Other Benefits and Reimbursements

In This Chapter

![]()

- Retirement plans for you and your employees

- Reimbursements for business use of a vehicle and other expenses

- Section 125 cafeteria plans

- Vacation, sick, and other leave

Small businesses typically have many options when it comes to the benefits you offer employees. Although you have flexibility in what benefits you offer, you’re often required to provide the same benefits to all full-time employees. Exceptions are sometimes possible for part-time employees.

In this chapter, you learn about the various types of retirement plans small business owners can establish, including SIMPLE, SEP, 401(k), and Keogh plans. We also explain how to remit retirement plan contributions and what points of government oversight to anticipate. Finally, we discuss auto and other business expense reimbursements, as well as paid vacation and sick leave issues.

Many people have already accumulated some amount of retirement savings through current or previous employers, so your employees likely have started saving a nest egg for their retirement.

As an employer, you can choose from several different offerings to help your employees continue their retirement savings. Small businesses have access to many of the tools larger companies do, with some special options specially geared toward small businesses. Let’s take a look at the various retirement plan options.

SIMPLE IRAs

Savings Incentive Match Plan for Employees (SIMPLE) Individual Retirement Account (IRA) plans are designed for employers that don’t presently offer any type of retirement savings vehicles to employees. These plans can be set up through many mutual fund companies such as Vanguard (vanguard.com), Fidelity (fidelity.com), and T. Rowe Price (troweprice.com). There’s usually a low fee structure for both employers and employees.

With SIMPLE IRAs, employees can direct a portion of each paycheck into a tax-deferred retirement savings account, and employers are required to match up to 3 percent of an employee’s compensation.

Businesses with up to 100 employees are eligible to establish SIMPLE IRA plans. The amounts employees can contribute each year are indexed for inflation, but as of the 2016 tax year, the contribution limit is up to $12,500 per employee. Employees 50 or over can contribute an additional $3,000 as of the 2016 tax year.

One caveat of SIMPLE plans is that employers must match employee contributions on a dollar-for-dollar basis up to as much as 3 percent of the employee’s compensation. Let’s say an employee earns $50,000 per year and contributes $5,000 toward his SIMPLE IRA. The employer is required to contribute the lesser of 3 percent of $50,000 or the employee’s contribution. In this case, 3 percent of $50,000 is $1,500, so the employer is required to contribute at least $1,500. Any employer contributions to a SIMPLE IRA plan are immediately vested.

DEFINITION

In terms of retirement plans, vested means the contributions made on an employee’s behalf by an employer are permanent and cannot be taken away. If the employee leaves the company, he or she has access to all the money in the vested plan. Public companies often grant stock options to employees that only vest if the employee stays with the company for a specified period of time.

Simple Employee Pensions (SEPs)

This type of retirement plan gives small business owners more latitude on contributions. The maximum annual contribution is the lesser of 25 percent of compensation or $53,000 per year as of the 2016 tax year.

Employers can decide on a yearly basis how much to contribute. The catch is that each employee gets the same percentage match. Owners can’t elect to contribute 25 percent of their own compensation, for instance, without also contributing 25 percent of each employee’s compensation as well. This type of plan might be best suited to self-employed individuals with no employees.

401(k) Plans

You likely have some amount of savings already in a 401(k) plan. 401(k) plans share some similarities with SIMPLE IRA plans in that employees can make tax-deferred investments. However, 401(k) plans cost employers more to administer and require that Form 5500 be filed with the U.S. Department of Labor annually.

Employee participants can contribute up to $18,000 for the 2016 tax year, and employees age 50 or older can contribute an additional $6,000 per year.

Employers have discretion with regard to determining matching contributions for 401(k) plans, but they must follow the rules written into the plan. For 2015, a limit of $53,000 can be contributed to 401(k) plans, combining both the employee and the employer contribution. As with SIMPLE IRA plans, employer matching contributions vest upon deposit into an employee’s account.

There’s a special 401(k) provision called solo 401(k) or the one-participant 401(k) for businesses with no employees or businesses in which the only employee is the owner. (The owner’s spouse can be an employee as well.) The contribution limits are the same as for regular 401(k)s, but because the business owner is both the employer and the employee, the company can create a matching program and take advantage of both employer and employee contribution limits.

Keogh Plans

Historically, one of the main types of retirement plans for self-employed was the Keogh plan. Over time, these plans have fallen into disuse in favor of the easier-to-administer SIMPLE IRA and SEP plans discussed earlier.

Remitting Retirement Contributions

Employee retirement contributions are withdrawn from employee paychecks in the same fashion as an employee’s payroll taxes. However, instead of remitting funds to a government agency, you send the funds to the financial institution that administers your retirement plan.

Your business has a fiduciary responsibility to ensure the contributions are remitted timely. Delayed contributions can have serious ramifications, including the following:

- Employees miss out on potential investment income and gains during the delay.

- Civil or criminal penalties can apply to businesses that misuse employee retirement contributions.

DEFINITION

Fiduciaries are individuals or entities entrusted with a legal or financial responsibility on another’s behalf.

Government Oversight

Every retirement plan falls under the jurisdiction of the Employee Retirement Income Security Act (ERISA). This law, enacted in 1974, is administered by the U.S. Department of Labor (DOL). You might have noticed earlier that Form 5500 is filed with the DOL instead of the Internal Revenue Service (IRS). ERISA sets forth specific requirements for the fiduciary responsibilities of employers as well as the reporting requirements for employers and financial institutions.

This law is designed to protect the interests of employees who work for private employers. It does not apply to governmental entities or churches.

ACCOUNTING HACK

It’s not uncommon for an employee to overcontribute to a retirement plan. It’s not the employer’s responsibility to oversee how much an employee contributes; however, it’s helpful if the employer ensures employees are aware of the plan contribution limits. If an employee contributes more than the statutory limit in a given year, he or she needs to contact the custodian of the plan—typically the financial institution or brokerage house that maintains it—and make a request to withdraw the excess. There are tax penalties associated with contributing too much, so contributions should be made and carefully tracked throughout the year. You have until April 15 of the following year (the individual tax return filing date) to arrange for the refund without penalty.

Any employee or business owner who uses a personal vehicle in the course of business is engaging in a tax-deductible activity. Many businesses provide reimbursements for the vehicle expenses, but this is completely optional.

Employers can choose to reimburse for actual vehicle expenses, such as gasoline and maintenance costs, but an easier method is to utilize the standard mileage rate set by the IRS. The business miles driven are tracked and recorded in either a written log, your accounting software, or an app, and the employer reimburses based on the miles driven.

The standard mileage rate amount is published by the IRS and typically changes once a year, although the IRS has been known to change the rate mid-year during periods of severe gasoline price changes. The standard mileage rate is intended to compensate a vehicle owner for all costs of operating the vehicle or business on a per-mile basis. If you or an employee opts for the standard mileage rate, you cannot also deduct any direct costs related to operating the vehicle.

If you opt to utilize a mileage-based reimbursement plan within your business, be sure to maintain detailed records, such as a spreadsheet that tracks your mileage (see Chapter 22).

Your spreadsheet program might offer a ready-made mileage log, such as this one in Microsoft Excel.

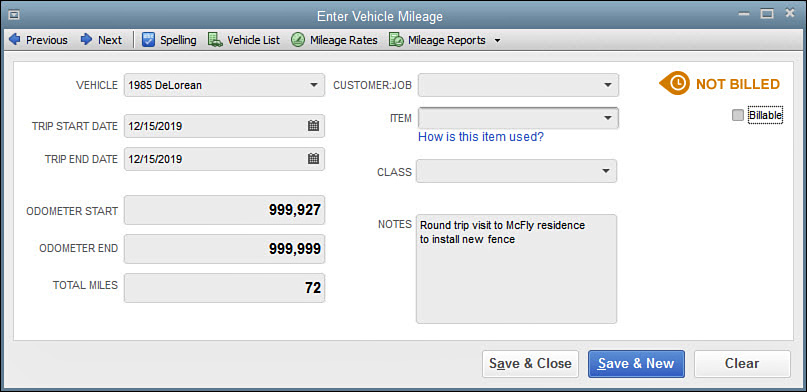

Your accounting software might offer built-in mileage tracking capabilities as well. In the desktop versions of QuickBooks, you can maintain a list of vehicles and then use the Enter Vehicle Mileage window to log individual trips. You can then run reports for any time period you choose that show the mileage for all or specific vehicles.

Your accounting program might offer built-in tools for tracking mileage, such as this example from QuickBooks desktop.

The downside to spreadsheet and accounting software-based mileage tracking is that employees are often relegated to writing down mileage on a piece of paper so the information can be entered into the spreadsheet or accounting program later. The IRS doesn’t mandate a specific logging method, but your records must be consistent and accurate to pass muster with an auditor.

The mileage rate fluctuates with the economy. It was as low as 31¢ a mile in 1999 and as high as 58.5¢ per mile during the second half of 2008. As of this writing, it’s 57.5¢ per mile. An internet search for “standard mileage rate” and the year can show you the current mileage rates.

BOTTOM LINE

If your business is taxed as a partnership or sole proprietorship, be sure to write yourself a reimbursement check for any mileage or other expenses applicable to your business. It’s possible to deduct unreimbursed expenses, such as mileage, on your personal income tax return (more on this coming up). However, sole proprietorships and businesses taxed as partnerships must pay self-employment tax (currently 15.6 percent) on net income of the business. Such owners pay more taxes than necessary opting not to run this expense through their business.

Other Reimbursements

Employers have a wide degree of latitude when it comes to reimbursing employee expenses. The expenses being reimbursed must have a valid business purpose, such as costs incurred while traveling for business, continuing-education classes, professional licenses, or other expenses that relate specifically to an employee’s work or compliance with professional standards. And they should be documented with paper or electronic receipts.

Some employers require specific documentation for travel expenses, and others opt to use per-diem rates set by the General Services Administration (GSA). The GSA sets these rates for each fiscal year to define the maximum amounts appropriate for lodging and meals in each geographic area within the United States.

Employees are not required to provide receipts for per-diem-based reimbursements, and these amounts are not taxable to the employees. If you choose to reimburse any employee expenses, be sure to document the policy in writing. You also might want to provide a standard expense report document to provide a formal reimbursement structure. Or you could use a productivity app to automate expense reimbursement tracking.

Most spreadsheet programs offer prebuilt expense report templates.

ACCOUNTING HACK

Many employers provide reimbursements for business vehicle usage. However, this is optional, and not all employers comply or reimburse at the full IRS standard mileage rates. If there’s no reimbursement, or only a partial reimbursement, the employee has the option of filing Form 2106, Employee Business Expenses, with his or her individual income tax return and claiming the unreimbursed vehicle expenses as an itemized deduction on Schedule A.

There are no set rules governing how you remit reimbursements to employees. Some employers add reimbursement amounts as line items on employee paychecks. Others write separate checks to the employee for the expense. With the latter, you might need to set up your employee as a vendor to issue them a nonpayroll check. (Contrary to popular belief, some reimbursements are actually taxable to your employees. Consult IRS Publication 463 to determine the specifics for your situation and any corresponding reporting requirements.)

In the case of nonemployee owners, you’ll simply issue a check directly to the owner.

Whether owner or employee, when we say “issue a check,” we mean handwrite or print a check, transfer funds through online banking, or remit the money through another agreed-upon reimbursement avenue. Even if you make the transfer electronically, you’ll still record this as a check in your books unless you include it as part of payroll.

Cafeteria Plans

A cafeteria plan allows employees to set aside a portion of each paycheck, income tax free, to put toward certain accident and health benefits, adoption fees, dependent care assistance, group-term life insurance coverage, or health savings accounts.

Cafeteria plans, sometimes called Section 125 plans for the Internal Revenue Code section that authorizes them, enable employees to pay for certain personal expenses with pre-tax income, while employers have a reduction in payroll taxes.

Cafeteria plans must be approved by the IRS and are administered by approved third-party companies. They can be limited to enabling employees to pay health and life insurance premiums with pretax dollars or to establish flexible spending accounts (FSAs), which allows employees to purchase certain medical expenses with pretax dollars.

You’ll be happy to know that the IRS does not typically require any type of annual filing for a cafeteria plan. Employers that offer a special type of plan known as a welfare benefit plan to retirees are required to submit Form 5500 to the DOL, but otherwise, your cafeteria plan shouldn’t require any ongoing governmental filings.

Paid Vacation and Sick Leave

The Fair Labor Standards Act (FLSA) does not require employers to offer paid vacation or sick leave for employees. However, this doesn’t mean you can necessarily disregard this benefit.

As of this writing, California, Connecticut, Massachusetts, and Oregon require employers to offer some amount of paid sick leave. Several cities and at least one county have enacted similar legislation. As an employer, you not only have to stay compliant with the federal law, but also any local laws.

Presently, paid vacation is not mandated by any level of government. This means as an employer, you can decide whether or not to offer paid time off to your employees. Businesses that do offer paid time off often require employees to accrue time off throughout the year. For instance, an employee who is entitled to 5 days of paid vacation per year accumulates just under a ½ day of vacation per month.

Employers have wide discretion when it comes to allowing employees to take time off that they haven’t formally accrued yet or not. Some employers grant an automatic block of paid time at the start of a new calendar year.

If you choose to offer paid vacation, your accounting software will likely have a built-in feature that enables you to track it, or your third-party payroll provider can handle the tracking for you.

The number of paid days earned and taken during a given calendar year should be reported on each employee’s paystub.

Business owners can decide whether paid vacation not taken at the end of the year expires or can be carried forward to a future year. Certain employers allow employees to sell back vacation time they haven’t taken. It’s always best to encourage your employees to take paid time off, and in fact, doing so can be an effective measure of internal control. (We cover the concept of internal control in detail in Chapter 15.)

Sick Leave

As noted, there’s no federal requirement for a business to offer paid sick leave, but a movement is afoot in some cities, counties, and states to require paid sick leave. Employers that don’t fall under a mandate can offer both paid vacation and paid sick leave, or just one or the other. Some employers try to simplify things by offering a general bank of paid time off that can be used for sick or vacation days.

As with vacation time, your accounting software enables you to track and report sick leave, or you can outsource the task to a payroll provider.

Family and Medical Leave Act

Private businesses that have 50 or more employees, any public agency, and any public or private school is required to offer certain employees up to 12 weeks of unpaid time off per year. Employers cannot fire employees for taking time off under the Family and Medical Leave Act (FMLA) and must protect the employee’s job while the employee is away for any of these reasons:

- Birth or adoption of a child

- Care for an immediate family member with a serious health condition

- Temporary disability that prevents the employee from performing his or her job

- Situations arising from an immediate family member being called for active military duty

Employers have discretion whether or not to maintain an employee’s pay during a FMLA absence, but they cannot penalize an employee for taking said time off.

The Least You Need to Know

- Small business owners have many attractive choices when it comes to offering retirement savings plans to employees.

- Reimbursing for the business use of automobiles is a common practice, and published rates are available for computing this. Employees can be reimbursed for other types of expenses as well, such as business-related travel.

- Employers can choose to offer cafeteria plans to their employees, giving the employees a menu of benefits choices.

- In general, employers are not required to offer paid vacation and sick leave, but the FMLA outlines certain situations in which employers must protect an employee’s job during unpaid leave.