CHAPTER 3

The Yield Curve

“Raisuli, what shall we do? We have lost everything …”

“Sherif, was there never anything in your life for which it was worth losing everything for?”

—From The Wind and The Lion, MGM Films, Columbia Pictures, 1975.

This is probably the most important chapter in the book. Interest rates and the term structure of rates are the very foundation of modern principles of finance, yet this topic is not one that most senior bank executives are most au fait with. No doubt many of them would suggest that it is not an area they need to be technically expert in, but the fact remains that an understanding of the yield curve is fundamental to an understanding of the principles of finance.

The extracts in this chapter cover every aspect of interest rates, their term structure, spot and forward rates, dynamics of asset prices, fitting the curve, the secured curve, the multicurrency curve – everything but the kitchen sink, as they might say in 1940s Britain.

The new material in this book follows the book extracts, and ties in curve interpolation methodology with issues of relevance for the bank's internal funding or “funds transfer pricing” curve.

This extract from The Principles of Banking (2012)

This extract from Analysing and Interpreting the Yield Curve (2004)

This extract from Analysing and Interpreting the Yield Curve (2004)

CONSTRUCTING THE BANK'S INTERNAL YIELD CURVE1

The construction of an internal yield curve is one of the major steps in the implementation of the internal funds pricing or “funds transfer pricing” (FTP) system in a bank. It should be done after the Trading book and the Banking book are split, but before internal funding methodologies for all balance sheet items and the internal bank result calculation methodology are approved and implemented in the balance sheet management information.

As is pointed out in regulatory recommendations, “the transfer prices should reflect current market conditions as well as the actual institution‐specific circumstances”2. Putting it simply, that means the curve should contain a market component responsible for interest rate risk and a bank‐specific spread over the market which will reflect the term liquidity cost for the bank.

There are several approaches for construction of an FTP curve. The choice of the approach depends on the scale of your bank, as well on the market where the bank operates. These main approaches are:

- Market approach (based on market interest rates): FTP rates reflect the rate of alternative placement of funds or borrowing in the market and change according to market dynamics;

- Cost approach (based on the borrowing rates): FTP rates motivate placement of funds at a higher rate than the rate at which the funds were raised;

- Mixed approach (based on the sum of the interest rate curves): FTP rates take into consideration diversified contents of liabilities at different tenors;

- Marginal approach (based on the price of the following additional asset or liability): FTP rates represent the most relevant pricing levels. This approach can be based on:

- Marginal rates of lending; or

- Marginal rates of borrowing.

We consider each of these approaches in turn. We also show in the Appendix the ALCO submission prepared by one of the authors on implementing an internal curve methodology, when he was working in the investment banking division of a global multinational bank.

MARKET APPROACH FOR FTP CURVE CONSTRUCTION

As implied by the name and definition of the approach, both components of an FTP curve should be derived from market quotes and indicators. The following is a list of requirements defining the characteristics of these market indicators:

- They should reflect accurately market conditions;

- The quotes should be published in well‐known sources and should be available for all market participants (or calculated according to a widely accepted formula);

- Instruments referenced should enable the user to define the spread to the market indicator, in order to obtain the funding cost for the bank.

Usually, as market indicators for FTP curve construction we understand Libor (Euribor, etc.), interest rate swap (IRS), cross‐currency swap (CCS), and credit default swap (CDS). Although as CDS is not available for each bank and sometimes is not representative when it is available, bond yields as market quotes can also be used. An FTP curve based on bond yields can be constructed using several methods which are deeply analysed in the special section. (See Application of Ordinary Least Squares method and Nelson‐Siegel family approaches.)

The market approach can be applied by large banks which have a lot of operations in financial markets. The deep and developed market of financial instruments (including derivatives) is required.

The advantages of this approach are:

- Objectivity and transparency (as a consequence, high level of trust);

- Instant reflection of the level of the market rates;

- Possibility to define FTP rates even for those tenors at which no balance sheet items exist;

- Construction of a smoothed curve without distortions.

Although this method also has limitations:

- Too high volatility of the money market indicators;

- Sometimes lack of market indicators for middle‐term and long‐term;

- Sometimes low volume of deals with government bonds and as a result loss of marketability of quotes;

- Insufficient volume of deals and instruments for representativeness of the results for mathematical modelling.

APPLICATION OF ORDINARY LEAST SQUARES METHOD AND NELSON‐SIEGEL FAMILY APPROACHES

The topic of constructing a yield curve was widely investigated in scientific literature and by practitioners of central banks. The reason for such a deep investigation for these researches was that each country which has government bonds needs to construct a realistic, trustworthy, and flexible zero‐coupon yield curve to reflect the level of the country's debt cost. Such reasons and the grade of responsibility for fair curve construction do not stop debates around the best methods and approaches. However not all approaches are feasible for use in ALM applications.

What are the main criteria for choosing the optimal approach? This approach should be simple enough to be executed without complicated technical packages, but at the same time reflect the market of a particular country, even when bond quotes are not available for all tenors.

According to a Bank for International Settlements survey about zero‐coupon yield curve estimation procedures at central banks (2005), the most commonly used approaches are spline‐based (for example, McCulloch, 1971, 1975) and parametric methods (Nelson, Siegel, 1987 and Svensson, 1994). Although the spline methods gain more positive assessments due to their provision of smoothness and accuracy, they are more complex. At the same time, Nelson and Siegel state in their work that their objective is simplicity rather than accuracy. The following part of this section is devoted to comparison and contrasting of parametric approaches and their practical implementation.

All the parametric methods are based on minimisation of the price / yield errors. Among parametric methods the most basic approach is the Ordinary Least Squares (OLS) method. This is the simplest parametric method which applies calculation of squares of deviations of actual quotes from the calculated approximated values and minimisation of their sum. Formula used to construct the curve is ![]() , where x – duration, f(x) – yield, parameters a, b, and c should satisfy the following: sum of the squares of deviations from the mean should be minimal.

, where x – duration, f(x) – yield, parameters a, b, and c should satisfy the following: sum of the squares of deviations from the mean should be minimal.

The implementation in practice consists of three steps:

- Collecting data from the information sources and placing in Excel spreadsheet (on the graph the bond quotes with different durations would represent a so‐called “starry sky”);

- Calculation of approximations according to the formula with some initial values of parameters a, b, and c, deviations from the actual values, squares of deviations and sum of squares; next through the “Goal Seek” in Excel determination of the most appropriate parameters a, b, and c;

- Solving the equation for some tenor in order to get the yield for this tenor.

The advantages of applying this method for ALM purposes are its simplicity and transparency. However, there are disadvantages which can significantly impact the result. The first and the main one is that the function which is used for approximation is parabolic – and, thus, is increasing in its first half, but after the extremum it starts to decline (see Figure 3.1). It's evident that this is not the best function to describe the market structure of interest rates – at least due to the reason that according to the expectations hypothesis theory, in the long run the rates tend to increase.

FIGURE 3.1 Curve results when employing Nelson‐Siegel and OLS methods

Source: www.micex.ru, Author's calculations.

This method can, though, be used by an ALM unit of a bank in the following cases: a) the market does not have long tenors (so the declining part of the curve won't be used); b) the market yield curve is increasing (that means that it is not inverted and does not have troughs); c) the ALM unit doesn't have resources to try to implement any more complicated method (usually in small banks).

Figure 3.1 shows an example of the difference in output of the N‐S and OLS methodologies when using the same inputs.

In order to make the curve more flexible Nelson‐Siegel family curves are used.

The first approach was suggested by Nelson and Siegel (basic N‐S). They use four parameters in the equation to describe the yield curve:

where

| β0 | is a long‐term interest rate; |

| β1 | represents the spread between short‐term and long‐term rates (this parameter defines the slope of the curve: if parameter is positive, then the slope is negative). |

| β2 | is the difference between the middle‐term and the long‐term rates, defining the hump of the curve (if |

| τ | is a constant parameter, representing the tenor at which the maximum of the hump is achieved. |

The main difference between the basic N‐S approach and the OLS method is the addition of dependence between short‐term and long‐term rates, which tend to make the curve more flexible. This model assumes that long‐term rates directly impact the short‐term rates and, thus, some segments of the curve can't change while other segments are stable. Moreover, this basic approach provides a curve with only one hump or trough. And that is not always true in practice.

Svensson suggested an extension to basic N‐S approach and implemented an additional component to provide a better description of the first part of the curve:

Thus the curve can have two extremums, β3 determines the size and the form of the second hump, τ2 specifies the tenor for the second hump.

The advantages of the Svensson method in comparison to OLS and basic N‐S approaches are even better flexibility and better accuracy. However even two humps do not perfectly reflect the market curve. That is why in practice further adjustments were made.

One of them is the adjusted Nelson‐Siegel (adjusted N‐S) approach with a set of seven parameters. The vector of curve's parameters is recalculated after each new bond / new quote is added. The first four parameters (βs) are responsible for the level of yields on short‐term, middle‐term, and long‐term segments of the yield curve (the shifts up and down), and the remaining three parameters (τs) are responsible for convexity / concavity of the appropriate segments.

Such adjustment provides even more advantages: such flexibility that the yield curve by adjusted N‐S approach can have all types of forms: monotonous increasing, or decreasing, convex, U‐form, or S‐form; memory, because the calculation is based on the previous parameters, so additional data doesn't change the form suddenly. This may be especially useful for markets with low liquidity of some bond issues – when on one day bonds are traded, there's a quote and the bond is included in the calculation, but on another day they are not traded, there's no quote and, thus, there's no input for calculation.

The disadvantage of all types of Nelson‐Siegel approaches is their complexity in comparison with the OLS method. As far as one needs to assign initial values to parameters and then apply the “goal seek” function – there's risk that at this moment a mistake is made and further calculations are incorrect.

Nevertheless, one of the Nelson‐Siegel family approaches would be recommended to be used for ALM purposes in the following cases: a) for larger banks with bigger ALM units, equipped with automatic systems; b) on the markets where the curve is supposed to demonstrate several humps on different tenors; c) on bond markets with low liquidity.

To summarise, not all of the existing methods to construct a yield curve can be successfully applied by ALM units. Parametric approaches are most simple in their implementation. The choice between the most “plain vanilla” OLS method and more complicated Nelson‐Siegel family approaches should be done according to the size of the bank and market conditions and peculiarities.

SONIA YIELD CURVE3

An important reference yield curve today is the overnight index swap (OIS) curve. This is similar to the conventional swap curve except it refers to the overnight rate on the floating leg of the swap, compared to the 3‐month or 6‐month rate on the floating leg of a conventional swap.

Prior to the 2008 crash derivative pricing and valuations were based on the simple principle of the time value of money. A breakeven price was calculated such that when all the future implied cash flows were discounted back to today the Net Present Value of all the cash flows was zero. The breakeven price was used for valuations or spread by a bid–offer price to create a trading price. Bid–offers would generally incorporate a counterparty‐dependent mark‐up to cover various costs and a return on capital in a fairly ill‐defined way.

A breakeven price required the construction of a projection curve for the index being referenced, which could be a tenor of Libor, such as 3‐month, for 3‐month Libor swaps or an overnight rate in the case of overnight index swaps. The projection curve would use market observable inputs and various interpolation methodologies to derive market implied future rates used to project the future floating‐rate fixings. In other words:

- A conventional swap curve is a projection curve based on the 3‐month (or 6‐month) Libor fix; whereas

- An OIS curve is a projection curve based on the overnight rate.

Once the market implied future fixings are known, a discount curve was then used to discount cash flow mismatches in such a way that the breakeven fixed rate gives a result where all the cash flow mismatches have a present value of zero. Historically market practice was to discount cash flows using a Libor discount curve, the assumption being that all cash flow mismatches could be borrowed or reinvested at Libor. It was implicitly assumed that Libor was the risk‐free rate at which these cash flow mismatches could be funded.

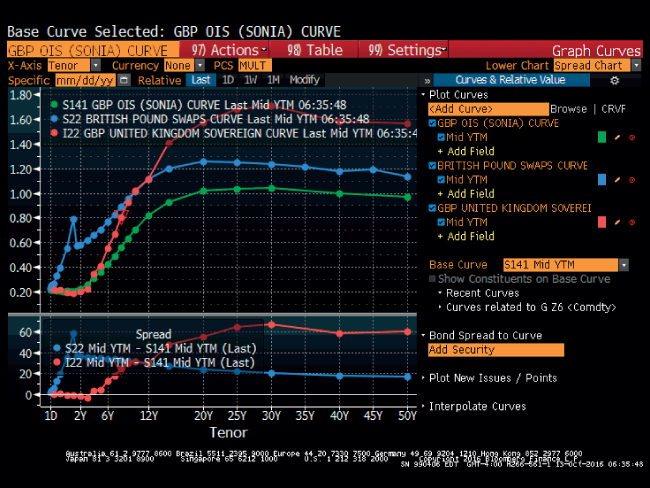

Figure 3.2 shows the GBP OIS (known as SONIA) and GBP swap curves as at 13 October 2016. The OIS curve lies below the conventional swap curve because of the term liquidity premium (TLP) difference between the two tenors (the TLP is higher the longer the tenor).

FIGURE 3.2 GBP SONIA and GBP Swap curves, 13 October 2016

Source: © Bloomberg LP. Reproduced with permission.

In the case of a collateralised trade transacted under the terms of a CSA, the posting of collateral ensures that the NPV of a trade is always zero net of collateral held or posted. All future funding mismatches are therefore explicitly funded directly by the exchange of collateral and as a result do not require any external funding. The collateral remuneration rate is defined by the CSA and is normally the relevant OIS rate. As it is the relevant OIS rate that becomes the applicable rate for funding cash flow mismatches, market practice has evolved to discount future cash flows using OIS rates when pricing or valuing a collateralised trade, so‐called OIS discounting. It is impossible to determine when this market practice changed but it is generally accepted that when the London Clearing House (which clears derivative transactions) changed to OIS discounting in 2010 it was doing so to reflect best market practice.

Where multiple forms of collateral were permissible under a CSA, market practice evolved to take into account the embedded option for the collateral poster. Pricing assumed that a counterparty would always act rationally and post the cheapest to deliver collateral with the discount curve reflecting the relevant collateral OIS rate, so‐called CTD or CSA discounting. A further enhancement is often used where the collateral is non‐cash such as a government bond, in these instances the discount curve reflects the price at which the bonds can be traded in the repo market. For complex CSAs where collateral was multicurrency, the discount curve is often a multicurrency hybrid curve which reflects that the CTD may change at a future date.

For uncollateralised trades, not only was the use of a Libor rate to discount cash flow mismatches clearly inappropriate given the increase in funding spreads during the 2008 crisis but also, in the absence of collateral, the NPV of an uncollateralised trade represented a potential funding requirement. Pricing for uncollateralised trades now generally contains an upfront adjustment to the price to take into account the expected funding costs of non‐collateralisation referred to as the Funding Valuation Adjustment or FVA. FVA along with a Credit Valuation Adjustment CVA now represent a more rigorously defined part of the bid–offer price adjustment.

Collateral posted at the LCH has no optionality allowed – it must be in cash and in the currency of the transaction. Hence the swap screen price now reflects the price for a cleared swap at LCH. Because the collateral is unambiguous (cash in the currency of the trade) remunerated at the relevant OIS, so the discount / funding rate is always known and is not counterparty dependent. Anything other than a LCH cleared trade means the swap price is different to take into account the impact of the type of collateral. This is an important point: observable swap rates are for LCH cleared trades only.

CONCLUSION

The yield curve is the best snapshot of the state of the financial markets. It is not the sole driver of customer prices in banking, but it is the most influential. Hence it is important that all practitioners understand the behaviour of the curve and how to analyse and interpret it. Being aware of the relationship between spot rates, forward rates, and yield to maturity is also important. Ultimately, there should be no short‐cuts when it comes to understanding the yield curve.

APPENDIX 3.A: ALCO Submission Paper

SELECTED BIBLIOGRAPHY AND REFERENCES

- Choudhry, M. (2012), The Principles of Banking, Wiley.

- Ferstl, R., Hayden, J., Zero‐Coupon Yield Curve Estimation with the Package termstrc. https://r‐forge.r‐project.org/scm/viewvc.php/*checkout*/pkg/doc/termstrc.pdf?revision=253&root=termstrc&pathrev=253.

- Guidelines on Liquidity Cost Benefit Allocation, CEBS, October 2010.

- Klein, S. and van Deventer, D. (2009), Yield Curve Smoothing: Nelson‐Siegel versus Spline Technologies, Part 1, Kamakura Corporation Honolulu, 21 July 2009.

- Nelson, Ch. and Siegel, A. “Parsimonious Modeling of Yield Curves”, The Journal of Business, Vol. 60, No. 4, October 1987, pp. 473–489.

- Principles for Sound Liquidity Risk Management and Supervision. BIS, September 2008.

- Zero‐coupon yield curves: technical documentation, BIS Papers, No. 25, Bank for International Settlements, October 2005.