Chapter 41

Retirement and Medical Plans for Self-Employed

Self-employed persons and partners can take advantage of tax-sheltered retirement plans or simplified employee pension plans (SEPs) (41.2).

Advantages flow from: (1) tax deductions allowed for contributions to the plan (a form of forced savings); (2) tax-free accumulations of income earned on assets held by the plan; and (3) in limited cases, special averaging for lump-sum benefits paid from a qualified retirement plan on retirement.

If you have employees, you must consider the cost of covering them when setting up your plan.

If you do not have any other retirement plan and have no more than 100 employees, you may set up a salary-reduction SIMPLE plan.

Sole proprietors must have minimum essential health coverage. Those who want to buy it through a government exchange must use the Marketplace for individuals; they cannot use the SHOPs for small businesses. Self-employed persons can pay for their health coverage on a more advantageous basis than other individuals. They can also use special health-related plans to further lower out-of-pocket medical costs while obtaining tax breaks. If you pay a certain amount for coverage of employees, you may be entitled to a tax credit (41.14).

41.1 Overview of Retirement and Medical Plans

Self-employed individuals can shelter income and obtain desired retirement savings and health coverage using various plans. While the plans are tied to being in business, the deductions for them are not business write-offs. Instead, deductions for the self-employed person’s own coverage are claimed directly on page 1 of Form 1040. For example, a self-employed person’s deductions for contributions to his or her own account in a qualified retirement plan (41.2), SEP (41.3), or SIMPLE IRA (41.9) are claimed on Line 28 of Form 1040. If the plans also cover employees of the self-employed person, deductions related to employees are claimed on Schedule C.

Self-employed individuals who obtain their own health insurance can deduct the premiums from gross income, rather than as an itemized medical expense (12.2). They may be able to cut the high cost of health coverage by using a high-deductible health plan, combined with a health savings account (HSA) (41.10). Contributions to the HSA are also deductible from gross income (41.11). Alternatively, self-employed individuals who have previously set up Archer MSAs can continue to use these tax-advantaged accounts to pay for medical costs not covered by insurance (41.13).

41.2 Choosing a Qualified Retirement Plan

You may set up a self-employed retirement plan if you have net earnings (gross business or professional income less allowable business deductions) from your sole proprietorship or partnership for which the plan is established. A qualified retirement plan for a self-employed individual is sometimes referred to as a Keogh (or H.R. 10) plan. If you are an inactive owner, such as a limited partner, you do not qualify to set up a qualified plan—unless you receive guaranteed payments for services that are treated as earnings from self-employment.

Set-up deadline. To deduct contributions for a tax year, your qualified plan must be adopted by the last day of that year (December 31 if you report on a calendar year basis). If it is, contributions can be made up to the due date of your return for that year, plus extensions.

Partnership plans. An individual partner or partners, although self-employed, may not set up a qualified plan. The plan must be established by the partnership. Partnership deductions for contributions to an individual partner’s account are reported on the partner’s Schedule K-1 (Form 1065) and deducted by the partner as an adjustment to income on Line 28 of Form 1040.

Including employees in your plan. You must include in your plan all employees who have reached age 21 with at least one year of service. An employee may be required to complete two years of service before participating if your plan provides for full and immediate vesting after no more than two years. You generally are not required to cover seasonal or part-time employees who work less than 1,000 hours during a 12-month period.

A minimum coverage rule requires that a defined benefit plan must include at least 40% of all employees, or 50 employees if that is less.

Your plan may not exclude employees who are over a certain age.

A plan may not discriminate in favor of officers or other highly compensated personnel. Benefits must be for the employees and their beneficiaries, and their plan rights may not be subject to forfeiture. A plan may not allow any of its funds to be diverted for purposes other than pension benefits. Contributions made on your behalf may not exceed the ratio of contributions made on behalf of employees.

Types of qualified plans. There are two types of qualified plans: defined benefit plans and defined contribution plans, and different rules apply to each. A defined benefit plan provides in advance for a specific retirement benefit funded by quarterly contributions based on an IRS formula and actuarial assumptions. A defined contribution plan does not fix a specific retirement benefit, but rather sets the amount of annual contributions so that the amount of retirement benefits depends on contributions and income earned on those contributions. If contributions are geared to profits, the plan is a profit-sharing plan, but fixed annual contributions are not required. A plan that requires fixed contributions regardless of profits is a money purchase plan. If you have a profit-sharing plan, a 401(k) plan arrangement can be included to allow you (and other participants) to make elective deferral contributions of before-tax compensation to the plan.

A defined benefit plan may prove costly if you have older employees who also must be provided with proportionate defined benefits. Furthermore, a defined benefit plan requires you to contribute to their accounts even if you do not have profits. For 2017, the benefit limit is the lesser of (a) 100% of the participant’s average compensation for the three consecutive years of highest compensation as an active participant or (b) $215,000. This dollar limit is reduced if benefits begin before age 62 and increased if benefits begin after age 65. The $215,000 limit is subject to cost-of-living increases; seethe e-Supplement at jklasser.comfor the 2018 limit.

For defined contribution plans, the 2017 limit on annual contributions and other additions (excluding earnings) was the lesser of 100% of compensation or $54,000. For 2018, the $54,000 limit may be adjusted for inflation; seethe e-Supplement at jklasser.com.

41.3 Choosing a SEP

Under a SEP (simplified employee pension plan), you may contribute to a special type of IRA more than is allowed under the regular IRA rules. Contributions do not have to be made every year. When you do make contributions, they must be based on a written allocation formula and must not discriminate in favor of yourself, other owners with more than a 5% interest, or highly compensated employees. Coverage requirements for employees are in 8.15. A salary-reduction arrangement for employees may be provided under a qualifying SEP established before 1997 or under a SIMPLE IRA plan established after 1996 (8.17).

The deadline for both setting up and contributing to a SEP is the due date for your return, including extensions. Thus, if you have not set up a qualified plan by the end of the taxable year (41.2), you may still make a deductible retirement contribution for the year by contributing to a SEP by the due date of your return.

41.4 Deductible Contributions

The deductible limit for a qualified retirement plan depends on whether you have a defined contribution plan (profit-sharing or money purchase pension plan) or a defined benefit plan. A SEP is treated as a profit-sharing plan subject to the defined contribution plan deduction limits explained below.

If you have a defined benefit plan, you generally may deduct contributions needed to produce the accrued benefits provided for by the plan, including any unfunded current liability. This is a complicated calculation requiring actuarial computations that call for the services of a pension expert.

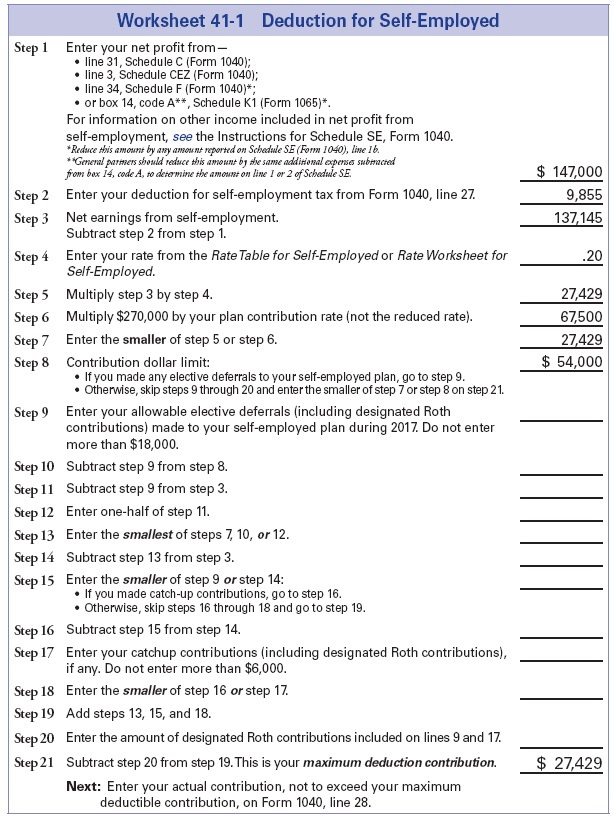

Deductible contribution to a defined contribution qualified retirement plan or a SEP. Before figuring the deductible contribution you can make for2017 to a profit-sharingplan or SEP account, or to a money purchase pension plan, you must first figure your self-employment tax liability on Schedule SE and your deduction for one-halfof theself-employment tax to be claimed on Line 27 of Form 1040. In computing your deductible plan contribution, your net profit from Line 31 ofSchedule C, Line 3 ofSchedule C-EZ, or Line 34 ofSchedule F is reduced by the deduction for one half of your self-employment tax; seethe Example below.

As a self-employed person, you are not allowed to figure the deductible contribution for yourself by applying the contribution rate stated in your plan. The rate must be reduced, as required by law, to reflect the reduction of net earnings by the deductible contribution itself. If your plan rate is a whole number, the reduced percentage is shown in the Rate Table for Self-Employed (Table 41-1) below. If the plan rate is fractional, the reduced percentage is figured using the Fractional Rate Worksheet for Self-Employed (Worksheet 41-2).

Figuring your maximum deductible contribution. After figuring your net earnings and reducing that amount by one-half of your self-employment tax liability, you multiply the balance by the reduced rate from Table 41-1 or Worksheet 41-2. This is generally your maximum deductible contribution to a profit-sharing qualified retirement plan or SEP. However, the maximum deductible contribution cannot exceed the annual limit on additions to a defined contribution plan. The annual limit for 2017 is the lesser of (1) $54,000, or (2) $270,000 (maximum compensation that can be taken into account) multiplied by the stated plan contribution rate, not the reduced rate. Seethe Deduction Worksheet for Self-Employed (Worksheet 41-1) below, which takes you through the steps of figuring your deductible contribution.

If elective deferrals were made during the year, extra steps are required to compute the maximum deductible contribution; seeStep 9 of Worksheet 41-1, shown below. Any “catch-up” contributions are entered in Step 17 of the worksheet.

Table 41-1 Rate Table for Self-Employed

If plan rate is— |

Self-employed person’s reduced rate is— |

1 % |

.009901 |

2 |

.019608 |

3 |

.029126 |

4 |

.038462 |

5 |

.047619 |

6 |

.056604 |

7 |

.065421 |

8 |

.074074 |

9 |

.082569 |

10 |

.090909 |

11 |

.099099 |

12 |

.107143 |

13 |

.115044 |

14 |

.122807 |

15 |

.130435 |

16 |

.137931 |

17 |

.145299 |

18 |

.152542 |

19 |

.159664 |

20 |

.166667 |

21 |

.173554 |

22 |

.180328 |

23 |

.186992 |

24 |

.193548 |

25* |

.200000* |

|

* The maximum deductible percentage for contributions (other than elective deferrals) to your own profit-sharing, money-purchase, or SEP is 20% and for your employees, 25%. |

|

Contributions for your employees. The deduction complications that apply to your own contributions do not apply to contributions for employees. You make contributions for your employees at the rate specified in your plan, based upon their compensation, subject to the annual limit discussed above. Thus, if your plan contribution rate is 25%, you would contribute 25% of your employees’ pay to the plan, even though your own contribution rate is reduced to 20% under the Rate Table for Self Employed shown above. You deduct contributions for employees when figuring your net earnings from self-employment on Schedule C or Schedule F before figuring your own deductible contribution using the steps shown in the Example above.

Contributions allowed after age 70½. You may continue to make contributions for yourself to a qualified retirement plan or SEP as long as you have self-employment income. However, you must begin to receive required minimum distributions from a SEP by April 1 of the year following the year in which you reach age 70½ (8.15). This age 70½ required distribution beginning date also applies to a qualified retirement plan if you are a more-than-5% owner of the business (7.11).

Excess contributions. Contributions to a plan exceeding the deduction ceiling may be carried over and deducted in later years subject to the ceiling for those years. However, if contributions exceed the deductible amount, you are generally subject to a 10% penalty on nondeductible contributions that are not returned by the end of your tax year. The penalty is computed on Form 5330, which must be filed with the IRS by the end of the seventh month following the end of the tax year.

41.5 How To Claim the Deduction for Contributions

Contributions made to your qualified or SEP account as a self-employed person are deducted as an adjustment to gross income on Line 28 of Form 1040. A deduction for a contribution made for your benefit may not be part of a net operating loss.

Contributions for your employees are entered as deductions on Schedule C (or Schedule F) for purposes of computing profit or loss from your business. Trustees’ fees not provided for by contributions are deductible in addition to the maximum contribution deduction.

Deductible plan contributions may generally be made at any time up to the due date of your return, including any extension of time. However, the plan itself must be set up before the close of the taxable year for which the deduction is sought. If you miss the December 31 deadline for setting up a qualified plan, you have at least up to April 17, 2018, to set up a SEP for 2017. If you have a filing extension, you have until the extended due date to set up a SEP and make your contribution.

41.6 How To Qualify a Retirement Plan or SEP Plan

You may set up a qualified retirement plan and contribute to it without advance approval. But since advance approval is advisable, you may, in a determination letter, ask the IRS to review your plan. Approval requirements depend on whether you set up your own administered plan or join a master plan administered by a bank, insurance company, mutual fund, or a prototype plan sponsored by a trade or professional association. If you start your own individually designed plan, you pay the IRS a fee and request a determination letter; seeIRS Publication 560.

If you join a master or prototype plan, the sponsoring organization applies to the IRS for approval of its plan. You should then be given a copy of the approved plan and copies of any subsequent amendments.

To set up a SEP with a bank, broker, or other financial institution, you do not need IRS approval. If you do not maintain any other qualified retirement plan apart from another SEP and other tests are met, a model SEP may be adopted using Form 5305-SEP.

41.7 Annual Qualified Retirement Plan Reporting

Partial relief from one burdensome IRS paperwork requirement may be available if your pension or profit-sharing plan covers only yourself, or you and your spouse, or you and your business partners and the spouses of the partners. Such plans are treated as one-participant plans by the IRS.

A one-participant plan does not file the extensive annual Form 5500 information return. A one-participant plan either files Form 5500-EZ on paper, or if eligible, it may file the form electronically. If a sole proprietor has a plan for employees, file Form 5500-SF.

Under an exception for small one-participant plans, Form 5500-EZ does not have to be filed if the value of plan assets at the end of the year is not more than $250,000. The exception applies if you have two or more one-participant plans that together have not exceeded the $250,000 asset threshold. All one-participant plans must file a Form 5500-EZ for their final plan year even if the plan assets have always been below $250,000.

The filing deadline for 5500 forms is the last day of the seventh month after the end of the plan year unless an extension is obtained; seethe forms instructions. The 5500 forms not filed with the IRS; seethe form instructions for filing electronically or when a paper form can be used.

41.8 How Qualified Retirement Plan Distributions Are Taxed

Distributions from a qualified retirement plan generally may not be received without penalty before age 59½ unless you are disabled or meet the other exceptions listed in 7.13. If you are a more-than-5% owner, you must begin to receive minimum required distributions by April 1 of the year following the year in which you reach age 70½, even though you are not retired; penalties may apply if an insufficient distribution is received (7.11).

A lump-sum and other eligible distributions (7.5) may be rolled over tax free to another employer plan or IRA. For participants born before January 2, 1936, 10-year averaging may be available (7.3). Pension distributions from a defined benefit plan are taxed under the annuity rules discussed in 7.24-7.27, but for purposes of figuring your cost investment, include only nondeductible voluntary contributions; deductible contributions made on your behalf are not part of your investment.

If you receive amounts in excess of the benefits provided for you under the plan formula and you own more than a 5% interest in the employer, the excess benefit is subject to a 10% penalty. The penalty also applies if you were a more-than-5% owner at any time during the five plan years preceding the plan year that ends within the year of an excess distribution.

Other rules discussed in 7.1 – 7.14 apply to self-employed qualified plans as well as qualified corporate plans.

After the death of a self-employed plan owner, distributions from the plan to beneficiaries may be spread over the periods discussed at 7.12provided the plan covers more than one person. Distributions to a surviving spouse can be rolled over to that spouse’s IRA (7.4). Distributions to non-spouse beneficiaries can be directly rolled over in a trustee-to-trustee transfer to an IRA that is treated as an inherited IRA from which required minimum distributions must be received annually (7.6, 8.14).

SEP distributions. Distributions from a SEP are subject to the IRA rules at 8.8.

41.9 SIMPLE IRA Plans

If you do not maintain any other retirement plan and have 100 or fewer employees, you may set up a salary-reduction type of plan for yourself and your employees. The SIMPLE IRA contribution rules are discussed at 8.17. A SIMPLE plan may also be made as part of a 401(k) plan (7.15).

Under a SIMPLE IRA for 2017, you may contribute to your own account $12,500 of net earnings plus an additional $3,000 if age 50 or over by the end of the year. You may also make a “matching” contribution of up to 3% of your net earnings.

If you have employees, they generally could make elective salary-reduction contributions for 2017 up to $12,500 (plus $3,000 if age 50 or over). You must make a 3% matching contribution unless you choose to make a 2% non-elective contribution.

See Chapter 8 for further details on SIMPLE IRAs (8.17 – 8.18).

41.10 Health Savings Account (HSA) Basics

Health savings accounts (HSAs) can be used by individuals covered by a high-deductible health plan (HDHP) to save for health-care costs on a tax-free basis in an IRA-like account. HSAs are intended to supplant Archer MSAs; seethe discussion of Archer MSA rules later in this Chapter (41.13).

The HSA provides a tax-sheltered account for paying routine medical expenses that fall below the deductible set by the HDHP. To contribute to an HSA, you must not be enrolled in Medicare Part A or Part B and you must not be a dependent of another taxpayer.

A qualifying HDHP must have a minimum annual deductible and a maximum annual limit on out-of-pocket costs (see below). HDHPs typically are bronze plans on the government marketplace (see HealthCare.gov).

Generally, contributions to an HSA are not allowed if the taxpayer has coverage under any health plan that does not meet the “high deductible” requirement of an HDHP, but there are exceptions. A plan that otherwise satisfies HDHP rules may provide preventive care benefits without a deductible or with a deductible below the minimum annual deductible. Benefits may also be provided under certain types of “permitted” coverage and insurance before the deductible of the HDHP is satisfied. Permitted coverage includes coverage for vision, dental or long-term care, accidents, and disability. Permitted insurance includes per diem insurance while hospitalized, insurance for a specific disease or illness (such as cancer, diabetes, asthma, or heart failure), and insurance relating to workers’ compensation liability, tort liability, or liabilities relating to owning or using a car or other property.

Qualifying HDHP for 2017. For 2017, the minimum annual HDHP deductible is $1,300 for self-only coverage and $2,600 for family coverage. The limit on out-of-pocket costs for 2017 is $6,550 for self-only coverage and $13,100 for family coverage. The limit applies to co-payments, deductibles, and other payments but not premiums.

41.11 Limits on Deductible HSA Contributions

If you are an eligible individual (41.10), you can set up an HSA with an insurance company, bank, or other financial institution that has been approved by the IRS for this purpose. Contributions can be made up until the due date for filing your tax return (without extensions). Thus, HSA contributions for 2017 can be made through April 17, 2018. HSA contributions are reported to the IRS on Form 5498-SA.

The full contribution limit for 2017 (depending on your coverage; seebelow) is available regardless of when during the year you became eligible (41.10) for an HSA, so long as you were eligible on December 1, 2017; you are treated as if you were enrolled in the December 1 plan for the entire year. However, if you do not remain eligible for the next 12 months (December 1, 2017 through December 31, 2018), and are not disabled, you have to recapture as income on your 2018 return the contribution that could not have been made without the December 1 rule; seePublication 969 and the Form 8889 instructions for details on this recapture rule. If the December 1 rule does not apply, the contribution limit is figured on a monthly basis.

For 2017, the maximum deductible contribution limit for an individual with self-only HDHP coverage is $3,400. For an individual with family coverage, the maximum deductible contribution for 2017 is $6,750. If a married couple has family HDHP coverage and both spouses are eligible for an HSA, they can decide between themselves how to allocate HSA contributions.

The contribution limit is increased for an account owner who is at least age 55 by the end of the year and who has not enrolled in Medicare. The “catch-up” contribution limit is $1,000. However, starting with the month that an individual enrolls in Medicare Part A, B, or Medicare Advantage (generally at age 65), no further contributions, including catch-up contributions, can be made to his or her HSA. For example, if you turned age 65 and enrolled in Medicare in September 2017 and had been contributing to a HDHP with self-only coverage, you can make an HSA contribution for the eight months preceding the month of Medicare enrollment. Since the full-year contribution limit for 2017 would be $4,350 ($3,400 for self-only HDHP plus $1,000 additional for being at least age 55), your contribution limit for eight months (January through August) is $2,933 ($4,400 x 8/12).

You may have more than one HSA, but the above maximum annual contribution limit applies to the aggregate contributions to all of the HSAs.

If you are an employee eligible to contribute and your employer contributes to an HSA on your behalf, employer contributions within the limit are excludable from your income (3.2). If your employer’s contribution is below the applicable limit, you may contribute to your HSA but the totals of all the contributions cannot exceed the applicable limit.

Contributions exceeding your applicable HSA limit are not deductible and are subject to a 6% excise tax. Contributions by an employer to an employee’s HSA in excess of the limit are includible in the employee’s income and subject to the excise tax. However, the excise tax can be avoided by a timely withdrawal of the excess contribution and any allocable income. The withdrawal deadline is generally the filing due date including extensions, or April 17, 2018, for an excess 2017 contribution. However, if you timely file without making the withdrawal, you may do so by October 15, 2018. On a timely withdrawal, the income is taxed in the year withdrawn but the excise tax does not apply and the distribution of the excess contribution is not taxed. Seethe instructions to Form 5329 for further details.

Use Form 8889 to report your HSA contributions and figure your deduction. You must report your HSA contributions for 2017 and apply the deduction limits on Form 8889, which must be attached to Form 1040. The deduction from Form 8889 is entered on Line 25 of Form 1040, where it is deductible “above the line” from gross income.

41.12 Distributions From HSAs

Earnings accumulate tax free within an HSA, as with an IRA. Distributions from an HSA used exclusively to pay or reimburse qualified medical expenses of the account owner, his or her spouse, or dependents are not taxable. Distributions used for anything other than qualified medical expenses are taxable. Taxable distributions are also subject to a 20% penalty unless the distribution is made after the account owner becomes disabled, reaches age 65, or dies.

Distributions need not be taken in the year in which the expense is incurred to be tax free; they can be taken in the following year or in any later year. This may be necessary if there are insufficient funds to cover the expense at the time it is incurred. For example, an HSA account holder who incurs a $1,500 medical expense on December 1, 2017, can wait until 2018 (or later) when the account balance exceeds $1,500. The distribution is tax free so long as records are kept to show that the distribution was used to reimburse qualified medical expenses that were not covered by insurance or otherwise reimbursed and not claimed in a prior year as an itemized deduction. The HSA must have been set up before the expense was incurred.

For tax-free distribution purposes, a “qualified medical expense” is generally a non-reimbursed payment for medical care that would otherwise be eligible for an itemized deduction (17.2). In addition, over-the-counter medications for which you get a doctor’s prescription are qualified medical expenses for HSA purposes although they are not eligible for an itemized deduction. Health-care premiums generally do not qualify for HSA purposes, but there are exceptions. An HSA can pay for premiums for long-term-care insurance, COBRA health-care continuation coverage, health coverage while an individual is receiving unemployment compensation, and for individuals over age 65, Medicare Part A, B, or D, Medicare Advantage, and the employee share of premiums for employer-sponsored health insurance including retiree health insurance. HSA distributions used to pay or reimburse long-term-care premiums are tax free only to the extent of the age-based deductible limit for such premiums (17.5). For example, if a person age 41 uses HSA funds to pay long-term-care premiums of $1,800 in 2017, only $770 (the deductible limit for those age 41 through 50 in 2017) is tax free. The balance of the distribution is taxable and subject to a 20% penalty for withdrawal of funds prior to age 65.

A qualified medical expense may be for the care of the account owner, his or her spouse, or dependents, without regard to whether they are eligible to make HSA contributions. In the case of a married couple where both spouses have HSAs, one spouse may use a distribution from his or her HSA to pay or reimburse the qualified medical costs of the other spouse. However, both HSAs may not reimburse the same expense.

If an HSA account holder mistakenly takes a distribution such as to reimburse an expense he or she reasonably but mistakenly believes is a qualified medical expense, the funds can be repaid to the HSA in order to avoid tax on the withdrawn amount, assuming the plan accepts a return of mistaken distributions. The funds must be returned by April 15 of the year following the first year that the account holder knew or should have known of the mistake.

Inherited HSAs. If the beneficiary of an HSA is the surviving spouse of the deceased account owner, the surviving spouse becomes the owner of the account and will be subject to tax only on distributions that are not used for qualified medical expenses. If the beneficiary is not the surviving spouse, the account ceases to be an HSA as of the date of the owner’s death and the date-of-death value of the HSA assets must be included in the beneficiary’s income. The beneficiary (other than the decedent’s estate) may reduce the taxable amount by any HSA payments for the decedent’s medical expenses made within one year after death. A beneficiary is not subject to the penalty for taxable distributions.

Report HSA distributions on Form 8889. You must report an HSA distribution on Part II of Form 8889, which must be attached to Form 1040. A taxable distribution, if any, from Form 8889 is reported on Line 21 of Form 1040 (“Other income”). On the dotted line next to Line 21 enter “HSA” and the amount. If there is a taxable distribution and no exception to the penalty is available, the 20% penalty is entered on Form 8889 and reported on Line 62 of Form 1040. On the dotted line next to Line 62, enter “HSA” and the amount. The HSA custodian or trustee will report the distribution to the IRS on Form 1099-SA.

41.13 Archer MSAs

Archer MSAs (medical savings accounts) have largely been replaced by health savings accounts (HSAs). The law authorizing the establishment of new Archer MSAs has expired. However, taxpayers who set up Archer MSAs before 2008 can continue to fund them.

An Archer MSA can be rolled over to an HSA. Contributions may not be made to an Archer MSA or to an HSA after you become entitled to Medicare benefits.

For 2017, a high-deductible health plan for self-only coverage must have a deductible of at least $2,250 and no more than $3,350. For family coverage, the deductible must be at least $4,500 and no more than $6,750. The high-deductible plan must limit out-of-pocket costs (other than premiums) for 2017 to $4,500 for self-only coverage and $8,250 for family coverage. You generally may not have any other coverage in addition to the high-deductible plan, but separate policies are allowed for disability, vision or dental care, long-term care, accidental injuries, specific diseases or illnesses, fixed payments during hospitalization, workers’ compensation liability, tort liability, and liabilities arising from the ownership or use of property.

Deductible contribution limit. If you are self-employed, the maximum deductible contribution is 65% of the annual policy deductible if you have self-only coverage under a high-deductible plan, and 75% of the annual policy deductible if you have family coverage. To deduct the maximum amount, you must have the policy for the entire year. Otherwise one-twelfth of the limit may be deducted for each full month of coverage. The deduction may not exceed your net self-employment income from the business through which you have the high-deductible insurance.

If you are an employee of an MSA-participating employer and your employer makes any contributions to your Archer MSA, you are barred from making a deductible contribution; also seethe Caution on employer contributions to a spouse’s Archer MSA. Your employer’s contribution to your Archer MSA is not taxable to you if it is within the 65%/75% limit discussed above (3.2).

Report contributions to your Archer MSA on Form 8853, which must be attached to your Form 1040. The deductible contribution shown on Form 8853 is entered on Line 36 of Form 1040; write “MSA” next to the entry.

Distributions from Archer MSA. You can take a distribution from your Archer MSA to pay for medical expenses that are not reimbursable under your high-deductible plan. For distribution rules, see 41.12.

41.14 Small Employer Health Insurance Credit

If you pay at least half of the premiums for your staff and you meet eligibility requirements, you can claim a tax credit of 50 percent of your eligible payments on Form 8941. The credit is highly complex.

Eligibility.You must meet these four tests for a 2017 credit:

- You have fewer than 25 full-time equivalent employees (FTEs) for the tax year. Add up the hours per year (but not more than 2,080 hours per employee) that employees (other than owners, relatives, and seasonal workers) work and divide by 2,080 to find the number of full-time equivalents.

- The average annual wages of its employees for the year is less than $52,400 per FTE.

- You must pay the premiums under a “qualifying arrangement.”

- You purchase the coverage through a government Marketplace.

Credit amount. A full credit applies if you have no more than 10 FTEs with average wages of $26,200 per FTE. The credit phases out for those with 10 to 25 FTEs and with wages of $26,200 to $52.400.

The credit is based on the lesser of actual payments or the average premium for the small group market in the states where your employees work. The 2017 average premiums will be listed on a county-by-county basis for each state in the Form 8941 instructions.