Chapter 6

Tax-Free Exchanges of Property

You may exchange investment or business property for “like-kind” property without incurring a tax in the year of exchange if you meet the rules detailed in this chapter. Gain may be taxed upon a later disposition of the replacement property because the basis of the replacement property is usually the same as the basis of the property surrendered in the exchange. Thus, if you exchange property with a tax basis of $10,000 for property worth $50,000, the basis of the property received in exchange is fixed at $10,000, even though its fair market value is $50,000. The gain of $40,000 ($50,000 – $10,000), which is not taxed at the time of the exchange, is technically called “unrecognized gain.” If you later sell the property for $50,000, you will realize a taxable gain of $40,000 ($50,000 – $10,000).

Where property received in a tax-free exchange is held until death, the unrecognized gain escapes income tax forever because basis of the property in the hands of an heir is generally the value of the property at the date of death. If the exchange involves the transfer of boot, such as cash or other property, gain on the exchange is taxable to the extent of the value of boot.

You may not make a tax-free exchange of U.S. real estate for foreign real estate.

Tax-free exchanges between related parties may become taxable if either party disposes of the exchanged property within a two-year period.

6.1 Trades of Like-Kind Property

You may not have to pay tax on gain realized on the “like-kind” exchange of business or investment property (Code Section 1031). By making a qualifying exchange, you can defer the gain. On the other hand, a loss is not deductible unless you give up “unlike” property (not like-kind); see below. For tax-free gain treatment, you must trade property held for business use or investment for like-kind business or investment property. If the properties are not simultaneously exchanged, the time limits for deferred exchanges (6.4) must be satisfied. The entire gain is deferred only if you do not receive any “boot”; gain is taxed to the extent of boot received (6.3). Where gain on a qualifying exchange is deferred and not immediately taxed, it may be taxable in a later year when you sell the property because your basis for the new property (called “replacement property”) is generally the same as the basis for the property you traded (called “relinquished property”) (5.16 – 5.20).

If you make a qualifying like-kind exchange with certain related parties, tax-free treatment may be lost unless both of you keep the exchanged properties for at least two years (6.6).

The term like-kind refers to the nature or character of the property, that is, whether real estate is traded for real estate. It does not refer to grade or quality, that is, whether the properties traded are new or used, improved or unimproved. In the case of real estate, land may be traded for a building, farm land for city lots, or a leasehold interest of 30 years or more for an outright ownership in realty. Trades of personal property are discussed in 6.2.

Personal use safe harbor for rental residence. An IRS safe harbor (Revenue Procedure 2008-16) allows rental real estate used occasionally as a vacation home to be treated as investment property so that it can be exchanged without endangering tax-deferred treatment.

To qualify, the relinquished residence has to be owned for at least 24 months immediately before the exchange, and, in each of the two 12-month periods immediately preceding the exchange, the residence must be rented at a fair rental for at least 14 days and personal use by the owner and his or her relatives cannot exceed the greater of 14 days or 10% of the days for which the residence is rented at a fair rental in the 12-month period.

Parallel requirements apply to the replacement residence. The replacement residence must be owned for at least 24 months after the exchange and, within each of the two 12-month periods following the exchange, it must be rented at a fair rental for 14 days or more and the taxpayer’s personal use (including use by relatives) cannot exceed the greater of 14 days or 10% of the fair rental days during the 12-month period.

If a taxpayer expects to meet the fair rental and personal use tests for the replacement residence and based on that expectation reports the exchange on his or her return as a tax-deferred exchange, but it turns out that the tests are not met, an amended return must be filed to report the exchange as a taxable sale.

Losses. If a loss is incurred on a like-kind exchange, the loss is not deductible, whether you receive only like-kind property or “unlike” property together with like-kind property. However, a deductible loss may be incurred if you give up unlike property as part of the exchange; the loss equals any excess of the adjusted basis of the unlike property over its fair market value.

Reporting an exchange. You must file Form 8824 to report an exchange of like-kind property. If you figure a recognized gain on Form 8824, you also must report the gain on Schedule D (investment property) or on Form 4797 (business property).

If in addition to the like-kind property you gave up “unlike” property (other than cash), you figure the gain or loss on the unlike property on Lines 12-14 of Form 8824 and report it as if it were from a regular sale. If the fair market value of the unlike property exceeds its adjusted basis, the gain should be reported on Form 8949 and Schedule D (if investment property) or Form 4797 (business property). If the adjusted basis of the unlike property exceeds its fair market value, the loss is deductible on Form 8949/Schedule D or Form 4797 as if the exchange were a regular sale.

If your exchange is with a related party (6.6), Form 8824 must be filed not only for the year of the exchange but also for the two years following the year of the exchange.

Property not within the tax-free trade rules:

- Property used for personal purposes (but exchanges of principal residences may qualify as tax free under different rules; see Chapter 29)

- Foreign real estate

- Property held for sale

- Inventory or stock-in-trade

- Securities

- Notes

- Partnership interest; see below

See also 31.3 for tax-free exchanges of realty and 6.12 for tax-free exchanges of insurance policies.

Exchange of partnership interests. Exchanges of partnership interests in different partnerships are not within the tax-free exchange rules. Under IRS regulations, tax-free exchange treatment is denied regardless of whether the interests are in the same or different partnerships.

If you made an election to exclude a partnership interest from the application of partnership rules, your interest is treated as interest in each partnership asset, not as an interest in the partnership.

Real estate or personal property in foreign countries. You may not make a tax-free exchange of U.S. real estate for foreign real estate; by law they are not considered like-kind property. However, if your real estate is condemned, foreign and U.S. real estate are treated as like-kind property for purposes of making a tax-free reinvestment (18.23).

You may not make tax-free exchanges of personal property used predominantly in the U.S. for personal property used predominantly outside the U.S.

6.2 Personal Property Held for Business or Investment

Gain on an exchange of depreciable tangible personal property held for productive business or investment use is not taxed if the properties meet either the general like-kind test (6.1) or a more specific “like-class” test created by IRS regulations. The assumption of liabilities is treated as “boot” (6.3). Where each party assumes a liability of the other party, the respective liabilities are offset against each other to figure boot, if any.

Under the like-class test, there are two types of “like” classes: (1) General Asset Classes and (2) Product Classes. The like-class test is satisfied if the exchanged properties are both within the same General Asset Class or the same Product Class. A specific asset may be classified within only one class. Thus, if an asset is within an Asset Class, it is not within a Product Class. The Asset Class or Product Class is determined as of the date of the exchange. This limitation may disqualify an exchange when exchanged assets do not fit within the same Asset Class and are not allowed to qualify within the Product Class; see the Brown Example below.

General Asset Classes. There are 13 classes of depreciable tangible business property. Here are some of the asset classifications: office furniture, fixtures, and equipment (class 00.11); information systems: computers and peripheral equipment (class 00.12); data handling equipment, except computers (class 00.13); airplanes and helicopters, except for airplanes used to carry passengers or freight (class 00.21); automobiles and taxis (class 00.22); light trucks (class 00.241); heavy trucks (class 00.242); and over-the-road tractor units (class 00.26). For example, trades of trucks in class 00.241 would be of like class.

Even if exchanged properties are in different General Asset Classes (and thus are not of “like class”), they can be of like kind, so that gain on the exchange is not immediately taxed under the like-kind exchange rules (6.1). For example, the IRS in a private ruling held that although an SUV and an automobile are in different asset classes, the differences between them are merely in grade or quality and do not rise to the level of a difference in nature or character. They are therefore of like kind and gain on the exchange is not taxed.

Product Classes. The IRS uses the North American Industry Classification System (NAICS) for determining product classes of depreciable tangible personal property. A product class is assigned a six-digit NAICS code.

Intangible personal property and goodwill. Exchanges of intangible personal property (such as a patent or copyright) or nondepreciable personal property must meet the general like-kind test to qualify for tax-free treatment; the like-class tests do not apply. However, regulations close the door for qualifying exchanges of goodwill in an exchange of going businesses. According to the regulations, goodwill or going concern value of one business can never be of a like kind to goodwill or going concern value of another business.

Exchanges of multiple properties. Generally, exchanges of assets are considered on a one-to-one basis. Regulations provide an exception for exchanges of multiple properties, such as an exchange of businesses. Transferred assets are separated into exchange groups. An exchange group consists of all properties transferred and received in the exchange that are of a like kind or like class. All properties within the same General Asset Class or same Product Class are in the same exchange group. For example, automobiles and computers are exchanged for other automobiles and computers; two exchange groups are set up—one for the automobiles and the other for the computers. If the aggregate fair market values of the properties transferred and received in each exchange group are not equal, the regulations provide calculations for setting up a residual group for purposes of calculating taxable gain, if any.

All liabilities of which a taxpayer is relieved in the exchange are offset against all liabilities assumed by the taxpayer in the exchange, regardless of whether the liabilities are recourse, nonrecourse, or are secured by the specific property transferred or received. If excess liabilities are assumed by the taxpayer as part of the exchange, regulations provide rules for allocating the excess among the properties.

6.3 Receipt of Cash and Other Property—“Boot”

If, in addition to like-kind (6.1) property, you receive cash or other property (unlike kind), gain is taxable up to the amount of the cash and the fair market value of any unlike property received. The additional cash or unlike property is called “boot.” If a loss was incurred on the exchange, the receipt of boot does not permit you to deduct the loss unless it is attributable to unlike-kind property you gave up in the exchange.

Assumption of mortgages. If you transfer mortgaged property and the other party assumes the mortgage, the amount of the assumed mortgage is part of your boot, as if you had received cash equal to the liability. If both you and the other party assume mortgages on the exchanged properties, the party giving up the larger debt treats the excess as taxable boot. The party giving up the smaller debt does not have boot; see also 31.3. If you pay cash to the other party, or give up unlike-kind property, add this to the mortgage you assume in figuring which party has given up the larger debt.

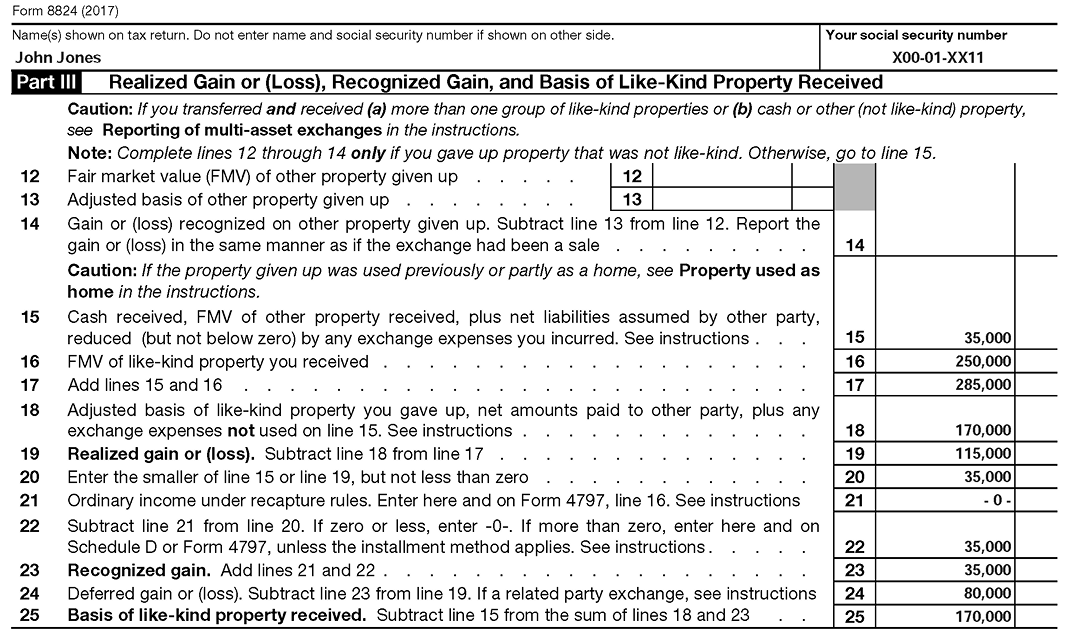

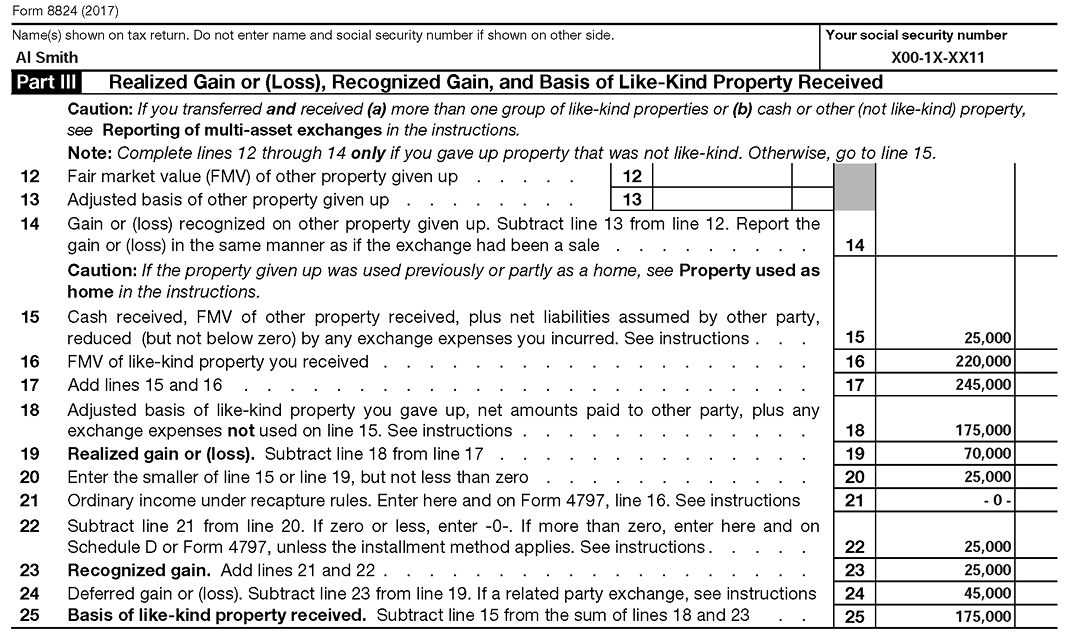

Form 8824. The computation of boot, gain (or loss), and basis of the property received is made on Form 8824. Form 8824 must be filed for the year in which you transfer like-kind property. If the other party to the exchange is related to you, Form 8824 must also be filed for each of the two years following your transfer (6.6).

Sample Form 8824 for Jones ( see the Example beginning on the next page)

Sample Form 8824 for Smith ( see the Example beginning on the next page)

6.4 Time Limits and Security Arrangements for Deferred Exchanges

Assume you own property that has appreciated in value. You want to sell it and reinvest the proceeds in other property, but you would like to avoid having to pay tax on the appreciation. You can defer the tax on the gain if you are able to arrange an exchange for like-kind (6.1) property.

The problem is that it may be difficult to find a buyer who has property you want in exchange, and the time for closing the exchange is restricted. If IRS tests are met, intermediaries and security arrangements may be used without running afoul of constructive receipt rules that could trigger an immediate tax.

Deferred exchange distinguished from a reverse exchange. A deferred exchange is one in which you first transfer investment or business property and then later receive like-kind investment or business property (6.1). If before you receive the replacement property you actually or constructively receive money or unlike property as full payment for the property you have transferred, the transaction will be treated as a sale rather than a deferred exchange. In that case, you must recognize gain (or loss) on the transaction even if you later receive like-kind replacement property. In determining whether you have received money or unlike property, you may take advantage of certain safe harbor security arrangements that allow you to ensure that the replacement property will be provided to you without jeopardizing like-kind exchange treatment; see below for the safe harbor security tests.

A reverse exchange is one in which you acquire replacement property before you transfer the relinquished property. The like-kind exchange rules generally do not apply to reverse exchanges. However, the IRS has provided safe harbor rules that allow like-kind exchange treatment to be obtained if either the replacement property or the relinquished property is held in a qualified exchange accommodation arrangement (QEAA) (6.5).

Time limits for completing deferred exchanges. You enerally have up to 180 days to complete an exchange, but the period may be shorter. Specifically, property will not be treated as like-kind property if received (1) more than 180 days after the date you transferred the property you are relinquishing or (2) after the due date of your return (including extensions) for the year in which you made the transfer, whichever is earlier. Furthermore, the property to be received must be identified within 45 days after the date on which you transferred property.

If the transaction involves more than one property, the 45-day identification period and the 180-day exchange period are determined by the earliest date on which any property is transferred. When the identification or exchange period ends on a Saturday, Sunday, or legal holiday, the deadline is not advanced to the next business day (as it is when the deadline for filing a tax return is on a weekend or holiday).

How to identify replacement property. You must identify replacement property in a written document signed by you and delivered before the end of the 45-day identification period to the person handling the transfer of the replacement property or to any other person involved in the exchange other than yourself or a related party. The identification may also be made in a written agreement. The property must be unambiguously described by a legal description or street address.

You may identify more than one property as replacement property. However, the maximum number of replacement properties that you may identify without regard to the fair market value is three properties. You may identify any number of properties provided the aggregate fair market value at the end of the 45-day identification period does not exceed 200% of the aggregate fair market value of all the relinquished properties as of the date you transferred them. If, as of the end of the identification period, you have identified more than the allowable number of properties, you are generally treated as if no replacement property has been identified.

If property is valued at no more than 15% of the total value of a larger item of property that it is transferred with, the smaller property is considered “incidental” and does not have to be separately identified.

Avoiding constructive receipt. In a deferred exchange, you want financial security for the buyer’s performance and compensation for delay in receiving property. To avoid immediate tax, you must not make a security arrangement that gives you an unrestricted right to funds before the deal is closed. As discussed next, certain safe harbor security arrangements may be used without endangering like-kind exchange treatment.

Safe harbor tests for deferred exchange security arrangements. If one of the following safe harbors applies to your security arrangement, you are not treated by the IRS as having actually or constructively received cash or unlike property prior to receiving the like-kind replacement, so tax-deferred exchange treatment may be obtained.

The first two “safe harbors” cover escrow accounts, mortgages and other security arrangements with your transferee. The third allows the use of professional intermediaries who, for a fee, arrange the details of the deferred exchange. The fourth allows you to earn interest on an escrow account.

- The transferee may give you a mortgage, deed of trust, or other security interest in property (other than cash or a cash equivalent), or a third-party guarantee. A standby letter of credit may be given if you are not allowed to draw on such standby letter except upon a default of the transferee’s obligation to transfer like-kind replacement property.

- The transferee may put cash or a cash equivalent in a qualified escrow account or a qualified trust. The escrow holder or trustee must not be related to you. Your rights to receive, pledge, borrow, or otherwise obtain the cash must be limited. For example, you may obtain the cash after all of the replacement property to which you are entitled is received. After you identify replacement property, you may obtain the cash after the later of (1) the end of the identification period and (2) the occurrence of a contingency beyond your control that you have specified in writing. You may receive the funds after the end of the identification period if within that period you do not identify replacement property. In other cases, there can be no right to the funds until the exchange period ends.

- You may use a qualified intermediary if your right to receive money or other property is limited (as discussed in safe harbor rule 2, above). A qualified intermediary (QI) is an unrelated party who, for a fee, acts to facilitate a deferred exchange by entering into an agreement with you for the exchange of properties pursuant to which the intermediary acquires your property from you and transfers it, acquires the replacement property, and transfers the replacement property to you. Typically, the QI transfers your property to the buyer in exchange for cash and uses the cash to purchase the replacement property that will be transferred to you.

There are restrictions on who may act as an intermediary. You may not employ any person as an intermediary who is your employee or is related to you or your agent or has generally acted as your professional adviser, such as an attorney, accountant, investment broker, real estate agent, or banker, in a two-year period preceding the exchange. Related parties include family members and controlled businesses or trusts (5.6), except that for purposes of control, a 10% interest is sufficient under the intermediary rule. The performance of routine financial, escrow, trust, or title insurance services by a financial institution or title company within the two-year period is not taken into account. State laws that may be interpreted as fixing an agency relationship between the transferor and transferee or fixing the transferor’s right to security funds are ignored.

In a simultaneous exchange, the intermediary is not considered the transferor’s agent.

- You are permitted to receive interest or a “growth factor” on escrowed funds if your right to receive the amount is limited as discussed under safe harbor rule 2.

Escrow account earnings are generally exempt from imputed interest rules. Under final IRS regulations, it is possible for a taxpayer who has an escrow arrangement with a qualified intermediary to be taxed on imputed interest, but there is a $2 million exemption that is expected to apply to the majority of exchange arrangements with small business exchange facilitators. Under the regulations, when a qualified intermediary holds exchange funds (cash, cash equivalents, or relinquished property) in escrow for a taxpayer under a deferred exchange agreement prior to the acquisition of replacement property, the exchange funds are treated as a loan from the taxpayer to the qualified intermediary unless the agreement provides that all of the earnings (such as bank interest) on the exchange funds will be paid to the taxpayer.

However, even when the intermediary retains the escrow earnings, as is typically the case with small nonbank exchange facilitators, the imputed interest rules do not apply if the deemed loan does not exceed $2 million and the loan does not extend beyond six months. If the loan exceeds $2 million or lasts more than six months, the taxpayer must report imputed interest. For example, a taxpayer transfers property to a qualified intermediary who transfers it to a purchaser in exchange for $2.1 million cash, which the intermediary deposits in a money market account for three months until the intermediary withdraws the funds and purchases replacement property identified by the taxpayer. Assuming that the taxpayer is not entitled to the earnings under the exchange agreement, the taxpayer is treated as having made a $2.1 million loan to the intermediary. The amount of the imputed interest taxable to the taxpayer is based on the lower of (1) the short-term applicable federal rate in effect on the day the deemed loan was made, compounded semiannually, or (2) the rate on a 91-day Treasury bill issued on or before the date of the deemed loan. The IRS could increase the $2 million exempt amount in future guidance.

6.5 Qualified Exchange Accommodation Arrangements (QEAAs) for Reverse Exchanges

The like-kind exchange rules (6.1) generally do not apply to a so-called reverse exchange in which you acquire replacement property before you transfer relinquished property. However, if you use a qualified exchange accommodation arrangement (QEAA), the transfer may qualify as a like-kind exchange.

Under a QEAA, either the replacement property or the relinquished property is transferred to an exchange accommodation titleholder (EAT) who is treated as the beneficial owner of the property for federal income tax purposes. If the property is held in a QEAA, the IRS will accept the qualification of property as either replacement property or relinquished property, and the treatment of an EAT as the beneficial owner of the property for federal income tax purposes.

The QEAA rules allow taxpayers to structure “parking transactions” in which the replacement property is acquired by the EAT before the transfer of the relinquished property. However, the QEAA safe harbor does not apply if the taxpayer transfers property to an EAT and receives that same property back as replacement property for other property of the taxpayer.

The IRS has set numerous technical requirements for QEAAs. Property is held in a QEAA only if you have a written agreement with the EAT, the time limits for identifying and transferring the property are met, and the qualified indicia of ownership of property are transferred to the EAT.

The EAT must meet all the following requirements: (1) Hold qualified indicia of ownership (see below) at all times from the date of acquisition of the property until the property is transferred within the 180-day period (see below); (2) be someone other than you, your agent, or a person related to you or your agent; (3) be subject to federal income tax. If the EAT is treated as a partnership or S corporation, more than 90% of its interests or stock must be owned by partners or shareholders who are subject to federal income tax.

The IRS defines qualified indicia of ownership as either legal title to the property, other indicia of ownership of the property that are treated as beneficial ownership of the property under principles of commercial law (for example, a contract for deed), or interests in an entity that is disregarded as an entity separate from its owner for federal income tax purposes (for example, a single member limited liability company) and that holds either legal title to the property or other indicia of ownership.

There are time limits for identifying and transferring property under a QEAA. No later than 45 days after the transfer of qualified indicia of ownership of the replacement property to the EAT, you must identify the relinquished property in a manner consistent with the principles for deferred exchanges (6.4). If qualified indicia of ownership in replacement property have been transferred to the EAT, then no later than 180 days after that transfer, the replacement property must be transferred to you either directly or indirectly through a qualified intermediary (6.4). If the EAT receives qualified indicia of ownership in the relinquished property, then no later than 180 days after that transfer, the relinquished property must be transferred to a person other than you, your agent at the time of the transaction, or a person who is related to you or your agent.

Note: For further details on the IRS’ guidelines for QEAAs, see IRS Publication 544 and Revenue Procedure 2000-37, as modified by Revenue Procedure 2004-51 (parking transactions).

6.6 Exchanges Between Related Parties

A like-kind exchange between related persons may be disqualified if either party disposes of the property received in the exchange within two years after the date of the last transfer that was part of the exchange. Unless an exception applies, any gain deferred on the original exchange becomes taxable when the original like-kind property is disposed of by either party within the two-year period. If a loss was deferred on the original exchange, the loss becomes deductible if allowed under the rules in 5.6.

Indirect dispositions of the property within the two-year period, such as transfer of stock of a corporation or interests in a partnership that owns the property, may also be treated as taxable dispositions.

Related parties. Related persons falling within the two-year rule include your children, grandchildren, parent, brother, or sister, controlled corporations or partnerships (more than 50% ownership), and a trust in which you are a beneficiary. A transfer to a spouse is not subject to the two-year rule unless he or she is a nonresident alien.

Plan to avoid two-year rule. If you set up a prearranged plan under which you first transfer property to an unrelated party who within two years makes an exchange with a party related to you, the related party will not qualify for tax-free treatment on that exchange.

Exceptions. No tax will be incurred on a disposition made after the death of either related party; in an involuntary conversion provided the original exchange occurred before the threat of the conversion; or if you can prove that neither the exchange nor the later disposition was for a tax avoidance purpose.

6.7 Property Transfers Between Spouses and Ex-Spouses

Under Section 1041, all transfers of property between spouses are treated as tax-free exchanges, other than transfers to a nonresident alien spouse, certain trust transfers of mortgaged property, and transfers of U.S. Savings Bonds; these exceptions are discussed below. Section 1041 applies to transfers during marriage as well as to property settlements incident to a divorce. In a Section 1041 transfer, there is no taxable gain or deductible loss to the transferor spouse. The transferee-spouse takes the transferor’s basis in the property, and so appreciation in value will be taxed to the recipient on a later sale. This basis rule applies to all property received after July 18, 1984, under divorce or separation instruments in effect after that date.

A transfer is “incident to the divorce” if it occurs either within one year after the date the marriage ceases or, if later, is related to the cessation of the marriage, such as a transfer authorized by a divorce decree. A Treasury regulation provides that any transfer pursuant to a divorce or separation instrument occurring within six years of the end of the marriage is considered to be “related to the cessation of the marriage,” and therefore as “incident to a divorce.” Transfers made pursuant to the divorce or separation instrument that are more than six years after the end of the marriage, or transfers made within the six-year period that are not pursuant to the divorce or separation instrument, are considered related to the cessation of the marriage if they were made to effect the division of property owned by the spouses at the time of the cessation of the marriage. For example, a transfer not made within the six-year period qualifies if it is shown that an earlier sale was hampered by legal or business disputes such as a fight over the property value.

Nonresident alien. The tax-free exchange rule does not apply to transfers to a nonresident alien spouse or former spouse.

Transfers of U.S. Savings Bonds. The IRS has ruled that the tax-free exchange rules do not apply to transfers of U.S. Savings Bonds. For example, if a husband has deferred the reporting of interest on EE bonds and transfers the bonds to his ex-wife as part of a divorce settlement, the deferred interest is taxed to him on the transfer. The wife’s basis for the bonds is the husband’s basis plus the income he realizes on the transfer. When she redeems the bonds, she will be taxed on the interest accrued from the date of the transfer to the redemption date.

Payment for release of community property interest in retirement pay. The Tax Court allowed tax-free treatment for a payment made to a wife for releasing her community property claim to her husband’s military retirement pay. The IRS had argued that the tax-free exchange rules discussed in this section did not apply to the release of rights to retirement pay that would otherwise be subject to ordinary income tax. The Tax Court disagreed, holding that the tax-free exchange rule applies whether the transfer is for relinquishment of marital rights, cash, or other property.

Transfers in trust. The tax-free exchange rules generally apply to transfers in trust for the benefit of a spouse or a former spouse if incident to a divorce. However, gain cannot be avoided on a trust transfer of heavily mortgaged property. If the trust property is mortgaged, the transferor spouse must report a taxable gain to the extent that the liabilities assumed by the transferee spouse plus the liabilities to which the property is subject (even if not assumed) exceed the transferor’s adjusted basis for the property. If the transferor realizes a taxable gain under this rule, the transferee’s basis for the property is increased by the gain.

Sole proprietorship sale to spouse. Tax-free exchange rules may apply to a sale of business property by a sole proprietor to a spouse. The buyer spouse assumes a carryover basis even if fair market value is paid. The transferor is not required to recapture previously claimed depreciation deductions or investment credits. However, the transferee is subject to the recapture rules on premature dispositions or if the property ceases to be used for business purposes.

Transfer of nonstatutory options or nonqualified deferred compensation. According to the IRS, if a vested interest in nonstatutory (nonqualified) stock options or nonqualified deferred compensation is transferred to a former spouse as part of a property settlement, the transferor-spouse (the employee) does not have to report any income; the Section 1041 tax-free exchange rules apply. When the transferee-spouse later exercises the options or receives the deferred compensation, he or she will be taxed on the option spread (2.17) or the deferred compensation as if he or she was the employee. Income tax withholding and FICA tax withholding (Social Security and Medicare taxes) is generally required from the payments made to the transferee-spouse.

Divorce-related redemptions of stock in closely held corporation. When a married couple own all (or most) of the stock in a closely held corporation, the corporation may redeem the stock of one of the spouses as part of an overall divorce settlement. Does the transferring spouse avoid tax on the redemption under the Section 1041 tax-free exchange rules?

If the redemption of one of the spouses’ stock is treated as a transfer to a third party on behalf of the other spouse, Section 1041 applies and the transferor-spouse would escape tax on the redemption. However, there has been much confusion and litigation as to the standards for determining whether a redemption is “on behalf of” the non-transferor spouse, and whether different tests should apply for determining the tax treatment of each spouse. Court decisions have generally supported tax-free treatment for a spouse whose stock is redeemed under the terms of the couple’s divorce or separation instrument, or where the other (non-transferring) spouse requests or consents to the redemption. However, the courts are divided on the issue of whether the non-transferor spouse, who is left in control of the corporation, has realized a constructive dividend as a result of the redemption. See Example 2 below for the disputed positions taken by Tax Court judges in the Read case.

In response to the inconsistent standards used by the courts (see the Examples below), the IRS amended its regulations to provide a specific rule for determining which spouse will be taxed on the redemption. The regulation allows tax-free exchange treatment under Section 1041 to the transferor spouse (whose stock was redeemed) only if under applicable law the redemption is treated as resulting in a constructive dividend to the non-transferor spouse. If constructive dividend treatment does not apply to the non-transferor spouse, the form of the redemption transaction is followed and the transferor-spouse taxed on the redemption. The IRS regulation adopts the position of some of the dissenting judges in the Read case; see Example 2 below. The spouses are allowed to provide in a divorce or separation agreement that the redemption will be taxable to the nontransferor spouse even if the redemption would not result in a constructive dividend to that spouse under applicable law. Alternatively, they can provide that the transferor will be taxed on the redemption although the redemption would otherwise be treated as a constructive dividend to the nontransferor spouse.

Basis of property received before July 19, 1984, or under instruments in effect before that date. The tax-free exchange rules do not apply to property received before July 19, 1984, from your spouse (or former spouse if the transfer was incident to divorce). Your basis for determining gain or loss when you sell such property is its fair market value when you received it. The same fair market value basis rule applies to property received after June 18, 1984, under an instrument in effect on or before that date unless a Section 1041 election was made to have the tax-free exchange rules apply. For property subject to such an election, your basis is the same as the transferor-spouse’s adjusted basis.

6.8 Tax-Free Exchanges of Stock in Same Corporation

Gain on the exchange of common stock for other common stock of the same corporation is not taxable. The same rule generally applies to an exchange of preferred stock of the same corporation, but not if “nonqualified” preferred with special redemption rights or a varying dividend rate is received. Loss realized on a qualifying exchange is not deductible. The exchange may take place between the stockholder and the company or between two stockholders.

An exchange of preferred stock for common, or common for preferred, in the same company is generally not tax free, unless the exchange is part of a tax-free recapitalization. In such exchanges, the company should inform you of the tax consequences.

Convertible securities. A conversion of securities under a conversion privilege is tax free (30.7).

6.9 Joint Ownership Interests

The change to a tenancy in common from a joint tenancy is tax free. You may convert a joint tenancy in corporate stock to a tenancy in common without income-tax consequences. The transfer is tax free even though survivorship rights are eliminated. Similarly, a partition and issuance of separate certificates in the names of each joint tenant is also tax free.

A joint tenancy and a tenancy in common differ in this respect. On the death of a joint tenant, ownership passes to the surviving joint tenant or tenants. But on the death of a tenant holding property in common, ownership passes to his or her heirs, not to the other tenant or tenants with whom the property was held.

A tenancy by the entirety is a form of joint ownership recognized in some states and can be only between a husband and wife.

Dividing properties held in common. A division of properties held as tenants in common may qualify as tax-free exchanges.

For example, three men owned three pieces of real estate as tenants in common. Each man wanted to be the sole owner of one of the pieces of property. They disentangled themselves by exchanging interests in a three-way exchange. No money or property other than the three pieces of real estate changed hands, and none of the men assumed the others’ liability. The transactions qualified as tax-free exchanges and no gain or loss was recognized.

Receipt of boot. Exchanges of jointly owned property are tax free as long as no “boot,” such as cash or other property, passes between the parties (6.3).

6.10 Setting up Closely Held Corporations

Tax-free exchange rules facilitate the organization of a corporation. When you transfer property to a corporation that you control solely in exchange for corporate stock in that corporation (but not nonqualified preferred stock), no gain or loss is recognized on the transfer. For control, you alone or together with other transferors (such as partners, where a partnership is being incorporated) must own at least 80% of the combined voting power of the corporation and 80% of all other classes of stock immediately after the transfer to the corporation. If you receive securities in addition to stock, the securities are treated as taxable “boot.” The corporation takes your basis in the property, and your basis in the stock received in the exchange is the same as your basis in the property. Gain not recognized on the organization of the corporation may be taxed when you sell your stock, or the corporation disposes of the property.

Transfer of liabilities. When assets subject to liabilities are transferred to the corporation, the liability assumed by the corporation is not treated as taxable “boot,” but your stock basis is reduced by the amount of liability. The transfer of liabilities may be taxable when the transfer is part of a tax avoidance scheme, or the liabilities exceed the basis of the property transferred to the corporation.

6.11 Exchanges of Coins and Bullion

An exchange of “gold for gold” coins or “silver for silver” coins may qualify as a tax-free exchange of like-kind investment property. An exchange is tax free if both coins represent the same type of underlying investment. An exchange of bullion-type coins for bullion-type coins is a tax-free like-kind exchange. For example, the exchange of Mexican pesos for Austrian coronas has been held to be a tax-free exchange as both are bullion-type coins.

However, an exchange of U.S. gold collector’s coins for South African Krugerrands is taxable. Krugerrands are bullion-type coins whose value is determined solely by metal content, whereas the U.S. gold coins are numismatic coins whose value depends on age, condition, number minted, and artistic merit, as well as metal content. Although both coins appear to be similar in gold content, each represents a different type of investment.

6.12 Tax-Free Exchanges of Insurance Policies

These exchanges of insurance policies are considered tax free:

- Life insurance policy for another life insurance policy, endowment policy, or an annuity contract.

- Life insurance policy, an endowment policy, or an annuity contract for a qualified long-term care policy.

- Endowment policy for another endowment policy that provides for regular payments beginning no later than the date payments would have started under the old policy, or in exchange for an annuity contract.

- Annuity contract for another annuity contract with identical annuitants.

These exchanges are not tax free:

- Endowment policy for a life insurance policy, or for another endowment policy that provides for payments beginning at a date later than payments would have started under the old policy.

- Annuity contract for a life insurance or endowment policy.

- Transfers of life insurance contracts where the insured is not the same person in both contracts. The IRS held that a company could not make a tax-free exchange of a key executive policy where the company could change insured executives as they leave or join the firm.

Endorsement of annuity check for another annuity is taxable. Cashing out a commercial annuity or nonqualified employee contract and investing it in another annuity does not qualify as a tax-free exchange. The IRS denied tax-free exchange treatment to a taxpayer who tried to complete a direct exchange of a non-qualified annuity contract but was foiled by the insurance company holding the contract. The taxpayer had asked the insurance company to issue a check directly to another insurer as consideration for a new annuity contract, intending the transaction to be treated as a tax-free exchange under Section 1035. The insurer refused and instead issued a check to the taxpayer. The taxpayer did not deposit the check, but instead endorsed it to the second insurance company to obtain the new annuity contract.

The IRS ruled that endorsing the check over to the second insurance company as consideration for the new contract was not a tax-free exchange. Instead, the taxpayer had to include in gross income the portion of the check that was allocable to income on the contract. If this had been a tax-sheltered 403(b) annuity or a qualified employee annuity, a distribution from the policy could have been rolled over tax-free to another such annuity, or even to another eligible retirement plan such as an IRA or qualified employer trust. However, in the case of a non-qualified annuity, there is no rollover provision for amounts distributed from the contract.

Note: Tax-free exchange treatment may be allowed if you surrender an annuity contract or insurance policy of an insurer in serious financial difficulty, and roll over the proceeds in a new policy or contract with a different insurer; see the Planning Reminder in this section (6.12).

IRS scrutiny of partial exchanges of annuity contracts. The IRS has been concerned that a direct transfer of a portion of the cash surrender value of an existing annuity contract for another annuity contract, followed by a withdrawal from or surrender of either the original annuity contract or the new contract, could be used to reduce the tax on earnings that would otherwise be due on a non-annuity distribution. The IRS has guidelines for determining whether the direct transfer of a portion of the cash surrender value of an existing annuity contract to another contract is a tax-free exchange. The rules apply whether or not the two contracts are issued by the same or different companies. Revenue Procedure 2011-38 allows tax-free exchange treatment for a direct transfer of a portion of the cash surrender value of an existing annuity contract for a second annuity contract if no amount, other than an amount received as an annuity for 10 or more years or during one or more lives, is received under either the original or new contract during the 180-day period starting on the transfer date. If tax-free exchange treatment is allowed under these guidelines, the two annuity contracts will be treated separately and the IRS will not require that they be aggregated even if the same insurance company issued both. If the 180-day test is not met, the IRS will determine if the amount received under either contract within the 180 days should be treated as a distribution taxable to the extent of earnings, or as boot (6.3) in a tax-free exchange.