1

Laying the foundations

YOUR MONEY MINDSET

Our money mindset and attitudes towards money ultimately shape how we handle our finances. The money mindset we have is usually shaped by how we grew up around money, our experience with it growing up and witnessing how our parents and other people interacted with money. For example, if you come from a household where your dad handled all the finances and your mum didn't make any of those decisions, then this is likely to lead to you having similar beliefs as an adult. Or if money was always scarce and a source of stress in your household, this will impact how you handle money as an adult. Improving our money mindset comes from rewiring our limiting beliefs, educating ourselves about key financial concepts and strategies, and having open discussions about our financial goals and journeys.

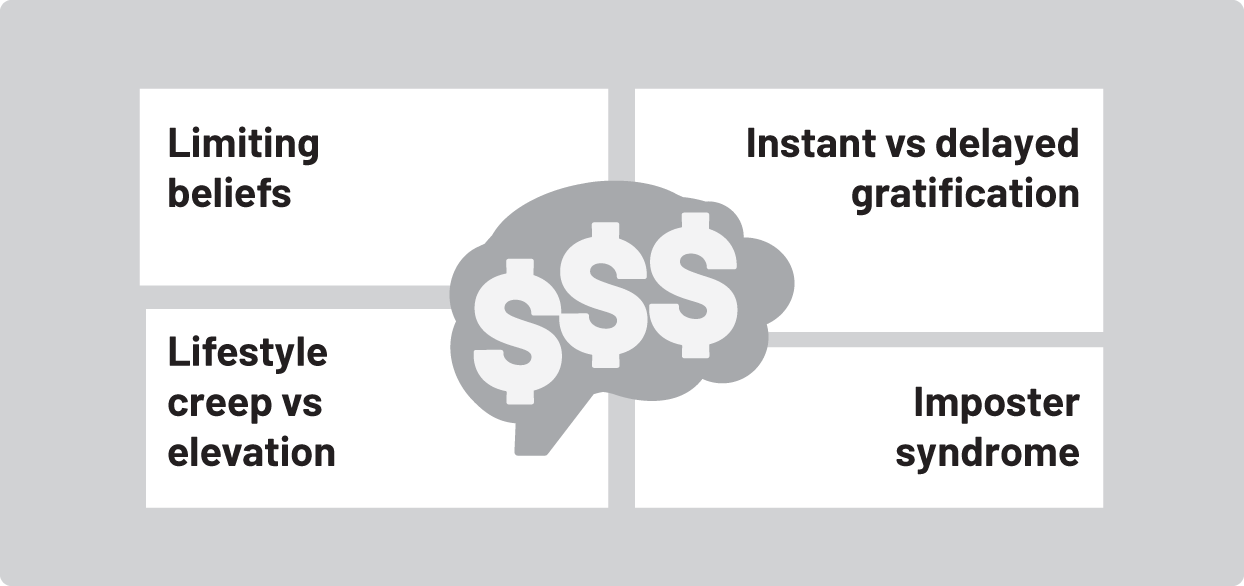

LIMITING BELIEFS

A lot of people tend to have a range of limiting beliefs when it comes to money — that it's too hard or too complicated and they'll just never be good with it. These are the self-doubting thoughts that we tell ourselves that set limits on what we can achieve before we even start. The problem with holding these limiting beliefs is that it places a mental block on your ability to grow and develop a positive relationship with your money. Changing your self-talk around money is a major step in reframing your limiting beliefs into empowering beliefs.

Instead of: I am terrible with money.

Say: I am working on improving my finances every day.

Instead of: I'm such a failure.

Say: I am proud of myself for taking steps to improve my financial situation.

Instead of: I can't afford it.

Say: How can I afford this?

Instead of: Saving money is hard and complex.

Say: I break down my savings goals and automate them.

Instead of: Everyone else has so much more than me.

Say: I am on my financial journey.

Instead of: Why didn't I start earlier?

Say: I can't change the past, and there is no better time to start than today.

INSTANT VS DELAYED GRATIFICATION

Many of us are prone to wanting instant gratification: constantly buying new clothes to be ‘trendy', wanting the latest thing to ‘keep up' or seeking immediate results or pleasure. Even though choosing something now may feel good in the moment, taking a longer-term view and developing self-discipline can result in bigger and better rewards in the future. Delayed gratification is our ability to resist these temptations of instant pleasure, allowing us to stay focused on our long-term goals. It involves budgeting and spending mindfully, as well as developing discipline and patience to avoid impulse spending and decision making. Think about instant vs delayed gratification when you are developing your own financial goals. Consider whether your goals are focused on short-term gains or designed to look forward to a bigger picture.

LIFESTYLE CREEP VS ELEVATION

One of the biggest money mindset mistakes you can make is lifestyle creep. When you receive a pay rise at work or you increase your income with a new job or side hustle, it can be tempting to spend that extra money on a nicer car, more expensive restaurants or fancier clothes. Before you know it, these former luxuries become ‘necessary' spending and you find yourself running out of money every month. Avoiding lifestyle creep involves having clear financial goals that you are working towards, tracking your spending and automating transfers to your savings and investments so they occur before any non-essential spending happens. When you receive an increase to your income, allocate a small portion to treat yourself and put the rest towards your financial goals.

In contrast to lifestyle creep, lifestyle elevation is the way we act following an increase in income that benefits our lives. Rather than seeing this as a negative, lifestyle elevation focuses on the positive benefit that can come from spending more on your lifestyle. This includes investing in personal self-care, spending more on higher quality items that will last longer, improving your standard of living, having the ability to travel and paying for convenience that frees up your time. Lifestyle elevation will align with your personal financial goals and values, whereas lifestyle creep will hold you back from achieving them.

IMPOSTER SYNDROME

We can often feel a sense of imposter syndrome when it comes to our finances. This includes feelings that we are not smart enough or good enough despite our experience, qualifications and achievements. Imposter syndrome can affect our finances in a variety of ways. It can cause us to not apply for a well-paid job that we are qualified for, not negotiate our salaries when starting a new role, not start investing or not pursue a promotion or business idea due to a fear of failure. Tracking your accomplishments and progress towards your goals is a great way to remind yourself of your abilities and how capable you are.

FINANCIAL GOALS

If you find yourself feeling unmotivated or stuck when it comes to budgeting or saving money, you may not be setting effective money goals. Setting goals gives you a sense of direction and purpose for all the effort that you are putting into improving your finances. Without meaningful financial goals, we can lose interest or feel indifferent, which can result in bad money habits. Put yourself in the best position to take control of your money by defining your financial values and setting smart goals that align with these values.

DEFINE YOUR FINANCIAL VALUES

Your financial values are the foundation on which the rest of your money journey is built. They are the guiding light that keep you on track with your goals and define the reasons why you set your money goals in the first place. Your financial values are the beliefs you hold on what is important. For example, you might value travelling and new experiences, or you might value stability and buying a home is your top priority.

The values you uphold will influence how you spend your money and decide on your long-term financial priorities. Think about what you value spending your money on. What brings you joy and fulfilment? What brings you comfort and security? Your financial values are not permanent, and they will change over time as your priorities and circumstances change.

CREATE YOUR FINANCIAL GOALS

Once you have defined your financial values, the next step is setting short-, medium- and long-term goals that align with these values. Think of what you want to achieve in the next year, next few years and well into the future and write out your goals using the SMART goals framework.

- Specific: Be really specific about exactly what you want to achieve. For example, your goal should be ‘I want to save $5000 by the end of the year' as opposed to ‘I want to save more money this year'.

- Measurable: Make sure your goals are measurable so you can track progress and success. For example, ‘I want to pay off my debt in six months' or ‘I want to save $3000 for my holiday in December'.

- Attainable: Dream big, but make sure your goals are still attainable and realistic. For example, it would be very difficult to save $50 000 a year if you earn $55 000. Your goals should be motivating but not unachievable.

- Relevant: Is this goal really what you want to achieve? How does this goal tie into your values and priorities in life? Having goals that are important to you will help you stay motivated to achieve them.

- Time bound: Set yourself a time period to achieve the goal. It's important to keep yourself accountable by setting a realistic deadline to achieve your goal.

BREAK DOWN YOUR GOALS AND TRACK YOUR PROGRESS

Once you have set your goals, break them down into smaller steps and milestones. If you have a yearly goal, think about what milestone you want to reach every quarter. If you have a monthly goal, think about what you want to achieve each week. Mark these milestones in your calendar and schedule check-ins to evaluate your progress.

STAY COMMITTED AND REWARD YOURSELF ALONG THE WAY

Achieving your money goals is never a linear path. Embrace the ups and downs of your journey and remember that small progress is still progress. What's important is that you stay consistent, resilient and remember the ‘why’ behind wanting to achieve your goal.

FIVE FINANCIAL NUMBERS YOU NEED TO KNOW

If you want to take control of your finances, you need to know exactly where you stand at the current point in time and where you want to be. There are five financial numbers that you need to know: your income, spending, debt, savings/investments/asset equity and your net worth. Determining your current financial position will help you identify the areas where you are doing well, as well as the areas that need improvement. Tracking with these numbers over time will also show you the progress that you are making to help keep you motivated.

YOUR INCOME

Your income is any money that you receive on a regular basis. This will include your wages or salary, net income earned through a business, dividends or profit from your investments, interest from your bank, government payments, selling something you create or own, and any other notable positive money gain you receive. Relying on one source of income can be risky, especially if you are unexpectedly made redundant or have to quit your job. Instead, protect yourself by building multiple streams of income so you are less reliant on your wage/salary.

What you need to know:

- What are your income streams?

- How much money do you make on average from each of your income streams?

YOUR SPENDING

Your spending each month can be divided into essential and non-essential. Essential expenses are the things you need to spend money on each month to live, such as housing, bills, groceries and transport. Conversely, non-essential spending covers things like new clothes, eating out at restaurants and subscription services.

If you are unsure of your spending habits, print off your last two to three months of bank statements, grab two highlighters and go through each transaction line by line. Use one colour to highlight essential spending and the other colour for non-essential, discretionary spending.

What you need to know:

- How much do you spend each month?

- How much are your essential and non-essential expenses?

- For your non-essential spending, are there any areas you can reduce or cut down on?

YOUR DEBT

Your debt is the amount of money that you have borrowed from another person or party, which you owe back to them.

What you need to know:

- How much money do you owe and to whom?

- What are the terms of the debt, including the value, interest, payment due dates and any other obligations associated with the debt?

YOUR SAVINGS, INVESTMENTS AND ASSETS

Savings and investments include the money that you put into your bank account for short-term savings, longer-term savings, emergency funds, sinking funds or into investment accounts.

Your assets are the things that you own that have positive economic value. Your asset equity refers to the value of what you own in your assets. In other words, the total value of the asset minus any outstanding loan/debt you may have on that asset.

What you need to know:

- How much do you have in your savings accounts?

- How much do you have in your investment accounts?

- How much equity do you have in your assets?

YOUR NET WORTH

Your personal net worth is the combination of what you own (assets) and what you owe (liabilities). You should use your net worth to track your progress from year to year, and to hopefully see it improve and grow over time.

To calculate your net worth, calculate the total value of your assets. This includes the value of your home, value of vehicles, cash in bank accounts, value of investment accounts, value of bonds and any other notable asset that holds value. Then, calculate the total value of your liabilities. This includes the outstanding value of your mortgage, investment loans, credit card debt, car loan, personal loans and student loans. The difference between the two is your net worth.

What you need to know:

- What is the total value of your assets?

- What is the total value of your liabilities?

- What is your net worth (the difference between the total value of your assets and liabilities)?

SIGNS YOU ARE FINANCIALLY CONFIDENT

There is no better feeling than being confident with and in control of your money. Financial confidence is about so much more than material things like buying flashy cars, eating at expensive restaurants or splurging on designer clothes and bags. It's about being in control of your money and not letting it control you. It's about not feeling stressed about how you will pay for things. It's about not having money hold you back from living your best life. We develop this confidence over time by adjusting our money mindset and implementing a money management system that helps us achieve our financial goals. As you start to take control of and change your relationship with your finances, you will begin to view money as a tool instead of a stressor.