Chapter 45

Figuring Self-Employment Tax

Self-employment tax provides funds for Social Security and Medicare benefits. The self-employment tax is calculated on Schedule SE. You are required to prepare Schedule SE if you have self-employment net earnings of $400 or more in 2017, but you will not incur the tax unless your net self-employment earnings exceed $433.13. The tax is added to your income tax liability. When preparing your estimated tax liability, you must also include an estimate of self-employment tax; see Chapter 27.

On Schedule SE, self-employment income is reduced by a deduction reflected in the decimal of .9235 listed on the form. You also deduct the employer-equivalent portion of the self-employment tax on Line 27 of Form 1040.

For 2017, the self-employment tax of 15.3% consists of the following two rates: 12.4% for Social Security and 2.9% for Medicare. After multiplying the net earnings by .9235, the combined 15.3% rate applies to a taxable earnings base of $127,200 or less; the 2.9% rate applies to all taxable earnings exceeding $127,200.

You are required to pay self-employment tax on self-employment income even after you retire and receive Social Security benefits.

45.1 What Is Self-Employment Income?

On Schedule SE, you generally figure self-employment tax on the net profit from your business or profession whether you participate in its activities full or part time. Net profit is generally the amount shown on Line 31 of Schedule C (or Line 3 of Schedule C-EZ) if you are a sole proprietor. If you are a partner, net earnings subject to self-employment tax are taken from Box 14, Schedule K-1, of Form 1065. If you are a farmer, net farm profit is shown on Line 34, Schedule F.

If you have more than one self-employed operation, your net profit from all the operations is combined. A loss in one self-employed business will reduce the income from another business. You file separate Schedules C for each operation and one Schedule SE showing the combined income (less losses, if any).

For self-employment tax purposes, net earnings are not reduced by deductible contributions to your own SEP or self-employed qualified retirement plan (41.4).

Married couples. Where you and your spouse each have self-employment income, each spouse must figure separate self-employment income on a separate Schedule SE. Each pays the tax on the separate self-employment income. Both schedules are attached to the joint return.

If you live in a community property state, business income is not treated as community property for self-employment tax purposes. The spouse who is actually carrying on the business is subject to self-employment tax on the earnings.

Qualified joint venture election by spouses. If you and your spouse are the only members of a business that you jointly own and operate, you each materially participate in the business, and you file a joint return, you can make a joint election to file as sole proprietors on Schedule C (“qualified joint venture election”) instead of as a partnership. You make the joint venture election by filing separate Schedule Cs or C-EZs on which you each report your respective share (according to respective ownership interests) of the business income, gains, losses, deductions, and credits. If you make the election, each of you must file a separate Schedule SE to figure self-employment tax on your share of the joint venture income.

However, the reporting rule is different if you are making the election for a rental real estate business. In that case, use Schedule E instead of Schedule C. On one Schedule E, you each report your respective interests in the qualified joint venture and divide the income, gains, losses, deductions, and credits between you; check the "QJV" box on Schedule E and see the instructions. Since rental real estate income is generally not subject to self-employment tax (see exception 1 below), you do not have to file Schedule SE unless you have other income that is subject to self-employment tax.

Exceptions to self-employment tax. The following types of income or payments are not included as self-employment income on Schedule SE:

- Rent from real estate is generally not self-employment income. However, self-employment tax applies to the business income of a real estate dealer or income in a rental business where substantial services are rendered to the occupant, as in the leasing of—

- Rooms in a hotel or in a boarding house.

- Apartments, but only if extra services for the occupants’ convenience, such as maid service or changing linens, are provided.

- Cabins or cabanas in tourist camps where you provide maid services, linens, utensils, and swimming, boating, fishing, and other facilities, for which you do not charge separately.

- Farmland in which the landlord materially participates in the actual production of the farm or in the management of production. For purposes of “material participation,” the activities of a landlord’s agent are not counted, only the landlord’s actual participation.

- Capital gains are not self-employment income. Self-employment income does not include gains from the sale of property unless it is inventory or held for sale to customers in the ordinary course of business. Thus, traders in securities who buy and sell securities for their own account do not treat net gains or losses from the sales as self-employment income or loss. Dealers in commodities and options are subject to self-employment tax see Table 45.1.

- Dividends and interest. Generally, dividends and interest are not self-employment income. However, dividends earned by a dealer in securities and interest on accounts receivable are treated as self-employment income if the securities are not being held for investment. A dealer is one who buys stock as inventory to sell to customers.

- Conservation Reserve Program payments received by farmers receiving Social Security retirement or disability benefits. These payments reduce net farm profit reported on Schedule SE.

- Certain family-related compensation. Payments you receive from an insurance company or government program as a family caregiver are not treated as self-employment income unless you are in the trade or business of being a caregiver. Similarly, executor fees for handling an estate are not considered self-employment income unless you are in the business of regularly acting as an executor for estates.

Net operating loss deduction. A loss carryover from past years does not reduce business income for self-employment tax purposes. Similarly, the personal exemption may not be used to reduce self-employment income.

Statutory employees. Wages of a statutory employee, such as a full-time life insurance salesperson (40.6), are not subject to self-employment tax, as Social Security and Medicare tax have been withheld.

Farmers. A share farmer's part of the profit from crops on land owned by another is self-employment income.

Business interruption proceeds. The IRS and the Tax Court disagree over whether business interruption insurance proceeds must be reported as earnings subject to self-employment tax. The Tax Court held that insurance payments made to a grocer as compensation for lost earnings due to a fire were not subject to self-employment tax because the payment was not for actual services. The IRS refuses to follow the decision, holding that such payments represented income that would have been earned had business operations not been interrupted.

45.2 Partners Pay Self-Employment Tax

A general partner includes his or her share of partnership income or loss in net earnings from self-employment, including guaranteed payments. If your personal tax year is different from the partnership’s tax year, you include your share of partnership income or loss for the partnership tax year ending within 2017.

A limited partner is not subject to self-employment tax on his or her share of partnership income except for guaranteed payments for services performed, which are subject to the tax.

If a general partner dies within the partnership’s tax year, self-employment income includes his or her distributive share of the income earned by the partnership through the end of the month in which the death occurs. This is true even though his or her heirs or estate succeeds to the partnership rights. For this purpose, partnership income for the year is considered to be earned ratably each month.

Retirement payments from partnership. Retirement payments you receive from your partnership are not subject to self-employment tax if the following conditions are met:

- The payments are made under a qualified written plan providing for periodic payments on retirement of partners with payments to continue until death.

- You rendered no services in any business conducted by the partnership during the tax year of the partnership ending within or with your tax year.

- By the end of the partnership’s tax year, your share in the partnership’s capital has been paid to you in full, and there is no obligation from the other partners to you other than with respect to the retirement payments under the plan.

Limited liability company (LLC) members. Are LLC members treated as general or limited partners for purposes of self-employment tax? The matter is not completely settled, but it appears that members owe self-employment tax when they perform services for their business, participate in management activities, and are not mere investors.

45.3 Schedule SE

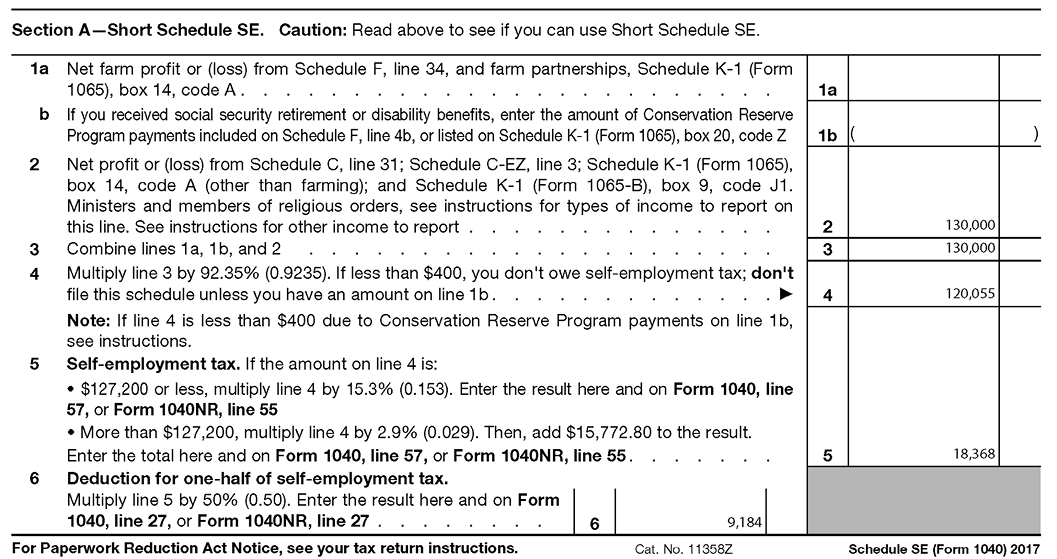

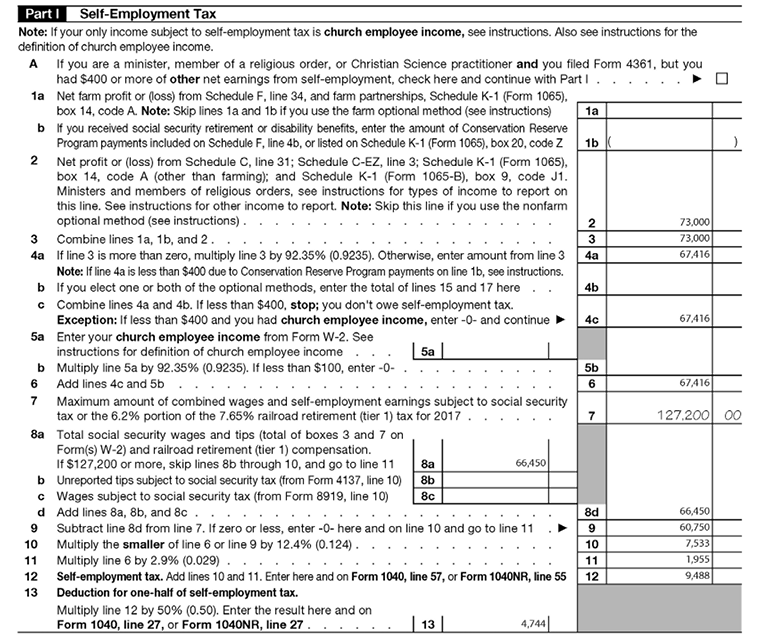

Schedule SE has an introductory “road map” designed to lead you to either the short or long version of Schedule SE. Once you pass through the road map, the preparation of either the short or long schedule for 2017 is not difficult. On both schedules, you reduce your net profit by .9235 to get your net earnings from self-employment. In other words, only 92.35% of the net earnings is subject to self-employment tax. The .9235 adjustment is the equivalent of a 7.65% reduction to net earnings, which, along with the income tax deduction for one-half of self-employment tax on Line 27 of Form 1040, attempts to place self-employed individuals on the same level as employees subject to FICA taxes.

The .9235 adjustment is made on Line 4 of either the short or long Schedule SE. After the .9235 adjustment is made, net earnings are subject to the 12.4% and 2.9% rates, assuming the resulting net earnings are $400 or more. For 2017, the 12.4% Social Security rate applies to the first $127,200 of net earnings and the 2.9% Medicare rate applies to all of the net earnings.

Worksheet—Short Schedule SE

45.4 How Wages Affect Self-Employment Tax

If you have both net earnings from self-employment and also wage and/or tip income subject to FICA taxes (Social Security and Medicare), the amount of such FICA earnings may affect your self-employment tax liability.

If your 2017 FICA wages or tips were $127,200 or over, your net self-employment earnings (after the .9235 adjustment) are subject only to the 2.9% Medicare rate. If the total of your 2017 FICA wages (and tips) and net self-employment earnings was $127,200 or less, all of your net earnings are subject to the 12.4% Social Security rate and the 2.9% Medicare rate.

If your 2017 FICA wages or tips were under $127,200, but the total of the wages and tips plus your 2017 net earnings was over the $127,200 limit for the 12.4% Social Security rate, the 12.4% rate applies to the lesser of: (1) Line 6 of the Long Schedule SE, which shows your net self-employment earnings (after the .9235 adjustment), or (2) Line 9 of the Long Schedule SE, which shows the excess of $127,200 over the FICA wages and tips. The 2.9% Medicare rate applies to the entire amount of net self-employment earnings. See the following Example and the filled-in long Schedule SE worksheet below.

Worksheet—Long Schedule SE

45.5 Optional Method If 2017 Was a Low-Income or Loss Year

The law provides a small increased tax base for Social Security coverage if you have a low net profit or a net loss. The increased tax base is provided by an optional method and is figured in Part II of Section B of Schedule SE. One optional method is for nonfarm self-employment and another for farm income. You may not use the optional method to report an amount less than your actual net earnings from nonfarm self-employment.

Nonfarm optional method. You may use the nonfarm optional method for 2017 if you meet all the following tests:

| Test 1. | Your net earnings (profit) from nonfarm self-employment on Line 31 of Schedule C, Line 3 of Schedule C-EZ, or Box 14 (Code A) of Schedule K-1 (Form 1065) are less than $5,631. |

| Test 2. | Your net nonfarm profits are less than 72.189% of your gross nonfarm income. |

| Test 3. | You had net earnings from self-employment of $400 or more in at least two of the following years: 2014, 2015 and 2016. |

| Test 4. | You have not previously used this method for more than four years. There is a five-year lifetime limit for use of the nonfarm optional base. The years do not have to be consecutive. |

If your net profit from all nonfarm trades or businesses is less than $5,631 and also less than 72.189% of gross nonfarm income, and you have no gross farm income, you may report two-thirds of the gross income from your nonfarm business, but no more than $5,200, as net earnings from self-employment for 2017.

Optional farm method. If you have farming income (other than as a limited partner) you may use the farm optional method to figure your net earnings from farm self-employment.

You can use the farm optional method for 2017 only if your gross farm income was not more than $7,800 or your net farm profits were less than $5,631.

You may report the smaller of two-thirds of your gross income or $5,200 as your net earnings from farm self-employment.

Farm income includes income from cultivating the soil or harvesting any agricultural commodities. It also includes income from the operation of a livestock, dairy, poultry, bee, fish, fruit, or truck farm, or plantation, ranch, nursery, range, orchard, or oyster bed, as well as income in the form of crop shares if you materially participate in production or management of production.

45.6 Self-Employment Tax Rules for Certain Positions

Table 45-1 Self-Employed or Employee?

| If you are— | Tax rule— |

Babysitter |

Where you perform services in your own home and determine the nature and manner of the services to be performed, you are considered to have self-employment income. However, where services are performed in the parent’s home according to instructions by the parents, you are an employee of the parents and do not have self-employment earnings. In one case, the Tax Court held that grandparents who provided care only for their own grandchildren and received payments from a state-sponsored childcare assistance program had to pay income tax on the payments, but the payments were not subject to self-employment tax because the grandparents' primary purpose in providing the care was not to make a profit. |

Clergy |

If you are an ordained minister, priest, or rabbi, a member of a religious order who has not taken a vow of poverty, or a Christian Science practitioner, you are subject to self-employment tax, unless you elect not to be covered on the grounds of conscientious or religious objection to Social Security benefits. An application for exemption from Social Security coverage must be filed on Form 4361 by the due date, including extensions, of your income tax return for the second taxable year for which you have net earnings from services of $400 or more. An exemption, once granted, is irrevocable. Self-employment tax does not apply to the rental value of any parsonage or parsonage allowance provided after retirement. Other retirement benefits from a church plan are also exempted. |

Consultant |

The IRS generally takes the position that income earned by a consultant is subject to self-employment tax. The IRS has also held that a retired executive hired as a consultant by his former firm received self-employment income, even though he was subject to an agreement prohibiting him from giving advice to competing companies. According to the IRS, consulting for one firm is a business; it makes no difference that you act as a consultant only with your former company. The IRS has also imposed self-employment tax on consulting fees, although no services were performed for them. The courts have generally approved the IRS position. |

Dealer in commodities and options |

Registered options dealers and commodities dealers are subject to self-employment tax on net gains from trading in Section 1256 contracts, which include regulated futures contracts, foreign currency contracts, dealer equity options, and non-equity options. Self-employment tax also applies to net gains from trading property related to such contracts, like stock used to hedge options. |

Director |

You are taxed as a self-employed person if you are not an employee of the company. Fees for attendance at meetings are self-employment income. If the fees are not received until after the year you provide the services, you treat the fees as self-employment earnings in the year they are received. |

Employee of foreign government or international organization |

If you are a U.S. citizen and you work in the United States, Puerto Rico, the Virgin Islands, American Samoa, the Commonwealth of the Northern Mariana Islands, or Guam, for a foreign government or its wholly owned instrumentality, or an international organization, you pay self-employment tax on your earnings if Social Security and Medicare taxes are not withheld from your pay. |

Executor or guardian |

If you are a professional fiduciary, your fees will always be treated as self-employment income, regardless of the assets held by the estate. But if you serve as a nonprofessional executor or administrator for the estate of a deceased friend or relative, your fees will not be treated as self-employment income unless all of the following tests are met: (1) the estate includes a business; (2) you actively participate in the operation of the business; and (3) all or part of your fee is related to your operation of the business. The IRS applied similar business tests to deny self-employment treatment for a guardian who was appointed by a court to care for a disabled cousin. The guardian negotiated sales of the cousin’s property and invested the proceeds, but these activities were not extensive enough to be considered management of a business. |

Former insurance salespersons |

Termination payments by a former insurance salesperson may be exempt from self-employment tax. They must be received from an insurance company after the termination of a services agreement. No services may be performed for the company after the agreement ends and before the end of the tax year. The payments must be conditioned on the salesperson’s entering into a covenant not to compete with the company for at least one year after termination. The amount of the payment must be primarily based on policies sold by (or credited to) the salesperson during the last year of the services agreement or on the period for which such policies remain in force after the termination. |

Lecturer |

You are not taxed as a self-employed person if you give only occasional lectures. If, however, you seek lecture engagements and get them with reasonable regularity, your lecture fees are treated as self-employment income. |

Nonresident alien |

You generally do not pay Social Security tax on your self-employment income derived from a trade, business, or profession in the United States. This is so even though you pay income tax. However, an international agreement between the United States and another country might provide that you are covered under the U.S. Social Security system, in which case, you are subject to self-employment tax. In the absence of such an agreement, you are exempt from self-employment tax even if your business in the United States is carried on by an agent, employee, or partnership of which you are a member. However, if you live in Puerto Rico, the Virgin Islands, American Samoa, the Commonwealth of the Northern Mariana Islands, or Guam, you are not considered a nonresident alien and are subject to self-employment tax. |

Nurse |

If you are a registered nurse or licensed practical nurse who is hired directly by clients for private nursing services, you are considered self-employed. You are an employee if hired directly by a hospital or a private physician and work for a salary following a strict routine during fixed hours, or if you provide primarily domestic services in the home of a client. Where registered or licensed practical nurses are assigned nursing jobs by an agency that pays them, the IRS, in several rulings, has treated such nurses as employees of the agency. Nurses’ aides, domestics, and other unlicensed individuals who classify themselves as practical nurses are treated by the IRS as employees, regardless of whether they work for a medical institution, a private physician, or a private household. |

Real estate agent or door-to-door salesperson |

Licensed real estate agents are considered self-employed if they have a contract specifying that they are not to be treated as employees and if substantially all of their pay is related to sales rather than number of hours worked. The same rule also applies to door-to-door salespeople with similar contracts who work on a commission basis selling products in homes or other non-retail establishments. |

Technical service contractor |

Consulting engineers and computer technicians who receive assignments from technical service agencies are generally treated as employees and do not pay self-employment tax. The IRS distinguishes between (1) technicians who in three-party arrangements are assigned clients by a technical services agency and (2) those who directly enter into contracts with clients. Employee status covers only technicians in Group 1. Technical specialists who contract directly with clients may be classified as independent contractors by showing that they have been consistently treated as independent contractors by the client, and that other workers in similar positions have also been treated as independent contractors. Thus, they may treat their income as self-employment income. Firms that are treated as employers of technical specialists are responsible for withholding and payroll taxes. |

Traders in securities |

Gains and losses from a trading business are not subject to self-employment tax. |

Writer |

Royalties from writing books are self-employment income to a writer. Royalties on books by a professor employed by a university may also be self-employment income despite employment as a professor. |