Chapter 42

Claiming Depreciation Deductions

There are several methods of claiming expense deductions for your purchases in 2017 of equipment, fixtures, autos, and trucks used in your business:

- First-year expensing (Section 179 deduction), which allows a deduction of up to $510,000 (42.3).

- Bonus depreciation, which is another first-year deduction at 50% of cost for eligible property (42.20).

- Regular depreciation, which allows a prorated deduction over a period of years. Most business equipment is depreciable under MACRS (modified accelerated cost recovery system) over a six-year period. MACRS applies to new and used property. The objective of MACRS is to provide rapid depreciation and to eliminate disputes over useful life, salvage value, and depreciation methods. Useful life and depreciation methods are fixed by law; salvage value is treated as zero. If you do not want to use MACRS accelerated rates, you may elect the straight-line method.

Capital investments in buildings are depreciable using the straight-line method; residential buildings are depreciated over 27.5 years; nonresidential real property placed in service after May 12, 1993, is depreciated over 39 years (42.12). Specific annual rates for each class of property are provided by IRS tables.

Land is not depreciable.

42.1 What Property May Be Depreciated?

Depreciation deductions may be claimed only for property used in your business or other income-producing activity. If the primary purpose of the property is to produce income but it fails to yield any income, the property may still be depreciated.

Depreciation may not be claimed on property held for personal purposes such as a personal residence or pleasure car. If property, such as a car, is used both for business and pleasure, only the business portion may be depreciated.

Nondepreciable assets. Not all assets used in your business or for the production of income may be depreciable. Land is not depreciable, but the cost of landscaping business property may be depreciated if the landscaping is so closely associated with a building that it would have to be destroyed if the building were replaced. Qualifying trees and bushes are depreciable over 15 years.

Property held primarily for sale to customers or property includible in inventory is not depreciable, regardless of its useful life.

Amortization for business intangibles. The cost of goodwill, going concern value, and other intangibles including covenants not to compete, information bases, customer lists, franchises, licenses, and trademarks is amortizable over a 15-year period.

The amortization rule generally applies to property acquired after August 10, 1993 (42.17).

Residences. For depreciation of rented residences, see9.5. For depreciation of a home office, see40.13. For depreciation of a sublet cooperative apartment or one used in business, see40.17.

Farm property. Farmland is not depreciable; farm machinery and buildings are. Livestock acquired for work, breeding, or dairy purposes and not included in inventory may also be depreciated. For a detailed explanation of the highly technical rules for depreciating farm property and livestock, seeIRS Publication 225, Farmer’s Tax Guide.

Relevance of useful life. According to the Tax Court, under current MACRS law (as under prior ACRS rules for assets placed in service 1981-1986), useful life is irrelevant for claiming depreciation if you can show that an asset is subject to exhaustion, wear and tear, or obsolescence. Thus, in the case of antique musical instruments played by professional musicians, depreciation is allowable because of wear and tear, even though the instruments have an indeterminable useful life. Two federal appeals courts agreed, allowing professional violinists to deduct ACRS depreciation for their instruments.

In a case involving exotic cars that were not used for transportation but for exhibition, MACRS depreciation was allowed because the owner showed that they were subject to obsolescence. The autos were purchased solely for exhibition. The three state-of-the-art autos were a 1987 Lotus Pantera costing $63,000, a Lotus Espirit costing $48,000, and a Ferrari Testarossa costing $290,453. Over a four-year period, the owner deducted depreciation of over $298,000 while reporting gross income from exhibition fees of $96,630. The IRS disallowed the depreciation because the cars had no determinable useful life. The Tax Court allowed the depreciation because such cars are subject to obsolescence in the car-show business when new models appear with newer designs and high-tech features. One witness testified this could occur in some cases within a year.

The Tax Court warned that such exotic cars should not be confused with museum pieces. If they had been museum pieces, such as antique cars, no depreciation would have been allowed. In the case of art objects and antiques used as business assets, the useful life requirement remains relevant because such assets are not subject to exhaustion, wear or tear, or obsolescence.

The IRS may continue to dispute and litigate cases in which depreciation is claimed on assets with indeterminable useful lives. For example, in a private ruling, the IRS did not allow a developer to depreciate street improvements that had been turned over to a city. The improvements were an intangible asset that improved the developer’s access to its real estate projects, but this asset had an unlimited life. There was no determinable useful life because the city had agreed to maintain and replace the improvements as necessary, and there was no evidence that the city would ever assess the developer for replacement costs.

Basis for depreciation. Generally, the basis of the property on which you figure depreciation is its adjusted basis, which usually is its cost. To determine basis when property is acquired other than by purchase, see 5.16through 5.20.

If you convert property from personal to business use, the basis for depreciation purposes is the lower of its adjusted basis or its fair market value at the time of the conversion.

42.2 Claiming Depreciation on Your Tax Return

If you report business or professional self-employed income, use Form 4562 for assets placed in service during 2017 and enter the total deduction on Line 13, Schedule C. For claiming depreciation on “listed property” such as cars and computers, you use Form 4562, regardless of the year placed in service. Seethe explanation of listed property in this chapter (42.10). If your only depreciation deduction is for pre-2017 assets, none of which is listed property, you do not need to use Form 4562; figure the deduction on your own worksheet, and enter it on Line 13, Schedule C.

If you are an employee claiming auto expenses, you must use Form 2106 to claim depreciation on an automobile used for business purposes.

If you claim a home office deduction using the actual expense method (40.13), you must use Form 8829 to claim depreciation on the portion of your home used for business.

If you report rental income on Schedule E, you must use Form 4562 for claiming depreciation on buildings placed in service in 2017. For buildings placed in service before 2017, enter the depreciation deduction directly on Schedule E. If you have a rental loss on Schedule E, your deduction for depreciation and other expenses may have to be included on Form 8582 to figure net passive activity income or loss; see Chapter 10.

42.3 First-Year Expensing Deduction

The dollar limit on first-year expensing in 2017 is $510,000. The dollar limit is phased out if the cost of qualifying property placed in service during the year exceeds a set dollar limit ($2,030,000 in 2017).

Costs eligible for expensing. You may elect first-year expensing for tangible personal property bought for business use, such as machinery, equipment, or a car, truck or computer, provided the property is acquired from a non-related party. Qualified leasehold and retail improvements and qualified restaurant property also qualify for expensing (42.14). Expensing is not allowed for property held for investment.

To elect the expensing deduction for the cost of qualifying property for 2017, the qualifying property must have been purchased and placed in service in 2017. You may not elect first-year expensing for property purchased before 2017, even if 2017 is the first year you use it for business. For example, if you bought a laptop for family use in 2016 and in 2017 you converted it to business use, expensing is not allowed on your 2017 return. Vehicles are subject to special dollar limits (43.4).

The portion of cost not eligible for first-year expensing may be recovered by depreciation under the regular MACRS rules (42.4–42.5). The first-year expensing deduction is technically called the “Section 179 deduction.”

Electing first-year expensing. You make the election simply by reporting on Form 4562 the assets for which the election applies. You are permitted to make an election or revoke an election (or change the amount of an election or the assets for which the election applies) on a timely filed amended return. You do not need IRS consent. A revocation, once made, is irrevocable.

Partial business use. If you use the equipment for both business and personal use, business use must exceed 50% in the year the equipment is first placed into service to claim a first-year expensing deduction. The expensing deduction may be claimed for the cost allocated to business use up to the dollar limit. For business vehicles, the deduction may not exceed the annual depreciation limit (43.4).

To elect first-year expensing for “listed property” such as a computer or car (42.10), business use in the first year you use it must exceed 50%. If it does, you show the amount eligible for expensing in the section for “Listed Property” on Form 4562 and then transfer the amount to the part of Form 4562 where the expensing election is claimed.

Figuring the deduction. For business use of less than 100% (but more than 50%), the expensing deduction is limited to the business portion of the cost. As discussed below, the dollar limit may have to be reduced because your taxable income is lower than the applicable dollar limit ($510,000 in 2017), eligible purchases exceed a set dollar amount ($2,030,000), or you are married filing separately.

If you qualify for expensing, you do not have to claim the entire amount. If in 2017 you place in service more than one item of property, you may allocate the dollar limit between the items. If you placed in service only one item of qualifying property that cost less than the dollar limit, your deduction is limited to that cost.

If you acquire property in a trade-in, the cost eligible for expensing is limited to the cash you paid. You may not include the adjusted basis of the property traded in, although your basis for the new property includes that amount.

Effect on regular depreciation. If the cost basis of the property exceeds the first-year expensing limit, you compute depreciation on the cost of the property less the amount of the first-year deduction.

Limit reduced if taxable income is lower. Your expensing deduction may not exceed net income from all your active businesses; seethe Caution on this page.

Limit reduced if qualifying purchases exceed threshold. If the total cost of qualifying property placed in service during 2017 exceeds the purchase limit of $2,030,000, the dollar limit on expensing is reduced dollar for dollar by the cost of qualifying property exceeding the limit. For example, if in 2017 you place in service machinery costing $2,100,000, the $510,000 limit is reduced by $70,000 ($2,100,000 – $2,030,000). The reduced limit of $440,000 is shown on Form 4562 on Line 5 of Part I (labeled “Dollar limitation for tax year.”) If the total cost is $2,540,000 or more, no first-year expensing deduction is allowed for 2017.

Limit reduced if married filing separately. If you and your spouse file separate returns, the 2017 expensing limit for both of you is one-half the usual amount. Unless you agree to a different allocation, you are each allowed only one-half of the limit or $255,000. The phaseout threshold for purchases also applies to both of you as a unit. Thus, the dollar limit is fully phased out when purchases exceed $2,540,000.

Partners and S corporation stockholders. For property bought by a partnership or an S corporation, the dollar limit and taxable income limit applies to the business, as well as the owners as individual taxpayers. The partnership or S corporation determines its expensing deduction subject to the limits and allocates the deduction, if any, among the partners or shareholders. The allocated deduction may not exceed the net taxable income of the partnership or S corporation from actively conducted businesses.

An individual partner’s expensing deduction may not exceed dollar limit, regardless of how many partnership interests he or she has. However, the partner must reduce the basis of each partnership interest by the full allocable share of each partnership’s expensing deduction, even if that amount is not deductible because of the dollar limit.

Disqualified acquisitions from related parties. Property does not qualify for the expense election if:

- It is acquired from a spouse, ancestor, or lineal descendant, or from non–family-related parties subject to the loss disallowance rule (5.6). For purposes of the expensing election, a corporation is controlled by you and thus subject to the loss disallowance rule (5.6) if 50% or more of the stock is owned by you, your spouse, your ancestors, or your descendants.

- The property is acquired by a member of the same controlled group (using a 50% control test).

- The basis of the property is determined in whole or in part (a) by reference to the adjusted basis of the property of the person from whom you acquired it or (b) under the stepped-up basis rules for inherited property.

Recapture of expensing deduction. Recapture of the first-year expensing deduction may occur on a disposition of the asset or if business use falls to 50% or less. If business use falls to 50% or less after the year the property is placed in service but before the end of the depreciable recovery period (42.4, 42.10), you must “recapture” the benefit from the first-year expensing deduction. The amount recaptured is the excess of the expensing deduction over the amount of depreciation that would have been claimed (through the year of recapture) without expensing (42.10). Recaptured amounts are reported as ordinary income on Form 4797.

When you sell or dispose of the property, the first-year expensing deduction is treated as depreciation for purposes of the recapture rules (44.3) that treat gain as ordinary income to the extent of depreciation claimed.

42.4 MACRS Recovery Periods

Depreciable assets other than buildings fall within a three-, five-, seven-, 10-, 15-, or 20-year recovery period under the general depreciation system (GDS).

Straight-line recovery for buildings is claimed over a period of 27.5 years for residential rental property or 39 years for nonresidential real property (42.13).

Note: The actual write-off period of depreciation for an asset is one year longer than the class life because of the convention rules (42.5–42.7).

Three-year property. This class includes property with a class life of four years or less, other than cars and light-duty trucks, which are in the five-year class.

This class includes: special handling devices for the manufacture of food and beverages; special tools and devices for the manufacture of rubber products; special tools for the manufacture of finished plastic products, fabricated metal products, or motor vehicles; and breeding hogs. By law, racehorses of any age and other horses more than 12 years old when placed in service are also in the three-year class. However, the three-year period will not apply to racehorses two years or younger in 2017 unless Congress extends the law. Seethe e-Supplement at jklasser.com for any update.

Five-year property. This class includes property with a class life of more than four years and less than 10 years such as computers (42.10), typewriters, copiers, duplicating equipment, heavy general-purpose trucks, trailers, cargo containers, and trailer-mounted containers. Also included by law in the five-year class are cars, light-duty trucks (actual unloaded weight less than 13,000 pounds), taxis, buses, computer-based telephone central office switching equipment, computer-related peripheral equipment, semiconductor manufacturing equipment, and property used in research and experimentation. These leasehold improvements eligible for a five-year recovery period must be depreciated using the straight-line method.

Seven-year property. This class includes any property with a class life of 10 years or more but less than 16 years. This is also a catch-all category for assets with no class life that have not been assigned by law to another class. Included in the seven-year class are: office furniture and fixtures, such as desks, safes, and files; cellular phones; fax machines; refrigerators; dishwashers; and machines used to produce jewelry, musical instruments, toys, and sporting goods. Qualified motor sports entertainment complexes were seven-year properties in 2016 but the law expired; see the e-Supplement at jklasser.com for any update on an extension.

Ten-year property. This includes property with a class life of 16 years or more and less than 20 years, such as vessels, barges, tugs, and water transportation equipment, and assets used in petroleum refining or in the manufacture of tobacco products and certain food products. The 10-year class also includes single-purpose agricultural and horticultural structures, and trees or vines bearing fruit or nuts.

Fifteen-year property. This includes land improvements such as fences, sidewalks, docks, shrubbery, roads, and bridges. It also includes other property with a class life of 20 years or more but less than 25 years, such as municipal sewage plants and telephone distribution plants. Gas station convenience stores are in the 15-year class if the property is no more than 1,400 square feet, or at least 50% of the floor space is devoted to selling petroleum products, or at least 50% of revenues are from petroleum sales. The owner of the gas station property does not have to be the operator of businesses on the property.

Twenty-year property. This class includes property with a class life of 25 years or more, such as farm buildings and municipal sewers, except that residential and nonresidential real estate is excluded (42.13).

42.5 MACRS Rates

The MACRS rate under the general depreciation system depends on the recovery period (42.4) for the property and whether the half-year or mid-quarter convention applies. The 200% declining balance rate applies to three-year property, five-year property, seven-year property, and ten-year property. See42.8for the 150% declining balance rate election. These rates are adjusted for the convention rules explained below. When the 200% declining balance rate provides a lower annual deduction than the straight-line rate, the 200% declining balance rate is replaced by the straight-line rate. The rates in the tables at the end of this section incorporate the applicable convention and the change from the 200% declining balance rate to a straight-line recovery. MACRS straight-line rates are discussed later in this Chapter (42.9).

Conventions. Under the half-year convention, all property acquired during the year, regardless of when acquired during the year, is treated as acquired in the middle of the year. As a result, only one-half of the full first-year depreciation is deductible and in the year after the last class life year, the balance of the depreciation is written off. Furthermore, in the year property is sold, only half of the full depreciation for that year is deductible (42.6).

The half-year convention applies unless the total cost bases of depreciable assets placed in service during the last three months of the taxable year exceed 40% of the total bases of all property placed in service during the entire year. If this 40% test applies, you must use a mid-quarter convention to figure your annual depreciation deduction (42.7).

Buildings are depreciated using a mid-month convention (42.12).

Depreciation tables. Table 42-1 provides year-by-year rates for property in the three, five-, and seven-year classes. The rates incorporate the adjustment for the half-year or mid-quarter convention and the switch from the 200% declining balance rate to the straight-line method. Use the rate shown in the table under the convention for your asset. The rate is applied to original basis, minus any first-year expensing deduction (42.3) and bonus depreciation (42.20) you claimed. After applying the rate from the table to the basis, you claim the deduction on Form 4562, Part III, Section B, labeled “General Depreciation System” (GDS).

You use the tables for the entire recovery period unless you claim a deductible casualty loss that reduces your basis in the property. For the year of the casualty loss and later years, depreciation must be based on the adjusted basis of the property at the end of the year. The tables may no longer be used; seeIRS Publication 946 for further details.

Table 42-1 MACRS Depreciation Rates

|

Mid-Quarter Convention |

|||||

Year |

Half-Year Convention |

1st (Quarter) |

2nd (Quarter) |

3rd (Quarter) |

4th (Quarter) |

|

3-Year Property |

|||||

1 |

33.33% |

58.33% |

41.67% |

25.00% |

8.33% |

2 |

44.45 |

27.78 |

38.89 |

50.00 |

61.11 |

3 |

14.81 |

12.35 |

14.14 |

16.67 |

20.37 |

4 |

7.41 |

1.54 |

5.30 |

8.33 |

10.19 |

|

5-Year Property |

|||||

1 |

20.00% |

35.00% |

25.00% |

15.00% |

5.00% |

2 |

32.00 |

26.00 |

30.00 |

34.00 |

38.00 |

3 |

19.20 |

15.60 |

18.00 |

20.40 |

22.80 |

4 |

11.52 |

11.01 |

11.37 |

12.24 |

13.68 |

5 |

11.52 |

11.01 |

11.37 |

11.30 |

10.94 |

6 |

5.76 |

1.38 |

4.26 |

7.06 |

9.58 |

|

7-Year Property |

|||||

1 |

14.29% |

25.00% |

17.85% |

10.71% |

3.57% |

2 |

24.49 |

21.43 |

23.47 |

25.51 |

27.55 |

3 |

17.49 |

15.31 |

16.76 |

18.22 |

19.68 |

4 |

12.49 |

10.93 |

11.97 |

13.02 |

14.06 |

5 |

8.93 |

8.75 |

8.87 |

9.30 |

10.04 |

6 |

8.92 |

8.74 |

8.87 |

8.85 |

8.73 |

7 |

8.93 |

8.75 |

8.87 |

8.86 |

8.73 |

8 |

4.46 |

1.09 |

3.33 |

5.53 |

7.64 |

42.6 Half-Year Convention for MACRS

The half-year convention treats all business equipment placed in service during a tax year as placed in service in the midpoint of that tax year. The same rule applies in the year in which the property is disposed of. The effect of this rule is as follows: A half-year of depreciation is allowed in the first year property is placed in service, regardless of when the property is placed in service during the tax year. For each of the remaining years of the recovery period, a full year of depreciation is claimed. If you hold the property for the entire recovery period, a half-year of depreciation is claimed for the year following the end of the recovery period. If you dispose of the property before the end of the recovery period, a half-year of depreciation is allowable for the year of disposition.

See Table 42-1(MACRS Depreciation Rates(42.5). for year-by-year rates under the half-year convention. Apply the rate from the table to the original basis, minus any first-year expensing (42.3) deduction and bonus depreciation (42.20) claimed. The Example in 42.5 shows the year-by-year deduction computation for five-year property under the half-year convention.

If you dispose of property before the end of its recovery period (42.5), your deduction for the year of disposition is one-half of the deduction that would be allowed for the full year using the rate shown in the table. For example, if you sell the machine in the Example in 42.5 in year three, the deduction is $1,920 (½ of $3,840).

42.7 Last Quarter Placements—Mid-Quarter Convention

A mid-quarter convention generally applies if the total cost basis of business equipment placed in service during the last three months of the tax year exceeds 40% of the total basis of all the property placed in service during the year. In applying the 40% rule, you do not count residential rental property, nonresidential realty, and assets that were placed in service and disposed of during the same year.

Under the mid-quarter convention, the first-year depreciation allowance for all property (other than nonresidential real property and residential rental property) placed in service during the year is based on the number of quarters that the asset was in service. Property placed in service at any time during a quarter is treated as having been placed in service in the middle of the quarter. The mid-quarter convention also applies to sales and disposals of property. The disposal is treated as occurring in the midpoint of the quarter.

If you dispose of property before the end of its recovery period (42.5), your deduction for the year is figured by multiplying a full year of depreciation by the percentage listed in the following chart for the quarter in which you disposed of the property.

|

Quarter |

Percentage |

|

First |

12.5% |

|

Second |

37.5% |

|

Third |

62.5% |

|

Fourth |

87.5% |

42.8 150% Rate Election

Instead of using the 200% declining balance rate for property in the three-, five-, seven-, and 10-year classes, you may elect a 150% declining balance rate. You may prefer the 150% rate when you are subject to the alternative minimum tax (AMT). For AMT purposes, you must use the 150% rate and adjust your taxable income if the 200% rate was used for regular tax purposes (23.2). If for regular tax purposes you elect to apply the 150% rate, use the same recovery period (42.4) you would have used if you had claimed the 200% declining balance rate. Thus, the recovery period is five years for cars and computers and seven years for office furniture and fixtures. If the half-year convention applies, the first-year rate for the five-year class is 15%, and 10.71% for the seven-year class; seethe table below. Apply the rate from the table to your original basis, minus any first-year expensing deduction and bonus depreciation claimed. If you are subject to the mid-quarter convention, seeIRS Publication 946 for the tables showing mid-quarter convention rates.

The election to use the 150% rate must be made for all property within a given class placed in service in the same year. The election is irrevocable.

Table 42-2 Half-Year Convention—150% Rate

|

Recovery Period |

||

Year— |

5-Year— |

7-Year— |

1 |

15.00% |

10.71% |

2 |

25.50 |

19.13 |

3 |

17.85 |

15.03 |

4 |

16.66 |

12.25 |

5 |

16.66 |

12.25 |

6 |

8.33 |

12.25 |

7 |

|

12.25 |

8 |

|

6.13 |

42.9 Straight-Line Depreciation

You may not want an accelerated rate and may prefer to write off depreciation at an even pace. There are two straight-line methods. You may make an irrevocable election to use the straight-line method over the regular MACRS recovery period (42.4) under the general depreciation system (GDS). Alternatively, you may elect straight-line recovery over the designated recovery period for the class life under the alternative depreciation system (ADS). For some assets, such as cars, the GDS and ADS recovery periods are the same (five years for a car). In most cases, the ADS recovery period is longer than the GDS recovery period. For example, the recovery period for office furniture and fixtures is seven years under GDS and 10 years under ADS.

Half-year and quarter-year conventions apply to both straight-line methods (42.6, 42.7). A mid-month convention applies under the straight-line rule for buildings (42.12).

Straight-line over regular recovery period (GDS). You make this election on Form 4562, Part III, Section B, labeled “General Depreciation System”. To elect this method for one asset, you must also use it for all other assets in the same class that are placed in service during the year. The straight-line election is irrevocable.

Straight-line under the alternative depreciation system (ADS). Under the alternative depreciation system (ADS), the straight-line recovery period is generally the same as the “class life” of the asset as determined by the IRS; the ADS recovery periods are shown in IRS Publication 946. The ADS recovery period for cars, light trucks, and computers is five years, the same as under the GDS. For business office furniture and fixtures, the ADS straight-line recovery period is 10 years. The ADS recovery period for personal property with no class life is 12 years. For nonresidential real and residential rental property, you may elect ADS straight-line recovery over 40 years. SeeIRS Publication 946 for other ADS class lives.

Except for real estate, the ADS election applies to all property within the same class placed in service during the taxable year. For real estate, the election to use the alternative depreciation method may be made on a property-by-property basis. The election is irrevocable. The deduction is claimed on Form 4562, Part III, Section C, labeled “Alternative Depreciation System”.

Straight-line rate table. The table below shows straight-line rates for five-year, seven-year, and 10-year property under the half-year convention. As discussed earlier, the recovery period depends on whether the GDS or ADS straight-line method is used. If you are subject to the mid-quarter convention (42.7), seeIRS Publication 946 for tables showing the applicable rates.

Table 42-3 Half-Year Convention—Straight-Line Rate

|

Recovery Period |

|||

Year— |

5-Year— |

7-Year— |

10-Year— |

1 |

10.00% |

7.14% |

5.00% |

2 |

20.00 |

14.29 |

10.00 |

3 |

20.00 |

14.29 |

10.00 |

4 |

20.00 |

14.28 |

10.00 |

5 |

20.00 |

14.29 |

10.00 |

6 |

10.00 |

14.28 |

10.00 |

7 |

|

14.29 |

10.00 |

8 |

|

7.14 |

10.00 |

9 |

|

|

10.00 |

10 |

|

|

10.00 |

11 |

|

|

5.00 |

AMT depreciation. There is no AMT adjustment for depreciation if for regular tax purposes straight-line depreciation is claimed on tangible personal property placed in service after 1998. Similarly, for real estate placed in service after 1998, the straight-line depreciation deduction claimed for regular tax purposes does not have to be refigured for AMT. For real property placed in service before 1999, regular tax straight-line depreciation is refigured for AMT purposes using the straight-line method over 40 years.

Mandatory straight-line depreciation. You are required to use the alternative depreciation system for automobiles (43.3) and certain computers (42.10) used 50% or less for business.

Alternative MACRS depreciation must also be used for:

- Figuring earnings and profits;

- Tangible property which, during the taxable year, is used predominantly outside the United States;

- Tax-exempt use property;

- Tax-exempt bond financed property; and

- Imported property covered by an executive order.

42.10 Computers and Other Listed Property

“Listed property” is a term applied to certain equipment that may be used for personal and business purposes. For such property, the law allows first-year expensing (42.3),bonus depreciation (42.20), or accelerated MACRS (42.5) deductions only if business use exceeds 50%. For business use of 50% or less, you must use ADS straight-line depreciation (42.9). Deductions for listed property are claimed on Part V of Form 4562. If the more-than-50%-business-use test is met in the first year and first-year expensing or accelerated MACRS is claimed, but business use of listed property falls to 50% or less during the ADS straight-line recovery period (42.9), you must “recapture” first-year expensing, bonus depreciation and accelerated MACRS deductions.

What is “listed property”? Listed property includes passenger autos and other transportation vehicles (43.4), computers and peripheral equipment, boats, airplanes, and any photographic, sound, or video recording equipment that could be used for entertainment or recreational purposes. However, exceptions remove some items from the listed property category for many businesses. Listed property does not include (1) any computer or peripheral equipment that you own or lease that is used exclusively at a regular business establishment, and (2) photographic, phonographic, communications, or video equipment used exclusively and regularly in your business or regular business establishment. A home office that meets the requirements for deducting home office expenses(40.12) is considered a regular business establishment.

Deductions subject to recapture. If business use of listed property exceeds 50% in the first year but drops to 50% or less within the ADS recovery period (Table 42-3), bonus depreciation, MACRS and any first-year expensing deduction are subject to “recapture.” In the year in which business use drops to 50% or less, you recapture the excess of (1) the MACRS, bonus depreciation, and first-year expensing deductions claimed in prior years over (2) the deductions that would have been allowed using ADS straight-line depreciation (42.9). For the rest of the recovery period, you continue to use the alternative straight-line rate.

Recapture is figured on Form 4797. The recapture computation follows the steps shown in 43.10 for recapture of excess depreciation on an automobile.

Investor’s use of a computer. For an investor who uses a home computer for managing an investment portfolio, the computer is treated as listed property. Unless the computer is also used for business, and the computer time spent on business work exceeds 50% of the total, only straight-line depreciation may be claimed; neither first-year expensing nor accelerated MACRS is allowed. Although the investment use is disregarded for purposes of the more-than-50%-business-use test, the investment use is combined with the business use for purposes of determining the percentage of depreciable cost. Depreciable investment use must relate to managing investments that produce taxable income. Seethe Examples below.

Leasing listed property. You may deduct the portion of your lease payments attributable to business use. However, if business use is 50% or less for any year, you must report as income an amount based on the fair market value of the unit, the percentage of business plus investment use, and percentages from two IRS tables shown in Publication 946. Special rules apply for leasing cars, light trucks, and vans (43.12).

42.11 Assets in Service Before 1987

Assets placed in service before 1987 were depreciated under a different recovery system called ACRS. Most of the assets have already been fully depreciated, although some assets, such as certain real estate placed in service before 1987, continue to be governed by these rules (42.15).

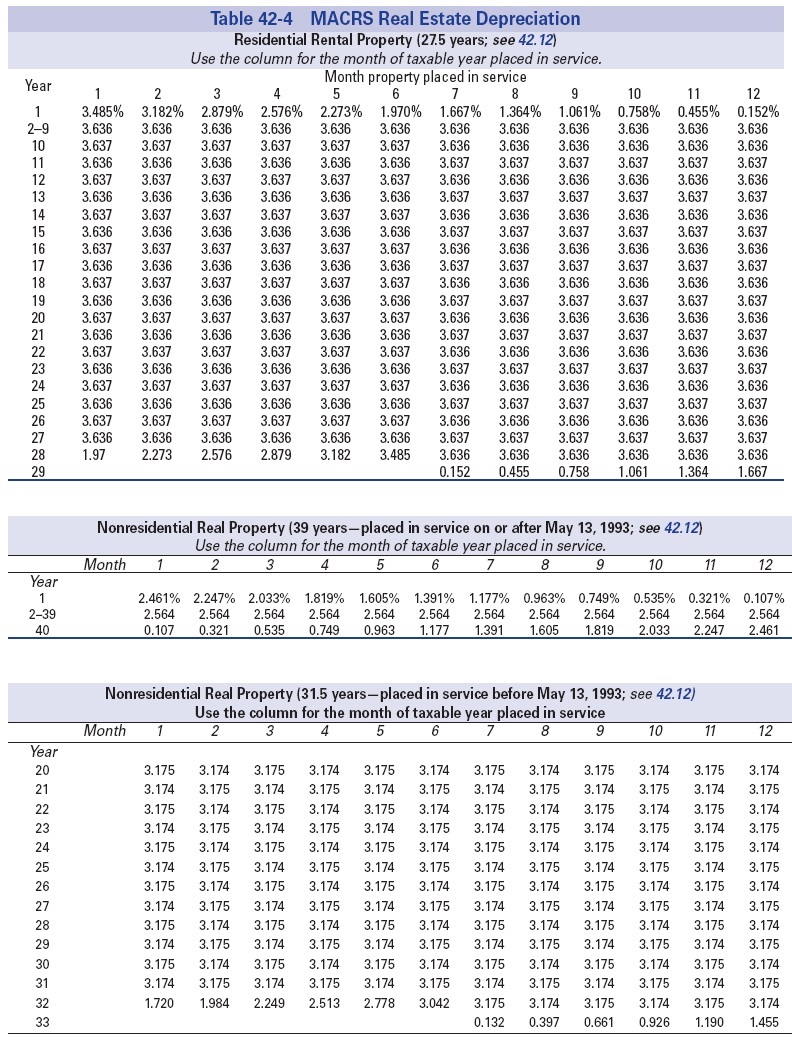

42.12 MACRS for Real Estate Placed in Service After 1986

The recovery period for residential rental property placed in service after December 31, 1986, is 27.5 years. The recovery period for nonresidential real property is either 39 years or 31.5 years, depending on when the property was placed in service.

The method of recovery for nonresidential or residential property is the straight-line method using a mid-month convention. SeeTable 42-4 for rate tables for each class of property.

For nonresidential real property placed in service after December 31, 1986, but before May 13, 1993, the depreciation recovery period is 31.5 years.

For nonresidential real property placed in service after May 12, 1993, the recovery period is 39 years. Under a transition rule, the 31.5-year recovery period rather than the 39-year recovery period applies to a building placed in service before 1994 if before May 13, 1993, you had entered into a binding, written contract to buy or build it, or if, before that date, you had begun construction. The transition rule also applies if you obtained the contract or property from someone else who satisfied the pre–May 13, 1993, contract or construction requirement, provided he or she never put the building in service and you did so before 1994.

However, see 42.14 for qualified leasehold improvements, qualified restaurant property, and qualified retail improvement property.

Residential rental property subject to the 27.5 year recovery period is defined as a rental building or structure for which 80% or more of the gross rental income for the tax year is rental income from dwelling units. If you occupy any part of the building, the gross rental income includes the fair rental value of the part you occupy.

A dwelling unit is a house or an apartment used to provide living accommodations in a building or structure, but not a unit in a hotel, motel, inn, or other establishment where more than one-half of the units are used on a transient basis.

Mid-month convention. Under a mid-month convention, all residential rental property and nonresidential real property placed in service or disposed of during any month is treated as placed in service or disposed of at the midpoint of that month. You may determine the first-year deduction for your property by applying the percentage from Table 42-4 to the original depreciable basis. In later years, use the same column of the table to figure your deduction. If the property is disposed of before the end of the recovery period, the deduction for the year of disposition is figured by prorating the full-year deduction for the months the property was in service, treating the month of dispostion as one-half of a month of use.

Additions or improvements to property. The depreciation deduction for any additions to, or improvement of, any property is figured in the same way as the deduction for the property would be figured if the property had been placed in service at the same time as the addition or improvement. However, see 42.14 for qualified leasehold improvements, qualified restaurant property, and qualified retail improvement property.

42.13 Demolishing a Building

When you buy improved property, the purchase price is allocated between the land and the building; only the building may be depreciated. The land may not (42.1). If you later demolish the building, you may not deduct the cost of the demolition or the undepreciated basis of the building as a loss in the year of demolition. Expenses or losses in connection with the demolition of any structure, including certified historic structures, are not deductible. They must be capitalized and added to the basis of the land on which the structure is located.

Major rehabilitation. Where you are considering a major rehabilitation of a building that involves some demolition of the building, IRS guidelines may allow you to deduct the costs of demolition and a removal of part of the structure. Under the IRS rules, the costs of structural modification may avoid capitalization if 75% or more of the existing external walls are retained as internal or external walls and 75% or more of the existing internal framework is also retained. For certified historic structures, the modification must also be part of a certified rehabilitation.

42.14 Qualified Leasehold and Retail Improvements and Restaurant Property

The cost of qualified leasehold improvements, qualified restaurant property, and qualified retail improvement property can be expensed up to the overall first-year expensing limit of $510,000 (42.3). In addition, qualified leasehold and retail improvements and qualified restaurant property are depreciable under MACRS over a 15-year period using the straight-line method. These rules for expensing and 15-year straight-line depreciation have been made permanent. In addition, qualified improvement propertyqualifies for bonus depreciation (42.20).

Improvements that do not meet the tests for qualified leasehold, restaurant, and retail improvement must be depreciated under the MACRS rates for buildings shown at 42.12. For a leasehold improvement, the term of the lease is ignored under MACRS. If the lease term is shorter than the MACRS life and you do not retain the improvements at the end of the term, the remaining undepreciated basis is a deductible loss.

Qualified improvements eligible for first-year expensing and 15-year recovery. A qualified leasehold improvement is generally any improvement made under a lease to an interior part of a building that is nonresidential realty. A qualified retail improvement is an improvement to an interior part of a nonresidential building that is open to the general public and used in the retail trade or business of selling tangible personal property to the general public.

However, both qualified leasehold improvements and qualified retail improvements must be placed in service more than three years after the date that the building was first placed in service. Further, an improvement is not a qualified leasehold improvement or a qualified retail improvement if it relates to the enlargement of the building, an elevator or escalator, the internal structural framework of the building, or a structural component benefiting a common area.

For restaurant improvements, more than 50% of the building’s square footage must be devoted to the preparation of meals and seating for on-premises consumption of prepared meals. Note that the definition of “qualified restaurant property” includes restaurant buildings themselves, as well as restaurant improvements, provided the more-than-50%-square-footage test is met.

To elect first-year expensing for a qualified leasehold improvement, qualified retail improvement, or qualified restaurant property, a statement must be attached to your return that specifically indicates (1) that you are electing to apply Section 179 (f) of the Internal Revenue Code and (2) which specifies the type of qualifying property and the cost for which the expensing election is being made.

See the Form 4562 instructions for further details.

42.15 Depreciating Real Estate Placed in Service After 1980 and Before 1987

The ACRS recovery period of almost all buildings placed in service before 1987 has already ended. Some pre-1987 buildings are still being depreciated over a 35-year or 45-year period if the straight-line election discussed in the next paragraph was made.

Election to use straight-line depreciation. For 15-year, 18-year, or 19-year real property, you may have elected to use the straight-line method over 35 or 45 years. An election of the straight-line method for real property had to be made on a property-by-property basis, by the return due date, plus extensions, for the year the property was placed in service.

Rate of recovery. The rate of recovery is listed in Treasury tables that are available in IRS Publication 534.

Substantial improvements. Substantial improvements made after 1986 to an ACRS building are depreciable under MACRS (42.13), not ACRS.

Recapture. See 44.1 for recapture rules on the sale of ACRS property.

42.16 When MACRS Is Not Allowed

If you place in service personal property that you previously used or that was previously owned by a related taxpayer before 1987, you may not be able to apply MACRS rules. This anti-churning restriction is designed to discourage asset transfers between related persons to take advantage of MACRS deductions that exceed the deductions allowed before 1987 under ACRS. The anti-churning rule does not bar MACRS rules for real estate acquired after 1986, unless you lease back the real estate to a related party who owned it before 1987.

Special rules also apply to the transfer of property in certain tax-free corporate or partnership transactions where the property was used before 1987. If you receive property in a tax-free exchange, you may have to use the method used by the transferor in computing the ACRS deduction for that part of basis that does not exceed what was the transferor’s basis in the property. To the extent that basis exceeds the transferor’s, the MACRS rules may apply; for example, when you paid boot in addition to transferring property.

Where property is disposed of and reacquired, the depreciation deduction is computed as if the disposition had not occurred.

42.17 Amortizing Goodwill and Other Intangibles (Section 197)

The costs of intangibles coming within Section 197 are amortized over a 15-year period. The 15-year period applies regardless of the actual useful life of “Section 197 intangibles” acquired after August 10, 1993 (or after July 25, 1991, if elected), and held in connection with a business or income-producing activity.

Generally, the amount subject to amortization is cost. Annual amortization is reported on Form 4562. The 15-year period starts with the month the intangible was acquired.

A “Section 197 intangible” is: (1) goodwill; (2) going-concern value; (3) workforce in place; (4) information base; (5) know-how, but seeexceptions below; (6) any customer-based intangible; (7) any supplier-based intangible; (8) any license, permit, or other right granted by a governmental unit or agency; (9) any covenant not to compete made in the acquisition of a business; and (10) any franchise, trademark, or trade name.

Goodwill. Goodwill is the value of a business attributable to the expectancy of continued customer patronage, due to the name or reputation of a business or any other factor.

Franchises, trademarks, and trade names. A franchise (excluding sports franchises), trademark, or trade name is a Section 197 intangible. Amounts, whether fixed or contingent, paid on the transfer of a trademark, trade name, or franchise are chargeable to capital account and must be ratably amortized over a 15-year period. The renewal of a franchise, trademark, or trade name is treated as an acquisition of the franchise, trademark, or trade name. Renewal costs are amortized over 15 years beginning in the month of renewal.

Know-how. A patent, copyright, formula, process, design, pattern, format, or similar item may be a Section 197 intangible. However, the following interests are not Section 197 intangibles unless acquired as part of the acquisition of a business: patents, copyrights, and interests in films, sound recordings, videotapes, books, or other similar property.

Customer-based intangibles. Customer-based intangibles include the portion of an acquired trade or business attributable to a customer base, circulation base, undeveloped market or market growth, insurance in force, investment management contracts, or other relationships with customers that involve the future provision of goods or services.

Supplier-based intangibles. The portion of the purchase price of an acquired business attributable to a favorable relationship with persons who provide distribution services, such as favorable shelf or display space at a retail outlet, the existence of a favorable credit rating, or the existence of favorable supply contracts, are Section 197 intangibles.

Going-concern value. This is the additional value that attaches to property because it is an integral part of a going concern. This includes the value attributable to the ability of a trade or business to continue to operate and generate sales without interruption in spite of a change in ownership.

Workforce in place. The portion of the purchase price of an acquired business attributable to a highly skilled workforce is amortizable over 15 years. Similarly, the cost of acquiring an existing employment contract is amortizable over 15 years.

Information base. This includes the cost of acquiring customer lists; subscription lists; insurance expirations; patient or client files; lists of newspaper, magazine, radio, or television advertisers; business books and records; and operating systems. The intangible value of technical manuals, training manuals or programs, data files, and accounting or inventory control systems is also a Section 197 intangible.

Self-created intangibles. A Section 197 intangible created by a taxpayer is generally not amortizable, unless created in connection with a transaction that involves the acquisition of assets of a business. However, this deduction bar for self-created intangibles does not apply to the following: (1) any license, permit, or other right granted by a governmental unit or agency; (2) a covenant not to compete entered into on the acquisition of a business; or (3) any franchise, trademark, or trade name. For example, the 15-year amortization period may apply to the capitalized costs of registering or developing a trademark or trade name.

A person who contracts for or renews a contract for the use of a Section 197 intangible may not be considered to have created that intangible. For example, a licensee who contracts for the use of know-how may amortize capitalized costs over 15 years.

The following intangible assets are not Section 197 intangibles. (1) interests in a corporation, partnership, trust, or estate; (2) interests under certain financial contracts; (3) interests in land; (4) certain computer software (42.18); (5) certain separately acquired rights and interests; (6) interests under existing leases of tangible property; (7) interests under existing indebtedness; (8) sports franchises; (9) certain residential mortgage servicing rights; and (10) certain corporate transaction costs.

Loss limitations. A person who disposes of an amortizable Section 197 intangible at a loss and at the same time retains other Section 197 intangibles acquired in the same transaction may not deduct the loss. The disallowed loss is added to the basis of the retained Section 197 intangibles. The same rule applies if a Section 197 intangible is abandoned or becomes worthless and other Section 197 intangibles acquired in the same transaction are kept. The basis of the remaining intangibles is increased by the disallowed loss.

You may not treat a covenant not to compete as worthless any earlier than the disposition or worthlessness of the entire interest in a business.

Dispositions. An amortizable Section 197 intangible is not a capital asset. It is treated as depreciable property, and if held for more than one year, it will generally qualify as a Section 1231 asset (44.1). Amortization claimed on a Section 197 intangible is subject to recapture under Section 1245 and gain on its sale to certain related persons is subject to ordinary income treatment under Section 1239.

42.18 Deducting the Cost of Computer Software

The cost of software installed in a computer that you buy and use in your business is not deducted separately, unless the software cost is separately stated. In most cases, the cost of software bundled with a computer is not separately stated. The cost of the computer including such software is depreciable (42.10).

If you buy software for business use, such as a database or spreadsheet program, the treatment of the cost depends on your use of the program. If you use it for a year or less, such as an annual tax program, you may deduct the cost as a business expense for that year. If the useful life in your business exceeds a year, and the software meets the three tests in the Planning Reminder on this page, it is considered off-the-shelf software eligible for first-year expensing (42.3). Alternatively, you may depreciate the cost over 36 months using the straight-line method.

Software acquired in the acquisition of a business is eligible for first-year expensing (42.3) or depreciable over 36 months if it meets the three tests listed in the Planning Reminder on this page; otherwise, 15-year amortization applies under the Section 197 intangible rules (42.17).

42.19 Amortizing Research and Experimentation Costs

If you have these costs, you can deduct them currently or elect to amortize them over a period of not less than 60 months. The election may be advisable if you do not have current income; the deductions may become more valuable to you in the future.

You may be eligible for a tax credit for increasing your R&D costs (40.26). However, you cannot take a deduction and a credit with respect to the same costs.

42.20 Bonus Depreciation

Bonus depreciation is an additional first-year depreciation allowance equal to a set percentage of the adjusted basis of eligible property. The percentage for bonus depreciation for 2017 is 50%. For eligible property placed in service in 2018 (other than certain longer-lived and transportation property), the bonus percentage is scheduled to drop to 40%.

Bonus depreciation (also called a Section 168(k) allowance and a special depreciation allowance) can be claimed in addition to any first-year expensing. In figuring “adjusted basis” for purposes of bonus depreciation, any first-year expensing deduction is taken into account first. Then, you figure bonus depreciation on the cost of the property minus the first-year expensing allowance. Bonus depreciation is fully deductible for alternative minimum tax purposes (23.2); no adjustment is required.

You must be the original user of the property. In other words, bonus depreciation does not apply to used or pre-owned property.

Bonus depreciation cannot be claimed for property that must be depreciated under the ADS straight-line method (42.9). For example, it may not be used for listed property used 50% or less for business since such property must be depreciated under ADS.

Bonus depreciation allows the first-year dollar limit on write-offs for vehicles weighing less than 6,000 pounds to be increased by a fixed dollar amount reflecting bonus depreciation, provided the vehicle is purchased new and business use exceeds 50%. The bonus allowance increases the total dollar limit for such vehicles placed in service during 2017 by $8,000 (43.4).

Eligible property. Bonus depreciation can be claimed for any property with a recovery period of 20 years or less, computer software (other than a Section 197 intangible (42.17), and buildings that replace or rehabilitate property damaged, destroyed, or condemned as a result of a federally declared disaster.

Bonus depreciation is also allowed for “qualified improvements.” Qualified improvements are improvements made to the interior of a nonresidential building after the building is placed in service, other than elevators, escalators, enlargements, or changes to the structural framework. This is a broader improvement category now than under the pre-2016 rules, which allowed bonus depreciation for improvements only if they were qualified leasehold improvements. Under the new rule, a qualified improvement does not have to be subject to a lease and does not have to be placed in service more than three years after the building was placed in service.

Claiming bonus depreciation. You report bonus depreciation in Part II of Form 4562 labeled “Special Depreciation Allowance,” unless the property is a computer or other “listed property” (42.10). For listed property, use Part V of Form 4562.

Election out of bonus depreciation. Unlike regular depreciation, you are not required to use bonus depreciation and have the option of electing out of its use. If eligible for bonus depreciation, you can elect not to use it. The election out is made on a per-asset-class basis. Thus, for example, you can opt out of bonus depreciation for all five-year property while claiming it for seven-year property. To make the election out of claiming bonus depreciation, attach a statement to your return specifying the class of property for which the election not to claim additional depreciation is being made.

If you fail to make an election not to claim bonus depreciation, then you are deemed to have claimed it (even though you did not) and must reduce the basis of the property by the amount of bonus depreciation that could have been claimed.