CHAPTER 3

Taxation of Partnerships and Joint Ventures

- § 3.1 Scope of Chapter

- § 3.3 Classification as a Partnership

- § 3.4 Alternatives to Partnerships

- § 3.7 Formation of Partnership

- § 3.8 Tax Basis in Partnership Interest

- § 3.9 Partnership Operations

- § 3.10 Partnership Distributions to Partners (New)

- § 3.11 Sale or Other Disposition of Assets or Interests

- § 3.12 Other Tax Issues

§ 3.1 SCOPE OF CHAPTER

p. 195. Insert the following at the end of this subsection:

(a) Treatment of Business Income to Noncorporate Taxpayers

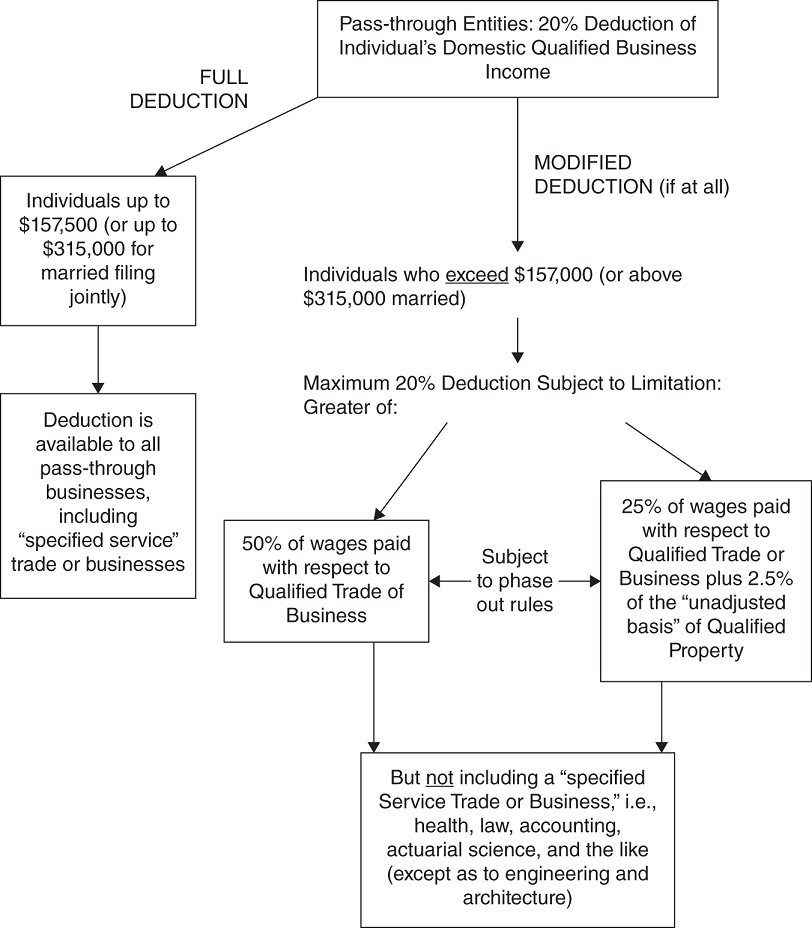

For tax years beginning after 2017 (subject to a sunset at the end of 2025), the 2017 Tax Act (Pub. L. No. 115-97) (the “Tax Act”) will allow an individual taxpayer (including a trust or estate) who participates in a joint venture with a nonprofit a deduction of 20 percent of the individual's domestic qualified business income of a partnership, S Corp, or sole proprietorship.

An individual's qualified business income is the net amount of domestic qualified items of income, gain, loss, and deduction with respect to a taxpayer's “qualified business.” Qualified business generally is defined to include any trade or business other than a “specified service trade or business,” which includes any trade or business activity involving the performance of services in the field of health, law, accounting, actuarial signs, performing arts, consulting, athletics, financial services, brokerage services, and any trade or business the principal asset of which is “reputation or skill” of one or more of its owners or employees. Engineering and architecture are excluded from the limitation.

There is an important limitation, however: the deduction is subject to a limit based either on wages paid or wages paid plus a capital element. Specifically, the limitation is the greater of (i) 50 percent of wages paid with respect to a qualified trade or business or (ii) the sum of 25 percent of the W-2 wages with respect to a qualified business plus 2.5 of the unadjusted basis (determined immediately after the acquisition) not including land of all qualified property. The latter additional modification apparently has been added as a result of the real estate industry, although it presents significant accounting issues, including a determination of the remaining useful life of property.

EXAMPLE: EO and taxpayer (T) enter into an equal joint venture in an LLC to be taxed as a partnership, organized to train unemployed handicapped high school graduates. T's allocable share of the net operating income from the LLC is $150,000 for 2018. T also earns $600,000 of taxable income from sources unrelated to the handicap business, which subjects him to the maximum tax bracket. The LLC pays its employees $50,000 in wages during 2018 and has $300,000 in unadjusted basis in its equipment used in the business for which the recovery period for depreciation purposes is under § 168.

T's deduction under § 199(A) is equal to the lesser of (1) 20 percent of T's allocable share of qualified income from the trade or business (which is not a “specified service” business otherwise excluded) or (2) the greater of (a) 50 percent of T's allocable share of W-2 wages paid by the LLC or (b) 25 percent of T's allocable share of W-2 wages paid by the LLC, plus 2.5 percent of the unadjusted basis of qualified property used in the LLC's trade or business. Based on T's 50 percent ownership, the initial computation under § 199(A) would allow a deduction equal to 20 percent of $75,000, or $15,000 as an initial deduction. However, pursuant to the restriction that provides a limitation equal to the greater of the following: 50 percent of T's $25,000 share of W-2 wages paid by the LLC ($12,500) or 25 percent of T's $25,000 share of W-2 wages paid by the LLC ($6,250) plus 2.5 percent of T's $150,000 share of the unadjusted basis of the qualified property held by the LLC ($3,750), as a result, T's deduction under § 199(A) is capped at $10,000, which is less than $15,000 under the general rule.

§ 3.3 CLASSIFICATION AS A PARTNERSHIP

(b) Overview of the Check-the-Box Regulations

(iv) Consequences of Electing to Change Classification p. 203. Add quotation marks around the first sentence under paragraph (D).

(f) IRS Analysis: The Double-Prong Test and Rev. Rul. 98-15

(vi) United Cancer Council p. 214. The citation in footnote 76 should be deleted and replaced with the following:

109 T.C. 326 (Dec. 2, 1997).

§ 3.4 ALTERNATIVES TO PARTNERSHIPS

(b) Title-Holding Companies

p. 218. Add the following to the end of footnote 91:

See subsection § 13.6(w)(v) regarding the use of a title-holding company as a QALICB.

§ 3.7 FORMATION OF PARTNERSHIP

(b) Partnership Interest in Exchange for Services

p. 233. Insert the following at the end of this subsection:

New § 1061 provides a special rule for taxpayers holding an applicable partnership interest, which generally is a partnership interest transferred to or held by a taxpayer in connection with the performance of substantial services by the taxpayer in any “applicable trade or business,” the latter of which encompasses any activity conducted on a regular, continuous, and substantial basis, which consist of (a) raising or returning capital and (b) investing in or developing a range of specified assets consisting of a broad range of financial investments, including securities, commodities, option, derivatives, and cash equivalents as well as real estate held for rent or investment. See § 1061(c)(2), (3). Section 1061 lengthens the holding period for determining long-term capital gain in this context, by imposing a three-year holding period for long-term treatment.

§ 3.8 TAX BASIS IN PARTNERSHIP INTEREST

(a) Loss Limitation

p. 233. Insert the following at the end of footnote 162:

The Tax Act added § 704(d)(3) to provide generally that the limitation takes into account the borrower's share of charitable contribution as defined in § 170(c) and foreign taxes described in § 901.

(b) Basis

(ii) Partnership's Basis in Its Assets (Inside Basis) p. 236. Insert the following as footnote 169.1 to the first sentence of the second paragraph of this subsection:

169.1 Proposed regulations (January 2014) provide that, if a partnership has a substantial built-in loss immediately after the transfer of a partnership interest, the partnership is treated as having a § 754 election in effect for the taxable year in which the transfer occurs, but only with respect to that transfer. Prop. Reg. § 1.743-1(k)(1)(iii).

(c) Liabilities and Economic Risk of Loss

p. 239. Insert the following as footnote 171.1 at the end of the first full paragraph on this page:

171.1 Proposed regulations would overhaul this safe harbor by permitting partners to specify their interests in partnership profits only if those interests are based on the partners' “liquidation value percentages.” A partner's liquidation value percentage is determined under a “liquidation value test,” which looks to the amount a partner would be entitled to receive if all of the partnership property were sold for fair market value and each partner received his or her proportionate share of the proceeds. Once that amount is determined for each partner, the figure is converted to a percentage by dividing the liquidation value to be received by each partner by the combined liquidation value to be received by all partners.

p. 240. Add the following to the end of footnote 182:

Due to the IRS's concern that “some partners or related persons have entered into payment obligations that are not commercial solely to achieve an allocation of a partnership liability to such partner,” on January 30, 2014, the IRS proposed new regulations under § 752, Notice of Proposed Rulemaking, REG-119305, 2014-9 I.R.B. 524, 523. The proposed regulations eliminate the presumption that partners will be called upon to satisfy their contractual payment obligations. Instead payment obligations will be respected for § 752 purposes only if the partner satisfies a host of conditions, which include maintenance of reasonable net worth, commercially reasonable documentation, and reasonable arm's-length considerations, inter alia. Prop. Reg. § 1.752-2(b)(3)(ii).

§ 3.9 PARTNERSHIP OPERATIONS

(d) Transactions between Partner and Partnership

(i) Payments to Partner Acting in Capacity as Nonpartner p. 246. Insert the following to the end of footnote 206:

See subsection 16.7(e).

(ii) Sale of Property between Partnership and Related Party p. 248. Insert the following at the end of the second full paragraph on this page: Moreover, the transfer of tax credits in exchange for capital contribution may also be treated as a disguised sale.215.1

p. 249. Add the following to the end of footnote 217:

In July 2015, the IRS issued proposed regulations under § 707 to provide guidance on when certain partnership arrangements should be treated as disguised payments for services rather than distributive shares of partnership income. Generally, the proposed regulations apply a “facts and circumstances” test to determine whether certain transactions are disguised payments for services. Prop. Reg. § 1.707-2. It appears that the most important factor is whether the arrangement lacks significant entrepreneurial risk to the service provider relative to the overall entrepreneurial risk of the partnership at the time the parties enter into or modify the arrangement. Prop. Reg. § 1.707-2(c).

§ 3.10 PARTNERSHIP DISTRIBUTIONS TO PARTNERS (NEW)

p. 251. Insert the following new paragraph after the first full paragraph on the page:

The term “waterfall” is often used relative to the distribution section in partnership agreements and limited liability company agreements to define the manner in which distributions flow from the investment to the limited partners/members, and dictate the terms of the sponsor's incentive fee or carried interest. Agreements also frequently include “claw back” provisions that may come into effect when subsequent circumstances are inconsistent with the prior distributions. There are many different structures and variations for defining waterfalls and claw backs, each leading to different economic consequences for limited partners/members. The partners need to understand how these mechanisms work, as an unfavorable waterfall can tilt risk toward the limited partners/nonmanaging members, including exempt organizations. Variations in the structure can alter the economic results and can impact the overall economic deal.

§ 3.11 SALE OR OTHER DISPOSITION OF ASSETS OR INTERESTS

(c) Termination of the Partnership

p. 258. Insert the following at the end of the subsection:

The Tax Act eliminates the “technical termination” under former § 708(b)(1). In effect, the partnership will no longer be terminated by the sale of a partnership interest, assuming the entity continues to have more than one partner.

(d) Liquidating Distributions

p. 259. Insert the following as footnote 261.1 at the end of the first full paragraph on this page:

261.1 Proposed regulations (January 2014) provide that, if a liquidating distribution results in a substantial basis reduction (greater than $250,000), the partnership is treated as having an election under § 754 in effect for the year in which the distribution occurs, but only with respect to the distribution to which the substantial basis reduction relates. Prop. Reg. § 1.734-1(a)(2).

(f) Application of Bargain Sale Technique to “Burned Out” Shelters

p. 260. Insert the following as footnote 266.1 at the end of the second sentence in the first paragraph of this subsection:

266.1 See discussion regarding contributions of LLC partnership interest to charities in subsection 2.11(f).

§ 3.12 OTHER TAX ISSUES

(c) Passive Activity Loss Rules

p. 269. Insert the following at the end of the subsection:

The Tax Act added new § 461(l), which disallows a current deduction for “excess business losses” of individuals who are noncorporate taxpayers. This limitation applies after the application of the passive activity loss rules of § 469 and applies to partners who materially participate in a business activity that operates at a loss. The limitation applies at the partner level, to the partner's distributive share of all tax items from trades or businesses attributable to the entity. See § 461(l)(4). However, any disallowed excess business loss may be carried forward and treated as part of the taxpayer's net operating loss carryforward in subsequent years, subject to the new rule allowing NOLs up to 80 percent of taxable income for losses arising in taxable years beginning after December 31, 2017.

(f) Unified Audits and Adjustments

p. 272. Insert the following at the end of this subsection:

New Partnership Audit Rules.319.1 The new Bipartisan Budget Act of 2015 repealed the current TEFRA unified partnership and electing large partnership (ELP) rules with a new streamlined audit approach, the effect of which is that adjustments of income, gain, loss, deduction, or credit determined at the partnership level and the taxes attributable thereto will be assessed and collected at the partnership level. The new law is effective for taxable years beginning after January 1, 2018; however, small partnerships may opt out, and any partnership may elect to apply the new law before such date.

The final regulations, which were published in February 2019, provide that a partnership will not be eligible to elect out of the new partnership regime if it has a partner that is itself a partnership or disregarded entity, such as a disregarded single-member LLC or grantor trust.319.2

The partnership may also have to substantiate the tax status of the partners, including shareholders that are S Corporations, to make this election.

In order to elect out of the partnership audit regime for a particular tax year, the partnership must make the election on a timely filed partnership return (including extensions) for the tax year in which the election relates. In addition, the partnership must provide:

- Name

- Taxpayer Identification Number

- Federal Tax Classification for each partner and shareholder of the partner that is an S Corp

In addition, a partnership that is electing out of the regime must notify each of its partners of the election within 30 days thereof.

The IRS will need to make assessments against all of the partners in a separate partner-level proceeding if a partnership elects out of the BBA rules. Thus, if a partnership makes the election out, its partners should confirm that they will have sufficient access to the partnership's books and records in order to substantiate the amounts allocated by the partnership in an IRS audit, as stated above. A more crucial aspect is the fact that if a partnership makes a valid election out, the applicable statute of limitations of assessment of tax will be determined at the partner level and is further determined separately for each partner.

(i) Partnership Representative It is important for the parties to select a “partnership representative”; the individual does not need to be a partner but, if so, should not have a potential conflict, which may arise if the partner's interest is changed from one year to the next. The partnership representative will be able to make an election as to which partners will be taxed on any adjustments for a given taxable year if it is in the best interest of the partnership relative to the reviewed year.

It is important to emphasize that the current partners in a partnership could bear economic responsibility for improper tax reporting in prior years. Negotiations are necessary to determine how the partnership will elect to pay the tax due. In addition, the IRS needs to provide guidance on how multitiered partnership structures will be handled in the future.

The partnership representative serves in a similar role as the tax matters partner under TEFRA in that the partnership representative has the sole authority to act on behalf of the partnership; however, there are two important differences between the tax matters partner and the partnership representative. First, whereas the tax matters partner must be a general partner and may be an individual or an entity, the partnership representative can be any person or entity, including a nonpartner, so long as the partnership representative has a substantial presence in the United States. A substantial U.S. presence is required so that the partnership representative is available to communicate with the IRS during an audit.

It should be noted that a partnership may elect out of the new rules if it meets the following criteria:

- All partners are individuals, estates of a deceased partner, S corporations, or C corporations (or foreign entities taxed in the United States as a C corporation), including nonprofits organized as corporations.

- It is not required to issue more than 100 Schedule K-1s.

- Note: If a partnership furnishes more K-1s than are actually required by § 6031(b), then these additional K-1s are not taken into account when determining whether this criterion is met.

- The election is made on a timely filed partnership return (including extensions) for that taxable year.

If a partnership elects out of the new rules, it must notify each of its partners that it made the election within 30 days of making the election (i.e., within 30 days of submitting the tax return).

NOTES

- 215.1 231 LLC v. Commissioner, No. 14-1983 (4th Cir. 2016). The appellate court found that a transfer of state tax credits to a partner who had contributed $3.8 million to the partnership was a disguised sale requiring the partnership to recognize income from the transfer.

- 319.1 The author acknowledges contribution to this subsection of the materials prepared by Marks, Paneth, written by Mark Baran, Principal Tax, a copy of which is on file with the author.

- 319.2 All eligible foreign partners, even those with no U.S. filing requirements, must apply for and obtain a valid U.S. TIN for the partnership to file a valid election out of the new budget act rules.