Financial Reports and Stakeholders

In This Chapter

![]()

- What the IRS looks for in your tax returns

- Information lenders and investors want to see

- Understanding financial ratios

Even if you’re the sole owner of your business, you’re by no means the only stakeholder with an interest in your company’s activities. As you’ll learn in later chapters, various governmental agencies levy a dizzying array of taxes, including payroll taxes, income taxes, business license taxes, property taxes, and more. The Internal Revenue Service (IRS) in particular carefully watches the financial results you report on your tax returns.

In some situations, you might seek financing to help get your business off the ground, expand, or function on an ongoing basis. Lenders rely on your financial statements for much of the basis for their lending decisions. We explain some of the tools that quickly give them insights into the current state of your business.

We also cover what primary stakeholders look for in your business financials, as well as introduce you to financial ratios, which are quick ways to measure the health of your business.

How the IRS Reviews Your Financials

The IRS projects it will receive around 11 million corporation and partnership tax returns for the 2015 tax year. This doesn’t include Schedule C returns for sole proprietorships.

One of the ways the IRS tests the reasonableness of your income tax returns is to compare your results to other businesses like yours. To do this, it looks at your NAICS code, one piece of information every business must provide, no matter the tax form. When filing your tax return, choose the NAICS code that corresponds to the largest percentage of your revenue. In addition to the NAICS code, you need to provide brief written descriptions of your primary line(s) of business.

DEFINITION

The North American Industry Classification System, or NAICS, is a numbered list of business activities comprised of around 1,000 six-digit codes that group businesses by sector, subsector, and group. The list provides a means for governmental departments to track and compare economic activity. NAICS supersedes the previous four-digit Standard Industrial Classification (SIC) codes used for several decades.

The IRS also maintains the National Research Program through which it develops statistical norms for each type of business. Although your revenue can vary drastically from other businesses in your industry, certain patterns emerge when large cross-sections of data are compared. It’s through this research that the IRS can identify outliers, such as extraordinarily large amounts of meal and entertainment expenses or unusually high travel expenses.

The IRS makes these determinations in part based on ratios, such as those we’ll discuss later in this chapter. Some ratios are based on percentages of revenue; others may center on percentages of net income. Not only does the IRS compare your tax returns to your industry peers, but it also looks at your historical returns. Large fluctuations in revenue or expenses can be cause for additional scrutiny.

RED FLAG

Although your odds of being audited are rather low, keep in mind that the IRS has up to 3 years to request an examination of your books. This time period can be extended if the IRS determines there are material mistakes in your books. Keep in mind that mistakes aren’t necessarily fraud. Many IRS audits are conducted by mail, when the IRS requests information and you mail it in. Serious inquiries often result in an on-site visit by an IRS auditor who expects immediate access to your books and records—hence the on-site visit instead of you going to an IRS office.

Periodically during the life of your business, you might need to borrow money from a bank, investor, or even a family member. Many businesses can’t get off the ground without borrowing money, while some business owners can bootstrap their way off the ground.

DEFINITION

In a business context, bootstrap means to use one’s own resources instead of relying on others. Instead of borrowing money, bootstrappers rely on their own savings or personal credit cards, and plow profits back into the business.

In this section, we give you an idea of what lenders look for in your financial reports should you seek to borrow money.

Consistency

Lenders like consistency in revenue and expenses. This doesn’t mean your revenues and expenses have to be the same year after year, but rather that the overall trend is consistent. Lenders first and foremost want assurance you’ll be able to pay back a loan.

Your financials can only tell a portion of your story, so when meeting with a lender, be sure to disclose any extraordinary circumstances within your financial statements that have caused significant changes in your revenues and/or expenses. Sometimes, the inconsistency can be caused by something positive, like acquiring a large customer. You can use this type of variation to explain the need for a new equipment loan or other costs of growing your business.

Collateral

The paradox of borrowing money is that it often seems banks only want to loan money to people who don’t need it. In some cases, your money may be tied up in illiquid assets, such as equipment or real estate—items that can be converted to cash but usually not quickly. The ability to guarantee some portion of the loan with collateral increases the odds of you being approved for a loan.

DEFINITION

Collateral is business or personal assets that you pledge as security as repayment for a loan. You must have full title to any item you want to use as collateral. In the event that you fail to repay the loan, the bank either claims ownership of the collateral or forces you to sell the asset to repay the loan.

In addition to any collateral your business may have, lenders also look to the owners of the business to personally guarantee any loans made. As discussed in Chapter 2, many businesses choose some form of incorporation to protect against litigation and isolate business activities from personal activities.

When it comes to financing, no matter what business structure you have, lenders want you to have some personal interest in the game. The term you’ll see is guaranteeing the loan, so each owner is likely to be considered a guarantor. This means if the business fails to pay back the loan, the lender can look to each guarantor personally for repayment.

Cash Flow

Lenders want to ensure that your business has an ongoing cash flow. In most cases, you’ll need to make monthly loan payments, so lenders will want assurance your business has the liquidity each month to easily make the loan payments.

If your business has seasonal peaks, having sufficient cash reserves to cover debt service during slow periods can make a difference in your ability to get the loan.

Some lenders entice borrowers by agreeing to waive interest and principal for a period of time. Others might offer to collect monthly interest payments only and let the principal ride. Most loans require payment of both interest and principal on a recurring monthly basis.

DEFINITION

In business terms, liquidity is a measurement of the amount of cash on hand, as well as assets that are easily converted to cash. Liquid assets include your business bank account(s), accounts receivable you expect to collect in the near term, stock and bond investments, certificates of deposit, and in certain cases, inventory. Debt service relates to repayment of a loan over time.

Minimal Revenue Concentrations

Lenders have to weigh lending money to your business versus other uses of their funds. Many of the tests we discuss in this section fall under the umbrella of risk management.

The interest you pay on the loan compensates the lender for the risk they’re taking. Therefore, lenders are going to be looking for potential exposures, such as how diversified your revenues are. If an overwhelming amount of your revenues are derived from a small number of customers, the lender might not be comfortable with that exposure.

Risk management is a discipline that focuses on identifying risks and their potential impact on an organization. Lenders weigh the risk of lending money. In turn, businesses weigh the odds of customers paying their invoices in a timely fashion. Businesses of all sorts face exposures that must be managed.

Financial Ratios

Lenders might review multiple sets of financial statements in a single day. You may have experienced the blur that can set in from just reviewing your own numbers. Accordingly, lenders employ financial ratios such as those we discuss later in this chapter to get a quick read on whether or not they should employ more time and money to make a formal investigation into the creditworthiness of your business, or if the application should be disapproved without more time or thought.

In the first section of this chapter, we explained how the IRS compares your tax returns with those of like businesses to try to identify irregularities. Banks use financial ratios in much the same fashion.

Depreciated Assets

Earlier in this section, we discussed how lenders look at the type of collateral you have that serves as security for a loan. Your balance sheet might not always offer the best representation of the collateral you have, particularly if some of your major assets are highly depreciated. For example, a piece of equipment you’ve owned for 5 years might reflect a near zero net value on your books, but it could have significant market value.

When applying for a loan, be sure to inform your lender of any assets that might have a low book value but a higher market value. Depending on the asset, the lender might order an appraisal of the asset to determine the amount a third party would be willing to be pay for the item.

Discretionary and Owner Expenses

Businesses have wide discretion on how to spend their money. As a business owner, you can’t treat truly personal items, such as clothes for your children, groceries for your house, and your home cable television bill, as business expenses. However, many expenses do fall in a gray area known as discretionary expenses. These might include subscriptions to business newspapers and industry websites, and in some cases, advertising expenses. Discretionary means you have a large amount of control over whether or not to spend money on these items, which means you could eliminate the expenses to free up money for debt service if necessary.

Owner expenses are items you, as an owner, may choose to incur but that another owner might eschew. Examples of this might be golf club memberships, cost of the owner’s automobile, and entertainment expenses not directly related to the business.

Using Financial Ratios

We touched on financial ratios a bit earlier in this chapter. Now let’s take a closer look.

Every business has different combinations of revenue and expense, which can make comparing financial statements difficult. Financial ratios serve as an equalizer to condense even the most complex financial statements into easy-to-grasp measurements. In this section, we discuss some of the ratios lenders use to determine the creditworthiness of your business. You also might find these ratios useful in determining the health of your business, as well as in comparing yourself to industry standards in your field.

Public libraries and certain websites provide free or paid access to industry benchmarks that make it easy to see how your business measures up against its peers. And of course, you can be assured that the ever-present IRS is using some of these measurements to test the reasonableness of the figures presented on your income tax return.

Current Ratio

The current ratio is a liquidity measurement that identifies how easily your business can repay short-term debt obligations. As shown in the following figure, the current ratio is your current assets divided by your current liabilities. (We defined these terms in Chapter 4.)

A current ratio of 1 means your current assets exactly equal your current liabilities. This is a fragile liquidity state because not all current assets are likely to be cash. If a significant portion of your current assets are accounts receivable, there’s a chance customers will be unable to pay some of their invoices, which can make your business unable to pay its short-term bills in full.

A current ratio of .9 means your business only has current assets on hand to cover 90 percent of your short-term liabilities, which can mean your business is technically insolvent.

A current ratio of 1.5 means the business has one and a half times as many current assets as current liabilities.

From an accounting perspective, short-term means 12 months or fewer. You might have a 30-year mortgage on a building you use in your business, but only the amount that’s presently due within the next 12 months is considered short-term. The balance of the loan is considered long-term debt.

Quick Ratio

Whereas the current ratio includes inventory, which depending on the industry, can be a somewhat illiquid asset, the quick ratio strips inventory out of total current assets to determine the ability of a business to fund short-term liabilities without involving inventory. This is done because a business might not receive full value for inventory that must be sold off quickly to cover the debts of the business.

A quick ratio of 1 means the business has the liquidity to pay short-term bills without having to sell inventory.

The quick ratio is sometimes referred to as the acid test for a business.

Debt-to-Equity Ratio

As we noted earlier, lenders very much want to see that owners have a personal interest in their business. A ratio that immediately shows how much money owners have either invested directly or indirectly by leaving profits in the business is the debt-to-equity ratio. You also might see this referred to as debt to worth.

The closer this ratio is to 1, the more the owners have put into the business. Conversely, the closer the number is to 0, the more leverage the business is using, which raises the likelihood that the debts may not be able to be repaid. These amounts can be derived from your balance sheet.

Bankers or other lenders usually exclude shareholder loans (money the owners invest in the business) from this equation because the bank subordinates debt from the owner(s) to the debt from the bank. Subordination is a lender’s term that means the lender’s debt legally comes ahead of the shareholder’s debt.

The debt-to-equity ratio identifies how much owners and investors have put into a business versus how much lenders have contributed.

DEFINITION

Leverage represents the ratio of a company’s debt to the value of its equity. The higher the leverage, the more it appears the business is using debt to finance its operations rather than increasing its earnings or managing its expenses. When used properly, leverage can help you multiply the impact of money you’ve invested in the business. When used improperly, the business can be put at risk, which can detrimentally impact the livelihood of owners, employees, and stakeholders.

Cash Flow Coverage Ratio

You’re probably starting to see a pattern in the ratios here, where the goal is to determine a business’s ability to pay back borrowed money. Even if you don’t formally take out a bank loan, every business, in effect, borrows money in some form by utilizing services that are used today but paid for later.

Lenders considering extending credit always seek assurance that their money will be repaid. In that regard, they often use the cash flow coverage ratio to determine how much cash flow a business has with respect to its total liabilities. In this method, the annual cash flow from operations amount comes from the year-end version of the statement of cash flows report (Chapter 14).

The cash flow coverage ratio compares the annual cash flow of a business to its total liabilities, or total debt.

Performance and Probability Ratios

Depending on your industry, lenders might use one or more performance measurements to compare your business to other similar businesses, and to your company’s prior financial history. Each of these measurements focuses on different operational aspects of your business, which isn’t necessarily related to servicing debt.

Gross profit margin determines the profit a business is making from selling products. This can be an indication of pricing strength and effectiveness, and it also reflects a company’s ability to pay its overhead and administrative expenses. In this case, the calculation is multiplied by 100 percent to return a percentage amount instead of a decimal value like some of the other ratios.

The gross profit margin is a measure of pricing effectiveness and ability to cover other expenses of the business.

Profit margin is also often referred to as net profit margin. This bottom line–oriented ratio makes it easy to compare the effectiveness of different businesses by dividing the net income by total revenue. As with gross profit, this can be multiplied by 100 percent to return a percentage amount.

Profit margin, or net profit margin, measures the bottom line effectiveness of a business.

Accounts Receivable Turnover Ratio

Some businesses, such as fast-food restaurants, coin laundries, and retail stores, have the luxury of getting paid at the time of sale for their products and services. Most businesses, however, extend credit in some form by providing goods and services that customers pay for later. This ratio is predicated on the payment terms you offer your customers. Some businesses expect payment within 10 days of an invoice being presented, while many businesses allow 30 days for payment.

A turnover ratio of 12 or higher for a business with 30-day payment terms means most customers are paying their invoices in a timely fashion. A lower turnover ratio tends to wave a caution flag that the business may be headed into cash flow challenges.

The accounts receivable (AR) turnover ratio shows how effective a business is at extending credit to customers and collecting on its invoices.

RED FLAG

The older a customer’s invoice gets, the less likely you’ll collect the money. Always pay close attention to your Aged Accounts Receivable report. Unfortunately, many people are more than willing to take advantage of generous payment terms. Payment terms are a powerful constraint you can use to ensure the health of your business and your cash flow.

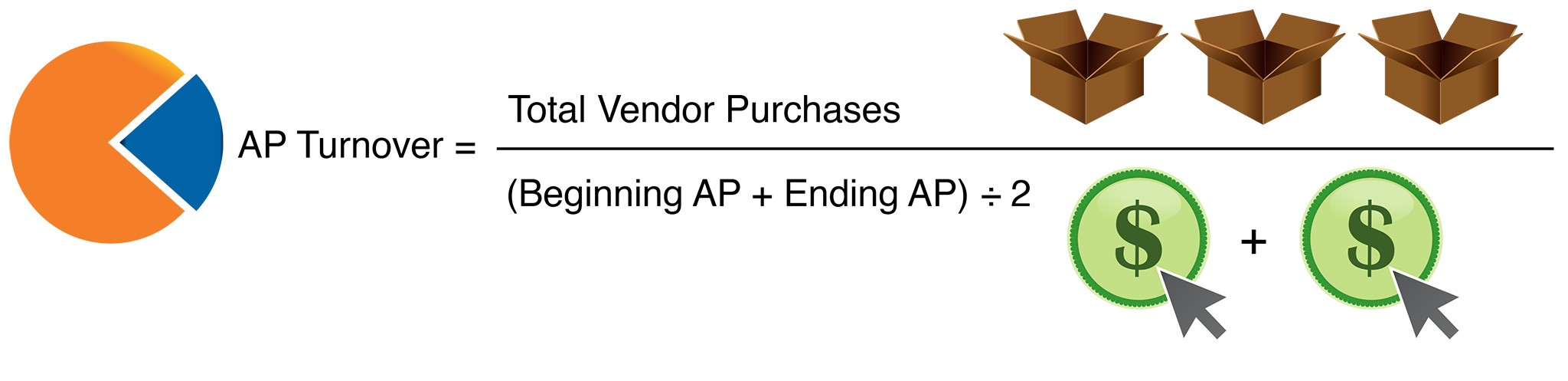

Accounts Payable Turnover Ratio

This ratio is the inverse of the accounts receivable turnover in that it measures how effectively a business pays its vendors. Lenders can identify trends by looking at this ratio for different accounting periods.

When the ratio trends lower, the business may be having difficulty paying its bills. A higher ratio may not necessarily be better because although it’s good to pay bills on time, it can be better to take advantage of payment terms, such as paying bills within 30 days instead of immediately to help smooth out cash flow and enable the business to hang on to its cash for a bit longer.

The accounts payable (AP) turnover ratio shows how effective a business is at paying what it owes to its vendors and suppliers.

Inventory Turnover Ratio

By now, we hope you’ve realized that a constant theme in business is that it’s all about flow and movement. This is particularly important with regard to inventory. Inventory that lingers can cost your business in many subtle and indirect ways:

- Increased rent for storage

- Less space to store products that are selling well

- More time spent inventorying the same items over and over

- The possibility of money down the drain for items that become unsellable

The inventory turnover ratio determines how effective your business is at moving inventory as a whole. Keep in mind that this ratio can enable some problematic items to lay around unnoticed on your shelves, but overall, it gives an indication of how effectively you’re managing your inventory. In this context, we use the words annual sales to distinguish sales of inventory items. Your business may derive revenue from services and nonrelated inventory activities, which should not be factored into this ratio.

The inventory turnover ratio indicates the number of days inventory items remain in your possession before you sell them.

All the ratios in this section help lenders quickly compare your business to its peers. Be sure to clearly describe the operations of your business, and provide the same NAICS code you use on your income tax returns. This ensures that lenders perform a fair comparison. Ratios also can help you manage your business more effectively, as exposures that concern lenders should also be of concern to owners.

Take the time to calculate these ratios yourself before meeting with lenders and investors. By doing so, you’ll notice where your weaknesses lie before your discussions and can better prepare yourself by anticipating questions lenders might have.

The Least You Need to Know

- The IRS can analyze your business by comparing the amounts on your tax returns with other similar businesses.

- Banks, lenders, and investors use a series of ratios to take the financial temperature of your business and determine how healthy it is.

- The accounts receivable turnover ratio can help you determine if you’ve been lackadaisical with regard to ensuring customers pay you timely.

- The inventory turnover ratio enables you to objectively see if inventory is lingering on your shelves.