CHAPTER 1

A Primer on Banking, Finance and Financial Instruments

“People still crave explanations even when there is no underlying understanding about what's going on…erratic stock market movements always find a ready explanation in the next day's financial columns: a price rise is attributed to sentiment that ‘pessimism about interest rate increases was exaggerated,’ or to the view that ‘company X had been oversold.’ Of course these explanations are always a posteriori: commentators could offer an equally ready explanation if a stock price had moved the other way.”

—Professor Martin Rees, Our Cosmic Habitat, Phoenix 2003, page 101

This chapter is reference material for newcomers to the market, junior bankers and finance students, or for those that require a refresher course on the core subject matter. The purpose of this primer is to introduce all the essential basics of banking, which is necessary if one is to gain a strategic overview of what banks do, what risk exposures they face and how to manage them properly. We begin with the concept of banking, and follow this with a description of bank cash flows, calculation of return, the risks faced in banking, and organisation and strategy.

Banking is a subset of “finance”. The principles of finance underlay the principles of banking. It would be difficult to become conversant with the principles of banking, and thus be in a position to manage a bank efficiently and effectively to the benefit of all stakeholders, unless one was also familiar with the principles of finance. That said, it is not uncommon to encounter senior executives and non‐executive directors on bank Boards who are perhaps not as au fait with basic principles as they should be. Hence, these basic principles are introduced here and remain the theme of Part I of this book.

AN INTRODUCTION TO BANKING

This extract from Bank Asset and Liability Management (2007)

Interest Rate Benchmarks

A transparent and readily accessible interest rate benchmark is a key ingredient in maintaining market efficiency. Countries that do not benefit from such a benchmark are markedly less liquid as a result.

Possibly the most well‐known interest rate benchmark is the London Interbank Offered Rate or Libor. It is calculated and published daily by ICE.

Wikipedia describes the Libor process as follows:

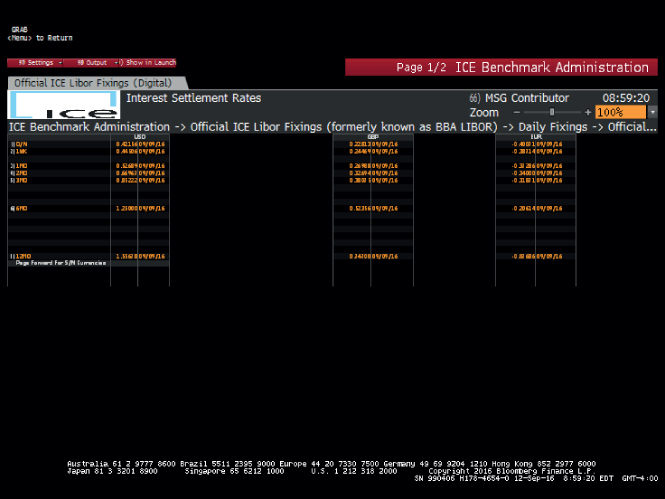

Figure 1.1 shows the Libor rates for 13 September 2016, as seen on the Bloomberg service, for USD, GBP and EUR. We note, for example, that GBP 3‐month Libor was 0.38%. Figure 1.2 shows the history for GBP 3‐month Libor from September 2011 to September 2016.

FIGURE 1.1 Libor screen on Bloomberg, 13 September 2016.

Source: © Bloomberg LP. Used with permission.

FIGURE 1.2 Libor history 2011–2016.

Source: © Bloomberg LP. Used with permission.

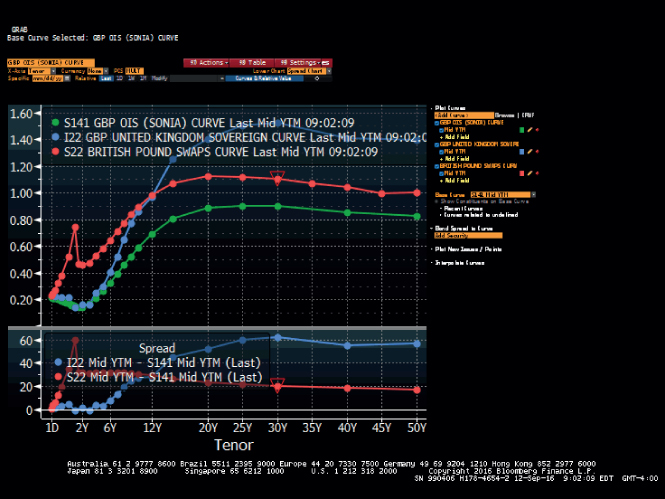

In developed markets, of course, there are usually a range of interest rate indicators. For example, depending on what instrument and market one is concerned with, the sovereign bond interest rates may be worth monitoring, or the overnight index swap (OIS) rate, and so on. It is important to be aware of rates relevant to the balance sheet risk management of your bank, and to understand as well as possible how they interact. Also important is some knowledge of the predictive power of yield curves and how to analyse and interpret them. For illustration, we show the GBP sovereign, interest rate swap, and overnight index swap (SONIA) yield curves for 13 September 2016 at Figure 1.3.

FIGURE 1.3 Sterling curves, 13 September 2016.

Source: © Bloomberg LP. Used with permission.

AN INTRODUCTION TO DEBT FINANCIAL MARKETS

In essence, banks deal in the business of debt, either deposits from customers (banks borrowing from customers), or loans to customers (banks lending to customers). They all “clear” at the end of the day with each other or directly with the central bank.1 Therefore we introduce the debt money markets and debt capital markets in this first chapter.

This extract from The Money Markets Handbook (2004)

This extract from The Money Markets Handbook (2004)

This extract from Fixed Income Markets, Second Edition (2014)

This extract from The Global Repo Markets (2004)

AN INTRODUCTION TO FINANCIAL MARKET PRODUCTS

There is almost, but not quite, infinite variety in financial market products. But more than the 80–20 rule, in finance it is more like the 95–5 rule, whereby 95% of the customer needs of the global financial marketplace can be met with 5% of its product types. We summarise the main “cash” products in Table 1.1. We'll cover derivative instruments and structured finance products in subsequent chapters.

TABLE 1.1 “Cash” Products

| Retail products | Corporate banking products | Wholesale banking products |

| Assets | ||

| Personal loan (unsecured, fixed‐ or floating‐rate) | Corporate loan, unsecured, secured | Money market (CD / CP) |

| Personal loan (secured, fixed‐ or floating‐rate) | Corporate loan, fixed‐ or floating‐rate | Fixed income securities |

| Personal loan, bullet or amortising | Corporate loan, bullet or amortising | Equity market‐making |

| Residential mortgage | Commercial mortgage | |

| Credit card | Credit card | |

| Overdraft | Overdraft | |

| Foreign exchange (spot) | Liquidity line, revolving credit, etc. | |

| Trade Finance (Letter of Credit, Trade Bill, Guarantee, etc.) | ||

| Invoice Discounting, Factoring | ||

| Foreign exchange (spot and forward) | ||

| Liabilities | ||

| Current account | Current account | Structured products (MTNs, etc.) |

| Deposit account | Deposit account | Structured deposit |

| Notice and Fixed‐Term, Fixed‐Rate Deposit accounts | Call account | |

| Call account | Structured deposit |

Commercial Bank Products

Banking is a commoditised product (or service). Most financial products are essentially of long standing and all of them nothing more (or less) than a series of cash flows. Thus to a great extent most of the main products can be obtained (provided the specific customer is acceptable to the bank in question) from most banks. They are summarised in Table 1.1.

Note that “products” does not mean “customer interface”. Hence a mobile banking app for use on Apple or Android is not a “product”. “Contactless” is not a product, although we would suggest that Credit Cards are a product because they are a specific form of bank loan.

From an accounting perspective, the essential distinction to make is whether the product is “on” or “off” balance sheet (or “cash” or “derivative”). However off‐balance sheet products, a term still in common use to describe derivative instruments, are still a package of cash flows. From an asset–liability management (ALM) perspective the distinction between cash and derivative is something of a red herring, because both products give rise to balance sheet risk issues. The ALM practitioner is concerned with cash impact on both sides of the balance sheet, so making a distinction between on‐ and off‐balance‐sheet is to miss the point.

In the ALM discipline, cash and its impact on the balance sheet are everything. So it is important to have an intimate understanding of the cash flow behaviour of every product that the bank deals in. This may seem like a statement of the obvious, but there is no shortage of senior (and not so senior) bankers who are unfamiliar with the product characteristics of some of the instruments on their balance sheet. When we say “understanding” we mean:

- The product's contractual cash flows, their pattern and timing;

- The cash flows' sensitivity (if any) to changes in external and/or relevant market parameters such as interest rates, FX rates, inflation, credit rating, and so on;

- The cash flows' sensitivity to customer behaviour;

- The cash flows' sensitivity to factors impacting the bank itself.

Without this understanding it is not possible to undertake effective NIM management, let alone effective ALM.

This extract from The Principles of Banking (2012)

BANK STRUCTURES AND BUSINESS MODELS

The Role of Banking Institutions in the Global Economy

Although different countries will exhibit different levels of development and sophistication in their individual banking sectors, ultimately all jurisdictions will desire a well‐developed banking system, such that their banks are well‐managed with fit‐for‐purpose risk management systems and good corporate governance. This is because banks play an important role in every economy.

As Agents of Liquidity Banks play a vital role in providing liquidity to the financial system. Their deposit‐taking activities allow them to on‐lend these funds to institutions and individuals, in order to provide liquidity to market operations. Financial intermediaries offer the ability to transform assets into money at relatively low cost. By collecting funds from a large number of small investors, a bank can reduce the cost of their combined investment, offering the individual investor both liquidity and rates of return. Financial intermediaries enable us to diversify our investments and reduce risk. As a last resort in exceptional circumstances, banks also may have access to funding from the country's central bank or “reserve bank”.

To Facilitate Investment by Firms and to Enable Growth and Job Creation Banking institutions play the role of financial intermediaries. These are business entities that bring together providers and users of capital. Banks can act as either agents acting on behalf of clients or they can act as principals conducting financial transactions for their own account. Financial intermediaries develop the facilities and financial instruments which make lending and borrowing possible. They provide the means by which funds can be transferred from surplus units (for example, someone with savings to invest in the economy) to deficit units (for example, someone who wants to borrow money to buy a house).

If lending and borrowing or other financial transactions between unrelated parties takes place without financial intermediation, they are said to be dealing directly.

Banks also provide capital, technical assistance and other facilities which promote trade. They finance agricultural and industrial development and help increase the rate of capital formation. They increase a country's production capabilities by strengthening capital investment.

To Facilitate Local and International Trade Banks make possible the reliable transfer of funds and the transmission of business practices between different countries and different customs all over the world. The global nature of banking also makes possible the distribution of valuable economic and business information among customers and capital markets of all countries. Banking also serves as a worldwide barometer of economic health and business trends. Banks help traders from different countries undertake business opportunities by arranging cross‐border facilities and foreign exchange.

Types of Banks

Banks come in different shapes, sizes, and types. At one end of the spectrum are small specialist or “niche” banks, while at the other end are the global cross‐border banks. Generally, a vanilla bank that offers deposit and loan products to firms and individuals would be a “commercial bank”. We summarise here the different types of institutions.

Traditional Deposit Taking Banks Traditional deposit taking banks are also known as commercial banks or retail banks. Commercial banks provide services such as accepting deposits, providing loans, mortgage lending, and basic investment products like savings accounts and certificates of deposit. Commercial banks are usually public limited companies that are regulated, listed on major stock exchanges, and owned by their shareholders. They may work alongside an associated investment bank in the banking group that can, and will, use the assets (depositors' savings) from the commercial (retail) bank.

Wholesale Funding Operations Wholesale banking involves providing banking services to other banks, medium and large corporate clients, fund managers, and other non‐bank financial institutions. Individual loans and deposits are generally much larger in wholesale than in retail banking. Often banks will fund their wholesale or retail lending by borrowing in financial markets themselves. For a traditional bank, most of its assets will consist of loans and financial securities, such as shares and bonds. These are funded by liabilities, which are mainly customer deposits in most cases, but can also be wholesale funding.

Banks that provide money market services to other banks are known as “clearing” banks or “money centre” banks.

Investment Banking “Investment banking” is the term used to refer to financial market activities such as debt raising and equity financing for corporations, other banks, or governments. This includes originating the securities, underwriting them, and then placing them with investors. In a normal arrangement, a company seeks out an investment bank provider, proposing that it wants to raise a given amount of financing in the form of debt, equity, or hybrid instruments, such as convertible bonds. The bank acts as underwriter for the securities, which are originated to investors along with legal documentation describing the rights of the security holders.

Besides helping companies with new issues of securities, investment banking also involves offering advice to companies on mergers, acquisitions, divestitures, corporate restructurings, and so on. The service also may include assistance in finding merger partners and takeover targets, and also aiding companies in finding buyers for units or subsidiaries which they wish to divest. They also advise a corporation's management which is itself a target for merger or takeover.

Note that what we describe above is not “banking” as such, as it does not involve the bank itself lending money or taking deposits.

Community Banks The broad definition of community banks encompasses membership‐based, decentralised, and self‐help financial institutions. Under this definition fall several variants, such as credit unions and building societies.

Development Banks Development banks are, generically speaking, alternative financial institutions including microfinance institutions, community development institutions, and revolving loan funds. These entities fill a critical role in providing credit through higher risk loans, equity stakes and risk guarantee instruments to private sector initiatives in developing countries. Typically they are supported by states with developed economies. They provide finance to the private sector for investment to promote development and to aid companies in investing, particularly in nations with various market restrictions.

Examples of development banks include the Asian Development Bank and the Islamic Development Bank. The African Development Bank (AfDB) is a regional multilateral development bank that finances development projects in Africa. Financing mainly takes the form of loans to or guaranteed by sovereign institutions, the rest being loans to the private sector and equity participations.

Reserve Bank The role of the central or reserve bank, which is the government bank of the country, is to achieve and maintain price stability in the interests of balanced and sustainable economic growth. Along with other institutions (the public and private sectors) it plays a critical part in helping to ensure financial stability in the country. For example, the Bank of England (BoE) and the South African Reserve Bank (SARB) carry out these missions in their respective countries through the formulation and implementation of inflation targeting and monetary policy. They issue banknotes and coinage, supervise the domestic banking system, and ensure the effective functioning of the national payments system. Their remit extends to managing the official gold and foreign exchange reserves, and they act as banker to the government.

A critical role of the central bank in many countries is as the country's banking supervisory authority, responsible for bank regulation and supervision. The purpose is to achieve a sound, efficient banking system in the interest of the depositors of banks and the economy as a whole. In order to achieve this purpose, a central bank monitors different functions within the banks themselves to help ensure they are run in a sustainable manner. Some of these checks extend to the regular monitoring of the capital requirements of the bank (based on the “Basel” requirements as well as the Internal Capital Adequacy Assessment Process (ICAAP) models), scrutinising of the models used in formulating the risk parameters used within the capital calculations, periodically performing end‐to‐end product level reviews (or reviewing processes within the banks), and performing periodic regulatory checks within the banks to ensure regulatory and prudential compliance.

Activities Carried Out by Banks

Retail Banking Activities Retail banks offer investment and loan products to customers. On the investment side, there are a number of deposit account varieties provided, which could be long‐term savings accounts (for example, fixed deposits) or current accounts with checking facilities. Money market accounts are another type of short‐term investment account. Portfolio cash accounts earn a return from a portfolio of cash and money market investments.

Corporate Banking Activities Today's large banks operate on a global basis and transact business in many different sectors. They are still occupied with the traditional commercial banking activities of taking deposits, making loans, and clearing cheques (both domestically and internationally). They also offer retail customers credit cards, telephone banking, internet banking, and automatic teller machines (ATMs), and provide payroll services to businesses.

Large banks also offer lines of credit to businesses and individual customers. They provide a variety of services to companies exporting goods and services. Companies can enter into a range of contracts with banks which are designed to hedge the risks, relating to foreign exchange, commodity prices, interest rates, and other market variables, they may confront.

Larger banks may conduct research on securities and offer recommendations on individual stocks. They offer brokerage services, as well as trust services where they are willing to manage portfolios of assets for clients. They possess economics departments that consider macroeconomic trends and actions likely to be taken by central banks. These departments deliver forecasts on interest rates, exchange rates, commodity prices, inflation rates, and other variables. Large banks also offer a slate of mutual funds and in some cases have their own hedge funds. Increasingly they also offer insurance products (for example, life insurance).

Investment Banking Activities Valuation, strategy, and tactics pursued represent fundamental aspects of the advisory services offered by investment banks. Banks, and particularly investment banks, often are involved in securities trading, providing brokerage services, and making markets in individual securities. In so doing, they enter into competition with smaller securities firms that are not in a position to offer other banking services.

Brokers intermediate in the trading of securities by taking orders from clients and arranging for them to be fulfilled on an exchange. Some brokers have a national presence, while others may serve only a particular region. So‐called full‐service brokers typically offer investment research and advice. Discount brokers, on the other hand, charge lower commissions, and provide no advice. Frequently, online services are offered. Some, like E‐trade, make available a platform for customers to trade without a broker.

Market‐making involves the quotation of a bid price (the price at which you are prepared to buy) and an offer price (the price at which you are willing to sell). When consulted for a price, a market‐maker also quotes both bid and offer without knowing whether the person asking for the price wishes to buy or sell. Market‐makers make a profit from the spread between bid and offer, but bear the risk that they will be left with an exposure that is unacceptably high.

Trading is very closely related to market‐making. Many large investment and even commercial banks undertake extensive trading activities. Their counterparties are typically other banks, corporations, and fund managers. Banks trade for three primary reasons:

- To meet the needs of counterparties. A bank may sell a currency option to a corporate client to aid in reducing foreign exchange risk, or purchase a credit derivative from a hedge fund to help in following a trading strategy;

- To lower its own risks;

- To take a speculative position in the hope of making a profit. This activity is referred to as trading for its own account or proprietary (“prop”) trading.

Trading activity undertaken by banks is regulated under a different set of regulatory and accounting rules to banking activity.

Financial Statements

Bank Income Statement and Components The majority of a commercial bank's revenues will come from net interest income, representing the positive spread between the gross interest earned on loans and securities, less the cost of funding those loans. Other revenue line items in a bank's income statement will include net fees and commissions, and trading profits. There may also be income from insurance activities and other operating income. This results in a level of pre‐impairment operating income. Each year a certain amount of loan impairment charges will be subtracted from this level, depending on credit loss experience, to result in an operating profit or loss, which is then adjusted for non‐recurring and non‐operating income and expenses. The resultant pre‐tax income has income tax deducted from it, as well as any income from discontinued operations. The bottom line is thus the overall net income of the bank. An example of a typical income statement for a bank (a simplified version) is shown at Figure 1.4.

| Rm | Rm | ||

| Net Interest Income | 14495 | ||

| Gross Interest Income | 21050 | ||

| Less Cost of Funding | −6205 | ||

| Less ISP (Interest Suspended on NPL’s) | −350 | ||

| Impairments (Bad Debt Charge) | −2256 | ||

| Write‐offs | −2105 | ||

| Net Provision Adjustments | −451 | ||

| Post Write‐off Recoveries | 300 | ||

| Income from Lending Activities | 12239 | ||

| Non‐Interest Revenue | 6540 | ||

| Credit Life Insurance Income | 2010 | ||

| Fee Income (Initiation, Admin Fees) | 4530 | ||

| Total Operating Expenses | −11712 | ||

| VAT | −300 | ||

| Profit Before Tax (PBT) | 6767 | ||

| Direct Taxation | −1628 | ||

| Profit After Tax | 5139 |

FIGURE 1.4 Typical income statement for a simple bank.

Bank Balance Sheet and Components By far the majority of a typical bank's assets will be its loan book, which can be subdivided into residential mortgage loans, vehicle asset finance, other consumer loans (unsecured loans, credit cards, overdrafts), and corporate and commercial loans. This gross loan book, or bank book, has a loan loss reserve set against it to cover expected loan losses based on the experience of nonperforming loans (NPLs) historically. Other earning assets will include loans and advances to other banks, trading securities, and derivatives (the trading book), as well as securities, debt, equity, or related, intended to be held to maturity.

Besides these earning assets, banks will possess non‐earning assets such as cash and amounts due from banks, fixed assets and goodwill, or other intangibles.

These assets are balanced by liabilities and equity. For commercial banks, the major liability is customer deposits, and there will also be deposits and cash‐collateralised instruments from other banks. Many banks also have short‐ and long‐term debt issued in the wholesale markets for funding purposes. Also reflected will be liabilities associated with derivatives and the trading book. While the above are interest‐bearing liabilities, there may also be non‐interest bearing liabilities such as tax or insurance liabilities.

On the equity side, in addition to common equity, banks may also have hybrid capital, which possesses features of both debt and equity, and typically qualifies for some regulatory recognition as core capital.

Accounting for Impairments The major impairment a lending bank would typically encounter is that of loan losses, as discussed above. This requires loan loss reserves to be set aside to absorb the expected losses (exactly how this “expectation” is defined will depend on the accounting principles in place in the country in question). In addition, impairments on the value of securities held can also occur in the daily marking‐to‐market process. Fair value accounting is discussed in the following section.

Fair Value Accounting Accountants refer to marking‐to‐market as “fair value accounting”. As explained above, a financial institution is required to mark‐to‐market its trading book on a daily basis. This means it has to estimate a value for each financial instrument in its trading portfolio and then calculate the total value of the portfolio. The valuations are used in value‐at‐risk calculations to determine capital requirements, and by accountants to calculate financial statements.

A number of different approaches are used to calculate the mark‐to‐market price of an asset:

- When there are market‐makers for an asset, or an asset is traded on an exchange, the price of the asset can be based on the most recent quotes.

- When the financial institution itself has traded the asset in the last day, the price of the asset can be based on the price it paid or received.

- When interdealer brokers provide information on the prices at which the asset has been traded by other financial institutions in the over‐the‐counter market, the financial institution can base the price of the asset on this information.

- When interdealer brokers provide price indications (not the prices of actual trades), the financial institution will (in the absence of anything better) base its prices on this information.

- For exotic deals and structured products, the price is usually based on a model developed by the financial institution. Using a model instead of a market price for daily marking‐to‐market is sometimes called marking‐to‐model.

The fair value accounting rules of the International Accounting Standards Board (IASB) require banks to classify instruments as “held for sale” or “held to maturity”. Those “held to maturity” are in the banking book and their values are not changed unless they become impaired. Those “held for sale” are in the trading book and must be marked‐to‐market. Three types of valuation are reported for instruments “held for sale”. Level 1 instruments are those for which there are quoted prices in active markets. Level 2 instruments are those for which there are quoted prices for similar assets in active markets, or quoted prices for the same assets in markets that are not active. Level 3 instruments require some valuation assumptions by the bank.

Types of Capital Held by Banks

Central bank regulators require banks to hold enough capital for the risks that they are bearing. In 1987, international standards were developed to determine this capital, which have evolved since then. The Basel rules assign capital for three types of risk: credit risk, market risk, and operational risk. The total required capital is the capital for credit risk along with the capital for market risk and the capital for operational risk.

We discuss bank regulatory capital in Chapter 8.

Sources of Funds Used to Fund Operations

Deposit Taking The major funding source for most lending banks is deposits made by retail and corporate customers. For banks, this is seen as a low‐cost and relatively reliable source. The arrangement also tends to be low risk for the depositors, given the existence of deposit insurance in most major bank markets. To maintain public confidence in banks, government regulators in many nations have introduced guarantee programmes, which typically insure depositors against losses up to a certain level. After the 1929 US stock market crash, the US government created the Federal Deposit Insurance Company to protect depositors. Banks pay a premium that is a percentage of their domestic deposits and upon failure of a bank, the insurance pays out claims to the depositors that lost funds as a result of the bank failure. In the UK, deposit insurance covers up to £85,000 per depositor.

In countries where deposit insurance has not been implemented by the regulators, it is up to the banks themselves to ensure that they are capitalised to sufficiently reduce the risk of failure.

Wholesale Markets Funding Wholesale funding is a method that banks use in addition to core demand deposits to finance operations and manage risk. Wholesale funding sources include, but are not limited to, reserve bank funds, public funds (such as state and local governments), foreign deposits, and borrowing from institutional investors. While core deposits remain a key liability funding source, some depositary institutions experience difficulty attracting core deposits and increasingly look to wholesale funding to meet loan funding and liquidity management needs.

Wholesale funding providers are generally sensitive to changes in the credit risk profile of the banks to which these funds are provided and to the interest rate environment. For example, such providers closely track the institution's financial condition and are likely to cut back such funding if other investment opportunities offer more attractive interest rates. As a consequence, an institution may experience liquidity problems due to lack of wholesale funding availability when needed. The wide use of short‐term wholesale funding was one of the contributors to many banks' vulnerability during the 2007–2010 financial crisis.

Central Bank Funding Many central banks use a classical cash reserve system as the framework for their monetary policy implementation. An appropriate liquidity requirement is created by levying a cash reserve requirement on banks in the country. The primary refinancing operation is a weekly 7‐day repurchase (repo) auction, which is conducted with commercial banks at the repo rate set by the central bank's Monetary Policy Committee. The reserve bank lends funds to the banks against eligible collateral, comprising assets that also qualify as liquid assets. Besides the main repo facility, many central banks offer a range of end‐of‐day facilities to help commercial banks square off their daily positions, i.e., to access to their cash reserve balances.

Beyond that, open market operations are conducted to manage market liquidity in realisation of monetary policy. These include issuance of debentures, reverse repos, movement of public sector funds, and foreign exchange money market swaps.

Main Types of Financial and Non‐Financial Risk Faced by Banks

Credit Risk The reason for the original 1988 Basel Accord, focusing on credit risk, was a recognition of its primary importance in the risk profile of many financial institutions. At the most basic level, credit risk is simply the risk that, having extended a loan to another party, it is not repaid as agreed. Therefore, techniques can be examined that can be used to assess the probability that third parties default (i.e., fail to repay). These techniques can be applied to individual third parties (known as counterparties) or the industry within which they operate, or even the country within which they are based. This is because the likelihood of a counterparty defaulting is strongly correlated with the success of their industry as well as the economic state of their home country.

Larger counterparties are credit‐rated by firms known as ratings agencies: the higher the rating, the better the credit risk – or to put it another way, the lower the likelihood of default. Smaller firms are not rated by an agency, and so lending institutions have to perform their own assessment of the likelihood of default. This is also true for retail customers.

Another important consideration when assessing credit risk is the quality of any assets which have been used as collateral in the event of default. The higher the quality, the less concerned the lending institution is about default because the underlying security (perhaps the house of one of the borrowing company's directors) can be sold to recoup the loss.

Credit risk is the risk of loss caused by the failure of a counterparty or issuer to meet its obligations. The party that has the financial obligation is called the obligor. The goal of credit risk management is to maximise a firm's risk‐adjusted rates of return by maintaining credit risk exposure within acceptable parameters.

Credit risk exists in two broad forms: counterparty risk and issuer risk. Counterparty risk is the risk that a counterparty fails to fulfil its contractual obligations. A counterparty is one of the parties to a transaction – either the buyer or the seller. Examples of counterparty credit risk from a bank's perspective would include:

- The risk that a customer fails to pay back a loan;

- The risk that a company with whom the bank does business declares bankruptcy before having paid for goods or services supplied by the bank;

- The risk that a broker from whom the bank has purchased a bond fails to deliver – or delivers late;

- In the third of the above examples, the bond itself also carries issuer risk. This is the risk that the issuer of the bond could default on its obligations to pay coupons or repay the principal on the bond.

Concentration risk in credit portfolios arises through an uneven distribution of bank loans to individual issuers or counterparties (single‐name concentration), or within industry sectors and geographical regions (sectorial concentration).

If a bank is overly dependent on a small number of counterparties – single‐name concentration risk – then, if any of those counterparties default, the bank's revenues could drop by a significant amount. Over‐concentration at the country, sector, or industry levels also holds risk for a bank – if, for example, the country in which it is overly concentrated suffers an economic downturn, then its revenues will again be adversely affected compared to competitors who are better diversified.

For most banks, loans are the largest and most obvious source of credit risk. However, other sources of credit risk exist throughout the activities of a bank, including in the banking book and in the trading book, and both on and off the balance sheet. These sources include:

- The extension of commitments and guarantees;

- Inter‐bank transactions;

- Financial instruments such as futures, options, swaps, and bonds;

- The settlement of these and other transactions.

Transaction settlement is a key source of counterparty risk. This is the point at which the buyer and seller exchange the instrument and the cash to pay for it. Here is a risk that one party delivers, but the other fails to do so.

Ideally, the transfer of the purchased item and the transfer of cash would occur at exactly the same time, and there are electronic settlement systems to ensure that this happens. However, this is not always possible – and even when it is, there is always the chance that the mechanism may fail and one party to the agreement is still owed what they are due.

Certain financial instruments also carry “pre‐settlement risk”. This is the risk that an institution defaults before the settlement of the transaction, where the traded instrument has a positive economic value to the other party.

Market Risk Market risk can be subdivided into the following types:

- Volatility risk: the risk of price movements that are more uncertain than usual affecting the pricing of products. All priced instruments suffer from this form of volatility. This especially affects options pricing because if the market is more volatile, then the pricing of an option is more difficult and options will become more expensive.

- Trading liquidity risk: in the context of market risk, this is the risk of loss through not being able to trade in a market or obtain a price on a desired product when required. This can occur in a market due to either a lack of supply or demand or a shortage of market‐makers.

- Currency risk: this exists due to adverse movements in exchange rates. It affects any portfolio or instrument with cash flows denominated in a currency other than the base currency of the business underpinning the financial instrument and/or where an investment portfolio contains holdings in investments priced in non‐base currencies.

- Basis risk: this occurs when one risk exposure is hedged with an offsetting exposure in another instrument that behaves in a similar, but not identical, manner. If the two positions were truly “equal and opposite”, then there would be no risk in the combined position. Basis risk exists to the extent that the two positions do not exactly mirror each other.

- Interest rate risk: this exists due to adverse movements in interest rates and will directly affect fixed‐income securities, loans, futures, options, and forwards. It may also indirectly affect other instruments.

- Equity price risk: the returns from investing in equities comes from capital growth (if the company does well the price of its shares goes up) and income (through the distribution by the company of its profits as dividends). Therefore, investing in equities carries risks that can affect the capital (the share price may fall, or fail to rise in line with inflation, or with the performance of other, less risky investments) and the income (if the company is not as profitable as hoped, the dividends it pays may not keep pace with inflation; indeed they may fall or even not be paid at all. Unlike bond coupons, dividend payments are not compulsory).

As discussed above, there is a link between market risk and a firm's capital adequacy. The ability of a firm to bear market risk is linked to the amount of capital it possesses and the losses it can absorb.

Currency Risk This exists due to adverse movements in exchange rates. It affects any portfolio or instrument with cash flows denominated in a currency other than the base currency of the business. One way that banks attempt to address this risk is through matching of assets, liabilities, and cash inflows, and inflows in the same currency. Where this is not possible, then the usual course of action is to use the wholesale inter‐bank market to hedge the FX mismatch, using forwards and other products. Of course funding mismatch – lending in a currency funded by another currency – cannot be hedged with any real effectiveness, to any practical purpose, and is a significant risk if ever wholesale markets dry up as they did in 2008–2009.

Interest Rate Risk This exists due to adverse movements in interest rates and will directly affect loans, deposits, fixed‐income securities, futures, options, and forwards. It may also indirectly affect other instruments. Interest‐rate risk can be mitigated through hedging using market instruments and through careful matching.

Liquidity Risk The term liquidity is used in various ways, all relating to availability of, or access to, or convertibility into cash. Liquidity risk is discussed in detail in Chapters 11–12.

Operational Risk Operational risks arise from the people, processes, and systems in use within a firm, or from external events. There is very little commonality between people, or processes, or IT systems, or external events (such as bomb threats or power cuts). The techniques used to understand and manage operational risk are therefore very diverse.

In addition to managing expected operational risks, firms also need to hold capital against unexpected losses. Firms can choose between one of three regulatory methods for calculating their operational risk capital requirement. The methods are associated with increasing levels of risk management sophistication, and moving up the levels results in firms having to hold less capital. The three method levels are called:

- The basic indicator approach (BIA);

- The standardised approach (TSA); and

- The advanced measurement approach (AMA).

As well as working out the known risks and holding capital for the unknowns, firms also need to remain vigilant to changes in their risk profile. The two common methods of achieving this are the creation of key risk indicators, and the capture and analysis of loss data.

Firms also have choices to make on how to keep their operational risk exposure within their operational risk appetite. This can be achieved firstly by avoiding the risk altogether, for example, by choosing to withdraw a product which has proved too complex to administer at an acceptable cost without repeated processing errors. A second method for reducing the risk profile to within appetite is to transfer the risk to a third party. This can take several forms including:

- Outsourcing an area of the company, such as back office administration, to another company which specialises in this type of business;

- Taking out insurance against certain events such as fraud or loss of premises through flooding.

As observed above, the simplest approach is to use the basic indicator approach. This sets the operational risk capital equal to the bank's average annual gross income, over the last 3 years, multiplied by 0.15.

Re‐Investment Risk This is the risk that future payments from a bond or a loan will not be reinvested at the prevailing interest rate when the bond was initially bought or the loan extended. Reinvestment risk is more likely when interest rates are declining. It affects the yield‐to‐maturity of a bond or loan, which is calculated on the assumption that all future payments will be reinvested at the interest rate in effect when the bond was first bought or the loan was made. Zero coupon instruments are the only ones to have no reinvestment risk, since they have no interim payments. Two factors that have an effect on the extent of reinvestment risk are:

- The maturity of the instrument: the longer the maturity, the higher the likelihood that interest rates will be lower than they were at the time of investment.

- The interest rate on the bond: the higher the interest rate, the bigger the payments which have to be reinvested, and thus the reinvestment risk.

Pre‐Payment Risk Pre‐payment risk is the risk associated with the early, unscheduled return of principal on an instrument. Some fixed‐income securities, such as mortgage‐backed securities, have embedded call options which may be exercised by the issuer or the borrower.

The yield‐to‐maturity of such instruments cannot be known for certain at the time of investment since the cash flows are not known. When principal is returned early, future interest payments will not be paid on that part of the principal. If a bond were purchased at a premium, the bond's yield will be less than what was estimated at the time of purchase.

This risk also extends to typical retail lending products (for instance, unsecured loans, mortgages, and vehicle finance). This risk is twofold:

- A loan product that is repaid quicker than anticipated within the pricing models will cause the loan to make a smaller profit than anticipated. If the loan is settled particularly quickly, the acquisition costs of writing the loan may not be recovered before it is settled and the loan may actually be loss‐making.

- Where the loan product is a fixed‐rate product, banks will often look to hedge out some of the interest rate risk by purchasing interest rates swaps available to them within the market. The duration of these swaps will be based on the anticipated repayment period of the product. Should the loan product be repaid quicker (or slower) than anticipated, the bank will incur breakage charges on the swaps purchased.

Model Risk Models are approximations of reality. They are needed for determining the price at which an instrument should be traded. They are also needed for marking‐to‐market a financial institution's position in an instrument once it has been traded, as well as for estimating the reserves required on a portfolio of assets (loans).

There are two primary types of model risk. One is the risk that the model will give the wrong price at the time a product is bought or sold. This can result in a company buying a product for too high a price or selling it at too low a price. The other risk involves hedging. If a company does not use the right model, the risk measures it calculates and the hedges it arranges based on those measures, are liable to be wrong (this would include raising reserves to cover loss expectations on the portfolio).

The skill in building a model for a financial product lies in capturing the key features of the product without permitting the model to become so complicated that it is difficult to use.

Country Risk This refers to the risk of investing in a country, which is mainly dependent on changes in the business environment that may adversely affect operating profits or the value of assets in a specific country. For instance, financial factors such as currency controls, devaluation, or regulatory changes, or stability factors such as mass riots, civil war, and other potential events contribute to bank operational risks. This phenomenon is also sometimes referred to as political risk. However, country risk is a more general term that refers only to risks affecting all companies operating within a particular country.

Business Risk As described above, operational risk includes model risk and legal risk, but does not include risk arising from strategic decisions (for example, related to a bank's decision to enter new markets and develop new products), or reputational risk. This type of risk is collectively referred to as business risk. Regulatory capital is not required under Basel II for business risk, but some banks do assess economic capital for business risk.

Counterparty Credit Risk Counterparty risk, also known as a default risk, is a risk that a counterparty will not pay as obliged on a bond, credit derivative, trade credit insurance or payment protection insurance contract, or other trade or transaction. Financial institutions may hedge or take out credit insurance. Offsetting counterparty risk is not always possible, for example, because of temporary liquidity issues or longer‐term systemic reasons. Counterparty risk increases due to positively correlated risk factors. Accounting for correlation among portfolio risk factors and counterparty default in risk management can be challenging.

APPENDIX 1.A: Financial Markets Arithmetic

This extract from An Introduction to Banking (2011)

APPENDIX 1.B: Leadership Lessons From The World of Sport

The following is reproduced from the matchday programme for AFC Wimbledon, published 13 September 2013.

Reproduced from CNBC, AFC Wimbledon

APPENDIX 1.C: The Global Master Repurchase Agreement

To view the GMRA, please go to this website and download the document from the link on this page: http://www.icmagroup.org/Regulatory‐Policy‐and‐Market‐Practice/repo‐and‐collateral‐markets/global‐master‐repurchase‐agreement‐gmra/.

SELECTED BIBLIOGRAPHY AND REFERENCES

- Basel III proposals: www.bis.org/bcbs/basel3.htm.

- Country risk: www.businessmonitor.com/bmo/country‐risk.

- Development banks: www.ft.com/reports/development‐banks‐2012.

- Hull, J. (2010). Risk Management and Financial Institutions, Boston: Pearson, Chapters 2, 11, 14, 18–20.