one observes no heterogeneity in the data. The papers by Cardon and Hendel (2001), Cohen and Einav (2007), Einav et al. (2010c), and Einav et al. (2011) are examples in this vein.

The plan valuation approach requires weaker assumptions but commensurately limits the type of analysis one can do. At one extreme, the approach taken by Einav et al. (2010a) recovers the willingness to pay for one health plan over another, but provides no information on the characteristics of the plan determining that valuation. With this approach, inferences about contracts that are not observed in the data are not feasible. Other papers in this literature analyze valuation of contracts as a function of plan and individual characteristics, making it feasible to extrapolate to contracts not observed provided that the model’s assumptions are accurate outside the estimation sample. Examples in this vein include Carlin and Town (2010) and Lustig (2011).

2.2.3.1 Estimates of Welfare Costs of Selection

Relative to the literature discussed earlier that tests for the existence of selection, there has been substantially less empirical work attempting to estimate the welfare costs of selection. The work that has been done to date has focused on the welfare cost of selection in the health insurance market for acute medical expenses or the market for annuities. The empirical estimates of the welfare cost of selection have consistently tended to be a few percent of premia, bounding the potential welfare gains from policy interventions that aim to address selection at relatively low levels. This is true both in the insurance markets for acute medical expenses (see e.g., Cutler & Reber, 1998; Carlin & Town, 2010; Einav et al., 2010a, 2011; Handel, 2011; Lustig, 2011) as well as annuity markets (Einav et al., 2010c). However, as emphasized above and as we return to below, virtually all of these papers have studied only the welfare cost of selection arising from inefficient pricing of a given set of contracts, and have not investigated the potentially much larger welfare losses arising from selection limiting the set of contracts offered or, in the extreme, causing a market to unravel completely.

2.2.3.2 Welfare Consequences of Public Policy Interventions

Beyond estimating the welfare cost of selection, several papers have analyzed the welfare consequences of alternative public policy interventions. A recurring theme of this empirical work is that—as indicated by the stylized model we began with—the welfare consequences of “textbook” public policy interventions are not as straightforward as the simple theory suggests.

For example, recent work on mandatory insurance—perhaps the canonical public policy response to selection—has failed to find welfare improvements from the set of mandates considered (Einav et al., 2010a). Other work has concluded that while the optimal mandate would be welfare improving, it is difficult to determine which mandate would raise welfare with preference heterogeneity and some types of mandates may actually reduce welfare (Einav et al., 2010c).

Another focus of the literature has been on the welfare consequences of regulating the characteristics of consumers that can be used in pricing insurance contracts. Bundorf et al. (2012) emphasize that in the presence of heterogeneity in preferences for coverage that is not perfectly correlated with risk, uniform pricing of contracts across consumers of different risk types cannot induce efficient consumer choice. This creates scope for welfare improvements through characteristic-based pricing, often known as “risk adjustment.” In their empirical application, which uses data on employer-provided health insurance at several firms, they estimate that the welfare gains from feasible risk adjustment turn out to be relatively modest. In a similar spirit, Geruso (2011) empirically explores the potential welfare gains from age-adjusted pricing in a different employer-provided health insurance context. Focusing instead on distributional impacts, Finkelstein, Poterba, and Rothschild (2009b) calibrate a stylized equilibrium screening model of annuities to investigate the impact of banning gender-based pricing in a compulsory annuity market; they find that the redistribution inherent in requiring unisex pricing can be greatly undone by equilibrium adjustment of annuity contracts to the restricted pricing regime.

Other work, focusing once again on health insurance, has examined the implications of pricing restrictions for insurance coverage and government expenditures. Empirical examinations of restrictions on characteristic-based pricing, such as community rating in the small group and non-group health insurance markets have shown that such regulations can reduce coverage among lower risk individuals (e.g., Buchmueller & DiNardo, 2002; Bundorf & Simon, 2006; Simon, 2005). Examining risk adjustment in Medicare Advantage plans, where the government is the insurer, Brown, Duggan, Kuziemko, and Woolston (2011) conclude that more detailed pricing on consumer characteristics can exacerbate, rather than ameliorate, the selection problem as defined with respect to government expenditures. The intuition stems from the fact that the variance of medical spending is increasing with its mean. More detailed risk adjustment—which puts consumers into finer pricing “bins” on the basis of their expected health care costs—results in higher dispersion in the high expected spending bins than in the overall pool, increasing the incentives for an insurer to invest in cream skimming within the finer risk classifications.13

2.2.3.3 Welfare Consequences with Multiple Imperfections

Another interesting vein of this literature has investigated how adverse selection impacts welfare in the presence of other market imperfections. When selection is the only departure from the perfectly competitive neoclassical benchmark, eliminating private information is always welfare improving. This need not be the case when there are multiple frictions. For example, Starc (2011) discusses how, when firms have market power, moving from symmetric information to asymmetric information can improve consumer welfare. Intuitively, when firms have market power, prices are inefficiently high. Adverse selection reduces the incentive for firms to mark up prices because the marginal consumers they lose when they raise prices have lower costs (and thus are higher profits) than the infra-marginal ones that they retain. In a similar spirit, Handel (2011) demonstrates how in the presence of adverse selection, switching costs that reduce consumer response to changes in plan pricing can be welfare increasing by blunting the selection pressures that would otherwise operate.

Measuring the welfare costs of selection is also more complicated in models with additional imperfections. Spinnewijn (2012) shows that calculations based on revealed preference—as in Einav et al. (2010a)—may understate the welfare costs of adverse selection in the presence of frictions such as misperception of risks or adjustment costs. Intuitively, such frictions create a wedge between the revealed demand for insurance via the demand curve and the actual value of insurance. As a result, the demand curve overstates the surplus from insurance for those who buy insurance (because some who purchased do not truly value insurance above cost) and understates it for those who do not (because some who do not purchase should have purchased).

More generally, though the graphical framework developed above assumes perfect competition among insurers, one can generalize the welfare analysis to any other given model of the insurance market as long as one can solve for the equilibrium allocation. Lustig (2011), for example, examines the welfare cost of adverse selection in Medicare Advantage, allowing for imperfect competition on the supply side.

2.2.4 Directions for Future Work

Most of the empirical papers to date on welfare in insurance markets have taken the relatively narrow (albeit practical) approach of focusing on the welfare costs associated with the pricing distortions selection induces in insurance markets. In general, these papers have concluded that, defined in this way, the welfare costs of selection are relatively small. One limitation to this work, discussed above, is that it analyzes adverse selection in the absence of other potential frictions, which can be important for both the sign and magnitude of the welfare costs of selection. In addition, in at least two important respects, the existing work may be missing important potential welfare consequences of selection or of government intervention. These omissions highlight both the challenges and opportunities for further empirical work.

First, most of the existing empirical welfare analysis has abstracted from a potentially more significant welfare cost of selection that could arise from distortions in the set of contracts offered. Selection may result in certain types of coverage not being available, as in the classic Akerlof (1970) unraveling of a market, and the welfare costs of the disappearance of certain contracts is potentially much larger than the welfare costs of pricing distortions of the contracts that do exist. The ability to make empirically based estimates of the welfare cost of selection via selection’s effect on the set of contracts offered remains a very important area for future work.

There are several challenges inherent in any such attempts. One is that although in principle estimates from realized utility models can use the recovered primitives to say something about the welfare consequences of offering contracts not observed in the data, researchers have been (reasonably) wary of using the estimates of such models to say much about contracts that are too far from the observed contracts. Another challenge stems from the supply side task of trying to characterize the counterfactual equilibrium for unobserved contracts; as discussed by Einav et al. (2010b), this can be particularly challenging when allowing for realistic consumer heterogeneity as well as imperfect competition.

Even more challenging is empirical work in markets that have almost or completely unraveled, yet it may be that these markets are precisely where the welfare costs of selection are largest; in other words, the “lamp post problem” of empirical work gravitating to markets for which there are data and dimensions of coverage along which there is observed variation may be one reason that existing papers have found relatively small welfare losses.

A few recent papers have used calibration exercises to try to investigate the value of insurance in markets that are virtually non-existent; examples include the market for annuities (Hosseini, 2010), long-term care insurance (Brown & Finkelstein, 2008), and high deductible health insurance (Mahoney, 2012). Such exercises require that the researchers make assumptions about the population distribution of certain primitives such as risk aversion and risk type, which are often based on estimates made in other, thicker markets. As noted, Hendren (2011) makes important progress in empirically characterizing the distribution of private information in markets where trade does not occur. More work is needed in this area so that researchers may be equipped to examine the counterfactual functioning of private insurance markets that currently do not exist but where we have important social insurance programs such as unemployment insurance, worker’s compensation, and disability insurance.

Second, existing empirical work has focused on testing for the presence of selection and examining its welfare consequences given the existing public policies, such as tax subsidies to employer-provided health insurance or publicly provided annuities through Social Security. This raises the question of whether selection would exist—and what its welfare consequences would be—in the absence of these public programs or under very different public programs than we currently have. Theoretically, it is not clear whether or when government intervention mitigates or exacerbates selection. For example, as discussed earlier, regulatory restrictions on the consumer characteristics insurance companies may use in setting pricing may potentially increase or decrease the welfare costs of selection in the private market. As another example, the impact of mandatory, partial social insurance (such as Medicare which covers some but not all medical expenses or Social Security which provides partial annuitization) on adverse selection in the residual private market for insurance is theoretically ambiguous. Under different assumptions regarding the ability to offer exclusive contracts, Abel (1986) finds that partial public annuities provided by Social Security exacerbates adverse selection pressures in the residual private market while Eckstein, Eichenbaum, and Peled (1985) document a potential welfare enhancing role for partial public annuities. Empirically, we know little about whether the existing partial public insurance programs such as Medicare and Social Security have exacerbated or ameliorated adverse selection problems in the residual private markets for the elderly for health insurance (Medigap) and annuities. Finkelstein (2004) attempts to try to begin to examine such questions empirically. The recent introduction of Medicare Part D, which covers some but not all prescription drug expenses, may provide a fruitful opportunity for empirical work on this question.

2.3 Other Motivations

Following much of the recent literature, we have concentrated our discussion above on asymmetric information as a motive for social insurance.14 This recent focus should not be interpreted as a reflection of a conclusion that selection is the important rationale for social insurance. Here, we briefly summarize several other potential rationales for social insurance. Many of these are ripe for empirical work quantifying their importance.

Incomplete Contracts. Private insurance contracts can only insure risks which are realized after birth, as one cannot write contracts behind the Rawlsian veil of ignorance. Social insurance programs can address this problem by redistributing across individuals born with different endowments (e.g., of skills or health). The ability of social insurance to insure risks realized at or before birth might explain why most developed countries—including the United States in the near future—provide or mandate universal health insurance. Social insurance for risks behind the veil of ignorance is formally analogous to optimal taxation and hence we do not treat it further here; see the chapter by Piketty and Saez in this volume for a review of this literature.

Aggregate Risks. Some risks represent aggregate shocks for which the private insurance market’s ability to diversify the risk cross-sectionally may be impaired. By contrast, the government may be able to spread such risk intergenerationally. This may suggest a welfare-improving role for social insurance against such correlated risks as aggregate unemployment shocks, natural disasters, changes in population life expectancy, or technological change in medicine.

An interesting vein of this literature has investigated why such aggregate shocks cannot instead be effectively diversified—and thus insured—intertemporally through private capital markets. In the context of catastrophe risk (e.g., hurricanes and earthquakes), Froot (2001) discusses a variety of possible demand-side and supply-side explanations for why in practice the role of capital markets in reinsuring these risks appears to be limited and prices appear to be high. He also reviews the available evidence for each hypothesis. Demand-side explanations include agency issues with insurance company managers who do not value protection for policyholders against extremely high losses if the protection does not avoid default by the firm, ex-post intervention by third parties such as the Federal Emergency Management Agency (FEMA) that substitute for insurance, and optimization failures. Supply side explanations include potential market failures such as adverse selection and moral hazard, firm market power, capital market imperfections that restrict the supply of reinsurance, and high transaction costs.

A related set of issues for private insurance concerns aggregate uncertainty. On the supply-side, it may be difficult for would be providers to offer insurance against risks with considerable parameter uncertainty; terrorism risk insurance is an example of where this issue may be important (e.g., Brown, Kroszner, & Jenn, 2002). On the demand-side, aggregate uncertainty may reduce demand for long-term insurance contracts against future risk. For example, Brown and Finkelstein (2011) conjecture that aggregate uncertainty regarding future policy and the survivorship of private insurance companies may depress demand among prime age adults for long-term care insurance that would cover nursing and home health costs in old age.

Externalities. Externalities from insurance constitute another potential rationale for government intervention. One possibility is physical externalities, particularly in the case of health insurance, which subsidizes the treatment or prevention of infectious disease.15 Another is the possibility of fiscal externalities stemming from the Samaritan’s dilemma (Buchanan, 1975). If an altruistic society will provide charitable assistance to those experiencing adverse events ex-post, this can reduce individuals’ incentives to purchase insurance ex-ante. Coate (1995) demonstrates that the optimal transfer policy therefore involves in-kind transfers of insurance to address the inefficient underinsurance that arises in response to unconditional transfers. Ex-post unconditional public transfers are frequently observed in the context of health, natural disasters, and terrorism and thus may deter ex-ante insurance purchases in these markets to some extent. In health insurance, researchers have documented the relationship between charity care and private insurance coverage (e.g., Herring, 2005) and the role of bankruptcy protection in reducing demand for high deductible health insurance (Mahoney, 2012). However, we have little evidence on the overall importance of the Samaritan’s dilemma effects as a motive for social insurance.

Optimization Failures. Another class of motivations for social insurance is a paternalistic motive premised on imperfect optimization in individual insurance purchases. There is considerable evidence that individuals do not adhere to the lifecycle expected utility model underlying traditional models of risk and insurance. For instance, demand for insurance that covers very small risks with high loads—such as toaster warranties, flight insurance, or homeowners insurance deductibles (e.g., Sydnor, 2010)—implies levels of risk aversion that are inconsistent with expected utility theory (Rabin, 2000). Barseghyan, O’Donoghue, and Teitelbaum (2012) argue that this excess demand for low deductibles is explained by misperceptions of loss probabilities. The lack of demand for other types of insurance such as annuities is also difficult to explain in neoclassical models (e.g., Davidoff et al., 2005).

In the context of Medicare Part D—the 2006 addition to the Medicare program that allows individuals to choose a subsidized prescription drug plan—there is also evidence that individuals make suboptimal choices in choosing not just the level but also the characteristics of insurance coverage. Abaluck and Gruber (2011) argue that many individuals choose suboptimal drug insurance plans in the Medicare Part D program given the risks they face. Kling, Mullainathan, Shafir, Vermeulen, and Wrobel (2012) implement a field experiment which suggests that these suboptimal choices in drug insurance plans are due to “comparison frictions”—difficulty for consumers in using available information about plan features to make choices. These are just some examples from a vast literature in psychology and economics that has documented that individuals are prone to various biases such as impatience, loss aversion, overconfidence, and inattention.

The need to account for such biases is especially evident in dynamic models of temporary shocks such as unemployment. As we discuss below, unemployment shocks are quite costly as judged by ex-post measures of consumption smoothing or liquidity effects. Given these costs, rational agents would build up buffer stocks to help cushion temporary shocks (Carroll, 1997; Deaton, 1991). But in practice, most individuals build very limited buffer stocks. The median job loser has less than $200 in liquid assets at the beginning of his unemployment spell (Chetty, 2008).16 Thus, it is difficult to reconcile the ex-post costs of shocks with optimizing behavior even in an environment without any private insurance markets, because self insurance would be adequate to smooth most temporary shocks.17 Indeed, Lucas (1987) calculates that optimizing agents would pay less than 1% of lifetime consumption to entirely eliminate business cycle fluctuations even without any private insurance. Hence, the role for social insurance against temporary shocks is quite limited in optimizing models. This suggests that imperfect optimization must be an important motive for social insurance programs in practice. We briefly discuss recent work on optimal social insurance with agents who do not optimize perfectly in Section 3.3.5.

3 Design of Public Insurance Programs

A large literature has analyzed the optimal government response to the failures in private insurance markets discussed above. The goal of this literature is to find the optimal system in terms of trading off protection against risk with minimizing moral hazard. In practice, this problem has several dimensions. Conditional on deciding to insure a risk such as unemployment, there are several policy choices to be made. What level of benefits should be paid? Should benefits rise or fall over an unemployment spell? Should the insurance plan be financed by taxing firms or workers?

The traditional approach to answering such policy questions is to identify a model’s structural primitives and conduct welfare analysis by simulating alternative policies. In social insurance, Wolpin (1987), Hansen and Imrohoroglu (1992), Wang and Williamson (1996), and Hopenhayn and Nicolini (1997) are influential examples of such work. Lentz (2009) and Huggett and Parra (2010) provide recent state-of-the-art applications. While the structural approach is in principle the ideal method of analyzing policy, in practice it is difficult to fully identify all the primitives of complex dynamic models.

Because of this problem, recent studies have instead tackled the optimal policy problem using a “sufficient statistic” approach, which we focus on here. This approach seeks formulas for optimal policy that are a function of high-level empirically estimable elasticities and are relatively robust to changes in the underlying model of behavior. The advantage of this approach is that it offers results about optimal policy that do not rely on the strong assumptions made in structural studies for tractability and identification. The cost is that it can only be used to analyze marginal changes in policy, e.g., the impact of changing the level of benefits incrementally from its current observed level. See Chetty (2009) for a more detailed discussion of the advantages and disadvantages of the sufficient statistic approach.

Research on social insurance has focused primarily on identifying the optimal level of benefits. We organize our discussion of the optimal level of benefits into three subsections. First, we analyze a static model of insurance in which individuals live for a single period and face one risk. In this static model, it is straightforward to derive an intuitive condition for the optimal level of benefits that trades off the moral hazard costs with the benefits of smaller consumption fluctuations.

Second, we show that this condition for the optimal level of benefits can be written in terms of various empirically estimable parameters. We derive three representations of the formula discussed in recent work: consumption-smoothing benefits, moral hazard vs. liquidity effects, and changes in reservation wages. We discuss empirical evidence on each of these parameters and their implications for the optimal level of benefits.

Third, we analyze the implications of relaxing the assumptions made in the static model. Some of the assumptions are inconsequential. For instance, the formulas obtained from the static model carry over with minor modifications to more realistic dynamic models with endogenous savings, borrowing constraints, and persistent uncertainty. But other extensions to the model—in particular, introducing features such that total private surplus is not maximized by agents’ choices—have significant consequences. For example, if private markets provide insurance that also generates moral hazard, the simple formulas no longer apply because of “multiple dealing” externalities. Similarly, if agents do not maximize their expected utilities because of behavioral failures, the formulas again require modification.

After discussing the literature on the optimal level of benefits, we review recent work on three other aspects of optimal social insurance. First, we discuss work on using mandated savings accounts instead of tax-and-transfer systems to help agents smooth consumption when they face shocks. Next, we discuss imperfect take up of social insurance programs and its implications for optimal policy. Finally, we review recent work on the optimal path of benefits in dynamic models. Unlike the work on the optimal level of benefits, this literature is primarily theoretical. We therefore present brief summaries of some of the key results in this literature and discuss ways in which theory could be connected to data to make further progress on these questions.

Most recent work on connecting theory to data in optimal social insurance has focused on the case of unemployment insurance. Formal models of unemployment translate readily to most other insurance programs such as worker’s compensation, disability, and catastrophic risks. One exception is the analysis of social security. The models we consider below focus on redistribution across states of nature for a given individual. Social security programs do insure against longevity risk by providing annuities, but also have important effects on the path of individuals’ consumption profiles over their lifecycle. As a result, models of optimal social security typically focus on other factors—such as discount rates and wealth accumulation for retirement—independent of risk reduction. We do not consider models of optimal social security design here; see the chapter by Feldstein and Liebman (2002) for a survey of these models. Gruber and Wise (1999) and Krueger and Meyer (2002) summarize the existing evidence on the impacts of social security programs on retirement behavior. Unlike other social insurance programs, the evidence on social security has not been integrated as tightly with theoretical models to make quantitative statements about welfare and optimal policy. We view this as a fertile area for future research and return to this issue in the concluding section.

3.1 Optimal Benefit Level in a Static Model

Setup. The simplest model of insurance is static and has two states, high (![]() ) and low (

) and low (![]() ). These states could reflect the risk of job loss (unemployment insurance), injury at work (Worker’s Compensation), or natural disasters (home insurance). Let

). These states could reflect the risk of job loss (unemployment insurance), injury at work (Worker’s Compensation), or natural disasters (home insurance). Let ![]() denote the individual’s income in the high state and

denote the individual’s income in the high state and ![]() income in the low state. Individuals enter the model with exogenously determined assets

income in the low state. Individuals enter the model with exogenously determined assets ![]() . The government pays a benefit

. The government pays a benefit ![]() in the low state that is financed by an actuarially fair tax

in the low state that is financed by an actuarially fair tax ![]() in the high state. Let

in the high state. Let ![]() denote consumption in the high state and

denote consumption in the high state and ![]() denote consumption in the low state. Let

denote consumption in the low state. Let ![]() denote the agent’s utility as a function of consumption in the high state and

denote the agent’s utility as a function of consumption in the high state and ![]() utility in the low state. This allows for the possibility that utility is state-dependent, e.g., agents may value consumption more when healthy. We assume that both

utility in the low state. This allows for the possibility that utility is state-dependent, e.g., agents may value consumption more when healthy. We assume that both ![]() and

and ![]() are smooth and strictly concave.

are smooth and strictly concave.

A critical feature of the optimal social insurance problem is moral hazard. If individuals’ behaviors were not distorted by the provision of insurance, the planner would achieve the first best by setting ![]() to perfectly smooth marginal utilities,

to perfectly smooth marginal utilities, ![]() . We model moral hazard by assuming that the agent can control the probability of being in the bad state by exerting effort

. We model moral hazard by assuming that the agent can control the probability of being in the bad state by exerting effort ![]() at a cost

at a cost ![]() . For instance, “effort” could reflect spending time to search for a job, taking precautions to avoid injury, or locating a house away from areas prone to natural disasters. We choose units of

. For instance, “effort” could reflect spending time to search for a job, taking precautions to avoid injury, or locating a house away from areas prone to natural disasters. We choose units of ![]() so that the probability of being in the high state is given by

so that the probability of being in the high state is given by ![]() .

.

Agent’s Problem. The agent chooses effort ![]() to maximize his expected utility:

to maximize his expected utility:

![]() (9)

(9)

Importantly, we assume that the agent takes the tax and benefit levels offered by the government (![]() ) as fixed when solving this maximization problem. This assumption is a convenient analytical approximation to capture behavior in an economy with a large number of agents, in which the impact of any single agent’s choice of

) as fixed when solving this maximization problem. This assumption is a convenient analytical approximation to capture behavior in an economy with a large number of agents, in which the impact of any single agent’s choice of ![]() on the tax rate

on the tax rate ![]() is negligible.18 The first-order condition for the maximization problem in (9) is:

is negligible.18 The first-order condition for the maximization problem in (9) is:

![]() (10)

(10)

Intuitively, the level of ![]() that maximizes

that maximizes ![]() equates the marginal benefit of an extra unit of effort, given by the difference in utilities in the low and high states, with the marginal cost of exerting an extra unit of effort. Let

equates the marginal benefit of an extra unit of effort, given by the difference in utilities in the low and high states, with the marginal cost of exerting an extra unit of effort. Let ![]() denote the agent’s optimal choice of effort given a benefit level

denote the agent’s optimal choice of effort given a benefit level ![]() .

.

Planner’s Problem. The social planner’s objective is to choose the benefit level ![]() that maximizes the agent’s expected utility, taking into account the agent’s endogenous choice of effort:

that maximizes the agent’s expected utility, taking into account the agent’s endogenous choice of effort:

![]() (11)

(11)

![]()

Differentiating (11) and using the first-order condition for ![]() in (10) gives

in (10) gives

![]() (12)

(12)

![]()

where ![]() denotes the elasticity of the probability of being in the bad state (which can be measured as the unemployment rate, rate of health insurance claims, etc.) with respect to the benefit level.19 Notice that in this expression, the behavioral response

denotes the elasticity of the probability of being in the bad state (which can be measured as the unemployment rate, rate of health insurance claims, etc.) with respect to the benefit level.19 Notice that in this expression, the behavioral response ![]() enters only via its impact on the government budget constraint

enters only via its impact on the government budget constraint ![]() . The direct impact of changes in

. The direct impact of changes in ![]() on the agent’s private welfare is second order because the agent has already set

on the agent’s private welfare is second order because the agent has already set ![]() at the optimum that maximizes his private welfare (

at the optimum that maximizes his private welfare (![]() ). This envelope condition plays a critical role in generalizing (12) to richer, more realistic models, as we discuss in Section 3.3.1.

). This envelope condition plays a critical role in generalizing (12) to richer, more realistic models, as we discuss in Section 3.3.1.

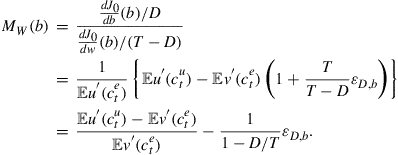

Equation (12) does not have a cardinal interpretation because it is scaled in utils. One natural cardinal metric is to normalize the welfare gain from a $1 (balanced budget) increase in the size of the government insurance program by the welfare gain from raising the wage bill in the high state by $1:

(13)

(13)

The first term in (13) measures the gap in marginal utilities between the high and low states, which quantifies the welfare gain from transferring an additional dollar from the high to low state. The second term measures the net cost to the government of transferring this $1 across states due to behavioral responses. The second term arises because the agent does not internalize the fiscal externality that he imposes on the government budget when changing his level of effort. This creates a wedge between the private return to effort and the social return to effort, generating a welfare loss.

At the optimal benefit level ![]() and hence

and hence

![]() (14)

(14)

This expression is a simple variant of Baily’s (1978) classic formula for the optimal level of social insurance. It captures a simple—and, as we show below, quite robust—intuition about optimal policy: the optimal benefit level equates the marginal gains from a smoother consumption path with the marginal cost, measured by the behavioral response in effort. Note that (14) is a condition that must hold at the optimal benefit level ![]() but is not an explicit formula for the level of benefits because all the parameters in (14) are endogenous to

but is not an explicit formula for the level of benefits because all the parameters in (14) are endogenous to ![]() .

.

Another way to write (14) is in terms of the replacement rate, ![]() :

:

![]() (15)

(15)

where ![]() denotes the elasticity of the probability of being in the bad state with respect to the net wage

denotes the elasticity of the probability of being in the bad state with respect to the net wage ![]() . This formula bears a close resemblance to the inverse elasticity rules that are familiar from the literature on optimal commodity taxation (Auerbach, 1985). Indeed, the optimal social insurance problem is formally identical to an optimal Ramsey taxation problem (Chetty & Saez, 2010).

. This formula bears a close resemblance to the inverse elasticity rules that are familiar from the literature on optimal commodity taxation (Auerbach, 1985). Indeed, the optimal social insurance problem is formally identical to an optimal Ramsey taxation problem (Chetty & Saez, 2010).

It is important to note that Eq. (15) is not an explicit formula for the optimal replacement rate ![]() . The reason is again that the parameters on the right hand side are all functions of

. The reason is again that the parameters on the right hand side are all functions of ![]() . The very purpose of raising

. The very purpose of raising ![]() is to reduce

is to reduce ![]() . Moreover, the elasticity

. Moreover, the elasticity ![]() may also vary with

may also vary with ![]() because of liquidity effects (Chetty, 2008), as we explain below.

because of liquidity effects (Chetty, 2008), as we explain below.

Even in this simple static model, calculating the marginal welfare gain (13) empirically requires some work. The challenge is estimating the gap in marginal utilities ![]() , which requires knowledge of the utility function as well as assets

, which requires knowledge of the utility function as well as assets ![]() and wage rates, which may be unobserved by the econometrician. We now discuss recent approaches to tackling this problem.

and wage rates, which may be unobserved by the econometrician. We now discuss recent approaches to tackling this problem.

3.2 Sufficient Statistics Implementation

The modern literature on social insurance has developed three approaches to recover the marginal utility gap in (13): studying consumption fluctuations (Gruber, 1997), liquidity and substitution effects in effort (Chetty, 2008), and reservation wages (Shimer & Werning, 2007). We present simple derivations of each approach here and review empirical evidence in each context.

3.2.1 Consumption Smoothing

Gruber (1997) implements (13) under the assumption that utility is state independent, i.e., ![]() . We first present Gruber’s approach under this assumption and then show how it can be extended to allow for state-dependent utility. Taking a quadratic approximation to the utility function yields:

. We first present Gruber’s approach under this assumption and then show how it can be extended to allow for state-dependent utility. Taking a quadratic approximation to the utility function yields:

![]() (16)

(16)

where ![]() is the coefficient of relative risk aversion evaluated at

is the coefficient of relative risk aversion evaluated at ![]() and

and ![]() . Plugging this expression into (13), one obtains the following expression for the marginal welfare gain of raising

. Plugging this expression into (13), one obtains the following expression for the marginal welfare gain of raising ![]() :

:

![]()

This equation shows that risk aversion ![]() , the observed consumption drop from the high to low state

, the observed consumption drop from the high to low state ![]() , and the elasticity

, and the elasticity ![]() are together sufficient to calculate the marginal welfare consequences of changing benefits from the current level. It follows that estimating these statistics is adequate to determine whether the current benefit level is too high or low if the welfare function is concave. To go further and calculate the optimal level of benefits, Gruber estimates the relationship between the size of the consumption drop

are together sufficient to calculate the marginal welfare consequences of changing benefits from the current level. It follows that estimating these statistics is adequate to determine whether the current benefit level is too high or low if the welfare function is concave. To go further and calculate the optimal level of benefits, Gruber estimates the relationship between the size of the consumption drop ![]() and the level of benefits

and the level of benefits ![]() . He posits that the effect of benefits on consumption is a linear function of the replacement rate

. He posits that the effect of benefits on consumption is a linear function of the replacement rate ![]() :

:

![]() (17)

(17)

In this specification, ![]() measures the drop in consumption that would occur absent government intervention while

measures the drop in consumption that would occur absent government intervention while ![]() measures the slope of the consumption function with respect to the benefit level. Putting this equation together with (16) and (13) yields the following expression for the marginal welfare gain from increasing the benefit level:

measures the slope of the consumption function with respect to the benefit level. Putting this equation together with (16) and (13) yields the following expression for the marginal welfare gain from increasing the benefit level:

![]() (18)

(18)

Gruber solves for the level of ![]() that sets (18) equal to zero to identify the optimal replacement rate.20 Implementing this formula empirically requires estimates of how consumption fluctuates around shocks as a function of benefit levels (

that sets (18) equal to zero to identify the optimal replacement rate.20 Implementing this formula empirically requires estimates of how consumption fluctuates around shocks as a function of benefit levels (![]() ), the curvature of the utility function

), the curvature of the utility function ![]() , and the elasticity that measures distortions in behavior

, and the elasticity that measures distortions in behavior ![]() . There are now several studies estimating each of these parameters for various social insurance programs; we briefly review some illustrative examples of quasi-experimental studies from this literature here.

. There are now several studies estimating each of these parameters for various social insurance programs; we briefly review some illustrative examples of quasi-experimental studies from this literature here.

Evidence on Consumption Smoothing. An early study by Hamermesh (1982) investigates the impacts of unemployment insurance on consumption using cross-sectional consumption data from the Consumer Expenditure Survey. Because Hamermesh does not have panel data, he cannot study changes in consumption around unemployment shocks. Instead, he compares individuals who are currently unemployed and receiving UI with those who are employed. He finds evidence that the marginal propensity to consume out of UI benefits is significantly higher than out of other sources of income, which he interprets as evidence supporting a consumption-smoothing role of UI.

Cochrane (1991) improves upon the analysis in Hamermesh (1982) by using panel data from the Panel Study of Income Dynamics (PSID). Using panel data, he studies how unemployment shocks affect within-household food consumption fluctuations. This is a significant advance over cross-household comparisons, which are likely to be plagued by omitted variable bias. Cochrane finds that unemployment shocks are imperfectly insured—i.e., ![]() in (17)—implying that there is a potential role for government intervention via unemployment insurance. However, Cochrane does not estimate the extent to which providing insurance through a UI system would affect consumption.21

in (17)—implying that there is a potential role for government intervention via unemployment insurance. However, Cochrane does not estimate the extent to which providing insurance through a UI system would affect consumption.21

Gruber (1997) exploits variation in UI benefit levels that is driven by state law changes to identify ![]() using data on food consumption from the PSID. By controlling flexibly for cross-sectional determinants of the level of UI benefits (such as prior wage rates) and simulating UI benefits based on state laws, Gruber isolates variation in UI benefits that is plausibly orthogonal to other determinants of consumption. Gruber’s point estimates of (17) are

using data on food consumption from the PSID. By controlling flexibly for cross-sectional determinants of the level of UI benefits (such as prior wage rates) and simulating UI benefits based on state laws, Gruber isolates variation in UI benefits that is plausibly orthogonal to other determinants of consumption. Gruber’s point estimates of (17) are ![]() and

and ![]() . These estimates imply that consumption drops on average by 10% given existing UI replacement rates, which are approximately 50% of wages. In the absence of UI, consumption would drop by 24%. Hence, UI plays a significant role in smoothing consumption. However, a 10% increase in UI replacement rates generates only a 2.8% point reduction in the consumption drop. This implies that part of the increase in UI benefits is crowded out by other responses, such as reductions in savings (Engen & Gruber, 2001) and changes in spousal labor supply (Cullen & Gruber, 2000).22

. These estimates imply that consumption drops on average by 10% given existing UI replacement rates, which are approximately 50% of wages. In the absence of UI, consumption would drop by 24%. Hence, UI plays a significant role in smoothing consumption. However, a 10% increase in UI replacement rates generates only a 2.8% point reduction in the consumption drop. This implies that part of the increase in UI benefits is crowded out by other responses, such as reductions in savings (Engen & Gruber, 2001) and changes in spousal labor supply (Cullen & Gruber, 2000).22

Gruber’s approach has since become the benchmark quasi-experimental strategy for analyzing how social insurance affects consumption.23 For instance, Browning and Crossley (2001) implement a similar analysis using data on a broader set of consumption goods from Canada. They find that the average impact of increases in UI benefits on consumption is quite modest, but the impacts are especially large among a subset of households that are likely to be liquidity constrained. Gertler and Gruber (2002) show that severe health shocks have large effects on consumption using panel data from Indonesia and that buffering these shocks by reducing income fluctuations would significantly reduce consumption fluctuations. Bronchetti (2012) implements an approach analogous to Gruber (1997) to the Worker’s Compensation program in the US and again finds evidence that increases in Worker’s Compensation benefits significantly increase consumption levels while individuals are out of work due to injury.

While the evidence that has been accumulated clearly demonstrates that insurance markets are incomplete—i.e., consumption does fall when individuals are hit with shocks—the consumption-smoothing role of social insurance programs is less clear. We can be confident given available evidence that ![]() for at least a subset of households, but we have very imprecise estimates of

for at least a subset of households, but we have very imprecise estimates of ![]() . For instance, the estimates of

. For instance, the estimates of ![]() from Gruber (1997) have a confidence interval spanning

from Gruber (1997) have a confidence interval spanning ![]() . The imprecision and instability of estimates arise from the fact that consumption is very difficult to measure accurately due to noise and recall errors and is typically available for relatively small samples. Obtaining a more precise understanding of the consumption-smoothing benefits of insurance will likely require administrative data on consumption, e.g., from credit-card databases, scanner data, or value-added tax registers.

. The imprecision and instability of estimates arise from the fact that consumption is very difficult to measure accurately due to noise and recall errors and is typically available for relatively small samples. Obtaining a more precise understanding of the consumption-smoothing benefits of insurance will likely require administrative data on consumption, e.g., from credit-card databases, scanner data, or value-added tax registers.

Empirical studies of consumption smoothing have focused on the short-run drop in consumption from employment to unemployment. We show below that this short-run consumption drop is what matters for calculating optimal unemployment benefit levels using (18) irrespective of how consumption evolves after the individual finds a new job. However, it is important to recognize that long-term impacts of temporary shocks on consumption are also significant. von Wachter et al. (2009) show that unemployment shocks due to mass layoffs have large, permanent impacts on earnings. Given that consumption must converge to income in the long run for all workers except the few with substantial wealth before job loss, this result strongly suggests that even temporary unemployment shocks have long-lasting effects. If shocks have persistent impacts on consumption, the optimal insurance policy may not be just to provide benefits while agents are out of work, but rather a wage insurance system that insures long-lasting earnings losses, as proposed e.g., by LaLonde (2007).24 An interesting direction for further work would be to apply the methods reviewed here to analyze optimal wage insurance policies.

Evidence on Distortions in Behavior. The literature on measuring behavioral responses to social insurance programs—the impacts of unemployment insurance on unemployment durations, health insurance on health expenditures, disability insurance on labor force participation rates—has a long tradition that predates the theoretical work on social insurance discussed here. We have much more evidence on the distortions created by insurance programs than their consumption-smoothing benefits because of data availability. For instance, administrative data on unemployment durations must be collected in order to make UI payments, making it much easier to study the impacts of UI on durations than on consumption.

There are many excellent surveys of the literature on how social insurance affects behavior; see e.g., Krueger and Meyer (2002) for a review of work on how UI, DI, and Worker’s Compensation affect labor supply and Cutler and Zeckhauser (2000) or Cutler (2002) for a review on how health insurance affects the demand for medical care. Here, we briefly discuss selected findings from the literature that have been used to inform theoretical calculations of optimal benefit levels using sufficient statistic formulas.

In the context of unemployment, most studies have focused on measuring the impacts of increases in UI benefits on the duration of unemployment. The probability of being laid off could also respond to the level of benefits. The literature has focused less on this issue because UI benefits are typically at least partially experience rated, meaning that firms bear the unemployment insurance cost of laying off workers. In a perfectly experience rated system, changes in the level of benefits do not distort incentives to lay off workers. However, with imperfect experience rating, changes in the level of UI benefits can also affect unemployment rates by distorting firms’ layoff decisions (Blanchard & Tirole, 2008; Feldstein, 1978). While studies such as Topel (1983) and Anderson and Meyer (1993) have documented significant effects of experience rating on firm layoffs, there is relatively little recent work on this issue. Analyzing whether social insurance programs affect the rate at which firms hire and lay off workers using modern quasi-experimental designs is a very promising area for further research.

The modern literature estimating the impact of UI on durations has adopted the hazard model specifications used by Meyer (1990). Meyer estimates semi-parametric models for the hazard of exiting unemployment as a function of UI benefits and other variables using administrative data on the duration of UI claims. He exploits variation in UI benefits coming from differential changes in benefits over time across states, as in Gruber (1997). Meyer finds that higher UI benefits reduce the hazard of exiting unemployment significantly, with an implied elasticity above 0.8 in most specifications.

Subsequent studies have obtained qualitatively similar results using a variety of different data sources. For instance, Lalive, van Ours, and Zweimüller (2006) use a regression-discontinuity design in administrative data from Austria and find that UI benefit increases significantly raise unemployment durations, although to a lesser extent than suggested by Meyer’s estimates. Chetty (2008) estimates elasticities of approximately 0.5 using survey data from the Survey of Income and Program Participation. Landais (2012) replicates Meyer’s analysis using a regression-kink design and estimates smaller elasticities, around 0.3. In general, the literature has settled on a consensus estimate of ![]() for UI and unemployment durations of about 0.5 (Krueger & Meyer, 2002).

for UI and unemployment durations of about 0.5 (Krueger & Meyer, 2002).

Meyer (1990) and Katz and Meyer (1990) document a spike in hazard rates when unemployment benefits expire. This is typically viewed as prima facie evidence that UI distorts search behavior, as it suggests that people time their unemployment exits to coincide with the expiry of social assistance. This spike in unemployment exit hazards in the weeks prior to benefit exhaustion is now a well-established empirical regularity; see Card et al. (2007a) for a review of this literature.

However, Card et al. (2007a) use data from Austria to show that the spike in job finding rates when UI benefits expire is far smaller than the spike in unemployment exit rates. In Austria, as in most other European countries, individuals can stay on the UI system to receive job finding assistance and other benefits even after their benefits expire, but the majority of individuals choose to drop out of the UI system when their benefits end. Most of these individuals, however, remain unemployed even after they leave the UI system. In the US, individuals may choose not to collect their last unemployment check because it is often a small leftover amount, which would create the appearance of a surge in hazard rates in the weeks before benefits expire. Because the margin relevant for calculating the efficiency costs of the UI system are time spent working rather than time spent on the UI system, this evidence suggests that the original sharp spikes documented in the literature likely overstate the degree of moral hazard created by UI. The more general lesson is that it is crucial to measure distortions in real economic choices rather than simply use measures that are well recorded in administrative databases.

Analogous behavioral responses have been documented for other social insurance programs beyond unemployment insurance. Meyer, Viscusi, and Durbin (1995) use differential changes in worker’s compensation benefits across states to show that higher benefit levels induce injured workers to stay out of work longer before returning to work. Gruber (2000) analyzes a disability insurance expansion in Canada that raised benefit levels for individuals in all provinces except Quebec. He finds that this benefit increase significantly reduced labor force participation rates for males ages 45–59, implying an elasticity of the non-participation rate with respect to DI benefits of 0.25. Maestas, Mullen, and Strand (forthcoming) use random variation in assignment to disability insurance examiners to estimate that eligibility for DI reduces labor force participation rates for the marginal entrant to DI by approximately 20% points, with significantly smaller effects for those with more severe impairments. In the context of health insurance, the RAND health insurance experiment (Manning, Newhouse, Duan, Keeler, & Leibowitz, 1987) and Oregon health insurance lotteries (Finkelstein et al., 2011) have demonstrated that increases in consumer cost-sharing significantly reduce health care expenditures.

Evidence on Risk Aversion. Economists have estimated risk aversion using a broad array of techniques. The most direct and widely used method of estimating risk aversion is to assess preferences over gambles. Using empirical estimates of the distribution of risk and an expected utility model with a specific functional form for utility such as constant relative risk aversion, one can back out the value of ![]() implied by individuals’ choices over risky streams of income. Early work in asset pricing inferred risk aversion from portfolio choice and asset returns in standard asset pricing models (e.g., Kocherlakota, 1996; Mehra & Prescott, 1985). More recent work has used responses to hypothetical large-stake gambles (Barsky, Juster, Kimball, & Shapiro, 1997), automobile insurance choices (Cohen & Einav, 2007), risk taking in game shows (Metrick, 1995), and home insurance deductible choices (Sydnor, 2010) to infer risk aversion. There is little consensus on the value of

implied by individuals’ choices over risky streams of income. Early work in asset pricing inferred risk aversion from portfolio choice and asset returns in standard asset pricing models (e.g., Kocherlakota, 1996; Mehra & Prescott, 1985). More recent work has used responses to hypothetical large-stake gambles (Barsky, Juster, Kimball, & Shapiro, 1997), automobile insurance choices (Cohen & Einav, 2007), risk taking in game shows (Metrick, 1995), and home insurance deductible choices (Sydnor, 2010) to infer risk aversion. There is little consensus on the value of ![]() from this literature: the estimates range from 1 to well above 10 in the case of deductible choices and asset prices. One explanation of this discrepancy in estimates is that they reflect the behavior of different subgroups of the population. Barseghyan, Prince, and Teitelbaum (2011) and Einav, Finkelstein, Pascu, and Cullen (forthcoming) test this explanation by examining the risk preferences of the same individuals in different domains of choice, such as health insurance deductibles and 401(k) portfolio allocations. While individuals’ risk preferences are correlated across the domains, there is substantial heterogeneity in estimated risk aversion from each choice.

from this literature: the estimates range from 1 to well above 10 in the case of deductible choices and asset prices. One explanation of this discrepancy in estimates is that they reflect the behavior of different subgroups of the population. Barseghyan, Prince, and Teitelbaum (2011) and Einav, Finkelstein, Pascu, and Cullen (forthcoming) test this explanation by examining the risk preferences of the same individuals in different domains of choice, such as health insurance deductibles and 401(k) portfolio allocations. While individuals’ risk preferences are correlated across the domains, there is substantial heterogeneity in estimated risk aversion from each choice.

All of these estimates of risk aversion are based on ex-ante choices, which requires that individuals’ subjective assessment of risks (e.g., the probability of a large fluctuation in stock prices) and other parameters are consistent with the model assumed by the researcher as well as the maintained assumptions of expected utility theory. Chetty (2006a) proposes a different method of estimating ![]() that does not rely on subjective probabilities. He shows that expected utility models imply a direct connection between the curvature of the utility function over consumption and the impacts of wage changes on labor supply. Intuitively, if the utility function is very curved, individuals should become sated with goods as their income rises, and should choose to work less as their wages rise. The fact that uncompensated wage increases almost always raise labor supply in practice implies an upper bound on the coefficient of relative risk aversion of approximately 1 without any assumptions about the structure of the utility function.25 Because this method of estimating risk aversion uses the same types of ex-post data used to measure

that does not rely on subjective probabilities. He shows that expected utility models imply a direct connection between the curvature of the utility function over consumption and the impacts of wage changes on labor supply. Intuitively, if the utility function is very curved, individuals should become sated with goods as their income rises, and should choose to work less as their wages rise. The fact that uncompensated wage increases almost always raise labor supply in practice implies an upper bound on the coefficient of relative risk aversion of approximately 1 without any assumptions about the structure of the utility function.25 Because this method of estimating risk aversion uses the same types of ex-post data used to measure ![]() and

and ![]() , it offers a more direct estimate of the curvature of utility that matters for evaluating the welfare cost of shocks.26

, it offers a more direct estimate of the curvature of utility that matters for evaluating the welfare cost of shocks.26

Unfortunately, even this ex-post measure of risk aversion varies significantly across contexts. Chetty and Szeidl (2007) develop a theoretical model of risk preferences in which individuals have “consumption commitments”—goods such as housing or fixed service contracts which can only be adjusted by paying fixed transaction costs. In this environment, individuals have amplified risk aversion over moderate-stake shocks because of their commitments. To understand the intuition, consider a two good model in which the agent spends half his income on housing (which can only be adjusted by paying a transaction cost) and half on food (which is freely adjustable). When facing a shock such as temporary job loss that forces them to reduce expenditure by say 10%, most individuals will rationally choose to bear the shock by cutting food consumption by 20% in order to avoid having to move out of their house. This concentrated reduction in food expenditures raises marginal utility sharply, amplifying risk aversion. Chetty and Szeidl confirm this prediction of the model in the PSID data used by Cochrane and Gruber: homeowners who become unemployed do not change housing consumption but cut back on food consumption significantly, while renters (who face lower adjustment costs) diversify the shocks more broadly by reducing consumption of both food and housing. Chetty and Szeidl’s analysis suggests that the value of ![]() relevant for shocks such as unemployment could be as high as

relevant for shocks such as unemployment could be as high as ![]() because of fixed commitments. However, for large shocks such as permanent disability that induce households to abandon commitments, the relevant value of

because of fixed commitments. However, for large shocks such as permanent disability that induce households to abandon commitments, the relevant value of ![]() could be closer to 1.

could be closer to 1.

Because of the tremendous uncertainty about the appropriate value of ![]() , researchers typically report welfare calculations for a range of values of

, researchers typically report welfare calculations for a range of values of ![]() . Gruber implements the formula in (18) using his own estimates of the consumption smoothing response and estimates of

. Gruber implements the formula in (18) using his own estimates of the consumption smoothing response and estimates of ![]() from Meyer (1990). He finds that with a coefficient of relative risk aversion

from Meyer (1990). He finds that with a coefficient of relative risk aversion ![]() , increasing the UI benefit level above the levels observed in his data (roughly 50% of the wage) would lead to substantial welfare losses. Extrapolating out-of-sample based on the assumption that

, increasing the UI benefit level above the levels observed in his data (roughly 50% of the wage) would lead to substantial welfare losses. Extrapolating out-of-sample based on the assumption that ![]() remains constant and the consumption function is given by (17), Gruber shows that it is difficult to justify having a positive level of UI benefits (

remains constant and the consumption function is given by (17), Gruber shows that it is difficult to justify having a positive level of UI benefits (![]() ) with risk aversion

) with risk aversion ![]() given his estimates of the consumption-smoothing benefit of UI. With

given his estimates of the consumption-smoothing benefit of UI. With ![]() , however, the optimal benefit level could be as large as 50%. Bronchetti (2012) presents estimates of the optimal level of Worker’s Compensation benefits based on a range of values for

, however, the optimal benefit level could be as large as 50%. Bronchetti (2012) presents estimates of the optimal level of Worker’s Compensation benefits based on a range of values for ![]() using the formula in (18). She concludes that the optimal level of worker’s compensation benefits is likely to be below the current level of 68%, but her estimates of the optimal replacement rate range from 26% to 61% as risk aversion varies from

using the formula in (18). She concludes that the optimal level of worker’s compensation benefits is likely to be below the current level of 68%, but her estimates of the optimal replacement rate range from 26% to 61% as risk aversion varies from ![]() to

to ![]() . Bound, Cullen, Nichols, and Schmidt (2004) calculate the welfare gains from the current Disability Insurance program under varying degrees of risk aversion taking account of heterogeneity across individuals. Based on simulations of the benefits of DI, they conclude that the optimal level of benefits is likely somewhat lower than current levels, but the optimal level of benefits again is quite sensitive to assumptions about

. Bound, Cullen, Nichols, and Schmidt (2004) calculate the welfare gains from the current Disability Insurance program under varying degrees of risk aversion taking account of heterogeneity across individuals. Based on simulations of the benefits of DI, they conclude that the optimal level of benefits is likely somewhat lower than current levels, but the optimal level of benefits again is quite sensitive to assumptions about ![]() .

.

Estimating risk aversion accurately is particularly important because the size of the consumption drop ![]() is inversely related to